making sense of balance sheets€¦ · balance sheet abc company as of 12/31/2015 current assets...

TRANSCRIPT

MAKING SENSE OF

BALANCE SHEETS

Ronald Sereika, CCE, CEW

How to start analysis process

• The user of a firm’s annual report can expect to

encounter a great quantity of information that

encompasses the required information- Financial

statements, notes to the financial statements, the

auditors report, a five year summary of key

financial data, management’s discussion and

analysis of operations – as well as material that is

included in the report at the imagination and

discretion of management.

Starting the analysis process

• To understand how to navigate the vast amount of

information available to financial statement users,

background on the accounting rule-making

environment is necessary.

• Financial statements are prepared according to

generally accepted accounting principles (GAAP)

that have been adopted in order to achieve a

presentation of financial information that is

understandable by as well as relevant and reliable

for decision making.

Continuing the analysis

process

• The SEC regulates US companies that issue

securities to the public and requires issuance of a

prospectus for any new security offering. The SEC

also requires regular filings of:

• Annual reports – 10-K

• Quarterly reports 10-Q

• Other reports- if you change auditors that would be

a 8-K.

Who regulates the SEC

• The SEC has congressional authority to set the accounting policies and has issued rulings called Accounting Series Releases (ASRs) and Financial Reporting Rulings (FRR’s).

• For the most part however, accounting rule making has been delegated to the Financial Accounting Standards Board (FASB).

• The FASB is comprised of seven full time paid members. The Board issues Statements of Financial Accounting Standards and Interpretations, usually after some lengthy process of deliberations.

• The SEC and FASB work together to develop accounting policy, with the SEC playing mainly a supporting role.

Where to find financial

information

• Corporate financial statements are available from

several sources. All publicly held companies must

file a form 10-K annually with the SEC. The

information in this document is mandated by the

SEC and contains uniform content, presented in

the same order for all filing companies.

• Documents filed with the SEC can usually be

accessed through the Electronic Data Gathering,

Analysis, Retrieval (EDGAR) database at the

SEC’s website www.sec.gov

WWW.SEC.GOV

Which Financial statements to

use

• Balance Sheet- Shows the financial position –

assets, liabilities, and stockholders equity of a firm

on a particular date, such as the end of quarter or

year.

• The statement is a summary of what a firm owns

(Assets) and what the firm owes to outsiders

(Liabilities) and to internal owners (Stockholders

Equity)

The Balance Sheet

• The accounts balances on a balance sheet must

balance, meaning the total of all assets must

equal the sum of the liabilities and stockholders

equity.

• Assets= Liabilities + Stockholders equity

A=L+OE

Balance Sheet and P&L Related

• Balance sheet - one point in time

• Profit and loss - running summary of time period

• Statement of Cash Flows- Cash must be generated for a

company to remain in business even if they are

showing increases in sales and profits

Balance Sheet

• current assets

• fixed assets

• current liabilities

• long term liabilities

• net worth

Current Assets• Cash

• Marketable Securities

• Accounts Receivable

• Inventory

• Prepaids

• Current assets include cash or those assets expected to be

converted into cash within one year or one

operating cycle, whichever is longer.

Fixed Assets

• Land

• Buildings

• Depreciation

• Long term Notes

• Goodwill

• Intangible

• These assets produce

economic benefits for more than one year for the

company.

Current Liabilities

• Accounts payable

• Short term notes due bank

• Current maturities of long term debt

• Accrued liabilities

• Taxes

• Current Liabilities are the claims against the assets that must

be paid in one year or one operating cycle, whichever is longer.

Long term Liabilities

• Long term debt

• long term notes to suppliers, owners

• Capital leases

• Pension liability

• Long term Liabilities are obligations by the company of greater

than one year that will need to be satisfied.

Net Worth / Equity

• Capital Stock

• Paid In Capital

• Retained Earnings

• Treasury Stock

• Shareholder/Stockholder equity is the residual interest in

assets that remains after deducting liabilities.

Working Capital formula

Current Assets – Current Liabilities = Working capital

If this calculation ever shows a negative number

than the company you are reviewing is

BANKRUPT

Balance Sheet

ABC Company

As of

12/31/2015

Current Assets Current LiabilitiesCash and Cash Equivalents $50,000 Accounts Payable $490,000

Accounts Rec. Less Allowance for $590,000 Accrued Liablilites $40,000

Doubtful Acounts $10,000 Income Taxes Paybale $25,000

Inventories $990,000 Current Maturities of LT Debt $125,000

Prepaid Expenses $5,000 Short term debt $50,000

Total Current Assets $1,635,000 Total Current Liabilities $730,000

Property Plant & Equip Deferred Federal Income Taxes $30,000

Land $1,000,000 Long Term Debt $150,000

Buildings and leasehold Improve $650,000 Total Liabilities $910,000

Equipment $250,000

$1,900,000 Stockholders Equity Less: Accumaulated Depreciation $60,000 Common Stock Par Value $1.00

Net Property Plant and Equipment $1,840,000 1,000,000 Shares issued, $1,000,000

GoodWill $325,000 Additonal Paid in Capital $250,000

Other Assets $75,000 Retained Earnings $1,715,000

Total Assets $3,875,000 Total Stockholders Equity $2,965,000

Total Liabilities and Stockholders $3,875,000

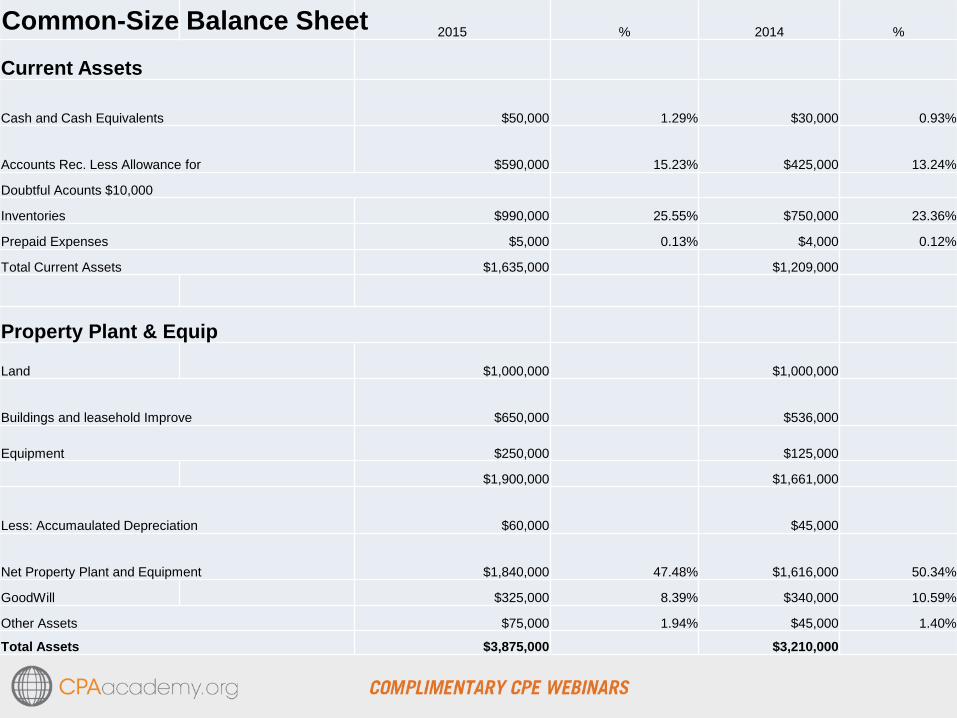

2015 % 2014 %

Current Assets

Cash and Cash Equivalents $50,000 1.29% $30,000 0.93%

Accounts Rec. Less Allowance for $590,000 15.23% $425,000 13.24%

Doubtful Acounts $10,000

Inventories $990,000 25.55% $750,000 23.36%

Prepaid Expenses $5,000 0.13% $4,000 0.12%

Total Current Assets $1,635,000 $1,209,000

Property Plant & Equip

Land $1,000,000 $1,000,000

Buildings and leasehold Improve $650,000 $536,000

Equipment $250,000 $125,000

$1,900,000 $1,661,000

Less: Accumaulated Depreciation $60,000 $45,000

Net Property Plant and Equipment $1,840,000 47.48% $1,616,000 50.34%

GoodWill $325,000 8.39% $340,000 10.59%

Other Assets $75,000 1.94% $45,000 1.40%

Total Assets $3,875,000 $3,210,000

Common-Size Balance Sheet

2015 % 2014 %

Current Liabilities

Accounts Payable $490,000 12.65% $285,000 8.88%

Accrued Liablilites $40,000 1.03% $25,000 0.78%

Income Taxes Paybale $25,000 0.65% $15,000 0.47%

Current Maturities of LT Debt $125,000 3.23% $140,000 4.36%

Short term debt $50,000 1.29% $60,000 1.87%

Total Current Liabilities $730,000 $525,000

Deferred Federal Income Taxes $30,000 0.77% $18,000 0.56%

Long Term Debt $150,000 3.87% $175,000 5.45%

Total Liabilities $910,000 $718,000

Stockholders Equity

Common Stock Par Value $1.00

1,000,0000,Shares issued, $1,000,000 25.81% $1,000,000 31.15%

Additonal Paid in Capital $250,000 6.45% $124,000 3.86%

Retained Earnings $1,715,000 44.26% $650,000 20.25%

Total Stockholders Equity $2,965,000 $2,492,000

Total Liabilities and Stockholders $3,875,000 $3,210,000

Common-Size Balance Sheet

Liquidity Ratios

• Current ratio

Current Assets/Current Liabilities

2015 $1,635,000 / $730,000 2.24:1

2014 $1,209,000/ $525,000 2.30:1

• Quick ratio

Current Assets-Inventory/Current Liabilities

Days sales outstanding DSO

Accounts Receivable/Sales/365

This will tell you how fast you are collecting AR

Educate your management that this formula is

driven more by sales than collections, avoid

having DSO as a measurement for your review.

To show how well you are collecting cash take

the amount of cash you collect in a month and

divide the AR balance from the beginning of that

month into the amount you collected- compare months

Days Payable outstanding DPO

• Accounts Payable/CGS/365

This will tell you how fast the company is paying their bills

This is helpful if you are looking to set up a new customer

and you want to see on average how they are paying their

bills, can they meet your payment terms?

Leverage Ratios

Debt Ratio -Total Liabilities/Total Assets

Shows the proportion of all assets what are financed with

debt.

Debt to Equity – Total Liabilities /Stockholders Equity

Measures the total debt relative to your equity.

Times Interest earned- Operating Profit/Interest Expense

Measures how many times interest expense is covered by

operating earnings.

the amount of cash you collect in a month and

divide the AR balance from the beginning of that

month into the amount you collected- compare months

The 5 C’s of Credit

#1 Character- The moral qualities and actions of a credit

applicant which oblige the applicant to pay

debts as they become due.

#2 Capacity- The ability to pay when debt is due

#3 Capital- The financial strength of a risk as measured by

the equity or Net Worth of an applicant.

#4 Collateral- Those possessions or equities from which the

customer or debtor might be expected to draw

upon should character and capacity fail.

#5 Conditions-The current and expected general economic

situations as they might affect the applicant.

How to make a credit decision just

from a Balance Sheet

Look at the Working Capital ratio first to make sure they have

enough assets to cover debt for coming year

Do ratios; Current Ratio, Debt to Equity, DPO, DSO

Look at the total they have in Accounts Payable, see what

the percentage of what you want to sell to them or loan

them is of the AP total.

#1 answer- Call and talk to the controller, ask them about

your concerns and she how he/she responds (Character)

To show how well you are collecting cash take

the amount of cash you collect in a month and

divide the AR balance from the beginning of that

month into the amount you collected- compare months

QUESTIONS

Ronald A Sereika, CCE,CEW

Copyright 3/1/2016