maritime cluster in japan - shipbuilding and wp6 4_b - shin otsubo - web.pdf · maritime cluster in...

TRANSCRIPT

Ministry of Land, Infrastructure, Transport and Tourism

Maritime Cluster in Japan

- Shipbuilding and WP6 -

Shin Otsubo

Deputy Director-General

Maritime Bureau

Ministry of Land, Infrastructure, Transport and Tourism (MLIT)

Contents

• Maritime Cluster in Japan

• Shipbuilding industry and WP6

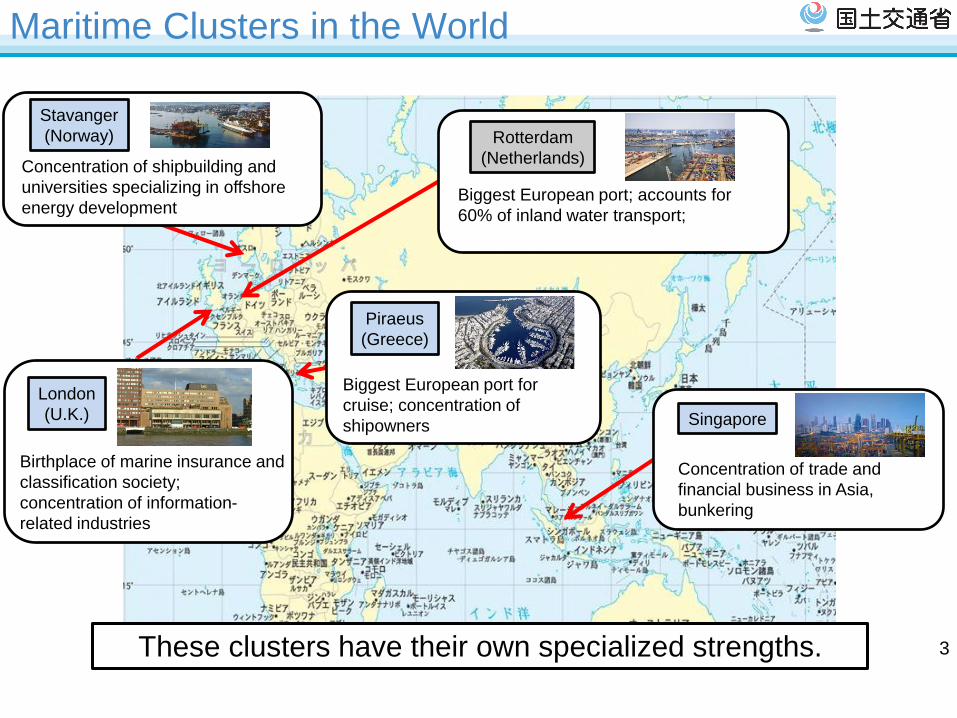

Maritime Clusters in the World

3

Stavanger

(Norway)

Concentration of shipbuilding and

universities specializing in offshore

energy development

Birthplace of marine insurance and

classification society;

concentration of information-

related industries

London

(U.K.)

Rotterdam

(Netherlands)

Biggest European port; accounts for

60% of inland water transport;

Biggest European port for

cruise; concentration of

shipowners

Piraeus

(Greece)

Singapore

Concentration of trade and

financial business in Asia,

bunkering

These clusters have their own specialized strengths.

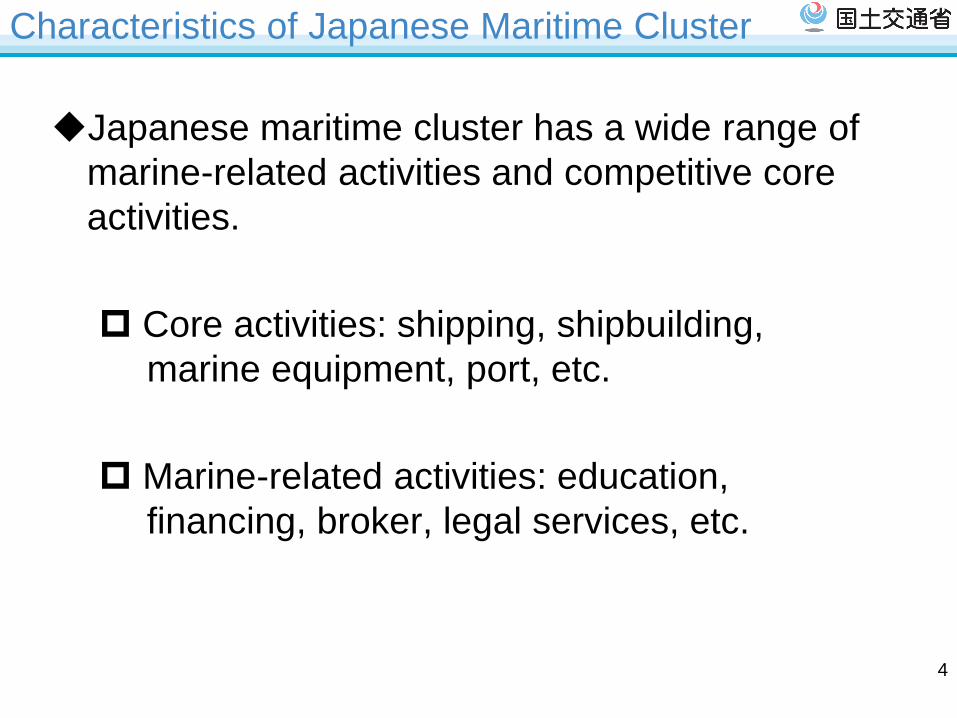

Characteristics of Japanese Maritime Cluster

Japanese maritime cluster has a wide range of

marine-related activities and competitive core

activities.

Core activities: shipping, shipbuilding,

marine equipment, port, etc.

Marine-related activities: education,

financing, broker, legal services, etc.

4

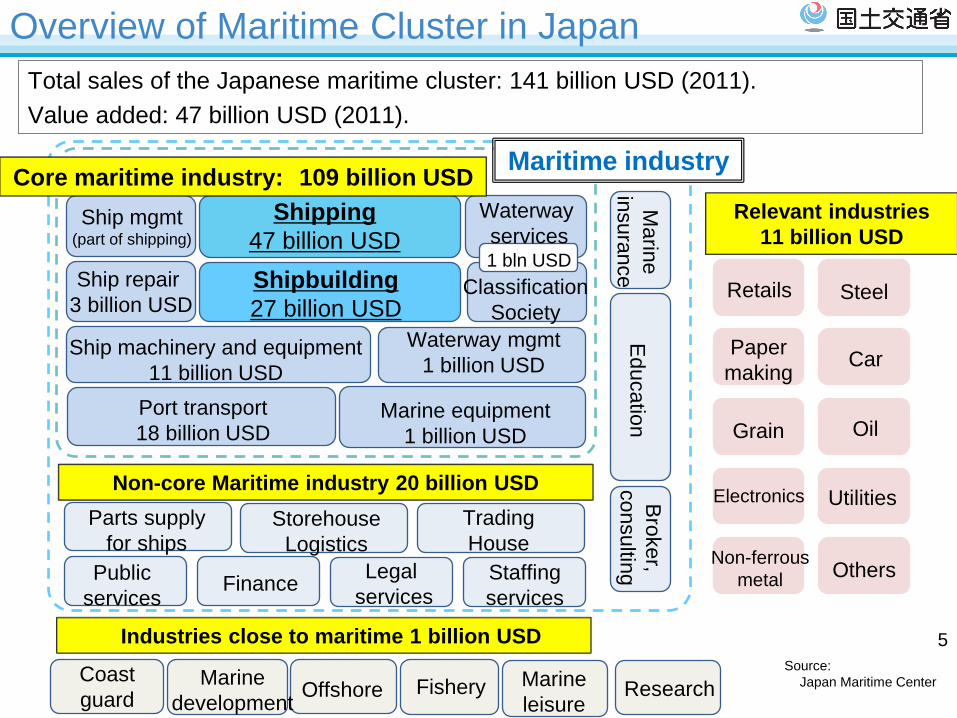

Overview of Maritime Cluster in Japan

5

Maritime industry

Non-core Maritime industry 20 billion USD

Core maritime industry: 109 billion USD

Industries close to maritime 1 billion USD

Bro

ker,

consultin

g

Marin

e

insura

nce

E

ducatio

n

Marine

development Offshore Fishery Marine

leisure Research

Relevant industries

11 billion USD

Waterway mgmt

1 billion USD

Ship mgmt (part of shipping)

Shipbuilding

27 billion USD Retails Classification

Society

Ship repair

3 billion USD

Marine equipment

1 billion USD

Port transport

18 billion USD

Parts supply

for ships Storehouse

Logistics

Public

services Finance

Legal

services

Trading

House

Staffing

services

1 bln USD

Shipping

47 billion USD

Waterway

services

Steel

Grain

Electronics

Non-ferrous

metal

Car

Oil

Utilities

Others

Paper

making

Total sales of the Japanese maritime cluster: 141 billion USD (2011).

Value added: 47 billion USD (2011).

Source:

Japan Maritime Center

Ship machinery and equipment

11 billion USD

Coast

guard

6

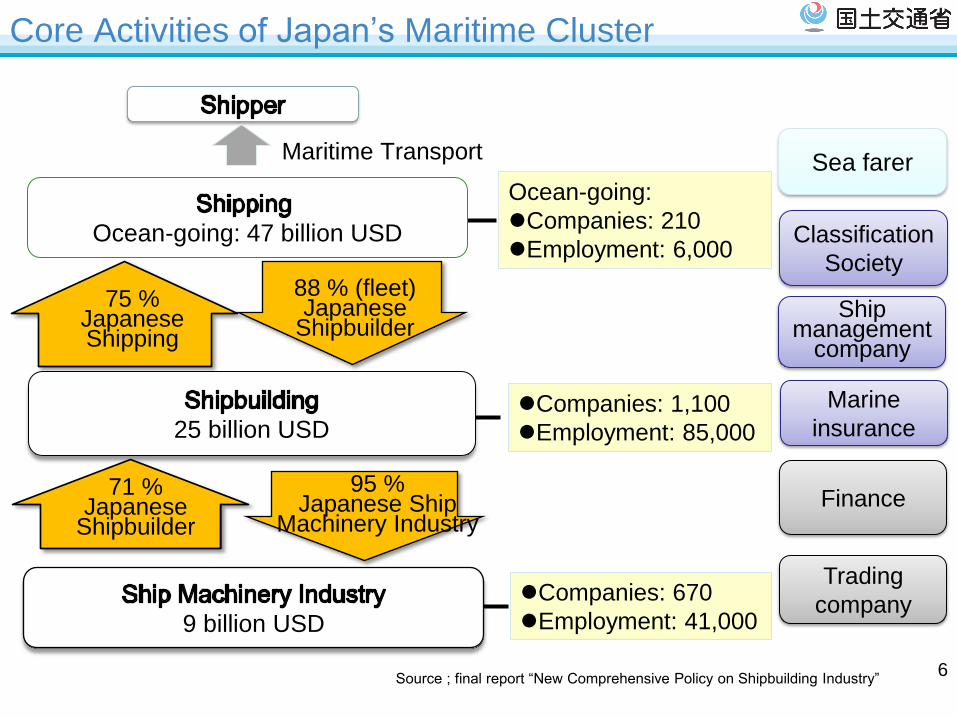

9 billion USD

75 % Japanese Shipping

88 % (fleet) Japanese

Shipbuilder

25 billion USD

Ocean-going: 47 billion USD

Maritime Transport Sea farer

Marine

insurance

Trading

company

Classification

Society

Finance 71 %

Japanese Shipbuilder

95 % Japanese Ship

Machinery Industry

Source ; final report “New Comprehensive Policy on Shipbuilding Industry”

Ship management

company

Core Activities of Japan’s Maritime Cluster

Ocean-going:

Companies: 210

Employment: 6,000

Companies: 1,100

Employment: 85,000

Companies: 670

Employment: 41,000

Concentration of shipyards in western Japan

◆The shipbuilding industry is concentrated in Western Japan.

◆In many local cities, a large portion of economies depend on shipbuilding.

Source: Clarksons Research,

Japan Ship Machinery & Equipment Association

出典: 製造業全体は、経済産業省「平成25年工業統計調査」 造船業は、国土交通省調べ

Share of shipbuilding in local economy

出典:製造業全体は、経済産業省「工業統計調査」

造船業は、海事局調べ

30%

伊万里市

23%

長崎市

36%

玉名郡

18%

佐世保市

17%

三原市

35%

丸亀市

35%

佐伯市24%

臼杵市

22%

仲多度郡

24%

今治市

81%

西海市

Tamana:36%

Saeki:35% Nagasaki:23%

Saikai:81%

Sasebo:18%

Marugame:33%

Imabari:24%

Usuki:24%

Nakatado:22% Mihara:17% Imari:30%

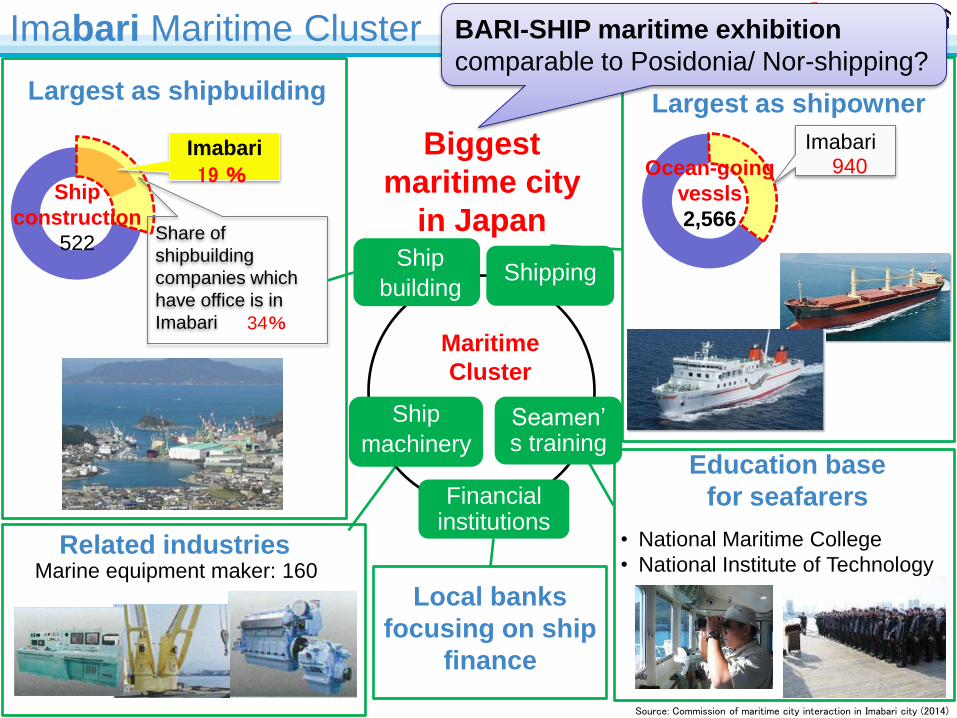

Imabari Maritime Cluster

Source: Commission of maritime city interaction in Imabari city (2014)

• National Maritime College

• National Institute of Technology

Ship

construction

522

Imabari 19 %

Share of

shipbuilding

companies which

have office is in

Imabari 34%

Imabari 940

Largest as shipbuilding

Ship

building

Seamen’s training

Financial institutions

Ship

machinery

Shipping

Biggest

maritime city

in Japan

Maritime

Cluster

Largest as shipowner

Ocean-going

vessls

2,566

Local banks

focusing on ship

finance

Education base

for seafarers

Marine equipment maker: 160 Related industries

BARI-SHIP maritime exhibition

comparable to Posidonia/ Nor-shipping?

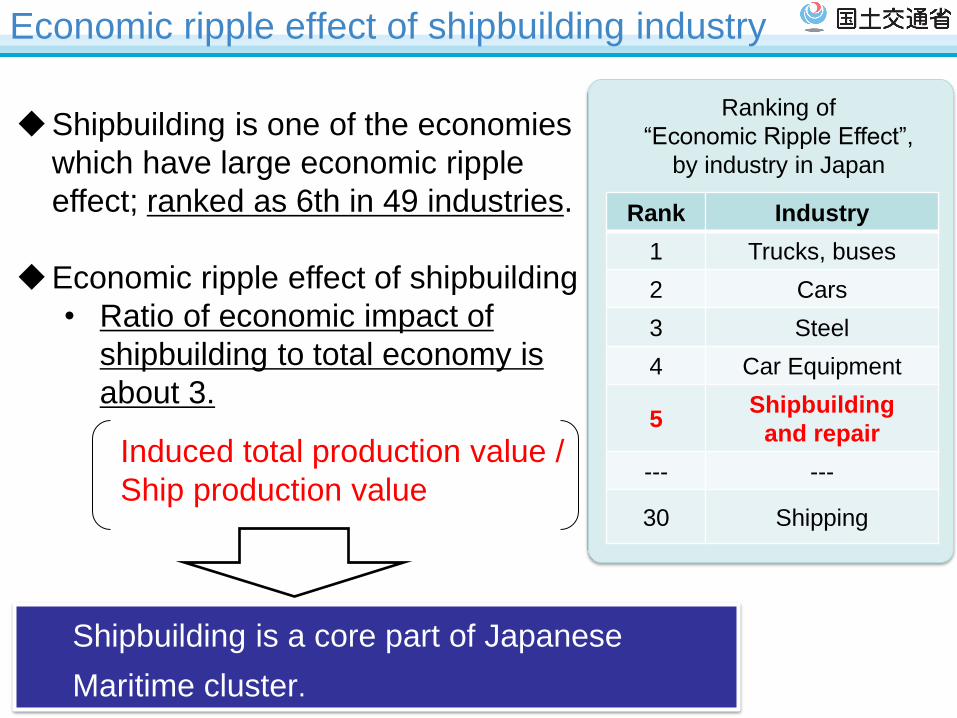

Economic ripple effect of shipbuilding industry 産業名 影響力順位

その他の自動車(トラック・バスなど) 1

乗用車 2

鉄鋼 3

自動車部品・同附属品 4

自家輸送 5

船舶・同修理 6

自動車整備 7

金属製品 8

その他の輸送機械・同修理 9

プラスチック・ゴム 10

化学製品 11

はん用機械 12

パルプ・紙・木製品 13

電気機械 14

情報・通信機器 15

航空輸送 16

電子部品 17

業務用機械 18

生産用機械 19

鉱業 20

飲食料品 21

建設 22

その他の製造 工業製品 23

水道 24

繊維製品 25

非鉄金属 26

農林水産業 27

窯業・土石製品 28

情報通信 29

水運 30

Shipbuilding is one of the economies

which have large economic ripple

effect; ranked as 6th in 49 industries.

Economic ripple effect of shipbuilding

• Ratio of economic impact of

shipbuilding to total economy is

about 3.

Shipbuilding is a core part of Japanese

Maritime cluster.

Rank Industry

1 Trucks, buses

2 Cars

3 Steel

4 Car Equipment

5 Shipbuilding

and repair

--- ---

30 Shipping

Ranking of

“Economic Ripple Effect”,

by industry in Japan

Induced total production value /

Ship production value

Contents

• Maritime Cluster in Japan

• Shipbuilding industry and WP6

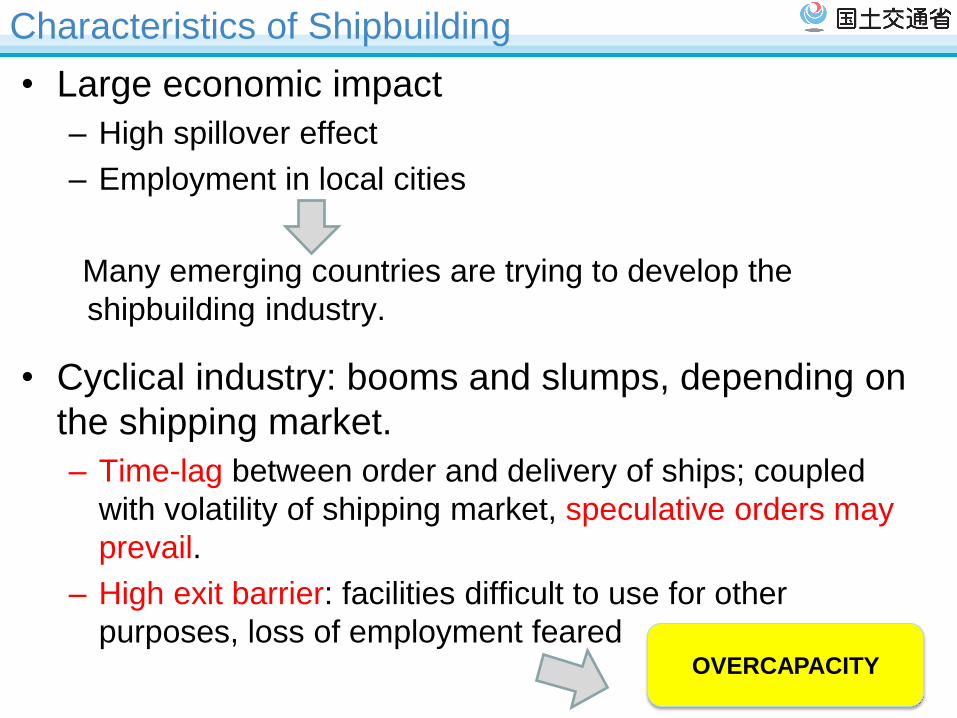

Characteristics of Shipbuilding

• Large economic impact

– High spillover effect

– Employment in local cities

Many emerging countries are trying to develop the

shipbuilding industry.

• Cyclical industry: booms and slumps, depending on

the shipping market.

– Time-lag between order and delivery of ships; coupled

with volatility of shipping market, speculative orders may

prevail.

– High exit barrier: facilities difficult to use for other

purposes, loss of employment feared OVERCAPACITY

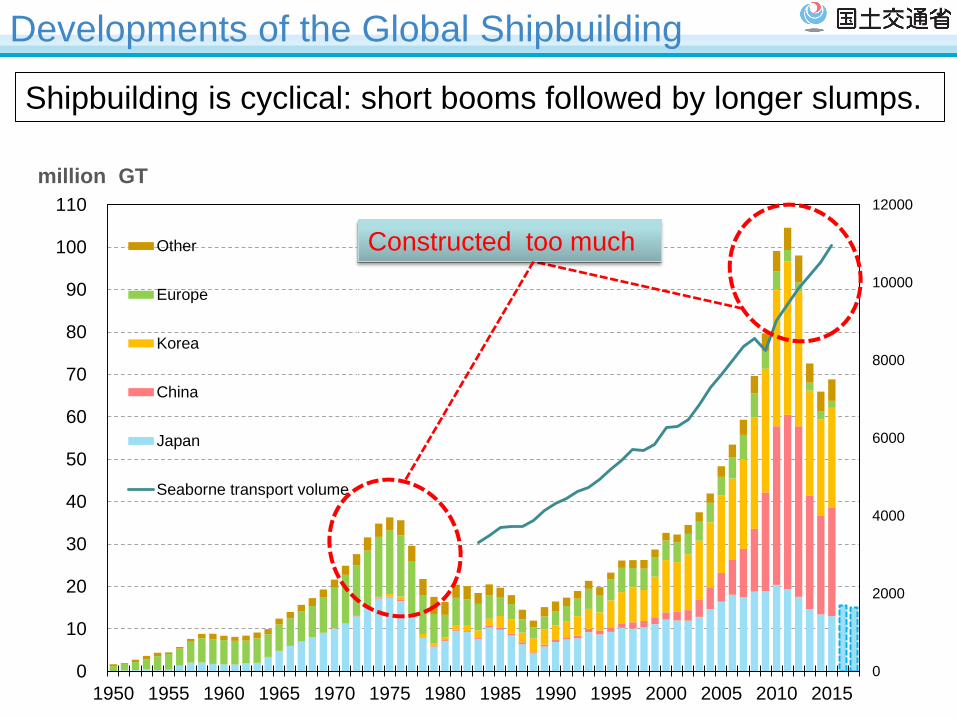

Developments of the Global Shipbuilding

Shipbuilding is cyclical: short booms followed by longer slumps.

million GT

0

2000

4000

6000

8000

10000

12000

0

10

20

30

40

50

60

70

80

90

100

110

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Other

Europe

Korea

China

Japan

Seaborne transport volume

Constructed too much

0

20

40

60

80

100

120

140

2000 2002 2004 2006 2008 2010 2012 2014 2016 …

million GT

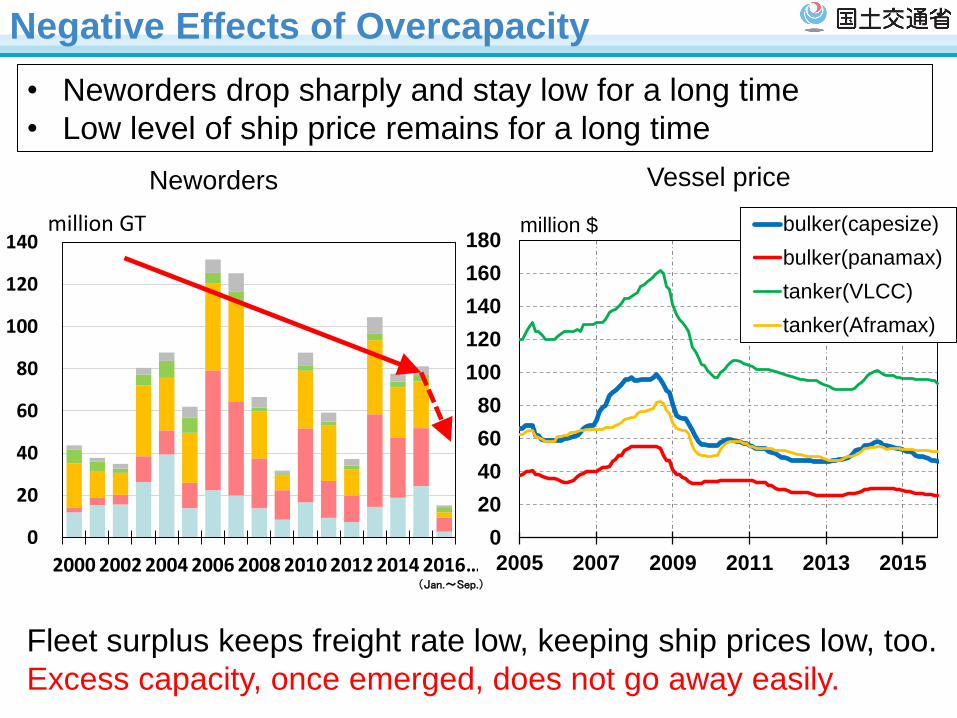

Negative Effects of Overcapacity

0

20

40

60

80

100

120

140

160

180

2005 2007 2009 2011 2013 2015

million $ bulker(capesize)

bulker(panamax)

tanker(VLCC)

tanker(Aframax)

• Neworders drop sharply and stay low for a long time

• Low level of ship price remains for a long time

Vessel price Neworders

Fleet surplus keeps freight rate low, keeping ship prices low, too.

Excess capacity, once emerged, does not go away easily.

(Jan.~Sep.)

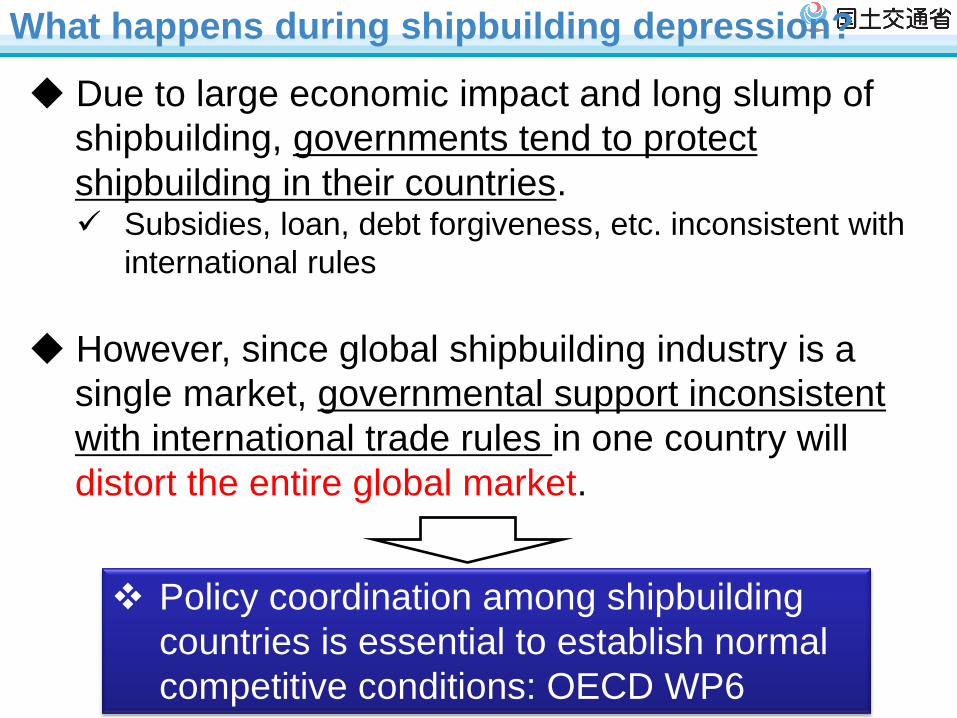

What happens during shipbuilding depression?

Policy coordination among shipbuilding

countries is essential to establish normal

competitive conditions: OECD WP6

◆ Due to large economic impact and long slump of

shipbuilding, governments tend to protect

shipbuilding in their countries. Subsidies, loan, debt forgiveness, etc. inconsistent with

international rules

◆ However, since global shipbuilding industry is a

single market, governmental support inconsistent

with international trade rules in one country will

distort the entire global market.

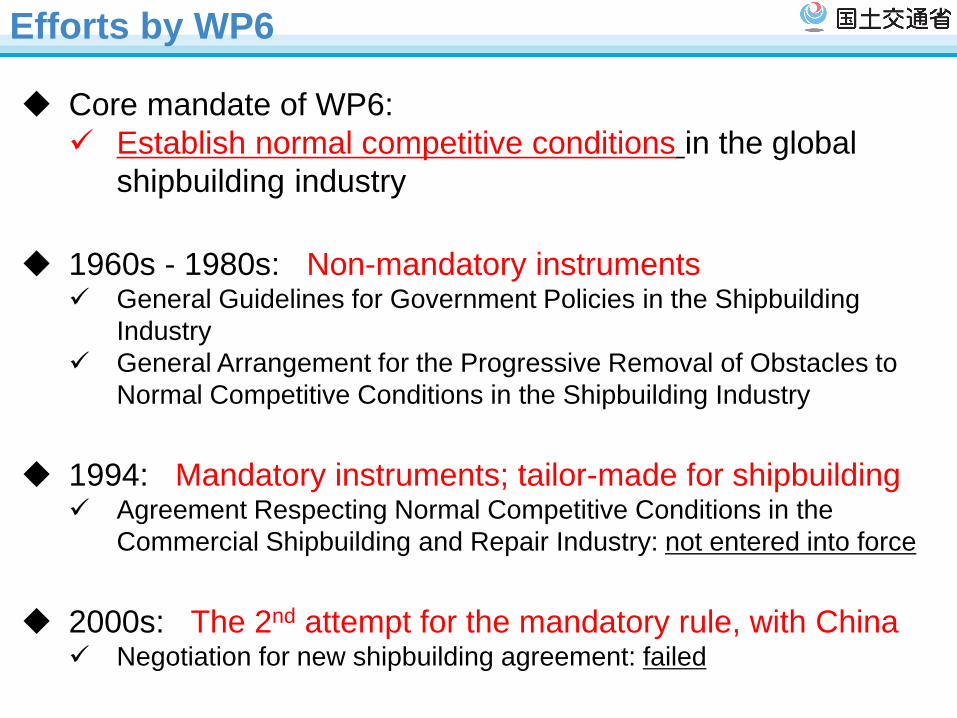

Efforts by WP6

Core mandate of WP6:

Establish normal competitive conditions in the global

shipbuilding industry

1960s - 1980s: Non-mandatory instruments

General Guidelines for Government Policies in the Shipbuilding

Industry

General Arrangement for the Progressive Removal of Obstacles to

Normal Competitive Conditions in the Shipbuilding Industry

1994: Mandatory instruments; tailor-made for shipbuilding

Agreement Respecting Normal Competitive Conditions in the

Commercial Shipbuilding and Repair Industry: not entered into force

2000s: The 2nd attempt for the mandatory rule, with China

Negotiation for new shipbuilding agreement: failed

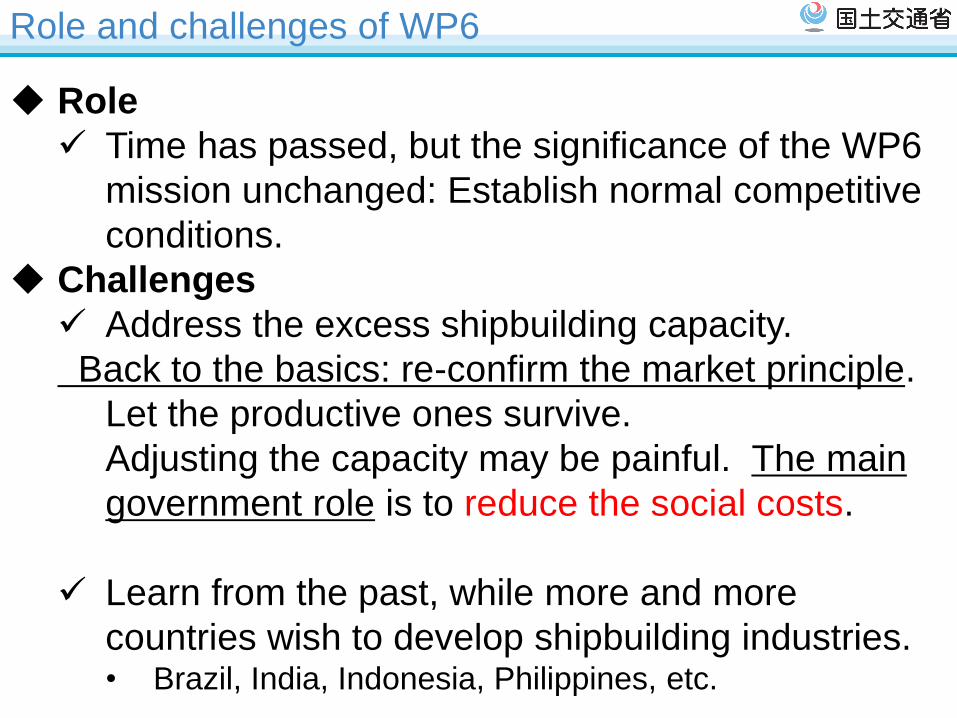

Role and challenges of WP6

Role

Time has passed, but the significance of the WP6

mission unchanged: Establish normal competitive

conditions.

Challenges

Address the excess shipbuilding capacity.

Back to the basics: re-confirm the market principle.

Let the productive ones survive.

Adjusting the capacity may be painful. The main

government role is to reduce the social costs.

Learn from the past, while more and more

countries wish to develop shipbuilding industries. • Brazil, India, Indonesia, Philippines, etc.

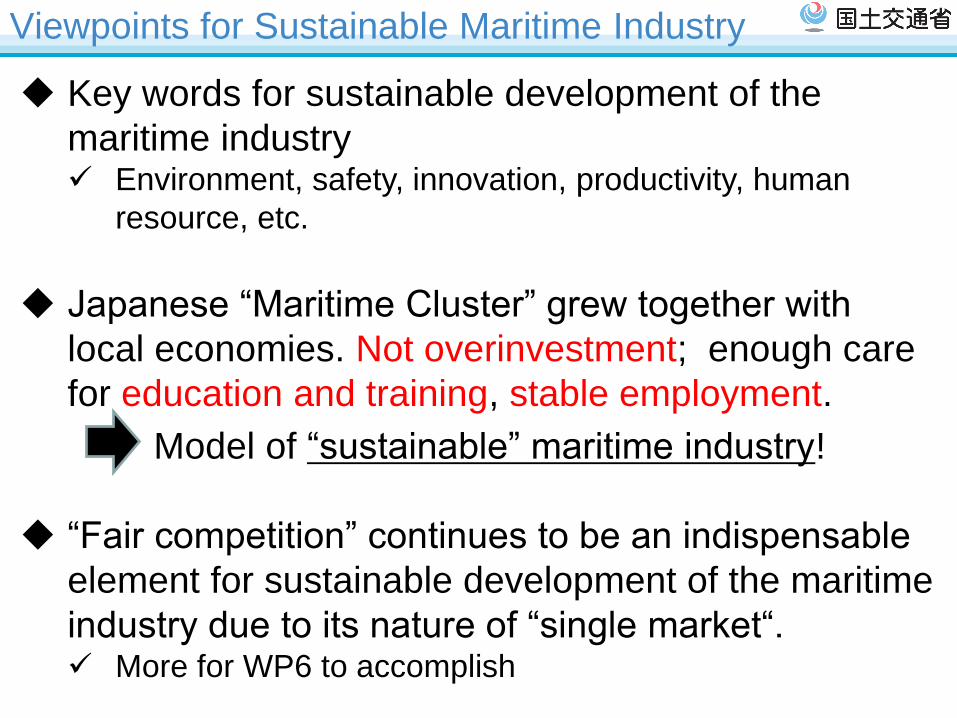

Viewpoints for Sustainable Maritime Industry

Key words for sustainable development of the

maritime industry Environment, safety, innovation, productivity, human

resource, etc.

Japanese “Maritime Cluster” grew together with

local economies. Not overinvestment; enough care

for education and training, stable employment.

Model of “sustainable” maritime industry!

“Fair competition” continues to be an indispensable

element for sustainable development of the maritime

industry due to its nature of “single market“. More for WP6 to accomplish