market for corporate control: takeovers€¦ · market for corporate control: takeovers nino...

TRANSCRIPT

Market for Corporate Control: Takeovers

Nino Papiashvili

Institute of Finance

Ulm University

1

Introduction

Takeovers - the market for corporate control - where management teams compete with one another for the right to manage assets owned by shareholders

The team that offers the highest value to the shareholders takes over the right to manage the assets until it is replaced by another management team that discovers a higher value of the assets.

2

Introduction

Takeovers are expected to occur when the target firm performs poorly and its internal corporate governance mechanisms fail to discipline managers

Takeovers are considered as an alternative corporate governance mechanism that corrects for opportunistic managerial behavior

Thus the takeover market serves as an important source of protection for investors

3

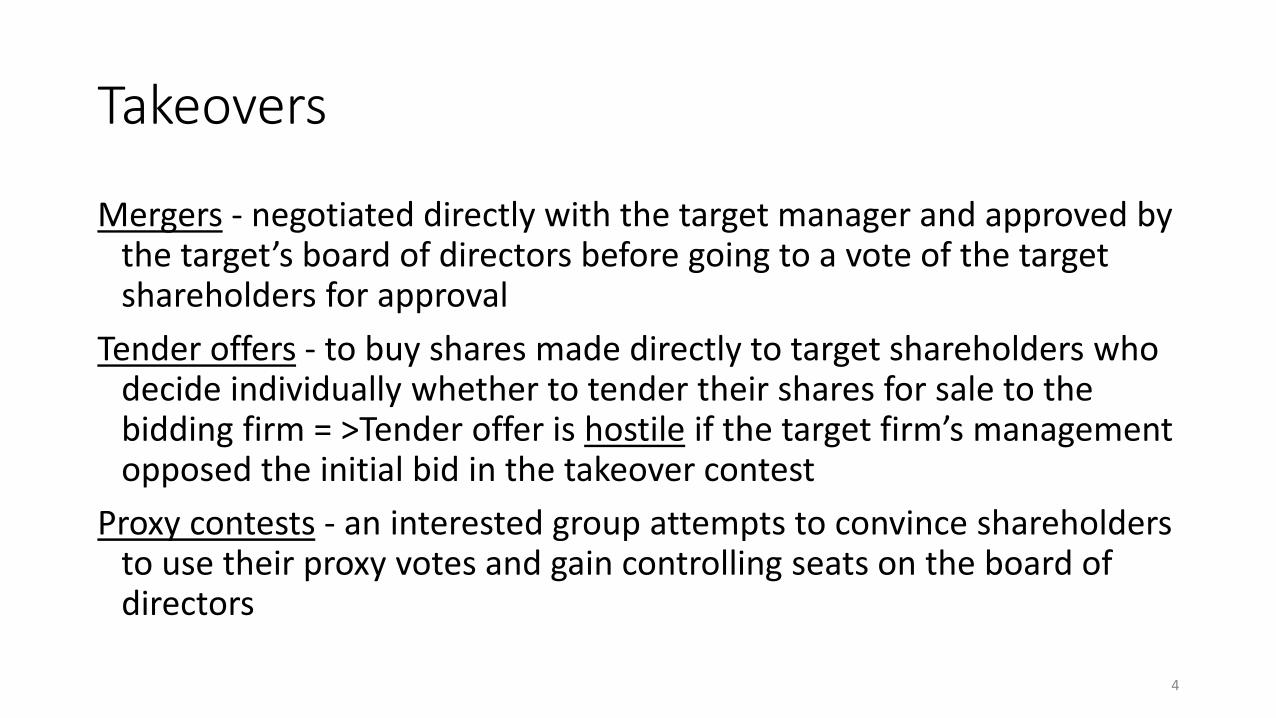

Takeovers

Mergers - negotiated directly with the target manager and approved by the target’s board of directors before going to a vote of the target shareholders for approval

Tender offers - to buy shares made directly to target shareholders who decide individually whether to tender their shares for sale to the bidding firm = >Tender offer is hostile if the target firm’s management opposed the initial bid in the takeover contest

Proxy contests - an interested group attempts to convince shareholders to use their proxy votes and gain controlling seats on the board of directors

4

Takeovers

Cash offers vs. Equity offers

When bidder management considers that its stock is overvalued it will prefer a equity offer and vice versa for a cash offer.

=> market participants will interpret a cash offer as good news and a stock offer as bad news about bidder’s stock value

Consequently, stock-based deals are associated with negative returns to the bidder’s shareholders at deal announcements, whereas cash deals are zero or slightly positive

5

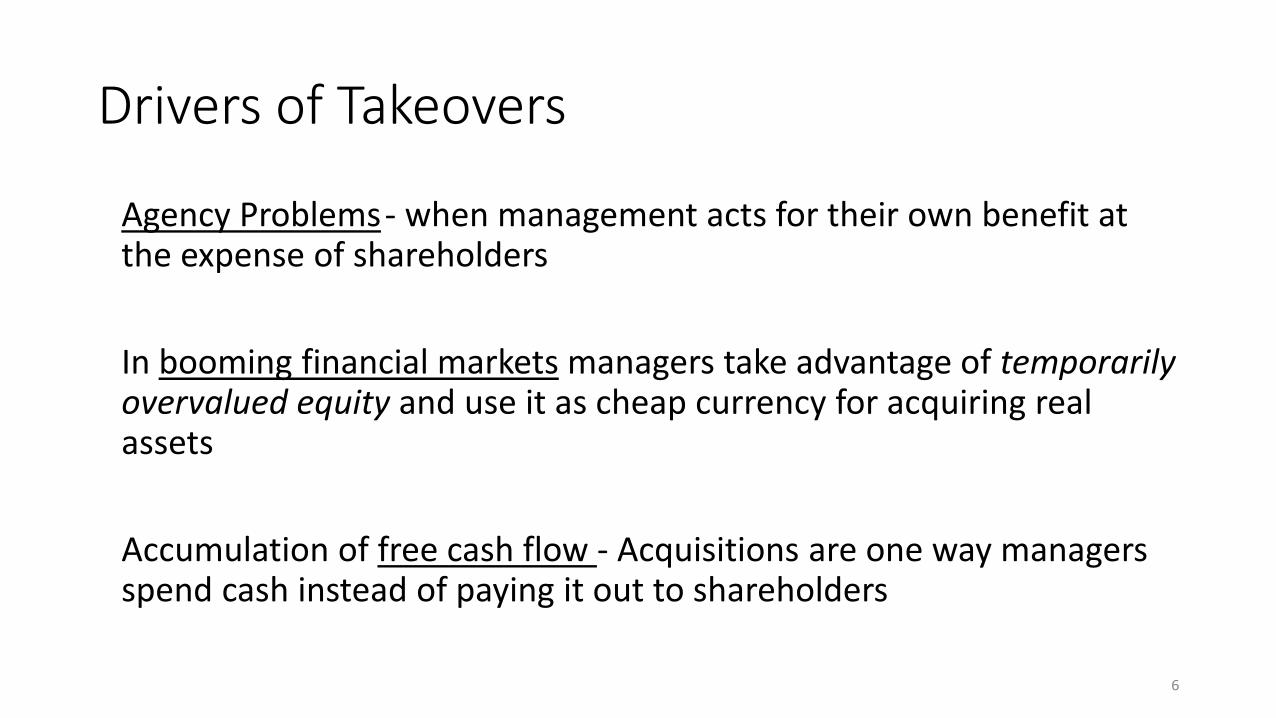

Drivers of Takeovers

Agency Problems- when management acts for their own benefit at the expense of shareholders

In booming financial markets managers take advantage of temporarily overvalued equity and use it as cheap currency for acquiring real assets

Accumulation of free cash flow - Acquisitions are one way managers spend cash instead of paying it out to shareholders

6

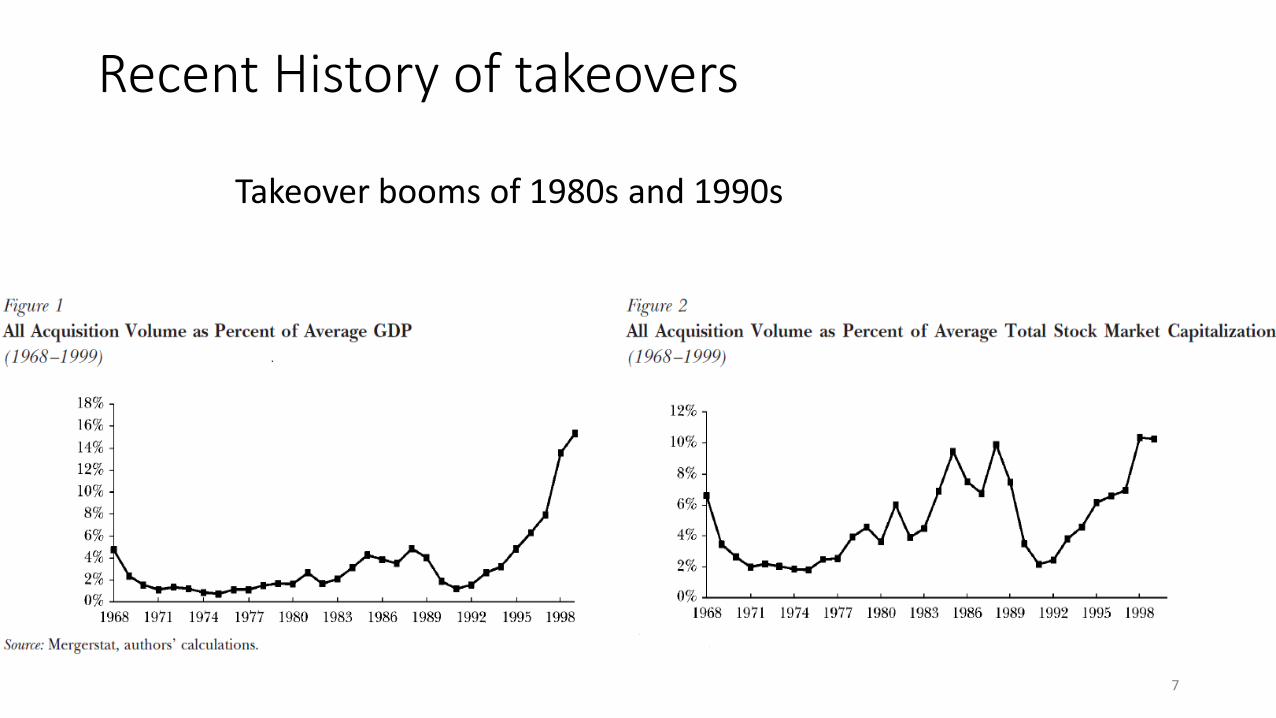

Recent History of takeovers

7

Takeover booms of 1980s and 1990s

Almost half of all major US companies received Hostile Takeover bids in the 1980s as opposed to 15% in the 1990s

8

Takeover Boom of 1980s

The fundamental causes:

Failure in the internal governance mechanisms: weaker CEO incentives with more widely dispersed shareholders, passive boards

Changes in Technology: started from oil industry where large gains mainly led to increased capacity (also spread to other industries) => takeovers as successful tool in eliminating excess cash flow

In the 1980s the rise in the number of institutional shareholders shifted balance from stakeholders to shareholders (activism increased)

9

Takeover Boom of 1980s

Characterized by heavy use of leverage

=>increased incidences of Leveraged Buyouts (LBOs)

Examination of the special characteristics and the value of LBOs:

• Change in managerial incentives – more equity stake at the firm

• High debt=strong financial discipline on the management => improved efficiency

10

Takeovers in 1990s

Hostile takeovers were not needed anymore because companies followed the experience of LBOs and voluntarily restructured:

• The rise of incentive (equity) based compensation of the managers – CEO option grants increased 7 times from 1980 to 1994

=> increase in pay-for-performance sensitivity

• Recognition of cost of capital: New performance measurement (based on return on equity over cost of equity) for CEOs as compared to excessive debt effect on LBOs

• Increased monitoring: increase in professional institutional investors and shareholder activism, more active boards with pay-for-performance sensitive compensations

11

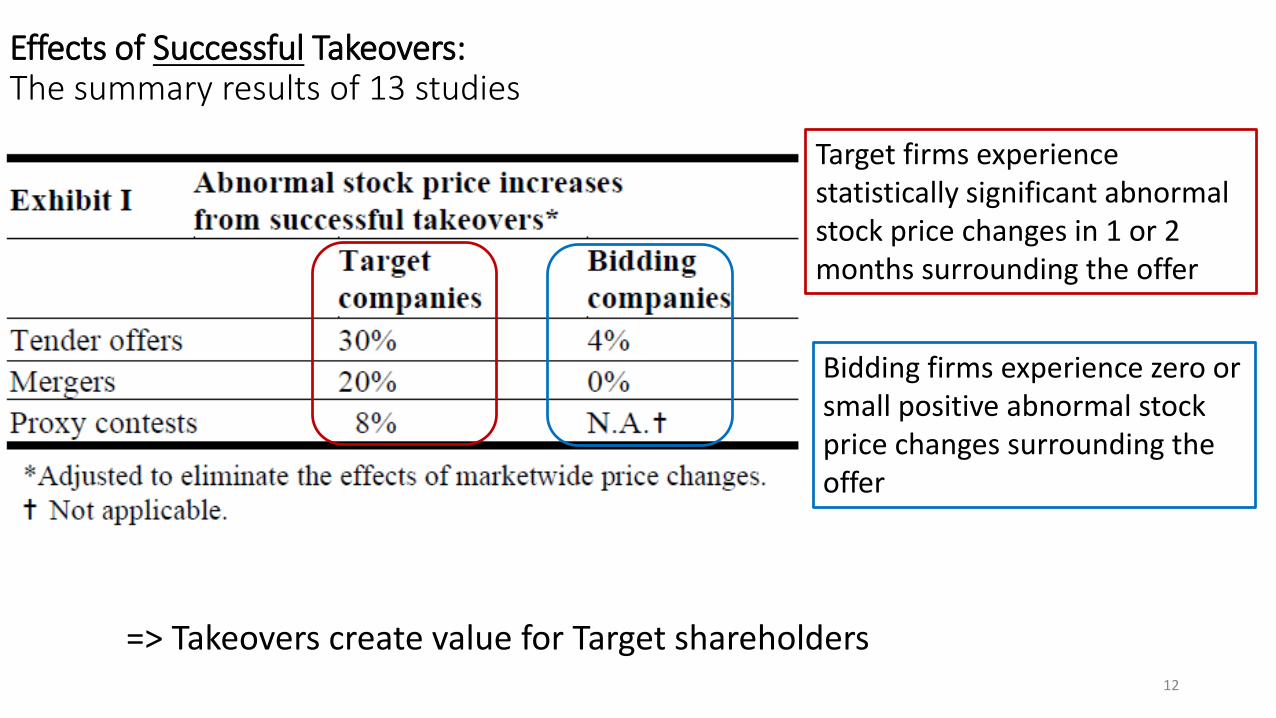

Effects of Successful Takeovers:The summary results of 13 studies

12

Target firms experience statistically significant abnormal stock price changes in 1 or 2 months surrounding the offer

Bidding firms experience zero or small positive abnormal stock price changes surrounding the offer

=> Takeovers create value for Target shareholders

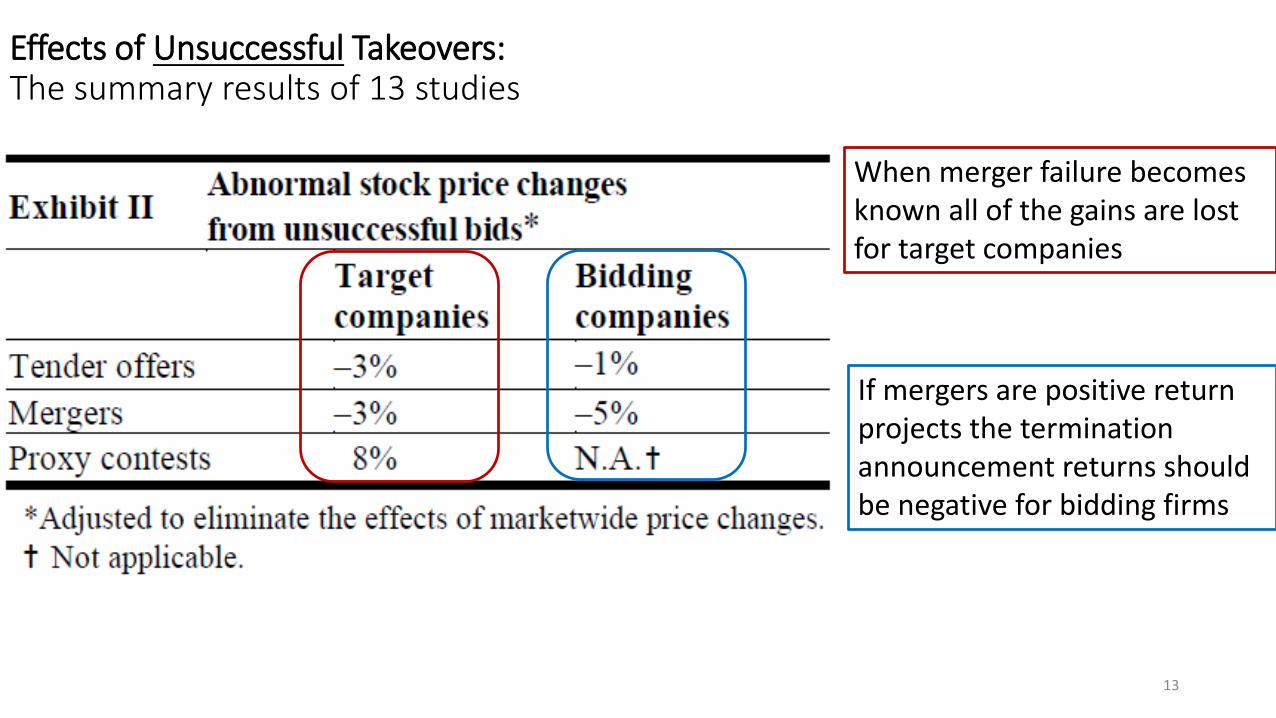

Effects of Unsuccessful Takeovers:The summary results of 13 studies

13

When merger failure becomes known all of the gains are lost for target companies

If mergers are positive return projects the termination announcement returns should be negative for bidding firms

Summary of Findings

Targets of successful tender offers and mergers earn significantly positive abnormal returns on announcement of the offers and through completion of the offers

Bidders of successful tender offers earn small positive abnormal returns, returns to successful bidding firms in mergers are zero

Both targets and bidders of unsuccessful bidders lose all previous announcement gains which is consistent with the hypothesis that mergers are positive net present value projects

=>Since targets gain and bidders do not appear to lose, the evidence suggests that takeovers create value. However, because bidding firms tend to be larger than target firms, the sum of the returns to bidding and target returns do not translate into the joint gains to the merging firms

14

Sources of Gains from TakeoversElimination of inefficient target management

Synergies - Potential reductions in production or distribution costs through:• economies of scale• vertical integration • adoption of more efficient production or organizational technology • increased utilization of the bidder’s management team • reduction of agency costs by bringing organization-specific assets under common ownership

Use of underutilized tax shields and other types of tax advantages

Increase in market power – increase of the product prices and/or output due to decreased competition (=>empirical evidence not found)

=>Each of these hypotheses predicts that the combined firm generates cash flows with a present value in excess of the sum of the market values of the bidding and target firms. 15

Cross Country Determinants of Takeovers

Study of 49 countries

Examination of M&As announced between 1990-1999

Only deals with transfer of stakes above 50%

Empirical Test: The study of how and if investor protection environment in different countries affects M&A activities

16

DATA

In all countries the frequency of attempted acquisitions is 23.5 % of domestic traded firms, whereas hostile takeovers is rare – only 1%. Hostile takeovers are present only in 28 countries not exceeding 6.4% of traded firms (USA)

The number of cross border M&As (acquirer and target are from different countries) represent 42.8% of the total number of takeovers

Bid premium (% of pre-bid stock price) ranges from 99.6% (Japan) to 227% (Indonesia)

88% of Italian acquisitions are paid in cash as opposed to 37% in the US

Investor Protection = Accounting Standards and Antidirector Rights Index from LaPorta et al. (1998)

17

Characteristics of Mergers & AcquisitionsVolume - % of traded firms that are targets of successful takeovers

The incidence of Hostile Takeovers – the % of hostile takeovers in traded firms

The Cross Border Ratio - number of cross border deals (Bidder & Target Countries are different) as a % of all deals by target country

Takeover Premiums – bid price as a % of pre-bid stock price

The Method of Payment – Cash vs. Equity

Investor Protection=Common Law, Accounting Standards, Shareholder Protection(Antidirector Index)

X- Other controls (GDP and GNP per capita)

18

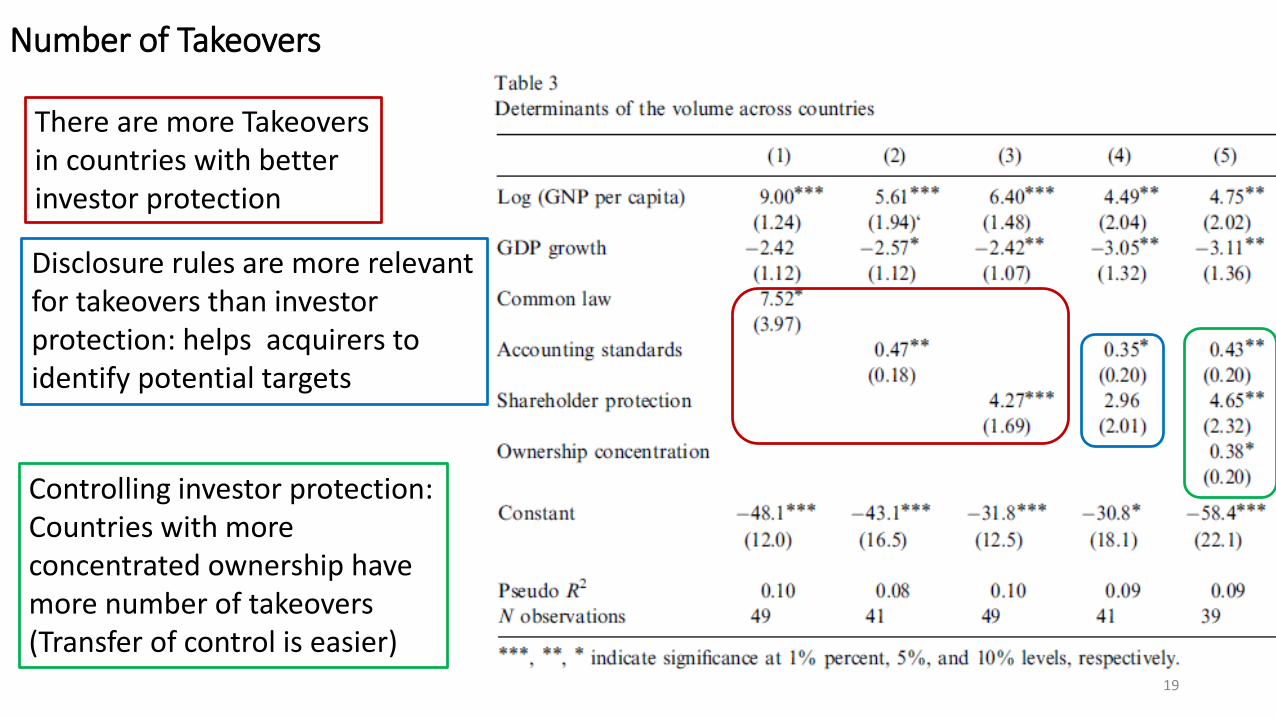

Number of Takeovers

19

There are more Takeovers in countries with better investor protection

Disclosure rules are more relevant for takeovers than investor protection: helps acquirers to identify potential targets

Controlling investor protection: Countries with more concentrated ownership have more number of takeovers (Transfer of control is easier)

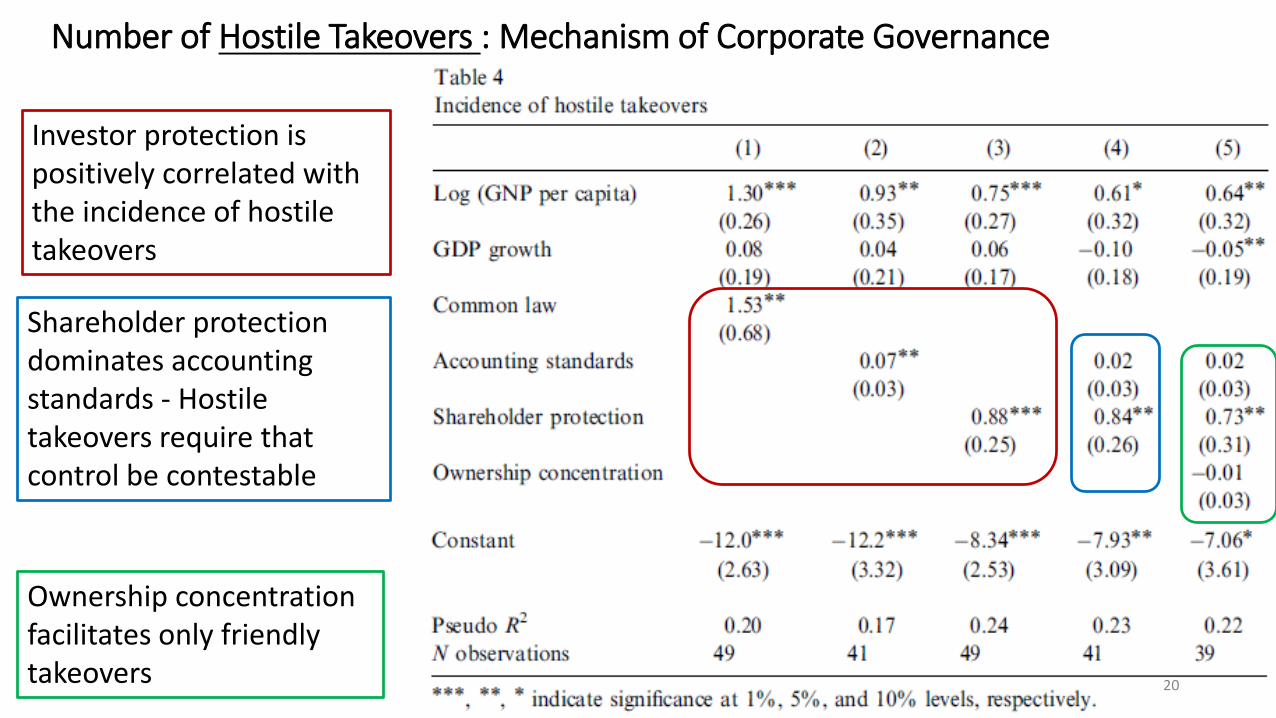

Number of Hostile Takeovers : Mechanism of Corporate Governance

20

Shareholder protection dominates accounting standards - Hostile takeovers require that control be contestable

Ownership concentration facilitates only friendly takeovers

Investor protection is positively correlated with the incidence of hostile takeovers

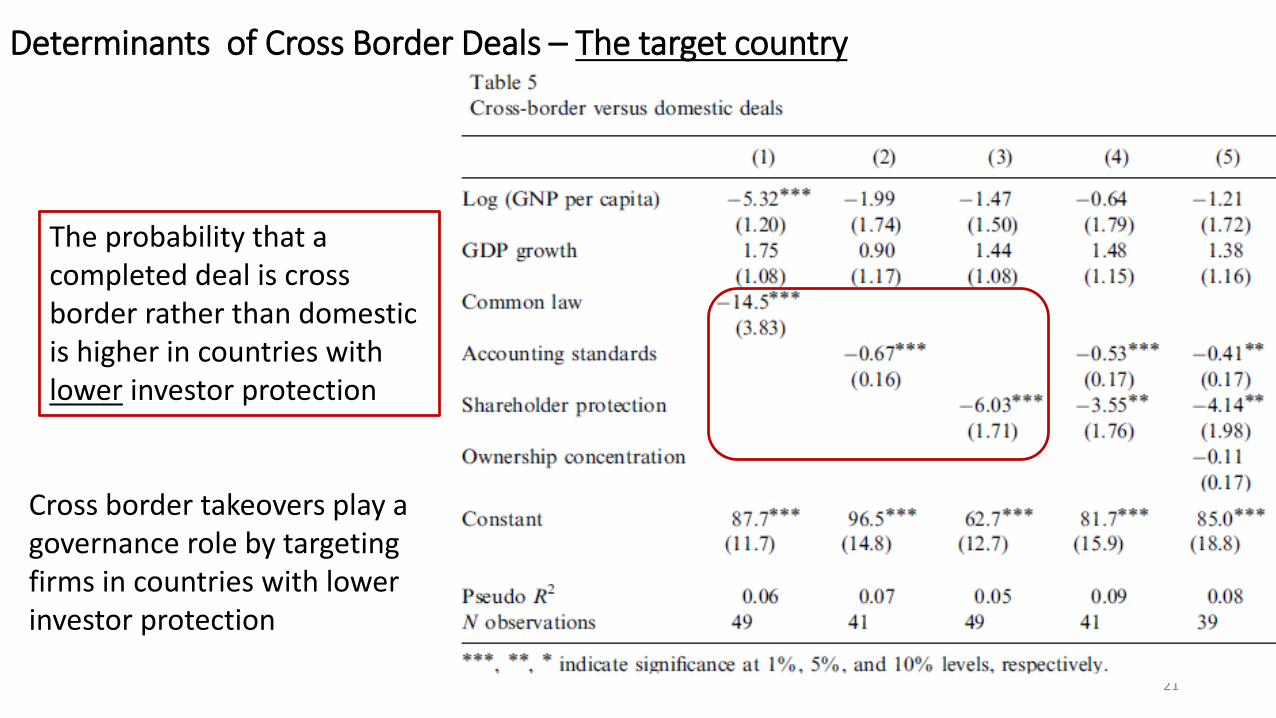

Determinants of Cross Border Deals – The target country

21

The probability that a completed deal is cross border rather than domestic is higher in countries with lower investor protection

Cross border takeovers play a governance role by targeting firms in countries with lower investor protection

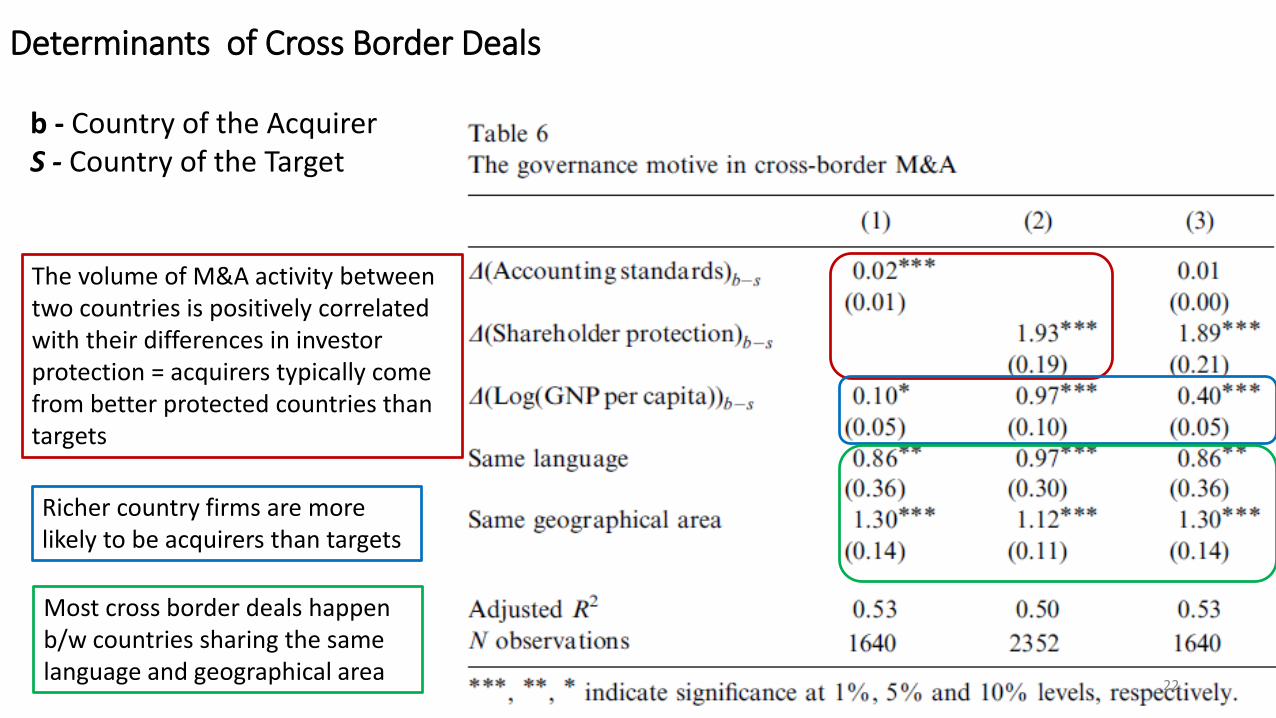

Determinants of Cross Border Deals

22

b - Country of the AcquirerS - Country of the Target

The volume of M&A activity between two countries is positively correlated with their differences in investor protection = acquirers typically come from better protected countries than targets

Richer country firms are more likely to be acquirers than targets

Most cross border deals happen b/w countries sharing the same language and geographical area

Determinants of Takeover Premiums - Shareholder protection at target country level

23

Shareholder protection is positively related to the takeover premium: i) Shareholder protection reduces cost of capital=>increases competition among bidders; ii) dispersed ownership is more common in countries with good investor protection=>free rider problem present during takeovers

Larger deals are associated with lower premiums

Bidder in tender offer needs to pay higher premium to induce shareholders to tender their shares (free rider problem)

Contested bids – more competition for targets higher the premiums

Determinants of the Means of Payments - Measuring the Probability of Cash Payments

24

When shareholder protection is low the probability of cash payments is high: equity payments entail higher risk of expropriation for minority shareholders

Larger deals are less likely to be paid entirely with cash

Cross border deals are more likely to be paid in cash due to investors dislike of foreign stock as compensation

To induce the shareholders to bit hostile and tender offers are positively correlated with all cash payments

Summary of Results

M&A activity is correlated with investor-friendly legal environments. Better investor protection is associated with:• More mergers and acquisitions• More attempted hostile takeovers• Fewer cross border deals• Greater use of stock as a method of payment• Higher takeover premiums

In Cross border deals acquirers have higher investor protection than targetsThe possibility of convergence in corporate governance: countries with better

investor protection will end up buying companies from countries with weak investor protection. Targets almost always adopt the governance standards of the acquirers

25

Conclusion

• Takeovers create value for target companies – numerous studies find abnormal stock returns surrounding takeover announcements

=>the stock price change is the best measure of the takeover’s future impact on the organization. Positive stock price changes indicate arise in the total profitability of the merged companies

• The best way to discourage the competing manager (takeover attempt) is to run a company in a way that maximizes its value

26

Required Readings:

*Jensen, M. C. (1984). Takeovers: Folklore and science. Harvard Business Review, November-December.

*Rossi, S., & Volpin, P. F. (2004). Cross-country determinants of mergers and acquisitions. Journal of Financial Economics, 74(2), 277-304.

27

Optional Readings/Presentations:

• Harford, J. (2003). Takeover bids and target directors’ incentives: The impact of a bid on directors’ wealth and board seats. Journal of Financial Economics, 69(1), 51-83.

• Chatterjee, S., Harrison, J. S., & Bergh, D. D. (2003). Failed takeover attempts, corporate governance and refocusing. Strategic Management Journal, 24(1), 87-96.

• Goergen, M., & Renneboog, L. (2004). Shareholder Wealth Effects of European Domestic and Cross‐border Takeover Bids. European Financial Management, 10(1), 9-45.

• Masulis, R. W., Wang, C., & Xie, F. (2007). Corporate governance and acquirer returns. The Journal of Finance, 62(4), 1851-1889.

28