making great food affordable - corporate - morrisons annual report... · making great food...

TRANSCRIPT

Annual report and financial statements 2011/12

Wm Morrison Supermarkets PLC

Making great food affordable

Introduction What matters to us

Business and strategy review Wm Morrison Supermarkets PLC

About us

We are the UK’s fourth largest food retailer by sales, with an annual turnover in excess of £17bn. We have 475 stores across Britain, ranging in size from 3,000 to over 40,000 square feet. Over 11 million customers visit our stores each week, served by more than 131,000 employees.

Our business

Our strategy

Our financial performance

We are proud of what makes us different – a distinctive offer to customers centred around fresh food, craft skills and food production through our manufacturing business; the way we lead and support our colleagues; and our unique heritage. It is our vision to be ‘Different and Better than Ever’, being ‘different’ means building on these advantages; and being ‘better than ever’ is about improving the way we do business.

Chief Executive’s business and strategy review — page 4

We have developed a strategy based on our view of how the market will evolve, what will be most appealing to our customers and how we make best use of our internal capabilities. Our strategy is based on six convictions (outlined on page 7), and we have a clearly defined set of initiatives that will deliver our strategy grouped by our objectives of ‘driving topline’, ‘increasing efficiency’ and ‘capturing growth’.

Our strategic objectives — page 12

Our financial performance in 2011/12 was strong in what remains a challenging environment for the consumer. We continued to invest in the long term growth of the business and to deliver increasing returns to shareholders, whilst maintaining a strong balance sheet. The business is well placed to deliver sustainable long term growth.

Group Finance Director’s financial review — page 8

Financial performanceGroup turnover

£17.7bn up 7%

Like-for-like sales (ex-fuel, ex-VAT)

1.8%

Profit before tax

£947m up 8%

Basic earnings per share

26.7p up 11%

Net debt

£1,471mTotal dividend per share

10.7p up 11%

Note: Throughout the Directors’ report and business review(1) Unless otherwise stated, 2011/12 refers to

the 52 week period ended 29 January 2012 and 2010/11 refers to the 52 week period ended 30 January 2011. 2011 and 2012 refer to calendar years.

(2) Underlying profit is defined as profit before one off costs and credits, property transactions and IAS19 pension interest, as reconciled in note 1 of the Group financial statements.

1Annual report and financial statements 2011/12

What’s in our report

Richard PennycookOur strong financial performance positions us well for sustainable long term growth.

Page 8

Sir Ian GibsonWe are committed to making food shopping fresh, friendly and affordable.

Page 2

Johanna WaterousA strong performance culture, long term shareholder value and competitive positioning remain key principles.

Page 46

Dalton PhilipsA clear strategy is in place that is delivering our objectives.

Page 4

Investor relations websitewww.morrisons.co.uk/corporate

Corporate responsibility review 2011/12

Also see...

Features Directors’ report and business review

Introduction2 Chairman’s statement

Business and strategy review4 Chief Executive’s business and strategy review8 Group Finance Director’s financial review12 Our strategic objectives

Performance review26 Key performance indicators28 Risks and uncertainties30 Corporate responsibility33 Our people

Governance36 Board of Directors and Management Board40 Corporate governance report46 Directors’ remuneration report56 General information59 Statement of Directors’ responsibilities

Financial statements

60 Group financial statements 60 Independent auditor’s report 61 Consolidated statement

of comprehensive income 62 Consolidated balance sheet 63 Consolidated cash flow statement 64 Consolidated statement of changes in equity 65 Group accounting policies 70 Notes to the Group financial statements

95 Company financial statements 95 Company balance sheet 96 Company accounting policies 99 Notes to the Company financial statements

Investor information108 Five year summary of results109 Supplementary information110 Investor relations and financial calendar

Annual review2011/12

2 Wm Morrison Supermarkets PLCBusiness and strategy review

Chairman’s statementIntroduction from the Chairman

Sir Ian GibsonChairman

Against the backdrop of a very challenging environment for the consumer, where value, freshness and quality are key, I am pleased to report another year of good progress for Morrisons.

Record numbers of customers visited our stores, demonstrating that Morrisons unique offer is in tune with the needs of consumers in these uncertain times. The delivery of good earnings growth and the resultant increase in the dividend demonstrates resilience of our business model in a tough economic environment.

Group highlightsUnderlying profit before tax

£935mUnderlying earnings per share

25.6pFinal dividend per share

7.53pProfit share pool for colleagues

£49mRaised for Save the Children charity

£2.3m

See our reportvisit: www.morrisons.co.uk/corporate/ar2012

3Annual report and financial statements 2011/12

At the start of the year, we outlined a range of initiatives to grow our sales profitability, make our business more efficient and develop further growth opportunities that would deliver enhanced value to shareholders. The management team has made good progress in all these areas and we are on track to deliver our vision to make Morrisons ‘Different and Better than Ever’.

ResultsProfit before tax was £947m, an increase of £73m (8%) when compared with £874m last year. Underlying profit before tax, which we regard as the true measure of business performance, was up 8% to £935m. Statutory basic earnings per share increased by 11% over the previous year to 26.7p, with underlying basic earnings per share up by 11% to 25.6p.

Our policy is to increase the dividend in line with underlying earnings growth subject to a minimum increase of 10% in each of the three years to 2013/14. In line with this policy, the Board is therefore recommending a final dividend of 7.53p per share, to bring the total dividend for the year to 10.7p, an increase of 11% on 2010/11. The dividend is covered 2.4 times by underlying earnings.

Cash flow from operations of £1,264m was up by £123m (11%), when compared to the previous year. Capital expenditure and investments of £901m was £306m higher than the previous year. This was the result of a planned acceleration in our store opening programme, the addition of a new regional distribution centre at Willow Green, Bridgwater, and investments to support our expansion ambitions for online shopping and vertical integration. We expect capital expenditure to be higher in 2012/13 as we continue to invest for future growth. £368m was invested into our equity retirement programme, and we are on track to meet our objective of returning £1bn to shareholders over the two years to March 2013, in addition to normal dividends.

These investments, together with an increased dividend payment, resulted in a rise in net debt to £1,471m (2010/11: £817m), to leave gearing at 27%. At this level it remains low for the sector. At the year end the Group had undrawn, committed facilities of £725m and a credit rating of A3 from Moody’s. This is a strong investment grade which is only held by two other European retailers.

Community and the environmentOur customers expect us to trade responsibly, and we are committed to managing resources carefully, maintaining ethical standards and working with the communities in which

we operate. During the year, we have continued to undertake research projects through the Morrisons Farming Programme, have been enthusiastic supporters of the Government’s Public Health Responsibility Deal and have made good progress towards our long term energy reduction targets. Our Let’s Grow programme, now in its fifth year, continues to help school children throughout the UK to get out of the classroom and learn about the food cycle first hand.

It is a source of pride that our colleagues and customers always go out of their way to support our charitable activities, and I am delighted that Save the Children was selected by our colleagues, for the second successive year, as our charity partner. Specifically, we have helped fund its award-winning Families and Schools Together (FAST) programme across the UK, which is designed to give the most disadvantaged children a chance of a better future. With an array of fundraising activities, we have raised £2.3m for FAST this year, successfully funding 24 programmes, as well as Save the Children’s emergency appeals in Japan and East Africa.

Industry recognitionMorrisons commitment to providing customers with an outstanding shopping experience and making it a great place to work for colleagues has again been recognised with numerous industry awards. These included nine The Grocer Own Label Food and Drink Awards, Fresh Produce Retailer of The Year (multiple category) at the Retail Industry Awards and Employer of the Year from both Retail Week and The Grocer Gold Awards.

Our colleaguesThese awards are testimony to the passion and hard work of our 131,000 colleagues, who are making Morrisons ‘Different and Better than Ever’ for our customers every day.

I am delighted that our growth during the year will provide a profit share pool for them of £49m, an increase of 8% over last year.

We continue to invest in training and skills. Our award-winning Morrisons Academy provides specialist training to help colleagues develop new skills or work towards a nationally recognised qualification such as QCF. Over 100,000 colleagues were successfully accredited during the year and, at the time of rising youth unemployment, I am pleased that 40,000 of our colleagues are aged 16 to 24.

On behalf of the Board, I want to express our thanks to every one of our colleagues for their dedication, professionalism and service throughout the year.

We are committed to making food shopping fresh,

friendly and affordableIt underpins our unique promise to every single household in the UK – the best service and the freshest food for less.

Business and strategy review

Perform

ance review

Governance

Financial statements

Investor information

4 Wm Morrison Supermarkets PLCBusiness and strategy review

This has been Morrisons best year yet, with another good financial performance and growth ahead of the market. Customers were having a tough time, but we responded with a new M savers brand for budget conscious shoppers, promotions that customers understood, and industry leading service.

We know that 2012 will be tough, and we will be working hard to deliver even better value for our customers. At the same time, we have ambitious plans for the long term development of the business, through new supermarkets, convenience stores and the development of our multi-channel capabilities.

Chief Executive’s business and strategy review

Operational highlightsCustomer numbers

up 0.4m per week

Market share

12.8%*

Stores opened (including one replacement)

37Gross profit

£1,217m up 6%

Average basket spend

£22.67

*Source: Kantar Worldpanel◆Source: ONS/Economic & Fiscal Outlook, OBR, November 2011

Dalton PhilipsChief Executive

Our strategic objectivesPage 12

How our KPIs link to our strategyPage 26

See our reportvisit: www.morrisons.co.uk/corporate/ar2012

5Annual report and financial statements 2011/12

Turnover analysis

Like-for-like stores

Othersales

2011/12Total

2010/11Total

In-store (£m) 13,112 324 13,436 12,937Fuel (£m) 4,009 30 4,039 3,426Other sales (£m) – 188 188 116Total turnover (ex-VAT) (£m) 17,121 542 17,663 16,479In-store salesSales per square foot (£) 21.05 12.83 20.74 20.80Customer numbers per week (m) 11.0 0.4 11.4 11.0Customer spend (£) 22.82 17.69 22.67 22.67

Business and strategy review2011/12 was another good year for Morrisons. Against the backdrop of a difficult environment for the consumer, our unique fresh, quality and value offer made Morrisons a natural destination and more customers visited our stores than ever before. We continued to improve our financial performance whilst investing for future growth.

Turnover growthTotal turnover was £17.7bn, an increase of £1.2bn (7%). Our store sales (excluding fuel) grew by 3.9% to £13.4bn, with a record 11.4m customers coming into our stores each week. Sales from new stores contributed 2.1% of our total growth. Like-for-like sales grew by 1.8%, customer numbers were up by 1.3% and average basket spend up 0.6%. Whilst sales growth was strongest in London and the South East, we were pleased with our sales performance in all regions of the country.

For the second year in a row, consumers were faced with increases in the price of oil, exacerbated by ongoing Sterling weaknesses. With unleaded prices at the pump up by 15.4p per litre and diesel increasing by 18.5p, motorists were paying an average of 15% more per litre at the pump than they did last year. The demand for fuel is relatively inelastic and, whilst motorists continue to use their cars in times of austerity, they take time to shop around for the best deals, such as our ‘Fuel Brittania’ programmes. As a result, our volume sales increased by 4.8%. Overall, like-for-like fuel sales were up 18% in the year.

Inflationary effects took their toll on disposable incomes during the year, with the unwelcome impact of high oil prices feeding through, not just at the petrol pumps, but also throughout the supply chain. Other core commodities increased in price too, adding to the pressure. Market prices for beef and lamb rose by 15% and 11% respectively over the year, and average wheat prices were up by 32%.◆ The increase in fuel prices alone reduced our customers’ disposable income by some £600m, income that could otherwise have been spent in our stores. In this environment, consumers looked around for value and found it at Morrisons, where our sharp pricing, supported by innovative promotions, was welcomed by customers.

We maintain a prudent approach to adding new space to our estate and only approve investments that meet the required financial hurdle rate. As a result, our space opening programme, whilst being ahead of our published targets, was less, in relative terms, than our major competitors. Despite this, with good like-for-like sales, we maintained our market share.*

Throughout the year, we noted the rise of the ‘professional shopper’, with customers taking time to shop around and look very carefully at pricing and offers in order to search out value. This trend played to Morrisons strengths. Our value proposition of everyday low prices, coupled with industry leading offers, and the flexibility of our vertical integration enabled us to meet our customers’ need for great fresh food at affordable prices. Offers such as our 49p produce deal and our two loaves of bread for £1 promotion helped our customers manage on tight budgets. The market remained highly promotional, and our innovative promotions such as ‘Pay Day Price Crunch’ and ‘Morrisons Millions’ really caught the mood of the nation.

A clear strategy is in place that is delivering our objectives

The strategy we have pursued, and the investment choices we have made, have set our business up to produce sustainable rates of growth.

Business and strategy review

Perform

ance review

Governance

Financial statements

Investor information

6 Wm Morrison Supermarkets PLCBusiness and strategy review

Chief Executive’s business and strategy review – continued

Operating results

Summary income statement2011/12

£m2010/11

£mChange

%

Turnover 17,663 16,479 7Gross profit 1,217 1,148 6Gross profit margin 6.9% 7.0% (0.1)Other operating income 86 80 8Administrative expenses (329) (323) 2Underlying operating profit 974 905 8Property transactions (1) (1) –Operating profit 973 904 8Operating profit margin 5.5% 5.5% –Net finance charges (26) (30) (13)Taxation (257) (242) 6Profit for the period 690 632 9

Gross profit grew by 6% to £1,217m during the year. The gross profit margin was 6.9%, a fall of 10bps against last year due to the increased proportion of low margin fuel sales in the mix this year. After cost of goods sold, the Group’s two largest cost areas are store wages and distribution costs. We continued to manage costs and improve efficiency in both areas whilst maintaining excellent standards and customer service levels. As a result, we again improved our store labour costs relative to sales, with in-store labour productivity up by 2.9%. Distribution productivity improved by 4.3%, reflecting the benefits of the investment we have made in systems improvement.

Other operating income grew by 8% to £86m, primarily because of increased recycling credits.

Administrative expenses increased by 2%, well below the rate of profit and sales growth in the year. This reflects the strong cost control culture that exists throughout the business.

Although the operating margin of 5.5% was in line with the prior year’s, the underlying result was an improvement of 20bps, after adjusting for the increased proportion of low margin fuel sales.

Market overviewThe UK grocery market continues to operate in a very tough economic climate, with consumer confidence close to record lows during the year. In 2011, the market was worth £97bn, up by 4.2% on the previous year.* Whilst this appears to be solid growth, it should be noted that space growth was approximately 4%, a historically high figure. Within these figures, online grocery grew disproportionately, with 17% of UK adults buying food or groceries online, up from 10% three years ago. The convenience market, which is measured separately, grew 4.6% to £34bn in 2011, and is expected to continue growing at a faster rate than the traditional grocery market for some time to come.♠

Retail grocery volumes were flat in the year and it was inflation, averaging 5.5% through the year, which drove growth. CPI food inflation, as measured by the Office of National Statistics, was above 6% for much of the year but started to come down through the last quarter, reaching 3.4% in January 2012. Categories that saw particularly high inflation include oils and fats (10%), coffee and tea (10%), and meat (6%).◆

Value at the forefront of shoppers’ mindsHousehold incomes were squeezed throughout 2011, due to the previously mentioned commodity and energy price pressures, and also as a result of the Government’s fiscal measures, particularly the rise in VAT to 20%. Cost pressures ran well ahead of wage settlements, with the result that disposable incomes overall fell 2.3% in 2011. A general unease about current and future expectations for the economy and for personal finances also saw shoppers managing more closely to a budget.

As a result, pricing and overall value have become increasingly important factors in purchasing decisions. More shoppers now regard price as their first consideration when choosing between products, compared with a year ago, with almost seven out of ten now saying they make the majority of their grocery shopping decisions before they get to store. This is an increase of 40% since 2008. Promotions are increasingly important when shoppers are deciding which stores to shop at and what products to buy. 70% of shoppers say promotions play a very important role in determining which stores they shop in, compared to 64% of shoppers in December 2010.▲ The grocery retail market has responded to these customer needs through an increased weight of promotional activity on branded goods. Additionally, retailer own brand sales, which carry a lower average unit price, have been performing more strongly than branded products as shoppers look for ways to manage their expenditure.

♠ Source: IGD ▲ Source: IGD ShopperVista *Source: Kantar Worldpanel◆Source: ONS/Economic & Fiscal Outlook, OBR, November 2011

7Annual report and financial statements 2011/12

AboveFresh food with exceptional customer service is helping us be better than ever.

StrategyIn 2010, we outlined our vision to make Morrisons ‘Different and Better than Ever’. We are proud of what makes us different – a distinctive offer to customers centred around fresh food, craft skills and vertical integration through our manufacturing business; the way we lead and support our colleagues; and our unique heritage. Being ‘different’ means building on these advantages, which set us apart from all our competitors and position us to win. Being ‘better than ever’ is about improving the way we do business – doing more of the things that matter for our customers – making great food, offering outstanding service and being more efficient so we can pass on the best savings possible. It also means seizing opportunities to grow the business profitably through new formats, channels and categories, to meet more of our existing customers’ needs and to reach new customers.

Our strategy reflects our view of how the market will evolve, what will be most appealing to our customers and how we make best use of our internal capabilities. It is based on six convictions about the type of business that our customers want us to be.

1 — Food focused not generalist

We want to be the number one destination in the UK for fresh food at outstanding value for money. Fresh food is at the heart of the supermarket shopping experience and customers are seeking freshness, quality and provenance at great value as well as becoming more conscious about healthy eating.

Our manufacturing capabilities, unique craft skills, in-store food preparation, flexible supply chain and farming links all give us competitive advantage. We will continue to build on these to create a unique shopping experience offering customers the best fresh food in the UK, unrivalled value for money and fantastic service.

2 — Experiential over purely functional

Customers are seeking a deeper engagement with food and food shopping and moving away from a purely functional experience. They want to see, touch and smell the food. We want it to look different and feel different when customers shop at Morrisons.

3 — Value is forever

The world is changing but some things are for ever – value is one of them. This means offering an experience which is ‘fun and frugal’ through a combination of great range, quality and service, combined with great prices on everyday products and industry leading deals. We are already well known for delivering great value and we will keep this at the heart of our offer.

4 — Skills not just drills

Our great store colleagues are a competitive advantage we can build on. Customer experience is driven by friendly, knowledgeable service delivered through a skilled and engaged workforce who are all committed to offering customers a fantastic shopping experience.

5 — General merchandise – clicks not bricks

General merchandise is increasingly migrating online, and always from ‘big box’ supermarkets and the traditional high street. We believe therefore that the future for general merchandise is in ‘clicks not bricks’.

6 — Multi-format, multi-channel

We will serve the evolving needs of our customers by expanding into new channels and formats, tailoring our offer to suit the needs of different customers.

Better technology and busy lifestyles are changing the way customers shop. Different customers in different locations want different products. They shop using different channels, going online, via kiosks and on their smartphones, and also visit different formats, doing their weekly shop in larger stores, topping up in convenience stores and seeking out specific products or expertise in speciality stores. To serve more customers, more of the time, we need to be multi-format and multi-channel, tailoring our offer to suit the needs of different customers.

We have developed a clear set of strategic objectives to deliver our vision and strategy, these along with our 2011/12 initiatives are set out on page 12. KPIs and the risks to achieving our vision are set out on pages 26 to 29.

Business and strategy review

Perform

ance review

Governance

Financial statements

Investor information

8 Wm Morrison Supermarkets PLCBusiness and strategy review

Financial review

Group highlightsCash generated from operations

£1,264mGearing

27%

Capital investment, including capital expenditure, investments and acquisitions

£901mOur credit rating

A3Investment in equity retirement programme

£368m

Morrisons financial performance was strong, in what remains a challenging environment for the consumer. We continued to invest in the long term growth of the business and to deliver increasing returns to shareholders, whilst maintaining a strong balance sheet. The business is well placed to deliver sustainable long term growth.

The Group’s financial strategy continues to be to deliver improved margins, whilst positioning for long term growth.

Richard PennycookGroup Finance Director

Our risks and uncertaintiesPage 28

Our Group financial statementsPage 61

See our reportvisit: www.morrisons.co.uk/corporate/ar2012

Financial strategy The underlying principles behind this strategy are:

growing sales ahead of market; delivering earnings that meet the expectations of shareholders; and

maintaining a strong investment grade balance sheet.

We are meeting these principles by: increasing our customer appeal and growing sales organically and opening new stores;

converting sales growth into profitable growth; and investing to yield an appropriate rate of return.

9Annual report and financial statements 2011/12

Interest and taxInterestNet interest paid of £49m was slightly higher than prior year (2010/11: £47m), reflecting a higher average level of net debt during the year. The Group’s effective interest rate of 4.0% was in line with prior year. Interest was covered 37 times (2010/11: 30 times). Excluding net pension interest income, interest was covered 25 times (2010/11: 25 times).

TaxCorporation tax paid in the year was £281m. This cash outflow represented 50% of the total tax bill for the year to 30 January 2011, and 50% of the tax for the year to 29 January 2012.

The effective tax rate for the year was 27.1% (2010/11: 27.7%), which is slightly above the prevailing corporation tax rate of 26%. A combination of non-qualifying depreciation, and expenses for which the Group is unable to obtain a tax deduction for, increases our tax rate above the prevailing rate. Offsetting this, the change in corporation tax rate to 26% from 28% had the effect of reducing the rate compared to the prior year.

Our in-house tax department’s primary focus is on ensuring that the Group continues to pay the appropriate level of tax at the right time. The Group, which is predominantly UK based, operates a simple business model. We aim to be transparent in all our activities, and we do not engage in sophisticated tax planning structures.

Capital expenditureThe Group continues to invest in the infrastructure to support our long term growth. This includes building new stores, the ongoing replacement of our IT systems and the strengthening of our supply chain. Total capital expenditure of £796m during the period included £330m for the planned acceleration of our new store space and the enhancement of our existing estate, £54m for the ongoing development of our IT infrastructure and £59m for the completion of a new RDC for the South West, at Bridgwater.

During the period, we opened a further 37 new stores, of which one was a replacement and three were our new M local convenience format. We also improved our estate through the acquisition of new sites to support our planned future growth, the extension of 15 stores and the refurbishment of the first seven stores to incorporate our new fresh foods concepts. Overall, our net selling space increased by 5.2% during the year.

At 30 Jan2011

Newstores1

Storeextensions

At 29 Jan

2012

Number of core stores

439 33 15 472

Number of convenience stores

– 3 – 3

Total number of stores

439 36 152 475

Total area in square feet (‘000)

12,261 536 107 12,904

Number of petrol filling stations

296 4 – 300

1 Net of replacements.2 Number of store extensions is included in total number of stores.

The Business and strategy review on page 4 contains information about the Group’s financial performance for the year, in particular turnover growth, like-for-like sales growth and operating profit. The review also contains information on selling space increases and our future space expansion programme.

Underlying profit is the measure we use to assess normal underlying business performance and trends. Earnings are adjusted to remove volatile or one-off costs and credits. A reconciliation of underlying profit is provided in note 1 of the Group financial statements.

Summary cash flow

2011/12£m

2010/11£m

Cash generated from operations 1,264 1,141Tax, interest and servicing of finance (330) (238)Capital expenditure (796) (592)Proceeds from sale of plant, property and equipment

4 8

Acquisitions (including debt acquired)

(74) (7)

Investments (31) –Dividends paid (301) (220)Equity (retirement)/issues (368) 16Net cash (outflow)/inflow (632) 108Non-cash movements (22) (1)Opening net debt (817) (924)Closing net debt (1,471) (817)

In line with our planning assumptions, we saw a net cash outflow during the period.

Cash generated from operationsCash from operating activities increased by £123m as a result of the overall increase in profits, which was partly offset by an increase in working capital. During the year, stocks increased by £117m, reflecting our overall sales growth, as well as the acquisition of Kiddicare and the addition of our new regional distribtuion centre (RDC) at Willow Green, Bridgwater.

Our performance against this financial strategy was: sales growth ahead of the market in the year of 0.5%*; underlying EPS of 25.6p, an increase over the prior year of 11%; and

the Group’s balance sheet continues to reflect our strong financial position:

– 90% of our estate is freehold; – we maintain low levels of gearing; – we use prudent assumptions to value our defined

benefit pension schemes; and – adequate and balanced long term financing facilities

are in place to cover our planned investments.

*Source: Kantar Worldpanel

Business and strategy review

Perform

ance review

Governance

Financial statements

Investor information

10 Wm Morrison Supermarkets PLCBusiness and strategy review

In November 2011, we concluded a US private placement with Metropolitan Life Insurance of America Inc. This provided the Group with $250m of committed funding through to November 2026, and was swapped into Sterling at a fixed interest rate for the duration of the term.

In December 2011, the Group issued a 12 year Sterling bond to institutional investors, which provided £400m of funding through to December 2023.

The Group ended the year with a well diversified and mature funding base.

GearingAs anticipated, our gearing ratio increased slightly during the year, but at 27% (2010/11: 15%), it is still well below our sector average. The continuing strength of our balance sheet has been recognised by Moody’s, a leading credit ratings agency, who has confirmed an investment grade A3 rating. We continue to be one of only three European retailers to have this strong rating.

Pensions The Group sponsors two defined benefit pension arrangements and both of these pension schemes are managed externally to, and independently of, the Group’s operations. Our approach to valuing our defined benefit pension obligations remains prudent.

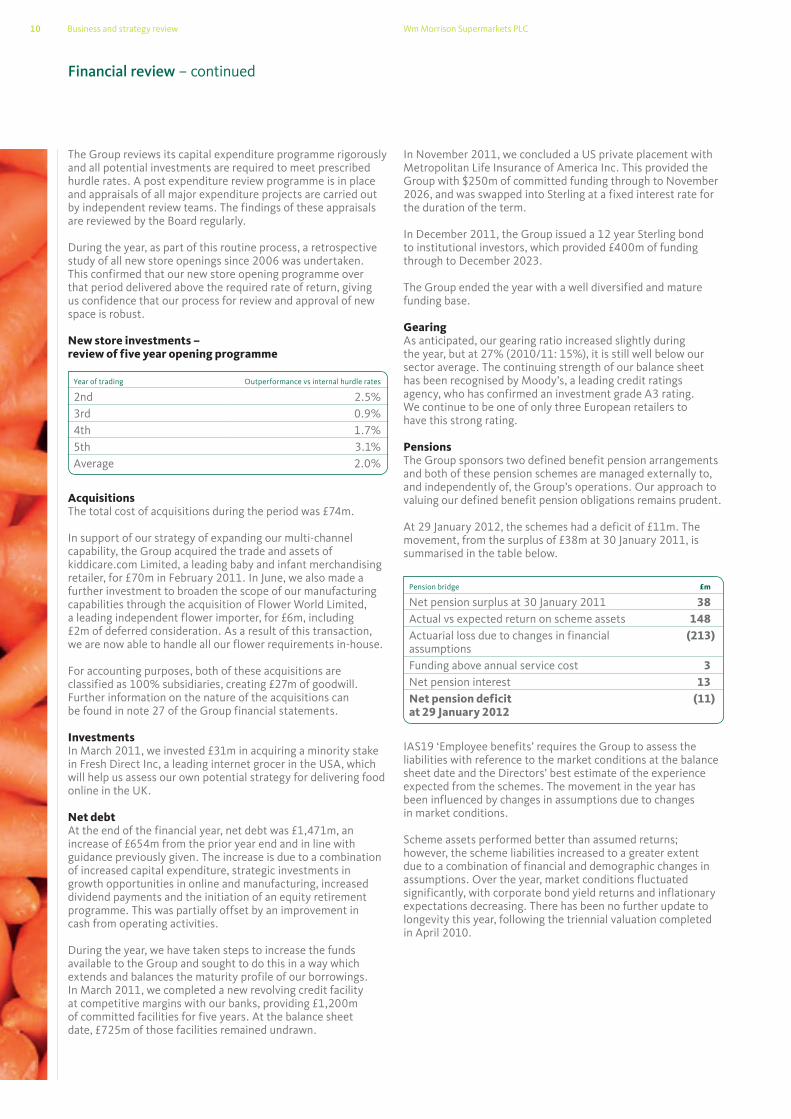

At 29 January 2012, the schemes had a deficit of £11m. The movement, from the surplus of £38m at 30 January 2011, is summarised in the table below.

Pension bridge £m

Net pension surplus at 30 January 2011 38Actual vs expected return on scheme assets 148Actuarial loss due to changes in financial assumptions

(213)

Funding above annual service cost 3Net pension interest 13Net pension deficit at 29 January 2012

(11)

IAS19 ‘Employee benefits’ requires the Group to assess the liabilities with reference to the market conditions at the balance sheet date and the Directors’ best estimate of the experience expected from the schemes. The movement in the year has been influenced by changes in assumptions due to changes in market conditions.

Scheme assets performed better than assumed returns; however, the scheme liabilities increased to a greater extent due to a combination of financial and demographic changes in assumptions. Over the year, market conditions fluctuated significantly, with corporate bond yield returns and inflationary expectations decreasing. There has been no further update to longevity this year, following the triennial valuation completed in April 2010.

The Group reviews its capital expenditure programme rigorously and all potential investments are required to meet prescribed hurdle rates. A post expenditure review programme is in place and appraisals of all major expenditure projects are carried out by independent review teams. The findings of these appraisals are reviewed by the Board regularly.

During the year, as part of this routine process, a retrospective study of all new store openings since 2006 was undertaken. This confirmed that our new store opening programme over that period delivered above the required rate of return, giving us confidence that our process for review and approval of new space is robust.

New store investments – review of five year opening programme

Year of trading Outperformance vs internal hurdle rates

2nd 2.5%3rd 0.9%4th 1.7%5th 3.1%Average 2.0%

AcquisitionsThe total cost of acquisitions during the period was £74m.

In support of our strategy of expanding our multi-channel capability, the Group acquired the trade and assets of kiddicare.com Limited, a leading baby and infant merchandising retailer, for £70m in February 2011. In June, we also made a further investment to broaden the scope of our manufacturing capabilities through the acquisition of Flower World Limited, a leading independent flower importer, for £6m, including £2m of deferred consideration. As a result of this transaction, we are now able to handle all our flower requirements in-house.

For accounting purposes, both of these acquisitions are classified as 100% subsidiaries, creating £27m of goodwill. Further information on the nature of the acquisitions can be found in note 27 of the Group financial statements.

Investments In March 2011, we invested £31m in acquiring a minority stake in Fresh Direct Inc, a leading internet grocer in the USA, which will help us assess our own potential strategy for delivering food online in the UK.

Net debtAt the end of the financial year, net debt was £1,471m, an increase of £654m from the prior year end and in line with guidance previously given. The increase is due to a combination of increased capital expenditure, strategic investments in growth opportunities in online and manufacturing, increased dividend payments and the initiation of an equity retirement programme. This was partially offset by an improvement in cash from operating activities.

During the year, we have taken steps to increase the funds available to the Group and sought to do this in a way which extends and balances the maturity profile of our borrowings. In March 2011, we completed a new revolving credit facility at competitive margins with our banks, providing £1,200m of committed facilities for five years. At the balance sheet date, £725m of those facilities remained undrawn.

Financial review – continued

11Annual report and financial statements 2011/12

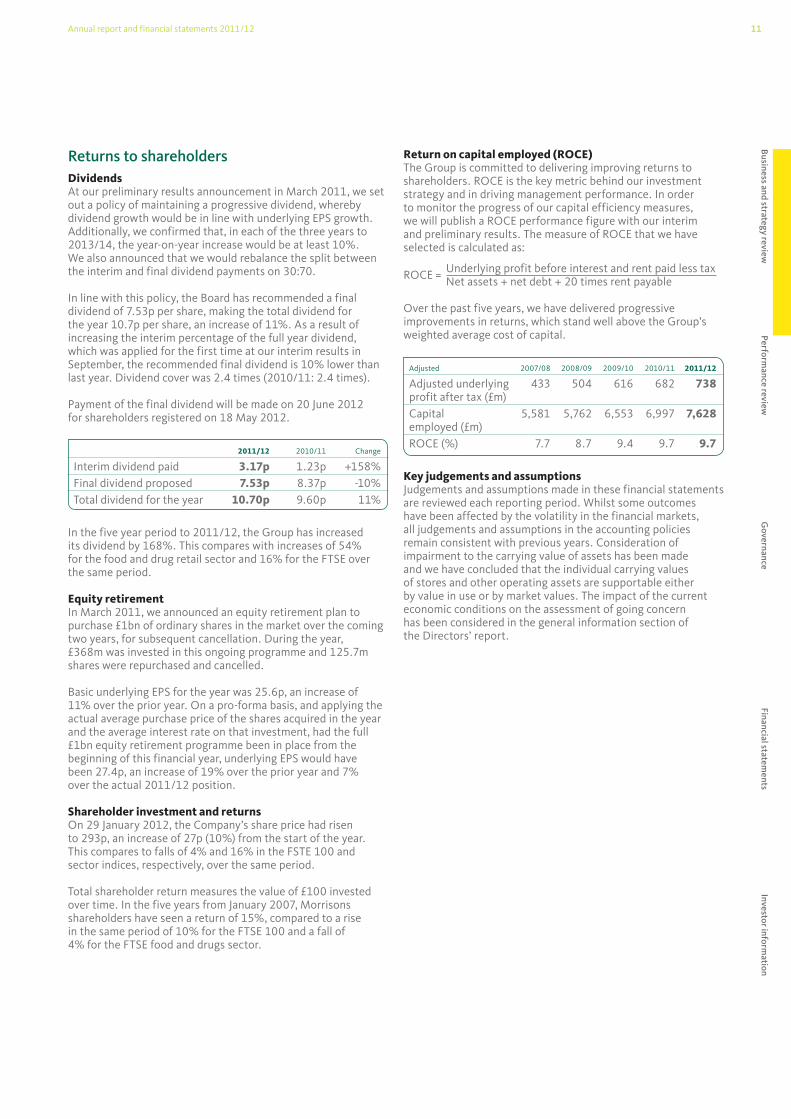

Returns to shareholdersDividendsAt our preliminary results announcement in March 2011, we set out a policy of maintaining a progressive dividend, whereby dividend growth would be in line with underlying EPS growth. Additionally, we confirmed that, in each of the three years to 2013/14, the year-on-year increase would be at least 10%. We also announced that we would rebalance the split between the interim and final dividend payments on 30:70.

In line with this policy, the Board has recommended a final dividend of 7.53p per share, making the total dividend for the year 10.7p per share, an increase of 11%. As a result of increasing the interim percentage of the full year dividend, which was applied for the first time at our interim results in September, the recommended final dividend is 10% lower than last year. Dividend cover was 2.4 times (2010/11: 2.4 times).

Payment of the final dividend will be made on 20 June 2012 for shareholders registered on 18 May 2012.

2011/12 2010/11 Change

Interim dividend paid 3.17p 1.23p +158%Final dividend proposed 7.53p 8.37p -10%Total dividend for the year 10.70p 9.60p 11%

In the five year period to 2011/12, the Group has increased its dividend by 168%. This compares with increases of 54% for the food and drug retail sector and 16% for the FTSE over the same period.

Equity retirementIn March 2011, we announced an equity retirement plan to purchase £1bn of ordinary shares in the market over the coming two years, for subsequent cancellation. During the year, £368m was invested in this ongoing programme and 125.7m shares were repurchased and cancelled.

Basic underlying EPS for the year was 25.6p, an increase of 11% over the prior year. On a pro-forma basis, and applying the actual average purchase price of the shares acquired in the year and the average interest rate on that investment, had the full £1bn equity retirement programme been in place from the beginning of this financial year, underlying EPS would have been 27.4p, an increase of 19% over the prior year and 7% over the actual 2011/12 position.

Shareholder investment and returnsOn 29 January 2012, the Company’s share price had risen to 293p, an increase of 27p (10%) from the start of the year. This compares to falls of 4% and 16% in the FSTE 100 and sector indices, respectively, over the same period.

Total shareholder return measures the value of £100 invested over time. In the five years from January 2007, Morrisons shareholders have seen a return of 15%, compared to a rise in the same period of 10% for the FTSE 100 and a fall of 4% for the FTSE food and drugs sector.

Return on capital employed (ROCE)The Group is committed to delivering improving returns to shareholders. ROCE is the key metric behind our investment strategy and in driving management performance. In order to monitor the progress of our capital efficiency measures, we will publish a ROCE performance figure with our interim and preliminary results. The measure of ROCE that we have selected is calculated as:

ROCE = Underlying profit before interest and rent paid less tax Net assets + net debt + 20 times rent payable

Over the past five years, we have delivered progressive improvements in returns, which stand well above the Group’s weighted average cost of capital.

Adjusted 2007/08 2008/09 2009/10 2010/11 2011/12

Adjusted underlying profit after tax (£m)

433 504 616 682 738

Capital employed (£m)

5,581 5,762 6,553 6,997 7,628

ROCE (%) 7.7 8.7 9.4 9.7 9.7

Key judgements and assumptionsJudgements and assumptions made in these financial statements are reviewed each reporting period. Whilst some outcomes have been affected by the volatility in the financial markets, all judgements and assumptions in the accounting policies remain consistent with previous years. Consideration of impairment to the carrying value of assets has been made and we have concluded that the individual carrying values of stores and other operating assets are supportable either by value in use or by market values. The impact of the current economic conditions on the assessment of going concern has been considered in the general information section of the Directors’ report.

Business and strategy review

Perform

ance review

Governance

Financial statements

Investor information

12 Wm Morrison Supermarkets PLCBusiness and strategy review

The convictions which underpin our objectives are set out on page 7.

Our strategy is in place

Increasing our efficiency

– Revamping our systems– Tackling indirect procurement– Increasing network efficiency– Driving in-store productivity

See pages 18 to 21 for further information

2

Capturing growth

– Exploring convenience – Vertical integration– Moving online

See pages 22 to 25 for further information

3

Our strategic objectives

Our vision for the business, to be ‘Different and Better then Ever’, is anchored by our convictions, and we have a clearly defined set of strategic initiatives that will deliver it. We have grouped these initiatives under the three strategic objectives of ‘driving the topline’, ‘increasing our efficiency’ and ‘capturing growth’.

Driving the topline

– Strengthening our brand– Moving further ahead on fresh– Optimising space– Enhancing our service culture– Completing National to Nationwide

See pages 14 to 17 for further information

1

13Annual report and financial statements 2011/12

Tackling indirect procurementIndirect procurement is an area where we have been working hard to strip out unnecessary cost.

Increasing network efficiencyThe opening of our new regional distribution centre at Willow Green, Bridgwater, completes our network efficiency initiative.Driving in-store productivityWe are continually working to improve our in-store processes to drive productivity whilst improving customer service.

We are upgrading our core IT systems through our Evolve initiative, a major six year programme of work. This will unlock efficiency savings and give us the solid platform we need to grow our existing business and seize new opportunities.

Revamping our systems Page 18

Vertical integrationFood production is a key differentiator and central to our ability to provide fresh food at affordable prices. We have increased our capabilities further in the year.

Moving onlineThe way customers shop is changing – they are becoming more and more accustomed to buying online. We have an exciting online agenda, building on the acquisition of Kiddicare and our stake in Fresh Direct.

The convenience sector is a significant opportunity for Morrisons, accounting for over £30bn sales and growing at twice the rate of the rest of the UK retail market. We entered this market in 2011/12 with our first M local stores.

Exploring convenience Page 22

Moving further ahead on freshWe aim to be the number one destination for fresh food in the UK at outstanding value for money.

Optimising spaceWe aim to get the best use out of every square foot in our store. We have been testing how we free up ambient space to give more space to fresh food and allow us to introduce new categories such as children’s clothing.

Enhancing our service cultureWe are enhancing our service culture and ensuring that our customers always get a warm and friendly experience in our stores.Completing National to NationwideWe aim to enable more customers across the country to be able to shop at Morrisons and have set out ambitious plans to increase our space.

Having a strong brand can be a real point of difference; we have set out to give customers an own brand range worth switching supermarkets for. We have made great progress in 2011/12, including the launch of our acclaimed M Kitchen range.

Strengthening our brand Page 14

Business and strategy review

Perform

ance review

Governance

Financial statements

Investor information

14 Wm Morrison Supermarkets PLCBusiness and strategy review

Traditional beefWe also launched our traditional beef breeds programme. This is a longer term programme, working in partnership with over 100 farmers to bring an exclusive range to our customers. The range will be available all year round at guaranteed quality and at an affordable price.

M saversIn January 2012, we launched M savers, our new entry price-point range, which is designed to be a clear proposition of good quality at the best price, in strong support of our conviction that value is forever.

We have increased our range to over 500 lines, competing with the broadest offer in the market and enabling customers to do a full value-led shop, should they choose to do so.

Coming upIn 2012/13, we will begin to deliver solutions across home and leisure, and other general merchandise categories. We will continue to leverage the expertise of our team of chefs to ensure our products and brands are consistently delivering quality, value and relevant innovation. In 2012/13, we aim to further increase own brand participation.

By the end of the journey, we will have a market-leading own brand, which customers trust to bring them everything from the best value, to unrivalled produce, to fabulous restaurant-quality meals at Morrisons prices. Customers will also be much more aware of the products we make and prepare in-store as well as those we manufacture ourselves in our own factories. Our new proposition will give us the relevant points of difference in every part of our store to support our positioning as a great food retailer, reaffirm our fresh credentials and offer unbeatable value to our customers.

Evolving the Morrisons experience

We are building on what we do best to be the number one destination for fresh food.

Strengthening our brand

We believe that having great own brand products can give consumers a reason to switch supermarkets, and we are ambitious to create an industry leading range.

Much work was done during the year, starting with a detailed benchmarking of existing Morrisons products against competitors. In blind taste testing, we found that our quality was already high, and overall was better than the average of our direct competitors. As always, there was room for improvement, particularly in going beyond just having a set of good own label products, to having a family of great relevant brands that influence consumer behaviour.

2011/12 saw the start of a three year programme of new product development, and we made good progress. Informed by research and customer insight, we built a plan, created a talented team and began the execution that will see 5,000 new products introduced this year and more than 10,000 products relaunched by Christmas 2013.

Our own brand is a major pillar in delivering our brand promise of ‘Friendly People Making Great Food Affordable for Everyone’.

M Kitchen launchWe commenced the rollout with our M Kitchen range in October 2011, launching over 600 products in a category where we knew that we were performing below the market.

Product quality is exceptional. Through close co-operation with suppliers and inspiration from great chefs including Pierre Koffman and Aldo Zilli, we have developed an innovative and exciting range with exceptional product quality.

The response from customers has been extremely positive and M Kitchen sales have increased 40% over the same categories last year.

In addition to the M Kitchen launch, we also relaunched our bread range, introducing new products, improving quality and finding ways to show our customers that we make our own bread. This has been really successful and we have seen own brand participation increase by 10%.

1 — Driving the topline

15Annual report and financial statements 2011/12

BelowHeadchef, Neil Nugent (right) and

in-house chef, Robert Craggs (left) creating new recipes.

An own brand range worth switching supermarkets for

“The new M Kitchen range means I have a fantastic home cooked style meal with minimal effort, in no time at all. Perfect!”Lindsey ScahillMorrisons customer, Leeds

Own brand facts

Sales increase in categories where M Kitchen was launched

40%

Number of M savers lines launched

500M Kitchen partners

Nigel Haworth, Atul Kochhar, Pierre Koffmann, Bryn Williams and Aldo Zilli

Business and strategy review

Perform

ance review

Governance

Financial statements

Investor information

16 Wm Morrison Supermarkets PLCBusiness and strategy review

Driving the topline – continued

Moving further ahead on fresh, optimising space and enhancing our service culture

These initiatives combine in our ‘Fresh Formats’, focused on offering customers the best fresh food in the UK, unrivalled value for money and fantastic service from an environment that really feels different. This initiative is a key part of our strategy and is underpinned by our core convictions that customers want fresh food, great value and a more experiential and engaging shopping environment.

We have brought together a number of separate strands of work to create a new shopping experience for our customers.

HOT service is an initiative to enhance our service culture and ensure that our customers always get a warm and friendly experience in our stores. Over 110,000 store colleagues have received service skills coaching – the largest training programme of its kind in the UK (read more in Our people, page 33).

During the year, we transformed 12 of our stores using this new thinking. We knocked down walls so that customers could see our craft skills in practice, introduced 350 more fruit and vegetable products, moved complementary products next to each other and rationalised the space given over to ambient grocery items. The results to date have been strong, with produce sales up 14% and sales in the delicatessen up over 40%. Where we rationalised ambient space, we successfully maintained sales and margin.

The work done in the Lab stores has enabled us to create a series of modules capable of being applied to our existing estate and to our new stores. In 2012/13, we will tailor the core concept to different locations and store sizes, ensuring that we provide customers with the elements they really want while maximising the benefits from our investment. This continuing evaluation will see around 15% of our space operating all or most of the new concept by the end of the first half of the year, with total capital expenditure per store of c.£1.7m. This is contained within our 2012/13 capital expenditure targets.

Our Space Lab, where we have found ways to work our space harder and eliminate duplicated items. The Lab has shown that we can ‘liberate’ up to 750,000 square feet of our existing store space, which will be available for an expanded fresh food offer and new ranges such as restaurant quality ready meals and children’s clothing.

Our Fresh Lab, where we have created a fantastic fresh food environment, transforming our produce and flowers sections, introducing new ranges and revitalising our counters.

17Annual report and financial statements 2011/12

Market overview

Own label growth

Retailer own brand sales have been performing more strongly than branded products as consumers look for ways to manage their budget. This is a positive trend for our business as we continue with the relaunch of our own brand range over the next two years.

Throughout 2011, retailer own brand value ranges have seen an increase in growth levels, outperforming other tiers. Coming into 2012, premium ranges have seen resurgence in growth.

8

10

6

4

2

0

-2

-4

-6

12 w

eeks

’ sal

es g

row

th v

s la

st y

ear %

23 Jan2011

20 Mar2011

Value

Source: Kantar Worldpanel

15 May2011

10 Jul2011

27 Nov2011

4 Sep2011

22 Jan2012

Premium

Consumer confidenceConsumer confidence remained fragile in 2011.The end of the year saw confidence close to an all-time low. 2012 is expected to continue to be challenging.

-20

-15

-25

-30

-35

-40

GFK

Con

sum

er C

onfid

ence

Jan2011

Mar2011

Source: GFK NOP Consumer Confidence

May2011

Jul2011

Nov2011

Sep2011

Jan2012

Completing National to Nationwide

We aim to offer customers throughout Great Britain easy access to a Morrisons store.

Currently, there are still approximately 6.6m households which do not have a Morrisons store in close proximity. This gives us significant headroom for growth, particularly in the South, where we are less well represented.

During the year, we opened a total of 37 new stores, including one replacement and three in our new convenience format. 19 of the new stores were previously operated by Netto. They have an average size of 8,000 square feet and are therefore much smaller than the majority of the Morrisons estate, which averages 27,100 square feet. Their success under the Morrisons brand, and the performance of our new convenience format, reinforce our confidence that we can operate effectively in smaller store sizes, where previously we had very few stores below 10,000 square feet.

Our net selling space increased by 643,000 square feet (5.2%) during the year, slightly ahead of our previously announced target of 600,000 square feet, through a combination of new stores, acquisitions and extensions. Of this, 107,000 square feet came from extending 15 stores in our existing estate. We ended the year with 12.9m square feet of net retail space and an estate of 475 stores.

In March 2011, we announced an accelerated space opening programme of 2.5m square feet of new space over the next three years to 2013/14. This year, we exceeded our first year target. In 2012/13, we expect to add a further 700,000 square feet and we are on track to meet our three year expansion objective.

BelowOpening our Wrexham store in November 2011.

Business and strategy review

Perform

ance review

Governance

Financial statements

Investor information

18 Wm Morrison Supermarkets PLCBusiness and strategy review

With two years in planning and 16 months in rollout, all the produce sites have invested in a huge collaborative process. The three month readiness programme before each go-live covered everything from leadership through to infrastructure. This, along with the commitment shown by colleagues, was the key success factor.

The new produce solution: provides advanced, centralised planning and scheduling; orders from the sales management system; checks raw material inventory and creates a demand for manufacturing and replenishment stocks from suppliers; and sets hourly schedules for production lines. We have automated the processes for bringing raw materials to site, receipt of orders and marrying up our resources. We now have consistent methods for planning and scheduling, and standard reporting.

The dispatch process is also more efficient, with produce allocation and picking lists generated automatically, meaning stock visibility has improved across the business. We can produce a report at any time to show exactly what is in every area of the business, and in what state, replacing the need for continual counts.

The new solution supports our drive for quality in fresh produce. It allows us to monitor the ongoing quality of all products, enabling better supplier management. Better visibility of stock also increases the focus on reducing inventory in the supply chain, which helps to ensure freshness.

In 2012/13, we aim to deliver benefits of £1.3m through improved labour efficiency and yield. The major benefit, however, is derived from improving sales order fulfilment against quantity and time. This will lead to improved availability in our stores for customers. The overall benefit is estimated at £2.7m a year.

Next up – meatOur meat manufacturing solution is going live to our first abattoir in the second half of 2012/13, with rollout to the other two sites by early 2013/14. The meat solution is necessarily more complex than produce, yet builds on the same model. Productivity and efficiency savings are expected, with an overall benefit of £2.2m year-on-year once the system is complete.

Innovative systems to realise efficiencies

We have been looking at every aspect of our business, from field to fork, to see where we can increase efficiency.

Revamping our systems

Our Evolve programme started in 2008 and is now approximately halfway to completion. Evolve is all about making sure we have the right systems in place to support our business processes, increase sales and efficiency, and compete strongly in today’s retail market as well as creating flexibility for the future. In short, making a well run business run better.

With a team of over 700 people, the programme has already delivered:

a new central accounting system and a single payroll system for colleagues;

12,500 new touchscreens on tills; a solution for simplifying cash reconciliations in-store; and voice picking in our distribution centres to increase the accuracy of deliveries.

A key focus in 2011/12 has been the introduction of a new produce manufacturing solution to our five manufacturing produce sites to improve efficiency.

Produce manufacturing solutionProduce manufacturing is central to the Morrisons commitment to quality from field to fork. Employing 2,700 people, our produce sites produce 29m packs of fresh fruit and vegetables every week for sale in our stores. Until 2010/11, each site was planning independently against daily orders and managing stock levels accordingly using manual systems. Visibility of inventory levels and yields was limited.

The Evolve programme means more than just new systems. With over 75% of the workforce set to use the new solution, skill levels across the entire division were raised. “We had to change the way people operate – and their mindset”, says Andy Joynson, Manufacturing Director for Produce, “we introduced more robust processes, structure and organisation – driven by better solutions.”

2 — Increasing our efficiency

19Annual report and financial statements 2011/12

Innovating our systems to make a well run business run better

“Improving availability in-store through better service means £2.7m each year to the business.”Andy JoynsonManufacturing Director for Produce

Produce Evolve facts

Locations in the UK

Cutler, Flaxby, Gadbrook, Rushden and Thrapston

Order fulfilment improved by

2%

BelowColleagues using the new

technology at Cutler Heights.

Business and strategy review

Perform

ance review

Governance

Financial statements

Investor information

20 Wm Morrison Supermarkets PLCBusiness and strategy review

Tackling indirect procurement

Our indirect procurement programme has a target of saving £100m by 2013/14 and we made good progress during the year, delivering £40m of benefit.

We reviewed every area of spend – both revenue and capital expenditure, and looked at a variety of ways to reduce cost, including the use of e-auctions, rate negotiations, consolidating spend and reducing consumption.

Examples of savings achieved include: renegotiation and re-specification of packaging across stores and manufacturing;

the consolidation of waste contracts across stores and packhouses; and

a significant reduction in marketing print costs.

We also undertook an exercise to reduce the build and fit out costs of new stores opening our first ‘Lean Store’ at Newport in November and achieved a saving of £2m against our original estimates, the equivalent of c.30% of the total store build and fit out cost. Around half of the savings are already being applied to all new build stores. The remaining 50% will be trialled further and implemented when we are confident that we can take the cost out without compromising our high standards.

Increasing network efficiency

Our network optimisation initiative, which was launched in 2007, has focused on building capacity, reducing costs and increasing efficiency throughout our supply chain.

In the final quarter of the year, we completed the original programme with the opening of a new, state-of-the-art RDC for the South West at Willow Green, Bridgwater. This 800,000 square foot site, which replaces a number of smaller centres, was opened ahead of schedule to enable us to manage the busy Christmas period and will become fully operational in the first quarter of 2012/13. The new RDC, a capital investment of £105m, enables us to consolidate service into one efficient centre and will deliver savings of £20m annually from 2014/15.

AboveBuilding our new Lean Store at Newport.

AboveOur new Willow Green RDC, completed ahead of schedule.

Increasing our efficiency – continued

Key Willow Green statistics

Site size

800,000 square feet

Volume throughput expected at

110m cases per year

Colleagues to be employed (on an FTE basis)

1,000Stores serviced through Willow Green at full maturity

63

21Annual report and financial statements 2011/12

AboveOpening our counters later means customers can see our craftspeople at work.

Driving in-store productivity

Great companies continually strive to be more efficient. Morrisons has a number of initiatives underway which will drive efficiency and cut unnecessary cost out of our business.

Every hour per day we save in all of our stores equates to approximately £1.4m of annual cost saving – so even small changes can deliver big benefits. In March 2011, we launched an initiative to focus on store productivity and have delivered savings of £25m in the year. Good progress was made on a number of initiatives, including opening our specialist counters later in the morning, which reduced labour cost but also allows our customers to see our craftspeople setting up for the day; automating the receipt of news and magazines, which avoids manual checking and administration; and changing the way bananas are displayed to reduce the labour cost whilst also reducing the wastage that arises from handling the fruit too much. During the coming year, we will continue to trial and roll out new ideas and we are on track to deliver our target of £100m by 2013/14.

Market overview

Value at the forefront of shoppers’ minds

Household incomes have come under pressure throughout 2011 as rising commodity and energy prices have resulted in CPI inflation rising above 5%.

As as result, pricing and overall value have become increasingly important factors in purchasing decisions.

Shoppers are becoming increasingly price conscious, with almost seven out of ten now saying they make the majority of their grocery shopping decisions before they get to store, an increase of 40% since 2008.

ABC1 55%

77%C2DE

Source: GFK NOP Consumer Confidence

Percentage who state how much they spend is the most important thing in their grocery shopping(Customer demographic ABC1 and C2DE)

The groups that are most conscious about how much they spend are families facing the pressure of lower incomes.

Extent to which shoppers plan their grocery shop

2011 67%

47%2008

Source: IGD ShopperVista

Business and strategy review

Perform

ance review

Governance

Financial statements

Investor information

22 Wm Morrison Supermarkets PLCBusiness and strategy review

Not only do we offer a truly market leading fresh proposition, but by staying true to our commitment to great value, we guarantee our customers will not pay more for their fresh produce, meat, fish and key ambient essentials than they do in our larger stores.

We are delighted with the results and customer feedback has been very positive. Sales and margins are both ahead of our business case, own label participation is 7% higher than in our core estate and fresh participation is 12% higher.

After only eight weeks of opening, we were highly commended in the prestigious NACS International Convenience Awards for innovation with fresh food in a small footprint, an accolade that no other top four multiple grocery retailer has achieved.

The key to success in the convenience sector is being flexible and ensuring that we adapt and are able to meet the differing needs of each local area.

A flexible conceptIn January 2012, we opened our third M local store at Grafton Street, close to The University of Manchester. This is our first suburban convenience format with high transient footfall, operating from 4,250 square feet, which is larger than our neighbourhood convenience formats. All the usual elements of M local are included, but we have specifically tailored our offer to the student population – extending our ‘hot food to go’ and fresh food and meal solution ranges, whilst flexing the grocery offer to include student essentials from a wide range of stationery, to home essentials.

There is also a prominent service counter, additional self scan customer checkouts and an external seating area enabled with free Wi-Fi where customers can sit and enjoy food and drinks they have purchased in our store.

Although we are still trialling these formats, the results to date have been ahead of our expectations, with very positive customer feedback.

We will continue to open more M locals during the course of 2012/13 and adapt our formats to cater for market opportunities and local customer needs, such as city centre formats and petrol station solutions. As our convenience estate grows, we will be investing in the infrastructure required to support a larger network of convenience stores.

Capturing growth throughfresh opportunities

We are expanding into new channels and formatsto serve the evolving needs of our customers.

Exploring convenience

The UK convenience market presents an opportunity for Morrisons to expand its business. It accounts for over £30bn of sales, represents £1 in every £5 spent on grocery and is growing at twice the rate of the rest of the UK retail market.♥

Customers are seeking easier ways to shop and want to be able to top up on items they need without having to travel to their nearest large supermarket. This is particularly true at a time when budgets are tight and customers are looking to spend less per shopping trip and save on fuel costs.

We believe that no one else is currently offering a truly great convenience shopping experience; too often convenience is about compromise – poor quality, bad value and limited choice.

Morrisons therefore has the opportunity to create something different by leveraging its vertical integration and great fresh and value credentials to develop a really distinctive and compelling fresh food experience, offering customers great food at affordable prices at a location which is convenient for them.

As planned, we opened three trial stores. They offer a very different convenience experience and are fresh led, with fresh prices in line with prices available across all our stores.

The M local propositionOver 50% of space is dedicated to fresh food and scratch cooking; significantly more than the industry average of 36%. We offer customers c.2,500 lines, including over 100 fruit and vegetable products, a broad range of meat, fish, bakery and deli, as well as freshly prepared sandwiches.

We also offer a salad bar, freshly baked bread delivered daily, freshly squeezed orange juice, a good range of locally sourced products and the option for customers to grind their own coffee in-store. We even offer an order and collect service, enabling customers to order products by 11.00 a.m. to be collected the same day. This is unique in the market and gives us great availability of fresh produce.

3 — Capturing growth

♥Source: BRC

23Annual report and financial statements 2011/12

Fresh food and convenience, it’s why our customers keep coming back...

“I’ve been really impressed with our new M local store – fresh food, convenient opening times, friendly staff and much better value than the alternative nearby shops.” Rachel GriffenM local customer, Ilkley

M local facts

Space dedicated to fresh food

over 50%

Number of fresh products delivered from a hub store each day

125Number of new M local stores to open in 2012/13

20

BelowOur M local store at Ilkley.

Business and strategy review

Perform

ance review

Governance

Financial statements

Investor information

24 Wm Morrison Supermarkets PLCBusiness and strategy review

Vertical integration

Vertical integration gives us a true source of competitive advantage and is crucial to our ambition of leading in fresh food – reinforcing our credentials around provenance and sourcing, giving us flexibility to run industry leading promotions and supporting Group profitability.

In 2010, we set out our strategic objective to increase the scope of our vertical integration and to invest £200m in additional capacity for relevant fresh categories over three years. Over the last two years, we have expanded into several new categories.

In June 2011, we acquired Flower World, adding fresh flowers to our range of fresh competencies and, in January 2012, we agreed to acquire a pork and lamb retail meat packing facility from Vion Group in Winsford. This 105,000 square foot site will enable us to gain greater control over the quality and provenance of our packed meat products by bringing more production in-house. In March 2012, we announced our intention to establish a seafood processing capability by the end of the year in order to further expand our authority in fish. We remain well on track to achieve our goal of extending our vertical integration further into new categories.

Capturing growth – continued

Our business model Where possible, we source locally and manufacture in our own sites. We distribute to our stores through our own network. The benefits are consistent freshness at a reduced cost whilst being in control of the supply chain.

AboveAll in-store flowers are now supplied by our Flower World subsidiary.

AboveHaving our own abattoirs increases the freshness of our food in-store.

1 From selection...

Being close to source means we can control the provenance and quality of our food, ensuring it has been sourced ethically and in a sustainable way.

2 To packhouse...

Our manufacturing facilities reduce our supply chain lead times, allowing us to maximise the freshness of food in-store and reduce waste.

3 Distributed and delivered to...

Operating our own transport fleet provides flexibility in moving products from suppliers to RDCs and from our food manufacturing sites to our stores. This ensures freshness and cost control.

4 All our stores

As we prepare food in-store, we can react to customer trends throughout the day. This allows us to reduce our waste and costs, and keep our prices low.

25Annual report and financial statements 2011/12

Moving online

The way customers shop is changing – they are becoming more and more accustomed to buying online.

The total online market in the UK is almost £70bn and growing at 16%, and the online grocery market is worth £6bn and growing at 19%.�

There is a clear opportunity for Morrisons and we have taken the first steps in our journey to developing both an online food and general merchandise offer.

Online general merchandiseGeneral merchandise is migrating online, away from the high street and from ‘big box’ supermarkets. We intend to complement our core supermarket offer with an online general merchandise offer in categories which have appeal and relevance to our customers. We have started this year with the acquisition of Kiddicare – the most successful online baby retail business in the UK. We are expanding Kiddicare as a genuine ‘multi-channel’ business and, during the year, announced plans for ten flagship stores throughout the UK. We are also leveraging our 11.4m weekly customers in Morrisons by increasing their awareness of the Kiddicare business, leading to strong growth. Additionally, using the industry leading operating platform acquired with Kiddicare, Morrisons.com will launch its first categories in the final quarter of 2012.

Online foodThe online food market is growing fast and is expected to reach £11.2bn by 2016, some 6% of the total grocery market.♠ Morrisons does not yet offer an online service, as we do not believe any retailer in the UK has achieved the right balance of service to customers and profitable returns for shareholders. In 2011, we took an initial step in online grocery through acquiring a minority stake in Fresh Direct, a leading fresh food, online retailer in New York. We have established a very positive relationship with them, including the embedding of a team into the business in order to understand it in great detail before bringing it back to the UK. We will outline our plans for online food towards the end of 2012/13.

AboveOur Kiddicare showroom gives customers the option of shopping in-store as well as online.

Actual Forecast

Key facts

Customers who have used the Morrisons app

900,000Visits to the Morrisons mobile website in Q4 2011/12

481,000

�Source: IMRG E-Business Information and IGD♠Source: IGD

Market overview

New channels to market

The market place is continually evolving, and a key trend has been the growth of different retailing channels and the rise of the multi-channel retailer.

Between 2011 and 2016, market sales through local convenience stores are anticipated to grow by 26% and online sales are estimated to grow by 90%. As we develop these areas, they provide further opportunity for us to grow and meet the needs of our customers.

Convenience sales £bn

2011 33.6

42.22016

Online sales £bn

2011 5.9

11.22016

Source: IGD

Business and strategy review

Perform

ance review

Governance

Financial statements

Investor information

26 Wm Morrison Supermarkets PLCPerformance review

How do we identify our KPIs?There are many internal and external factors affecting the performance of our business. We have focused on a few key indicators that are measurable, comparable, and can be acted on to reflect the performance and progress of our business.

Read more about business performance — page 4

Strategic objectives

1 Driving the toplinea Strengthening our brandb Moving further ahead on freshc Optimising spaced Enhancing our service culturee Completing National to

Nationwide

2 Increasing our efficiencyf Revamping our systemsg Tackling indirect procurementh Increasing network efficiencyi Driving in-store productivity

3 Capturing growthj Moving onlinek Exploring conveniencel Vertical integration

What is important to our colleagues?Over 105,000 colleagues participated in our opinion survey to give their thoughts on life at Morrisons.

See page 33

We have identified a number of measures that are important to the success of the Group’s financial performance and operational excellence, and to our stakeholders, customers, suppliers and colleagues. Below are the measures the Board consider to be key to the achievement of the Group’s strategy.

Financial KPIs Key Definition

Like-for-like sales a b c d Measures store-based sales on the same basis as the previous year, excluding the impact of new store openings, store disposals and the impact of major refurbishments and extensions. The measure excludes fuel sales and VAT.

UK grocery market share

e j k l The Group’s percentage of retail sales in the UK grocery sector, as measured by Kantar Worldpanel at the end of January.

Underlying profit e f g h i

Measures the normal underlying business performance. Profits are adjusted to remove volatile or one-off costs and credits.A reconciliation of underlying profit is provided in note 1 of the Group financial statements.

Underlying basic earnings per share (EPS)

a b c d e f g h

i

The EPS measure uses underlying profits, as defined above, divided by the weighted average number of shares in issue at the year end date. A calculation is provided in note 9 of the Group financial statements.

Dividend cover a b c d e f g h

i

Calculated as underlying basic earnings per share,as defined above, divided by total dividend per share for the year.

Net debt g h The Group’s overall debt position at the year end. A summary of net debt is provided in note 25 of the Group financial statements.

Capital investment

g e j k Measured as additions to property, plant and equipment, investment properties, intangible assets and investments.

Return on capital employed (ROCE)

g h i The Group measures ROCE as underlying profit before interest and rent paid less tax divided by the sum of net assets, net debt and 20 times rent.

Non-financial KPIs Key Definition

Carbon footprint reduction

h Our carbon footprint includes energy, waste, refrigeration and transport for our stores, offices, manufacturing and packing facilities.

Waste to landfill reduction

i Any remaining waste from our stores that we are unable to recycle or have processed, expressed as a percentage of total waste compared to the prior year.

Measuring performance against our strategy

27Annual report and financial statements 2011/12