mahindra pragati bluechip yojana · schemes of mahindra mutual fund may or may not have any present...

TRANSCRIPT

1

MAHINDRA PRAGATI BLUECHIP YOJANA

PRAGATI KE LIYE BLUECHIP TOH BANTA HAI

INDIA’s BIG 100

STABILITY

ECONOMYGAUGE

EMERGING TRENDS

2

• Market Scope

• Large Cap Advantage

• Product Introduction

• Investment Style

• Scheme Details for Investment

WHAT’S INSIDE

3

MARKET SCOPEContributes 70% of Total Market Cap

Invests in Top 1st -100th companies by Average Full Market Cap1: TCS (M-CAP: Rs 754972.12 Cr )

100: SAIL (M-CAP: Rs 28332.73 Cr)

Contributes 16% of Total Market CapInvests in 101st – 250th companies by Average Full Market Cap

101: TORRENT PHARMA (M-CAP: Rs 27943.86 Cr)250: RELIANCE POWER (M-CAP: Rs 8589.84 Cr)

Contributes 14% of Total Market CapInvests in 251st company onwards by Average Full Market Cap

251: V-GUARD IND (M-CAP: Rs 8518.70 Cr)4895: CITIZEN YARNS (M-CAP: Rs 0.02 Cr)

MCap positions as of December 31, 2018 | Source AMFI

The data provided above is for illustrative purpose only. The companies/stocks referred above should not be construed as recommendations from Mahindra Asset Management Company Private Limited / Mahindra Mutual Fund. Schemes of Mahindra Mutual Fund may or may not have any present or future positions in these companies/stocks. Mahindra Asset Management Company Private Limited/Mahindra Mutual Fund is not guaranteeing or forecasting any returns.

4

THE LARGE CAP ADVANTAGE

The Big 100

5

LEADERS

• Established businesses, large scale of operations and diversified distribution

• Scalable business models

ECONOMY GAUGE

• Is a good measure of economic health and impact of policy reforms

QUALITY INVESTMENT

• Well-researched companies with good corporate governance

• High liquidity high volume stocks, diversified shareholding

STRONG FUNDAMENTALS

• Capital efficient with robust balance-sheets

• Better access to capital• Resilient earnings growth

LARGE

CAP

ADVANTAGE

6

4 REASONS

WHY YOU NEED LARGE CAPS

Consistent Participation in Economic

Growth

Reasonably valued with relatively lower volatility

Stable growth potential in

long term

Represents Major Sectors

and Trends

7

BE WHERE THE ACTION IS

57.6 56.4 53.761.1

54.550.4

54.3

0

10

20

30

40

50

60

70

FY05 FY08 FY11 FY14 FY17 FY18 Jan-19

NIFTY 50 MARKET CAP TO OVERALL MARKET CAP %

1. India’s GDP has shown a strong growth2. India’s Market Cap to GDP is lower than that of developed markets 3. India’s Large Cap Market Cap to GDP has shown a positive trend4. Large Caps have historically represented more than half the market

INDIA’S GDP GROWTH MARKET CAP TO GDP RATIO

Data as on Dec 31, 2018 | Data Period: 1984 - 2018

Data as on Dec 31, 2018

Data as on Dec 31, 2018

Data period: Mar 31 2005 to Jan 15, 2019 | FY -Financial year end

1

INDIA

74.6

JAPAN

129.9

USA

152.9

UK

145.0

A

2 3

4

Data Source: Bloomberg

GD

P in

USD

Bln

2 trillion

1 trillion

0.5 trillionLiberalization

37%

64% 63%

38%

47% 45%53%

49% 48%

59%

0%

10%

20%

30%

40%

50%

60%

70%

CY 08 CY 09 CY 10 CY 11 CY 12 CY 13 CY 14 CY 15 CY 16 CY 17

LARGE CAP MARKET CAPITALIZATION TO GDP

8

STAY ON TRACK WITH EMERGING TRENDS

• Nifty 50 is made of the best performers in terms of earnings and volumes

• Best performers push out others to occupy place in the Big 100

• Identifying these trends early from macro economic indicators can help generate alpha

• There should be enough agility to take required exposures for making the most of such emerging trend

Source: Bloomberg, NSE | Data as of Dec 31st, 2018

B

Capex-linked: Industrials, Utilities, Materials, Telecom, EnergyFinancial Services: Banks and Financial ServicesExport-oriented: IT, PharmaceuticalsConsumption-linked: Consumer Staples, Consumer Discretionary

The above is as per internal thematic classification of index sectors

*Internal thematic classification of Index as per MSCI sectors

31

69

37 25 27

13

11

26

30 37

25

12

18 24

16

31

8 19 21 20

2 0 0 3 2 0 0 8 2 0 1 2 2 0 1 6 2 0 1 8

NIFTY COMPOSITION* BY SECTOR (%)

9

LOOK FOR STABILITY FROM MOST OF YOUR PORTFOLIO

Source: Bloomberg, NSE | Data as of Dec 31st, 2018

• Large Caps have shown lesser volatility in different market cycles

• Large Cap valuations have also remained relatively reasonable over these market cycles, making it an all season choice

Standard Deviation

Index 1

year 3

years5 years

Nifty 50 25.3 8.0 5.1

Nifty Midcap 100 34.1 10.8 5.1

Nifty Smallcap250

39.7 13.5 7.8

STANDARD DEVIATION – A MEASURE OF VOLITILITY

C

16.8

22.1

17.6

20.5 20.2

16.8

14.4

-

5.0

10.0

15.0

20.0

25.0

FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Source: Kotak Securities, Bloomberg | Data as of Jan 31, 2019Note: For FY20E & FY21E PE Index value has been taken as on Jan 31, 2019

NIFTY 50 VALUATION - 1 YEAR FORWARD PE

10

BUILD WEALTH IN LONG TERM

D

Source: ICRA| Data as on: Jan 31 2019

The data provided above is for illustrative purpose only and should not be construed as a promise on minimum returns and safeguard of capital. Mahindra Asset Management Company Private Limited/Mahindra Mutual Fund is not guaranteeing or forecasting any returns. Past performance may or may not be sustained in future.

Return Analysis of Monthly SIP

Period of SIP NIFTY 50 TRI (CAGR) NIFTY NEXT 50 TRI (CAGR) NIFTY 100 TRI (CAGR)

3 Year 12.20% 6.59% 11.40%

5 Year 11.02% 11.16% 11.09%

Risk –Return Analysis of Average Monthly Rolling Returns on Lumpsums

NIFTY 50 TRI NIFTY NEXT 50 TRI NIFTY 100 TRI

LumpsumPeriod

CAGRStandard Deviation

CAGRStandard Deviation

CAGRStandard Deviation

3 Year 11.27% 2.60% 19.64% 4.98% 12.58% 2.71%

5 Year 12.81% 4.29% 19.99% 6.25% 13.94% 4.39%

CAGR: Compounded Annual Growth Rate | TRI – Total Return Index

11

LARGE CAPS MAKE FOR MORE THAN HALF THE

MARKET ACROSS SEASONS.

THAT IS THE EMPHASIS IT DESERVES IN YOUR

PORTFOLIO TOO.

70%

16%

14%

Market Cap Weightages

Large Cap

Mid Cap

Small Cap

Mcap positions as of December 31, 2018 | Source AMFI

12

MAHINDRA PRAGATI BLUECHIP YOJANALarge Cap Fund - An open ended equity scheme predominantly investing in large cap stocks

NFO Opens: February 22, 2019 NFO Closes: March 8, 2019Scheme reopens for continuous sale and repurchase from: within 5 business days from the date of allotment

13

14

REASONS TO INVEST IN MAHINDRA PRAGATI BLUECHIP YOJANA

Agile quality portfolio from India’s

Big 100

Exposure to the more stable half of the

market

High conviction bottom up stock picking with a

focus on alpha generation

15

INVESTMENT STYLE

16

• High conviction*concentrated portfolio with a focus to generate alpha

• Blended style of growth and value stocks

• Top down approach to identify sectors with potential across different periods based on emerging macro trends

• Bottom up stock selection, that have good governance and strong leadership

• Agile portfolio management

• Tactical calls for short to medium investment horizons

INVESTMENT STYLE

*Conviction will be based on internal evaluation and price performance position keeping investor interest in mind

17

FOCUSED APPROACH TOWARDS IDENTIFYING EARLY STRUCTURAL TRENDS

Source: Haitong Securities research, Bloomberg | Data as on Mar 2017

• Fund would be focused on identifying structural trends which may play out over medium to long term. These could include, but not limited to -

• Increase in penetration in certain segments as per capita income of the country increases

• Large market share shifts either from unorganized to organized sectors or between segments of players in the market place

• Major economic transitions in the country such as infrastructure creation, policy reforms, socio economic transitions

• Technological disruptions/enablers which could alter the construct of businesses in the country

• By doing the above, the fund would aim to capture the changes in the index constituents over a period in time even before the same plays out

• A case study provided in the adjacent infographics demonstrates the large gap between India and China in consumer durables penetration which could be bridged as per capita income improves

Per Capita Income of India vs China

Low penetration in consumer durables segment

4xINDIA

$1,752

CHINA

$8,830

5

15

21

100

96

94

- 20 40 60 80 100

Air-conditioners

Washing machines

Refrigerators

China India

CASE STUDY 1: CONSUMPTION SECTOR

18

CAPTURING STRUCTURAL TRENDS CREATES MEANINGFUL ALPHA

Source: RBI, Bloomberg | * Nifty Bank index considered as proxy for private bank returns as PSU representation is fairly lowData as on Dec 30, 2018as on 30 December, 2018

Case Study 2: PSU Banks vs Private Banks

• The extent of market share shift and asset quality difference between PSU banks and private banks would have been difficult to envisage 3 to 5 years back

• But investors who bet on the same would have benefitted significantly over the same period as demonstrated by the returns for these indices

Market share shift from PSU banks to private sector banks

Return difference between PSU Banks and private banks*

Sharp rise in NPA ratio for PSU Banks

-

5.0

10.0

15.0

20.0

25.0

3YR CAGR 5YR CAGRPSU Bank Index Bank IndexNIFTY PSU Bank Index

Market-share FY13 FY15 FY18 5 YR change

PSU Banks 76.1 74.2 65.1 (10.93%)

Private Banks 19.4 21.4 30.4 11%

Foreign Banks 4.5 4.4 4.1 (0.4%)

Small Finance Banks - - 0.4 0.4%

3.7 4.7

13.6

-

5.0

10.0

15.0

FY13 FY15 FY18

NIFTY Bank Index

The data provided above is for illustrative purpose only. Mahindra Asset Management Company Private Limited/Mahindra Mutual Fund is not guaranteeing or forecasting any returns. Past performance may or may not be sustained in future.

19

TACTICAL CALLS TO CAPTURE SHORT TERM SECTOR ROTATION

CASE STUDY 3: METAL AND IT SECTORS

• Periodically, opportunities arise across sectors to benefit from some macro theme impacting the sector

• Cases in point being metal stocks which have strong correlation to commodity prices or IT sector’s dependence on currency

Metal sector performance highly correlated to steel prices

Periods* of correlation between exchange rate and IT sector performance

60.0

110.0

160.0

210.0

260.0

310.0

360.0

410.0

460.0

510.0

Jan

-05

Jan

-07

Jan

-09

Jan

-11

Jan

-13

Jan

-15

Jan

-17

Jan

-19

STEEL vs NSEMET

NSEMET STEEL

6.7

(10.1)

5.7

(10.3)(5.3)

37.0

(7.3)

21.2

(20.0)

(10.0)

-

10.0

20.0

30.0

40.0

Jan'06 - Jul'06 May'10 - Nov'10 Jan'15 - Jul'15 Nov'16 - May'17

PERFORMANCE: USDINR & NSEIT INDEX

USDINR NSEIT

Source: Bloomberg | Data as on Dec 31, 2018 Source: Bloomberg | Data as on Dec 31, 2018

* Only those periods that have exhibited a correlation between exchange rate and IT sector performance have been considered for this analysisPrice

The data provided above is for illustrative purpose only. Mahindra Asset Management Company Private Limited/Mahindra Mutual Fund is not guaranteeing or forecasting any returns. Past performance may or may not be sustained in future.

20

MARKET OUTLOOK

21

MARKET OUTLOOK

• Election results is the most keenly awaited event• We do not expect any major market movement before that• Earnings growth visible despite challenges• Valuation gap between midcap and large cap has narrowed.• Markets awaiting clarity on formation of new government, adherence to fiscal

deficit target for FY 19 and end to U.S.A. China trade war.

FY 19 EPS FY 19 PE FY 20 EPS FY 20 PE

Nifty 50 545 19.9 659 16.4

Nifty Midcap 100 867 19.5 1,136 14.9

INDEX RETURNS FOR CALENDAR 2018(Absolute Returns)

NIFTY 50 + 4.70%Nifty Midcap 100 -15.00%Nifty Smallcap 100 - 28.00%

Data Source: Bloomberg Consensus Estimates | Data as on 31 Jan 2019

All figures are estimates

The data provided above is for illustrative purpose only and should not be construed as a promise on minimum returns and safeguard of capital. Mahindra Asset Management Company Private Limited/Mahindra Mutual Fund is not guaranteeing or forecasting any returns. Past performance may or may not be sustained in future.

22

Source: Value Research : https://www.valueresearchonline.com/story/h2_storyView.asp?str=46202#prettyPhoto

There isn’t any statistical data showing election outcome or government in power or tenure to have any correlation with market performance

SHOULD YOU WORRY ABOUT ELECTION RESULTS?

23

FUND MANAGER PROFILE

24

Mr. V. BalasubramanianChief Portfolio Strategist (Equity)

Mr. V. Balasubramanian has over 38 years of work experience of which around 20 years have been in the Mutual Fund Industry and 8 years in Treasury of a nationalized bank.

Prior to joining Mahindra Asset Management Company Private Limited, he was the Chief Investment Officer at IDBI Mutual Fund.

FUND MANAGER

25

SCHEME DETAILS FOR INVESTMENT

26

Instruments

Indicative Allocation

(% of assets)

Risk Profile

Minimum Maximum High/Medium/Low

Equity and Equity related Securities of Large Cap

companies^*

80 100 High

Equity and Equity Related Securities of other

companies^

0 20 High

Debt and Money Market Securities^ (including

CBLO and Reverse Repo)

0 20 Low to Medium

Units issued by REITs & InvITs 0 10 Medium to High

ASSET ALLOCATION

*Definition of Large Cap Companies: 1st – 100th company in terms of full Market Capitalization. For the purpose of this definition, the list of stocks prepared by AMFI in this regard will be adopted. ^ including derivative instruments to the extent of 50% of the Net Assets of the Scheme. For detailed asset allocation refer SID of the Scheme available at www.mahindramutualfund.com or visit nearest Investor Service Centre.

Benchmark: Nifty 50

27

Available plans for subscription by investors Direct (D), Regular

Available option under each plan Growth (D), Dividend

Available Facilities under Dividend Option Dividend Payout, Dividend Reinvestment (D)

Loads Entry Load: NAExit Load: -An Exit Load of 1% is payable if Units are redeemed / switched-out upto 1 year from the date of allotment;-Nil if Units are redeemed / switched-out after 1 year from the date of allotment.

Minimum Application/ Additional Purchase Amount Rs. 1,000/- and in multiples of Re. 1/- thereafter

Minimum Amount for Switch-in Rs. 1,000/- and in multiples of Re. 0.01/- thereafter.

Minimum Amount for Redemption/ Switch-outs Rs. 1,000/- or 100 units or account balance, whichever is lower

Minimum SIP Amount Rs 500 under monthly frequency; Rs 1500 under quarterly frequency

D- Default

28

This product is suitable for investors who are seeking*

• Long term capital appreciation;

• Investment predominantly in equity and equity related securities including derivatives of large cap companies.

* Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

PRODUCT LABELING

Investors understand that their principal will be moderately high risk

Riskometer

29

ANNEXURES FOR IN-DEPTH DISCUSSIONS

30

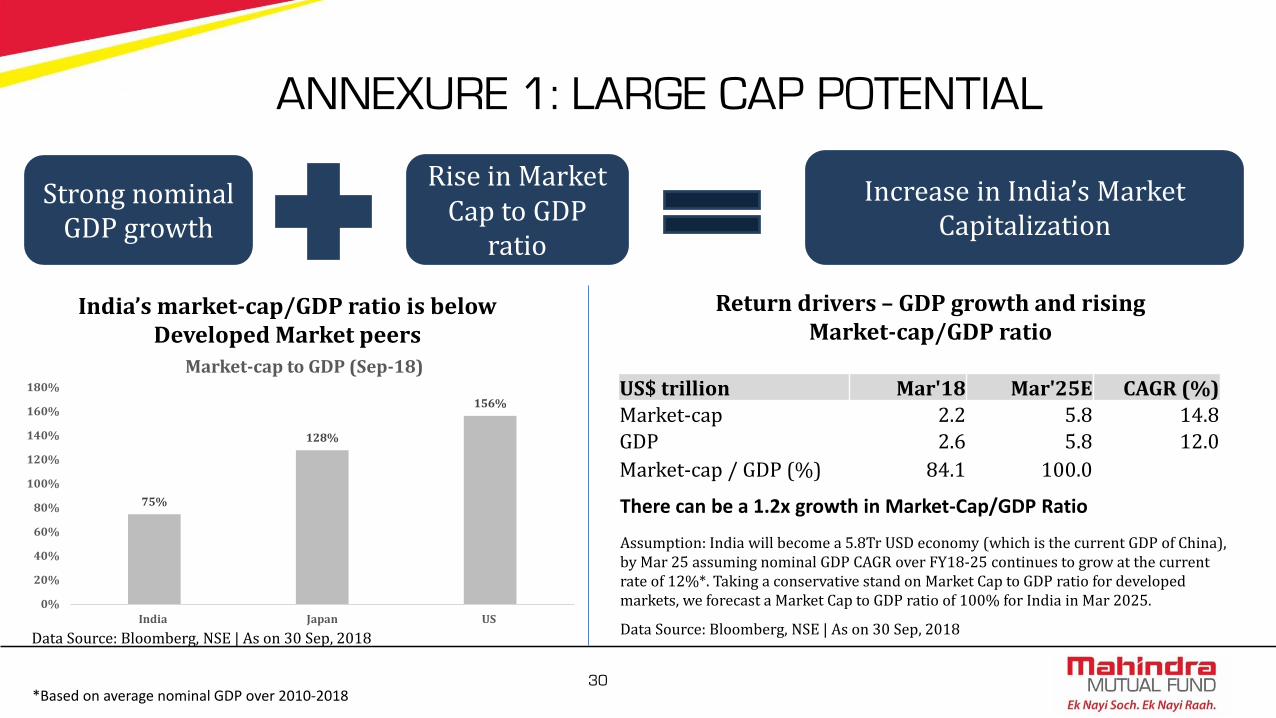

ANNEXURE 1: LARGE CAP POTENTIAL

India’s market-cap/GDP ratio is below Developed Market peers

Data Source: Bloomberg, NSE | As on 30 Sep, 2018

US$ trillion Mar'18 Mar'25E CAGR (%)

Market-cap 2.2 5.8 14.8 GDP 2.6 5.8 12.0

Market-cap / GDP (%) 84.1 100.0

75%

128%

156%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

India Japan US

Market-cap to GDP (Sep-18)

Return drivers – GDP growth and rising Market-cap/GDP ratio

Assumption: India will become a 5.8Tr USD economy (which is the current GDP of China), by Mar 25 assuming nominal GDP CAGR over FY18-25 continues to grow at the current rate of 12%*. Taking a conservative stand on Market Cap to GDP ratio for developed markets, we forecast a Market Cap to GDP ratio of 100% for India in Mar 2025.

Increase in India’s Market Capitalization

Strong nominal GDP growth

Rise in Market Cap to GDP

ratio

There can be a 1.2x growth in Market-Cap/GDP Ratio

Data Source: Bloomberg, NSE | As on 30 Sep, 2018

*Based on average nominal GDP over 2010-2018

31

ANNEXURE 2: LARGE CAP POTENTIAL (Cont..)

Market Capitalization US$ mn

Top-6 US companies market-cap

Microsoft Corp 788

Amazon 770

Google 747

Apple 704

Berkshire Hathaway 480

Facebook 397

Total - top 6 US companies 3,886

India - overall market-cap 2,050

India$2.2tn

India FY25E$5.8tn

Projected Market Capitalization

• Just the Top 6 US companies are 2x the Market Cap of entire India’s listed space

• India’s top 50 companies are less than US$1tn in market cap

Data Source: Bloomberg | As of 7th Jan 2019

Data Source: Bloomberg | As of 7th Jan 2019

32

50.0

55.0

60.0

65.0

70.0

75.0

80.0

85.0

90.0

95.0

100.0

CY07 CY08 CY09 CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17 CY18

LARGE CAP MARKET CAPITALIZATION TO COUNTRY GDP (% )

India Japan US UK

India - NIFTY + NIFTYJR TO GDP 8 YEAR AVERAGE : 67.4%Japan - NIKKEI225 TO GDP 8 YEAR AVERAGE: 60.7%

US - S&P500 TO GDP 8 YEAR AVERAGE: 77.6%UK - FTSE100 TO GDP 8 YEAR AVERAGE: 77.4%

ANNEXURE 3: COMPARISON WITH DEVELOPED

ECONOMIES

Source: Bloomberg| CY18 Data on Sep 30, 2018

33

ANNEXURE 4: VOLATILITY ACROSS MARKET CAPS

Source: Bloomberg, NSE | Data as of Dec 31st, 2018

Lower volatility in large caps compared to mid and small caps

Lower risk of draw downs compared to mid and small caps during corrections

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

Jan

-18

Jan

-19

NIFTY NIFTY Midcap 100 NIFTY Smallcap 100

34

ANNEXURE 5.A: THEMES PLAYING OUT IN THE INDEX

Capex-linked: Industrials, Utilities, Materials, Telecom, EnergyFinancial Services: Banks and Financial ServicesExport-oriented: IT, PharmaceuticalsConsumption-linked: Consumer Staples, Consumer Discretionary

Source: Bloomberg, NSE

31.4

69.4

36.8 25.1 26.6

12.6

11.1

26.2

29.7 37.1

25.3

11.8

18.3 24.4

16.4

30.9

7.6 18.7 20.8 19.9

2 0 0 3 2 0 0 8 2 0 1 2 2 0 1 6 2 0 1 8

NIFTY COMPOSITION* BY SECTOR (%)

• 2003-08: A period of high gross fixed capital formation growth; Rising share of investment linked segment in Nifty reflected this mix well.

• 2008-12: Consumption growth showed strong uptick even as capex slowed down; Pharma exports saw strong traction; Retail financing took strong roots and gained share from unorganized segments; Same got reflected in index mix;

• 2012-16: Above trends got accentuated; So did their reflection in Nifty. Many new NBFCs, private banks saw inclusion in index.

• 2016-18: Moderation in exports; Consumption and Financials services theme continue to see strong growth in economy; Capex stabilizes; All trend captured in Nifty mix;

Changing complexion of economy reflected in Nifty mix change

*Internal thematic classification of Index as per MSCI sectors

35

ANNEXURE 5.B: THEMATIC SPLIT OF THE INDEX

The above classification has been used to demonstrate category movements in NIFTY over years in previous slide

CONSUMPTION LINKED* EXPORT ORIENTED* FINANCIALS SERVICES* CAPEX LINKED*

Automobile - 4 Wheelers Computers - Software Banks and Financial Institutions Engineering

Cigarettes Pharmaceuticals Power

Diversified Mining

Automohiles - 2 And 3 Wheelers Cement & Cement Products

Paints Telecommunication - Services

Media & Entertainment Oil Exploration / Production

Auto Ancillaries Steel & Steel Products

Aluminium

Gas

Shipping

PESTICIDES AND AGROCHEMICALS

Telecommunication - Equipment

Electrical Equipment

Construction

Metals

*Internal thematic classification of Index as per MSCI sectors

36

The views expressed here in this presentation are for general information and reading purpose only and do not constitute anyguidelines and recommendations on any course of action to be followed by the reader / user of this presentation. No representationor warranty is made as to the accuracy, completeness or fairness of the information and opinions contained herein. The views are notmeant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of anyfinancial product or instrument or mutual fund units for the reader / user. This presentation has been prepared on the basis of publiclyavailable information, internally developed data and other sources believed to be reliable. While utmost care has been exercised whilepreparing this presentation, Mahindra Asset Management Company Private Limited (Mahindra AMC) does not warrant thecompleteness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information.The data/statistics, wherever provided, are given to explain general market trends in the securities market, it should not be construedas any research report/research recommendation. Readers / users of this presentation should rely on information / data arising out oftheir own investigations and are advised to seek independent professional advice and arrive at an informed decision before makingany investments. Neither Mahindra Mutual Fund, Mahindra AMC nor Mahindra Trustee Company Private Limited, its directors orassociates shall be liable for any damages that may arise from the use of the information contained herein.

For detailed asset allocation, investment strategy, scheme specific risk factors and more details, please read the SchemeInformation Document and Key Information Memorandum of Mahindra Pragati Bluechip Yojana available at the ISCs ofMahindra AMC and Computer Age Management Services Private Limited and are also available onwww.mahindramutualfund.com. Past performance may or may not be sustained in the future and should not be used as abasis for comparison with other investments.

Mutual fund investments are subject to market risks read all scheme related documents carefully.

CNo.00446

Disclaimer

धन्यवादThank You