marginal pricing of indian railway

DESCRIPTION

To understand the concept of marginal pricing by Indian railway. Concept of monopoly. Price Distribution Concept.TRANSCRIPT

Marginal Cost Pricing by Indian Railway

MBA RM

2015-17

Submitted to-

Dr. Ramakrushna Panigrahi

Prepared by-

Group 9

Bittu Samanta (UR15052)

Rohit Kumar Swain (UR15067)

ShilpaMariya George (UR15077)

Shobhan Kumar Meher ur15078 (UR15078)

SidhantNayak (UR15080)

Sumith S. (UR15085)

Marginal Cost Pricing by Indian Railways

Introduction: What is Marginal Costing?

Marginal costing is a technique for expense bookkeeping and choice making utilized for interior

reporting as a part of which just peripheral expenses are charged to cost units and altered expenses

are dealt with as a bump whole. It is otherwise called immediate, variable, and commitment costing.

Peripheral evaluating is in light of the presumption that since settled and variable expenses are

passed on by the present yield level, the expense of delivering any additional unit (minimal yield)

will include just of variable expenses of extra work and material expended.

Subsequently, the contention goes, any sum by which the offering cost surpasses the variable

expenses acquired by the peripheral yield will be immaculate benefit. Be that as it may, over the

long haul, this is a ruinous presumption on the grounds that the company's rivals will be forced to

cut down their expenses as well. Additionally, the customers will request these low expenses as the

standard while the firm, to survive, will even now need to guarantee its total income surpasses its

total costs. In peripheral costing, simply variable expenses are utilized to decide. It doesn't consider

altered expenses, which are thought to be associated with the time periods in which they were

caused. Minimal expenses include:

1. The expenses really expended when you make an item

2. The incremental increment in expenses when you increase generation

3. The expenses that vanish when you close down a creation line

4. The expenses that vanish when you close down a whole backup

In this procedure, cost information is given variable expenses and altered expenses indicated

independently with the end goal of administrative choice making. Negligible costing is not a system

for costing like procedure costing or employment costing. It is essentially an approach to investigate

cost information for the direction of administration, Rather, more often than not with the end goal of

comprehension the impact of benefit changes because of the volume of yield.

The immediate costing idea is to a great degree valuable for transient choices, on the other hand,

can prompt destructive results if used for long haul choice making, since it does exclude all

expenses that may apply to a more extended term choice. Besides, negligible costing does not

conform to outer reporting measures.

Basic Use Cases for Marginal Costing

Marginal costing can be an important gadget for surveying a couple sorts of choices. Here are likely

the most generally perceived situations where negligible costing can give the most advantage:

Automation investments: Marginal costing is helpful to decide the amount of a firm stands to pick

up or lose via computerizing some capacity. The key expenses to look into are the incremental work

expense of any representatives who will be ended versus the new expenses brought about from

hardware buy and resulting support.

Expense reporting: Marginal costing is exceptionally valuable for controlling variable expenses, in

light of the fact that you can make a change investigation report that contrasts the genuine variable

expense with what the variable.

Client benefit: Marginal costing can help figure out which clients merit keeping and which merit

disposing of.

Inner stock reporting: Since a firm must incorporate backhanded expenses in its stock in outside

reports, and these can set aside quite a while to finish, minimal costing is valuable for interior stock

reporting.

Benefit volume relationship: Marginal costing is important for plotting changes in benefit levels

as deals volumes change. It is generally easy to make a minor costing table that brings up the

volume levels at which extra peripheral expenses will be brought about, so administration can

assess the measure of benefit at diverse levels of corporate movement.

Outsourcing: Marginal costing is helpful for choosing whether to produce a thing in-house or keep

up a capacity in-house, or whether to outsource it.

Points of interest and Benefits of Marginal Costing

Expense control: Marginal costing makes it less demanding to focus and control expenses of

creation. By keeping away from the discretionary designation of settled overhead expenses,

administration can focus on accomplishing and keeping up a uniform and steady minimal expense.

Straightforwardness: Marginal costing is easy to comprehend and work and it can be consolidated

with different types of costing (e.g. budgetary costing and standard costing) without much trouble.

Disposal of expense difference per unit: Since settled overheads are not charged to the expense of

generation in minimal costing, units have a standard expense.

Fleeting benefit arranging: Marginal costing can help in transient benefit arranging and is

effectively shown with make back the initial investment diagrams and benefit charts. Near

productivity can be effortlessly surveyed and conveyed to the notification of the administration for

choice making.

Exact overhead recuperation rate: This technique for costing disposes of vast adjusts left in

overhead control accounts, which makes it less demanding to discover a precise overhead

recuperation rate.

Most extreme come back to the business: With peripheral costing, the impacts of option deals or

generation strategies are all the more promptly refreshing and surveyed, guaranteeing that the

choices taken will yield the greatest come back to the business.

Drawbacks and Limitations of Marginal Costing

Grouping expenses: It is exceptionally hard to discrete all expenses into settled and variable

expenses plainly, since all expenses are variable over the long haul. Subsequently such

characterization now and again may give misdirecting results. Besides, in a firm with a wide range

of sorts of items, minor costing can demonstrate less valuable.

Precisely speaking to benefits: Since the end stock comprises just of variable expenses and

overlooks altered expenses (which could be significant), this gives a bended picture of benefits to

shareholders.

Semi-variable expenses: Semi-variable expenses are either rejected or mistakenly broke down,

prompting twists.

Recovery of overheads: With marginal costing, there is often the problem of under or over-

recovery of overheads, since variable costs are apportioned on an estimated basis and not on actual

value.

External reporting: Marginal costing cannot be used in external reports, which must have a

complete view of all indirect and overhead costs.

Increasing costs: Since it is based on historical data, marginal costing can give an inaccurate

picture in the presence of increasing costs or increasing production.

Marginal Costing Can Be Helpful for Short-Term Decision Making

Marginal costing is a useful analysis tool which usually helps management make choice and

understand the answer to specific questions about revenue.

That said, it is not a costing methodology for creating financial statements. In fact, accounting

standards explicitly exclude marginal costing from financial statement reporting. Therefore, it does

not fill the role of a standard costing, job costing, or process costing system, all of which contribute

actual changes in the accounting records.

Still, it can be used to discover relevant information from a variety of sources and aggregate it to

help management with a number of tactical choices. It is most helpful in the short-term, and least

useful in the long-term, especially where a firm needs to generate adequate benefit to pay for a lot

of overhead.

Furthermore, direct costing can also cause problems in circumstances where incremental expenses

may change significantly, or where indirect costs have a bearing on the decision.

INDIAN RAILWAYS

The pretended by the Indian Railways in our nation's socio-political advancement is undeniable.

Aside from its expressed obligation of transporting men and merchandise over the length and

expansiveness of the nation, it has assumed a stellar part in times of common and man-made

catastrophes. The part of the railroads turns out to be much more significant to the advancement of

the nation as we enter the 21st century and the pace of the development of the economy quickens.

The requirement for a productive transportation division would turn out to be more pivotal with

each passing year. Along these lines it is fundamental for the Railways to stay aggressive, regarding

both expense and nature of administrations, to guarantee a proficiently working transport area in the

nation.

As is clear railroads frame some piece of the fundamental framework of the nation. Extensively all

foundation administrations can be partitioned into the accompanying two classes

1) Open Access Services : These administrations are those from which individuals can't be

effectively avoided, regardless of whether they have contributed financially to the foundation and

support of the administration or not. A few cases of this administration incorporate open lighting,

intra city streets and so on.

2) Limited Access Services : These administrations are those which can be given solely on a client

pays premise and the individuals who don't pay can be avoided from getting a charge out of the

advantages of this administration. These administrations in this way can act naturally financing.

Railways in a perfect world will fall in the last category, as it will not be too burdensome

assignment, making it impossible to counteract some person who has not paid for the administration

from taking the advantages of it. In India the railways now symbolize an institution which is there

to satisfy a social need and in addition a business one and on a regular this has prompted approach

mutilations far from the most financially solid ones. One by result of this impression of the

railroads has been the arrangement of cross-sponsorship of lower class travelers, which is the

classification with the most slender edges, by cargo administrations and higher class travelers, who

give the heftiest edges. This has prompted a serious money related smash in the Indian Railways

and as result the railways has neglected to pay a profit to the legislature without precedent for a long

time. Further its capacity to put resources into offices needed for modernizing the railways has

additionally endured a body blow

according to the liberalization arrangements of the Narasimha Rao government the railroads

confronted more difficulties. As the nation coordinated with the worldwide economy all costs in the

economy needed to adjust themselves to those appealing in the global markets. Along these lines as

costs of transport administrations fell worldwide the normal insurance that the residential segment,

including the railways, delighted in turned into good days gone by. In the meantime it faced

expanding levels of competiton from different wellsprings of transport from inside of the economy

a) Post deregulation of the trucking business the roadways have caught an immense piece of the

railroad of the overall industry. This has been fulfilled with expanded client introduction,

adaptability and lower expenses for short separation courses.

b) The improvement of freeways and six path parkways have just prompted the level of competition

being offered by the road segment expanding all. With the declaration of the 'Brilliant Quadrilateral'

venture the opposition to the railways can just increased.

c) Petroleum things once a fortress of the railroads, has been progressively moving towards

investigating pipelines as the most appropriate method of transport.

d) Coastal Shipping and Inland Waterways have proceeding taken away piece of the pie from the

railways, with the Government giving dynamic support as far as good strategy choices. Items like

concrete and coal have progressively begun using these as the most used method of transportation.

With a course length of 62,462 Km, running track stretching out to 79,188 Km of which about

22,000 Km, are energized, 7202 trains, 3,527 Electric Multiple Unit Coaches, 36,000 routine

mentors 3,15,000 wagons and lifting 400 million tons of cargo, 3800 million travelers for each year,

and utilizing 1,63 million staff, Indian Railways is the biggest railways system on the planet. Its

administration vests with the Railway Board consisting of 6 individuals and a Chairman, the

previous working as Ex-officio Secretaries to Government of India and the recent as Ex-officio

Principal Secretary to Government of India. They have added to national combination and have

advanced the improvement of in reverse ranges by powerful opening up of characteristic assets in

distinctive areas of the nation. Clearly, such a major and complex framework will call for

monstrous assets for its operation. Its to gross income surpasses Rs. I8, 000 crores and expenses

surpass Rs. 16,500 crores for every year. Indian Railways are the main examples in the realm of

procuring benefits, specially in the course of the last 6-8 years on regular basis. It's evaluating and

funds are, in this way, of vital noteworthiness.

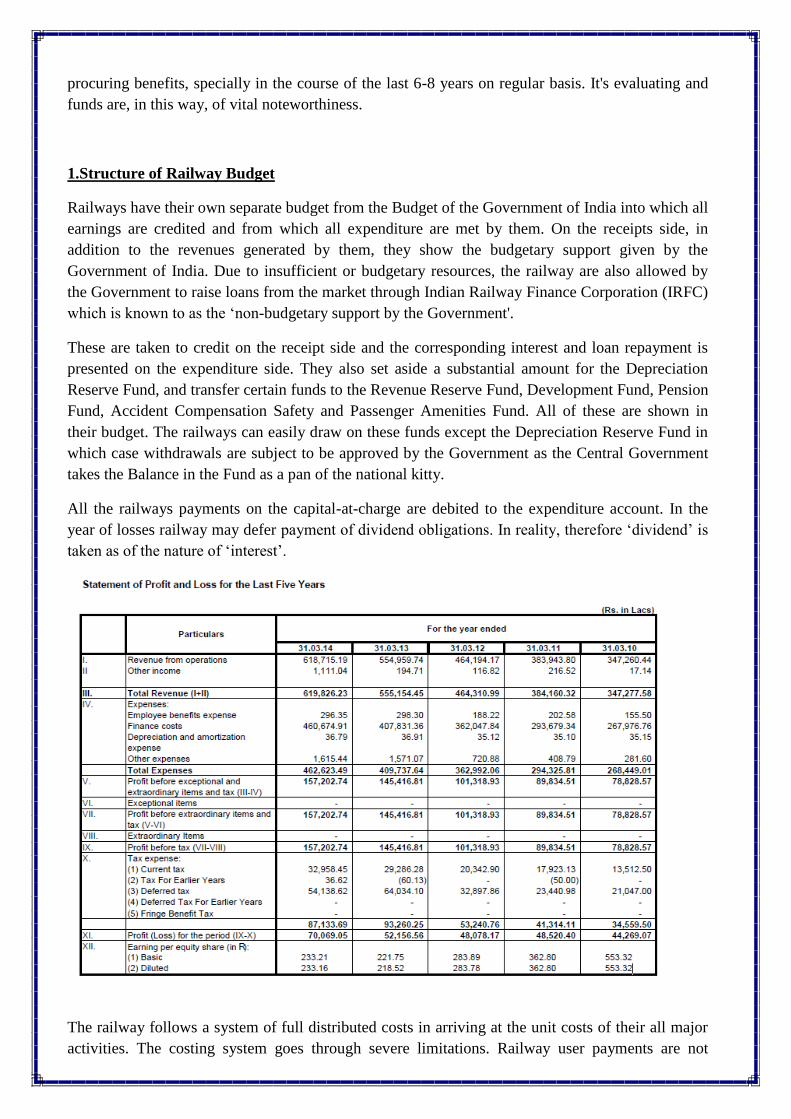

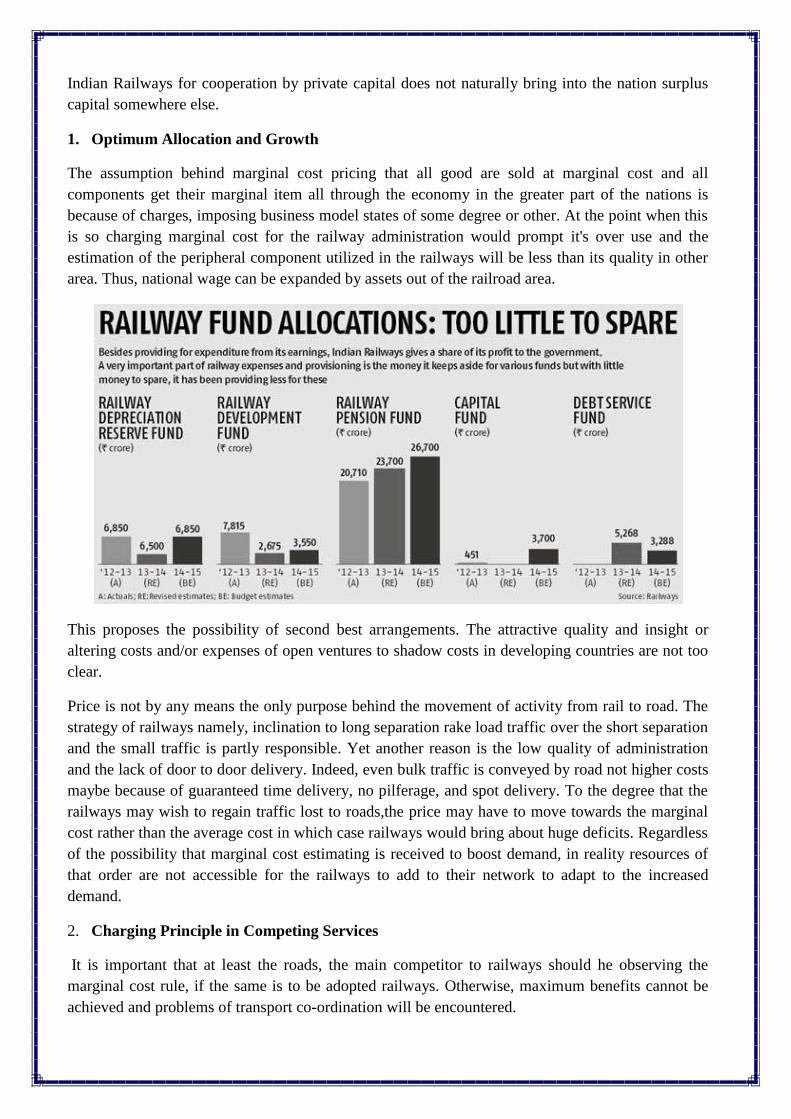

1.Structure of Railway Budget

Railways have their own separate budget from the Budget of the Government of India into which all

earnings are credited and from which all expenditure are met by them. On the receipts side, in

addition to the revenues generated by them, they show the budgetary support given by the

Government of India. Due to insufficient or budgetary resources, the railway are also allowed by

the Government to raise loans from the market through Indian Railway Finance Corporation (IRFC)

which is known to as the ‘non-budgetary support by the Government'.

These are taken to credit on the receipt side and the corresponding interest and loan repayment is

presented on the expenditure side. They also set aside a substantial amount for the Depreciation

Reserve Fund, and transfer certain funds to the Revenue Reserve Fund, Development Fund, Pension

Fund, Accident Compensation Safety and Passenger Amenities Fund. All of these are shown in

their budget. The railways can easily draw on these funds except the Depreciation Reserve Fund in

which case withdrawals are subject to be approved by the Government as the Central Government

takes the Balance in the Fund as a pan of the national kitty.

All the railways payments on the capital-at-charge are debited to the expenditure account. In the

year of losses railway may defer payment of dividend obligations. In reality, therefore ‘dividend’ is

taken as of the nature of ‘interest’.

The railway follows a system of full distributed costs in arriving at the unit costs of their all major

activities. The costing system goes through severe limitations. Railway user payments are not

rationally link to costs. The predicament of the users, as shown such as that fare and freight charges

are high and that they are being hiked too often without improvements in the quality of service is

explained by not relating the user payments to costs.

Clarifications behind the troublesome resources position of railways are various. The most basic is

that they are looked upon as open utility organizations regardless of the way that the game plan as

per the Indian Railway Act is one of rail lines to limit as business endeavors. In view of this

overwhelmed interpretation, populist measures are taken after for occasion charging the railroad

customers much underneath cost in appreciation of explorers, specialists and certain items like

sustenance grains, salt, sugarcane, food, manures, natural items, vegetables, etc.

Thus, the disasters realized on this record and from the operation of uneconomic lines are mounting.

The evaluating course of action in a split second took after is suggested to be regulated by the

principles of cost of organization and the estimation of organization with cross sponsorship of

hardship making organizations from the surplus on load action.

The weight for resources for financing Five Year Plans of the Government of India and the need to

give less costly railroad transport to progressing speedier improvement has provoked either creating

of overpowering mishaps or delivering fringe surpluses that are unreasonably deficient, making it

difficult to back rail course headway. There is a reluctance to spend attractive aggregates on

genuine upkeep of the railroad assets in light of the benefit crunch.

It might be seen that railroad organizations are sold to individuals when all is said in done and along

these lines railways can utilize client slant or choice to draw in the stores expected to deal with the

customers request. By excellence of control on confirmations, salary raised from rail customer

charges were found lacking for enthusiasm for railways. On the other hand railways were starving

of budgetary sponsorship for theory. Under the New Economic methodology, the railways told that,

if they raise more inside resources, they can have a greater Investment Plan. With this, the accent is

more on the right assessing of the railroad organizations for finishing powerful resource part and

perfect headway of rail line transport as a middle base industry.

2. Evaluating Considerations

An evaluating system serves the twofold limit of

(a) appropriating a given sum or strike course servicers in order to serve the best need of the best

number and

(b) supplying the appropriate measure of railroad organizations and conveying than in the an

extensive part of way. Its application to railways is rendered troublesome in light of the way that

railways, not in any way like some distinctive organizations, have largo fundamental costs (joint

cost) which are difficult to scatter amongst different things or organizations in any plan of

evaluating. Consequently, noteworthy alteration is relied upon to suit the perceiving traits like that

of joint costs and also the unmistakable parts which the Government would like the railways to look

for after.

Certain characteristics of railways are of unfathomable essentialness to their esteeming.

i) Sunkenness of cost.

At the point when a railroad is fabricated it can have no other usage however to give rail transport

along its course. It can't be secured and excess point of confinement in any one piece can't be made

available at some other place or time. Henceforth, unutilised farthest point has no alternative

utilization in the short run and its monetary matters quality is zero.

ii) Lumpiness of endeavor

A base endeavor central before the point of interest can be utilized by any stretch of the creative

ability. Likewise, theories take after a stage limit. They can be made just in a certain quantum. A

valid example, paying little respect to the way that a huge bit of a train is obliged, one full loco of a

given cutoff must be secured.

iii) Cremation of high farthest point early

In light of long time required for creation restrict, the breaking point must be made before hobby.

Thusly, if interest fails to show up or does not develop to the degree expected, it would provoke

unmoving breaking point. Railroad wanders, thusly, run the threat of unmoving utmost.

iv) Joint Cost and the bye-thing nature of railroad organizations

On the same railroad track, particular sorts of trains are run and in the railroad workshops

heterogeneous things are made for usage in assets like the rails, guides, wagons, prepares et cetera.

This makes division of costs to unmistakable things incredibly troublesome.

v: Decreasing cost with longer division completely dry dynamic squares of yield

The railways offer with other broad framework tries, budgetary parts of scale. This is the system for

thinking behind telescopic rates.

vi) Continuity or capital stock

The railroad framework, it may be said, can never be completely supplanted. To deal with

additional interest it is only essential to add to or change the present capital stock. The track, if truly

kept up, can be a tried and true asset. This makes connected inconveniences for describing costs.

As an unfathomable attempt of the Government, if railways are obliged to limit like business

undertaking they have to fit in with budgetary and business duties as are ordinary to each and every

business enterpris. A quality methodology which is fitting for railways must he chose in the

association of the going with standards;

• Pricing of railroad organizations should be, for instance, to yield a net give back that contrasts

with the lack estimation of capital in the economy;

• The quality charger for the railroad office must have a snug relationship to the costs of giving it;

and

▪ Monopoly assessing is to be kept up a vital separation from as it is thought to be against open

leisure act.

Indian Railway Act 1989 courses of action with Fixation of Rates.

• Section30(1)

•The Central Government may from time to time,by general or exceptional solicitation fix, for the

carriage of explorers and items, rates for the whole or any bit of the railroad. Differing rates may be

modified for unmistakable classes of stock, and show in such demand the conditions subject to

which such rates may apply

•Section30(2).

•The Central Government may by a like solicitation, modify the rates of whatever different charges

circumstantial to or connected with such carriage, including demurrage and wharfage, for the whole

or any bit of the railroad, and focus in the solicitation the conditions, subject to which such rates

ought to apply.

3, Full Cost Pricing

Under full cost assessing total costs or the railways should be detached among all customers. Where

the costs fluctuate beginning with One railroad then onto the following, portion should on an

essential level be related to individual rail courses: regardless, for all intents and purposes, they are

related to costs of the rail course structure when all is said in done.

Full cost assessing works through the typical cost charging framework as a singular or a two-area

demand. Under both the schedules, customers are subjected to uniform rates; yet the two-segment

obligation incorporates an adjusted and a variable toll while the two fragments are blended into one

under the single part require.

If there is to be no was wastage of advantages, the assessing standard should breaking point

excursions or action regarded at not precisely the costs and stimulate voyages regarded at more than

the costs they cause. This suggests that under equalization esteem should comparable costs

including that of wear and tear, and obstructing costs. Typical cost assessing prompts inefficient

resource part as it disregards the upgrading standard. A valid example, customers of uncongested

railways would get swindled and those of congested courses undercharged, realizing plenitude

demand on congested courses which can't be by SRMC esteeming. The second reason must be

played down altogether by virtue of a country like India where the upkeep of points of interest

neglect to inspire anybody.

LRMC fuses all costs, settled furthermore variable. There are inconveniences of choosing the

LRMC by virtue of railways in light of their characteristics discussed some time recently. As a

strategy for getting away from these inconveniences, the framework for treating capital utilization

in a given year as a present thing was suggested and grasped by the U.K. Transport Ministry. lf this

is recognized, LRMC evaluating means a worth proportionate to capital costs in any given year

notwithstanding the variable costs in that year, per unit of yield. This can't be recognized since it

conflicts particularly with the considered capital enthusiasm for any try figured on a substitution

preface clearly go into insignificant cost and any attempt to set expenses on such a reason is

opposite with fringe cost esteeming. It may in like manner be seen that when in concordance,

SRMC and LRMC, are proportional and a while later there need be no reduction in yield

Two imperative issues ascend out of these two esteeming regulations

1. Loss of yield under ordinary cost assessing,

2. Ascent of deficiencies under fringe cost assessing which has results for endeavor stores dry

transport of compensation.

As the condition 'Worth makes back the initial investment with Marginal Cost' ensures perfect out-

put, it is battled that the deficiency must be secured by assignments if the capital stock is to be

energized and such a system is attractive over the choice of setting the expense satisfactorily high to

recover its costs. For, this would put society on a lower of satisfaction than if the railroad

workplaces were esteemed at fringe cost and adversities secured through gift. The challenges to

fringe cost assessing are without a doubt caught on. We simply demonstrate to them here for

satisfaction.

The challenges are:

1. Benefit will be missing to meet the costs and there will defenselessness about inadequacies being

secured.

2. The consequent transport of points of interest will be instead of enquiry thought.

3. A couple costs are constrained on outcasts and the people who bear these costs will no doubt be

not able to assemble the points of interest. Basically a couple points of interest may be introduced

on outcasts who can't be made to contribute towards meeting the cost.

4. It is difficult to perceive the costs of differing organizations and where whimsies gets in the need

of an organization, some sort of immaterial costing esteeming may get the opportunity to be critical.

5. Insignificant costs are not charged in the straggling leftovers of the economy or battling

organizations like the road. In this way, utilization of immaterial costing rule in railways alone is

certain to provoke bendings in task of advantages.

6. It is hard to say whether railroad organizations are made under decreasing, developing steady

costs.

4. Choice or Price Policy

Before keeping on examining whether typical or Marginal cost esteeming is appealing for Indian

Railways, we should note that the choice must be critical to goals of methodology and institutional

framework to which it applies. Particular sorts of esteeming lead to samples of benefit utilization. A

worth course of action that is seen as suitable for a surrendered target finishes being tasteless when

goals of methodology difference. All things considered, esteeming considerations imperative to the

Indian commonplace portion and in converse extents won't related to the urban and made part.

The purposes of Indian money related system can be put into the going with general orders:

1. Advance perfect theory and higher improvement of the economy.

2. Finish updates in quality and benefit through engaging contention.

3. Urge tolls to handle the leveling of portions issues.

4. Plan resources for financing change extraordinarily the middle divisions like agriculture, nation

headway, wellbeing, power and other crucial structure.

5. Joining of Indian economy with the overall markets.

6. Wipe out all obstructions to free segment and inflow of capital by deregulation and privatization.

On a fundamental level, these focuses require not conflict with evaluating methodology on

railways. In any case, all the time railroad expenses are associated with them. It justifies taking a

gander at the above destinations the railways in fairly more detail. In case the esteeming

methodology is not honest to goodness, railways won't have enough internal resources and with

potential results of getting budgetary sponsorship be propelling "Nil" and the private hypothesis not

imminent, lacking hobbies in rail lines would genuinely impact the improvement of the economy.

To be perfectly honest, capital enthusiasm for railways depends on the openness of grams from

general society exchequer to meet the deficiency between endeavor obliged and what can be met

from inside resources.

As the railroad transport expense shapes an exceptional part of aggregate offering so as to assemble

expenses,to attempt achieving larger exports by offering lower freight charges is uncertain to

generate better performance in exports. Experience uncovers that the railroad cargo structure which

incorporates motivators for mass things like iron metal, has not prompted a great part of the sought

results. A superior edge ought to be found in creating quality items in aggressive costs or utilizing

iron metal as a part of the nation itself for fare of made iron and steel of high caliber.

More resource mobilisation is constrained by expanding arrangement consumption and absence of a

return on investment in public sector projects. Since, asset crunch is defying all divisions estimating

arrangement of the railroads ought to go for creating more surpluses without yielding the quality of

service. Marginal surpluses or negative surpluses and reliance on budgetary support intensify the

nation's income and financial shortfalls bringing about solid inflationary weights.

Competition is important when the principles of the the game obtained all round. In a flawed

business sector framework, railroads alone receiving the negligible expense evaluating can't

guarantee enhancements in quality of service or its productivity. Despite what might be expected,

with deficiencies glaring in the eyes even marginal investment required for quality change and

higher profitability come elusive.

Globalization concentrates on faster industrialisation exploiting universal division of work. This

can't be the exclusive concern of the railways alone. While effective railway transport can just add

to auspicious developments of merchandise and individuals, it can can seldom achieve integration

all by itself. It is far-fetched that the Indian Railways can play any major direct part in this matter.

The last target of free entry/inflow of remote capital is a non-valuing issues. Financial controls and

authorizing should be removed for foreign capital to come to areas open to it. Administered prices

scare away new participants and additionally capital. While railways are still subject to some sort of

regulated cost or the other, no special advantage can be guaranteed.

In favor of privatization, the massive or lumpy investments with long development periods appear

to be far beyond the reach of the private sector. More than this, just exercises which are profoundly

gainful can draw in capital, either domestic or international. This likewise falls into none-price

phenomena. It should be further mentioned that a choice to throw open productive fragments of the

Indian Railways for cooperation by private capital does not naturally bring into the nation surplus

capital somewhere else.

1. Optimum Allocation and Growth

The assumption behind marginal cost pricing that all good are sold at marginal cost and all

components get their marginal item all through the economy in the greater part of the nations is

because of charges, imposing business model states of some degree or other. At the point when this

is so charging marginal cost for the railway administration would prompt it's over use and the

estimation of the peripheral component utilized in the railways will be less than its quality in other

area. Thus, national wage can be expanded by assets out of the railroad area.

This proposes the possibility of second best arrangements. The attractive quality and insight or

altering costs and/or expenses of open ventures to shadow costs in developing countries are not too

clear.

Price is not by any means the only purpose behind the movement of activity from rail to road. The

strategy of railways namely, inclination to long separation rake load traffic over the short separation

and the small traffic is partly responsible. Yet another reason is the low quality of administration

and the lack of door to door delivery. Indeed, even bulk traffic is conveyed by road not higher costs

maybe because of guaranteed time delivery, no pilferage, and spot delivery. To the degree that the

railways may wish to regain traffic lost to roads,the price may have to move towards the marginal

cost rather than the average cost in which case railways would bring about huge deficits. Regardless

of the possibility that marginal cost estimating is received to boost demand, in reality resources of

that order are not accessible for the railways to add to their network to adapt to the increased

demand.

2. Charging Principle in Competing Services

It is important that at least the roads, the main competitor to railways should he observing the

marginal cost rule, if the same is to be adopted railways. Otherwise, maximum benefits cannot be

achieved and problems of transport co-ordination will be encountered.

Since Indian Railways charge a price which is less than the marginal cost for some commodities

and higher on some others, more of the former traffic is attracted to railways, consequently the

major contributing factor for railways deficits does not shift. On the contrary, it has a tendency to

increase, leading to an increase in deficit. The same reason also leads to over utilisation in certain

routes and its capacity in some others.

When marginal pricing is not followed by the competitor like roads, asking the railways to adopt

marginal cost pricing is common. The road users in India pay more than the total cost of road

provision. Thus when cost plus pricing prevails in the road sector, adoption of marginal cost pricing

in roads amounts to transition from higher cost pricing to marginal cost pricing whereas in respect

of railways, It is one of movement from below marginal cost and average cost plus pricing towards

marginal cost pricing.

If price is made equal to marginal cost in both the railways and roads, there would no doubt be an

efficient allocation between railways and roads, but there would be over utilisation of transport

services in relation to other sectors of the economy where average cost plus pricing tends to prevail.

Thus, adopting MC pricing in both the sectors is impracticable, politically and financially

unacceptable.

An approximation to average cost pricing for both roads and railways seems to be feasible. The rise

in price of railways from below marginal cost to average cost will help eliminate deficits. It should

be reiterated that any particular form of pricing cannot be advocated for railways ignoring what

prevails in the competing modes of transport.

3. Resource Mobilisation: International Surpluses

There can be several reasons for building up intentional surplus in the Railway Budget.

Firstly, Railways are to pay the dividend or 7% on the Capital-at-charge which is given

to them as a loan in perpetuity.

Secondly, in the new Economic Policy, railways are required to function more as a

commercial enterprise in which case the dependence on the general budget for both revenue and

development needs is either reduced or eliminated. Particularly in the budget of the Railways of

1996-97, the budgetary support is only Rs.1269 crores or 15.6%. The balance 84.4% of the total

will have to be generated by the railways from their internal resources. In fact, the future

development of the railway modernisation and providing adequate and efficient railway transport

depends upon the size of the surplus. In the event of losses, railways will be compelled to reduce

their development but also to seek loans from the Government for meeting the losses.

Thirdly, transport cost in manufacturing form s a negligible proportion except in case of

a low value commodity like coal or bulk commodity like iron and steel, cement etc. The transport

cost as such is spread over a very large output catering to the consumers throughout the length and

breadth of the country. Where there are experts making use of the railway transport, the incidence

of freight falls on the foreign consumers. Therefore, generating surplus poses no threat of

stimulating inflationary pressure in the country.

Fourthly, the contribution to the general budget made by the railway earnings will

finance the development ire other sectors. In this way, benefits of overall growth come back to the

Railways in the form of increased demand for railway transport. Thus, there will be a feedback and

the surplus is a payment for the amounts that accrue to the railway users from development.

Finally, the direct relationship between payment by users and benefits of travel received

by them renders, unlike taxes which are not quick payments, railway fares and freights a payment

for service. Surplus may have repercussions on the demand as well as on tolerance of the general

public especially the commuters. But in so far as the benefit is conferred, payment covering the cost

of the services need not be less attractive.

However, it needs to be mentioned that transport is in a large measure an intermediate good and a

very steep hike in fare and freight can have repercussions in the production of a wide range of

outputs. Reliance on railway user payments to create surplus should not be at the cost of diversion

of traffic and more distortions in the economy.

8.Redistributive Function

Income redistribution is not a direct objective of the New Economic Policy, which aims at a higher

growth rate. Reduction in income inequality is to be achieved indirectly through higher growth of

the Indian economy. Therefore, Railway pricing is not to be assessed from the view point of

achieving income redistribution.

The level of inequality and its changing pattern has raised some issues. The degree of concentration

of wealth and overall income inequality has somewhat increased in the urban sector. Distribution of

income in the rural sector is also becoming less equal. Again, distribution varies among different

occupational classes like salaried employees, self-employed and the owners of property. Available

data show that contractors among the self-employed have greatly improved their position and those

engaged in transport, manufacturing and financial policies are also fairly well off.

Changes in the method of railway pricing inevitably cause changes in the distribution of income.

The way in which pricing affects different sectors or occupational classes depends on the manner in

which earnings from the pricing system are used. In the present pricing system, there is a transfer of

income from freight customers to passenger customer.

In the case of industrialists and businessmen the incidence of higher pricing will not fall on them

because they may be shifted to the consumers of the goods produced or sold. In the case of

passengers and commuters whose travelling expenditure is not met either by their employers or

from sources other than their income (salary) the incidence will rest with them. While this may not

lead to any pressure on inflation, shifting of higher railway price in the case of freight can be

inflationary.

But it is difficult to say what actually the distribution effect in case of non-railway users is. In the

case of rising of freight on items like food-grains, fertilisers etc., the effect on distribution of

income will be marked in the case of poor farmers within the agricultural sector. As contractors and

those engaged in business and industry make use of railways to a greater extent than others, the fact

of railways getting higher revenue from the better-off sections may be a welcome effect. But one

cannot be sure that among the non-railway users, benefits have accrued to only those who are in the

low income groups.

Intentional surpluses are to be achieved in the railway budget not as a fleeting feature. The surplus

in the railway budget has two consequences: one is that investible funds become available to the

railway for investment. The other aspect is the relation of the surplus to the general budget. With a

reduction in the budgetary support to the railway, the overall budget deficit has been reduced. In

fact, in 1995-96, the budgetary deficit of Government of India was Rs 7,600 crores. The deficit

would have been more, by Rs. 1583 crores had the railways not paid the dividend (Rs 1583

Crores)on the capital-at-charge in that year. The point that is to be emphasized is that the influence

of the larger surplus on the general budget would be in the form of assisting the Government of

India in reducing both its revenue deficit and the fiscal deficit, and at the same time enable the

railways to maintain a rate of growth which can sustain a higher growth rate of the Indian economy.

Why should railway users be made to pay high charges for leaving a large surplus which will be

used to ease the deficits of the General Budget? It may not be used for financing any expenditure

from which they do not derive any additional traffic benefit. In so far as the surplus is earmarked for

the railway development providing coaching services in suburban passenger services in

metropolitan cities like Bombay, Calcutta and Chennai where they operate Electric multiple Unit

and Non-Electric Multiple Unit services.

9. Problems and issues

Indian Railways is deep in the red and reported a loss of ₹30,000 crores (₹300bn) in the traveler

section for the year closure March 2014. Working proportion, a key metric utilized by Indian

railroads to gage budgetary wellbeing, is 91.8% in the year 2014-15. Railroads convey a social

commitment of over ₹20,000 crores (₹200bn $3.5bn). The misfortune per traveler km expanded to

23 paise before the end of March 2014. Indian Railways is left with a surplus money of just ₹690

crores (₹6.9bn $115mn) before the end of March 2014.

It is evaluated that over ₹ 5 lakh crores (₹5 trillion) (about $85 bn at 2014 trade rates) is obliged to

finish the continuous ventures alone. The railroad is reliably losing piece of the pie to different

methods of transport both in cargo and travelers.

New railroad line ventures are frequently reported amid the Railway Budget every year without

securing extra financing for them. In the most recent 10 years, 99 New Line ventures worth ₹

60,000 crore (₹600bn) were authorized out of which one and only venture is finished till date, and

four undertakings are as old as 30 years, however are still not finish for some reason.

One of the undeniable reasons of the decay of the piece of the pie of the railroads is the proportion

of its cargo admissions to its traveler passages, which is one of the most elevated on the planet.

Aside from the expense edge, the low quality of the administrations that the railroads give had

additionally prompted its losing piece of the overall industry to its rivals. Transport models in the

course of the most recent couple of decades have been driven by expense diminishment and

expanded rate of cargo development. This has prompted the advancement of a multi modular

arrangement of transport including containerization of cargo and intuitive coordination between

railroads, ports and roadways. In this manner, the disregard of containerization of cargo has

additionally prompted the railroads dropping out of numerous clients thought set.

Sanjay Dina Patil an individual from the Lok Sabha in 2014 said that extra tracks, stature of stages

are still an issue and ascend in tickets, products, month to month passes has made a disturbing

circumstance where the common man is troubled..

10. Restructure Railway Finance

It is interesting to know the practice which obtains in some of the countries like Great Britain,

Germany, France and Switzerland. In these countries, while the Railways have their own pricing

policy based on cost plus pricing, the Government gives subsidy to the Railways where their

services are priced at below cost.

Indian Railway finances should get restructured to suit the requirements of the commercial

enterprise. Taking the total financial scenario of our country, further continuance of indiscreet

subsidies and neglecting efficiency in financial management of railways can only lead to further

destabilizing and destroying one of the most successful public enterprises of the government of

India. The resource requirements of the Indian Railways are enormous and the restructuring of their

finances brooks no further delay.

BIBLIOGRAPHY:

Mathew M. O. (1964). Rail and Road Transport in India – A Study in Optimum Size and

Organisation. Book Agency, Culcutta.

Anand, Y.P. (1998). Reforming Indian Railway Financial Management. Readings in Indian

Railway Finance, An Academic Foundation Publication, Delhi.

Dalvi, M.Q. (1998). Value Capture as a Method of Financing Rail Projects: Theory and

Practice. Readings in Indian Railway Finance, An Academic Foundation Publication, Delhi.

Iqbal, H. (1998). Business orientation on Indian Railway through cost management.

Readings in Indian Railway Finance, An Academic Foundation Publication, Delhi.

Nanjundappa, D.M. (1998). Railway Pricing and Finances in India. Readings in Indian

Railway Finance, An Academic Foundation Publication, Delhi.

Railway Traffic Enquire Committee. (1980). Citied in Poulose, A.V. Readings in Indian

Railway Finance, An Academic Foundation Publication, Delhi.

Sriraman, S. (1998), Financing Railway Infrastructure in India. Readings in Indian Railway

Finance, An Academic Foundation Publication, Delhi.

Subramaniam, K.S. (1998). Operation- Finance Interface in Indian Railways. Readings in

Indian Railway Finance, An Academic Foundation Publication, Delhi.

Ramsunder, A, V. (1987). Productivity in the Indian Railways 1960-61 to 1984-85. Mimeo,

Railway Board, Delhi.

Kundu, A. (1995). Alternative methods of financing investment in Indian Railways-

Economics of borrowing through Indian Railway Finance Corporation. Unpublished

doctoral dissertation, Jawaharlal Nehru University, Delhi.

Raghuram, G., & Gangwar, R. (2008). Indian Railways in the Past Twenty Years Issues,

Performance and Challenges. Working Paper No. 2008-07-05, Research and Publications,

Indian Institute of Management, Ahmedabad. Sharma, A.K., & Manimala, M.J., (2008).

Sustainability of the Indian Railways Turnaround: A Stage Theory Perspective. Working

Paper no.266, presented at The International Workshop on Innovation and Entrepreneurship,

held at Cankaya University, Turkey. Gupta. D., & Sathye, M. (2007). Financial turnaround

of the Indian Railways: Good Luck or Good Management. ASARC Working Paper 2008/06.

Readings in Indian Railway Finance- By K. B. Verma 1998