management accounting fundamentals - cga-education.org · 6.2 absorption and variable costing...

TRANSCRIPT

Management AccountingFundamentals

Module 6Absorption and variablecosting and budgeting

Lectures and handouts by:Shirley Mauger, HB Comm, CGA

2

Module 6 - Table of Contents

6.1 Absorption and variable costing6.2 Absorption and variable costing income statements6.3 Advantages and disadvantages of absorptions and variable

costing6.4 Impact of JIT inventory methods6.5 Basic framework of budgeting6.6 Advantages of budgets6.7 Preparing the master budget6.8 Computer illustration 6-1: Sales budget and cash collection

scheduleReview question: Variable and absorption costing income stmt.Review question: Variable and absorption costing calculationsReview question: Cash collection schedule, production budgetReview question: Cost of purchases & cash budgetReview question: Cash budgetReview question: Cash disbursementsReview question: Multiple choice

12

3

3,4N/A

567891011

Part Content

3

Part 1

Absorption and variablecosting

Topic 6.1

MA1 – MODULE 6

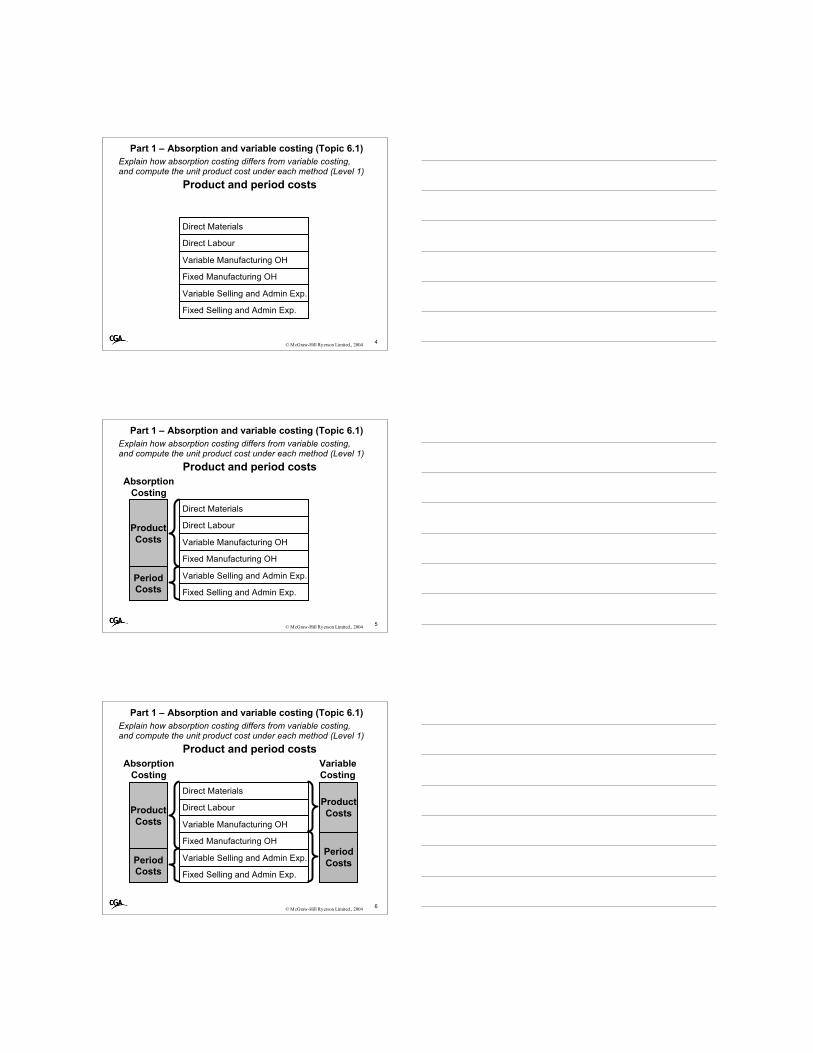

Part 1 – Absorption and variable costing (Topic 6.1)Explain how absorption costing differs from variable costing,and compute the unit product cost under each method (Level 1)

4

Direct Materials

Direct Labour

Variable Manufacturing OH

Fixed Manufacturing OH

Variable Selling and Admin Exp.

Fixed Selling and Admin Exp.

© McGraw-Hill Ryerson Limited., 2004

Product and period costs

Part 1 – Absorption and variable costing (Topic 6.1)Explain how absorption costing differs from variable costing,and compute the unit product cost under each method (Level 1)

5

Direct Materials

Direct Labour

Variable Manufacturing OH

Fixed Manufacturing OH

Variable Selling and Admin Exp.

Fixed Selling and Admin Exp.

AbsorptionCosting

ProductCosts

PeriodCosts

© McGraw-Hill Ryerson Limited., 2004

Product and period costs

Part 1 – Absorption and variable costing (Topic 6.1)Explain how absorption costing differs from variable costing,and compute the unit product cost under each method (Level 1)

6

Direct Materials

Direct Labour

Variable Manufacturing OH

Fixed Manufacturing OH

Variable Selling and Admin Exp.

Fixed Selling and Admin Exp.

VariableCosting

AbsorptionCosting

ProductCosts

PeriodCosts

ProductCosts

PeriodCosts

© McGraw-Hill Ryerson Limited., 2004

Product and period costs

Part 1 – Absorption and variable costing (Topic 6.1)

7

Direct Materials

Direct Labour

Variable Manufacturing OH

Fixed Manufacturing OH

Variable Selling and Admin Exp.

Fixed Selling and Admin Exp.

VariableCosting

AbsorptionCosting

ProductCosts

PeriodCosts

ProductCosts

PeriodCosts

© McGraw-Hill Ryerson Limited., 2004

Product and period costs

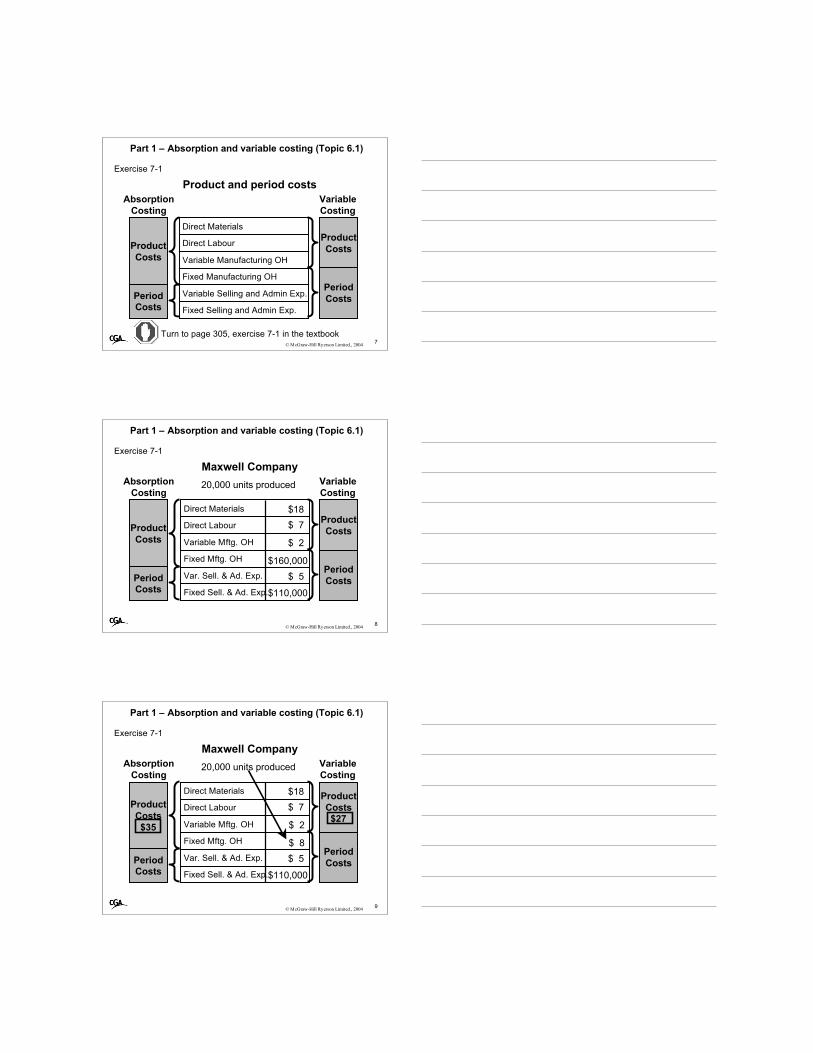

Turn to page 305, exercise 7-1 in the textbook

Exercise 7-1

Part 1 – Absorption and variable costing (Topic 6.1)

8

Direct Materials

Direct Labour

Variable Mftg. OH

Fixed Mftg. OH

Var. Sell. & Ad. Exp.

Fixed Sell. & Ad. Exp.

VariableCosting

AbsorptionCosting

ProductCosts

PeriodCosts

ProductCosts

PeriodCosts

© McGraw-Hill Ryerson Limited., 2004

Maxwell Company

$18$ 7

$ 2

$160,000$ 5

$110,000

20,000 units produced

Exercise 7-1

Part 1 – Absorption and variable costing (Topic 6.1)

9

Direct Materials

Direct Labour

Variable Mftg. OH

Fixed Mftg. OH

Var. Sell. & Ad. Exp.

Fixed Sell. & Ad. Exp.

VariableCosting

AbsorptionCosting

ProductCosts$27

PeriodCosts

ProductCosts$35

PeriodCosts

© McGraw-Hill Ryerson Limited., 2004

Maxwell Company

$18$ 7

$ 2

$ 8$ 5

$110,000

20,000 units produced

Exercise 7-1

10

Part 2

Absorption and variable costingincome statements

Advantages and disadvantages ofabsorption and variable costing

Impact of JIT inventory methodsTopics 6.2-6.4

MA1 – MODULE 6

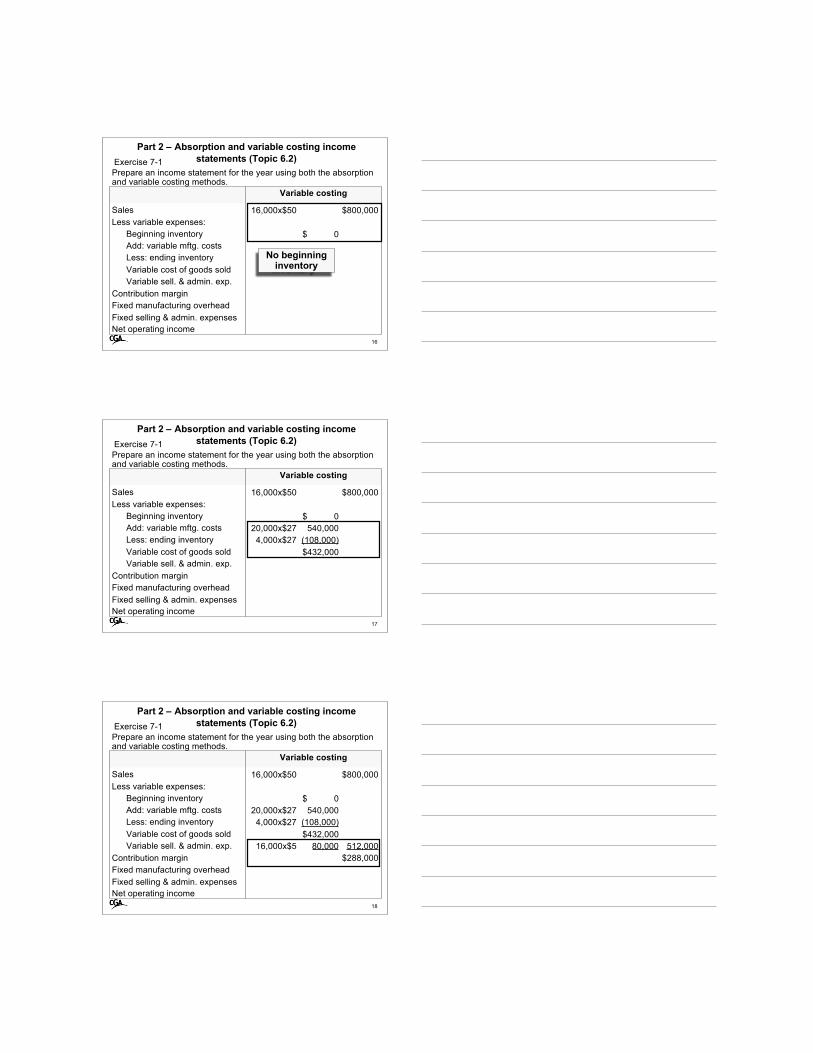

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

Prepare income statements using both absorption and variablecosting, and reconcile the two net income figures by observingthe effect of deferred manufacturing overhead costs. (Level 1)

11

Absorptioncosting

Sales $XXCost of goods sold

Beginning inventory $XXAdd: COGM (DM, DL andvariable and fixed OH)

XX

Less: ending inventory (XX) XXGross margin $XXVariable sell. & admin. XXFixed sell & admin. XXNet operating income $XX

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

Prepare income statements using both absorption and variablecosting, and reconcile the two net income figures by observingthe effect of deferred manufacturing overhead costs. (Level 1)

12

Variable costing

Sales $XXLess variable expenses:

Beginning inventory XXAdd: variable manufacturing costs XXLess: ending inventory (XX)Variable cost of goods sold $XXVariable sell. & admin. expenses XX XX

Contribution margin $XXFixed manufacturing overhead XXFixed selling & admin. expenses XXNet operating income $XX

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

13

Absorption costing

Sales 16,000x$50 $800,000Cost of goods sold

Beginning inventory $ 0Add: COGM (DM, DL andvariable and fixed OH)Less: ending inventory

Gross marginVariable sell. & admin.Fixed sell & admin.Net operating income

Exercise 7-1 Prepare an income statement for the year using both the absorptionand variable costing methods.

No beginninginventory

Turn to page 305, exercise 7-1 in the textbook

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

14

Absorption costing

Sales 16,000x$50 $800,000Cost of goods sold

Beginning inventory $ 0Add: COGM (DM, DL andvariable and fixed OH) 20,000x$35 700,000Less: ending inventory 4,000x$35 (140,000) 560,000

Gross marginVariable sell. & admin.Fixed sell & admin.Net operating income

Exercise 7-1 Prepare an income statement for the year using both the absorptionand variable costing methods.

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

15

Absorption costing

Sales 16,000x$50 $800,000Cost of goods sold

Beginning inventory $ 0Add: COGM (DM, DL andvariable and fixed OH) 20,000x$35 700,000Less: ending inventory 4,000x$35 (140,000) 560,000

Gross margin $240,000Variable sell. & admin. 16,000x$5 80,000Fixed sel.l & admin. 110,000Net operating income $50,000

Exercise 7-1 Prepare an income statement for the year using both the absorptionand variable costing methods.

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

16

Variable costing

Sales 16,000x$50 $800,000Less variable expenses:

Beginning inventory $ 0Add: variable mftg. costsLess: ending inventoryVariable cost of goods soldVariable sell. & admin. exp.

Contribution marginFixed manufacturing overheadFixed selling & admin. expensesNet operating income

Exercise 7-1 Prepare an income statement for the year using both the absorptionand variable costing methods.

No beginninginventory

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

17

Variable costing

Sales 16,000x$50 $800,000Less variable expenses:

Beginning inventory $ 0Add: variable mftg. costs 20,000x$27 540,000Less: ending inventory 4,000x$27 (108,000)Variable cost of goods sold $432,000Variable sell. & admin. exp.

Contribution marginFixed manufacturing overheadFixed selling & admin. expensesNet operating income

Exercise 7-1 Prepare an income statement for the year using both the absorptionand variable costing methods.

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

18

Variable costing

Sales 16,000x$50 $800,000Less variable expenses:

Beginning inventory $ 0Add: variable mftg. costs 20,000x$27 540,000Less: ending inventory 4,000x$27 (108,000)Variable cost of goods sold $432,000Variable sell. & admin. exp. 16,000x$5 80,000 512,000

Contribution margin $288,000Fixed manufacturing overheadFixed selling & admin. expensesNet operating income

Exercise 7-1 Prepare an income statement for the year using both the absorptionand variable costing methods.

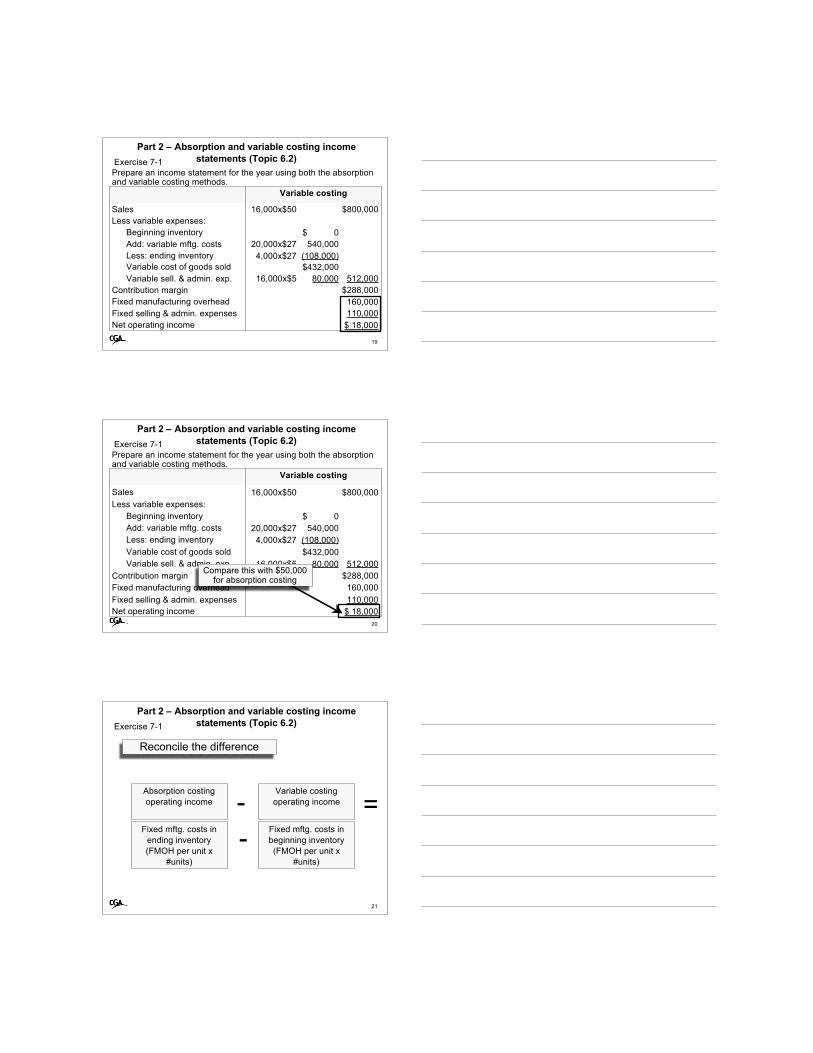

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

19

Variable costing

Sales 16,000x$50 $800,000Less variable expenses:

Beginning inventory $ 0Add: variable mftg. costs 20,000x$27 540,000Less: ending inventory 4,000x$27 (108,000)Variable cost of goods sold $432,000Variable sell. & admin. exp. 16,000x$5 80,000 512,000

Contribution margin $288,000Fixed manufacturing overhead 160,000Fixed selling & admin. expenses 110,000Net operating income $ 18,000

Exercise 7-1 Prepare an income statement for the year using both the absorptionand variable costing methods.

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

20

Variable costing

Sales 16,000x$50 $800,000Less variable expenses:

Beginning inventory $ 0Add: variable mftg. costs 20,000x$27 540,000Less: ending inventory 4,000x$27 (108,000)Variable cost of goods sold $432,000Variable sell. & admin. exp. 16,000x$5 80,000 512,000

Contribution margin $288,000Fixed manufacturing overhead 160,000Fixed selling & admin. expenses 110,000Net operating income $ 18,000

Exercise 7-1 Prepare an income statement for the year using both the absorptionand variable costing methods.

Compare this with $50,000for absorption costing

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

21

Absorption costingoperating income

Variable costingoperating income

Fixed mftg. costs inending inventory(FMOH per unit x

#units)

Fixed mftg. costs inbeginning inventory(FMOH per unit x

#units)

- =-

Reconcile the difference

Exercise 7-1

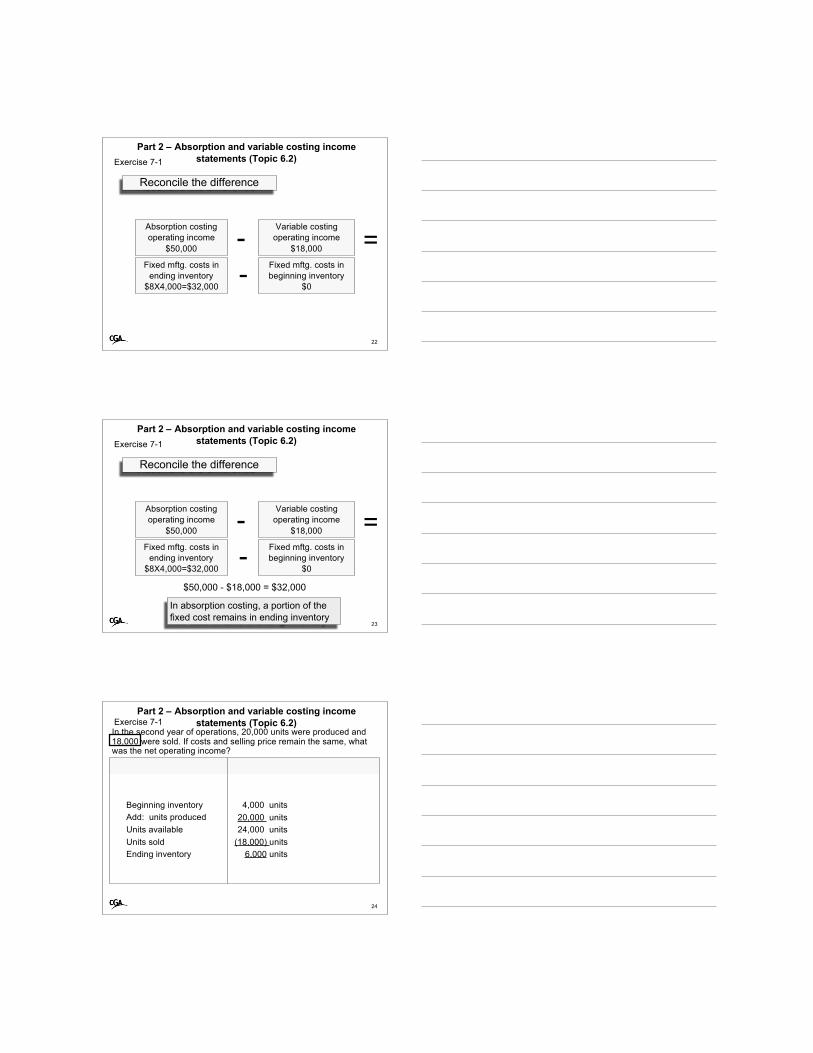

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

22

Absorption costingoperating income

$50,000

Variable costingoperating income

$18,000

Fixed mftg. costs inending inventory

$8X4,000=$32,000

Fixed mftg. costs inbeginning inventory

$0

- =-

Reconcile the difference

Exercise 7-1

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

23

Absorption costingoperating income

$50,000

Variable costingoperating income

$18,000

Fixed mftg. costs inending inventory

$8X4,000=$32,000

Fixed mftg. costs inbeginning inventory

$0

- =-

Reconcile the difference

$50,000 - $18,000 = $32,000

In absorption costing, a portion of thefixed cost remains in ending inventory

Exercise 7-1

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

24

Beginning inventory 4,000 unitsAdd: units produced 20,000 unitsUnits available 24,000 unitsUnits sold (18,000) unitsEnding inventory 6,000 units

Exercise 7-1 In the second year of operations, 20,000 units were produced and18,000 were sold. If costs and selling price remain the same, whatwas the net operating income?

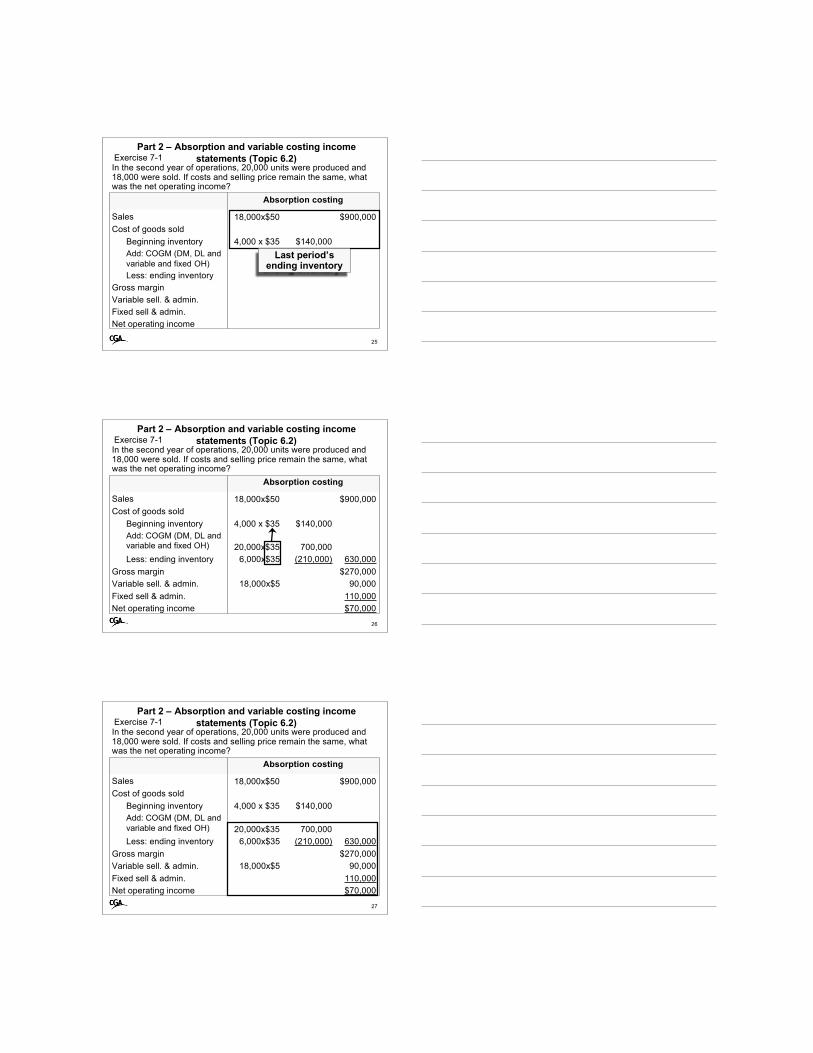

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

25

Absorption costing

Sales 18,000x$50 $900,000Cost of goods sold

Beginning inventory 4,000 x $35 $140,000Add: COGM (DM, DL andvariable and fixed OH)Less: ending inventory

Gross marginVariable sell. & admin.Fixed sell & admin.Net operating income

Exercise 7-1 In the second year of operations, 20,000 units were produced and18,000 were sold. If costs and selling price remain the same, whatwas the net operating income?

Last period’sending inventory

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

26

Absorption costing

Sales 18,000x$50 $900,000Cost of goods sold

Beginning inventory 4,000 x $35 $140,000Add: COGM (DM, DL andvariable and fixed OH) 20,000x$35 700,000Less: ending inventory 6,000x$35 (210,000) 630,000

Gross margin $270,000Variable sell. & admin. 18,000x$5 90,000Fixed sell & admin. 110,000Net operating income $70,000

Exercise 7-1 In the second year of operations, 20,000 units were produced and18,000 were sold. If costs and selling price remain the same, whatwas the net operating income?

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

27

Absorption costing

Sales 18,000x$50 $900,000Cost of goods sold

Beginning inventory 4,000 x $35 $140,000Add: COGM (DM, DL andvariable and fixed OH) 20,000x$35 700,000Less: ending inventory 6,000x$35 (210,000) 630,000

Gross margin $270,000Variable sell. & admin. 18,000x$5 90,000Fixed sell & admin. 110,000Net operating income $70,000

Exercise 7-1 In the second year of operations, 20,000 units were produced and18,000 were sold. If costs and selling price remain the same, whatwas the net operating income?

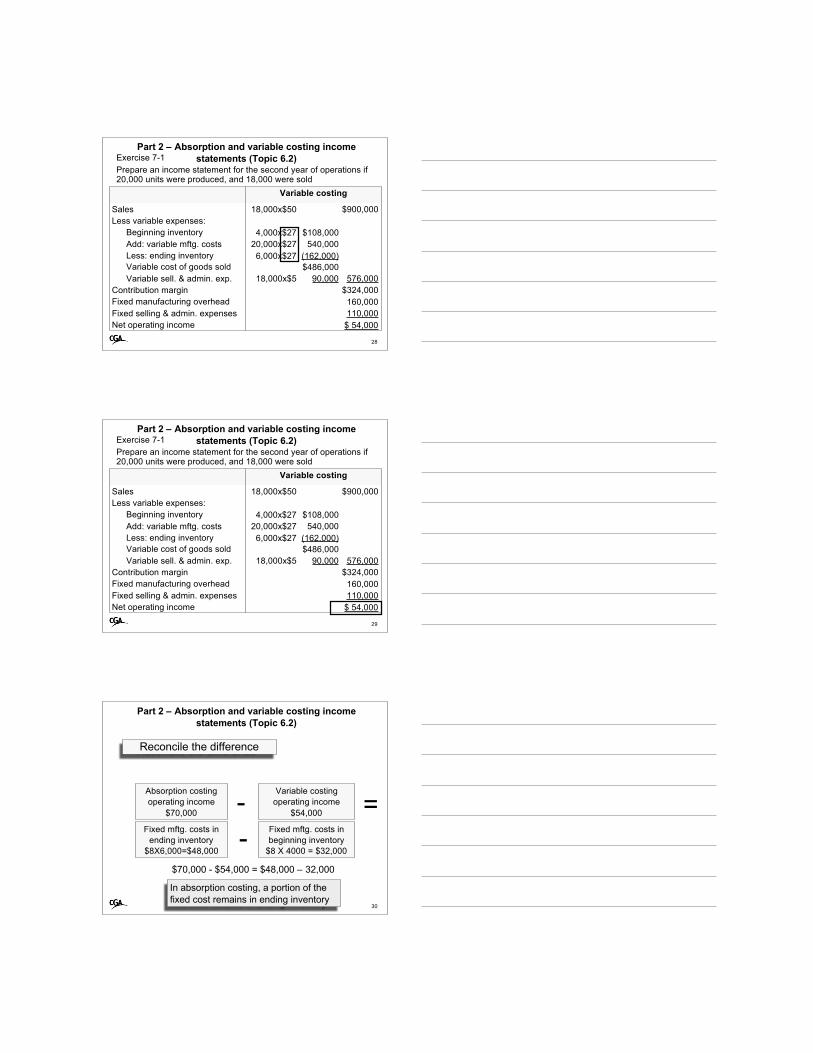

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

28

Variable costing

Sales 18,000x$50 $900,000Less variable expenses:

Beginning inventory 4,000x$27 $108,000Add: variable mftg. costs 20,000x$27 540,000Less: ending inventory 6,000x$27 (162,000)Variable cost of goods sold $486,000Variable sell. & admin. exp. 18,000x$5 90,000 576,000

Contribution margin $324,000Fixed manufacturing overhead 160,000Fixed selling & admin. expenses 110,000Net operating income $ 54,000

Exercise 7-1 Prepare an income statement for the second year of operations if20,000 units were produced, and 18,000 were sold

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

29

Variable costing

Sales 18,000x$50 $900,000Less variable expenses:

Beginning inventory 4,000x$27 $108,000Add: variable mftg. costs 20,000x$27 540,000Less: ending inventory 6,000x$27 (162,000)Variable cost of goods sold $486,000Variable sell. & admin. exp. 18,000x$5 90,000 576,000

Contribution margin $324,000Fixed manufacturing overhead 160,000Fixed selling & admin. expenses 110,000Net operating income $ 54,000

Exercise 7-1 Prepare an income statement for the second year of operations if20,000 units were produced, and 18,000 were sold

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

30

Absorption costingoperating income

$70,000

Variable costingoperating income

$54,000

Fixed mftg. costs inending inventory

$8X6,000=$48,000

Fixed mftg. costs inbeginning inventory

$8 X 4000 = $32,000

- =-

Reconcile the difference

$70,000 - $54,000 = $48,000 – 32,000

In absorption costing, a portion of thefixed cost remains in ending inventory

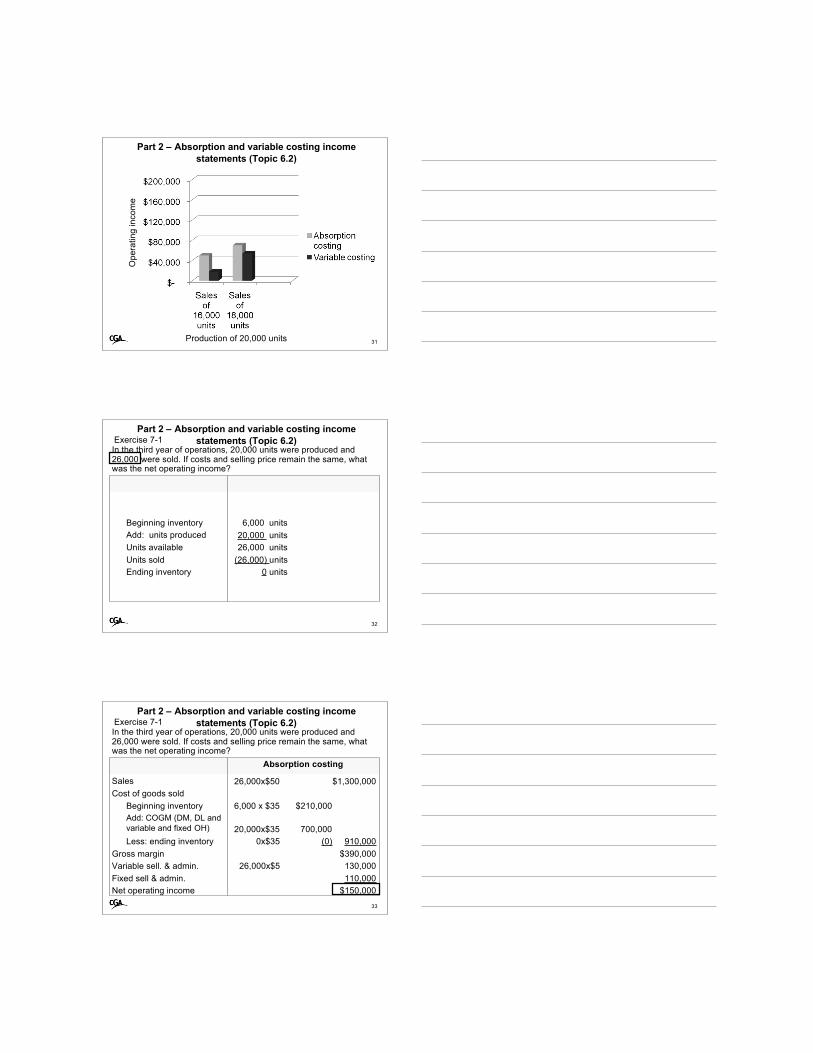

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

31

Ope

ratin

g in

com

e

Production of 20,000 units

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

32

Exercise 7-1 In the third year of operations, 20,000 units were produced and26,000 were sold. If costs and selling price remain the same, whatwas the net operating income?

Beginning inventory 6,000 unitsAdd: units produced 20,000 unitsUnits available 26,000 unitsUnits sold (26,000) unitsEnding inventory 0 units

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

33

Absorption costing

Sales 26,000x$50 $1,300,000Cost of goods sold

Beginning inventory 6,000 x $35 $210,000Add: COGM (DM, DL andvariable and fixed OH) 20,000x$35 700,000Less: ending inventory 0x$35 (0) 910,000

Gross margin $390,000Variable sell. & admin. 26,000x$5 130,000Fixed sell & admin. 110,000Net operating income $150,000

Exercise 7-1 In the third year of operations, 20,000 units were produced and26,000 were sold. If costs and selling price remain the same, whatwas the net operating income?

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

34

Variable costing

Sales 26,000x$50 $1,300,000Less variable expenses:

Beginning inventory 6,000x$27 $162,000Add: variable mftg. costs 20,000x$27 540,000Less: ending inventory 0x$27 (0)Variable cost of goods sold $702,000Variable sell. & admin. exp. 26,000x$5 130,000 832,000

Contribution margin $468,000Fixed manufacturing overhead 160,000Fixed selling & admin. expenses 110,000Net operating income $ 198,000

Exercise 7-1 Prepare an income statement for the second year of operations if20,000 units were produced, and 18,000 were sold

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

35

Ope

ratin

g in

com

e

Production of 20,000 units

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

36

Ope

ratin

g in

com

e

Production of 20,000 units

When sales < productionabsorption costing

reports higher income.WHY?

Ending inventory storesfixed costs

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

37

Ope

ratin

g in

com

e

Production of 20,000 units

When sales > productionabsorption costing

reports lower income.WHY?

Fixed costs stored inending inventory arereleased to COGS

Part 2 – Absorption and variable costing incomestatements (Topic 6.2)

38

Ope

ratin

g in

com

e

Production of 20,000 units

Part 2 – Advantages and disadvantages of absorptionand variable costing (Topic 6.3)

Explain the advantages and limitations of both the absorptionand variable costing methods. (Level 1)

39

•Accepted standard forexternal reporting

•Focus on full costing

Absorptioncosting

Variablecosting

•Useful for CVP analysis•Fixed costs do notappear to be variable

•Profit is not affected byinventory levels

•Operating income iscloser to cash flows andsales

Part 2 – Impact of JIT inventory methods (Topic 6.4)Explain how the use of JIT inventory methods decrease oreliminates the difference in net income reported under theabsorption and variable costing methods. (Level 1)

40

•The main issue with absorption costing is theeffect of fixed costs stored in ending inventory

•Just in time (JIT) inventory attempts to minimizeinventory on hand

•In a JIT environment absorption and variablecosting methods will show approximately thesame operating income

41

Part 3

Basic framework ofbudgeting

Prepare the masterbudget

Topics 6.5-6.7

MA1 – MODULE 6

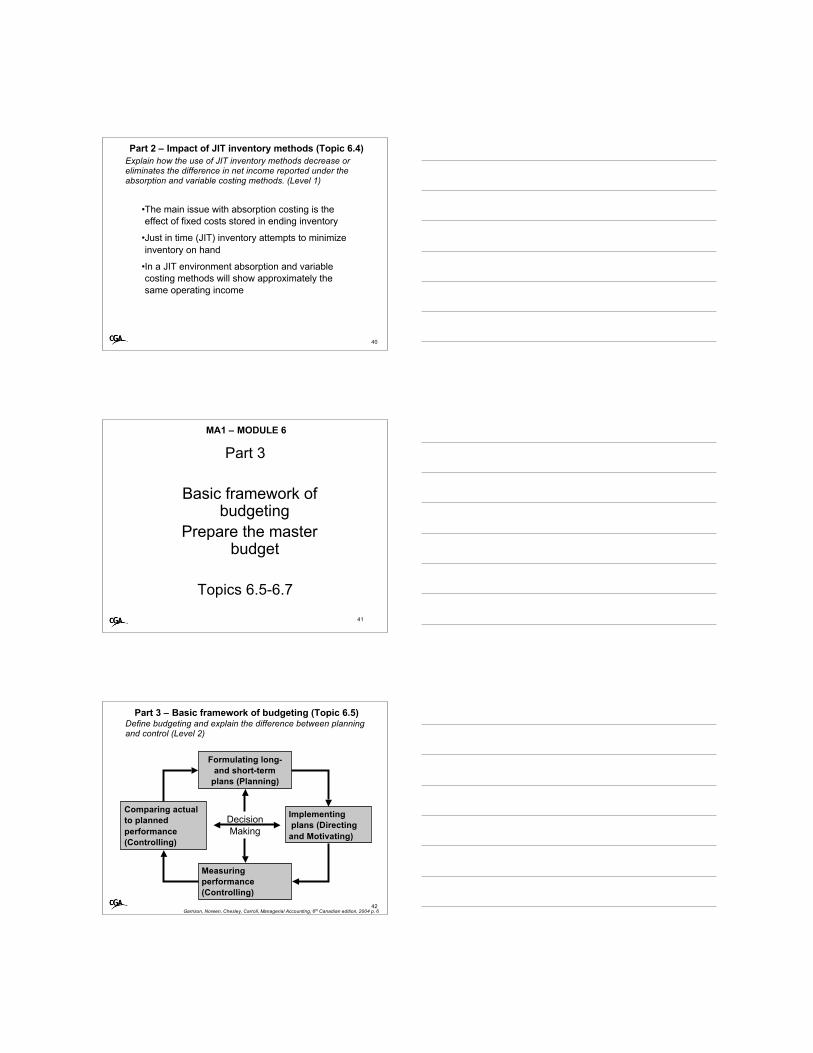

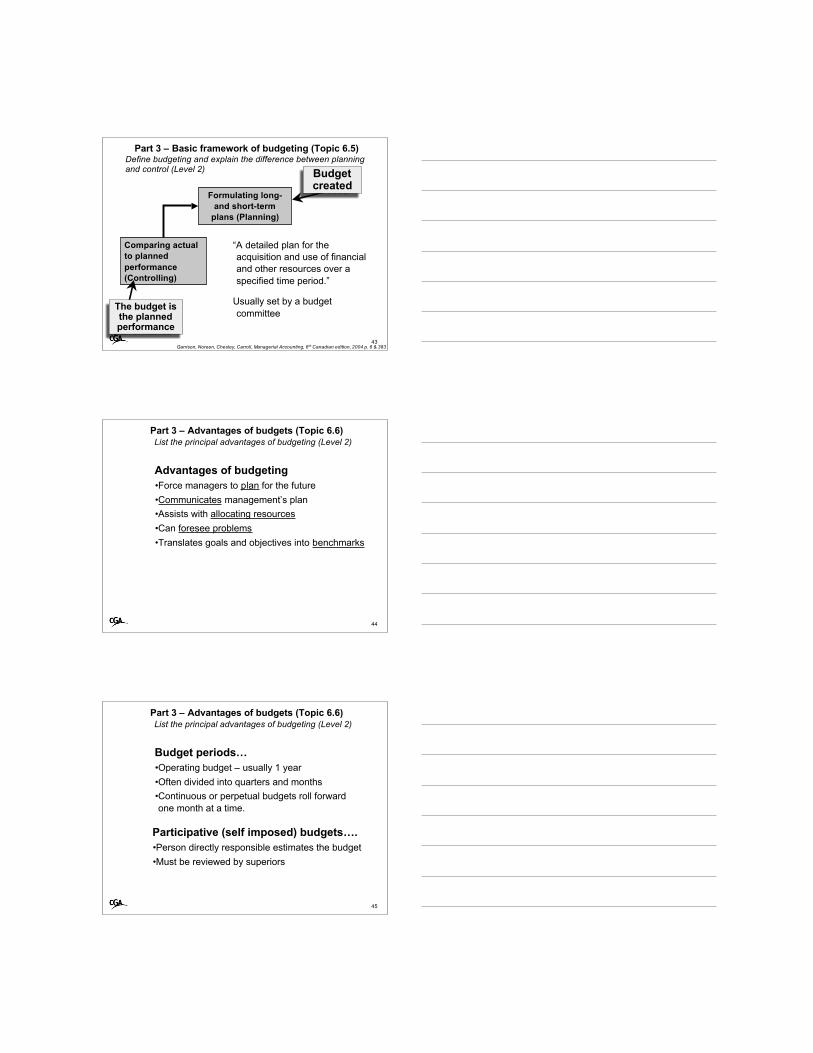

Part 3 – Basic framework of budgeting (Topic 6.5)Define budgeting and explain the difference between planningand control (Level 2)

42

DecisionMaking

Formulating long-and short-term

plans (Planning)

Measuringperformance(Controlling)

Implementing plans (Directingand Motivating)

Comparing actualto plannedperformance(Controlling)

Garrison, Noreen, Chesley, Carroll, Managerial Accounting, 6th Canadian edition, 2004 p. 6

Part 3 – Basic framework of budgeting (Topic 6.5)Define budgeting and explain the difference between planningand control (Level 2)

43

Formulating long-and short-term

plans (Planning)

Comparing actualto plannedperformance(Controlling)

Garrison, Noreen, Chesley, Carroll, Managerial Accounting, 6th Canadian edition, 2004 p. 6 & 383

Budgetcreated

The budget isthe plannedperformance

“A detailed plan for theacquisition and use of financialand other resources over aspecified time period.”

Usually set by a budgetcommittee

Part 3 – Advantages of budgets (Topic 6.6)List the principal advantages of budgeting (Level 2)

44

Advantages of budgeting•Force managers to plan for the future•Communicates management’s plan•Assists with allocating resources•Can foresee problems•Translates goals and objectives into benchmarks

Part 3 – Advantages of budgets (Topic 6.6)List the principal advantages of budgeting (Level 2)

45

Budget periods…•Operating budget – usually 1 year•Often divided into quarters and months•Continuous or perpetual budgets roll forwardone month at a time.

Participative (self imposed) budgets….•Person directly responsible estimates the budget•Must be reviewed by superiors

46

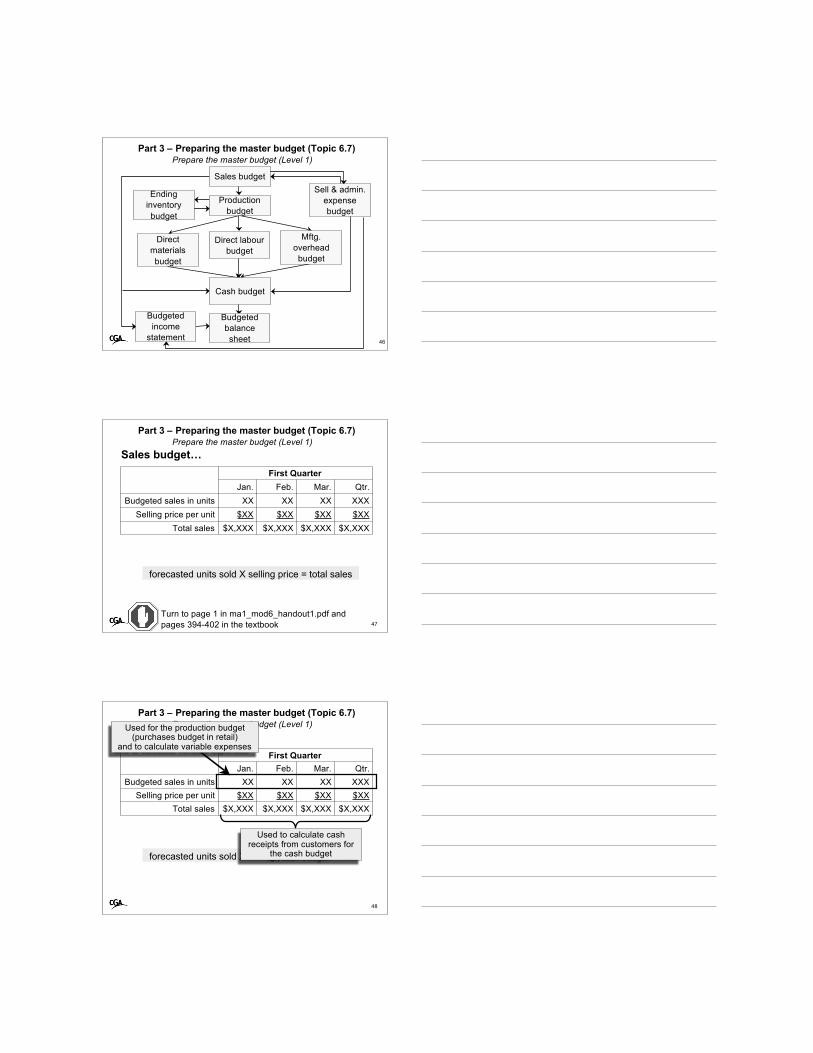

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

Sell & admin.expensebudget

Mftg.overheadbudget

Endinginventorybudget

Directmaterialsbudget

Budgetedincome

statement

Direct labourbudget

Productionbudget

Cash budget

Budgetedbalancesheet

Sales budget

47

forecasted units sold X selling price = total sales

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

Sales budget…First Quarter

Jan. Feb. Mar. Qtr.Budgeted sales in units XX XX XX XXX

Selling price per unit $XX $XX $XX $XXTotal sales $X,XXX $X,XXX $X,XXX $X,XXX

Turn to page 1 in ma1_mod6_handout1.pdf andpages 394-402 in the textbook

48

Sales budget…First Quarter

Jan. Feb. Mar. Qtr.Budgeted sales in units XX XX XX XXX

Selling price per unit $XX $XX $XX $XXTotal sales $X,XXX $X,XXX $X,XXX $X,XXX

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

forecasted units sold X selling price = total sales

Used to calculate cashreceipts from customers for

the cash budget

Used for the production budget(purchases budget in retail)

and to calculate variable expenses

First QuarterJan. Feb. Mar. Qtr.

Budgeted sales in units 400 500 700 1,600Add: desired ending inventory 200 260 155 155

Total needs 600 760 855 1,755Less: beginning inventory (170) (200) (260) (170)

Required production 430 560 595 1,585

Production budget…

Budgeted sales + desired ending inventory –beginning inventory= required production

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

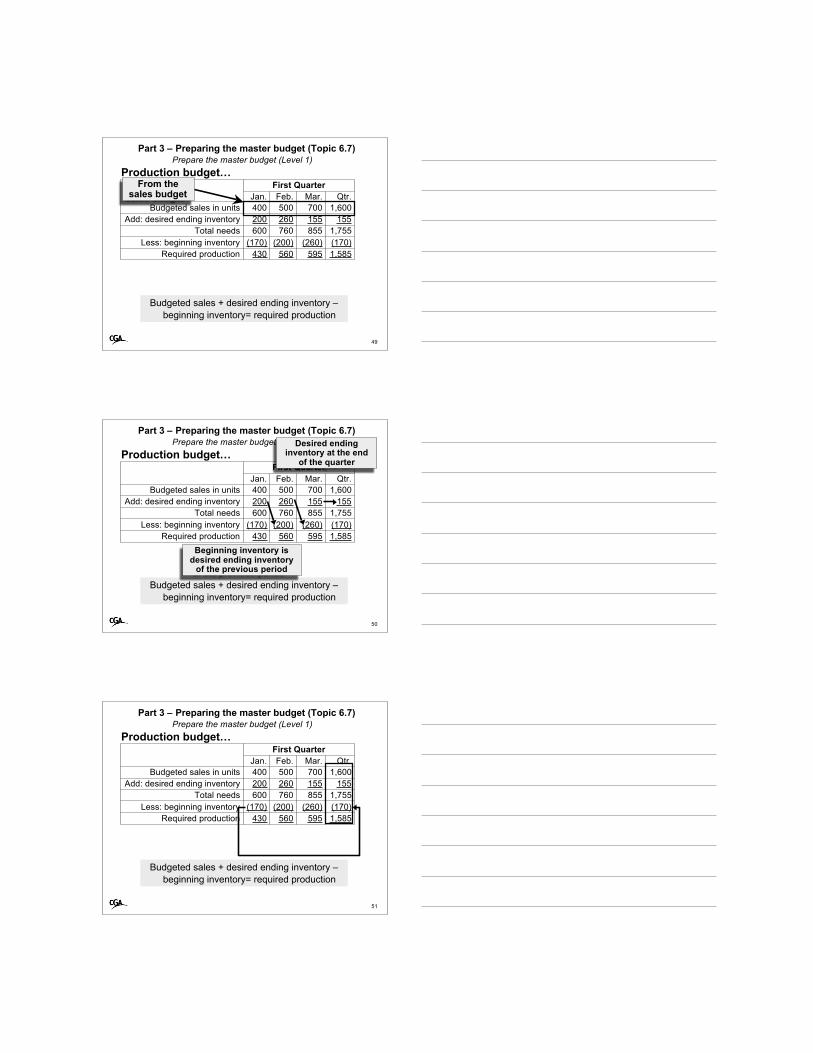

49

From thesales budget

First QuarterJan. Feb. Mar. Qtr.

Budgeted sales in units 400 500 700 1,600Add: desired ending inventory 200 260 155 155

Total needs 600 760 855 1,755Less: beginning inventory (170) (200) (260) (170)

Required production 430 560 595 1,585

Production budget…

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

50

Desired endinginventory at the end

of the quarter

Budgeted sales + desired ending inventory –beginning inventory= required production

Beginning inventory isdesired ending inventory

of the previous period

First QuarterJan. Feb. Mar. Qtr.

Budgeted sales in units 400 500 700 1,600Add: desired ending inventory 200 260 155 155

Total needs 600 760 855 1,755Less: beginning inventory (170) (200) (260) (170)

Required production 430 560 595 1,585

Production budget…

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

51

Budgeted sales + desired ending inventory –beginning inventory= required production

Production budget…

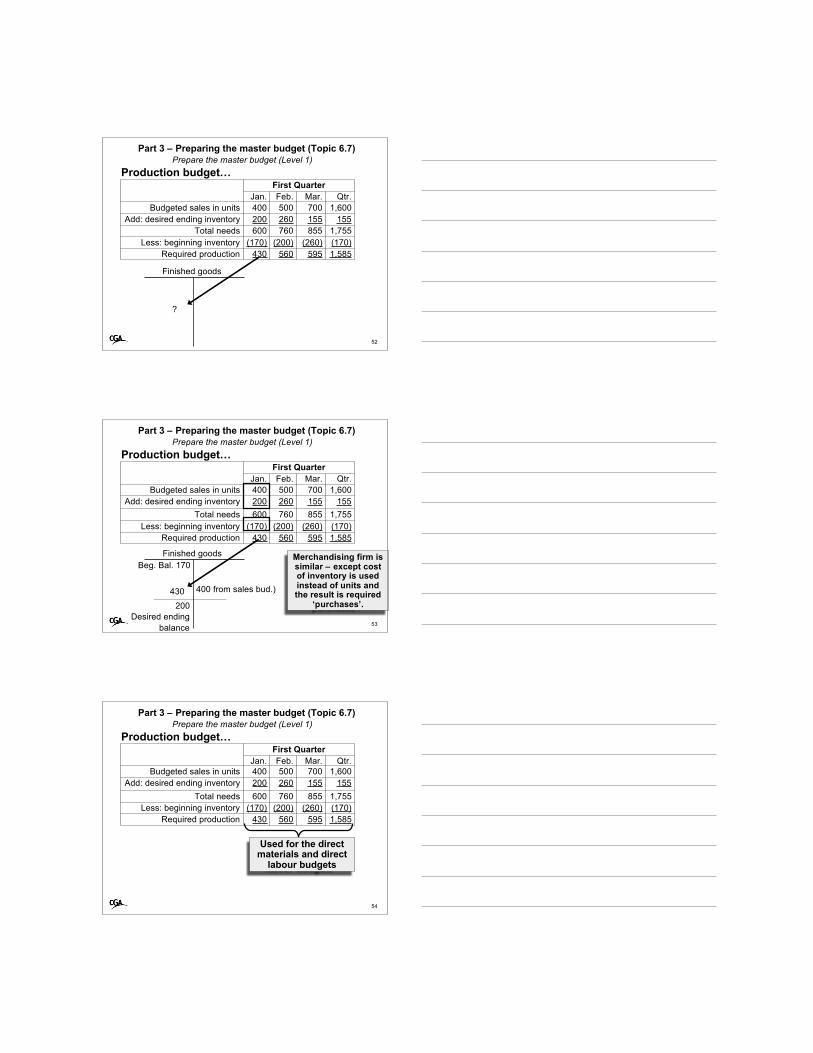

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

?

Finished goods

52

First QuarterJan. Feb. Mar. Qtr.

Budgeted sales in units 400 500 700 1,600Add: desired ending inventory 200 260 155 155

Total needs 600 760 855 1,755Less: beginning inventory (170) (200) (260) (170)

Required production 430 560 595 1,585

Production budget…

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

Merchandising firm issimilar – except costof inventory is usedinstead of units andthe result is required

‘purchases’.

Beg. Bal. 170

200Desired ending

balance

400 from sales bud.)430

Finished goods

53

First QuarterJan. Feb. Mar. Qtr.

Budgeted sales in units 400 500 700 1,600Add: desired ending inventory 200 260 155 155

Total needs 600 760 855 1,755Less: beginning inventory (170) (200) (260) (170)

Required production 430 560 595 1,585

Production budget…

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

54

Used for the directmaterials and direct

labour budgets

First QuarterJan. Feb. Mar. Qtr.

Budgeted sales in units 400 500 700 1,600Add: desired ending inventory 200 260 155 155

Total needs 600 760 855 1,755Less: beginning inventory (170) (200) (260) (170)

Required production 430 560 595 1,585

Direct materials budget…First Quarter

Jan. Feb. Mar. Qtr.Units to be produced XX XX XX XXX

Raw materials per unit X X X XProduction needs XX XX XX XXX

Add: desired ending inventory XX XX XX XXTotal needs XXX XXX XXX XXX

Less: beginning inventory (XX) (XX) (XX) (XX)Raw materials to purchase XX XX XX XX

Cost per unit of raw materials $X $X $X $XTotal cost for units purchased $XXX $XXX $XXX $XXX

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

55

From the productionbudget

(Units to produce x raw materials per unit) +desired ending inventory – beginninginventory = raw materials to purchase

Direct materials budget…First Quarter

Jan. Feb. Mar. Qtr.Units to be produced XX XX XX XXX

Raw materials per unit X X X XProduction needs XX XX XX XXX

Add: desired ending inventory XX XX XX XXTotal needs XXX XXX XXX XXX

Less: beginning inventory (XX) (XX) (XX) (XX)Raw materials to purchase XX XX XX XX

Cost per unit of raw materials $X $X $X $X Total cost for units purchased $XXX $XXX $XXX $XXX

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

56

Used for the cashbudget

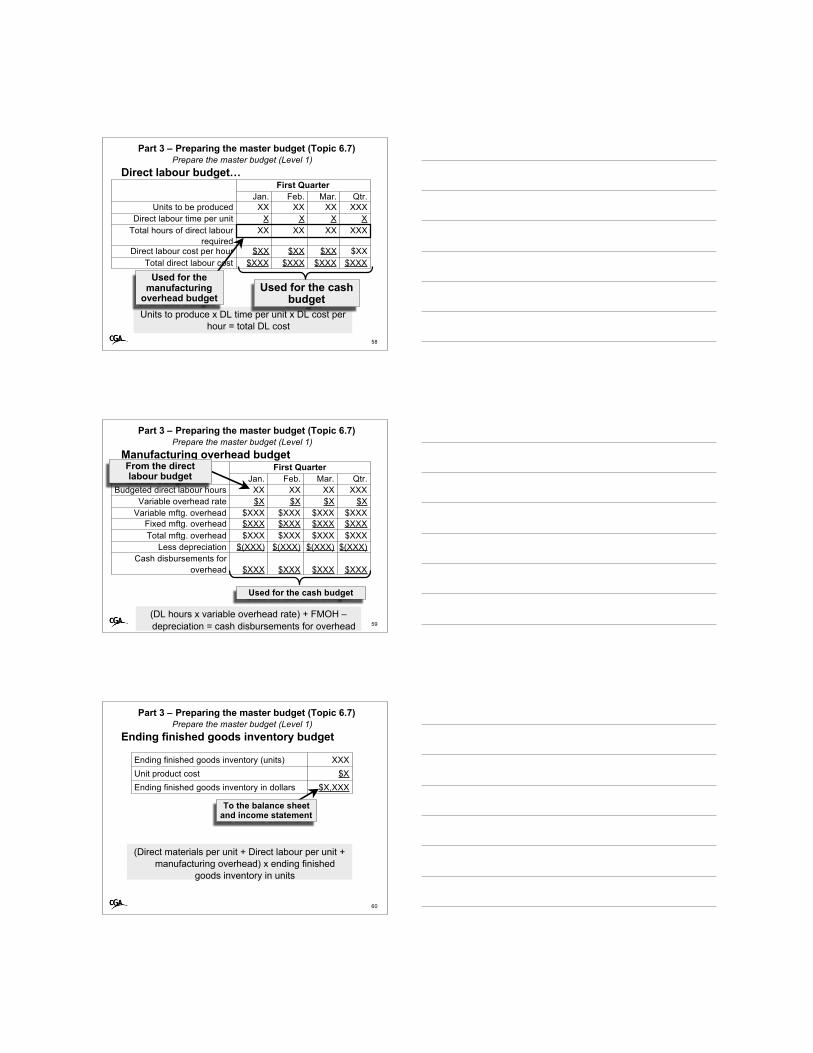

Direct labour budget…First Quarter

Jan. Feb. Mar. Qtr.Units to be produced XX XX XX XXX

Direct labour time per unit X X X XTotal hours of direct labour

requiredXX XX XX XXX

Direct labour cost per hour $XX $XX $XX $XXTotal direct labour cost $XXX $XXX $XXX $XXX

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

57

From the productionbudget

Units to produce x DL time per unit x DL cost perhour = total DL cost

Units to produce x DL time per unit x DL cost perhour = total DL cost

Direct labour budget…First Quarter

Jan. Feb. Mar. Qtr.Units to be produced XX XX XX XXX

Direct labour time per unit X X X XTotal hours of direct labour

requiredXX XX XX XXX

Direct labour cost per hour $XX $XX $XX $XXTotal direct labour cost $XXX $XXX $XXX $XXX

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

58

Used for the cashbudget

Used for themanufacturing

overhead budget

Manufacturing overhead budgetFirst Quarter

Jan. Feb. Mar. Qtr.Budgeted direct labour hours XX XX XX XXX

Variable overhead rate $X $X $X $XVariable mftg. overhead $XXX $XXX $XXX $XXX

Fixed mftg. overhead $XXX $XXX $XXX $XXXTotal mftg. overhead $XXX $XXX $XXX $XXX

Less depreciation $(XXX) $(XXX) $(XXX) $(XXX)Cash disbursements for

overhead $XXX $XXX $XXX $XXX

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

59

From the directlabour budget

(DL hours x variable overhead rate) + FMOH –depreciation = cash disbursements for overhead

Used for the cash budget

Ending finished goods inventory budget

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

60

(Direct materials per unit + Direct labour per unit +manufacturing overhead) x ending finished

goods inventory in units

Ending finished goods inventory (units) XXXUnit product cost $XEnding finished goods inventory in dollars $X,XXX

To the balance sheetand income statement

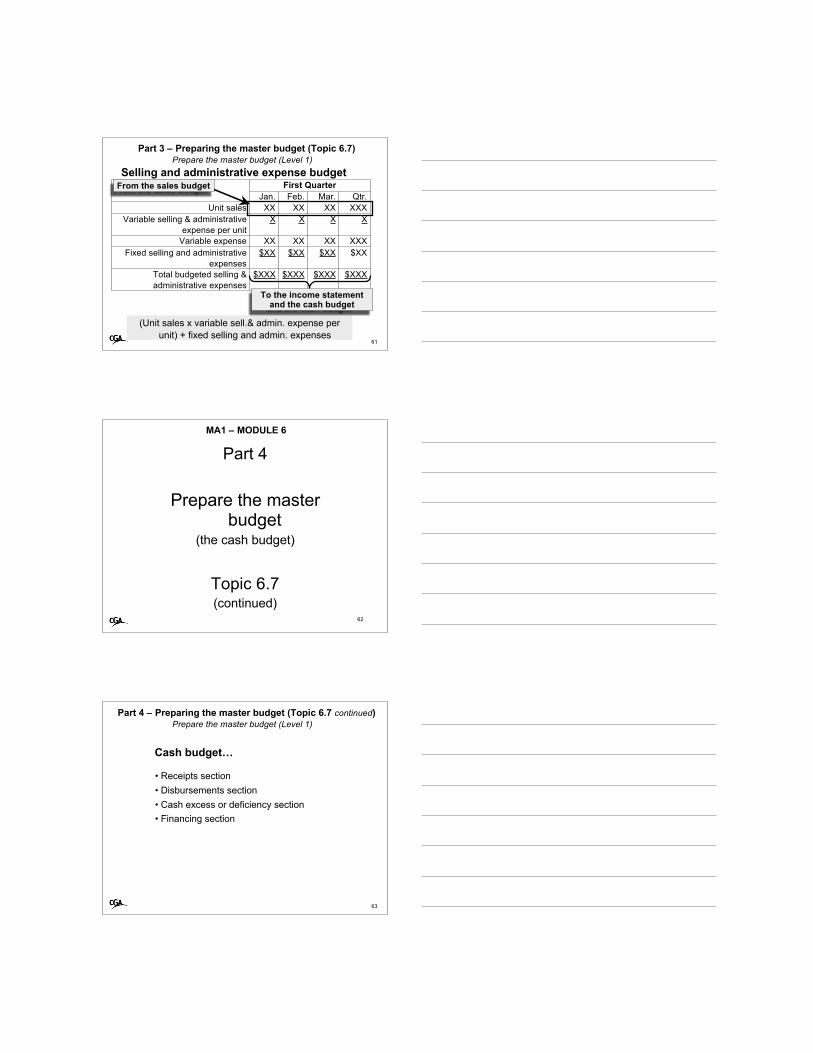

Selling and administrative expense budget

Part 3 – Preparing the master budget (Topic 6.7)Prepare the master budget (Level 1)

61

(Unit sales x variable sell.& admin. expense perunit) + fixed selling and admin. expenses

First QuarterJan. Feb. Mar. Qtr.

Unit sales XX XX XX XXXVariable selling & administrative

expense per unitX X X X

Variable expense XX XX XX XXXFixed selling and administrative

expenses$XX $XX $XX $XX

Total budgeted selling &administrative expenses

$XXX $XXX $XXX $XXX

To the income statementand the cash budget

From the sales budget

62

Part 4

Prepare the masterbudget

(the cash budget)

Topic 6.7(continued)

MA1 – MODULE 6

63

Cash budget…

• Receipts section• Disbursements section• Cash excess or deficiency section• Financing section

Part 4 – Preparing the master budget (Topic 6.7 continued)Prepare the master budget (Level 1)

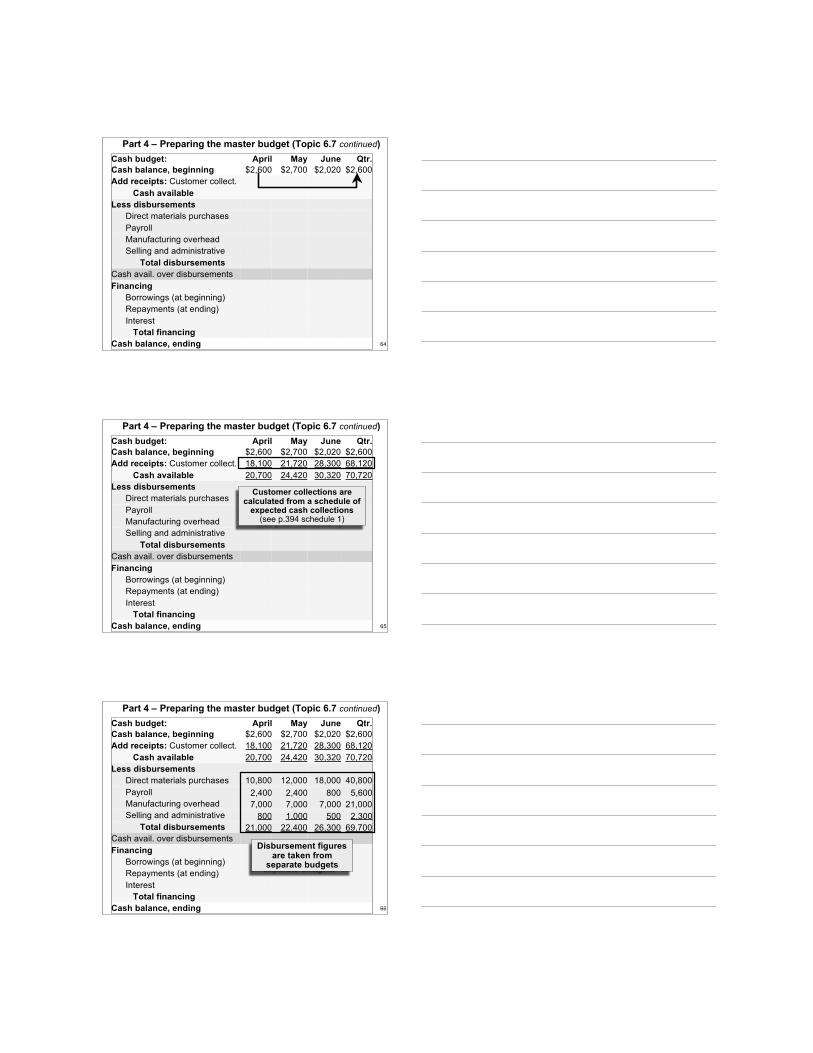

Cash budget: April May June Qtr.Cash balance, beginning $2,600 $2,700 $2,020 $2,600Add receipts: Customer collect.

Cash availableLess disbursements

Direct materials purchasesPayrollManufacturing overheadSelling and administrative

Total disbursementsCash avail. over disbursementsFinancing

Borrowings (at beginning)Repayments (at ending)Interest Total financing

Cash balance, ending 64

Part 4 – Preparing the master budget (Topic 6.7 continued)

Cash budget: April May June Qtr.Cash balance, beginning $2,600 $2,700 $2,020 $2,600Add receipts: Customer collect. 18,100 21,720 28,300 68,120

Cash available 20,700 24,420 30,320 70,720Less disbursements

Direct materials purchasesPayrollManufacturing overheadSelling and administrative

Total disbursementsCash avail. over disbursementsFinancing

Borrowings (at beginning)Repayments (at ending)Interest Total financing

Cash balance, ending

Customer collections arecalculated from a schedule of

expected cash collections(see p.394 schedule 1)

65

Part 4 – Preparing the master budget (Topic 6.7 continued)

Cash budget: April May June Qtr.Cash balance, beginning $2,600 $2,700 $2,020 $2,600Add receipts: Customer collect. 18,100 21,720 28,300 68,120

Cash available 20,700 24,420 30,320 70,720Less disbursements

Direct materials purchases 10,800 12,000 18,000 40,800Payroll 2,400 2,400 800 5,600Manufacturing overhead 7,000 7,000 7,000 21,000Selling and administrative 800 1,000 500 2,300

Total disbursements 21,000 22,400 26,300 69,700Cash avail. over disbursementsFinancing

Borrowings (at beginning)Repayments (at ending)Interest Total financing

Cash balance, ending 66

Part 4 – Preparing the master budget (Topic 6.7 continued)

Disbursement figuresare taken from

separate budgets

Cash budget: April May June Qtr.Cash balance, beginning $2,600 $2,700 $2,020 $2,600Add receipts: Customer collect. 18,100 21,720 28,300 68,120

Cash available 20,700 24,420 30,320 70,720Less disbursements

Direct materials purchases 10,800 12,000 18,000 40,800Payroll 2,400 2,400 800 5,600Manufacturing overhead 7,000 7,000 7,000 21,000Selling and administrative 800 1,000 500 2,300

Total disbursements 21,000 22,400 26,300 69,700Cash avail. over disbursements (300) 2,020 4,020 1,020Financing

Borrowings (at beginning)Repayments (at ending)Interest Total financing

Cash balance, ending 67

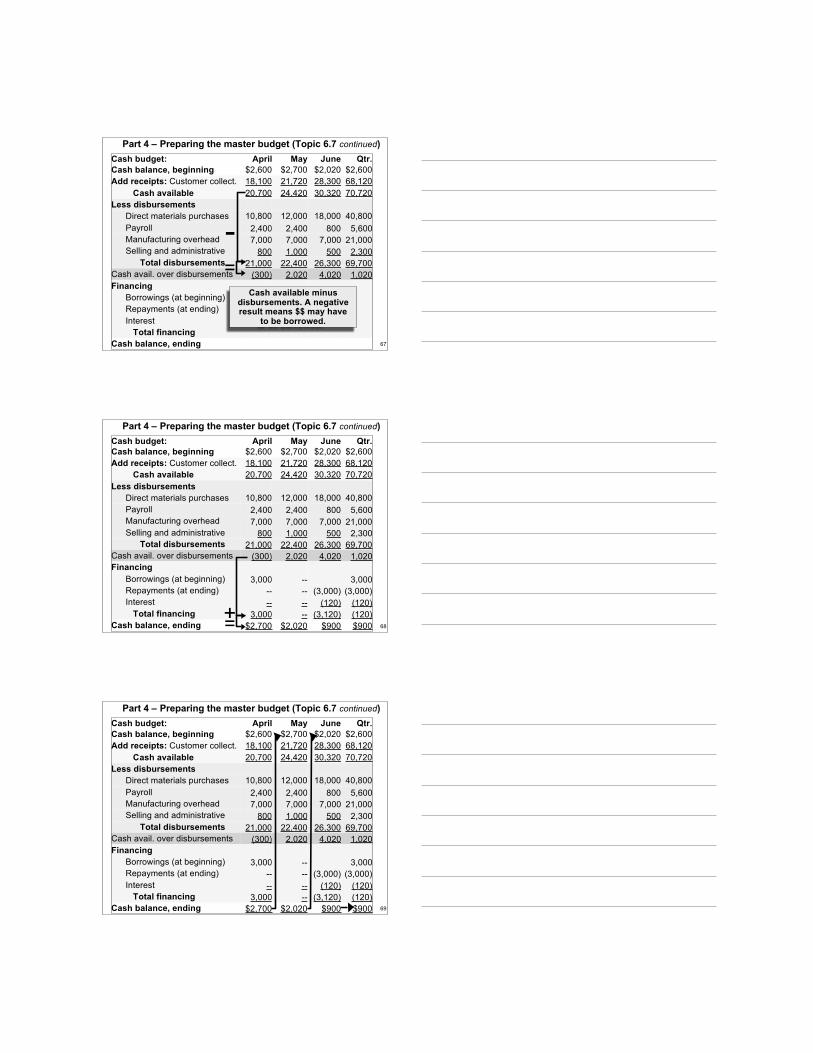

Part 4 – Preparing the master budget (Topic 6.7 continued)

-=

Cash available minusdisbursements. A negativeresult means $$ may have

to be borrowed.

Cash budget: April May June Qtr.Cash balance, beginning $2,600 $2,700 $2,020 $2,600Add receipts: Customer collect. 18,100 21,720 28,300 68,120

Cash available 20,700 24,420 30,320 70,720Less disbursements

Direct materials purchases 10,800 12,000 18,000 40,800Payroll 2,400 2,400 800 5,600Manufacturing overhead 7,000 7,000 7,000 21,000Selling and administrative 800 1,000 500 2,300

Total disbursements 21,000 22,400 26,300 69,700Cash avail. over disbursements (300) 2,020 4,020 1,020Financing

Borrowings (at beginning) 3,000 -- 3,000Repayments (at ending) -- -- (3,000) (3,000)Interest -- -- (120) (120) Total financing 3,000 -- (3,120) (120)

Cash balance, ending $2,700 $2,020 $900 $900 68

Part 4 – Preparing the master budget (Topic 6.7 continued)

+=

Cash budget: April May June Qtr.Cash balance, beginning $2,600 $2,700 $2,020 $2,600Add receipts: Customer collect. 18,100 21,720 28,300 68,120

Cash available 20,700 24,420 30,320 70,720Less disbursements

Direct materials purchases 10,800 12,000 18,000 40,800Payroll 2,400 2,400 800 5,600Manufacturing overhead 7,000 7,000 7,000 21,000Selling and administrative 800 1,000 500 2,300

Total disbursements 21,000 22,400 26,300 69,700Cash avail. over disbursements (300) 2,020 4,020 1,020Financing

Borrowings (at beginning) 3,000 -- 3,000Repayments (at ending) -- -- (3,000) (3,000)Interest -- -- (120) (120) Total financing 3,000 -- (3,120) (120)

Cash balance, ending $2,700 $2,020 $900 $900 69

Part 4 – Preparing the master budget (Topic 6.7 continued)

70

Budgeted income statement andbalance sheet

•Same format as actual statements•Income statement is based on the operatingbudgets

•Balance sheet is based on the current balancesheet data and then adjusted with the data fromthe other operating budgets.

Part 4 – Preparing the master budget (Topic 6.7 continued)

71

Part 5

Review question:Variable and absorption costing

income statements

(download the additional questions handout: ma1_mod6_handout1.pdf)

MA1 – MODULE 6

72

Question 4 March, 2005Handout pages 2 thru 3

a) Prepare in good form a variable costing incomestatement

b) Prepare in good form an absorption costing formatincome statement

c) Prepare a schedule reconciling the net incomes

Part 5 – Review question: Variable and absorptioncosting income statements

Stop the audio, read and attempt thequestion in the handout then come back tolisten to the solution.

73

Question 4 March, 2005Handout pages 2 thru 3

a) Prepare in good form a variable costing incomestatement

b) Prepare in good form an absorption costing formatincome statement

c) Prepare a schedule reconciling the net incomes

Part 5 – Review question: Variable and absorptioncosting income statements

74

Question 4 March, 2005Handout pages 2 thru 3

a) Prepare in good form a variable costing incomestatement

b) Prepare in good form an absorption costing formatincome statement

c) Prepare a schedule reconciling the net incomes

Part 5 – Review question: Variable and absorptioncosting income statements

75

Part 6

Review question:Variable and absorption costing

calculations

(download the additional questions handout: ma1_mod6_handout1.pdf)

MA1 – MODULE 6

76

Question 2 June, 2003Handout pages 4 thru 5

a) Calculate the units sold in fiscal 2002b) Calculate the total contribution margin under

variable costingc) Calculate the gross margin under absorption

costingd) Calculate the cost per unit sold under variable

costinge) Calculate the cost per unit sold under absorption

costing

Part 6 – Review question: Variable and absorptioncosting calculations

Stop the audio, read and attempt thequestion in the handout then come back tolisten to the solution.

77

Question 2 June, 2003Handout pages 4 thru 5

a) Calculate the units sold in fiscal 2002b) Calculate the total contribution margin under

variable costingc) Calculate the gross margin under absorption

costingd) Calculate the cost per unit sold under variable

costinge) Calculate the cost per unit sold under absorption

costing

Part 6 – Review question: Variable and absorptioncosting calculations

78

Question 2 June, 2003Handout pages 4 thru 5

a) Calculate the units sold in fiscal 2002b) Calculate the total contribution margin under

variable costingc) Calculate the gross margin under absorption

costingd) Calculate the cost per unit sold under variable

costinge) Calculate the cost per unit sold under absorption

costing

Part 6 – Review question: Variable and absorptioncosting calculations

79

Question 2 June, 2003Handout pages 4 thru 5

a) Calculate the units sold in fiscal 2002b) Calculate the total contribution margin under

variable costingc) Calculate the gross margin under absorption

costingd) Calculate the cost per unit sold under variable

costinge) Calculate the cost per unit sold under absorption

costing

Part 6 – Review question: Variable and absorptioncosting calculations

80

Part 7

Review questions:Cash collection schedule

Production budget

(download the additional questions handout: ma1_mod6_handout1.pdf)

MA1 – MODULE 6

81

Exercise 9-1 p. 410Handout page 6

1. Prepare a schedule of expected cash collectionsfrom sales by month and in total for the thirdquarter

2. Assume that the company will prepare a budgetedbalance sheet as of September 30. Compute theaccounts receivable as of that date.

Part 7 – Review question: Cash collection schedule,production budget

Stop the audio, read and attempt thequestion in the textbook then come back tolisten to the solution.

82

Exercise 9-2 p. 410Handout page 6

1. Prepare a production budget for the third quartershowing the number of units to be produced eachmonth and for the quarter in total

Part 7 – Review question: Cash collection schedule,production budget

83

Part 8

Review question:Cost of purchases and cash

budget

(download the additional questions handout: ma1_mod6_handout1.pdf)

MA1 – MODULE 6

84

Question 5 March, 2004Handout pages 7 thru 8

a. Prepare a cost of purchases schedule for Octoberand November

b. Prepare the cash budgets for October andNovember including the effects of financing

Part 8 – Review question: Cost of purchases and cashbudget

Stop the audio, read and attempt thequestion in the handout then come back tolisten to the solution.

85

Question 5 March, 2004Handout pages 7 thru 8

a. Prepare a cost of purchases schedule for Octoberand November

b. Prepare the cash budgets for October andNovember including the effects of financing

Part 8 – Review question: Cost of purchases and cashbudget

86

Question 5 March, 2004Handout pages 7 thru 8

a. Prepare a cost of purchases schedule for Octoberand November

b. Prepare the cash budgets for October andNovember including the effects of financing

Part 8 – Review question: Cost of purchases and cashbudget

87

Part 9

Review question:Cash budget

(download the additional questions handout: ma1_mod6_handout1.pdf)

MA1 – MODULE 6

88

Question 4 June, 1991Handout pages 9 thru 10

Prepare a cash budget for the month of April

Part 9 – Review question: Cash budget

Stop the audio, read and attempt thequestion in the handout then come back tolisten to the solution.

89

Part 10

Review question:Cash disbursements

(download the additional questions handout: ma1_mod6_handout1.pdf)

MA1 – MODULE 6

90

Question 3 December, 1992Handout page 11

Compute the April cash disbursements for payment ofaccounts payable regarding direct materialspurchased

Part 10 – Review question: Cash disbursements

Stop the audio, read and attempt thequestion in the handout then come back tolisten to the solution.

91

Part 11

Review questions:Multiple Choice Questions

(download the additional questions handout: ma1_mod6_handout1.pdf)

MA1 – MODULE 6

92

Multiple choice questionsHandout pages 12 thru 14Now working on page 12Q1

a. Cost of the ending finished goods inventoryunder variable costing

b.Cost of the ending finished goods inventoryunder absorption costing

c. Operating profit for the year under absorptioncosting

d.Operating profit for the year under variable costing

Part 11 – Review questions: Multiple choice

Stop the audio, read and attempt thequestion in the handout then come back tolisten to the solution.

93

Multiple choice questionsHandout pages 12 thru 14Now working on page 13

Q2 May variance from the master budget operatingincome

Q3 Expected production in February

Part 11 – Review questions: Multiple choice

94

Multiple choice questionsHandout pages 12 thru 14Now working on page 14

Q4 Which statement regarding variable vs absorptioncosting is true?

Q5 How does the accounting treatment of selling andadministration costs differ between absorption andvariable costing if more units are produced thansold?

Q6 a. What would be inventoriable costs be if Ventoruses variable costing?

b.What would be the inventoriable cost if Ventoruses absorption costing?

Part 11 – Review questions: Multiple choice