market minute. tuesday

TRANSCRIPT

Market Update1

Australia stocks had a shaky start following a mixed session on Wall Street last night but it did

not take long before our market moved higher for the fourth consecutive day. The S&P/ASX

200 added 0.3% to 7,401 points. Technology stocks were in line with the Nasdaq’s

performance. Nearmap rose 3.4%. Miners retreated as commodity prices were generally

weaker overnight. The mining heavyweights BHP, Rio Tinto and Fortescue were down

between 1.7% to 3.0%.

The Aussie dollar was firmer at US$0.7450.

The SPI was up 0.1% at 7,366 points on the Sydney Futures Exchange.

ASX TOP 202

ASX 200 Index Attribution3

ASX 200 Best & Worst Performers4

ASX 200 Index

Source: IRESS

MARKET MINUTE. TUESDAY

19 OCTOBER 2021

BELL POTTER SECURITIES LIMITED [email protected]

WWW.BELLPOTTER.COM.AU ABN 25 006 390 772

AFS LICENCE NO. 243480

1. Bloomberg 2. Bloomberg 3. Bloomberg 4. Bloomberg

ASX Sectors

Source: Bloomberg

7370

7380

7390

7400

7410

10:00 11:00 12:00 13:00

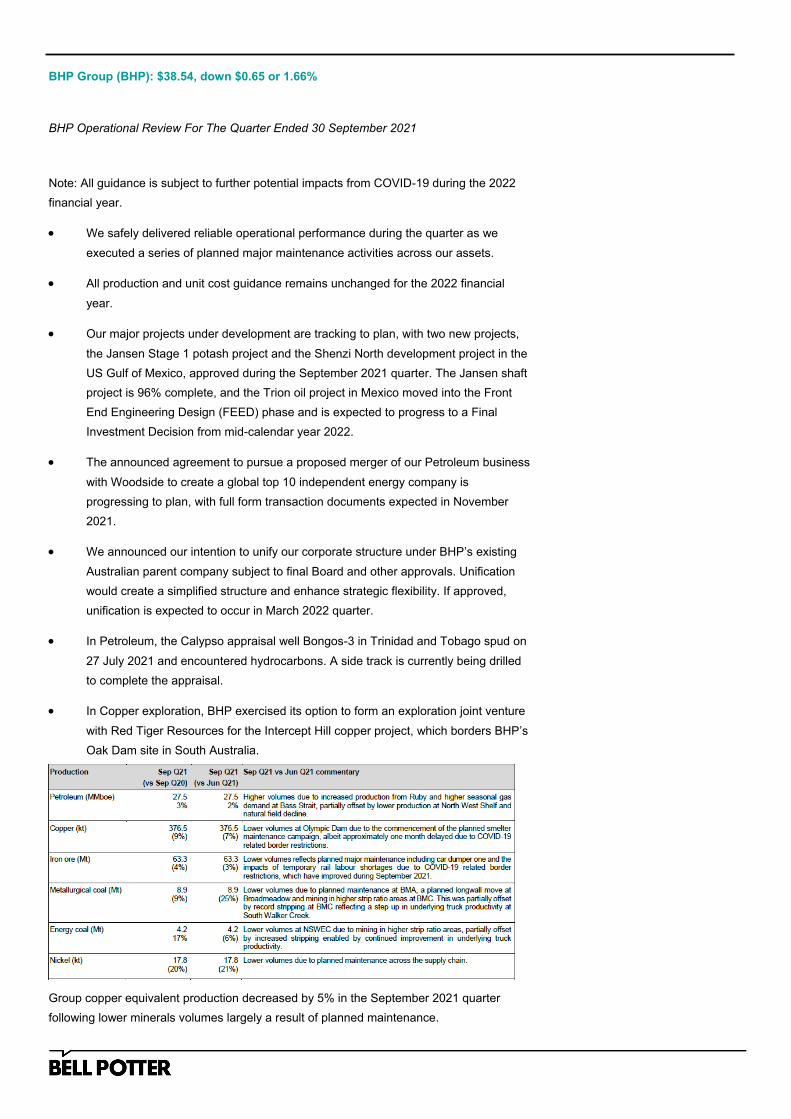

BHP Group (BHP): $38.54, down $0.65 or 1.66%

BHP Operational Review For The Quarter Ended 30 September 2021

Note: All guidance is subject to further potential impacts from COVID-19 during the 2022

financial year.

We safely delivered reliable operational performance during the quarter as we

executed a series of planned major maintenance activities across our assets.

All production and unit cost guidance remains unchanged for the 2022 financial

year.

Our major projects under development are tracking to plan, with two new projects,

the Jansen Stage 1 potash project and the Shenzi North development project in the

US Gulf of Mexico, approved during the September 2021 quarter. The Jansen shaft

project is 96% complete, and the Trion oil project in Mexico moved into the Front

End Engineering Design (FEED) phase and is expected to progress to a Final

Investment Decision from mid-calendar year 2022.

The announced agreement to pursue a proposed merger of our Petroleum business

with Woodside to create a global top 10 independent energy company is

progressing to plan, with full form transaction documents expected in November

2021.

We announced our intention to unify our corporate structure under BHP’s existing

Australian parent company subject to final Board and other approvals. Unification

would create a simplified structure and enhance strategic flexibility. If approved,

unification is expected to occur in March 2022 quarter.

In Petroleum, the Calypso appraisal well Bongos-3 in Trinidad and Tobago spud on

27 July 2021 and encountered hydrocarbons. A side track is currently being drilled

to complete the appraisal.

In Copper exploration, BHP exercised its option to form an exploration joint venture

with Red Tiger Resources for the Intercept Hill copper project, which borders BHP’s

Oak Dam site in South Australia.

Group copper equivalent production decreased by 5% in the September 2021 quarter

following lower minerals volumes largely a result of planned maintenance.

Tabcorp Holdings (TAH): $5.10, down $0.13 or 2.49%

AGM

Trading update

I would now like to provide an update on trading for the three months to 30

September 2021. This information is unaudited and provided for information

purposes only.

Particularly given the extraordinarily fluid situation pertaining to COVID-19, it should

not be considered a forecast or market guidance.

Extensive COVID-19 restrictions had a significant impact in the quarter, with group

revenue down 7.3% on the pcp.

Lotteries & Keno revenue was down 0.2%. Lotteries revenue was up 1.4% due to

growth in Powerball and Saturday Lotto, and the lotteries retail network was not

materially impacted. Keno revenue was down 19.3% due to the adverse impacts of

venue closures.

Wagering & Media revenue, which was down 17.2%, was adversely impacted by

venue closures, partly offset by some transfer to digital.

There was a significant increase in wagering generosities and advertising in a highly

competitive and largely digital market. The increased generosity spend also had a

negative impact on variable contribution margin in Wagering & Media.

Operating expense growth was also impacted by increased technology investment,

including

improved disaster recovery capability.

Gaming Services revenue was down 14.6%. Venue closures continued to adversely

impact revenues and the business continued to provide fee relief to closed venues.

Gaming Services had significant operating expense growth given COVID-19 cost

mitigations in the pcp.

The Star Entertainment Group (SGR): $3.71, up $0.01 or 0.27%

Debt Covenant Support

The Star Entertainment Group Limited (The Star) has secured debt covenant support

from its financiers for the 31 December 2021 and 30 June 2022 testing dates.

The Star has received a full waiver of the gearing and interest cover covenants for

the 31 December 2021 testing date.

For the 30 June 2022 testing date, The Star will be able to annualise its 2H FY2022

earnings for the purpose of calculating its financial covenant ratios and it has also

received an amendment to the gearing and interest cover ratio metrics, which provide

additional headroom.

Other than these amendments, there are no material changes to margins or terms of

existing debt facilities.

Consistent with the June 2020 covenant waiver, a restriction on the payment of cash

dividends remains to the extent gearing (net debt / trailing 12-month statutory

EBITDA) is above 2.5 times. The amendments to the June 2022 covenants provide

The Star the flexibility to pay a cash dividend for the 2H FY2022 period provided net

debt to annualised 2H FY2022 statutory EBITDA is below 2.5 times.

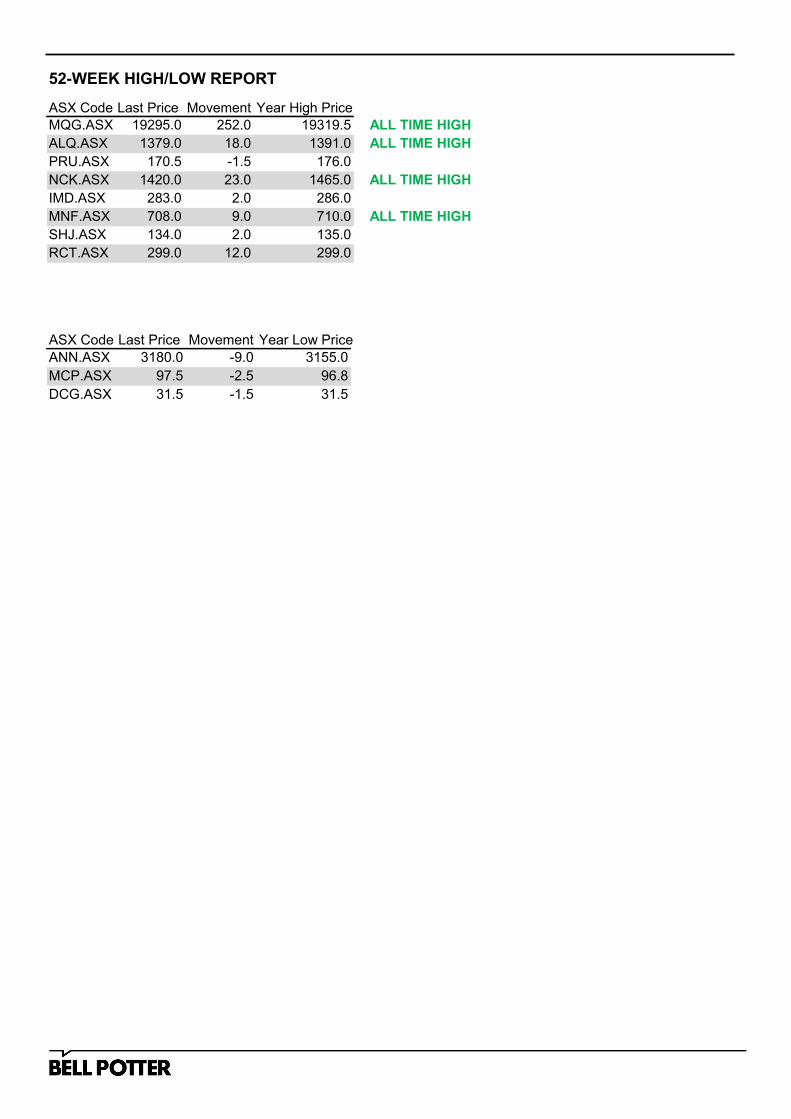

52-WEEK HIGH/LOW REPORT

ASX Code Last Price Movement Year Low Price

ANN.ASX 3180.0 -9.0 3155.0

MCP.ASX 97.5 -2.5 96.8

DCG.ASX 31.5 -1.5 31.5

ASX Code Last Price Movement Year High Price

MQG.ASX 19295.0 252.0 19319.5 ALL TIME HIGH

ALQ.ASX 1379.0 18.0 1391.0 ALL TIME HIGH

PRU.ASX 170.5 -1.5 176.0

NCK.ASX 1420.0 23.0 1465.0 ALL TIME HIGH

IMD.ASX 283.0 2.0 286.0

MNF.ASX 708.0 9.0 710.0 ALL TIME HIGH

SHJ.ASX 134.0 2.0 135.0

RCT.ASX 299.0 12.0 299.0

SHORT POSITION REPORT

Aggregate short position per stock (greater than 5%)

ASX Code % Short Position (14 Sep 2021) %Short Position (05 Oct 2021) % Short Position (12 Oct 2021) Weekly Movement

FLT 10.79% 10.62% 10.17% -4.20%

WEB 9.64% 8.02% 9.34% 16.39%

KGN 9.24% 7.76% 9.25% 19.12%

MSB 8.46% 8.24% 8.97% 8.85%

EOS 8.76% 6.72% 8.70% 29.40%

Z1P 9.21% 8.44% 8.68% 2.82%

RBL 7.72% 7.00% 8.38% 19.70%

ING 7.99% 8.06% 8.21% 1.89%

COE 7.59% 5.43% 7.38% 35.88%

TGR 7.20% 5.12% 7.08% 38.20%

TPW 6.20% 5.21% 6.31% 21.03%

BHP 5.63% 5.92% 6.24% 5.31%

MTS 6.38% 6.31% 6.16% -2.30%

A2M 6.53% 6.10% 100.00%

PNV 5.78% 6.10% 100.00%

AMA 5.43% 6.77% 6.00% -11.29%

EML 5.77% 100.00%

OBL 5.65% 100.00%

BGL 5.11% 100.00%

KLA 5.03% 100.00%

PLL 8.21%

RSG 7.37%

AGL 6.34%

SOURCE: ASIC

GLOBAL UPDATES

Index Last Change % Move Comments

Japan Nikkei 225 29,104.0 78.5 0.27%

China Shanghai

Composite

3,568.1 0.0 0.00%

Hong Kong Hang Seng 25,486.5 76.8 0.30%

Singapore Straits Times 3,200.4 26.6 0.84%

New Zealand NZ Exchange

50

13,047.9 49.4 0.38%

US & UK Futures

US Dow Jones 35,069.0 -64.0 -0.18%

US S&P 500 4,473.0 -4.5 -0.10%

UK FTSE 100 7,177.5 -4.5 -0.06%

6. IRESS

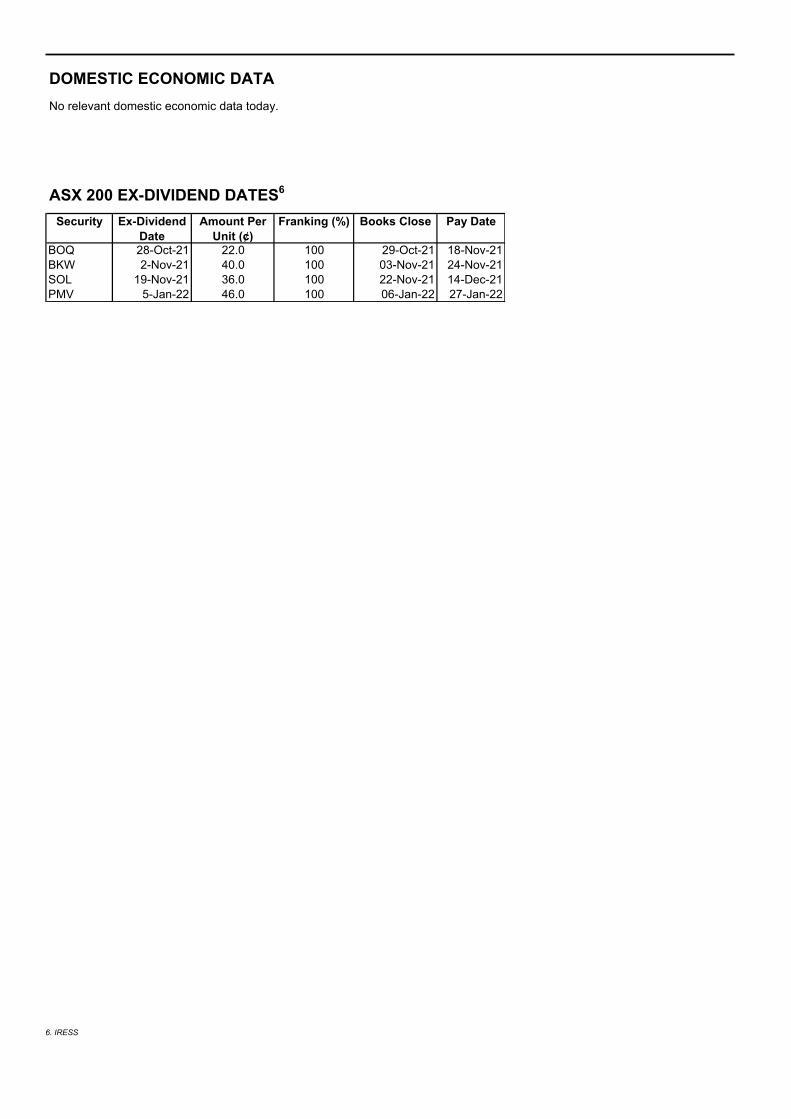

DOMESTIC ECONOMIC DATA

No relevant domestic economic data today.

ASX 200 EX-DIVIDEND DATES

6

Security Ex-Dividend

Date

Amount Per

Unit (¢)

Franking (%) Books Close Pay Date

BOQ 28-Oct-21 22.0 100 29-Oct-21 18-Nov-21

BKW 2-Nov-21 40.0 100 03-Nov-21 24-Nov-21

SOL 19-Nov-21 36.0 100 22-Nov-21 14-Dec-21

PMV 5-Jan-22 46.0 100 06-Jan-22 27-Jan-22

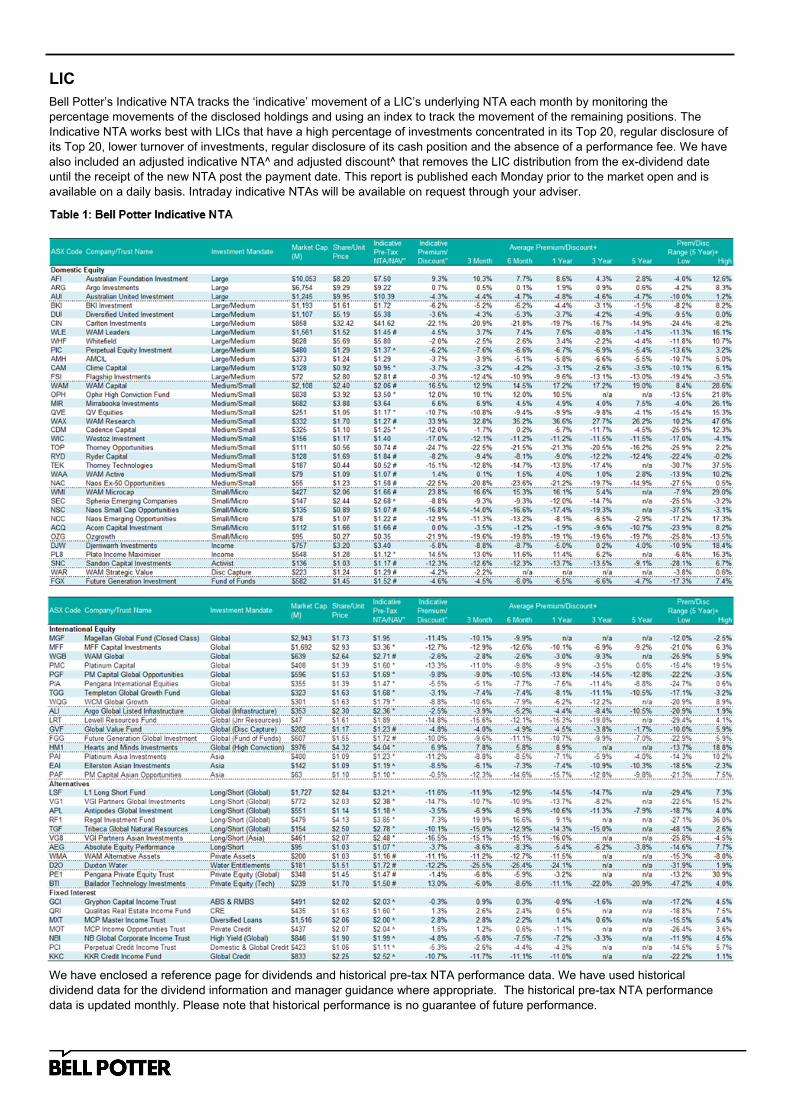

LIC

Bell Potter’s Indicative NTA tracks the ‘indicative’ movement of a LIC’s underlying NTA each month by monitoring the

percentage movements of the disclosed holdings and using an index to track the movement of the remaining positions. The

Indicative NTA works best with LICs that have a high percentage of investments concentrated in its Top 20, regular disclosure of

its Top 20, lower turnover of investments, regular disclosure of its cash position and the absence of a performance fee. We have

also included an adjusted indicative NTA^ and adjusted discount^ that removes the LIC distribution from the ex-dividend date

until the receipt of the new NTA post the payment date. This report is published each Monday prior to the market open and is

available on a daily basis. Intraday indicative NTAs will be available on request through your adviser.

We have enclosed a reference page for dividends and historical pre-tax NTA performance data. We have used historical

dividend data for the dividend information and manager guidance where appropriate. The historical pre-tax NTA performance

data is updated monthly. Please note that historical performance is no guarantee of future performance.

Please be aware that our back testing indicates that this process is not without error and is clearly susceptible to higher turnover,

tax realisation and the receipt and payment of dividends. The average absolute movement in any month of the All Ordinaries is

3.2% with a maximum monthly rise of 8.1% and decline of 13.9% over the last 10 years. Overlaid with the compression or

expansion of the discount or premium to the underlying pre-tax NTA can make it difficult for the investor to appropriately evaluate

the LIC. Please refer to the attached PDF for additional data.

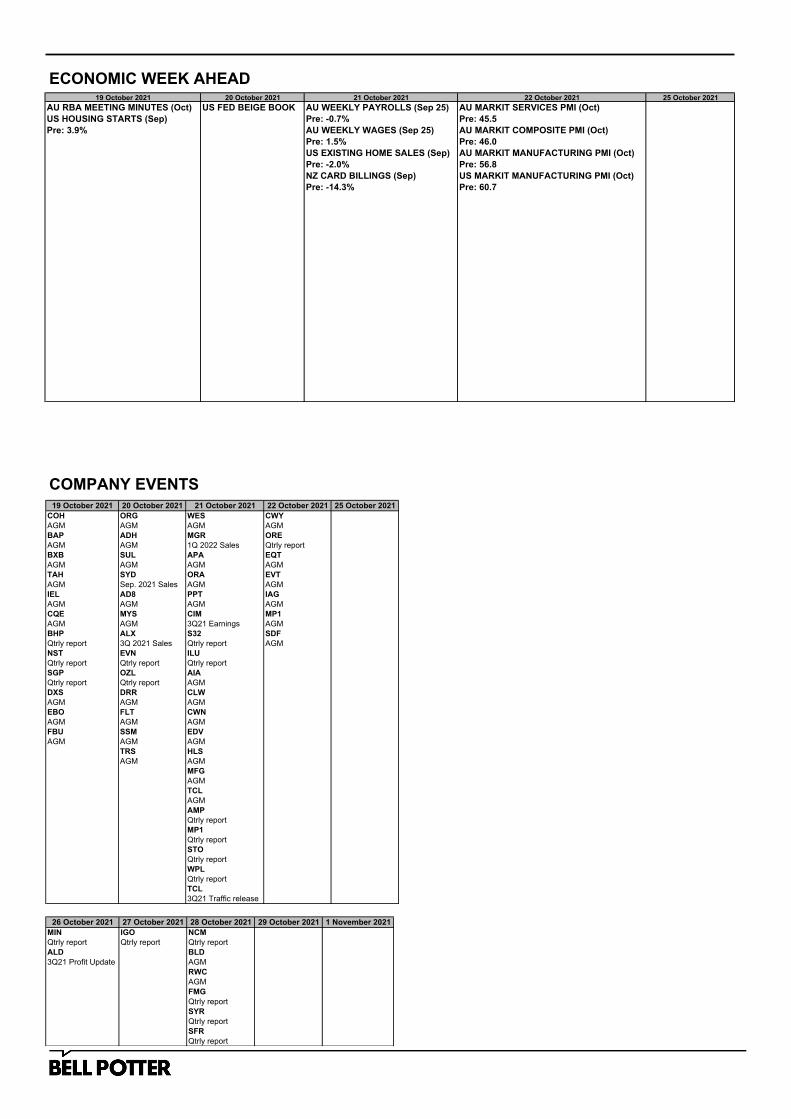

ECONOMIC WEEK AHEAD

COMPANY EVENTS

19 October 2021 20 October 2021 21 October 2021 22 October 2021 25 October 2021

AU RBA MEETING MINUTES (Oct)

US HOUSING STARTS (Sep)

Pre: 3.9%

US FED BEIGE BOOK AU WEEKLY PAYROLLS (Sep 25)

Pre: -0.7%

AU WEEKLY WAGES (Sep 25)

Pre: 1.5%

US EXISTING HOME SALES (Sep)

Pre: -2.0%

NZ CARD BILLINGS (Sep)

Pre: -14.3%

AU MARKIT SERVICES PMI (Oct)

Pre: 45.5

AU MARKIT COMPOSITE PMI (Oct)

Pre: 46.0

AU MARKIT MANUFACTURING PMI (Oct)

Pre: 56.8

US MARKIT MANUFACTURING PMI (Oct)

Pre: 60.7

19 October 2021 20 October 2021 21 October 2021 22 October 2021 25 October 2021

COH ORG WES CWY

AGM AGM AGM AGM

BAP ADH MGR ORE

AGM AGM 1Q 2022 Sales Qtrly report

BXB SUL APA EQT

AGM AGM AGM AGM

TAH SYD ORA EVT

AGM Sep. 2021 Sales AGM AGM

IEL AD8 PPT IAG

AGM AGM AGM AGM

CQE MYS CIM MP1

AGM AGM 3Q21 Earnings AGM

BHP ALX S32 SDF

Qtrly report 3Q 2021 Sales Qtrly report AGM

NST EVN ILU

Qtrly report Qtrly report Qtrly report

SGP OZL AIA

Qtrly report Qtrly report AGM

DXS DRR CLW

AGM AGM AGM

EBO FLT CWN

AGM AGM AGM

FBU SSM EDV

AGM AGM AGM

TRS HLS

AGM AGM

MFG

AGM

TCL

AGM

AMP

Qtrly report

MP1

Qtrly report

STO

Qtrly report

WPL

Qtrly report

TCL

3Q21 Traffic release

26 October 2021 27 October 2021 28 October 2021 29 October 2021 1 November 2021

MIN IGO NCM

Qtrly report Qtrly report Qtrly report

ALD BLD

3Q21 Profit Update AGM

RWC

AGM

FMG

Qtrly report

SYR

Qtrly report

SFR

Qtrly report

The following may affect your legal rights:

Important Disclaimer: This document is a private communication to clients and is not intended for public circulation or for the use of any third party, without the prior approval of Bell Potter Securities Limited. In the USA and the UK this research is only for institutional investors. It is not for release, publication or distribution in whole or in part to any persons in the two specified countries. This is general investment advice only and does not constitute personal advice to any person. Because this document has been prepared without consideration of any specific client’s financial situation, particular needs and investment objectives (‘relevant personal circumstances’), a Bell Potter Securities Limited investment adviser (or the financial services licensee, or the representative of such licensee, who has provided you with this report by arrangement with Bell Potter Securities Limited) should be made aware of your relevant personal circumstances and consulted before any investment decision is made on the basis of this document.

While this document is based on information from sources which are considered reliable, Bell Potter Securities Limited has not verified independently the information contained in the document and Bell Potter Securities Limited and its directors, employees and consultants do not represent, warrant or guarantee, expressly or impliedly, that the information contained in this document is complete or accurate. Nor does Bell Potter Securities Limited accept any responsibility to inform you of any matter that subsequently comes to its notice, which may affect any of the information contained in this document and Bell Potter assumes no responsibility for updating any advice, views, opinions, or recommendations contained in this document or for correcting any error or omission which may become apparent after the document has been issued.

Except insofar as liability under any statute cannot be excluded, Bell Potter Securities Limited and its directors, employees and consultants do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this document or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this document or any other person.

Disclosure of Interest: Bell Potter Securities Limited, its employees, consultants and its associates within the meaning of Chapter 7 of the Corporations Law may receive commissions, underwriting and management fees from transactions involving securities referred to in this document (which its representatives may directly share) and may from time to time hold interests in the securities referred to in this document.

BELL POTTER SECURITIES LIMITED

GPO BOX 4718 MELBOURNE VIC 3001 AUSTRALIA

TOLL FREE 1800 804 816 [email protected] WWW.BELLPOTTER.COM.AU

ABN 25 006 390 772 AFS LICENCE NO.243480