managing expectations - royal london for...

TRANSCRIPT

MANAGINGEXPECTATIONS

Prot

ectio

n Pega

sus

Who

le o

f Life

A guide to reviewable premiums

For a

dvis

ers

only

2

Reviewable premiums what to expect 3What happens at the review 4Premiums at review 4Total premiums payable over time 5Different needs different types of premium 6

WHAT’S INSIDE

THIS IS FOR FINANCIAL ADVISER USE ONLY AND SHOULDN’T BE RELIED UPON BY ANY OTHER PERSON.

2

Who should select reviewable premiums?

Reviewable premiums might be suitable for clients who have an inheritance tax liability (IHT). They may also be aiming to reduce their tax liability by using other tax planning methods such as making gifts to reduce the value of their estate. Choosing a reviewable premium gives them flexibility at each review to reduce or increase their cover amount in line with their IHT liability at that time.

Premium affordability

Your clients need to be comfortable that they’re able to afford the premiums not only today but also in the future. If they are not intending to reduce their cover amount in line with their IHT liability, both you and your client need to be happy to accept that the premium for their Pegasus Whole of Life Plan could increase significantly as they get older.

This guide has been produced to show how significant reviewable premiums increases are at older ages. The actual impact for your client will depend on their individual circumstances.

REVIEWABLE PREMIUMSWHAT TO EXPECT

3

Because these assumptions change over time we can’t guarantee how much your clients’ premium could increase at each review but the change will be fair and reasonable.

Premiums at review

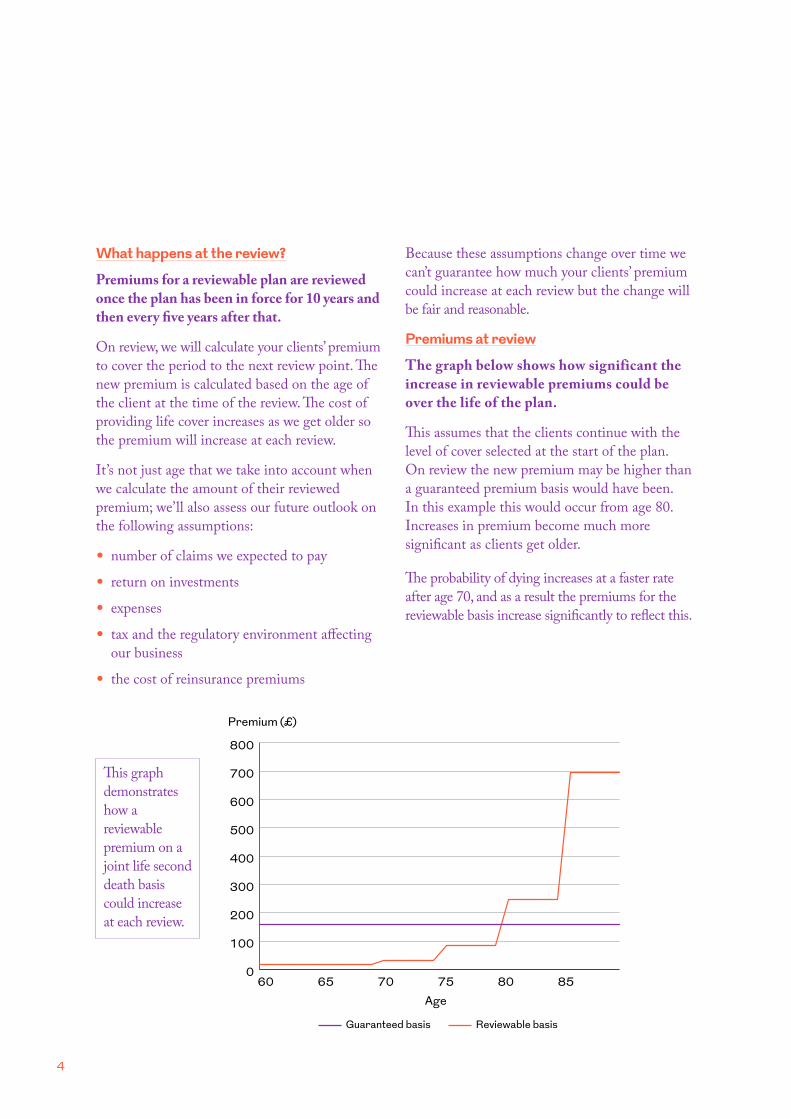

The graph below shows how significant the increase in reviewable premiums could be over the life of the plan.

This assumes that the clients continue with the level of cover selected at the start of the plan. On review the new premium may be higher than a guaranteed premium basis would have been. In this example this would occur from age 80. Increases in premium become much more significant as clients get older.

The probability of dying increases at a faster rate after age 70, and as a result the premiums for the reviewable basis increase significantly to reflect this.

What happens at the review?

Premiums for a reviewable plan are reviewed once the plan has been in force for 10 years and then every five years after that.

On review, we will calculate your clients’ premium to cover the period to the next review point. The new premium is calculated based on the age of the client at the time of the review. The cost of providing life cover increases as we get older so the premium will increase at each review.

It’s not just age that we take into account when we calculate the amount of their reviewed premium; we’ll also assess our future outlook on the following assumptions:

• number of claims we expected to pay• return on investments• expenses• tax and the regulatory environment affecting

our business• the cost of reinsurance premiums

Premium (£)

0

100

200

300

400

500

600

700

800

858075706560 Age

Guaranteed basis Reviewable basis

This graph demonstrates how a reviewable premium on a joint life second death basis could increase at each review.

4

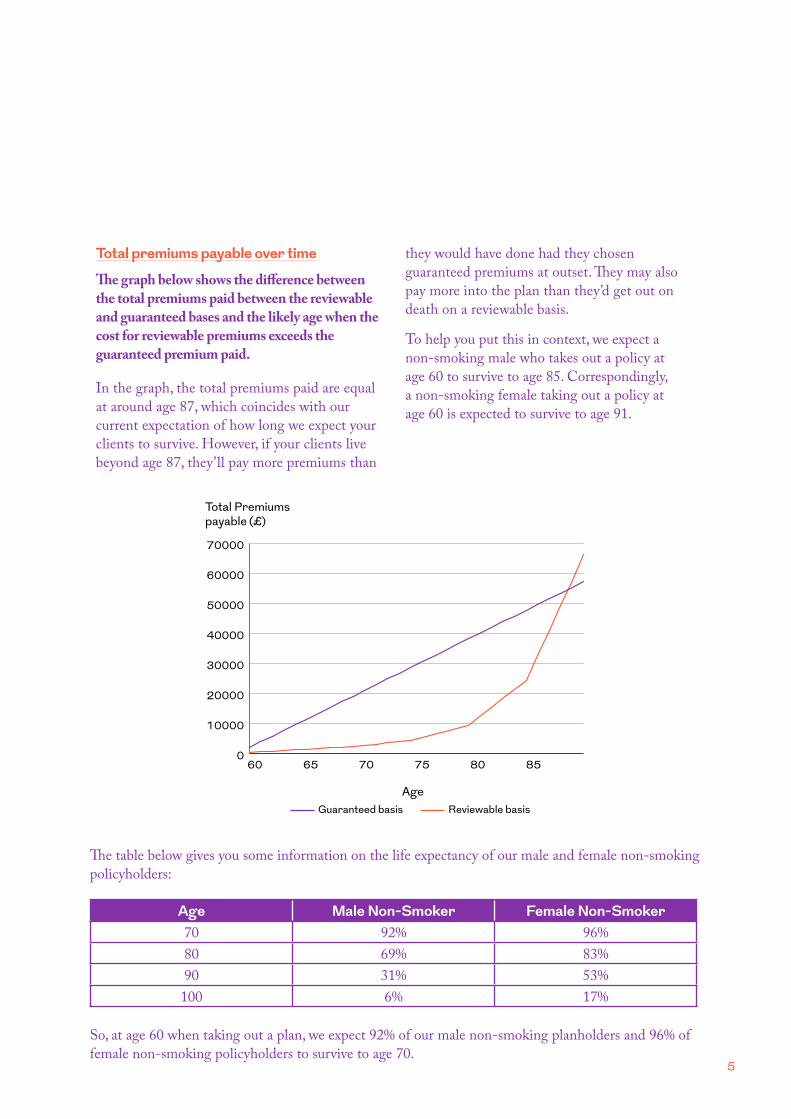

Total premiums payable over time

The graph below shows the difference between the total premiums paid between the reviewable and guaranteed bases and the likely age when the cost for reviewable premiums exceeds the guaranteed premium paid.

In the graph, the total premiums paid are equal at around age 87, which coincides with our current expectation of how long we expect your clients to survive. However, if your clients live beyond age 87, they’ll pay more premiums than

they would have done had they chosen guaranteed premiums at outset. They may also pay more into the plan than they’d get out on death on a reviewable basis.

To help you put this in context, we expect a non-smoking male who takes out a policy at age 60 to survive to age 85. Correspondingly, a non-smoking female taking out a policy at age 60 is expected to survive to age 91.

Total Premiums payable (£)

0

10000

20000

30000

40000

50000

60000

70000

858075706560

Age Guaranteed basis Reviewable basis

The table below gives you some information on the life expectancy of our male and female non-smoking policyholders:

Age Male Non-Smoker Female Non-Smoker70 92% 96%80 69% 83%90 31% 53%100 6% 17%

So, at age 60 when taking out a plan, we expect 92% of our male non-smoking planholders and 96% of female non-smoking policyholders to survive to age 70.

5

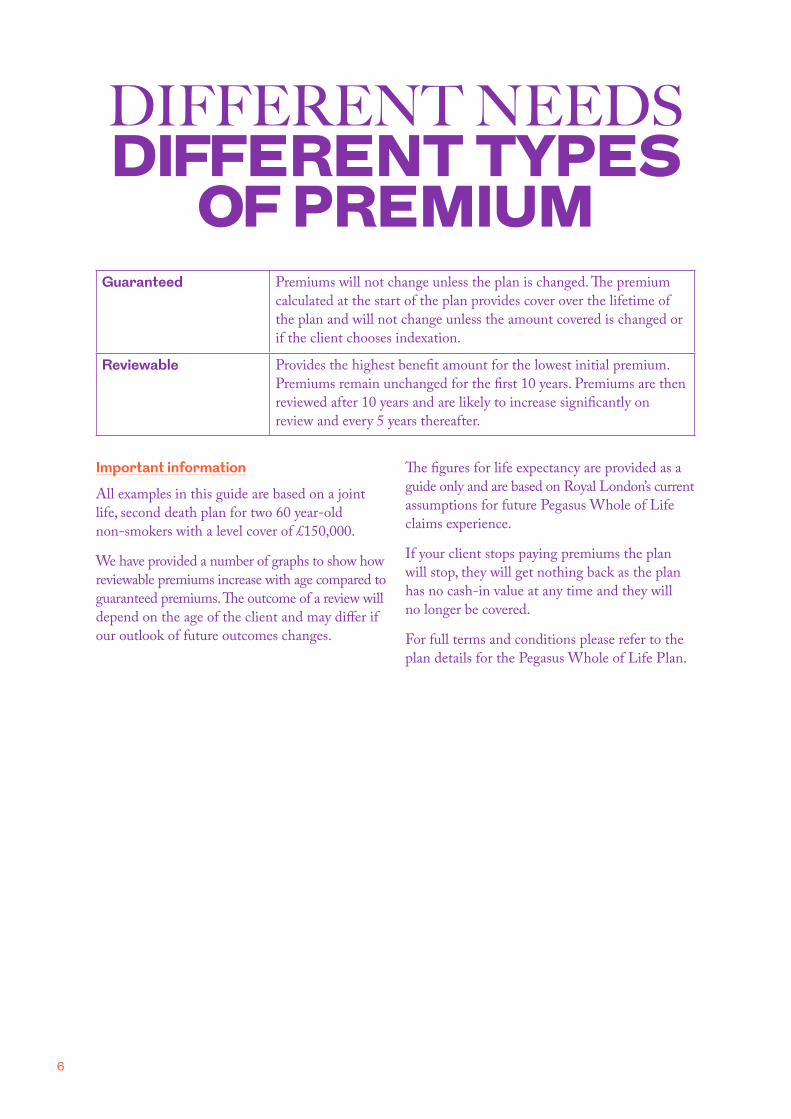

Guaranteed Premiums will not change unless the plan is changed. The premium calculated at the start of the plan provides cover over the lifetime of the plan and will not change unless the amount covered is changed or if the client chooses indexation.

Reviewable Provides the highest benefit amount for the lowest initial premium.Premiums remain unchanged for the first 10 years. Premiums are then reviewed after 10 years and are likely to increase significantly on review and every 5 years thereafter.

Important information

All examples in this guide are based on a joint life, second death plan for two 60 year-old non-smokers with a level cover of £150,000.

We have provided a number of graphs to show how reviewable premiums increase with age compared to guaranteed premiums. The outcome of a review will depend on the age of the client and may differ if our outlook of future outcomes changes.

The figures for life expectancy are provided as a guide only and are based on Royal London’s current assumptions for future Pegasus Whole of Life claims experience.

If your client stops paying premiums the plan will stop, they will get nothing back as the plan has no cash-in value at any time and they will no longer be covered.

For full terms and conditions please refer to the plan details for the Pegasus Whole of Life Plan.

DIFFERENT NEEDS DIFFERENT TYPES

OF PREMIUM

6

For more information about our Pegasus Whole of Life Plan, call us on 0345 6094 500. Alternatively, speak to your usual contact.

7

February 2017 P8P10003/1

Royal London1 Thistle Street, Edinburgh EH2 1DG

royallondon.com

All literature about products that carry the Royal London brand is available in large print format on request to the Marketing Department at

Royal London, 1 Thistle Street, Edinburgh EH2 1DG. All of our printed products are produced on stock which is from FSC® certified forests.

The Royal London Mutual Insurance Society Limited is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. The firm is on the Financial Services Register, registration number 117672. It provides life assurance and pensions. Registered in

England and Wales number 99064. Registered office: 55 Gracechurch Street, London, EC3V 0RL. Royal London Marketing Limited is authorised and regulated by the Financial Conduct Authority and introduces Royal London’s customers to other insurance companies. The firm is on the Financial Services Register, registration number

302391. Registered in England and Wales number 4414137. Registered office: 55 Gracechurch Street, London, EC3V 0RL.