managing (inherently risky) banking markets: the ... filebangko sentral ng pilipinas 1) banking is a...

TRANSCRIPT

Bangko Sentral ng Pilipinas

Managing (Inherently Risky) Banking Markets:The Experience of the BSP

Nestor A. Espenilla, Jr.Deputy Governor, BSP

SEACEN-Bank IndonesiaHigh Level Seminar for Deputy Governors

Bali, Indonesia December 2010

Bangko Sentral ng Pilipinas

1) Banking is a business of leverage and gaps. It is inherently risky but, if managed, is value-enhancing.

2) Banks lend more when economic conditions improve. Thus, bank credit is pro-cyclical by nature.

3) Financial governance is a shared responsibility between the banks, the public and the banking supervisor.

4) The banking supervisor must be the one to define the prudential framework while interacting with others.

Our Working Premises

Bangko Sentral ng Pilipinas

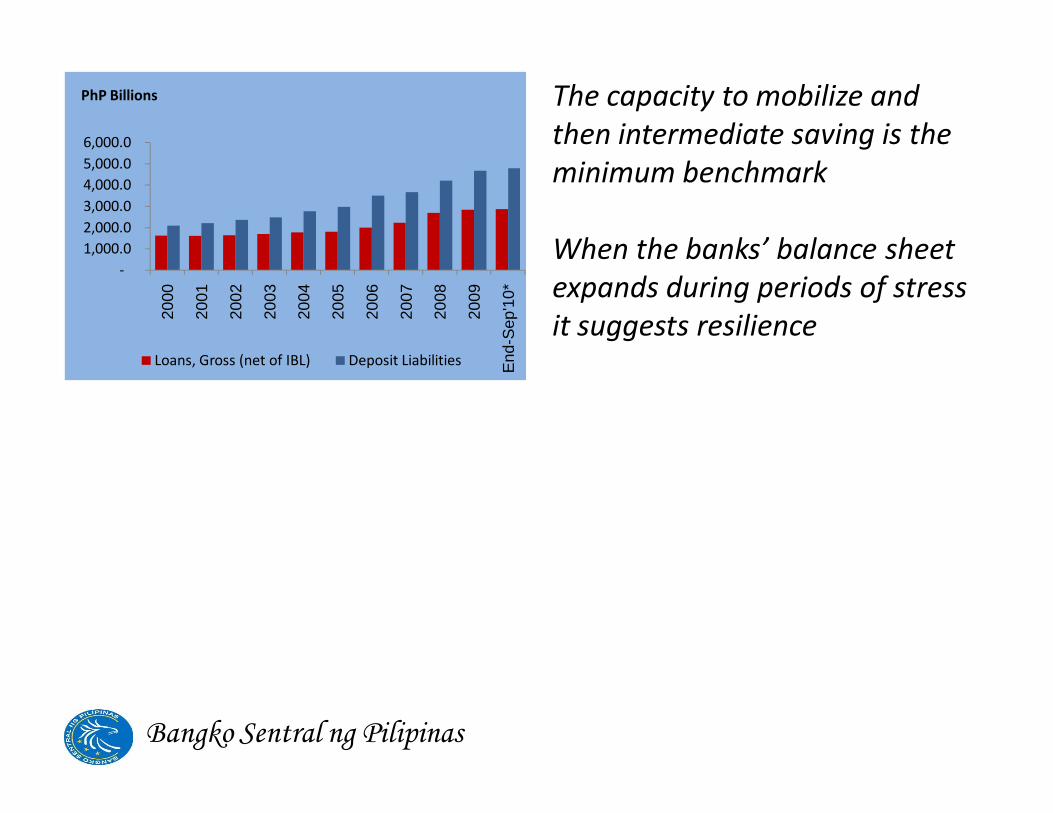

The capacity to mobilize and then intermediate saving is the minimum benchmark

When the banks’ balance sheet expands during periods of stress it suggests resilience

-1,000.0 2,000.0 3,000.0 4,000.0 5,000.0 6,000.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

End

-Sep

'10*

PhP Billions

Loans, Gross (net of IBL) Deposit Liabilities

Bangko Sentral ng Pilipinas

Capital remained consistently high even when the balance sheet was expanding

Bangko Sentral ng Pilipinas

Despite the extent of leverage, the balance sheet expansion occurred while the quality of the banks’ balance sheet clearly improved

Bangko Sentral ng Pilipinas

Financial Inclusion and Financial Learning have been hallmark advocacies.

Our inclusion program has recently been adjudged as among the best in the world

Bangko Sentral ng Pilipinas

-1,000.0 2,000.0 3,000.0 4,000.0 5,000.0 6,000.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

End

-Sep

'10*

PhP Billions

Loans, Gross (net of IBL) Deposit Liabilities

Bangko Sentral ng Pilipinas

A Perspective Reinforced by the Crisis . . .

Bangko Sentral ng Pilipinas

Terminology and Practice

• Terms like financial stability, macro-prudential and micro-prudential have been in use since the aftermath of the 1997 Asian financial crisis

• Recent work by the BIS study group on Corporate Governance and Financial Stability shows that

a) There is no universal definition of Financial Stabilityb) Current monitoring tools have been designed for specific

reasons … but macro-prudential indicators in a financial stability context have yet to be defined

• We need to contextualize the monitoring of banking behaviour to extend to its systemic implications

Bangko Sentral ng Pilipinas

A Fundamental Concern

=

• Capital• Asset Quality• Management• Earnings• Liquidity• Sensitivity to Risk

? CAMELS? Is CAMELS appropriate

for the system as a whole

? Are all the relevant risks covered

Bangko Sentral ng Pilipinas

Financial Market

Real Market

• Liquidity is central to what banks do

• Liquidity has micro and macro facets

Policy Handles

If Leverage is Impt … so is Liquidity

Bangko Sentral ng Pilipinas

If Leverage is Impt … so is Liquidity

1) Tenor matters

2) Pricing matters

3) Timing through the business cycle matters

4) Distribution matters

5) Risk appetite matters

Liquidity is not just about volume . . .

Bangko Sentral ng Pilipinas

Risks Need to be Properly Measured

• Standard categories of risks – Credit, Market, Ops –are necessary but not sufficient

a) Pillar 2 risks are importantb) In practice, risks are seldom stand-alone

• Risk models are meant to be simplified representation of market dynamics

a) Model parameters need to be re-calibrated for a particular market situation

b) The integrity of the model ultimately rests with the users of the model

Bangko Sentral ng Pilipinas

Putting All of These Together . . .

Bangko Sentral ng Pilipinas

The Challenges of Supervision

1) The “new normal”

2) Banks prefer the certainty

3) We need to analyze risks bettera) Better use of modelsb) Systemic risk

Bangko Sentral ng Pilipinas

The Challenges of Supervision

4) Liquidity will be key

5) Role of bank supervisors in financial stability

Bangko Sentral ng Pilipinas

The Challenges of Supervision

1) Enabling the new environment

2) Shorter phase-in period for changes

3) Sharper and broader analysis of risks

4) Key role of liquidity risk

5) Financial stability mandate

Bangko Sentral ng Pilipinas

Managing (Inherently Risky) Banking Markets:The Experience of the BSP

Nestor A. Espenilla, Jr.Deputy Governor, BSP

SEACEN-Bank IndonesiaHigh Level Seminar for Deputy Governors

Bali, Indonesia December 2010