make japan great again - wordpress.com 02, 2015 · make japan great again ... a town in fukushima...

TRANSCRIPT

Page 1 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Make Japan Great Again

How to halt mass migration out of Japan’s prefectures

Mike Newman President & CEO Analogica K.K.

February 8th, 2017

Page 2 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

The sad tale of Yubari City

Economic woes

Hokkaido in trouble

Akita the oldest prefecture in

Japan

Flocking to the big smoke

Merging towns

Tohoku most troubled

Depopulation

The state of inter-prefectural migration – a disturbing summary

The campaign poster on the cover page is from Yubari City in Hokkaido – “No money but love.”

Yubari is notable for five things. First, it is the region that produces Japan’s most expensive melons,

the type you see beautifully encased in a satin-lined pine box with a price label of US$200. Second,

it had to declare bankruptcy in 2007. Third, its population has fallen from 117,000 in the 1960s to

around 21,000 in the 1990s to less than 8,900 today, falling 19% in the last 5 years alone. Fourth,

the average age of the city’s residents is set to hit 65 by 2020. Fifth, taxable income continues to fall

with estimates that government coffers will swell by a woozy 25% of the levels seen 20 years ago.

Their claim that Yubari has the lowest divorce rate in Japan doesn’t seem to be stopping residents

from divorcing it. In fact, as we learnt in our Crime in Japan series, economic woes are preventing

more couples from divorcing but even some that break their vows end up living under the same roof.

The problem is so prevalent that the National Police Agency had to invent a new category for

domestic violence to tally the sharp rise in cases in 2014 of divorced couples living together.

Hokkaido’s woes are not just limited to Yubari. Sadly, the northern island holds 6 of the top 15

prefectures across Japan experiencing an exodus of its citizens. Hokkaido has 85 villages with less

than 5,000 residents. Over the last 5 years in percentage terms, Yubari has seen a greater flood of

people than Minamisoma, a town in Fukushima Pref. on the 30km exclusion zone border to the north

of the crippled Fukushima Daiichi nuclear reactor.

Akita Prefecture has the highest percentage of 65yo+ citizens in Japan at 33.2% of the prefectural

total. Over 27% of its workforce is in construction and manufacturing. In what world, can a community

avert such a skewed employment picture? If the working aged populace is leaving with their kids

(high school enrolment is down 22% in 5 years), one of the highest natural population declines and

Akita has the second highest prefectural debt per capita what need is there for new construction

projects or the rationale for a corporate to expand local production?

Perhaps not surprising, many citizens are seeking new fortunes in the major cities – Tokyo, Osaka,

Nagoya, Yokohama, Saitama and Chiba are capturing the socio-economic spoils. One name that

did surprise was Fukuoka in the southern island of Kyushu. Fukuoka Pref. can claim 3 of the top 20

fastest growing cities in Japan.

Around 20 years ago, the Japanese government embarked on a program known as

‘Shichosongappei’ (市町村合併)which loosely translates as mergers of cities and towns. However

as much as that plan to sensibly merge public services was – e.g. waste collection, councils, schools

and hospitals – the cities (especially to the north) have continued to shrink. Age is a big factor which

shows up in prefectural GDP/capita as well as suicide rates.

Cities in the northern prefectures (Tohoku) face the biggest challenges. The Great East Japan

Disaster of March 2011 has only exacerbated the move out of these areas. Eight of the top 10 places

for fastest rates of depopulation are in Tohoku. Shikoku, and cities on the Japan Sea coast are also

at the mercy of residents pulling up roots. We colour code these prefectures to show how our ‘basket’

correlates highly.

Our biggest concern in summary

Our biggest concern remains that of rapid acceleration of depopulation going forward. Things seem

normal until the Rubicon is crossed. Then the damned flood can’t be dammed. As the productive

Page 3 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Similar to German

reunification

Japan’s policies failing

Debt: Resident

Detroit

workforce looks to abandon its roots in search of sustainability we fear that corporates also face a

big dilemma. As was experienced with German reunification workers flocked to more economically

viable areas in the West scorching those businesses in the East. East German regions had to hike

wages significantly to stem the tide, ruining profitability. Even today the East has significantly higher

unemployment rates than the former West as businesses in the former communist bloc went to the

wall (no pun intended).

The Japanese government’s plans to revitalise the regions are not working because economic

reversals all hinges on confidence. The chicken and egg argument is simple. If corporates fear not

enough workers will remain to justify production and workers think long term quality of life will be far

more sustainable in economically healthier areas, growth won’t happen in the regions.

As regional Japan continues to shrink, the pressure will then be put back on the fiscal status of the

prefectural governments. The Japan Local Government Bond Association (JLGBA) highlights that

the financial strength index (FSI) of Shimane is the poorest in Japan. To put that in the context of

Detroit, which declared bankruptcy in 2013. Detroit has approximately $30,000 debt per resident

today. Looking at Shimane Prefecture its citizens carry around $14,000 prefectural government debt

per resident. Given the working age population of 54% (and falling) that number balloons to around

$26,000 per working age resident. Debt servicing (around 16% in Shimane) is one thing but in the

last 6 months, yields have begun to climb. As we know debt financing can turn on a dime.

Source: Custom Products Research, Japan Statistics Bureau

Although Detroit is incomparable on most measures to Japan it does highlight what a city can look

like when economic fortunes reverse. 30% of Detroit’s residents disappeared in 15 years. From the

highest per capita income in America during the 1960s it now languishes toward the bottom. 40%

live in poverty and the state suffered the ignominy of half the 350,000 home owners paid no property

taxes in 2011.

3,719,103

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

Shim

ane

Aki

ta

Toku

shim

a

Ko

chi

Tott

ori

Toya

ma

Iwat

e

Yam

anas

hi

Fuku

i

Ish

ikaw

a

Yam

agat

a

Ho

kkai

do

Niig

ata

Wak

ayam

a

Kag

osh

ima

Ao

mo

ri

Yam

agu

chi

Miy

azak

i

Oit

a

Kag

awa

Nag

asak

i

Saga

Ku

mam

oto

Nar

a

Hyo

go

Ehim

e

Nag

ano

Hir

osh

ima

Mie

Gif

u

Oka

yam

a

Kyo

to

Fuku

shim

a

Shiz

uo

ka

Shig

a

Ibar

aki

Miy

agi

Fuku

oka

Aic

hi

Osa

ka

Gu

nm

a

Toch

igi

Sait

ama

Ch

iba

Oki

naw

a

Kan

agaw

a

Toky

o

Fig. 1 - Prefectural Debt/30% fall in working age Citizens (¥)

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

Page 4 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Polish style tax reform

The sorry tale of Yubari

The Solution – Polish style tax reform

Our solution is to adopt a Polish style tax reform which simplifies the system and gets the 70% of

corporations that don’t pay tax to contribute. Poland doubled corporate tax revenues on a halving of

tax rates in short order as a result of making tax avoidance (not evasion) no longer worth it. Japan

must take risks – it has nothing to lose.

Source: Custom Products Research

Let’s look at the problem and solutions more deeply.

Here yesterday, gone today

Yubari City is a tragedy. Its population is 90% lower than it was in the 1960s. Yet its legacy is likely

to be repeated as other cities fade out. These ghost towns are not merely dying because its elderly

citizens are shuffling off this mortal coil, the youth and working aged population are seeing little

prospects for the future and are congregating in the more populous areas which offer much more

viable economic scope.

Let us begin with the fastest depopulating cities in Fig.3.

-0.027

-0.295

0.619

0.559

0.260

0.184 0.175

0.059

-0.400

-0.200

0.000

0.200

0.400

0.600

0.800

Iwat

e A

kita

Ao

mo

ri Y

amag

uch

i Y

amag

ata

Oki

naw

a T

ott

ori

To

yam

a N

agan

o S

him

ane

Ho

kkai

do

Eh

ime

Osa

ka H

yogo

Kag

osh

ima

Nar

a K

um

amo

to O

ita

Fu

kush

ima

Ko

chi

Sag

a T

oku

shim

a F

uku

i N

agas

aki

Niig

ata

Sh

iga

Kag

awa

Yam

anas

hi

Ibar

aki

Oka

yam

a M

ie M

iyaz

aki

Gu

mm

a H

iro

shim

a F

uku

oka

Kan

agaw

a K

yoto

Ch

iba

Sh

izu

oka

To

chig

i S

aita

ma

Gif

u M

iyag

i W

akay

ama

Aic

hi

Ish

ikaw

a T

oky

oJa

pan

Fig. 2: 10yr current bond yields by prefecure (%) vs 10yr yields 6mths prior

Generic 10yr Yield - July 2016 Generic 10yr Yield - Jan 2017

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

Page 5 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Hokkaido & Akita..

Aged population

skewed

Source: Custom Products Research, Japan Statistics Bureau

While many of these cities in Fig. 3 are relatively small (ranging from 3,500 to 65,000) the larger

cities in Hokkaido (Chitose and Sapporo have moved a mere +2% in the past 5 years) while all

others are at stall speed or falling. In the case of Akita Pref. all cities are in retreat, Fig.4.

Source: Custom Products Research, Japan Statistics Bureau

When we analyse the population pyramid we note that Akita tops the highest 65yo+ population in

the nation at 33%, Fig. 8. In the following charts, we’ll highlight Fukuoka (especially Fukuoka City)

as a hot spot outside the main metropoles. As the largest city in Kyushu it seems to be attracting

firm population growth which looks sustainable.

-19.0-18.5

-18.2

-15.2

-14.0

-12.2 -12.1 -11.9-11.7 -11.7 -11.5

-20.0

-19.0

-18.0

-17.0

-16.0

-15.0

-14.0

-13.0

-12.0

-11.0

-10.0 Yubari Minamisoma Utashinai Rikuzentakata Tosashimizu Akabira Oga Kumano Ashibetsu Kesennuma Bibai

Hokkaido Fukushima Pref Hokkaido Iwate Pref Kochi Pref Hokkaido Akita Pref Mie Pref Hokkaido Miyagi Pref Hokkaido

Fig.3 : % Rate of population change (2010-15)

Wiped out by tsunami in Mar 2011

On the 30km exclusion zone border north of Fukushima Daiichi nuclear plant

28,39533,230

46,620

25,330

54,746

32,057 27,530

82,77392,214

79,993 74,153

33,098

315,374

-12.1

-8.7-8.3 -8.0

-7.3 -7.0-6.9

-6.3 -6.3 -6.1 -6.1

-3.9-2.5

-14.0

-12.0

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Oga Kitaakita Yuzawa Nikaho Noshiro Kazuno Semboku Daisen Yokote Yurihonjo Odate Katagami Akita

Fig. 4: Disappearing Akita Prefecture (2010-2015) - fall in population over 5 years

Population % Rate of population change (2010-15)

Page 6 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Fukuoka looks vibrant

Osaka anomaly

Age a factor

Source: Custom Products Research, Japan Statistics Bureau

We can see in Fig. 5 that quite a lot of Fukuokan towns have seen solid growth over the past 5

years. If we roll out the 15-year average we can clearly see that Fukuoka Pref has been the strongest

regional area of all. It should come as no surprise that the metropoles of Tokyo, Yokohama

(Kanagawa Pref), Saitama, Chiba Pref and Nagoya (Aichi Pref) has claimed the bulk of the exodus.

As Fig.6 shows, only 9 out of 47 prefectures have experienced net annual population inflows over

the last 15 years.

Even Osaka saw average outflows of 7,200 per annum although part of that is to do with its close

proximity to Hyogo & Nara prefectures and rising numbers of commuters taking advantage of

cheaper property and relatively short journeys to work in Japan’s second largest city.

Source: Custom Products Research, Japan Statistics Bureau

Boiling down deeper into the data we see how age is a factor. When looking at the 0-14yo and 65yo+

populations by prefecture there is little surprise, Figs. 7-8. All of Tohoku has a 0-14yo population

below the national average and 5 out of 6 have 65yo+ populations above the national average.

Fukuoka Prefecture is the opposite. Hokkaido falls on the wrong side of both categories.

192,554 228,200 206,974

58,808

1,538,510

306,014

99,575 110,767

255,852 217,943

72,200

7.97.4 7.1

6.1

5.14.7 4.7

3.73.5

3.0

2.4

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

Chuo-ku Hakata-ku Nishi-ku Fukutsu Fukuoka Higashi-ku Onojo Kasuga Minami-ku Sawara-ku Dazaifu

Fig. 5: Fighting Fukuoka Pref (2010-2015)

Population % Rate of population change (2010-15)

66,653

3,650

903

-9,772

-20,000

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Toky

o

Kan

agaw

a

Sait

ama

Ch

iba

Aic

hi

Fuku

oka

Shig

a

Oki

naw

a

Miy

agi

Toch

igi

Toya

ma

Ish

ikaw

a

Tott

ori

Oka

yam

a

Kag

awa

Ko

chi

Shim

ane

Gu

mm

a

Yam

anas

hi

Toku

shim

a

Mie

Fuku

i

Saga

Oit

a

Hyo

go

Ku

mam

oto

Nag

ano

Kyo

to

Wak

ayam

a

Miy

azak

i

Hir

osh

ima

Ehim

e

Nar

a

Kag

osh

ima

Ibar

aki

Yam

agu

chi

Yam

agat

a

Iwat

e

Gif

u

Aki

ta

Shiz

uo

ka

Fuku

shim

a

Niig

ata

Ao

mo

ri

Nag

asak

i

Osa

ka

Ho

kkai

do

Fig. 6: Average Annual Prefectural Migration over the last 15 years

Page 7 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Okinawa the youngest

Shimane the same as 1920

Source: Custom Products Research, Japan Statistics Bureau

Okinawa is the prefecture with the youngest population. As far as its towns are concerned, Okinawa

is still seeing mild net migration. The largest city of Naha has grown 1.1% over the last 5 years

although smaller towns are growing faster. Only Miyakojima is sliding.

Source: Custom Products Research, Japan Statistics Bureau

When we look at population growth in the period since 1920, some sad tales are told. Shimane

Prefecture on the Japan Sea coast has not grown at all in almost 100 years. Kanagawa Prefecture

on the other hand has ballooned almost 6x, Fig.9. All prefectures in Tohoku, bar Miyagi (Sendai)

have seen population growth rates under the national average over the respective period.

17.0%

12.9%

12.5% 12.4%12.1%

11.9%

11.3%

11.2%

11.2%

10.5%

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

16.0%

17.0%

18.0%

Oki

naw

a

Shig

a

Saga

Aic

hi

Ku

mam

oto

Miy

azak

i

Kag

osh

ima

Gif

u

Fuku

i

Hir

osh

ima

Shiz

uo

ka

Toch

igi

Nag

ano

Gu

mm

a

Oka

yam

a

Ish

ikaw

a

Mie

Fuku

oka

Hyo

go

Nag

asak

i

Tott

ori

Ibar

aki

Kag

awa

Kan

agaw

a

Oit

a

Jap

an

Ch

iba

Sait

ama

Toya

ma

Miy

agi

Osa

ka

Yam

anas

hi

Shim

ane

Nar

a

Yam

agu

chi

Ehim

e

Yam

agat

a

Kyo

to

Niig

ata

Wak

ayam

a

Iwat

e

Ko

chi

Toku

shim

a

Ao

mo

ri

Fuku

shim

a

Ho

kkai

do

Toky

o

Aki

ta

Fig.7: Japan's 2015 Population - 0-14yo

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

33.2%

30.5% 30.2%29.5%

28.9% 28.7%

26.3%25.5%

25.0%

19.5%

15.0%

17.0%

19.0%

21.0%

23.0%

25.0%

27.0%

29.0%

31.0%

33.0%

35.0%

Aki

ta

Ko

chi

Shim

ane

Yam

agu

chi

Wak

ayam

a

Yam

agat

a

Toku

shim

a

Toya

ma

Iwat

e

Ehim

e

Oit

a

Niig

ata

Ao

mo

ri

Nag

ano

Kag

awa

Tott

ori

Nag

asak

i

Ho

kkai

do

Kag

osh

ima

Miy

azak

i

Fuku

shim

a

Ku

mam

oto

Fuku

i

Nar

a

Oka

yam

a

Yam

anas

hi

Hir

osh

ima

Gif

u

Saga

Shiz

uo

ka

Ish

ikaw

a

Mie

Gu

mm

a

Kyo

to

Hyo

go

Jap

an

Ibar

aki

Osa

ka

Ch

iba

Toch

igi

Fuku

oka

Miy

agi

Sait

ama

Shig

a

Kan

agaw

a

Aic

hi

Toky

o

Oki

naw

a

Fig.8: Japan's 2015 Population - 65yo+

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

Page 8 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

GDP/Capita

Crime

Source: Custom Products Research, Japan Statistics Bureau

When digging a bit deeper into the economics of the prefectures, it is clear to see that those with a

GDP/capita below the national average are those seeing an exodus of population, Fig.10. Naturally

all of Tohoku and Hokkaido are on the wrong side of the curve.

Source: Custom Products Research, Japan Statistics Bureau, Ministry of Finance

Two other sets of data to analyse the plight of these regions is the incidence of crime and suicide

rates by prefecture, Figs. 11-12.

In a somewhat counter-intuitive looking chart for a law-abiding country, perhaps a good indicator for

relative economic strength is crimes committed. The economic rationale for crime would be the

ability for the ‘second hand’ grey market to thrive in stolen goods. In the Tohoku region, crimes

committed per 100,000 population take the bottom four places which is unlikely to be solely down to

the inability of pensioners to literally outrun the law.

58

3.9

%

44

5.1

%

36

5.3

%

25

5.7

%

25

4.6

%

24

2.5

%

14

8.0

%

144.

1%

14

3.5

%

14

2.9

%

14

2.7

%

13

3.4

%

13

1.8

%

12

8.8

%

12

0.0

%

11

6.7

%

104.

8%

94

.5%

92

.0%

90

.7%

85

.5%

81

.6%

74

.3%

73

.5%

59

.7%

57.2

%

56

.6%

51

.0%

48

.9%

48

.0%

47

.4%

46

.9%

39

.4%

39

.2%

37

.7%

36

.7%

34

.6%

33

.7%

33

.6%

29

.5%

26

.1%

25

.6%

20

.8%

20

.6%

20

.5%

17

.2%

13

.9%

0.3

%

0.0%

100.0%

200.0%

300.0%

400.0%

500.0%

600.0%

700.0%

Kan

agaw

aSa

itam

aC

hib

aTo

kyo

Aic

hi

Osa

kaN

ara

Miy

agi

Oki

naw

aSh

izu

oka

Hyo

goH

okk

aid

oFu

kuo

kaJa

pan

Ibar

aki

Shig

aK

yoto

Gif

uTo

chig

iG

um

ma

Hir

osh

ima

Ao

mo

riM

iyaz

aki

Mie

Oka

yam

aIw

ate

Ish

ikaw

aTo

yam

aFu

kush

ima

Yam

anas

hi

Ku

mam

oto

Kag

awa

Yam

agu

chi

Oit

aN

agan

oEh

ime

Fuku

iN

iigat

aW

akay

ama

Tott

ori

Saga

Nag

asak

iA

kita

Yam

agat

aK

ago

shim

aTo

kush

ima

Ko

chi

Shim

ane

Fig.9: Population change in the prefectures between 1920 & 2013 (%)

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

4,423

2,9722,795

2,035

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Toky

o

Aic

hi

Shiz

uo

ka

Ibar

aki

Shig

a

Toya

ma

Toch

igi

Hir

osh

ima

Nat

ion

al A

vera

ge

Kyo

to

Osa

ka

Yam

agu

chi

Mie

Kan

agaw

a

Gu

mm

a

Kag

awa

Ish

ikaw

a

Yam

anas

hi

Ch

iba

Sait

ama

Fuku

i

Fuku

oka

Wak

ayam

a

Toku

shim

a

Niig

ata

Oka

yam

a

Gif

u

Miy

agi

Hyo

go

Nag

ano

Fuku

shim

a

Iwat

e

Yam

agat

a

Oit

a

Ho

kkai

do

Ehim

e

Aki

ta

Ku

mam

oto

Ao

mo

ri

Saga

Nag

asak

i

Nar

a

Kag

osh

ima

Shim

ane

Miy

azak

i

Ko

chi

Tott

ori

Oki

naw

a

Fig. 10: GDP/Capita by Prefecture (¥1,000)

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

Page 9 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Suicide

Residents to teacher

Source: Custom Products Research, Japan National Police Agency

Perhaps a more depressing statistic is to analyse the incidence of suicides in the prefectures. Sadly,

our worst fears are confirmed yet again. All of Tohoku is above the national average. Clearly, many

see little way out of hardship. We note the Japanese National Police Agency records that suicides

by age group show the 65yo+ age group to represent 40% of the total in 2014 up from 27% in the

early 1980s. Tohoku as we showed earlier has population rates of elderly above the national

average.

Source: Custom Products Research, Japan National Police Agency

We took a slightly more abstract way of looking at the state of prefectures using the incidence of the

number of residents per teacher. Once again, the idea that teachers would look to seek schools in

regions with a sustained future, Fig. 13. Fukuoka is once again the standout among the regional

areas by a substantial margin. Despite Kyushu possessing higher than national average 0-14yo

populations, the teacher numbers seem to be lagging growth.

1424.4

831

394.8

0

200

400

600

800

1000

1200

1400

1600

1800

Osa

ka

Fuku

oka

Aic

hi

Hyo

go

Toky

o

Ch

iba

Sait

ama

Ibar

aki

Kyo

to

Gif

u

Mie

Oka

yam

a

Shig

a

Wak

ayam

a

Toch

igi

Gu

nm

a

Ehim

e

Ko

chi

Yam

anas

hi

Kag

awa

Saga

Nar

a

Shiz

uo

ka

Kan

agaw

a

Miy

agi

Hir

osh

ima

Ho

kkai

do

Oki

naw

a

Niig

ata

Kag

awa

Yam

agu

chi

Miy

azak

i

Fuku

shim

a

Tott

ori

Ku

mam

oto

Nag

ano

Fuku

i

Ish

ikaw

a

Shim

ane

Kag

osh

ima

Toya

ma

Nag

asak

i

Oit

a

Ao

mo

ri

Yam

agat

a

Iwat

e

Aki

ta

Fig. 11: Crimes Committed per 100,000 by Prefecture (%) in 2014

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

30.3

28.9

26.4

26.1

24.

8

24.7

24.5

23.8

23.6

22.7

22.6

22.4

22.3

22.3

22.1

22.1

21.9

21.8

21.8

21.6

21.3

21.2

21.1

20.6

20.3

20.3

20.3

20.1

20.0

19.8

19.8

19.8

19.7

19.5

19.4

19.4

19.1

19.1

18.9

18.9

18.7

18.3

18.2

18.1

17.2

16.9

15.7

15.7

15

17

19

21

23

25

27

29

31

33

Yam

anas

hi

Iwat

e

Aki

ta

Niig

ata

Miy

azak

i

Toya

ma

Fuku

shim

a

Ko

chi

Shim

ane

Kag

osh

ima

Nag

ano

Ao

mo

ri

Miy

agi

Ehim

e

Gif

u

Yam

agat

a

Toku

shim

a

Jap

an

Toch

igi

Gu

mm

a

Fuku

oka

Ho

kkai

do

Nag

asak

i

Hyo

go

Shiz

uo

ka

Shig

a

Wak

ayam

a

Oki

naw

a

Hir

osh

ima

Toky

o

Oit

a

Saga

Tott

ori

Ch

iba

Ibar

aki

Mie

Sait

ama

Yam

agu

chi

Kyo

to

Ku

mam

oto

Aic

hi

Kag

awa

Fuku

i

Nar

a

Ish

ikaw

a

Oka

yam

a

Kan

agaw

a

Osa

ka

Fig. 12: Suicide rates by Prefecture (per 100,000) - 2014

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

Page 10 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Teachers/ School

Change in schools

Source: Custom Products Research, Ministry of Education, Culture, Sports, Science and Technology.

Teachers per school in each prefecture paints a similar picture. Fukuoka comes up positively on this

measure. Much of Kyushu on the other hand slips below the national average. Shikoku and the

Japan Sea prefectures also feature poorly.

Source: Custom Products Research, Ministry of Education, Culture, Sports, Science and Technology

Analysing the net change in the number of middle/high schools in 2015 vs 2009 also backs up the

claim that many of the identified regions are not only bleeding teachers and students but scuttling

schools. The sixteen highest percentage school closures by prefecture in that period were in Tohoku,

Shikoku, Kyushu and Japan Sea coast towns, Fig. 15.

2823.6

2411.3

2195.9

1968.6

1848.6

1686.7

1379.3

1000.0

1200.0

1400.0

1600.0

1800.0

2000.0

2200.0

2400.0

2600.0

2800.0

3000.0K

och

iK

ago

shim

aSh

iman

eSa

gaO

kin

awa

Iwat

eM

iyaz

aki

Nag

asak

iYa

man

ash

iA

om

ori

Tott

ori

Wak

ayam

aYa

mag

ata

Oit

aFu

kush

ima

Kag

awa

Toku

shim

aA

kita

Fuku

iTo

yam

aK

um

amo

toIs

hik

awa

Nag

ano

Yam

agu

chi

Oka

yam

aM

ieEh

ime

Shig

aK

yoto

Gif

uH

okk

aid

oM

iyag

iIb

arak

iN

iigat

aG

un

ma

Nar

aH

iro

shim

aTo

chig

iSh

izu

oka

Hyo

goN

atio

nal

Ave

rage

Osa

kaFu

kuo

kaA

ich

iC

hib

aSa

itam

aTo

kyo

Kan

agaw

a

Fig. 13 - Population: Teacher ratio per prefecture (2015)

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

58.6

52.2

47.6

37.4

30.0

35.0

40.0

45.0

50.0

55.0

60.0

65.0

Osa

ka

Sait

ama

Oki

naw

a

Aic

hi

Kan

agaw

a

Ch

iba

Fuku

oka

Kag

awa

Mie

Shiz

uo

ka

Kyo

to

Yam

anas

hi

Miy

azak

i

Nar

a

Hyo

go

Toch

igi

Shig

a

Miy

agi

Ku

mam

oto

Ibar

aki

Nat

ion

al A

vera

ge

Saga

Gu

nm

a

Oka

yam

a

Kag

osh

ima

Wak

ayam

a

Yam

anas

hi

Fuku

i

Toky

o

Ko

chi

Toku

shim

a

Oit

a

Ish

ikaw

a

Nag

ano

Toya

ma

Ehim

e

Niig

ata

Tott

ori

Yam

agat

a

Hir

osh

ima

Nag

asak

i

Aki

ta

Ao

mo

ri

Fuku

shim

a

Iwat

e

Shim

ane

Yam

agu

chi

Ho

kkai

do

Fig.14 - Teachers per school by prefecture (2015)

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

Page 11 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Akita seen a 22% fall in

students

I

Fiscal state of prefectures

Source: Custom Products Research, Ministry of Education, Culture, Sports, Science and Technology

If we dig one level deeper into students enrolled in middle/high school, the impacts are even worse,

Fig. 16. Akita has seen a 22% decline in high school students over the last 6 years versus the

national average of -4% and Fukuoka at -2.2%. 18 of the worst 21 prefectures once again fall into

the basket of what we have identified as depopulating zones.

Source: Custom Products Research, Ministry of Education, Culture, Sports, Science and Technology

The Statistics Bureau also posts some interesting subject matter on the fiscal state of the

prefectures. Put simply, the danger faced by state and local governments is simple. While everyone

faces a national tax levy in some form (income and/or consumption tax), local taxes are only paid if

one lives there on Dec 31st. This paints a rather disturbing picture because the worse off fiscally a

prefecture is, the higher the likelihood of crimped services thanks to higher debt burdens. However,

a resident can pull up the tent pegs and relocate to a healthier prefecture and there is nothing the

incumbent prefecture can do about it. Therefore, the future burden is exacerbated and the likelihood

of further local bankruptcies is heightened.

-17.5%

-10.5%

-4.9%

-2.3% -1.6%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

Yam

agat

aIw

ate

Aki

taK

ago

shim

aK

agaw

aK

um

amo

toN

agas

aki

Ish

ikaw

aH

okk

aid

oK

och

iFu

kush

ima

Ehim

eM

iyag

iA

om

ori

Saga

Shim

ane

Oki

naw

aIb

arak

iH

iro

shim

aTo

chig

iYa

mag

uch

iW

akay

ama

Gu

mm

aM

ieG

ifu

Oka

yam

aN

atio

nal

Ave

rage

Oit

aN

iigat

aYa

man

ash

iN

ara

Fuku

oka

Hyo

goM

iyaz

aki

Toya

ma

Kan

agaw

aN

agan

oK

yoto

Toky

oC

hib

aO

saka

Tott

ori

Toku

shim

aSa

itam

aSh

iga

Shiz

uo

kaA

ich

iFu

kui

Fig. 15 - % change in number of Middle/High schools (2015 vs 2009) by prefecture

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

-21.6%

-16.7%

-10.2%

-4.0%

-2.2%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

Aki

ta

Ao

mo

ri

Fuku

shim

a

Nag

asak

i

Yam

anas

hi

Niig

ata

Wak

ayam

a

Miy

azak

i

Yam

agat

a

Kag

osh

ima

Iwat

e

Shim

ane

Ho

kkai

do

Ehim

e

Ko

chi

Fuku

i

Oit

a

Toku

shim

a

Ku

mam

oto

Yam

agu

chi

Saga

Nar

a

Nag

ano

Gu

mm

a

Tott

ori

Ibar

aki

Miy

agi

Hir

osh

ima

Mie

Gif

u

Nat

ion

al A

vera

ge

Toch

igi

Shiz

uo

ka

Toya

ma

Oki

naw

a

Ish

ikaw

a

Oka

yam

a

Hyo

go

Fuku

oka

Kyo

to

Sait

ama

Osa

ka

Toky

o

Ch

iba

Aic

hi

Kag

awa

Kan

agaw

a

Shig

a

Fig. 16: Net % change in students enrolled in High School 2015 vs 2009

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

Page 12 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Future burden ratio

Financial strength index

Bond yields

Source: Custom Products Research, Japan Statistics Bureau, Ministry of Finance

The future burden ratio is the ratio of the debt currently held by local governments (the amount of

repayment of municipal bonds and the amount equivalent thereto) as a percentage of fiscal intake.

It is considered to be dangerous waters if it exceeds 400% in prefectural governments and 350% in

the municipalities. In FY2011, Yubari City had a future burden ratio of 891%.

Source: Custom Products Research, Japan Statistics Bureau, Ministry of Finance

The financial strength index (FSI) reflects the financial strength of local and prefectural governments.

It is derived by dividing basic financial revenue by financial spending. An FSI closer to or exceeding

one is considered healthy. Closer to zero is a poor score. Once again, the FSI by prefecture shows

the depopulating prefectures are suffering much greater than those growing. It makes sense. Higher

populations should lead to improving tax take.

Looking at the current 10-year bond yields we note that the usual suspects have seen the sharpest

rises and highest levels, Fig.19. While the Japan Local Government Bond Association (JLGBA)

333.0

247.7 241.2

187.0

49.7

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

Hyo

goH

okk

aid

oN

iigat

aTo

yam

aK

yoto

Fuku

oka

Hir

osh

ima

Aki

taIb

arak

iIw

ate

Yam

agat

aSh

izu

oka

Kag

osh

ima

Ish

ikaw

aYa

mag

uch

iYa

man

ash

iA

ich

iO

saka

Sait

ama

Oka

yam

aSh

iga

Gif

uK

um

amo

toK

agaw

aM

ieW

akay

ama

Toku

shim

aM

iyag

iN

atio

nal

Ave

rage

Nag

asak

iN

agan

oSh

iman

eFu

kui

Nar

aO

ita

Ch

iba

Gu

nm

aEh

ime

Ko

chi

Ao

mo

riK

anag

awa

Fuku

shim

aM

iyaz

aki

Saga

Tott

ori

Toch

igi

Oki

naw

aTo

kyo

Fig. 17: Future Burden Ratio by Prefecture (%)

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

0.93

0.60

0.47

0.40

0.280.23

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Toky

oA

ich

i

Kan

agaw

aC

hib

aSa

itam

aO

saka

Shiz

uo

ka

Ibar

aki

Hyo

go

Fuku

oka

Toch

igi

Gu

nm

aH

iro

shim

a

Mie

Miy

agi

Kyo

toSh

iga

Gif

uO

kaya

ma

Nat

ion

al A

vera

geFu

kush

ima

Nag

ano

Ish

ikaw

a

Kag

awa

Toya

ma

Niig

ata

Yam

agu

chi

Nar

a

Ho

kkai

do

Ehim

e

Yam

anas

hi

Fuku

i

Ku

mam

oto

Oit

a

Yam

agat

aIw

ate

Ao

mo

riSa

ga

Wak

ayam

aK

ago

shim

a

Miy

azak

iN

agas

aki

Toku

shim

aO

kin

awa

Aki

taTo

tto

ri

Ko

chi

Shim

ane

Fig. 18: Financial strength index by Prefecture (%) - 2015

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

Page 13 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Shotgun weddings

What industries employ?

Source: Custom Products Research

Switching gears to the prevalence of marriage during pregnancy or post child-birth (i.e. shotgun

weddings) our depopulating prefectures have a higher incidence. With a falling population,

businesses find it harder to justify operating there no doubt leaving residents with fewer things to do

compared to the cities.

Source: Custom Products Research, Ministry of Health, Labor & Welfare (MHLW)

This would also point to the prevalence of job opportunities in each prefecture. As two extreme

examples, we look at Akita and Aomori and look at Tokyo and Kanagawa as bellwethers. Fukuoka

is for illustrative purposes only. What sort of jobs employ in each prefecture?

-0.027

-0.295

0.619

0.559

0.260

0.184 0.175

0.059

-0.400

-0.200

0.000

0.200

0.400

0.600

0.800

Iwat

e A

kita

Ao

mo

ri Y

amag

uch

i Y

amag

ata

Oki

naw

a T

ott

ori

To

yam

a N

agan

o S

him

ane

Ho

kkai

do

Eh

ime

Osa

ka H

yogo

Kag

osh

ima

Nar

a K

um

amo

to O

ita

Fu

kush

ima

Ko

chi

Sag

a T

oku

shim

a F

uku

i N

agas

aki

Niig

ata

Sh

iga

Kag

awa

Yam

anas

hi

Ibar

aki

Oka

yam

a M

ie M

iyaz

aki

Gu

mm

a H

iro

shim

a F

uku

oka

Kan

agaw

a K

yoto

Ch

iba

Sh

izu

oka

To

chig

i S

aita

ma

Gif

u M

iyag

i W

akay

ama

Aic

hi

Ish

ikaw

a T

oky

oJa

pan

Fig.19: 10yr current bond yields by prefecure (%) vs 6m prior yields

Generic 10yr Yield - July 2016 Generic 10yr Yield - Jan 2017

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

42.4

37.

5

36.

736

.2

36.0

34.6

33

.5

33.0

32.9

32.

6

31

.4

31.2

30.6

30.2

30.1

29

.9

29.8

29.

4

29.

4

29.2

27.9

27.7

27.7

27.7

27.

6

27.4

27.3

26.

92

6.7

26

.6

26

.6

26.2

25

.3

25.2

24

.92

4.8

24.

3

24.0

22.9

22

.82

2.8

22.6

22.5

21.8

21.

7

21.6

19.5

19.5

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Oki

naw

a

Saga

Fuku

shim

a

Ao

mo

ri

Ku

mam

oto

Nag

asak

i

Miy

azak

i

Aki

ta

Iwat

e

Yam

agat

a

Ibar

aki

Kag

osh

ima

Oit

a

Shim

ane

Ko

chi

Tott

ori

Fuku

oka

Miy

agi

Wak

ayam

a

Ehim

e

Fuku

i

Ho

kkai

do

Gu

nm

a

Niig

ata

Oka

yam

a

Toch

igi

Yam

agu

chi

Toku

shim

a

Mie

Ish

ikaw

a

Yam

anas

hi

Shiz

uo

ka

Nat

ion

al A

vera

ge

Kag

awa

Hir

osh

ima

Gif

u

Nag

ano

Osa

ka

Toya

ma

Sait

ama

Ch

iba

Nar

a

Hyo

go

Aic

hi

Shig

a

Kyo

to

Toky

o

Kan

agaw

a

Fig. 20: % of Marriages as a result of unplanned pregnancy (shotgun wedding) - 2009

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

Page 14 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Akita skewed unsustainably

Source: Custom Products Research, Ministry of Health, Labor & Welfare (MHLW)

It is evident that Akita has too large a percentage of its populace in agriculture and with over one

quarter of workers in construction and manufacturing, the risk of depopulation should mean that

building projects (especially private sector) and manufacturing sustainability would be poor. Visits

several years back to companies such as Takeuchi (6432) and Hokuto (1379) in Nagano Pref have

highlighted the risks of losing employees and escalating wages to keep them. In Takeuchi’s case

line workers needed to have special qualifications to move its digging equipment which meant that

they had to hike wages double digit percentages to keep workers from moving out of Nagano. On

top of that it was actively hiring foreign labourers to address the looming shortfall. Akita will

undoubtedly face more acute problems.

Ag/Fishery MiningConstructi

onManufact

uringUtilities IT/Comm Transport

Wholesale/Retail

Financial/Insurance

RealEstate

ScienceRelated

Hotel/Bar/restaurant

DailyServices

EducationHealth/W

elfareCompound Services

Other

Aomori 1.63% 0.12% 10.34% 12.72% 0.42% 1.25% 6.16% 22.86% 2.98% 1.81% 2.19% 8.55% 5.37% 2.39% 13.52% 0.82% 7.16%

Akita 1.62% 0.12% 10.26% 16.95% 0.41% 0.93% 5.01% 21.24% 2.86% 1.41% 1.89% 8.35% 4.53% 2.22% 14.08% 1.22% 6.68%

Fukuoka 0.39% 0.03% 7.26% 11.68% 0.41% 2.67% 6.53% 22.34% 2.99% 2.62% 2.53% 9.70% 4.51% 3.31% 13.79% 0.46% 8.78%

Japan 0.64% 0.04% 6.94% 16.56% 0.36% 2.91% 5.91% 21.04% 2.85% 2.64% 2.98% 9.71% 4.56% 3.08% 11.07% 0.61% 8.10%

Kanagawa 0.19% 0.01% 6.41% 14.45% 0.25% 3.35% 6.17% 19.61% 2.05% 3.26% 4.54% 10.41% 4.84% 3.56% 12.04% 0.42% 8.42%

Tokyo 0.04% 0.01% 5.41% 8.17% 0.36% 9.09% 5.41% 22.18% 4.78% 3.97% 4.88% 9.84% 4.04% 3.72% 7.45% 0.23% 10.41%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Fig. 21: Employment sectors by prefecture as % of total (2012)

Aomori Akita Fukuoka Japan Kanagawa Tokyo

2.67%

0.64%

0.39%

0.06%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

Miy

azak

i

Iwat

e

Kag

osh

ima

Ho

kkai

do

Sh

iman

e

Ko

chi

Oit

a

Ao

mo

ri

Aki

ta

Niig

ata

Nag

ano

To

tto

ri

Nag

asak

i

Ku

mam

oto

Eh

ime

To

kush

ima

To

yam

a

Yam

agat

a

Sag

a

Yam

agu

chi

Kag

awa

Fu

kui

Ibar

aki

Fu

kush

ima

Mie

Gif

u

Ish

ikaw

a

Gu

mm

a

Hir

osh

ima

Wak

ayam

a

Miy

agi

To

chig

i

Sh

iga

Yam

anas

hi

Jap

an

Oka

yam

a

Oki

naw

a

Ch

iba

Sh

izu

oka

Fu

kuo

ka

Kyo

to

Hyo

go

Nar

a

Aic

hi

Sai

tam

a

Kan

agaw

a

Osa

ka

To

kyo

Fig. 22: Agriculture/Fisheries - Employment as a % of total by prefecture (2012)

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

Page 15 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

German reunification

Source: MHLW

It also brings to light the subject of the reunification of Germany in 1989. Workers in the former East

saw the employment opportunities in the West were far more lucrative and abandoned on masse

leading to large employment shortages and rising bankruptcies in the former communist bloc. The

situation became so acute that businesses in the East were forced to raise wages significantly to

stem the flow. Unfortunately, they were left with lower skilled workers and today unemployment rates

are much higher than the average because of the brain drain to the West.

While Japan faces this challenging demographic the plight of bankruptcy of towns from depopulation

will be exacerbated, Fig. 25.

10.34%

9.20%

7.26%6.94%

5.10%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

11.00%

Ao

mo

ri S

him

ane

Aki

ta N

iigat

a Iw

ate

Miy

agi

Fu

kush

ima

Yam

agat

a F

uku

i H

okk

aid

o O

ita

Yam

agu

chi

Ko

chi

To

yam

a T

ott

ori

Kag

osh

ima

Miy

azak

i S

aga

Ibar

aki

Nag

asak

i O

kin

awa

Wak

ayam

a N

agan

o Y

aman

ash

i E

him

e Is

hik

awa

Oka

yam

a K

um

amo

to C

hib

a T

oku

shim

a K

agaw

a F

uku

oka

Gif

u T

och

igi

Sai

tam

aJa

pan

Gu

mm

a H

iro

shim

a S

hiz

uo

ka K

anag

awa

Mie

Aic

hi

Sh

iga

Osa

ka H

yogo

To

kyo

Nar

a K

yoto

Fig.23: Construction - Employment as a % of total by prefecture (2012)

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

13.79%

9.71% 9.70%

8.24%

7.00%

8.00%

9.00%

10.00%

11.00%

12.00%

13.00%

14.00%

15.00%

Oki

naw

a Y

aman

ash

i K

yoto

Ko

chi

Ch

iba

Hyo

go N

ara

Nag

ano

Nag

asak

i K

anag

awa

Ish

ikaw

a H

okk

aid

o T

ott

ori

Miy

azak

i O

ita

Osa

ka G

ifu

To

kyo

Wak

ayam

a K

ago

shim

aJa

pan

Fu

kuo

ka K

um

amo

to A

ich

i S

hiz

uo

ka S

aita

ma

Mie

To

kush

ima

Sag

a T

och

igi

Eh

ime

Yam

agu

chi

Fu

kui

Sh

iga

Niig

ata

Kag

awa

Miy

agi

Sh

iman

e Y

amag

ata

Fu

kush

ima

Ao

mo

ri G

um

ma

Hir

osh

ima

Aki

ta Iw

ate

Oka

yam

a Ib

arak

i T

oya

ma

Fig.24: Hotel/Bar/Restaurant - Employment as a % of total by prefecture (2012)

Legend:Yellow -TohokuGrey - HokkaidoMauve - Shikoku/Kyushu/Japan SeaGreen - Fukuoka

Page 16 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Source: Custom Products Research, Japan Statistics Bureau, Ministry of Finance

126,193

91,933

42,860

27.5%

41.3%

25%

27%

29%

31%

33%

35%

37%

39%

41%

43%

30,000

50,000

70,000

90,000

110,000

130,000

150,000

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

2051

2052

2053

2054

2055

2060

2065

2070

2075

2080

2085

2090

2095

2100

2105

2110

Fig. 25: Japan's projected population ('000s) and the % of 65yo+ demographic

Population 65yo + (%)

60.2%

49.6%

45%

47%

49%

51%

53%

55%

57%

59%

61%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

2051

2052

2053

2054

2055

2060

2065

2070

2075

2080

2085

2090

2095

2100

2105

2110

Fig. 26: Japan's dwindling Labour Force ('000s)

Labour Force Labour force as % of total population

Page 17 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Economic plans are

unrealistic

Part-time growing

Employment agencies

Source: Japan Institute for Labour Policy & Training

Comparing Fig. 18 to Figs. 27-28 and we see why the plight of regions such as Akita and those

suffering demographic challenges will be crushed even with the government’s own optimistic ‘zero

growth’ and ‘economic revival’ scenarios. While much of these scenarios rely on productivity growth

the sad reality is that in the industrial areas Akita relies on now will see sharp declines of 10-40%

over the next 15 years. Hardly the most helpful stats to arrest further depopulation. What is worse is

that slowing activity only compounds on the downside.

Add to that the prospect of a higher incidence of part-time work and the ability for the elderly to trade

out of a terrifying retirement is worsened, meaning consumption is curtailed and pinching at the one

area that could help create jobs.

One dilemma in the data is the employment referrals by government unemployment agencies for

middle or advanced aged staff (45yo+) shows that around 25% of them end up with work in a fixed

term capacity of more than 4 months, Fig. 29. That is to say around 30,000 get placed per annum,

hardly a positive statistic. Perhaps the following statement explains part of the problem.

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%Fig. 27: The employment outlook on the 'economic revival' scenario (%)

Economic Revival (2020) Economic Revival (2030)

-60.0%

-50.0%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0% Fig. 28: The employment outlook on the 'zero growth' scenario (%)

Zero growth (2020) Zero growth (2030)

Page 18 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Inflexible workers

The dole shop

Impact of PT vs FT

Former Jobu University Professor and economist Nobuo Ikeda commented on the problems and

shortcomings of Japan’s lifetime employment system, “Salarymen, who are typically hired right out

of school in a batch . . . will start by learning (elementary skills) on the job. These include company

specific skills learned by watching more experienced workers, like personal skills, meaning they

aren’t useful in other companies…as companies rarely hire mid-career.”

Source: Statistics Bureau

In an interview with the government employment agency, Hello Work, in January 2016 the agency

noted the dilemma of dealing with Sharp’s voluntary redundancies. Of the 820 former Sharp workers

that registered with the Nara Prefecture agency, only 261 had found alternative employ. The biggest

issue is that 80% of those are over 50 years old and many have false expectations on their ‘real

value’ expecting the next job will pay similar salaries, benefits and title. Most still have housing loans

and education expenses outstanding.

Fig. 30 bears this out even better. The long running trend of full-time work in a regular capacity has

given way to a lot more part-time (lower paying) jobs which involves less other costs like insurance,

retirement and so on. This change puts pressure on the household budget.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Fig.29: Mid career introductions of unemployed persons (45yo+) and employment success ratio

Cases of Introduction Ratio of introductions where people found employment

Page 19 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Women in workforce

Employment quality falling

Save on wages

Source: Statistics Bureau

Fig. 31 shows that since 2003 more women are employed part time than full time. With PM Abe

looking to encourage more women back into the workforce to offset the declining (working)

population by expanding day-care centre places, job prospects will increasingly be part time.

Source: Statistics Bureau

What we can deduce is that the quality of employment is deteriorating. While the employment rate

in the recent decade has fallen contrary to1997-2003, the instance of lower paid part-time work has

grown since then from 30% to 37.4% of the total. For women, this is now 56%. If PM Abe wishes to

grow the economy, higher numbers of part-time workers will make the journey that much harder.

PM Abe has acknowledged that issue. This coming May he wishes to introduce a policy which

requires equal wages for full-time and contract hires. However, recruitment by firms will only be

marginalised should the law be introduced.

The Japanese Institute for Labour Policy & Training (JILPT) makes the case for employer’s reasons

to hire non-regular employees clear in Fig. 32. “To economise on wages” and “to economise on non-

labour costs” are the two highest categories.

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

Fig. 30: Full-time vs. Part-Time Trend as a % of total employees in Japan (%)

0

200

400

600

800

1000

1200

1400

1600

Fig. 31 : Full time vs Part-time Female Employees ('000 people)

Women Regular Employees Women Non-regular employees

Page 20 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Lack of Opportunities

Why females work part time

Fig. 32: Employer’s Reasons for Hiring non-regular employees (%)

Source: Japan Institute for Labour Policy & Training

While convenient work hours are a high factor for part-time workers note that “lack of regular

employment opportunities” is the most consistently high factor for male employees selecting non-

regular jobs, Fig. 33.

Fig. 33: Male Employee’s Reasons for selecting non-regular employment (%)

Source: Japan Institute for Labour Policy & Training

Female non-regular employees showed similar trends to that of men with regards to being unable

to secure regular employment, but “domestic reasons” (38%) was a high factor however 47% said

that “supplementing household income” was second to convenience in work hours (50.7%). In short

the labour market is preventing stable employment which adds to individual concerns.

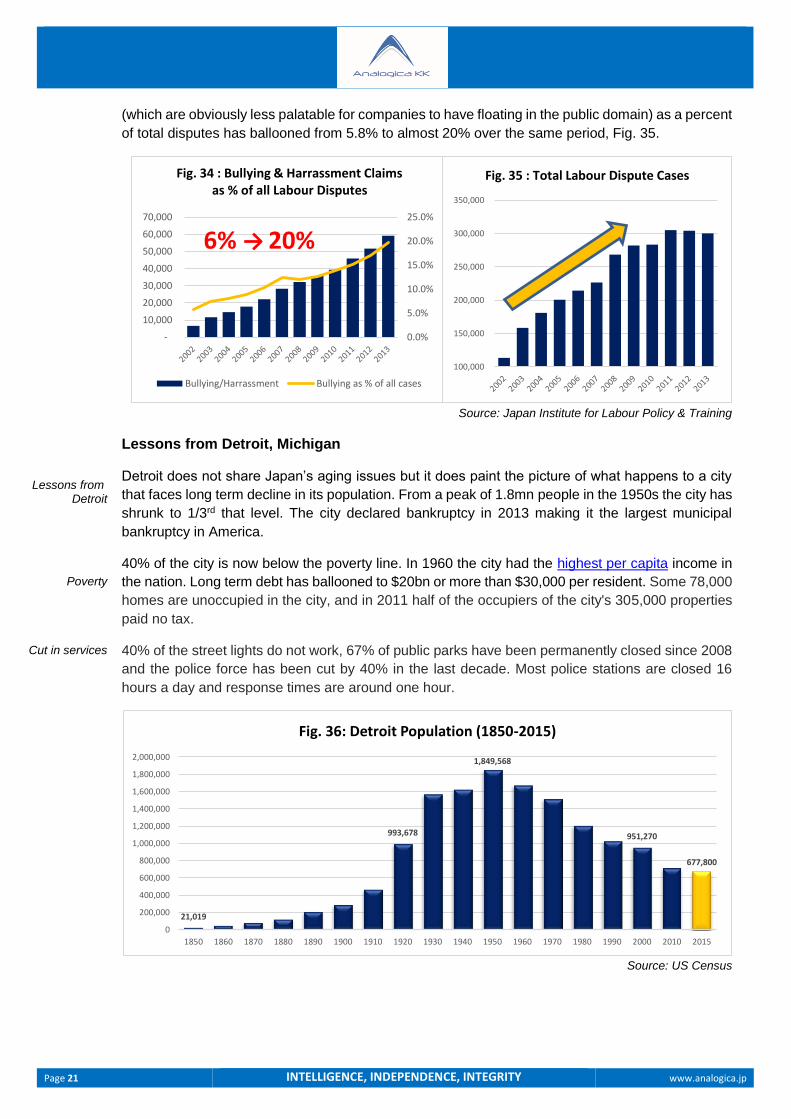

It is the smell of fear. Pressure to prevent losing one’s job is a factor in the steady increase in labour

disputes. Between 2002 and 2013, labour disputes almost trebled, Fig.34. Bullying and harassment

Page 21 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Lessons from Detroit

Poverty

Cut in services

(which are obviously less palatable for companies to have floating in the public domain) as a percent

of total disputes has ballooned from 5.8% to almost 20% over the same period, Fig. 35.

Source: Japan Institute for Labour Policy & Training

Lessons from Detroit, Michigan

Detroit does not share Japan’s aging issues but it does paint the picture of what happens to a city

that faces long term decline in its population. From a peak of 1.8mn people in the 1950s the city has

shrunk to 1/3rd that level. The city declared bankruptcy in 2013 making it the largest municipal

bankruptcy in America.

40% of the city is now below the poverty line. In 1960 the city had the highest per capita income in

the nation. Long term debt has ballooned to $20bn or more than $30,000 per resident. Some 78,000

homes are unoccupied in the city, and in 2011 half of the occupiers of the city's 305,000 properties

paid no tax.

40% of the street lights do not work, 67% of public parks have been permanently closed since 2008

and the police force has been cut by 40% in the last decade. Most police stations are closed 16

hours a day and response times are around one hour.

Source: US Census

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Fig. 34 : Bullying & Harrassment Claims as % of all Labour Disputes

Bullying/Harrassment Bullying as % of all cases

6% → 20%

100,000

150,000

200,000

250,000

300,000

350,000

Fig. 35 : Total Labour Dispute Cases

21,019

993,678

1,849,568

951,270

677,800

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

1850 1860 1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2015

Fig. 36: Detroit Population (1850-2015)

Page 22 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

America’s population is still

growing

Debt: GDP

Interest payments

While Japanese prefectures maybe depopulating a la Detroit, they lack the ability to recover even if

incentives are implemented as the American population continues to grow in numbers while Japan

shrinks. Detroit has shrunk 30% in the last 15 years. In Fig. 37, we note the number of towns that

have less than 5,000 people. Nara is home to 5 villages that have fallen 20% in the last 5 years.

While the scale is different, the rate of decline hits a certain point and heads into freefall most likely

as supermarkets, post offices, banks and petrol stations can’t justify serving such tiny markets.

Source: Custom Products Research, Japan Statistics Bureau

Is it really that bad?

Of course, it is easy to postulate that the plight of the regions is bleak. However, looking at pure

prefectural debt/GDP ratios it is not awful optically.

Source: Custom Products Research, Japan Statistics Bureau

Shimane has a prefectural debt: GDP ratio of 60%. It pays 16% of its tax intake on interest payments.

This is not the highest in Japan by any stretch but bond markets are fickle things. Sure, the Bank of

Japan can increase prefectural bond purchases to prevent the rate from going higher but the exodus

is not slowing. Shimane has lost 10% of its middle/high school pupils in the past 5 years. While some

85

28

16 15 13 128 8 8 7 7 6 6 5 5 5 5 4 4 4 4 4 3 3 3 2 2 2 2 2 1 1 1 1 1 1

0

10

20

30

40

50

60

70

80

90

Ho

kkai

do

Nag

ano

Oki

naw

a

Ko

chi

Nar

a

Fuku

shim

a

Ku

mam

oto

Ao

mo

ri

Toky

o

Gu

nm

a

Yam

anas

hi

Oka

yam

a

Wak

ayam

a

Miy

azak

i

Kag

osh

ima

Aki

ta

Niig

ata

Gif

u

Kyo

to

Shim

ane

Tott

ori

Toku

shim

a

Aic

hi

Iwat

e

Yam

agu

chi

Kag

awa

Yam

agat

a

Oit

a

Fuku

i

Fuku

oka

Ehim

e

Miy

agi

Sait

ama

Kan

agaw

a

Nag

asak

i

Toya

ma

Fig. 37: Towns in Japan with less than 5,000 people (2015) by Prefecture

60%

24%

0%

10%

20%

30%

40%

50%

60%

70%

Shim

ane

Aki

ta

Tott

ori

Ko

chi

Iwat

e

Ho

kkai

do

Toku

shim

a

Kag

osh

ima

Yam

agat

a

Yam

anas

hi

Miy

azak

i

Ao

mo

ri

Niig

ata

Fuku

i

Ish

ikaw

a

Toya

ma

Wak

ayam

a

Nag

asak

i

Oit

a

Saga

Nar

a

Ku

mam

oto

Yam

agu

chi

Kag

awa

Ehim

e

Hyo

go

Nag

ano

Fuku

shim

a

Gif

u

Oka

yam

a

Miy

agi

Mie

Hir

osh

ima

Kyo

to

Shig

a

Fuku

oka

Ibar

aki

Shiz

uo

ka

Oki

naw

a

Osa

ka

Gu

nm

a

Aic

hi

Toch

igi

Sait

ama

Ch

iba

Kan

agaw

a

Toky

o

Fig. 38: Prefectural Debt/Prefectural GDP (%) - 2014

Page 23 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

When it goes pear shaped

Lacking assets in Regions

How they derive tax

Future Burden Ratio

may have graduated, it would be safe to assume they are relocating to other prefectures with their

working age parent(s).

Were we to see a similar exodus from Shimane as has happened in Detroit (or Yubari for that matter)

debt/working person would grow to $33,000. Shimane’s 16% debt servicing ratio would likely head

north of 30% of annual tax revenue even when conservatively estimating refinancing rates and lower

tax revenue intake. Moreover debt: GDP would balloon because relative GDP would decline as well

putting upward pressure on effective future borrowing costs. Within the prefectures, smaller villages

and towns may head the way of Yubari and suddenly bad debt could spill over into a domino effect.

Recall Yubari’s tax collections are only one-quarter of what they were two decades ago so in the

more acutely aging areas, we could well see assumptions on a prefecture like Shimane over the

long term become unsustainable.

Therein lies the problem. The debt is not likely to change much yet the revenue side of the ledger

will continue to slide. Of course, the ¥200 trillion of prefectural/municipal debt (relatively unchanged

for a decade) pales in comparison to the national debt of ¥840 trillion. Yet many of the regions do

not possess the same level of asset creation that can reduce the net burden.

34% of tax revenues by prefectures derives from resident’s tax and 42% of municipalities fill their

coffers by fixed asset taxes, Figs. 39-40. If tax payers migrate to new prefectures they not only hit

the prefecture revenue collection (note you need to be resident on Dec 31st to have to pay residents

tax. If you move to another prefecture between Jan 1-Dec 30th the residents tax is paid to your new

place of residence. If more people look to leave depopulating regions, then the natural impact on

fixed assets will fall in lockstep.

Source: Ministry of Finance

As the JLGBA and Ministry of Finance note it is considered to be dangerous waters if the future

burden ratio (FBR) exceeds 400% in prefectural governments and 350% in the municipalities. As

we mentioned earlier, Yubari’s tax revenues fell 75% in two decades. Hokkaido would only need to

have a 20.7% fall in tax revenues to trigger the 400%.Akita would require just under 40% cut in tax

revenues.

Individual Residents Tax, 34%

Local Consumption

Tax, 18%Automobile

Tax, 10%

Others, 14%

Corporate Enterprise Tax, 18%

Corporate Residents Tax, 6%

Fig. 39: Prefectures Tax Revenue

Fixed Asset Tax, 42%

Individual Residents Tax, 34%

City Planning Tax, 6%

Others, 8%

Corporate Residents Tax, 10%

Fig. 40: Municipalities Tax Revenue

Page 24 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Rescue Plan

Who pays tax?

Source: Custom Products Research, Japan Statistics Bureau, Ministry of Finance

What did Yubari do?

To be fair, Yubari became a pilot case for how to handle a bankruptcy. In the FY2009-2029 Financial

Rebuilding Plan, public officials would be cut from 269 in FY2006 to 134 in FY2009 to 103 by

FY2010. Standard salaries for public servants would be cut 30% and subsidies would be trimmed

40%. The tax rate on fixed income was lifted to 1.45% from 1.4% and municipal income tax from 6%

to 6.5%. Services such as garbage collection are separate charges. Yubari City issued a ¥32.2bn

special deficit covering bond. Yubari’s real debt repayment ratio is ranging between 80-90% of tax

revenue per year until 2026.

The bigger issue will be what might happen if a string of Yubari’s come under similar bankruptcy

proceedings.

What should Japan do?

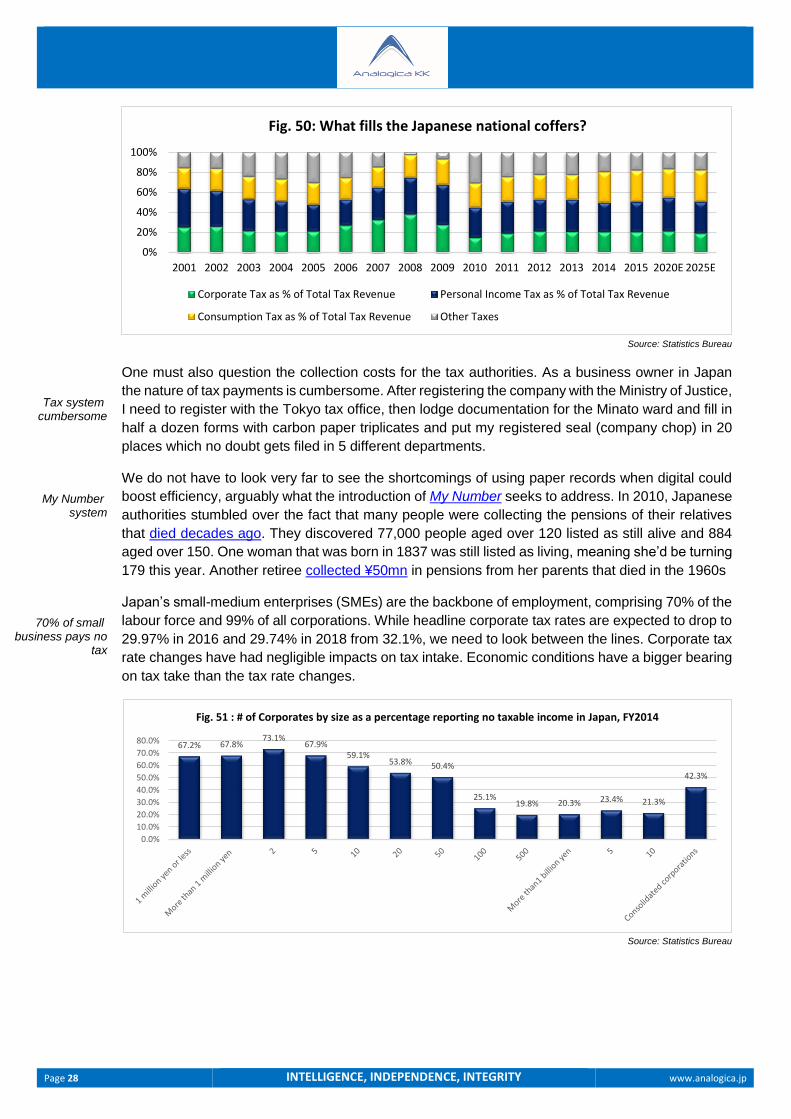

In Japan, 97% of the income tax burden is borne by the top 47% of earners. Over two-thirds of

Japanese SMEs (corporations capitalised under ¥100mn) pay no tax. While the government has

progressively eased the corporate tax rate from north of 50% in the 1990s to just over 40% during

most of the 2000s to under 30% by 2018 companies have avoided chipping in to the national coffers.

Fig.1 shows clearly that despite corporate tax rates coming down, the impact on the number of

corporates reporting losses to the tax office remains largely unchanged.

Source: Custom Products Research

16.8%

20.7%

39.7%

55.7%

73.2%

87.6%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Hyo

go

Ho

kkai

do

Niig

ata

Toya

ma

Kyo

to

Fuku

oka

Hir

osh

ima

Aki

ta

Ibar

aki

Iwat

e

Yam

agat

a

Shiz

uo

ka

Kag

osh

ima

Ish

ikaw

a

Yam

agu

chi

Yam

anas

hi

Aic

hi

Osa

ka

Sait

ama

Oka

yam

a

Shig

a

Gif

u

Ku

mam

oto

Kag

awa

Mie

Wak

ayam

a

Toku

shim

a

Miy

agi

Jap

an

Nag

asak

i

Nag

ano

Shim

ane

Fuku

i

Nar

a

Oit

a

Ch

iba

Gu

mm

a

Ko

chi

Ehim

e

Ao

mo

ri

Kan

agaw

a

Fuku

shim

a

Miy

azak

i

Saga

Tott

ori

Toch

igi

Oki

naw

a

Toky

o

Fig. 41: % fall in Prefectural Tax Revenue required to trigger 400% danger level FBR

69.6% 69.2% 69.4% 69.9%69.5% 68.8% 68.4% 67.8% 68.0%

71.1% 72.6%67.9%

37.0%

38.0%

39.0%

40.0%

41.0%

42.0%

43.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2013

Fig. 42 : Do Corporate Tax Rates really influence Corporate Behaviour?

Total # of Corporates Filing Losses (LHS) Corporate Tax Rate (%) RHS

GFC GFC

Page 25 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp

Poland’s plan

Japan drip feeds tax cuts

Japan & Poland demographics

similar

Poland faced similar issues but in 2004 introduced sensible taxation reform which lured long term

tax avoiders/evaders from their lairs. Authorities introduced a flat business tax (19%) and its impacts

were so favourable that the government saw a 50% increase in income reported by those corporates

in higher tax brackets before the change and a 50% increase in reported income from individuals

that fell into upper income tax brackets. In 2009 income tax rates at the top were slashed from 40%

from 32% Despite this income tax receipts jumped 17%. Since 2004 tax receipts soared 56.4%. It

clearly proved that lowering taxes created much higher tax compliance. There was a psychological

factor at play – the cut ‘encouraged’ honesty.

Japan on the other hand continues to drip feed corporate tax cuts at such slow rates that there is

little perceivable reason to change behaviour. Instead of burying the dwindling number of diligent

tax payers ever more Japan must reform its tax code. We estimate a flat tax with similar outcomes

to what Poland experienced would shrink the annual budget deficit by two thirds.