market mechanisms: incentives and integration in the post-2020 world

TRANSCRIPT

Bern 16th June 2015 – 2nd dialogue between the Swiss private sector and the Swiss Federal Administra@on on carbon markets

Juerg Fuessler (INFRAS) and Axel Michaelowa (Perspec@ves)

Market Mechanisms: Incen@ves and Integra@on in the Post-‐2020 World

Source: World Bank, Networked Carbon Market (NCM) Ini@a@ve

INFRAS

Agenda

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa

1. Incen@vizing mi@ga@on ac@on pre 2020 2. Accoun@ng – Important essen@als for deal in Paris 3. Transi@ons of market mechanisms – poten@al storylines 4. How to use elements from market mechanisms to improve climate finance?

5. Preliminary findings for Switzerland

2

Market mechanisms

1. Incen@vizing mi@ga@on ac@on pre 2020

INFRAS

Incen.vizing mi.ga.on ac.on pre 2020: Current categories of market mechanisms

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa 4

Kyoto mechanisms, mostly project-‐based (CDM and JI) § Successful but paralyzed by price crash § Efficiency of CDM hampered by addi@onality issues Other (domes@c and interna@onal) offsebng programs (VCS, CAR, JCM, CH-‐Kompensa@onsprojekte, …) Boeom-‐up upscaling of mechanisms (REDD+, NAMA credi@ng) § Niche ac@vi@es at the moment, but basis for poten@al upscaling

INFRAS

Incen.vizing mi.ga.on ac.on pre 2020: New mechanisms under the UNFCCC

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa 5

§ NMM and FVA: § Principles agreed but “hostage” to the nego@a@on process since 2012

§ Willingness to build up new market mechanism seems weak § REDD+

Key ques@ons: • How do climate finance and market mechanisms interact? • What role should the UNFCCC play? • How can environmental integrity and transparency be

maintained in a world of fragmented mechanisms?

INFRAS

Scenarios for assessment of market mechanisms

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa 6

High demand – strong governance § INDCs of industrialized countries and emerging economies are ambi@ous and envisage acquisi@on of interna@onal credits

§ Buyers want to ensure high level of integrity Low demand – weak governance § Limited share of INDCs envisages buying of credits § Scramble to get transac@ons may lead to low and/or fragmented standards

“Clubs” with common accoun@ng rules and/or “filters” for types of emission credits § Som linking to allow for a certain fungibility of units

Market mechanisms

2. Accoun@ng – Essen@als for deal in Paris

INFRAS

Accoun.ng – Bookkeeping of mi.ga.on outcomes

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa 8

Robust rules for accoun@ng of credi@ng units are key to ensure the integrity of any market based mechanism. § Environmental integrity, consistency and comparability of the units § Avoid double coun@ng/claiming: (i) accoun@ng of units, (ii) design of mechanisms that issue units, and (iii) consistent tracking and repor@ng on units.

§ Time dimension of units: validity of vintages (carry over), permanence issue

Minimum: robust accoun@ng rules for interna@onal transfer of units, even if there is no agreement on an interna@onally recognized compliance unit in the sense of an assigned amount -‐> need for «clubs»

INFRAS

0

2

4

6

8

10

12

Natl. BAU Domestic mitigation Crediting INDC (Net)

INDC not met

0

2

4

6

8

10

12

Natl. BAU Domestic mitigation Crediting INDC (Net)

INDC met

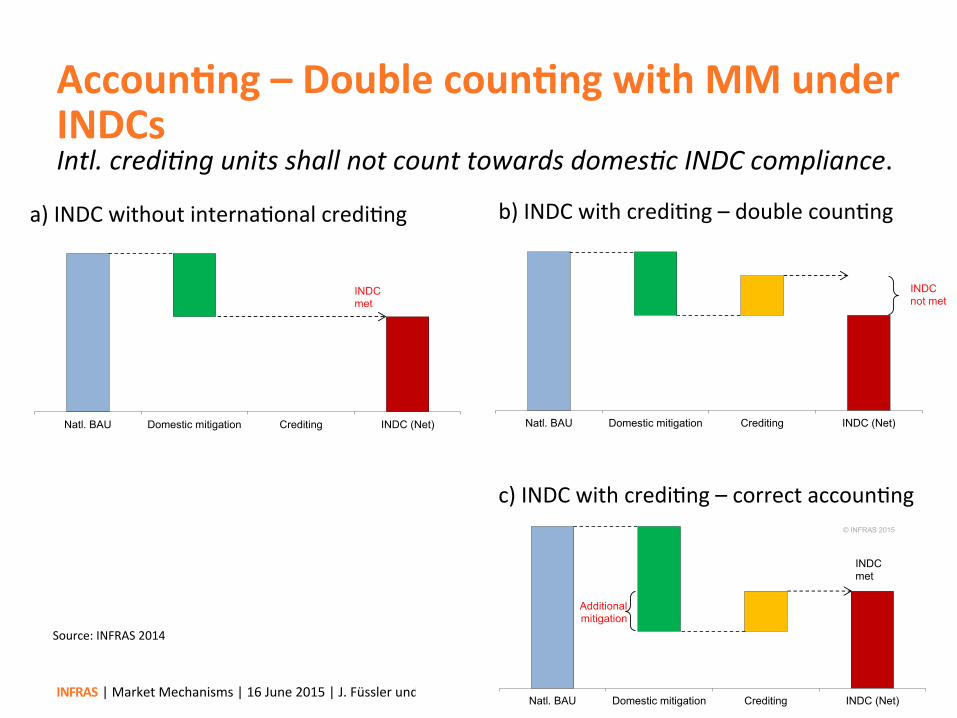

Accoun.ng – Double coun.ng with MM under INDCs

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa

9

Intl. credi,ng units shall not count towards domes,c INDC compliance.

0

2

4

6

8

10

12

Natl. BAU Domestic mitigation Crediting INDC (Net)

Additional mitigation

INDC met

© INFRAS 2015

a) INDC without interna@onal credi@ng b) INDC with credi@ng – double coun@ng

c) INDC with credi@ng – correct accoun@ng

Source: INFRAS 2014

INFRAS

Accoun.ng – Facilita.ng fungibility of units

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa 10

Comparability of accoun@ng approaches supports markets § Fungibility: describes the ability to exchange carbon credits from different schemes and make them eligible for compliance in another scheme

§ (“Som”-‐) linking of carbon markets through § Comparability of accoun@ng, consistency in ambi@on level § Filters or ra@ng of units and discoun@ng § Interna@onal Carbon Asset Reserve (ICAR) – Shared risk

mi@ga@on systems § “Clubs” – coali@ons of the willing

INFRAS

Accoun.ng – carry over of units

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa 11

Unlimited carry over of emissions reduc.ons units § generates trust in the market and reduces price fluctua@ons § limits the possibility to eliminate supply overhangs generated by lenient rules in the past

§ is not aerac@ve in the current situa@on Limi.ng carry over § Allows a “fresh start” (akin to a currency reform) § Could be seen as expropria@on by those stakeholders having invested heavily in the past into credit genera@on

Compromise solu.ons § Freezing certain units un@l the supply/demand balance has shimed (price triggers)

§ Linking carry over to the environmental integrity of the credits § Discoun@ng credits § Possibility of “re-‐registra@on” of exis@ng projects under new rules

Market mechanisms

3. Transi@ons of market mechanisms – poten@al storylines

INFRAS

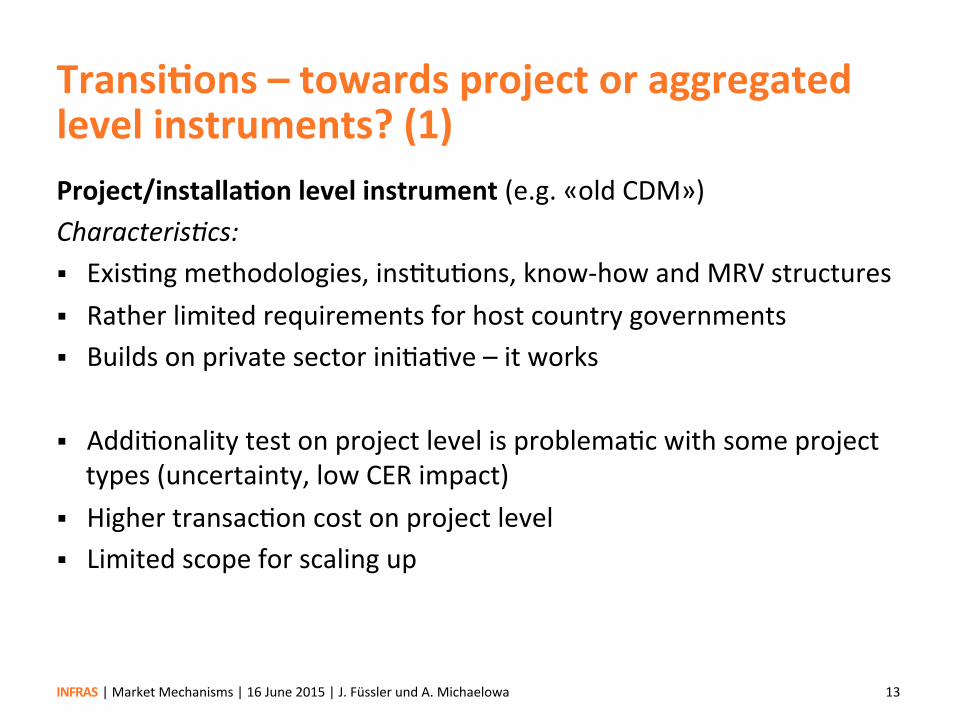

Transi.ons – towards project or aggregated level instruments? (1)

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa 13

Project/installa.on level instrument (e.g. «old CDM») Characteris,cs: § Exis@ng methodologies, ins@tu@ons, know-‐how and MRV structures § Rather limited requirements for host country governments § Builds on private sector ini@a@ve – it works

§ Addi@onality test on project level is problema@c with some project types (uncertainty, low CER impact)

§ Higher transac@on cost on project level § Limited scope for scaling up

INFRAS

Transi.ons – towards project or aggregated level instruments? (2)

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa 14

Aggregated/sector level instruments including - Policy instrument based credi@ng, - Sector target credi@ng and trading schemes, - Upscaling of CDM, POA and standardized baselines Characteris,cs: § Lower Requires significant capaci@es for data, methodologies, MRV, GHG inventory, legal frameworkt, etc. on aggregated level

§ Stronger role of governments – challenging in many countries § Key requirement: passing incen@ves to (private sector) actors § Addi@onality issues moves to level of credi@ng baseline sebng – remains challenging (level playing field for host countries with different (own) ambi@on levels)

INFRAS

Storylines for transi.on of market mechanisms

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa 15

How could market mechanisms develop over the next years? § Storyline 1: New market based mechanisms

Governing body defines common accoun@ng standards, modali@es and procedures, overseeing ins@tu@ons and valida@on/verifica@on bodies (similar to Kyoto mechanisms).

§ Storyline 2: Scaling up from CDM or recognizing other exis.ng standards The CDM provides a complete, func@oning and opera@onal interna@onally recognized market mechanism. Plus there are more standards to build on. § Pragma@c development of CDM also into aggregated level mechanisms § Solve accoun@ng issue with pledges/INDCs – level playing field issue

§ Storyline 3: Anything goes – seek transparency Minimum solu@on in absence of agreed standards under the UNFCCC § Par@es agree agree only on transparency and disclosure requirements

e.g. through publishing of all relevant documents related to interna@onally traded units

INFRAS

Storylines – Clubs

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa 16

In a weak demand – weak regula,on scenario there is a need for «clubs» of likeminded na@ons/jurisdic@ons to promote interna@onal mi@ga@on § Coali@ons of the willing, building on exis@ng (domes@c) credi@ng/ trading systems

§ Clubs allow to som-‐link mul@tude of fragmented markets § Liquidity of markets § Par@cipants’ markets may be similar, but not necessarily § Process of nego@a@ng agreements in club is key § Risk mi@ga@on instruments

INFRAS

Storylines – Clubs and ICAR

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa 17

Example: Landscape of globally networked carbon markets

Carbon Market

A

Carbon Market

B

Linking

Price floor/ceiling

Price fl./ceiling

Carbon Market

C

Carbon Market

D

Carbon Market

E

Carbon Market

F

Price floor/ceiling

Price floor/ceiling

Insurance

Insurance

International Carbon Reserve

Clearing house -‐ fungibility

Price fl./ceiling

©INFRAS 2014

Source: INFRAS 2015 Design op@ons for an interna@onal Carbon Asset Reserve. Networked Carbon Markets. A Knowledge Series. The World Bank Group.

INFRAS

Storylines – CDM as important stepping stone

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa 18

In a situa@on of uncertainty, CDM seems to be the only readily working tool in the toolbox (storyline 2) § Star@ng point:

§ CDM market down, acceptance, addi@onality, issue of carry-‐over § Exis@ng infrastructure, ins@tu@ons, skills

§ Op@ons for CDM going forward (M&P review, eligibility in countries): § „open gate“ with exis@ng or simplified addi@onality tes@ng

CDM should work for all project types/levels § „open gate plus“ with very stringent addi@onality tes@ng § „filter approach” to CDM (criteria: addi@onality)

CDM is not for all project types – only where it is game changer. For some project types, other instruments than offsebng may work beeer (supported domes@c ac@on, linking ETS, …)

Market mechanisms

4. How to use elements from market mechanisms to improve climate finance? (for part 2 of workshop)

INFRAS

Market mechanism elements for climate finance I

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa 20

Element from MM Role in climate finance

Modifica@ons required

CDM MRV methodologies for project-‐level and programma@c level ac@on

Reliable and comparable quan@fica@on of finance results

-‐ Further standardiza@on -‐ Simplifica@on possible -‐ Measure progress, not

only outcomes (tCO2) -‐ REBRANDING

Independent third party verifica@on

Transparent verifica@on of mi@ga@on progress, outcomes

-‐ Capacity building -‐ Simplifica@on

Regulatory, ins@tu@onal and governance sebng

Public documenta@on of criteria, indicators, and evalua@on results; Transparency, checks and balances in rules

-‐ Adapt for climate finance ins@tu@onal process (GCF,…)

-‐ approach civil society for consulta@ons

INFRAS

Market mechanism elements for climate finance II

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa 21

Element from MM Role in climate finance

Modifica@ons required

Country-‐specific sustainable development criteria and indicators

Country ownership of evalua@on of local co-‐benefits

Ensuring countries interest in aerac@ng foreign funding does not lead to minimum standards

Key role of the private sector

Need to create incen@ves for private sector similar to the CDM

Make sure CF can incen@vize governments, but also NGOs and private sector

Market mechanisms

5. Preliminary findings

INFRAS

Findings market mechanisms

| Market Mechanisms | 16 June 2015 | J. Füssler und A. Michaelowa 23

§ Uncertainty regarding demand and governance § Accoun@ng: transparency, environmental integrity and robust accoun@ng as necessary condi@on for market mechanisms

§ In absence of stringent interna@onal rules – seek likeminded par@es to form “club”

§ Storylines for transi@on: (i) New market based mechanisms, (ii) scaling up from CDM, (iii) anything goes

§ Stepping stone CDM: “open gate”, “open gate plus” stringent addi@onality, filter approach – best solu@on in a low demand scenario?

§ Make aggregated level mechanisms work for private sector § Ambi@ous mi@ga@on contribu@ons and domes@c ac@on will drive carbon markets

Thank you.

Authors team: Jürg Füssler, Mar.n Herren (INFRAS) Axel Michaelowa, Tyeler Matsuo, Maahias Honegger (Perspec.ves) Study commissioned by FOEN.