marine solutions: growth through a smart marine ecosystem

TRANSCRIPT

MARINE SOLUTIONS:GROWTH THROUGH A SMART MARINE ECOSYSTEM

Roger Holm,President, Marine Solutions & Executive Vice President

© Wärtsilä PUBLIC2

Positive global economic conditions support shipping tonnage demand growth, while political and regulatory uncertainty limit the market recovery

MARINE MARKETS AND DRIVERS

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018(f

)

2020

World seaborne trade and GDP

GDP growth

Seaborne trade growth

-500

0

500

1 000

1 500

2 000

2 500

201

3

201

5

201

7

201

9

202

1

202

3

202

5

202

7

202

9

Historical Forecast

No o

f vessels

Deliveries, removals and net fleet growth

Net fleet growth

Removals

Deliveries

Source: Clarksons Platou

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jan

-2014

Ma

r-2014

Ma

y-2

014

Jul-2

014

Se

p-2

014

Nov-2

014

Jan

-2015

Ma

r-2015

Ma

y-2

015

Jul-2

015

Se

p-2

015

Nov-2

015

Jan

-2016

Ma

r-2016

Ma

y-2

016

Jul-2

016

Se

p-2

016

Nov-2

016

Jan

-2017

Ma

r-2017

Ma

y-2

017

Jul-2

017

Se

p-2

017

Nov-2

017

Jan

-2018

Ma

r-2018

Newbuilding price index Yr/Yr change

Oil Tanker

Dry Cargo

Bulkcarrier

Gas Carrier Newbuilding Price Index

Newbuilding Price Index

Containership Newbuilding Price

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

Jan

-2014

Ap

r-2014

Jul-2

014

Oct-

2014

Jan

-2015

Ap

r-2015

Jul-2

015

Oct-

2015

Jan

-2016

Ap

r-2016

Jul-2

016

Oct-

2016

Jan

-2017

Ap

r-2017

Jul-2

017

Oct-

2017

Jan

-2018

Ap

r-2018

Clarksons average earnings (USD/Day)

ClarkSea Index

Tanker

Bulker

LPG Carrier

Containership

Containership Newbuilding Price

31 May 2018 Roger Holm

© Wärtsilä PUBLIC3

Despite higher oil prices, US onshore production growth delays the offshore recovery

OFFSHORE MARKETS AND DRIVERS

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

E&P capex spend, MUSD difference %

Offshore Onshore

0

50000

100000

150000

200000

250000

300000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

MU

SD

Offshore E&P capex

Ultra deepwater (1500+ meter)Deep water (125-1500 meter)Shelf (to 125 meter)

Source: Clarksons Platou, Rystad Energy

35%

25%

15%

5%

-5%

-15%

-25%40

45

50

55

60

65

0

10

20

30

40

50

60

70

80

Jan

-2016

Ma

r-2016

Ma

y-2

016

Jul-2

016

Se

p-2

016

Nov-2

016

Jan

-2017

Ma

r-2017

Ma

y-2

017

Jul-2

017

Se

p-2

017

Nov-2

017

Jan

-2018

Ma

r-2018

US

D/b

bl

Oil price and Clarksonsoffshore index

U.K., Brent Blend Spot Average Oil Price (USD/bbl)

Clarksons Offshore Index

31 May 2018 Roger Holm

© Wärtsilä PUBLIC4

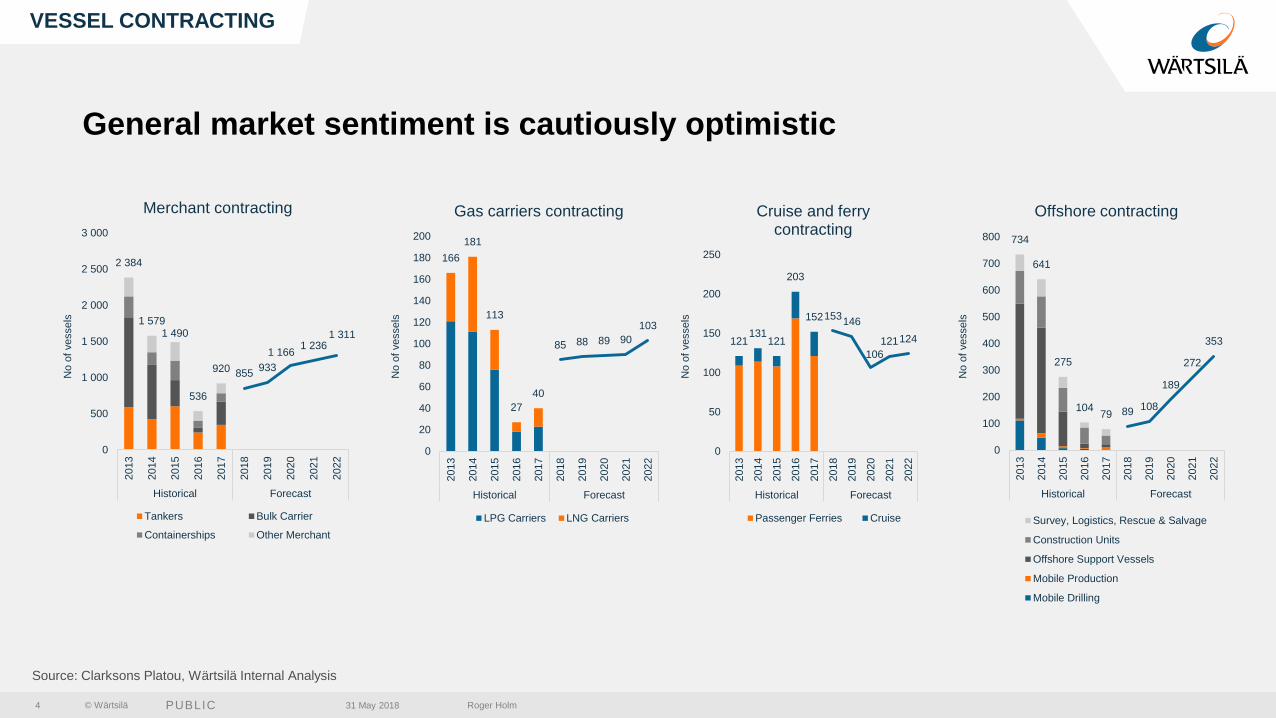

General market sentiment is cautiously optimistic

VESSEL CONTRACTING

2 384

1 5791 490

536

920 855933

1 1661 236

1 311

0

500

1 000

1 500

2 000

2 500

3 000

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Historical Forecast

Merchant contracting

Tankers Bulk Carrier

Containerships Other Merchant

166

181

113

27

40

85 88 89 90

103

0

20

40

60

80

100

120

140

160

180

200

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Historical Forecast

Gas carriers contracting

LPG Carriers LNG Carriers

121131

121

203

152153146

106

121124

0

50

100

150

200

250

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Historical Forecast

Cruise and ferry contracting

Passenger Ferries Cruise

734

641

275

10479 89

108

189

272

353

0

100

200

300

400

500

600

700

800

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Historical Forecast

Offshore contracting

Survey, Logistics, Rescue & Salvage

Construction Units

Offshore Support Vessels

Mobile Production

Mobile Drilling

Source: Clarksons Platou, Wärtsilä Internal Analysis

No o

f vessels

No o

f vessels

No o

f vessels

No o

f vessels

31 May 2018 Roger Holm

© Wärtsilä PUBLIC5

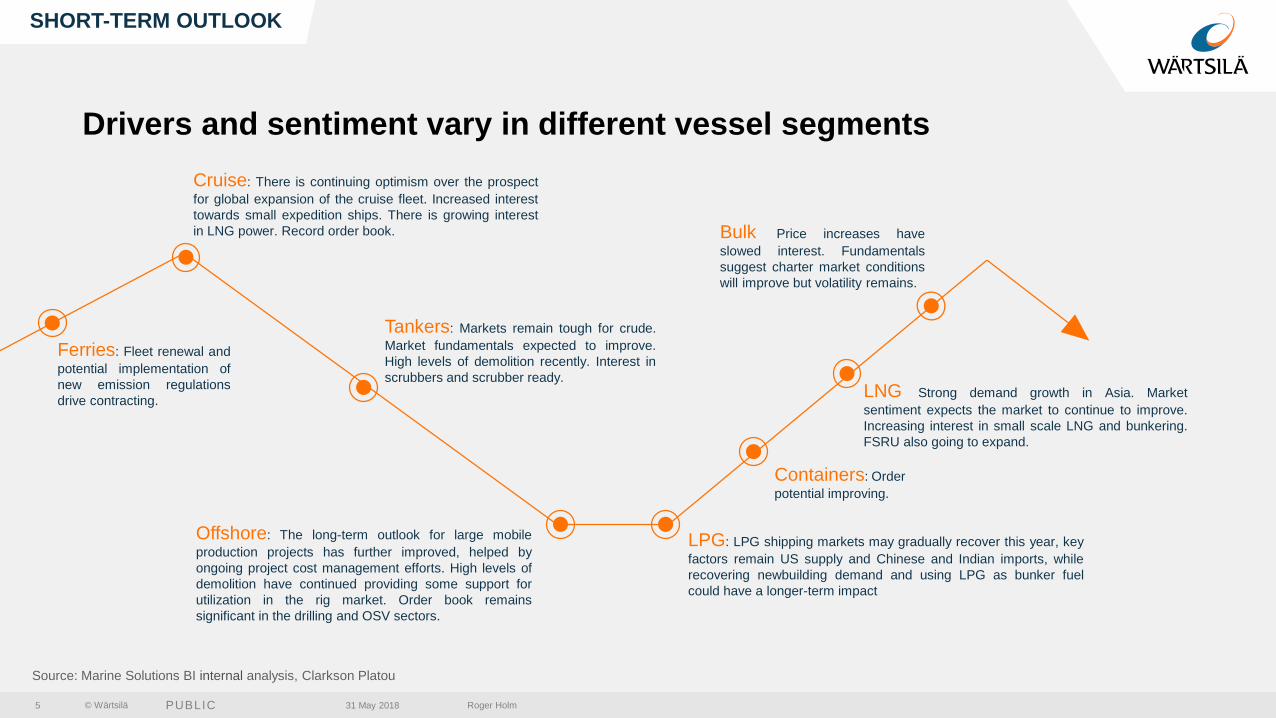

Drivers and sentiment vary in different vessel segments

SHORT-TERM OUTLOOK

Bulk: Price increases have

slowed interest. Fundamentals

suggest charter market conditions

will improve but volatility remains.

Tankers: Markets remain tough for crude.

Market fundamentals expected to improve.

High levels of demolition recently. Interest in

scrubbers and scrubber ready.

LPG: LPG shipping markets may gradually recover this year, key

factors remain US supply and Chinese and Indian imports, while

recovering newbuilding demand and using LPG as bunker fuel

could have a longer-term impact

LNG: Strong demand growth in Asia. Market

sentiment expects the market to continue to improve.

Increasing interest in small scale LNG and bunkering.

FSRU also going to expand.

Containers: Order

potential improving.

Offshore: The long-term outlook for large mobile

production projects has further improved, helped by

ongoing project cost management efforts. High levels of

demolition have continued providing some support for

utilization in the rig market. Order book remains

significant in the drilling and OSV sectors.

Ferries: Fleet renewal and

potential implementation of

new emission regulations

drive contracting.

Cruise: There is continuing optimism over the prospect

for global expansion of the cruise fleet. Increased interest

towards small expedition ships. There is growing interest

in LNG power. Record order book.

Source: Marine Solutions BI internal analysis, Clarkson Platou

31 May 2018 Roger Holm

© Wärtsilä PUBLIC

Transforming our operations to meet market requirements

6 31 May 2018 Roger Holm

© Wärtsilä PUBLIC7

ADAPTING OUR COST BASE

-90

-80

-70

-60

-50

-40

-30

-20

-10

0

2016 2017-800

-700

-600

-500

-400

-300

-200

-100

0

2016 2017

FTEs decreased with ~1,000 FTEsover the past two years

Realignment and operational excellence hassignificantly improved our competitiveness…

Capacity cost decreased with ~120 MEUR over the past two years

ME

UR

FT

Es

31 May 2018 Roger Holm

© Wärtsilä PUBLIC8

Machine stop reduction

40% By enabling Predictive

Maintenance

Defect reduction

15%

Less internal mistakes due to reworking or bad recording

of data.

Ease new products introduction

20% By enabling production data analytics about issues and

production set up

WIP reduction

30% By a better resources utilisation

& flexible planning

Reduction In energy usage

25% By smart energy

management systems

Reduction of survey costs

30% By means of remote survey &

data streaming

CONTINUOUS IMPROVEMENT

* Example from one factory

…and we have new targets for further improvements

Targets for further optimisation (2017–2020)Lead time reduction

achieved (2016–2018)

Production lead time -20%

Main assembly lead time -25%

Standard hours/MW -32%

31 May 2018 Roger Holm

© Wärtsilä PUBLIC9

MARINE SOLUTIONS MARKET POSITION AND COMPETITOR LANDSCAPE

Top playerGas carriers

Cruise & ferry

Offshore

Mid-playerSpecial vessels

ChallengerNavy

Traditional merchant

Top playerGas carriers

Mid-playerSpecial vessels

ChallengerTraditional merchant

Top playerCruise & ferry

Traditional merchant

Ports

Academy

Mid-playerSpecial vessels

ChallengerNavy

Marine power solutions Processing solutions Voyage solutions

• Automation,

navigation

& communication

• Entertainment

systems

• Simulation &

training solutions

• Fleet operations

solutions

• Ship traffic control

solutions

• Special products

• Water & waste

• Flow solutions

• Gas solutions

• Power supply

• Power conversion

• Propulsion,

• Exhaust treatment

31 May 2018 Roger Holm

© Wärtsilä PUBLIC

Leading the industry transformation towards a Smart Marine Ecosystem

10 31 May 2018 Roger Holm

© Wärtsilä PUBLIC

FROM PRODUCTS TO A SMART MARINE ECOSYSTEM

11 31 May 2018 Roger Holm

© Wärtsilä PUBLIC

Offshore

Cruise

Ferry

Gas Carrier

Containership

Fuel efficiency

0.2 BEUR

1.3 BEUR

0.3 BEUR

14.5 BEUR

Time at Terminal

0.7 BEUR

-

1.0 BEUR

2.1 BEUR

0.5 BEUR -

OPPORTUNITIES FOR WÄRTSILÄ AND CUSTOMERS

20 BEUR waste is incurred annually from poor fuel efficiency & time at terminal

Total global shipping fuel bill of roughly 100 BEUR today

12 31 May 2018 Roger Holm

© Wärtsilä PUBLIC

The Smart MarineEcosystem

13 31 May 2018 Roger Holm

© Wärtsilä PUBLIC

Towards a zero emission futureEliminating sources of waste through digitalisation

31 May 2018 Roger Holm14

© Wärtsilä PUBLIC15

Environmental legislation creating growth opportunities

TOWARDS A ZERO EMISSIONS FUTURE

2016 2017 2019 2020 2025

IMO Ballast Water Management Convention

IMO Polar Code

Global 0.5% SOx

limit reviewed

Amended IMO MEPC.227(64)

NOx Tier III in NECA (North America)

2018

Inert Gas System mandatory for

newbuild tankers above 8,000 DWT

as of 1 January 2018

Global cap 0.5% SOx

North sea and Baltic sea become NECA

Requirements for sewage discharges in the Baltic Sea

NOx Tier III proposed for North Europe

2050

Carbon emissions

halved

31 May 2018 Roger Holm

© Wärtsilä PUBLIC16

SHIPPING TODAY

F O S S I L

F U E L S

P O RT

C O N G E S T I ON

P R E S C R I P T I VEM A I N T E N A N C E

R O U T E B A S E D

O N H U M A N

E X P E RI E NCE

M A N U A L

O P E R AT I O N S

S H O RT T E R M P L A N N I N G

31 May 2018 Roger Holm

© Wärtsilä PUBLIC17

SHIPPING TODAY: WÄRTSILÄ CASE Saving per voyage with just-in-time arrival:

74.5 tons of fuel*

22,200 EUR**

CASE:

5,500 TEU Containership

Distance: 1,150 Nautical Miles

* Assuming average SFOC : 230 g/kwh

** Assuming fuel price: 300 EUR/t

964 MWh actually consumed –

640 MWh simulated consumption

324 MWh potential savings

3.5 days

31 May 2018 Roger Holm

© Wärtsilä PUBLIC18

CONNECTING SMART VESSELS TO SMART PORTS

Smart Energy

Management

Navigation &

Intelligent Automation

Smart

Ports

01000111000 01000111000 01000111000 010001110001

31 May 2018 Roger Holm

© Wärtsilä PUBLIC19 31 May 2018 Roger Holm

© Wärtsilä PUBLIC20

THE VOYAGE OF THE FUTURE REQUIRES AN INDUSTRY TRANSFORMATION

R E A L T I M E S L O T

I N F O R M AT I ON

CO NNE CTE D TO

E C O S YS T E M

O P TI MIS E D O P E RAT I ON

AV O I D C O N G E S T I ON

O P E X S AV I N G S

A R R I V E TO P O RT J U S T

I N T I M E

* Wärtsilä case study from one major port identified the range of 100-200 million euros per year of

total fuel savings and CO2 emission reduction potential in the range of 1-2 millions of tons per year

31 May 2018 Roger Holm

© Wärtsilä PUBLIC

Our customers view on future shipping

21 31 May 2018 Roger Holm

© Wärtsilä PUBLIC

“Making shipping a cleaner, more effective

way of transporting goods.”

The main ecological and economical features

compared to traditional vessels:

• CO2 eq. reduced by more than 42%

• NOx reduction of 80%

• SOx and particles almost entirely eliminated

• Use of VOC as fuel reduces bunkering of 40%

• Reduce machinery running hours of 29%

• Reduce overall fuel consumption of 10%

22

TEEKAY – NEW SHUTTLE SPIRIT

31 May 2018 Roger Holm

© Wärtsilä PUBLIC

“A mutually beneficial partnership.”

Norwegian ro-ro passenger ship

Folgefonn, owned by ferry operator

Norled.

Autodocking is one of the first steps in

fully autonomous shipping.

Wärtsilä’s autodocking technology

delivers notable benefits to operators.

These include:

• improved safety

• less wear and tear

• greater efficiency in docking

PLAY VIDEO ON DIFFERENT SCREEN

23

NORLED – AUTODOCKING

31 May 2018 Roger Holm

© Wärtsilä PUBLIC

“Creating the world’s fastest and

most reactive tug models.”

SeaWays has worked closely with

Transas over the past 10 years.

• 360° TugSim- the most advanced in

the world

• Simulation benefits: realistic

exercises, improved safety, time and

fuel savings

• Training benefits: enables to operate

the company assets with greater

efficiency and vastly reduce fuel burn

and carbon emissions

24

SEAWAYS – TRAINING FACILITIES

31 May 2018 Roger Holm

© Wärtsilä PUBLIC25

"Growth is at no time by mere chance; it is the result of forces

working together."

31 May 2018 Roger Holm

THANK YOU