managing federal receivables - bureau of the … · purpose of managing federal receivables ......

TRANSCRIPT

MANAGINGFEDERAL

RECEIVABLES

A Guide for Managing Loansand Administrative Debt

Department of the TreasuryFinancial Management Service

May 2005

This page is left intentionally blank.

TABLE OF CONTENTS

TC - 1

CHAPTER 1 – INTRODUCTION

Purpose of Managing Federal Receivables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-1Scope and Coverage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-2Key Related Legislation, Regulations and Guidance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-3Responsibilities of Departments and Agencies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-6

Office of Management and Budget (OMB) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-6Department of the Treasury’s Financial Management Service . . . . . . . . . . . . . . . . . . . 1-7Department of Justice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-8Program Agencies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-8

Program Review . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-13Form of Assistance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-13Financial Standards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-13The Credit Management and Debt Collection Cycle . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-14Document Organization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-15Inquiries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-15

CHAPTER 2 – BUDGET AND LEGISLATIVE POLICY FOR CREDIT PROGRAMS

Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2-1Program Review . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2-1Form of Assistance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2-2Financial Standards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2-2Implementation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2-3

CHAPTER 3 – CREDIT EXTENSION

Extending Credit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-1The Application . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-2Application and Origination Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-5Verifying Information Provided by the Applicant . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-6Credit Scoring . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-7Using Credit Reports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-8Credit Ratings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-10Conducting the Credit Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-11Appraisal of Real Property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-13Loan Closing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-15Non-Loan Screening . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-17Credit Extension Documentation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-18

TABLE OF CONTENTS

TC - 2

CHAPTER 4 – ACCOUNT SERVICING

Servicing Government Loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-1Billing the Debtor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-2Reporting Account Information to Credit Reporting Agencies . . . . . . . . . . . . . . . . . . . . . . . . . 4-4Account Monitoring . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-5Loan Classification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-6Consumer Loan Classification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-7Commercial Loan Classification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-8Allowance Accounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-9Servicing Documentation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-10Contract Servicing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-12Treasury Report on Receivables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-13

CHAPTER 5 – MANAGEMENT OF GUARANTEED LENDERS ANDSERVICERS

Managing Risks in Guaranteed Loan Programs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5-1Lender Eligibility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5-2Lender Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5-3General Participation Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5-4Performance Standards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5-4Reporting Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5-5Loan Servicers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5-5Lender and Servicer Reviews . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5-6Corrective Actions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5-7

TABLE OF CONTENTS

TC - 3

CHAPTER 6 – DELINQUENT DEBT COLLECTION

Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-1

Part I – Managing Delinquencies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-4Background . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-4

Delinquency Defined . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-4Changes in Governmentwide Debt Collection in 1996 . . . . . . . . . . . . . . . . . . . . . . . . 6-5Debt Collection Statutes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-5Governmentwide Debt Collection Regulations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-5Governmentwide Debt Collection Guidance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-6

Key Debt Collection Principles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-6Agency Regulations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-6Program Goals and Debt Collection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-7Due Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-7Minimum Due Process Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-8Privacy Protections . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-9

Determining the Appropriate Collection Technique to Use . . . . . . . . . . . . . . . . . . . . . . . . . . 6-10Establishing a Collection Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-11Collection Action Documentation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-12Agency Workout Groups . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-12Contact With the Debtor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-13Assessing Interest, Penalties and Administrative Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-17

Waiver of Interest, Penalties, and Administrative Costs . . . . . . . . . . . . . . . . . . . . . . . 6-18COLA Alternative to Assessment of Late Charges . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-19

Installment Payments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-20Acceleration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-22Rescheduling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-22Compromise . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-23Taking Action Against Co-borrowers/Guarantors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-25Application of Payments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-26

Part II – Debt Collection Tools and Programs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-27Transfer of Debts to FMS for Collection – Cross-Servicing . . . . . . . . . . . . . . . . . . . . . . . . . 6-27

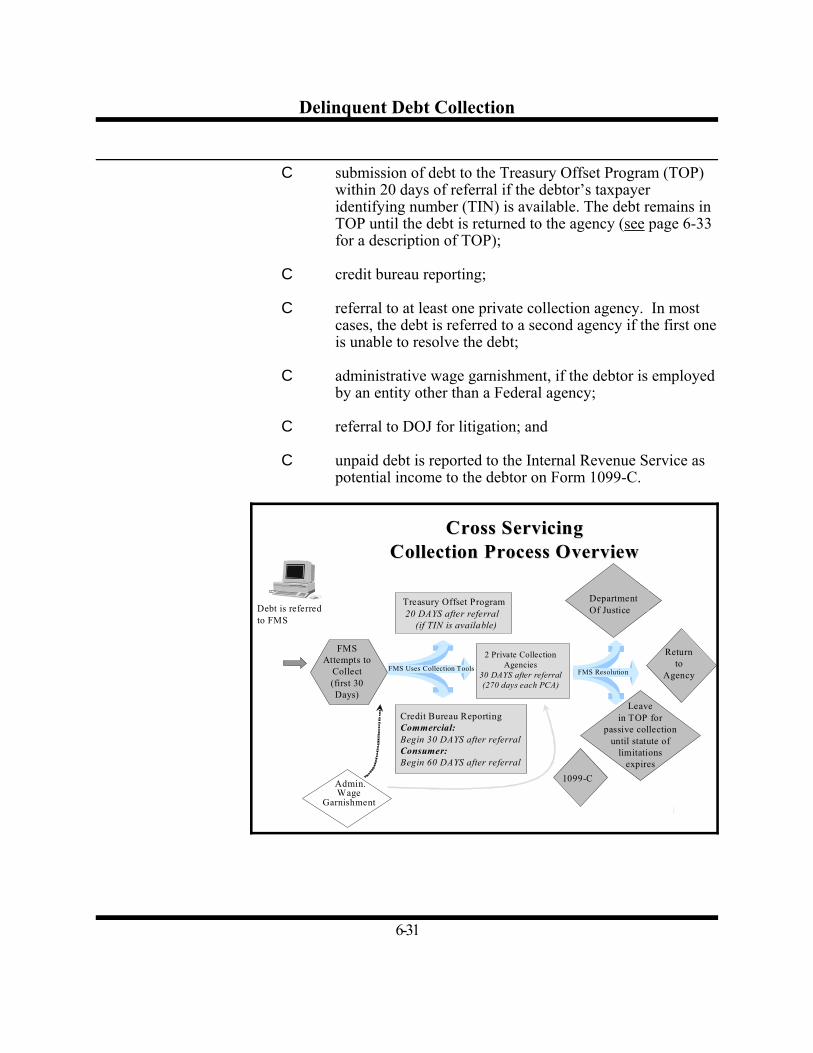

Debt Referral Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-27Exceptions to Referral Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-28Requirements for Agency Participation in Cross-Servicing . . . . . . . . . . . . . . . . . . . . 6-30Debt Collection Actions at FMS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-30Cross-Servicing Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-32

Administrative Offset (Including the Treasury Offset Program) . . . . . . . . . . . . . . . . . . . . . . . 6-33Centralized Offset Through the TOP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-33How TOP Works . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-34

TABLE OF CONTENTS

TC - 4

Debts Eligible for TOP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-35Exceptions to Referral Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-35Due Process Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-36Types of Federal Payments Eligible for Offset Under TOP . . . . . . . . . . . . . . . . . . . . 6-36Payments Exempt from Offset Under TOP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-37Special Provisions for Certain Recurring Payments . . . . . . . . . . . . . . . . . . . . . . . . . 6-37Offset of Federal Salary Payments Under TOP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-38TOP Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-38Computer Matching and Privacy Protection Act of 1988 . . . . . . . . . . . . . . . . . . . . . . 6-38

Non-Centralized Administrative Offset . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-39Types of Non-Centralized Administrative Offset . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-40

Internal Offsets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-41Contractor Payments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-41Collection of Travel Advances and Training Expenses from Federal Employees . . . 6-41Retirement Pay . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-42Federal Employee Salary Offset . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-42

Reporting Delinquent Debts to Credit Bureaus . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-44Private Collection Agencies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-45Administrative Wage Garnishment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-47

Requirements for Agency Use of Administrative Wage Garnishment . . . . . . . . . . . . 6-48Notice Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6-48Hearing Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6-49Administrative Wage Garnishment Form (SF-329) . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-50Amount of Garnishment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-50Wage Garnishment Worksheet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-51Limitations on Amount of Garnishment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6-52Financial Hardship . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-53Eligibility for Administrative Wage Garnishment . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-53Termination of the Wage Garnishment Order . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-54

Liquidating Collateral . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-54Bankruptcy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-56Litigation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-57

Fraud/False Claims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-60Statute of Limitations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-60Potentially Ineligible Referrals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-61Pre-Referral Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-62Post-Referral Activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-62

Barring Delinquent Debtors from Obtaining Federal Loans, Guaranties and Loan Insurance 6-64Delinquent Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-64Delinquency Resolution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-65

Revoking/Suspending Licenses or Eligibility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-66

TABLE OF CONTENTS

TC - 5

Part III – Miscellaneous Topics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-67Purchasing Credit Reports and Locating the Debtor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-67

Credit Reports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-67Consumer Credit Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-68Commercial Credit Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-68Reviewing Credit Report and Other Financial Information . . . . . . . . . . . . . . . . . . . 6-69Locating the Debtor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-70GSA’s Federal Supply Schedule for Business Information Services (Special Item Number 520-16) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-70Internet Resources . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-70Internal Revenue Service . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-71Post Office Trace . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-72Department of Motor Vehicles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-72Place of Employment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-72

Automated Collection Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6-73

CHAPTER 7 – TERMINATION OF COLLECTION ACTION, WRITE-OFFAND CLOSE-OUT/CANCELLATION OF INDEBTEDNESS

Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-1Termination of Collection Action Criteria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-5DOJ Concurrence for Terminating Collection Action . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-10Suspension of Collection Action . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-11Termination and Suspension of Collection Action and Compromise Regarding Fraud Claims 7-14Write-off . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-14Pursuit of Collection After Write-off/CNC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-17Write-Down . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-17Close-out Classification and Discharge of Indebtedness/Issuance of Form 1099-C . . . . . . . . 7-18

Close-out Classification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-18Discharge of Indebtedness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-19

Compromise of Debts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-23

CHAPTER 8 – PORTFOLIO SALES

Interim Guidance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8-1

TABLE OF CONTENTS

TC - 6

APPENDICES

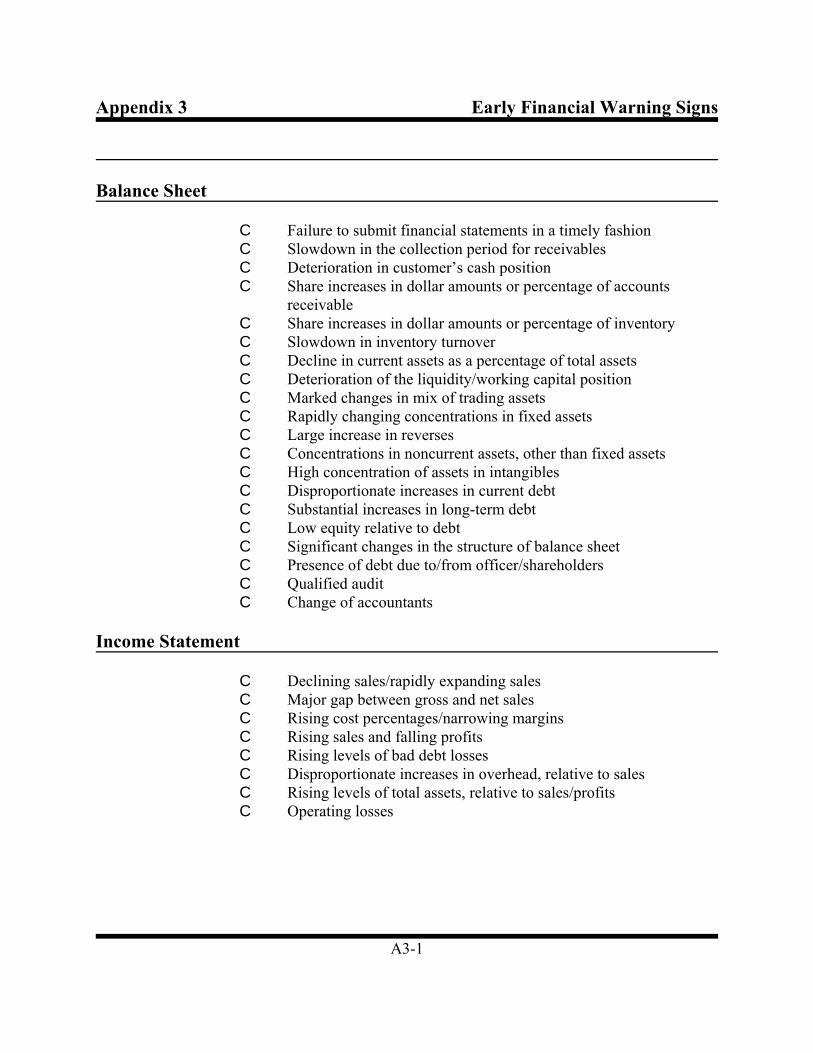

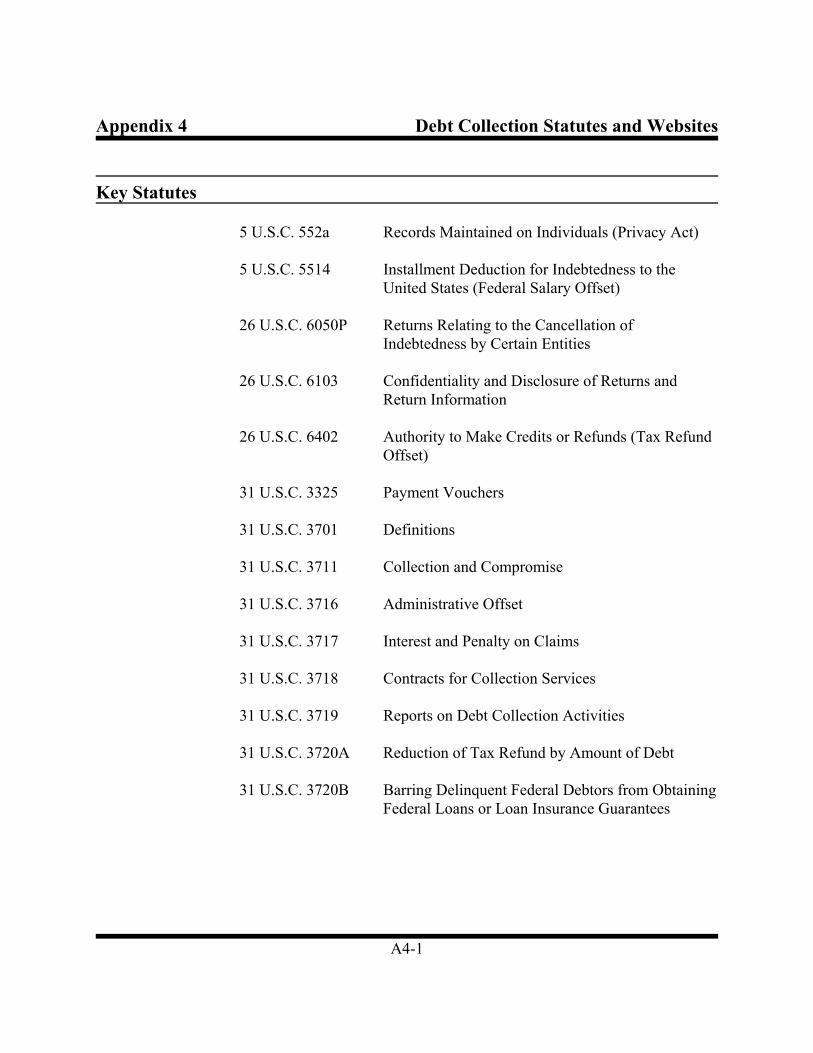

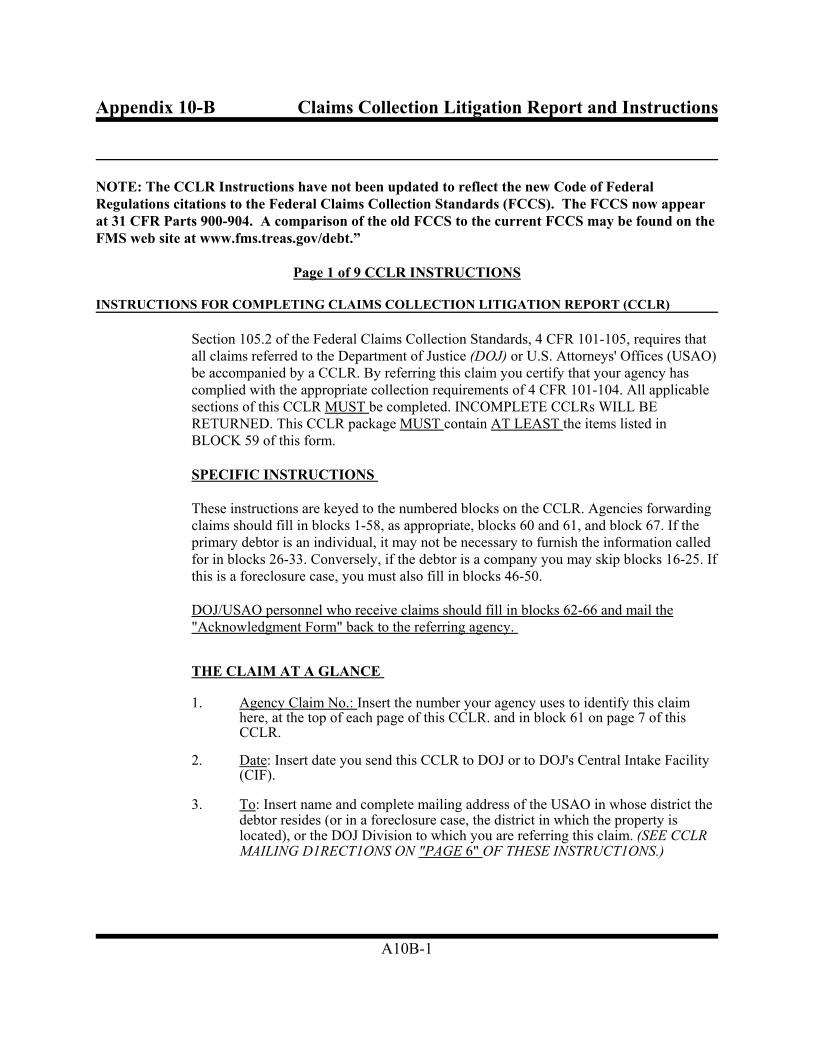

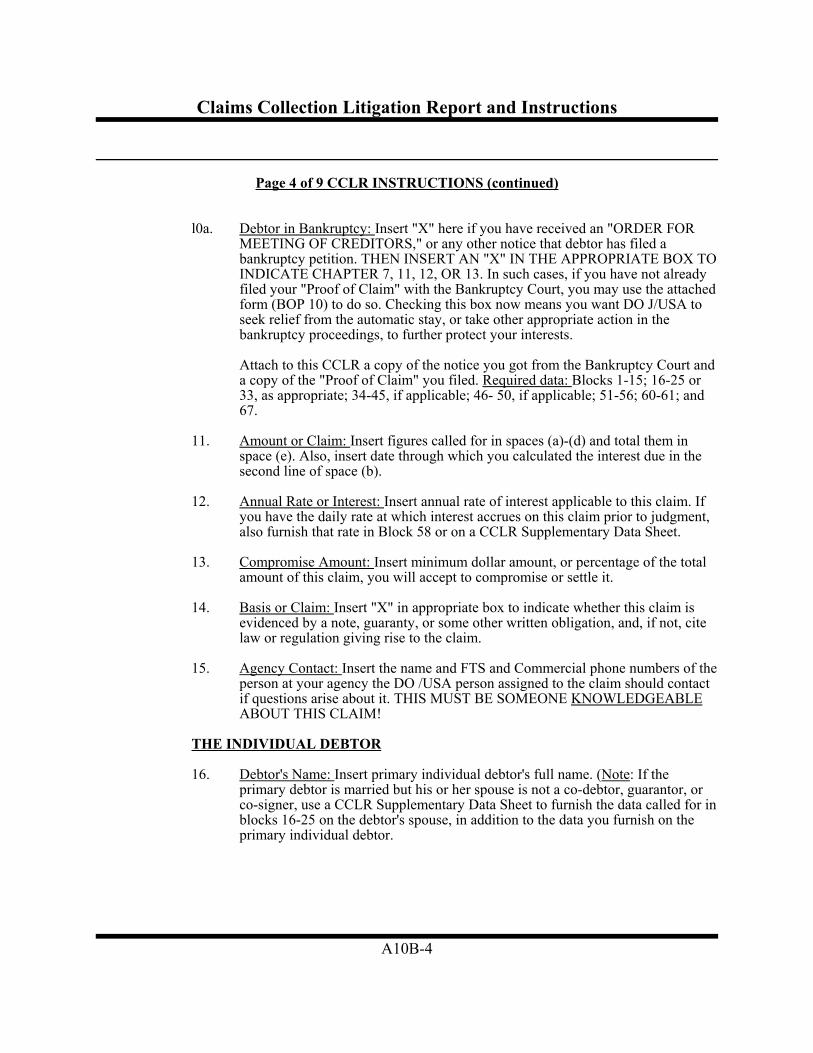

Appendix 1 - Credit Bureau Report KeyAppendix 2 - Credit Extension/Servicing Checklist Appendix 3 - Early Financial Warning SignsAppendix 4 - Debt Collection Statutes and WebsitesAppendix 5 - Debt Collection StrategiesAppendix 6 - Documentation of Collection ActivitiesAppendix 7 - Sample List of Appropriate Debt Collection PracticesAppendix 8 - Demand Letter Checklist Appendix 9 - Sample Financial Statement Appendix 10-A - Handling the Department of Justice’s 3% Fee Appendix 10-B - Claims Collection Litigation Report and Instructions

GLOSSARY

1-1

Chapter 1 Introduction

Purpose of Managing Federal Receivables

The purpose of "Managing Federal Receivables," is to provideFederal agencies with a general overview of standards, guidelines,and procedures for the successful management of Federal activitiesranging from the extension of credit or financial assistance toclosing-out uncollectible debts. Agency personnel who manageFederal credit programs and accounts receivable should alsofamiliarize themselves with the laws, regulations, policies andprocedures specific to their agency’s programs. Agenciesshould use the parts of these guidelines which pertain to theircredit management and debt collection activities and types of debt. The appendices include various checklists, documents and theappropriate references to assist agencies in managing their creditand debt collection activities. A glossary of relevant terms is alsoincluded at the end of the document. This edition supersedes theprior version of “Managing Federal Receivables” dated July 1994.

Since 1994, many changes have been made to Federal creditextension and debt collection policies and procedures. Federalagencies are now required to use credit reports as a screening tooland have applicants certify the accuracy of their initial applicationfor assistance. There are also several new delinquent debtcollection techniques, most notably, the requirement to refer debtsthat are delinquent 180 days or more to Treasury’s (Treasury)Financial Management Service (FMS). This document providesguidance on these and other changes to laws and policiesgoverning Federal receivables management and is consistent withthe Debt Collection Act of 1982, as amended by the DebtCollection Improvement Act of 1996 (DCIA); the revised FederalClaims Collection Standards (FCCS -31 CFR Parts 900-904)published November 22, 2000; and the revised Office ofManagement and Budget (OMB) Circular No. A-129 publishedNovember 29, 2000.

Introduction

1-2

Scope and Coverage

This document covers credit extension and receivablesmanagement functions related to:

C all direct loans where the Federal Government hasdisbursed funds to a borrower and enters into a contractwith the borrower for repayment;

C defaulted guaranteed loans where, under a guarantee orinsurance agreement, the Federal Government hasreimbursed a private financial institution or other entity fora borrower's default and assumed responsibility forrecovering any outstanding amounts;

C financial contracts designed to support borrowing;

C grant programs and contracts where financialresponsibility is a factor; and

C administrative debt, such as fines, fees, penalties andoverpayments.

The standards, guidelines and procedures described in thisdocument generally must be followed by all Federal agencies forall types of debt, unless otherwise provided by law. The standards,guidelines and procedures do not apply if they are statutorilyprohibited or are inconsistent with statutory requirements. See, forexample, Chapter 6, Delinquent Debt Collection, Overview (page6-1).

For the purposes of this document, the term "Federal agency"includes all Federal agencies and Government corporations definedunder 5 U.S.C. 105 and all other Federal instrumentalities, unlessthe application of a particular portion of this document isspecifically prohibited by statute. The term “Federal agency” alsoincludes judicial and legislative agencies to the extent authorizedby law. See, for example, 31 U.S.C. 3701 et seq. requiring judicial

and legislative agencies to collect delinquent debts using specifiedcollection remedies.

Introduction

1-3

Key Related Legislation, Regulations and Guidance

This document incorporates the relevant provisions of the:

C Federal Claims Collection Act of 1966 (FCCA) whichauthorized agencies to collect delinquent debt;

C Debt Collection Act of 1982 (DCA) which expanded theFederal Government's right to use debt collection toolssuch as offset, credit bureau reporting and private debtcollection agencies;

C Deficit Reduction Act of 1984 which added tax refundoffset as a debt collection tool;

C Chief Financial Officers Act of 1990 (CFO Act) whichinstituted effective financial management practices for theFederal Government and provided for the improvement ofthe Government's financial management, accounting, andinternal control systems;

C Federal Credit Reform Act of 1990 which requiredagencies to estimate a credit program's subsidy cost fordirect and guaranteed loans for inclusion in budget outlays;

C Federal Debt Collection Procedures Act of 1990(FDCPA) which established a uniform process through thecourt system for collecting debts owed the FederalGovernment and provides for uniform procedures forenforcing judgments to collect Federal debts;

C Administrative Dispute Resolution Act of 1990 (ADRA)which temporarily raised the authority of agencies tocompromise, suspend, and terminate collection action to$100,000 and gives the Attorney General the authority toincrease this threshold administratively. This authority wasmade permanent by the Debt Collection Improvement Actof 1996;

Introduction

1-4

C Cash Management Improvement Act Amendments of1992 (CMIAA) which expanded the use of tax refundoffset;

C Omnibus Budget Reconciliation Act of 1993 (OMBRA),as amended, which mandated that agencies, including theFederal Deposit Insurance Corporation (FDIC) and theNational Credit Union Administration, report dischargeddebts to the Internal Revenue Service as income to thedebtors;

C Department of Justice 1994 Appropriation Act whichauthorized the Department of Justice to charge a 3%administrative fee on amounts collected;

C Debt Collection Improvement Act of 1996 (DCIA) whichcentralized offset and other administrative debt collectionprocedures at the Treasury; bars delinquent debtors fromobtaining Federal loans, loan insurance or loan guarantees;mandates credit bureau reporting; and authorizesadministrative wage garnishment;

C General Accounting Office Act of 1996 which transferredfrom the General Accounting Office to Treasury certainauthorities, including the authority to promulgate theFederal Claims Collections Standards with the Departmentof Justice;

C Federal Claims Collections Standards (FCCS) (revisedNovember 22, 2000) which clarified and simplifiedFederal debt collection procedures and reflects changesunder the DCIA and the General Accounting Office Act of1996;

C Treasury Regulations which establish rules for certaindebt collection tools such as centralized administrativeoffset, cross-servicing and administrative wagegarnishment, as well as standards for barring delinquentdebtors;

Introduction

1-5

Federal Claims Collection Act Debt Collection Act

Deficit Reduction Act Debt Collection Improvement Act

CFO Act, Credit Reform, FDCPA, ADRA, CMIAA,

OMBRA, DOJ Act

Federal Claims Collection Standards

OMB Circular A-129

Agency Implementing Regulations and Standards

Managing Federal Receivables Credit Bureau Reporting Guide

Treasury Report on Receivables (TROR)

C Office of Personnel Management Salary OffsetRegulations which established rules and process foroffsetting the salaries of federal employees to collectdelinquent nontax debt; and

C OMB Circular No. A-129 “Policies for Federal CreditPrograms and Non-Tax Receivables” which establishedpolicies and procedures for justifying, designing andmanaging Federal credit programs and for collectingoutstanding receivables.

Key Credit Related Laws and Policies

Introduction

1-6

Responsibilities of Departments and Agencies

The successful implementation of a governmentwide creditmanagement/debt collection program depends upon the activeparticipation and support of several key agencies:

Office of Management and Budget (OMB)

C reviews legislation to establish new credit programs ormodify existing credit programs;

C monitors agency conformance with the Federal CreditReform Act;

C formulates and reviews agency credit reporting standardsand requirements;

C reviews testimony pertaining to credit programs and debtcollection activities;

C reviews agency budget submissions for credit programsand debt collection activities;

C develops and maintains the Federal credit subsidycalculator used to calculate the cost of credit programs;

C formulates and reviews credit management and debtcollection policy;

C approves agency credit management and debt collectionplans;

C provides training to credit agencies;

C chairs the Federal Credit Policy Working Group(FCPWG) which provides advice and assistance to agencies in the formulation and implementation ofcredit/debt policy governmentwide;

C resolves interagency issues;

Introduction

1-7

C sets credit management and debt collection programpriorities; and

C approves the asset management portions of the ChiefFinancial Officer Status Report and Five-Year Plans.

Department of the Treasury’s Financial Management Service

C serves as part of the FCPWG;

C develops and publishes, with the Department of Justice,the FCCS;

C works with OMB to develop Federal credit policiesand/or review legislation to create new credit programs orto expand or modify existing programs;

C promulgates governmentwide debt collection regulationsimplementing the debt collection provisions of the DCIAand other debt collection laws;

C provides collection services for delinquent non-taxFederal debts (referred to as “cross-servicing”), andmaintains a private collection contract for referral andcollection of delinquent debts;

• maintains a governmentwide delinquent debtor databaseand conducts offsets of Federal payments, including taxrefunds, under the Treasury Offset Program;

C works with Federal program agencies to identify debt thatis eligible for mandatory and voluntary referral toTreasury for cross-servicing and offset, and to establishtarget dates for referral;

C issues operational and procedural guidelines regardinggovernmentwide credit management and debt collection;

C assists in improving credit and debt management activitiesgovernmentwide;

Introduction

1-8

C tracks Federal Government receivables through theTreasury Report on Receivables and agencyimplementation of credit and debt management initiatives;

C develops guidelines and procedures on credit accountingand management information;

C provides operational assistance and consulting services toagencies;

C provides training on credit management and debtcollection related topics nationwide; and

C reports to Congress on governmentwide debt collectionactivities.

Department of Justice

C litigates on behalf of the Federal Government;

C approves compromises and terminations of collectionaction for debts over $100,000;

C develops and publishes, with Treasury, the FCCS;

C manages the Nationwide Central Intake Facility (NCIF) totrack and monitor agency referrals to the Department ofJustice;

C works with the program agencies to facilitate referrals tothe Department of Justice and resolve problems; and

C administers private counsel and special assistant U.S.attorney programs to collect Federal Government debt.

Program Agencies

Each agency is ultimately responsible for managing its ownreceivables activities and shall manage credit programs and non-tax receivables in accordance with applicable statutory authoritiesand prescribed policies to protect the Federal Government’s assetsand minimize losses in relation to social benefits provided.

Introduction

1-9

Each agency shall ensure that:

C Federal credit program legislation, regulations and policiesare designed and administered in compliance withprescribed legislative and regulatory requirements and thatthe costs of credit programs covered by the Federal CreditReform Act of 1990 are budgeted for and controlled inaccordance with the principles of that Act (unless anagency is expressly exempted from the statute);

C every effort is made to prevent future delinquencies byfollowing appropriate screening standards and proceduresfor determining creditworthiness and to determine whetherthe DCIA bars a loan applicant from loan assistance;

C lenders participating in guaranteed loan programs meet allapplicable financial and programmatic requirements;

C informed and cost effective decisions are made concerningportfolio management, giving full consideration to optionssuch as contracting for loan servicing functions or sellingthe portfolio;

C the full range of available and appropriate delinquent debtcollection techniques are used, such as those found in thisdocument (see Chapter 6, Delinquent Debt Collection), theFederal Claims Collection Standards and Treasuryregulations. Debt collection techniques include demandletters, administrative offset, salary offset, tax refundoffset, private collection agencies, cross-servicing byTreasury, administrative wage garnishment, and litigation;

C delinquent debts are written-off as soon as they aredetermined to be uncollectible, but no later than two (2)years from the date of delinquency (see Chapter 7,Termination of Collection Action, Write-off and CloseOut/Cancellation of Indebtedness);

C timely and accurate financial management andperformance data are submitted to OMB and Treasury sothat the Government’s credit management and debtcollection programs and policies can be evaluated;

Introduction

1-10

C regulations and forms are amended to comply withstatutory and regulatory requirements;

C credit management/debt collection tools and techniquesappropriate for the type and size of the agency's debts areimplemented;

C its personnel receive training on agency andgovernmentwide credit and debt management regulationsand procedures;

C the agency provides for receivables reporting and accounttracking systems to inform its own management, OMB,and FMS of essential credit information and to ensureaccurate financial reporting on the Treasury Report onReceivables (see Chapter 4, Account Servicing);

C the agency develops and implements portfolioperformance-based systems to ensure management andstaff accountability in administering and managingreceivables activities;

C the agency develops and implements the capability totrack and monitor key indicators of portfolio performance;

C the agency separates individual responsibility for creditactivity, for example, differentiating between extendingcredit and servicing accounts; and

• the agency maximizes the use of available technology andsystems to facilitate program operations.

Introduction

1-11

Key Participants in the Receivables Management Program

In order to establish these objectives, OMB Circular No. A-129requires that each agency shall:

(1) as appropriate, establish in accordance with OMB CircularNo. A-129, Section I, Subsection 4. b. (1), a board tocoordinate agency-wide credit management and debtcollection activities and to ensure full consideration ofcredit management and debt collection issues by allinterested and affected organizations within the agency. Ata minimum, the board should include the agency ChiefFinancial Officer (CFO) and the senior officials forprogram offices with credit activities or non-taxreceivables. The board may seek input from the agency’sInspector General based on findings and conclusions frompast audits and investigations;

(2) ensure that the statutory and regulatory requirements andstandards set forth in OMB Circular No. A-129,governmentwide regulations (e.g., FCCS and Treasuryregulations), and the supplementary guidance set forth inthis document are incorporated into agency regulations andprocedures for credit programs and debt collectionactivities;

OMB

Policy, Oversight

Federal Agencies

Implementation, Reporting

DOJ

FCCS, (with Treasury), Litigation

GOVERNMENTWIDE

RECEIVABLES

MANAGEMENT

PROGRAM

FMS

FCCS (with DOJ) , Delinquent Debt

Collection, Regulations, Guidelines, Consulting,

Training

Introduction

1-12

(3) propose new or revised legislation, regulations, and formsas necessary to ensure consistency with the provisions ofOMB Circular No. A-129;

(4) submit proposed legislation and testimony affecting creditprograms for review under the OMB Circular No. A-19legislative clearance process, and budget proposals forreview under the OMB Circular No. A-11 budgetjustification process;

(5) periodically evaluate Federal credit programs to assuretheir effectiveness in achieving program goals;

(6) assign to the agency CFO, in accordance with the ChiefFinancial Officers Act of 1990, responsibility for directing,managing, and providing policy guidance and oversight ofagency financial management personnel, activities, andoperations, including the implementation of assetmanagement systems for credit management and debtcollection;

(7) prepare, as part of the agency CFO Financial Management5-Year Plan, a Credit Management and Debt CollectionPlan for effectively managing credit extension, accountservicing, portfolio management and delinquent debtcollection. The plan must comply with the standards OMBCircular No. A-129; and

(8) ensure that information contained in loan applications anddocuments pertaining to individuals is managed inaccordance with the Privacy Act of 1974, as amended, andthe Right to Financial Privacy Act of 1978, as amended.

Introduction

1-13

Program ReviewProposals submitted to OMB for new programs and forpreauthorizing, expanding or significantly increasing funding forexisting credit programs should be accompanied by a writtenreview which examines at a minimum:

C Federal objectives to be achieved;

C justification for the use of a credit subsidy;

C estimated benefits of the program or program change;

C the effects on private capital markets;

C the estimated subsidy level; and

C the administrative resource requirements.

Form of Assistance

When Federal credit assistance is necessary to meet a Federalobjective, loan guarantees should be favored over direct loans,unless attaining the Federal objective requires a subsidy, as definedby the Federal Credit Reform Act of 1990, deeper than can beprovided by a loan guarantee. For further information on Formof Assistance, see OMB Circular No. A-129, Section II.2.

Financial Standards

In accordance with the Credit Reform Act of 1990, each agencymust analyze and control the risks and costs of its programs. Anagency must develop statistical models predictive of default andother deviations from loan contracts. An agency is required toestimate subsidy costs and obtain budget authority to cover suchcosts before obligating direct loans and committing loanguarantees. Instructions for budget justification and subsidy costestimation under the Federal Credit Reform Act of 1990 areprovided in OMB Circular No. A-11, and instructions for budgetexecution are provided in OMB Circular No. A-34. For furtherinformation on Financial Standards, see OMB Circular No. A-129, Section II. 3.

Introduction

1-14

The Credit Management and Debt Collection Cycle

The DCIA and OMB Circular No. A-129 have placed increasedemphasis on credit management and debt collection. New toolsand techniques have been introduced to reduce the FederalGovernment’s risk of losses and strengthen the Government’sability to collect its debts. The major elements of the “creditmanagement and debt collection cycle” will be explained in thisdocument as follows:

C credit extension - screen applicants for creditworthinessand financial responsibility, including the required use ofcredit reports; verify the accuracy of applicant creditinformation and whether the applicant owes delinquentFederal debts (and is barred by the DCIA from obtainingloan assistance); and determine the applicant’s inability toobtain funding from private sector markets;

C account servicing - bill and collect accounts, includingautomating this process and reporting current (non-delinquent) consumer and commercial accounts to creditreporting agencies (also known as credit bureaus) on aroutine, non-exclusive basis. Lenders participating in theFederal Government’s guaranteed loan programs are alsorequired to report accounts to credit bureaus;

C debt collection - collect delinquent accounts, including thereferral of delinquent debts to FMS for collection, offset,administrative wage garnishment, referral to privatecollection agencies, referral to the Department of Justicefor litigation, and reporting of delinquent consumer andcommercial accounts to credit bureaus;

C write-off/currently-not-collectible - remove the accountfrom the agency’s receivables, determine whether the debtis “currently not collectible” and place the account on asubsidiary ledger for continued collection activity;

C write-off/close out - cease all collection action onuncollectible debt and report the discharged debt amount tothe Internal Revenue Service (IRS) as potential income tothe debtor.

Introduction

1-15

Each element of the cycle applies to guaranteed and direct loanactivities. Individual elements, such as account servicing, debtcollection, and write-off, apply to defaulted guaranteed loans,grants, contracts, and administrative debt.

Document Organization

This document is divided into eight (8) chapters, with Chapters 3through 7 covering the elements of the credit management anddebt collection cycle. The chapters are:

• Chapter 1 - Introduction;

• Chapter 2 - Budget and Legislative Policy for CreditPrograms;

• Chapter 3 - Credit Extension;

C Chapter 4 - Account Servicing;

• Chapter 5 - Management of Guaranteed Lenders andServicers;

• Chapter 6 - Delinquent Debt Collection;

• Chapter 7 - Termination of Collection Action, Write-offand Close-Out/Cancellation of Indebtedness; and

• Chapter 8 - Portfolio Sales.

Separate detailed guidance on reporting debts to credit bureaus isavailable in the “Guide to the Federal Credit Bureau Program,”which is available on FMS’s web site at www.fms.treas.gov. Othercredit management and debt collection guidance is also availableon the FMS web site.

Inquiries

For information on this or other FMS publications/activities,please contact the Financial Management Service, Director,Agency Liaison and Reporting Division, Debt ManagementService (DMS) at 202-874-6660 or the Director, AgencyEnterprise Solutions Division, Federal Finance at 202-874-6638.

This page is left intentionally blank.

2-1

Chapter 2 Budget and Legislative Policy for Credit Programs

Overview

This Chapter describes policies with respect to Federal creditprograms, as outlined in the Office of Management and Budget(OMB) Circular No. A-129, “Policies for Federal Credit Programsand Non-Tax Receivables” which may be found at the OMB website at www.whitehouse.gov/omb and the Department of theTreasury’s Financial Management Service web site atwww.fms.treas.gov. When developing new or revising existingcredit programs, Federal agencies must take into consideration theBudget and Legislative Policy for Credit Programs promulgated inOMB Circular No. A-129, which states:

“Federal credit assistance should be provided only when it isnecessary and the best method to achieve clearly specified Federalobjectives. Use of private credit markets should be encouraged,and any impairment of such markets or misallocation of thenation's resources through the operation of Federal credit programsshould be minimized.”

OMB Circular No. A-129, Section II., provides four subsections toassist agencies with respect to development and review of budgetand legislative policy.

Program Review

Proposals submitted to OMB for new programs and forreauthorizing, expanding, or significantly increasing funding forexisting credit programs should be accompanied by a writtenreview. See OMB Circular No. A-129, Section II., subsection 1.,paragraphs a-f, for the factors that must be included in the writtenreview.

Budget and Legislative Policy for Credit Programs

2-2

Form of Assistance

When Federal credit assistance is necessary to meet a Federalobjective, loan guarantees should be favored over direct loans,unless attaining the Federal objective requires a subsidy, as definedby the Federal Credit Reform Act of 1990, deeper than can beprovided by a loan guarantee. See OMB Circular No. A-129,Section II., subsection 2., paragraphs a-f, for details on the use ofguaranteed loans over direct loans and other considerationsregarding loan guarantees.

Financial Standards

In accordance with the Federal Credit Reform Act of 1990,agencies must analyze and control the risk and cost of theirprograms. Agencies must develop models (statistical or otherwise)predictive of defaults and other deviations from loan contracts. Agencies are required to estimate subsidy costs and to obtainbudget authority to cover such costs before obligating direct loansand issuing loan guarantee commitments. Specific instructionsfor budget justification, subsidy cost estimation and budgetexecution under the Federal Credit Reform Act of 1990 areprovided in OMB Circular No. A-11.

Agencies shall follow sound financial practices in the design andadministration of their credit programs. Where program objectivescannot be achieved while following sound financial practices, thecost of these deviations shall be justified in agency budgetsubmissions in comparison with expected benefits. Unless awaiver is approved, agencies should follow the financialpractices discussed in Circular No. A-129, Section II.,subsection 3., paragraphs a-g.

Budget and Legislative Policy for Credit Programs

2-3

Implementation

The provisions of OMB Circular No. A-129, Section II will beimplemented through the OMB Circular No. A-19 legislativereview process and the OMB Circular No. A-11 budgetjustification and submission process.

For accounting standards for Federal credit programs, seeAccounting for Direct Loans and Loan Guarantees, Statement ofFederal Financial Accounting Standards Number 2, developed bythe Federal Accounting Standards Advisory Board. See OMBCircular No. A-129, Section II., subsection 4., paragraphs a-c, fordetails on such matters as:

a. proposed legislation on credit programs, reviews of creditproposals made by others, and testimony on credit activitiessubmitted by agencies under the OMB Circular No. A-19. The legislative review process should conform to theprovisions of this OMB Circular No. A-129;

b. How to request a waiver from OMB for use of proposedprovisions or language not in conformance with thepolicies of OMB Circular No. A-129. Agencies will berequired to request in writing that OMB waive therequirement, and the request must be submitted on astandard waiver request form, available from OMB. SeeOMB Circular No. A-129, Section II., subsection 4.,paragraph (c) 1, for details on how requests should becompleted;

c. the checklist for review of legislative and budgetaryproposals. See Appendix B of OMB Circular No. A-129;and

d. the model bill language to be used in developing andreviewing legislation (unless OMB has approved the use ofalternative language that includes the same substantiveelements) See Appendix C of OMB Circular No. A-129.

Budget and Legislative Policy for Credit Programs

2-4

Every four years, or more often at the request of the OMBexaminer with primary responsibility for the account, the agency'sannual budget submission (required by OMB Circular No. A-11,Section 15.2) should include:

a. a plan for periodic, results-oriented evaluations of theeffectiveness of the program, and the use of relevantprogram evaluations and/or other analyses of programeffectiveness or causes of escalating program costs. SeeOMB Circular No. A-129, Section II. for further details onprogram evaluation;

b. a review of the changes in financial markets and the statusof borrowers and beneficiaries to verify that continuation ofthe credit program is required to meet Federal objectives, toupdate its justification, and to recommend changes in itsdesign and operation to improve efficiency andeffectiveness; and

c. proposed changes to correct those cases where existinglegislation, regulations, or program policies are not inconformance with the policies of OMB Circular No. A-129, Section II. When an agency does not deem a changein existing legislation, regulations, or program policies tobe desirable, it will provide a justification for notconforming with the Circular.

Questions regarding this chapter should be referred to the Office ofManagement and Budget, Budget Review Division at202-395-3945.

3-1

CreditReports

Purchase

RECEIVE APPLICATION

SCREEN PROSPECTIVE BORROWERS

CAIVRS, DEBT CHECK

CREDIT BUREAU REPOSITORIES

APPLICATION REJECTED

LOAN AGREEMENT SIGNED

ACCOUNT SERVICING

SELL LOAN ON PRIVATE MARKET

Report Consumer and Commercial

Accounts

Other Credit

History

Chapter 3 Credit Extension

Extending Credit

This Chapter details how Federal agencies and lendersparticipating in guaranteed loan programs (guaranteed loanlenders) should manage, process, evaluate, and document loanapplications and awards for loan assistance. See Chapter 5“Management of Guaranteed Loan Lenders and Servicers” forinformation on how Federal agencies should manage lenders andservicers that participate in Federally insured guaranteed loanprograms. See also Office of Management and Budget (OMB)Circular No. A-129, “Policies for Federal Credit Programs andNon-Tax Receivables,” which may be found online atwww.whitehouse.gov/omb or www.fms.treas.gov.

Credit Extension

Credit Extension

3-2

When extending credit through a Government loan program,agencies and guaranteed loan lenders must ensure that applicationsare processed and that credit is analyzed in accordance with allstatutory and regulatory requirements. Lenders and agencies needto assess and document their loan applicants' eligibility for thespecific type of credit offered. Except where required by statute,an agency will not extend credit to individuals or entities whocould obtain credit from private sector sources. Further, except inlimited circumstances, no agency or guaranteed loan lender mayextend credit to an individual or entity that is delinquent on aFederal non-tax debt, until the delinquency is resolved and proofof the resolution is presented by the debtor. Where permitted bylaw, individuals who owe delinquent child support obligations arelikewise barred from obtaining Federal loan assistance. Federalcredit granting agency personnel should work with their agencycounsel to determine whether the eligibility requirements may beextended to principals of entities in commercial transactions.

The Application

Federal credit granting agencies and private sector lenders inguaranteed loan programs shall determine whether applicantscomply with statutory, regulatory, and administrative eligibilityrequirements for loan assistance. Lenders and agencies should usethe application process as a first step in their effort to evaluate anapplicant’s request for credit and to determine eligibility for thecredit being sought by the applicant. The application form itself isa critical piece of documentation for capturing key informationabout the applicant(s), co-applicant(s) and guarantor(s), including:

C full name and any "also/known/as" (AKA);

C taxpayer identification numbers (TINs) (Social SecurityNumbers [SSNs] for individuals or Employer IdentificationNumbers [EINs] for all other entities). An agency mustrequire a loan applicant to provide the applicant’s TIN forany program under which the agency makes, guarantees, orinsures loans. See 31 U.S.C. 7701(b). Applicants must beasked to identify all prior TINs that were used in otherFederal Government applications;

C address(es) and telephone number(s);

Credit Extension

3-3

C any personal information, such as number in household,required by the program in accordance with provisions ofthe Privacy Act of 1974, as amended;

C name(s), address(es), and telephone number(s) ofapplicant’s and co-applicant’s employer(s);

C all relevant financial information, such as income, assets,payments, and liabilities; and

C collateral information, including collateral location,estimated value and description.

The application form will also contain the following:

C a statement signed by each applicant attesting to theaccuracy of the information provided. The statement willdescribe any penalties the Federal Government imposes onthose who knowingly provide false information on aFederal credit or financial assistance application;

C a “Certification of Non-Delinquency” signed by eachapplicant stating that he/she/it is not delinquent on aFederal Government debt, including any tax debt, and doesnot own any property that is subject to a judgment liensecuring a debt to the Government. If the applicant isunable to make such certification, the applicant should beasked to explain any delinquencies or defaults andinformed that the applicant must resolve the delinquency ordefault, and present evidence of that fact to the agency,before the application process can proceed. The agencyshall stop processing on the application until suchevidence is presented.

Credit Extension

3-4

Pursuant to the Debt Collection Improvement Act of 1996(DCIA), persons owing outstanding delinquent non-tax debtto the United States may not obtain Federal loan assistanceuntil the delinquency is resolved. The DCIA eligibilityrequirement does not apply to disaster loans, or if therequirement is waived by the head of the lending agency. Otherwise, the DCIA eligibility requirement applies to allFederal direct, guaranteed and insured loans regardless ofwhether creditworthiness is an eligibility requirement. Anagency is not required to grant a loan merely because theDCIA does not render an applicant ineligible (for example,in the case of a delinquent tax debt or if the delinquent debthas been resolved but evidences bad credit history);

C to the extent allowed by law, a statement that each applicantdoes not owe delinquent child support obligations. Aspermitted by law, lenders and agencies shall deny Federalloan assistance to individuals who owe delinquent childsupport obligations that have been submitted to theDepartment of the Treasury (Treasury) for collectionthrough the offset of Federal tax refund and other payments. See Executive Order 13109, “Supporting Families:Collecting Delinquent Child Support Obligations.” Anagency that is authorized to deny a loan pursuant toExecutive Order 13109 must provide the loan applicant witha review process described in “Minimum Due ProcessGuidelines: Denial of Federal Financial Assistance” issuedby the Attorney General. The Executive Order and dueprocess guidelines may be found on the web site ofTreasury’s Financial Management Service (FMS) atwww.fms.treas.gov;

C a statement requiring the applicant(s) to affirm that he/shehas been unable to obtain credit from private sector sources(where it is consistent with statutory, regulatory andadministrative eligibility requirements); and

C a “Debt Collection Certification Statement” signed by theapplicant, detailing the consequences of delinquency (forexample, credit bureau reporting, tax refund offset, etc.) andcertifying that the Federal Government's debt collectionpolicies have been discussed with the applicant at the timeof application.

Credit Extension

3-5

All applicants and co-applicants must be required to sign anddate the completed application form.

The Application

Application and Origination Fees

The agency should assess a non-refundable application fee that, ata minimum, covers the costs of obtaining credit reports, appraisals,and supplemental data, where applicable. The application feeshould be collected at the time the applicant(s) completes andsubmits the application form. The amount of the application feeshould be reviewed on a regular basis and adjusted accordingly.

Names, addresses,phone numbers

Employername, address,phone numbers

Signed statementcertifying

accuracy ofinformation

Taxpayer IdentificationNumbers

LOANAPPLICATION

Signed debtcollection

certification

Applicantfinancialinformation

Collateral information

Signed non-delinquencycertification

Signed certification of non- delinquency ofchild support payments

Credit Extension

3-6

In addition, the agency should charge an origination or funding feewhich covers the costs of making the loan, including an amountsufficient to cover as much of the estimated losses as possible,based on past performance of the portfolio. The agency shouldreassess and adjust, as necessary, the amount of the origination orfunding fee at least annually, where permitted by statute.

The agency must inform the applicant at the time of application ofany application, origination or funding fees. The agency mustcollect the origination or funding fee at the time of application,upon loan approval, or at the time the loan funds are disbursed asagency regulations require.

Verifying Information Provided by the Applicant

After receiving the completed application form and making aninitial determination based on the application alone that theapplicant is eligible for the credit being sought, the agency and/orits lender, as appropriate, should verify the information providedby the applicant by:

C matching the applicant's name and social security numberagainst the Internal Revenue Services’s delinquent tax filesto determine if the applicant has a Federal tax liability. Applicants with such liablity are ineligible until the liabilityis satisfied;

C using, as appropriate, the Department of Housing and UrbanDevelopment’s Credit Alert Interactive Voice ResponseSystem (CAIVRS), the Debt Check program operated byFMS, and other databases including internal agencyinformation systems, to determine if the applicant isdelinquent or has defaulted on a Federal Government loanor has an outstanding Federal judgment;

C obtaining and using credit reports available through theGeneral Services Administration's (GSA) Federal SupplySchedule for Business Information Services. The creditreport will also be used to conduct the credit analysis anddetermine the applicant’s creditworthiness (see “Conductingthe Credit Analysis” in this chapter); and

Credit Extension

3-7

C requesting verification of the applicant's employment andincome, credit history, and bank deposits from theappropriate sources. Requests for verification of thisinformation should carry an expiration date. Informationshould be reverified if more than 90 days old at the time ofloan approval, 120 days old at closing, or at any time priorto closing if there is reason to believe that changes haveoccurred since the original verification. These time limitsmay be extended 30 days based upon market conditions ineffect at the time of application. All information receivedduring the origination and underwriting process becomespart of the permanent loan file.

Credit Scoring

Credit scoring is a specific standardized, statistical method ofrating applicants by assigning points to certain attributes andcriteria of the applicant. For example: low consumer debt and nodelinquencies -- 5 points; high consumer debt with 3 delinquencies-- 2 points; or, as a second example, occupancy in the sameresidence for 5 years -- 10 points; occupancy in the same residencefor 2 years -- 3 points. In this example, a higher score wouldindicate greater financial stability and responsibility and,presumably, represent a lower credit risk.

Criteria used in a credit scoring system must be relevant to anapplicant's ability to repay and must be uniformly applied to allapplicants to ensure agency/lender impartiality in its creditanalysis. In developing a credit scoring system, an agency must beable to demonstrate that there is a positive statistical relationshipbetween specific criteria, such as length of time at the sameresidence, and its applicants' creditworthiness. Wherecreditworthiness is a criterion for loan approval, agencies andprivate sector lenders shall determine if applicants have the abilityto repay the loan and a satisfactory history of repaying debt.

Credit scoring may be used to determine whether an applicantmeets baseline creditworthiness requirements prior to conducting afull credit analysis. Credit scoring should not be used as asubstitute for conducting such analysis, nor as the only means fordetermining creditworthiness.

Credit Extension

3-8

Using Credit Reports

Agencies and guaranteed loan lenders shall use reports originatingfrom credit bureau repositories as a screening tool. Credit reportsand supplementary data sources, such as financial statements andtax returns, should be used to verify or determine employment,income, assets and credit history. In addition to using a creditreport to verify information supplied by the applicant and wherecreditworthiness is a criterion for loan approval, the agency shallalso use it to answer two key questions: (1) does the applicant havethe ability to repay the loan or credit award in question; and (2) does the applicant have a satisfactory history of repaying debt? Guaranteed loan lenders and agencies need to determine whattype(s) of credit report(s) will best help them answer thesequestions and order the appropriate report. Through the GSA’sFederal Supply Schedule for Business Information Services,Federal agencies have access to a number of different types ofreports, with different types of information.

Depending upon the type obtained, the credit report will reveal:

C the type of credit history that has been established, includingwhether the applicant has met the terms of established creditaccounts;

C whether there have been any recent inquiries about theapplicant's credit status; and

C whether there are any outstanding liens against theapplicant's property.

The credit report will contain information on amounts owed to, andthe status of accounts held by, private sector companies, as well asGovernment agencies, and public record information, such asjudgments, liens and bankruptcies. The agency needs to evaluateall of the information in the credit report in terms of the followingquestions:

C How long has credit been established? A six month credithistory may be acceptable if the applicant just graduatedfrom college, but may be a cause of concern if the applicanthas indicated that he/she has a well-established credit history.

Credit Extension

3-9

C Are the credit accounts being paid as agreed? Theanswer to this question will indicate whether the applicant isable to handle the debts he/she incurs, identify potentialproblem accounts, and identify outstanding delinquentamounts owed to the United States or delinquent childsupport obligations that need to be resolved beforeadditional Federal loan assistance may be approved.

C Who is responsible for a given account? Applicant? Co-applicant? Information on the credit report will tell theagency who is liable for paying a given account. Theagency should follow-up with the applicant on any accountswhich show up on the credit report, but which the applicantdid not reveal.

C At the time of application, is there any bad credit? Hasthere been in the past? And, if so, what were thecircumstances -- medical problems, death, divorce,unemployment? If past due accounts have been broughtcurrent, the applicant may be trying to reestablish a goodcredit rating. Repeated one or two month delinquenciesmay indicate a cash flow problem -- or someone who knowshow to "play the system" so that the delinquencies neverlook so serious as to affect the applicant's ability to obtainnew credit.

Agency personnel should exercise judgment when reading anapplicant's credit report and should not hesitate to ask the applicantto clarify or explain any items of concern to the agency. (SeeAppendix 1 for a key to reading credit reports.)

Credit Extension

3-10

Credit Ratings

A credit rating may assist the agency in determining thecreditworthiness of the applicant. The rating is based upon theapplicant's financial condition, experience, and credit history. Under a credit rating system, each application is independentlyevaluated using specific standards and acceptable deviations fromthose standards developed by the agency. Ratios, in particularincome ratios, are often used to determine a credit rating. Incomeratios, which indicate the relationship between expenses andincome, are used to assess an applicant's ability to make additionalpayments or absorb future expenses.

To develop and apply a credit rating system, an agency must:

C determine, based on past credit experience, what it considersto be an acceptable level of risk for its loans;

C establish standards, including acceptable ratio levels, that itcan apply to relevant financial information obtained fromthe applicant;

C calculate all applicable ratios; and

C apply the appropriate standards to a loan application for aspecific type of credit to determine the credit rating.

If the agency determines that an applicant has an unacceptablecredit rating, it must decide if there are compensating factorswhich may mitigate the poor rating. Such factors would includethe applicant's:

C demonstrated ability for increased annual earnings, basedupon employment history;

C long-term employment prospect; and

C conservative use of credit or minimal amount of debt.

Credit Extension

3-11

Conducting the Credit Analysis

Using the information on the credit report, the verified applicationinformation, and the results of the credit rating, the agency shouldconduct a credit analysis to determine an applicant'screditworthiness, that is, the applicant’s ability and willingness torepay the loan.

A credit analysis for a consumer applicant will consider thefollowing:

C employment history for the past 2 years;

C current and potential income and benefits;

C financial statements including current assets, financialobligations, and liabilities;

C income tax returns for the past 2 years;

C credit rating;

C repayment history of prior debts;

C guarantees and collateral, ensuring that they are not pledgedto other debts;

C value of any pledged collateral; and

C homeownership status and residential stability.

Credit Extension

3-12

A credit analysis for a commercial entity will consider thefollowing:

C financial condition, as documented by annual and interimfinancial statements such as the balance sheet, incomestatement, and cash-flow statements. The agency should useaudited statements whenever possible and not requiredocumentation that is cost prohibitive for the applicant toobtain;

C any income tax returns for the past 2 years;

C ratios, such as total liability to total equity, net income tointerest expense, current assets to current liabilities, netincome to assets, and net income to equity;

C profit margin;

C amount and type of working capital;

C evaluation of the actual or potential market for thecommodity or service being offered and the entity'smarketing strategy for expanding or creating that market;

C company ownership (e.g., sole proprietor, partnership,corporation);

C managerial ability and/or experience of key companypersonnel;

C guarantees and collateral, ensuring that they are not pledgedor attached to other debts; and

C credit rating.

Generally, an agency should give particular attention to acompany's cash flow since it will be the source of the debtrepayment. The agency should also consider whether debts owedto the United States by officers, directors, major shareholders andpartners render the commercial entity ineligible for loan assistanceunder the DCIA. See 31 C.F.R. 285.13(c)(2).

Credit Extension

3-13

The agency should conduct comparable credit analyses on any co-borrower(s) and guarantor(s) listed on the application form. Theagency must document and maintain the appropriate creditanalyses in the applicant’s file.

Appraisal of Real Property

For many types of loans, the Federal Government can reduce itsrisk of default and potential losses through well managed collateralrequirements. Appraisals of real property serving as collateral fora direct or guaranteed loan (or property required for grantagreements and procurement contracts) must be conducted inaccordance with the following guidelines:

C agencies should require an independent, unbiased appraisalof property used as collateral. The appraisal should beconsistent with the "Uniform Standards of ProfessionalAppraisal Practice" (USPAP), as promulgated by theAppraisal Standards Board of the Appraisal Foundation, andany additional requirements established by the agency; and

C the appraiser should be qualified in accordance with theapplicable State and Federal regulatory requirements.Lenders and/or agencies shall determine whether anappraisal must be performed by a State licensed or certifiedappraiser based on the size of the loan and/or complexity ofthe appraisal. For non-business loans over $100,000 and forbusiness loans over $250,000, lenders and agencies shouldensure that a State licensed or certified appraiser preparesthe appraisal. Agencies may also require the services of aState licensed or certified appraiser for smaller direct orguaranteed loan transactions. The services of a Statelicensed or certified appraiser are not required for loans withno cash out and for those transactions where the collateral isnot a major factor in the decision to extend credit.

The appraisal will establish the fair market value of the propertyand serve as the basis for the agency's decision as to the maximumloan it will make on the property. The property should beappraised close to the commitment date of the lender. Theproperty should be reappraised if the appraisal is more than 6months old.

Credit Extension

3-14

Major elements addressed on the appraisal include:

C neighborhood analysis, including data related to theeconomic background of the region, city and neighborhood;

C site analysis, including data related to the size and shape ofthe property, the types of buildings on the property, frontfootage and parking;

C improvement analysis. A lot is considered "improved" if itcontains a structure. The improvement analysis focuses onthe structure or other dwelling(s), such as floor plans,energy efficiency, and age; and

C property condition and appraiser comments. Theappraiser must express an opinion about the condition of theproperty.

The “Subject Property Section” of the appraisal provides acomplete description of the property and its surroundings. A map,floor plan, and photographs of the property reflecting theproperty’s “curb appeal” should also be attached.

The appraiser uses the sales price of similar properties andestimated replacement costs to estimate the property's marketvalue. This estimate will be documented in the report's valuationsection.

In some credit programs, the primary purpose of the loan is tofinance the acquisition of an asset, such as a single family home,which then serves as collateral for the loan. Lenders and Federalagencies should ensure that borrowers assume an equity interest insuch assets to reduce defaults and losses. Federal agencies shouldexplicitly define the components of the loan-to-value ratio (LTV)for both direct and guaranteed loan programs. Lenders andagencies will review and approve the appraisal report containingthe estimated market value in order to determine the maximumavailable loan on the property (loan-to-value ratio). The approvedappraisal report will be placed in the permanent loan file.

Credit Extension

3-15

Unless exempted or otherwise authorized by law, agencies shouldestablish:

C a maximum acceptable LTV ratio. This could be in therange of 80 to 95%. Financing should be limited by notoffering terms (including the financing of closing costs) thatresult in a LTV equal to or greater than 100 percent. Further, the loan maturity should be shorter than theestimated useful economic life of the collateral;

C limitations on the proportion of up-front fees or transactionrelated expenses that a borrower can finance;

C an acceptable minimum down-payment amount; and

C a process for assessing higher loan premiums on loans withhigher loan-to-value ratios.

Loan Closing

Processing a Loan to Loan Closing

YES

Application Completed

Credit Analysis acceptable

Appraisal supports loan amount

Applicant Information verified

Private funding available

Non-delinquency verified

Eligible for type of credit

Loan Approved

YES

STOP

STOP

STOP

STOP

STOP

YES

STOP

NO

NO

NO

NO

NO

Credit Extension

3-16

Loan closing occurs after the completion of the processing of aloan which results in loan approval. At loan closing, the agency orlender will collect any loan documents or monies due. The agencyis responsible for ensuring that all legal documents including thepromissory note, collateral documents (such as security agreement,mortgage, and/or deeds of trust), loan agreement, certification ofnon-delinquency, and debt collection certification statement, aresigned by both the borrower(s) and co-borrower(s).

Where appropriate, the loan documents will state the terms ofrepayment, including:

C the frequency, due dates, and amount of principal andinterest payments. Generally, loan payments should bemonthly unless the borrower’s projected cash flow wouldmake monthly installments inappropriate;

C the amount of escrow payments, if required;

C the length of the loan - loan maturity should be shorter thanthe useful economic life of the asset being financed;

C the acceptable means of repayment, i.e., checks, money orders, credit cards, pre-authorized debit or electronicpayment via the internet (see, for example, www.Pay.gov);

C an explicit statement of borrower's rights and remedies;

C any special exemptions, such as cases of possibleforbearance or deferment;

C Federal delinquent debt collection policies and procedures;

C agency policies regarding the assessment of late charges ondelinquent payments. Amounts and/or rates to be assessedshould also be provided, when possible; and

C agency policies regarding the acceleration of the debt in theevent of a delinquency.

Credit Extension

3-17

Non-Loan Screening

Where financial responsibility is a factor, an agency should screenits potential contractors and grant applicants, in accordance withall statutory and regulatory requirements. Standards in Part 9 ofthe Federal Acquisition Regulations (FAR) apply to the screeningof contractors. As part of the application process, the agency mustobtain the following information from contractors and grantapplicants:

C taxpayer identification number(s); and

C certification of non-delinquent status. The applicant willcertify that he/she is not delinquent on a FederalGovernment debt, including tax debt. Agencies shouldinclude the certification statement on the application form.

Processing of contractor agreements and grant applications shall besuspended when applicants are delinquent on Federal tax or non-tax debts, including judgment liens against property for a debt tothe Federal Government. Processing should continue only whenthe debtor satisfactorily resolves the debt(s) (e.g., pays in full ornegotiates a new repayment plan).

Agencies shall obtain and use credit reports to verify theinformation provided by contractors and grant applicants, assessfinancial condition, and ascertain other financial agreements, ifany, between the applicant and the Federal Government. Theagency should also check the "List of Contractors Indebted to theUnited States" (Army Hold-Up List), published by the DefenseFinance and Accounting Service as part of its contractor eligibilityevaluation and verification process.

When an applicant is listed as debarred or suspended in the "List ofParties Excluded from Federal Procurement or Non-procurementPrograms," the agency will not make an award except asauthorized under agency regulations implementing ExecutiveOrder 12549 or FAR 9.4.

Credit Extension

3-18

L O A N AG R E EM E N T

____________________________________________________________________________________________________________________________________ ___________________________________________________________________________________________________ ______________________________________________________________________________________________________________________________________________________________________________________________________

S igned Loan Applica tion

L oan C om m itm ent

C redit R eport

V erification D ocum ents

C A IV R S and D ebt Check

D eb t C ollection Certification

N on-delinquency C ertification

C redit Analysis

Appra isa l

Credit Extension Documentation

Credit Extension Documentation