managing financial risk and loan performance in emerging markets

TRANSCRIPT

1Confidential Information – Copyright © First American Credco 2006

MANAGING RISK AND PERFORMANCE IN EMERGING MARKETS

ADDRESSING PERFORMANCE CONCERNSRisk Summit 2006Mark F. CatoneSenior Vice President, First American Credco

2Confidential Information – Copyright © First American Credco 2006

3Confidential Information – Copyright © First American Credco 2006

Market Dynamics/OpportunitiesThe Disparity Continues to Widen

Lower Costs of OriginationReduced Cost of CreditEasier AccessNew Products

Increasing Relative CostsExcluded from “New Model” scoring systemsSubject to Abusive Lending Practices

Prime Market Borrowers

Emerging Market BorrowersDisparity

4Confidential Information – Copyright © First American Credco 2006

Market Dynamics/ Opportunities Marketing Implications

Market Contraction and Growth 2000 - 2020

(4,000)(2,000)

02,0004,0006,000

White Black Asian Hispanic

Thou

sands

of Fa

milies

45 to 5435 to 4425 to 34Under 25

Brookings Institute White Paper Source: Thomas G. Exter, Ph.D.

5Confidential Information – Copyright © First American Credco 2006

Emerging Market Borrowers Across All Income Levelsare Concentrated in Subprime Pools

Refinanced Mortgage Loans in U.S. - 2002 Percent Subprime by Income Level

11.2% 9.7% 7.6% 5.2%

38.5%33.2%

27.8%19.6%19.9% 20.7% 19.4%

13.4%

0%10%20%30%40%50%

Low Moderate Middle Upper White African-American Latino

Source: Separate and Unequal: Predatory Lending in America, Published by Acorn 2004

6Confidential Information – Copyright © First American Credco 2006

The Consumer Portion• Pre-Loan Credit Counseling• Homeownership Planning• Monitoring• Loan Buyback as a Risk Management Strategy

7Confidential Information – Copyright © First American Credco 2006

Market Dynamics/ Opportunities are Enormous

32

22

0102030405060

BorrowersMillio

ns of

Poten

tial B

orrow

ers

No FileThin File

8Confidential Information – Copyright © First American Credco 2006

The Credit Portion• Favorable to the Consumer

– Add, Supplement, Build Credit– Keys Off of Housing as Predictive– Qualify for Best Loan Possible

• Lender Risk Management– Data Scrubbing & Integrity– Identity, Status Verification

9Confidential Information – Copyright © First American Credco 2006

Case Study #1• Consumer A “Thin” file

– Full File contents (before):• 4 closed accounts & 1 open account• 19 months of recent current history• FICO scores 684, 605, 628• Fraud Alert

– Anthem File contents (after):• 4 closed accounts & 5 open accounts• 29 recent months of current history ; min. 12 mo. rent• 91 months total recent, open history• FICO scores 684, 605, 628• Anthem Score 701• Consumer contacted directly

10Confidential Information – Copyright © First American Credco 2006

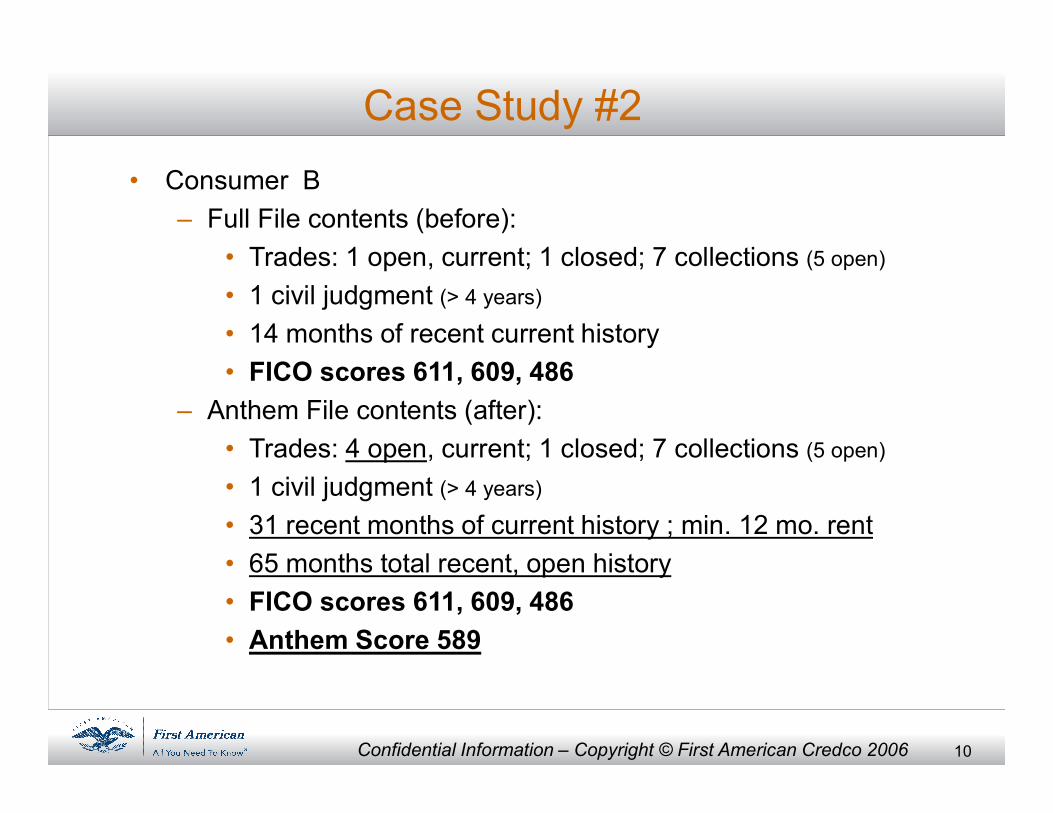

Case Study #2• Consumer B

– Full File contents (before):• Trades: 1 open, current; 1 closed; 7 collections (5 open)• 1 civil judgment (> 4 years)• 14 months of recent current history• FICO scores 611, 609, 486

– Anthem File contents (after):• Trades: 4 open, current; 1 closed; 7 collections (5 open)• 1 civil judgment (> 4 years)• 31 recent months of current history ; min. 12 mo. rent• 65 months total recent, open history• FICO scores 611, 609, 486• Anthem Score 589

11Confidential Information – Copyright © First American Credco 2006

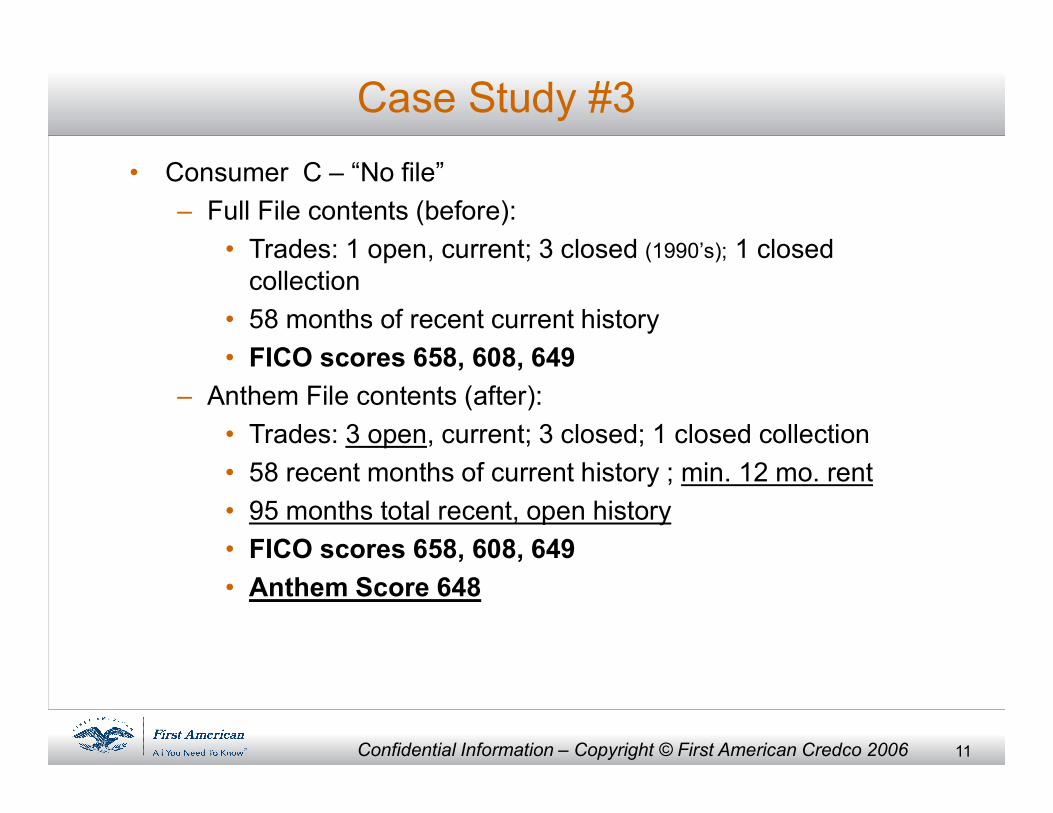

Case Study #3• Consumer C – “No file”

– Full File contents (before):• Trades: 1 open, current; 3 closed (1990’s); 1 closed

collection • 58 months of recent current history• FICO scores 658, 608, 649

– Anthem File contents (after):• Trades: 3 open, current; 3 closed; 1 closed collection• 58 recent months of current history ; min. 12 mo. rent• 95 months total recent, open history• FICO scores 658, 608, 649• Anthem Score 648

12Confidential Information – Copyright © First American Credco 2006

Percent Meeting Alternative Credit Minimums x FICO

0.0%10.0%20.0%30.0%40.0%50.0%60.0%70.0%80.0%90.0%

100.0%

0 - 45

9460

- 479

480 - 4

99500

- 519

520 - 5

39540

- 559

560 - 5

79580

- 599

600 - 6

19620

- 639

640 - 6

59660

- 679

680 - 6

99700

- 719

720 - 7

39740

- 759

760 - 7

79780

- 799

800 +

Score Range

Perce

nt Sa

tisfyi

ng Re

quire

ments

Anthem FICO• Requirements:

– At least 4 sources of NT data with at least 12 months of reported history.– Minimum of 12 months of rental history [Estimated].– Maximum 1 X 30 day delinquency on a rental tradeline.– Maximum 2 X 30 or 1 X 60 day delinquency on any tradeline.

13Confidential Information – Copyright © First American Credco 2006

Total Delinquencies Affordable s Market (quarter end)

• Over this time period NHSA’s high LTV 1st mortgage Private Label LLC loans total delinquency outperformed FHA by 507% & Prime by 107%

Total Delinquency LLC vs Market (balances)

0.00%5.00%

10.00%15.00%

Mar-0

1Ju

l-01

Nov-0

1Ma

r-02

Jul-0

2No

v-02

Mar-0

3Ju

l-03

Nov-0

3Ma

r-04

Jul-0

4No

v-04

Mar-0

5Ju

l-05

Total Private Label MBAA FHA MBA Prime

14Confidential Information – Copyright © First American Credco 2006

Total Delinquencies High LTV sales vs. Market (quarter end)

• Over this time period NHSA’s high LTV 1st mortgage GSE loans total delinquency performed at 94% of Prime loans

High LTV GSE Sales vs Market (balances)

0.00%1.00%2.00%3.00%4.00%5.00%6.00%7.00%

Mar-0

1Ju

l-01

Nov-0

1Ma

r-02

Jul-0

2No

v-02

Mar-0

3Ju

l-03

Nov-0

3Ma

r-04

Jul-0

4No

v-04

Mar-0

5Ju

l-05

Total GSE MBA Prime

15Confidential Information – Copyright © First American Credco 2006

Foreclosure % by Credit type (quarter end)

Foreclosure Balances

0.00%2.00%4.00%6.00%8.00%10.00%Ma

r-01

Jul-0

1No

v-01

Mar-0

2Ju

l-02

Nov-0

2Ma

r-03

Jul-0

3No

v-03

Mar-0

4Ju

l-04

Nov-0

4Ma

r-05

Jul-0

5

Portfolio Private Label GSEMBAA Nonprime MBAA FHA MBA Prime

16Confidential Information – Copyright © First American Credco 2006

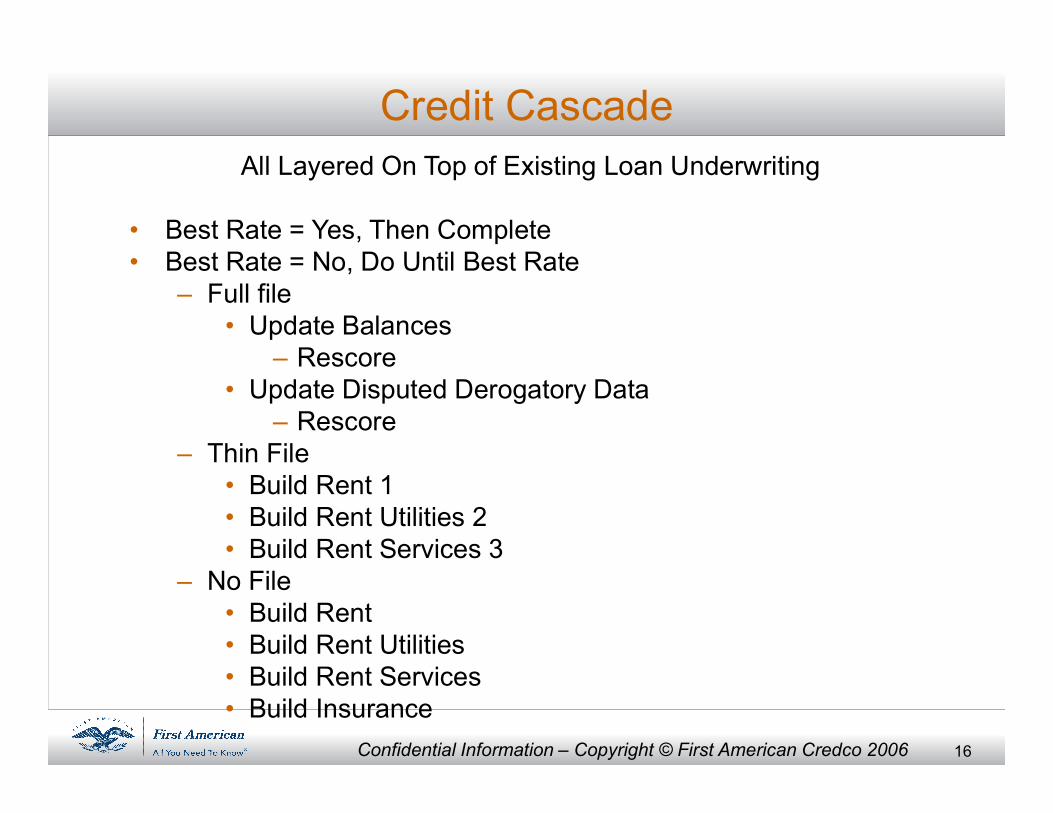

Credit CascadeAll Layered On Top of Existing Loan Underwriting

• Best Rate = Yes, Then Complete• Best Rate = No, Do Until Best Rate

– Full file• Update Balances

– Rescore• Update Disputed Derogatory Data

– Rescore– Thin File

• Build Rent 1• Build Rent Utilities 2• Build Rent Services 3

– No File• Build Rent• Build Rent Utilities• Build Rent Services• Build Insurance

17Confidential Information – Copyright © First American Credco 2006

Thank You

18Confidential Information – Copyright © First American Credco 2006