market outlook - sbi funds pms outlook_sep 2017.pdf · new project announcement averages at rs. 8.8...

TRANSCRIPT

Market Outlook

September 2017

EQUITY MARKET

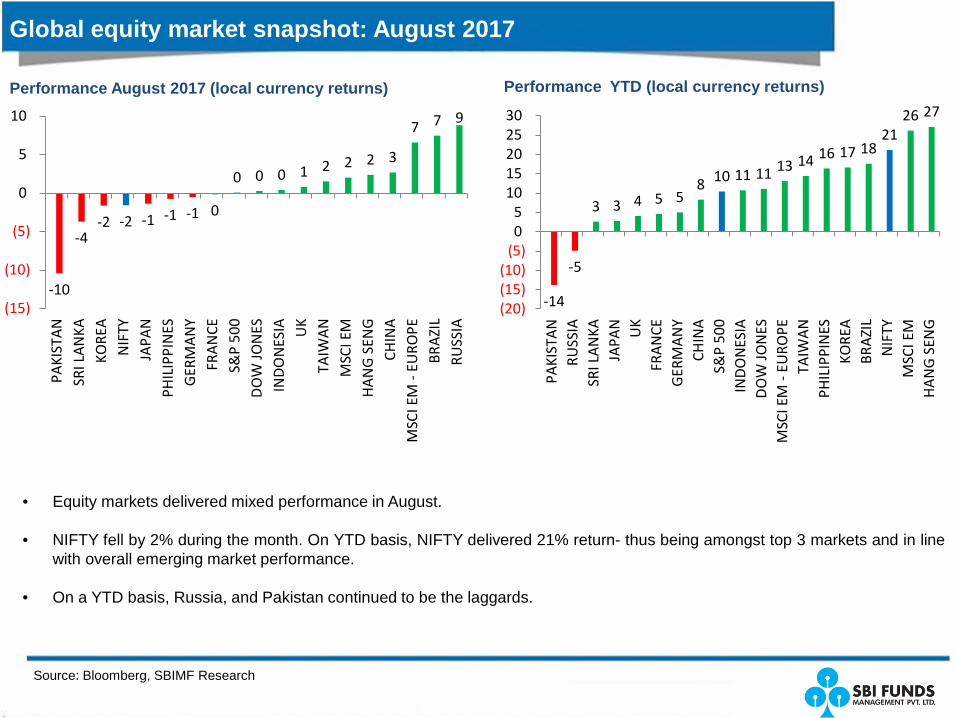

Global equity market snapshot: August 2017

Source: Bloomberg, SBIMF Research

• Equity markets delivered mixed performance in August.

• NIFTY fell by 2% during the month. On YTD basis, NIFTY delivered 21% return- thus being amongst top 3 markets and in linewith overall emerging market performance.

• On a YTD basis, Russia, and Pakistan continued to be the laggards.

Performance August 2017 (local currency returns) Performance YTD (local currency returns)

-10

-4-2 -2 -1 -1 -1 0

0 0 0 1 2 2 2 3

7 7 9

(15)

(10)

(5)

0

5

10

PAKI

STA

NSR

I LA

NKA

KORE

AN

IFTY

JAPA

NPH

ILIP

PIN

ESG

ERM

AN

YFR

AN

CES&

P 50

0D

OW

JON

ESIN

DO

NES

IA UK

TAIW

AN

MSC

I EM

HA

NG

SEN

GCH

INA

MSC

I EM

- EU

ROPE

BRA

ZIL

RUSS

IA

-14

-5

3 3 4 5 58 10 11 11 13 14 16 17 18

2126 27

(20)(15)(10)

(5)05

1015202530

PAKI

STA

NRU

SSIA

SRI L

AN

KAJA

PAN UK

FRA

NCE

GER

MA

NY

CHIN

AS&

P 50

0IN

DO

NES

IAD

OW

JON

ESM

SCI E

M -

EURO

PETA

IWA

NPH

ILIP

PIN

ESKO

REA

BRA

ZIL

NIF

TYM

SCI E

MH

AN

G S

ENG

Indian stock market snapshot: August 2017

Performance in August 2017

Source: Bloomberg, SBIMF Research

• Nifty and Sensex are down by 2% each in August. While the small cap was down by 1%, mid cap delivered positive 1% returnsduring the month.

• Sector-wise: While majority sectors under-performed (Pharma being the lowest), Oil & Gas, Metals and FMCG outshinedduring the month.

• YTD, Nifty and Sensex are up by 21% and 19% respectively. Sector-wise performance has been positive across all sectors ona YTD basis (barring Pharma and IT). Real estate continued to out-perform significantly (up 69%).

Performance YTD

-7

-4 -4 -3 -3-2 -2 -2 -1 -1 -1 0

1 1

7 7

(10)

(8)

(6)

(4)

(2)

0

2

4

6

8

PHA

RMA IT

CAP

GO

OD

S

BAN

KEX

AU

TO

SEN

SEX

REA

L ES

TATE

NIF

TY

BSE

100

BSE

500

SMA

LL C

AP

PSU

FMCG

MID

CA

P

MET

ALS

OIL

& G

AS

-11

-1

1217 19 21 23 25 25 25 27 29 31 32 33

69

(20)

(10)

0

10

20

30

40

50

60

70

80

PHA

RMA IT

PSU

AU

TO

SEN

SEX

NIF

TY

BSE

100

BSE

500

OIL

& G

AS

FMCG

CAP

GO

OD

S

MID

CA

P

MET

ALS

BAN

KEX

SMA

LL C

AP

REA

L ES

TATE

Source: CMIE, SBIMF Research,

Growth has been weakening; private investment is matter of concern

Growth has been moderating since June 2016

8.7

5.6

9.1

6.1

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Jun-

12

Oct

-12

Feb-

13

Jun-

13

Oct

-13

Feb-

14

Jun-

14

Oct

-14

Feb-

15

Jun-

15

Oct

-15

Feb-

16

Jun-

16

Oct

-16

Feb-

17

Jun-

17

Real GVA at basic prices Real GDP

% y-o-y• 1Q FY18 GDP depicted the continued weakness in growth trends

(5.7% y-o-y vs. 6.1% in 4Q FY18). Growth prints have beenheading south for 5 consecutive quarters now.

• Private consumption demand that has been the mainstay of GDPgrowth slowed to 6.7%YoY in 1Q (vs. 8.7% growth in FY17) asconsumer confidence took a knock post demonetization.Investment came at a muted 1.6% which is still better than adecline of -2.1% posted in the previous quarter. That said, theinvestment scenario is far from encouraging. Net exports was adrag in 1Q subtracting 2.6% from GDP growth. The nominal GDPgrowth slowed to 9.3%YoY from 12.5%.

• From the supply side, GVA growth stayed flat at 5.6%. While thegrowth in agriculture (2.3% y-o-y vs. 5.2% in Q4 FY17) and industry(1.6% vs. 3.1%) slipped, services growth accelerated to 8.7% (vs.7.2%) helped by improved prospects of business services andtrade , hotels and transport services. Social services, which reflectsgovernment expenditure, on the other hand, slipped significantly.

• We expect FY18 growth to average around 6.9% y-o-y, 40bps lowerthan RBI’s estimate of 7.3% for the year. Consumption mayimprove through the year helped by implementation of farm loanwaiver, pay commission implementation by states, third consecutiveseason of healthy agriculture output, rising recourse to leveragedconsumption. On the other hand, floundering investment climateshows no sign of recovery in near-term and can be a drag on thepotential of the economy.

6.1 7.3

31.9

-2.1

10.3 11.9

5.7 6.7

17.2

1.6 1.2

13.4

GD

Pmp

Pvt C

onsu

mpt

ion

Gov

t Spe

ndin

g

Inve

stm

ent

Expo

rts

Impo

rts

Q4-2016-17 Q1 2017-18

% y-o-y

Government spending is a major growth driver

Source: CMIE, CWC, IMDB, pib.nic.in, SBIMF Research,

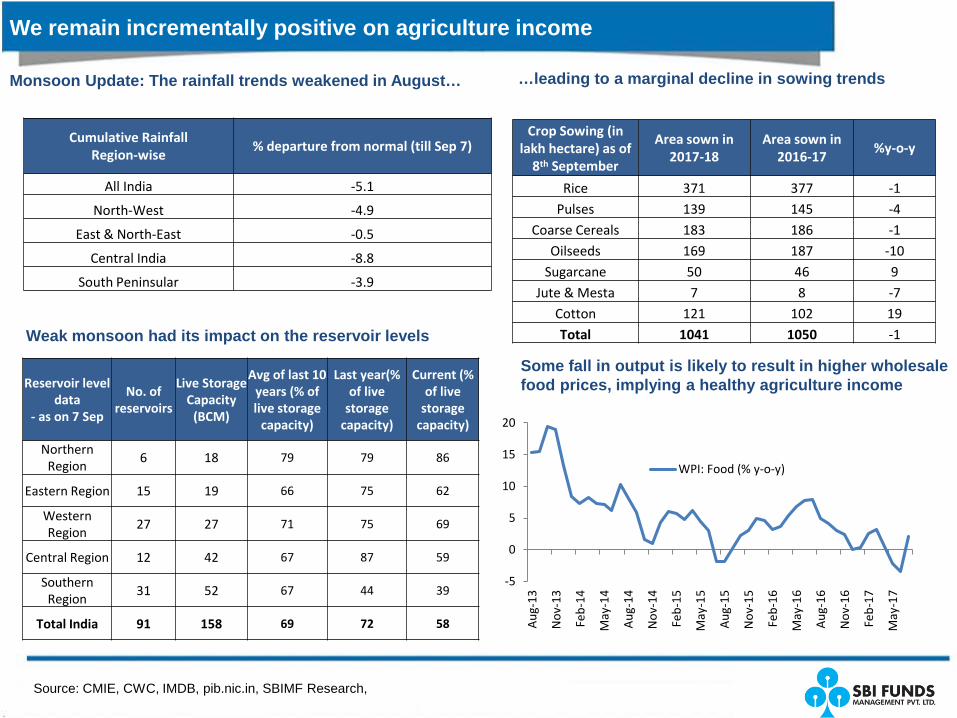

We remain incrementally positive on agriculture income

…leading to a marginal decline in sowing trends

Crop Sowing (in lakh hectare) as of

8th September

Area sown in 2017-18

Area sown in 2016-17 %y-o-y

Rice 371 377 -1Pulses 139 145 -4

Coarse Cereals 183 186 -1Oilseeds 169 187 -10

Sugarcane 50 46 9Jute & Mesta 7 8 -7

Cotton 121 102 19Total 1041 1050 -1

Some fall in output is likely to result in higher wholesale food prices, implying a healthy agriculture income

Cumulative RainfallRegion-wise % departure from normal (till Sep 7)

All India -5.1

North-West -4.9

East & North-East -0.5

Central India -8.8

South Peninsular -3.9

Monsoon Update: The rainfall trends weakened in August…

Reservoir level data

- as on 7 Sep

No. of reservoirs

Live Storage Capacity

(BCM)

Avg of last 10 years (% of live storage

capacity)

Last year(% of live

storage capacity)

Current (% of live

storage capacity)

Northern Region

6 18 79 79 86

Eastern Region 15 19 66 75 62

Western Region

27 27 71 75 69

Central Region 12 42 67 87 59

Southern Region

31 52 67 44 39

Total India 91 158 69 72 58

Weak monsoon had its impact on the reservoir levels

-5

0

5

10

15

20

Aug

-13

Nov

-13

Feb-

14

May

-14

Aug

-14

Nov

-14

Feb-

15

May

-15

Aug

-15

Nov

-15

Feb-

16

May

-16

Aug

-16

Nov

-16

Feb-

17

May

-17

WPI: Food (% y-o-y)

Source: CMIE, SBIMF Research,

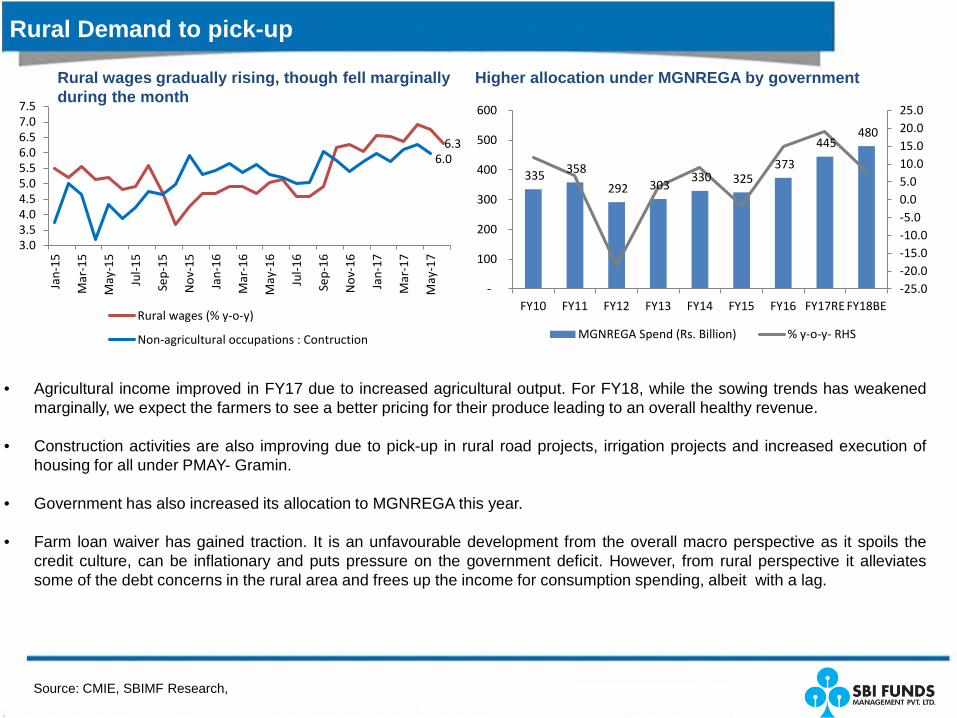

Rural Demand to pick-up

Rural wages gradually rising, though fell marginally during the month

• Agricultural income improved in FY17 due to increased agricultural output. For FY18, while the sowing trends has weakenedmarginally, we expect the farmers to see a better pricing for their produce leading to an overall healthy revenue.

• Construction activities are also improving due to pick-up in rural road projects, irrigation projects and increased execution ofhousing for all under PMAY- Gramin.

• Government has also increased its allocation to MGNREGA this year.

• Farm loan waiver has gained traction. It is an unfavourable development from the overall macro perspective as it spoils thecredit culture, can be inflationary and puts pressure on the government deficit. However, from rural perspective it alleviatessome of the debt concerns in the rural area and frees up the income for consumption spending, albeit with a lag.

Higher allocation under MGNREGA by government

335 358

292 303 330 325

373

445 480

-25.0-20.0-15.0-10.0-5.00.05.010.015.020.025.0

-

100

200

300

400

500

600

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17RE FY18BE

MGNREGA Spend (Rs. Billion) % y-o-y- RHS

6.36.0

3.03.54.04.55.05.56.06.57.07.5

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep-

16

Nov

-16

Jan-

17

Mar

-17

May

-17

Rural wages (% y-o-y)

Non-agricultural occupations : Contruction

Source: CMIE, SBIMF Research,

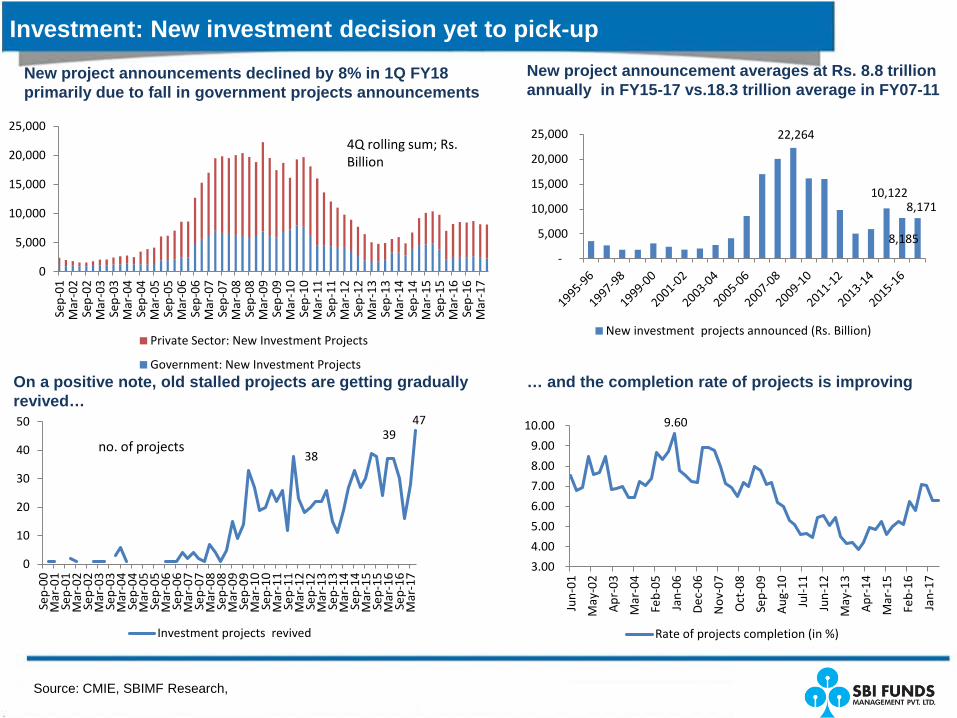

Investment: New investment decision yet to pick-up

0

5,000

10,000

15,000

20,000

25,000

Sep-

01M

ar-0

2Se

p-02

Mar

-03

Sep-

03M

ar-0

4Se

p-04

Mar

-05

Sep-

05M

ar-0

6Se

p-06

Mar

-07

Sep-

07M

ar-0

8Se

p-08

Mar

-09

Sep-

09M

ar-1

0Se

p-10

Mar

-11

Sep-

11M

ar-1

2Se

p-12

Mar

-13

Sep-

13M

ar-1

4Se

p-14

Mar

-15

Sep-

15M

ar-1

6Se

p-16

Mar

-17

Private Sector: New Investment Projects

Government: New Investment Projects

4Q rolling sum; Rs. Billion

New project announcements declined by 8% in 1Q FY18 primarily due to fall in government projects announcements

22,264

10,122

8,185

8,171

-

5,000

10,000

15,000

20,000

25,000

New investment projects announced (Rs. Billion)

New project announcement averages at Rs. 8.8 trillion annually in FY15-17 vs.18.3 trillion average in FY07-11

On a positive note, old stalled projects are getting gradually revived…

… and the completion rate of projects is improving

9.60

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Jun-

01

May

-02

Apr

-03

Mar

-04

Feb-

05

Jan-

06

Dec

-06

Nov

-07

Oct

-08

Sep-

09

Aug

-10

Jul-1

1

Jun-

12

May

-13

Apr

-14

Mar

-15

Feb-

16

Jan-

17

Rate of projects completion (in %)

38

3947

0

10

20

30

40

50

Sep-

00M

ar-0

1Se

p-01

Mar

-02

Sep-

02M

ar-0

3Se

p-03

Mar

-04

Sep-

04M

ar-0

5Se

p-05

Mar

-06

Sep-

06M

ar-0

7Se

p-07

Mar

-08

Sep-

08M

ar-0

9Se

p-09

Mar

-10

Sep-

10M

ar-1

1Se

p-11

Mar

-12

Sep-

12M

ar-1

3Se

p-13

Mar

-14

Sep-

14M

ar-1

5Se

p-15

Mar

-16

Sep-

16M

ar-1

7

Investment projects revived

no. of projects

Government Infrastructure push positive for growth

Source: Spark, Government documents, SBIFM Research

299384 386

932

13071432

0

200

400

600

800

1000

1200

1400

1600

FY13 FY14 FY15 FY16 FY17RE FY18BE

Road infra (Rs. Billion)

Spending on Road construction has jumped 3.7xtimes in last 3 years

Execution has picked up pace in Road construction

492 520643

935

12101310

0

200

400

600

800

1000

1200

1400

FY13 FY14 FY15 FY16 FY17RE FY18BE

Railways infra (Rs. Billion)

Spending on Railways has jumped 2 times in last 3 years

Railways- another key area of spend

55

90 84

121

196 199

0

50

100

150

200

250

FY13 FY14 FY15 FY16 FY17RE FY18BE

Metro and MRTS Projects

Metro spending projected to grow at 12%

Metro construction happening in partnership with states and JICA

980 9601059 1145

14411565

0

500

1000

1500

2000

FY13 FY14 FY15 FY16 FY17RE FY18BE

Rural and Agri Spending

Irrigation and Rural Development

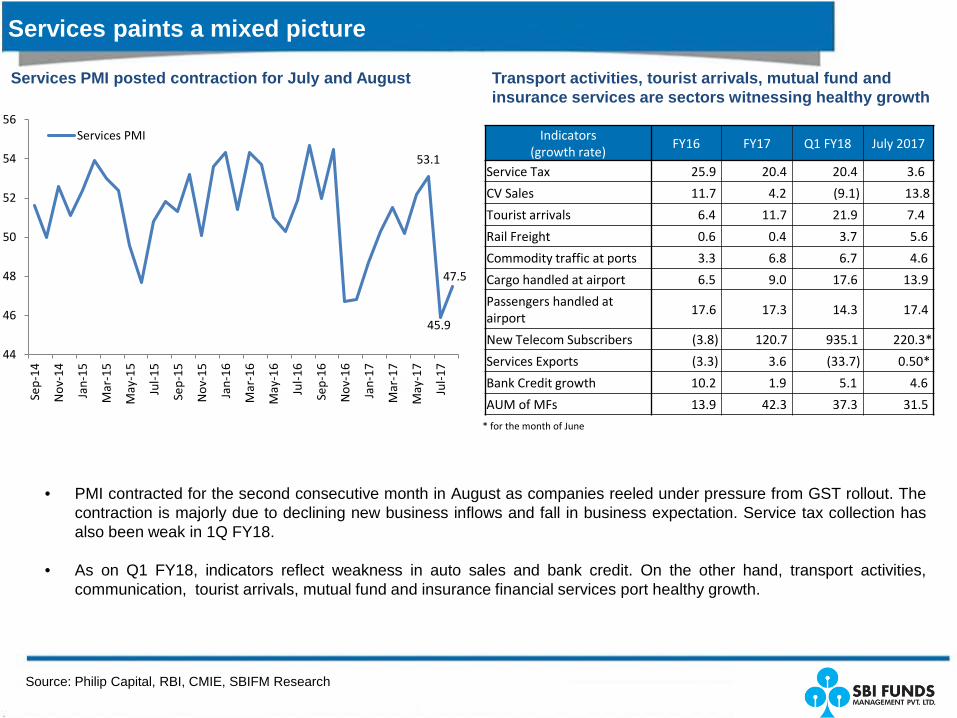

Services paints a mixed picture

Source: Philip Capital, RBI, CMIE, SBIFM Research

• PMI contracted for the second consecutive month in August as companies reeled under pressure from GST rollout. Thecontraction is majorly due to declining new business inflows and fall in business expectation. Service tax collection hasalso been weak in 1Q FY18.

• As on Q1 FY18, indicators reflect weakness in auto sales and bank credit. On the other hand, transport activities,communication, tourist arrivals, mutual fund and insurance financial services port healthy growth.

Services PMI posted contraction for July and August Transport activities, tourist arrivals, mutual fund and insurance services are sectors witnessing healthy growth

Indicators (growth rate)

FY16 FY17 Q1 FY18 July 2017

Service Tax 25.9 20.4 20.4 3.6

CV Sales 11.7 4.2 (9.1) 13.8

Tourist arrivals 6.4 11.7 21.9 7.4

Rail Freight 0.6 0.4 3.7 5.6

Commodity traffic at ports 3.3 6.8 6.7 4.6

Cargo handled at airport 6.5 9.0 17.6 13.9

Passengers handled at airport

17.6 17.3 14.3 17.4

New Telecom Subscribers (3.8) 120.7 935.1 220.3*

Services Exports (3.3) 3.6 (33.7) 0.50*

Bank Credit growth 10.2 1.9 5.1 4.6

AUM of MFs 13.9 42.3 37.3 31.5

53.1

45.9

47.5

44

46

48

50

52

54

56

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep-

16

Nov

-16

Jan-

17

Mar

-17

May

-17

Jul-1

7

Services PMI

* for the month of June

Source: SBIMF Research

Reforms by government makes market positive about future growth

Key Reforms in recent months

• Affordable Housing picks-up pace: The government has targeted construction of 51 lakh houses in 2017-18that would meet its target of one crore houses by 2019 under the revised Pradhan Mantri Awaas YojanaGramin (PMAY-G) and hopes to bring down the building time to 6-12 months from 18 months to 3 yearsearlier. Over 32 lakh houses have been reported complete in FY17 and 18 lakh in FY16.

• Real Estate Regulation Act: Implemented on a nation-wide basis on 1st May. RERA ensures that there isenough long term visibility for players with strong corporate governance, brand and capital allocationstandards

• Banking Regulation (Amendment) 2017 Act: The Ordinance empowering the RBI has been passed in theparliament. The measure allows the RBI to initiate insolvency resolution process on specific stressedassets.This is a positive move for clearing stressed loans which are 13% of total loans.

• GST: Smooth roll-out of GST is a significant positive for long-run growth of Indian economy

• Thrust on Rural economy: Measures such as rural electrification, construction of rural roads, crop insurancescheme and rural housing are structurally positive for Indian rural economy

• Disinvestment: The government will soon float a request for proposal (RFP) for selection of transactionadviser, legal adviser as well as asset valuer for the proposed Air India disinvestment.

• Revision of LPG and kerosene prices: Government has asked state-run oil companies to raise subsidisedcooking gas (LPG) prices by Rs 4 per cylinder every month and prices of subsidised kerosene by 25 paiseevery fortnight until the subsidy is eliminated. The hike in the price comes in the backdrop of the government’sdecision to eliminate all the subsidies on fuel by the fiscal end.

Earnings: Choppy for Q1 FY18

Source: Antique, SBIFM Research

Earnings for FY18 downgraded while markets continue to expect 20% EPS growth for FY19

• 1QFY18 PAT for the Nifty universe, earnings havecontracted by ~10.0% which was also below streetexpectations of a 5-6% decline. The majority of thedrop has been led by OMCs (on account of inventorylosses) and Tata Motors (earnings down 94% led byEBITDA decline in JLR), ex of which there is actually agrowth, albeit a tepid 1.2% y-o-y.

• Higher NPA issues and sector specific challenges in ITand Pharmaceuticals have also dragged the earningsdown. These issues can take longer to mend.

• Other factors explaining the tepid Earnings for thequarter were the adverse impact of GST as theprocess of inventory clearing was visible across thesectors. To simplify, the businesses were in theprocess of clearing out the inventory which were builtin the old taxation regime, had slowed the fresh orderswhich in turn had impacted the manufacturing. To thatextent, earnings should improve as the process ofrestocking start from the current quarter.

• Sharper than anticipated profit decline has led themarket to significantly downgrade FY18 earnings toearly teens (11-12%) while the expectations for FY19earnings continues to hold strong at +20%.

• Corporate profits as percentage of GDP has hit anextremely low point and logically should mean revert.Earnings revival is absolutely critical for such richvaluations to sustain.

95128

175207

239283

247284

330 351385

427391 402

427475

580

-20%

-10%

0%

10%

20%

30%

40%

0

100

200

300

400

500

600

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

e

FY19

e

Nifty EPS YoY, RHS

3.0

4.75.4

6.27.3 7.8

5.56.5 6.2

4.9 4.6 4.33.8

3.1 2.9

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

Average of 5.4%

Corporate profit as percentage of GDP

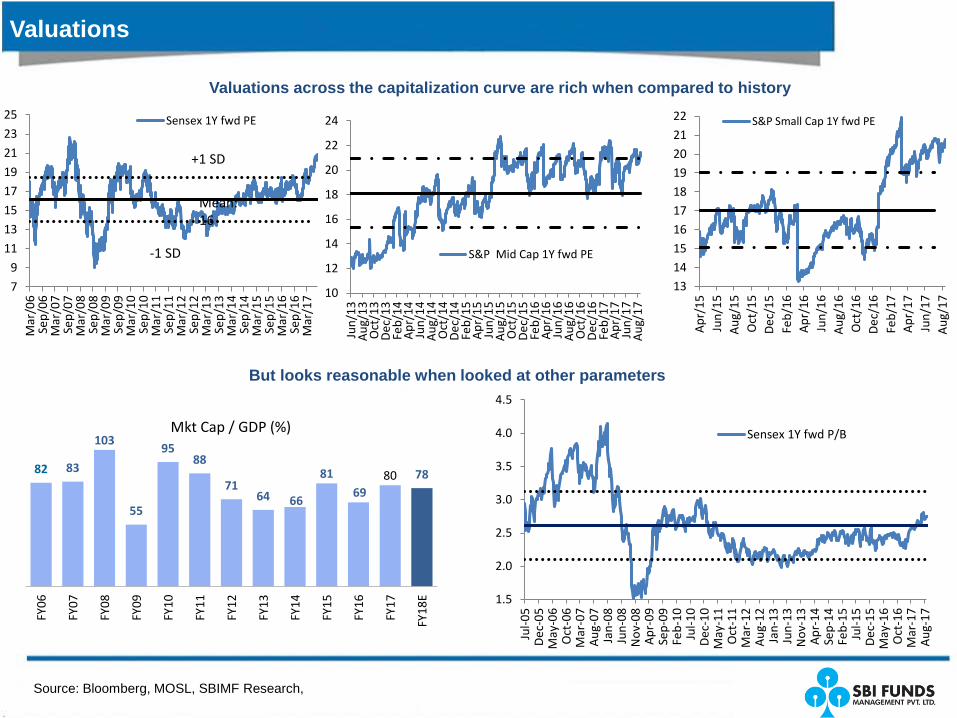

Valuations

13141516171819202122

Apr

/15

Jun/

15A

ug/1

5O

ct/1

5D

ec/1

5Fe

b/16

Apr

/16

Jun/

16A

ug/1

6O

ct/1

6D

ec/1

6Fe

b/17

Apr

/17

Jun/

17A

ug/1

7

S&P Small Cap 1Y fwd PE

10

12

14

16

18

20

22

24

Jun/

13A

ug/1

3O

ct/1

3D

ec/1

3Fe

b/14

Apr

/14

Jun/

14A

ug/1

4O

ct/1

4D

ec/1

4Fe

b/15

Apr

/15

Jun/

15A

ug/1

5O

ct/1

5D

ec/1

5Fe

b/16

Apr

/16

Jun/

16A

ug/1

6O

ct/1

6D

ec/1

6Fe

b/17

Apr

/17

Jun/

17A

ug/1

7

S&P Mid Cap 1Y fwd PE

7

9

11

13

15

17

19

21

23

25

Mar

/06

Sep/

06M

ar/0

7Se

p/07

Mar

/08

Sep/

08M

ar/0

9Se

p/09

Mar

/10

Sep/

10M

ar/1

1Se

p/11

Mar

/12

Sep/

12M

ar/1

3Se

p/13

Mar

/14

Sep/

14M

ar/1

5Se

p/15

Mar

/16

Sep/

16M

ar/1

7

Sensex 1Y fwd PE

Mean: 16

+1 SD

-1 SD

Valuations across the capitalization curve are rich when compared to history

But looks reasonable when looked at other parameters

82 83

103

55

9588

7164 66

8169

80 78

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

EMkt Cap / GDP (%)

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Jul-0

5D

ec-0

5M

ay-0

6O

ct-0

6M

ar-0

7A

ug-0

7Ja

n-08

Jun-

08N

ov-0

8A

pr-0

9Se

p-09

Feb-

10Ju

l-10

Dec

-10

May

-11

Oct

-11

Mar

-12

Aug

-12

Jan-

13Ju

n-13

Nov

-13

Apr

-14

Sep-

14Fe

b-15

Jul-1

5D

ec-1

5M

ay-1

6O

ct-1

6M

ar-1

7A

ug-1

7

Sensex 1Y fwd P/B

Source: Bloomberg, MOSL, SBIMF Research,

Source: Morgan Stanley, SBIMF Research,

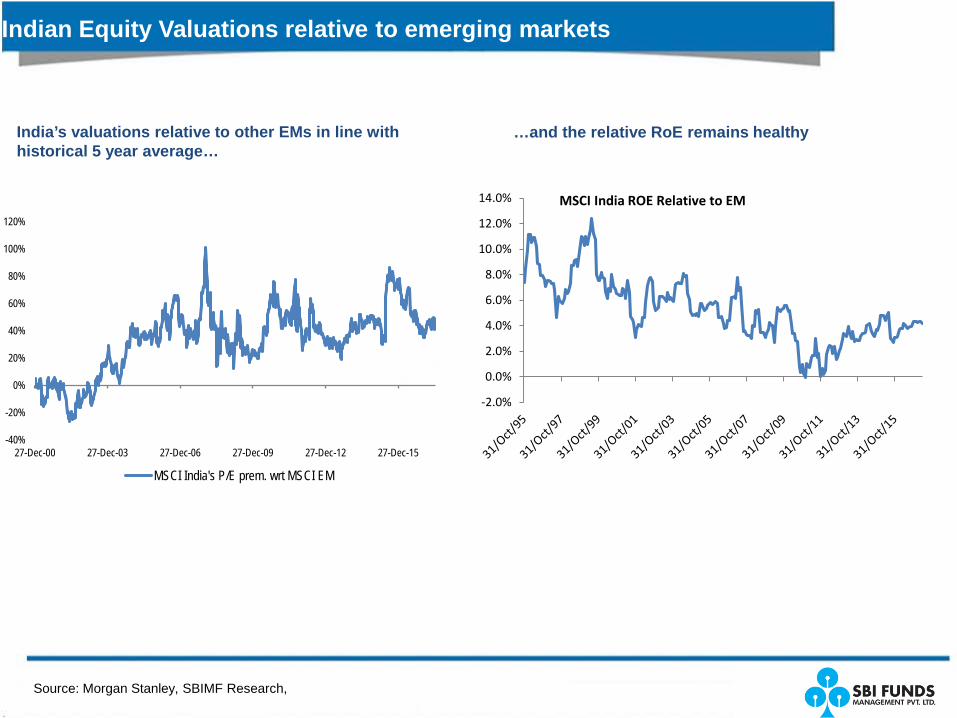

Indian Equity Valuations relative to emerging markets

India’s valuations relative to other EMs in line with historical 5 year average…

…and the relative RoE remains healthy

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0% MSCI India ROE Relative to EM

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

27-Dec-00 27-Dec-03 27-Dec-06 27-Dec-09 27-Dec-12 27-Dec-15

MSCI India's P/E prem. wrt MSCI EM

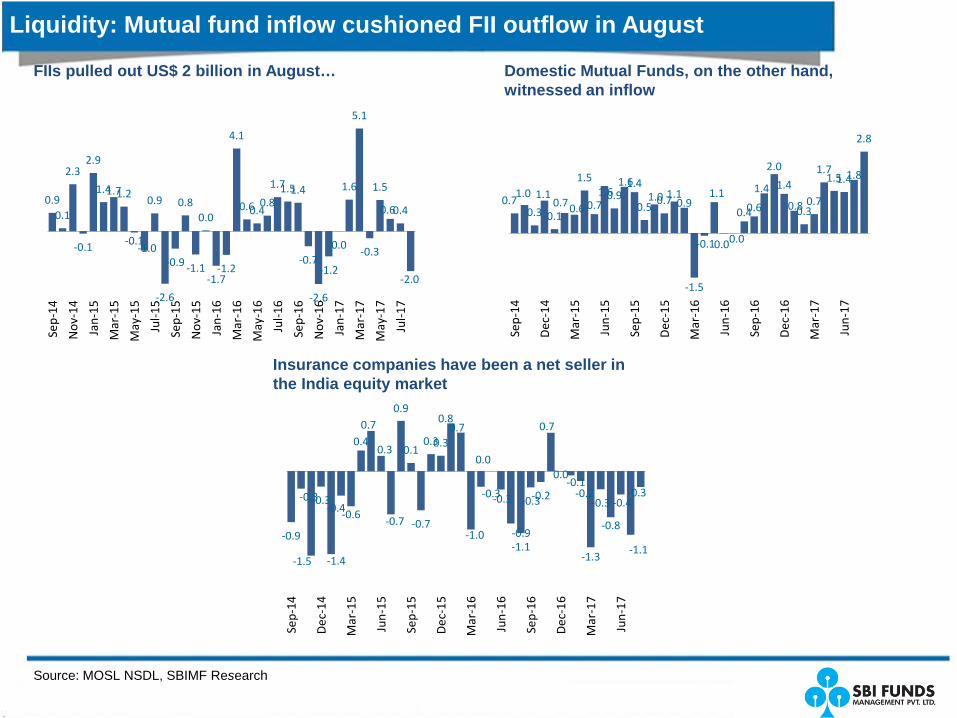

Liquidity: Mutual fund inflow cushioned FII outflow in August

Source: MOSL NSDL, SBIMF Research

FIIs pulled out US$ 2 billion in August… Domestic Mutual Funds, on the other hand, witnessed an inflow

Insurance companies have been a net seller in the India equity market

0.90.1

2.3

-0.1

2.9

1.41.71.2

-0.1-1.0

0.9

-2.6

-0.9

0.8

-1.1

0.0

-1.7-1.2

4.1

0.60.40.8

1.71.51.4

-0.7

-2.6

-1.2

0.0

1.6

5.1

-0.3

1.5

0.60.4

-2.0

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep-

16

Nov

-16

Jan-

17

Mar

-17

May

-17

Jul-1

7

0.71.0

0.3

1.1

0.10.70.6

1.5

0.71.60.9

1.61.4

0.51.00.71.1

0.9

-1.5

-0.1

1.1

0.00.0

0.40.6

1.4

2.0

1.4

0.80.30.7

1.71.51.41.8

2.8

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

Sep-

16

Dec

-16

Mar

-17

Jun-

17

-0.9

-0.3

-1.5

-0.3

-1.4

-0.4-0.6

0.40.7

0.3

-0.7

0.9

0.1

-0.7

0.30.3

0.80.7

-1.0

-0.3

0.0

-0.3

-0.9-1.1

-0.3-0.2

0.7

0.0-0.1

-0.2

-1.3

-0.3

-0.8

-0.4

-1.1

-0.3

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

Sep-

16

Dec

-16

Mar

-17

Jun-

17

Equity Market outlook

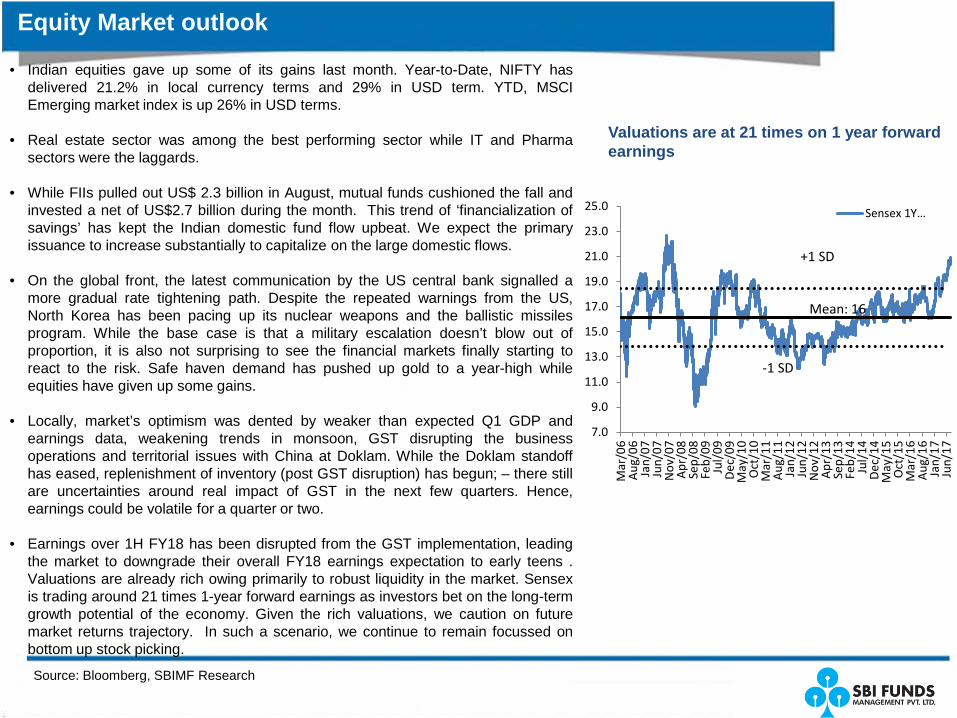

• Indian equities gave up some of its gains last month. Year-to-Date, NIFTY hasdelivered 21.2% in local currency terms and 29% in USD term. YTD, MSCIEmerging market index is up 26% in USD terms.

• Real estate sector was among the best performing sector while IT and Pharmasectors were the laggards.

• While FIIs pulled out US$ 2.3 billion in August, mutual funds cushioned the fall andinvested a net of US$2.7 billion during the month. This trend of ‘financialization ofsavings’ has kept the Indian domestic fund flow upbeat. We expect the primaryissuance to increase substantially to capitalize on the large domestic flows.

• On the global front, the latest communication by the US central bank signalled amore gradual rate tightening path. Despite the repeated warnings from the US,North Korea has been pacing up its nuclear weapons and the ballistic missilesprogram. While the base case is that a military escalation doesn’t blow out ofproportion, it is also not surprising to see the financial markets finally starting toreact to the risk. Safe haven demand has pushed up gold to a year-high whileequities have given up some gains.

• Locally, market’s optimism was dented by weaker than expected Q1 GDP andearnings data, weakening trends in monsoon, GST disrupting the businessoperations and territorial issues with China at Doklam. While the Doklam standoffhas eased, replenishment of inventory (post GST disruption) has begun; – there stillare uncertainties around real impact of GST in the next few quarters. Hence,earnings could be volatile for a quarter or two.

• Earnings over 1H FY18 has been disrupted from the GST implementation, leadingthe market to downgrade their overall FY18 earnings expectation to early teens .Valuations are already rich owing primarily to robust liquidity in the market. Sensexis trading around 21 times 1-year forward earnings as investors bet on the long-termgrowth potential of the economy. Given the rich valuations, we caution on futuremarket returns trajectory. In such a scenario, we continue to remain focussed onbottom up stock picking.

Valuations are at 21 times on 1 year forward earnings

Source: Bloomberg, SBIMF Research

7.0

9.0

11.0

13.0

15.0

17.0

19.0

21.0

23.0

25.0

Mar

/06

Aug

/06

Jan/

07Ju

n/07

Nov

/07

Apr

/08

Sep/

08Fe

b/09

Jul/

09D

ec/0

9M

ay/1

0O

ct/1

0M

ar/1

1A

ug/1

1Ja

n/12

Jun/

12N

ov/1

2A

pr/1

3Se

p/13

Feb/

14Ju

l/14

Dec

/14

May

/15

Oct

/15

Mar

/16

Aug

/16

Jan/

17Ju

n/17

Sensex 1Y…

Mean: 16

+1 SD

-1 SD

FIXED INCOME MARKET

Global rates snapshot for August 2017

• With geo-political tensions rising between US and North Korea, US bond yields have inched down by 17bps during the month –continued to remain soft since the start of the year.

• Similarly, yields inched down across other developed markets too (baring Spain).

Source: Bloomberg, SBIMF Research

10 Year G-sec Yield (% month end) 2015 end 2016 end May-17 Jun-17 Jul-17 Aug-17 3m Change (in

bps)% change in 2017 YTD

(in bps)

Developed market

US 2.27 2.44 2.20 2.30 2.29 2.12 -9 -33

Germany 0.63 0.21 0.30 0.47 0.54 0.36 6 15

Italy 1.35 1.82 1.91 1.87 1.80 1.75 -16 -6

Japan 0.27 0.05 0.05 0.09 0.08 0.01 -4 -4

Spain 1.77 1.38 1.55 1.54 1.50 1.56 1 18

Switzerland -0.06 -0.19 -0.17 -0.02 0.05 -0.14 3 5

UK 1.96 1.24 1.05 1.26 1.23 1.03 -1 -21

Emerging Market Bond yields- August 2017

Source: Bloomberg, SBIMF Research

Bond yields majorly fell in the Emerging markets. China and Korea depicted the rise in bond yields while bond yields fell or remained same for other key EMs YTD

10 Year Gsec Yield (% mth end) 2015 end 2016 end May-17 Jun-17 Jul-17 Aug-17 3m Change

(in bps)% change in 2017 YTD

(in bps)

Emerging Market

Brazil 16.5 11.4 10.7 10.5 10.0 10.0 -72 -143

China 2.8 3.0 3.6 3.6 3.62 3.66 2 62

India 7.8 6.5 6.7 6.5 6.47 6.53 -14 1

Indonesia 8.7 7.9 6.9 6.8 6.92 6.67 -27 -125

Korea 2.1 2.1 2.2 2.2 2.23 2.27 3 19

Malaysia 4.2 4.2 3.9 3.9 3.99 3.89 1 -30

Philippines 3.9 4.6 4.7 4.7 4.65 4.65 -2 2

Russia 9.6 8.4 7.6 7.7 7.81 7.75 14 -61

South Africa 9.8 8.9 8.6 8.8 8.62 8.56 -2 -35

Taiwan 1.0 1.2 1.0 1.1 1.08 1.04 2 -17

Thailand 2.5 2.6 2.6 2.5 2.43 2.32 -31 -33

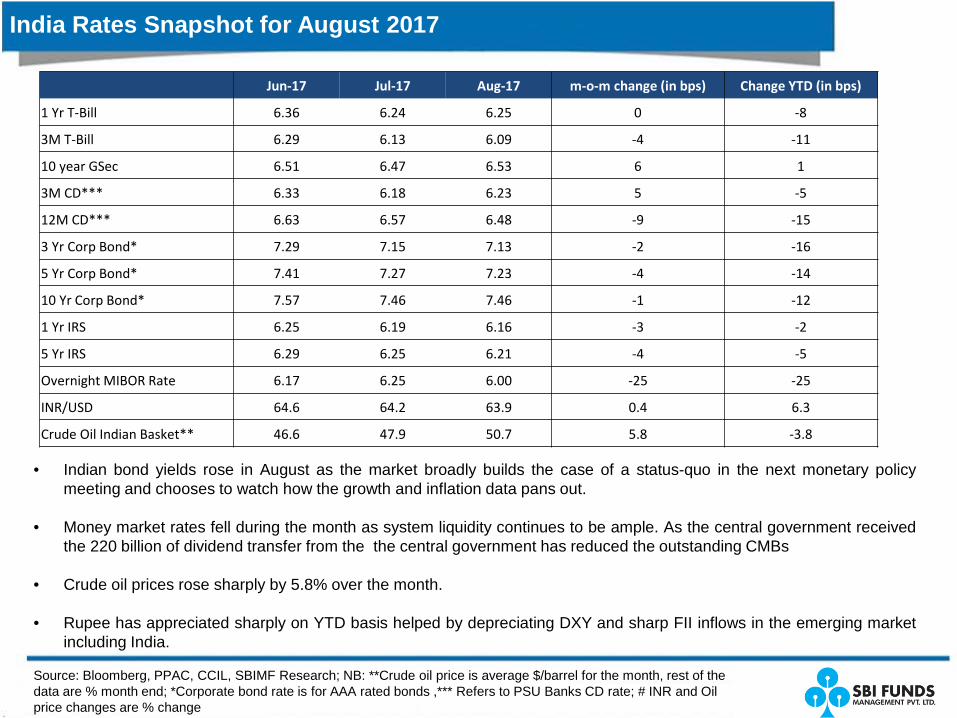

India Rates Snapshot for August 2017

• Indian bond yields rose in August as the market broadly builds the case of a status-quo in the next monetary policymeeting and chooses to watch how the growth and inflation data pans out.

• Money market rates fell during the month as system liquidity continues to be ample. As the central government receivedthe 220 billion of dividend transfer from the the central government has reduced the outstanding CMBs

• Crude oil prices rose sharply by 5.8% over the month.

• Rupee has appreciated sharply on YTD basis helped by depreciating DXY and sharp FII inflows in the emerging marketincluding India.

Source: Bloomberg, PPAC, CCIL, SBIMF Research; NB: **Crude oil price is average $/barrel for the month, rest of the data are % month end; *Corporate bond rate is for AAA rated bonds ,*** Refers to PSU Banks CD rate; # INR and Oil price changes are % change

Jun-17 Jul-17 Aug-17 m-o-m change (in bps) Change YTD (in bps)

1 Yr T-Bill 6.36 6.24 6.25 0 -8

3M T-Bill 6.29 6.13 6.09 -4 -11

10 year GSec 6.51 6.47 6.53 6 1

3M CD*** 6.33 6.18 6.23 5 -5

12M CD*** 6.63 6.57 6.48 -9 -15

3 Yr Corp Bond* 7.29 7.15 7.13 -2 -16

5 Yr Corp Bond* 7.41 7.27 7.23 -4 -14

10 Yr Corp Bond* 7.57 7.46 7.46 -1 -12

1 Yr IRS 6.25 6.19 6.16 -3 -2

5 Yr IRS 6.29 6.25 6.21 -4 -5

Overnight MIBOR Rate 6.17 6.25 6.00 -25 -25

INR/USD 64.6 64.2 63.9 0.4 6.3

Crude Oil Indian Basket** 46.6 47.9 50.7 5.8 -3.8

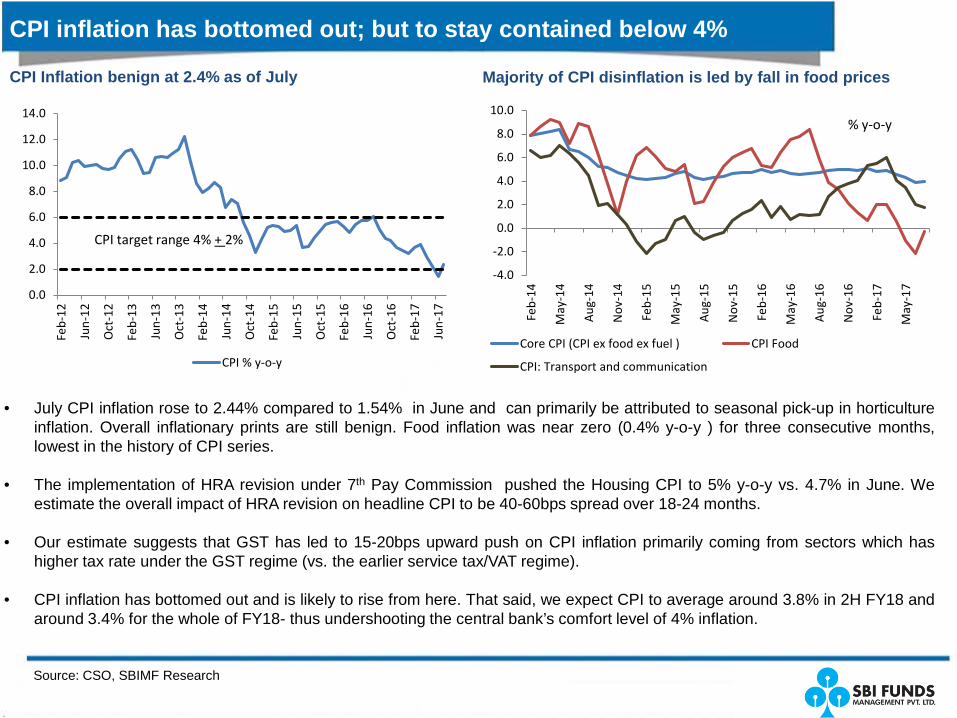

CPI inflation has bottomed out; but to stay contained below 4%

Source: CSO, SBIMF Research

• July CPI inflation rose to 2.44% compared to 1.54% in June and can primarily be attributed to seasonal pick-up in horticultureinflation. Overall inflationary prints are still benign. Food inflation was near zero (0.4% y-o-y ) for three consecutive months,lowest in the history of CPI series.

• The implementation of HRA revision under 7th Pay Commission pushed the Housing CPI to 5% y-o-y vs. 4.7% in June. Weestimate the overall impact of HRA revision on headline CPI to be 40-60bps spread over 18-24 months.

• Our estimate suggests that GST has led to 15-20bps upward push on CPI inflation primarily coming from sectors which hashigher tax rate under the GST regime (vs. the earlier service tax/VAT regime).

• CPI inflation has bottomed out and is likely to rise from here. That said, we expect CPI to average around 3.8% in 2H FY18 andaround 3.4% for the whole of FY18- thus undershooting the central bank’s comfort level of 4% inflation.

CPI Inflation benign at 2.4% as of July Majority of CPI disinflation is led by fall in food prices

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

Feb-

14

May

-14

Aug

-14

Nov

-14

Feb-

15

May

-15

Aug

-15

Nov

-15

Feb-

16

May

-16

Aug

-16

Nov

-16

Feb-

17

May

-17

Core CPI (CPI ex food ex fuel ) CPI Food

CPI: Transport and communication

% y-o-y

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Feb-

12

Jun-

12

Oct

-12

Feb-

13

Jun-

13

Oct

-13

Feb-

14

Jun-

14

Oct

-14

Feb-

15

Jun-

15

Oct

-15

Feb-

16

Jun-

16

Oct

-16

Feb-

17

Jun-

17

CPI % y-o-y

CPI target range 4% + 2%

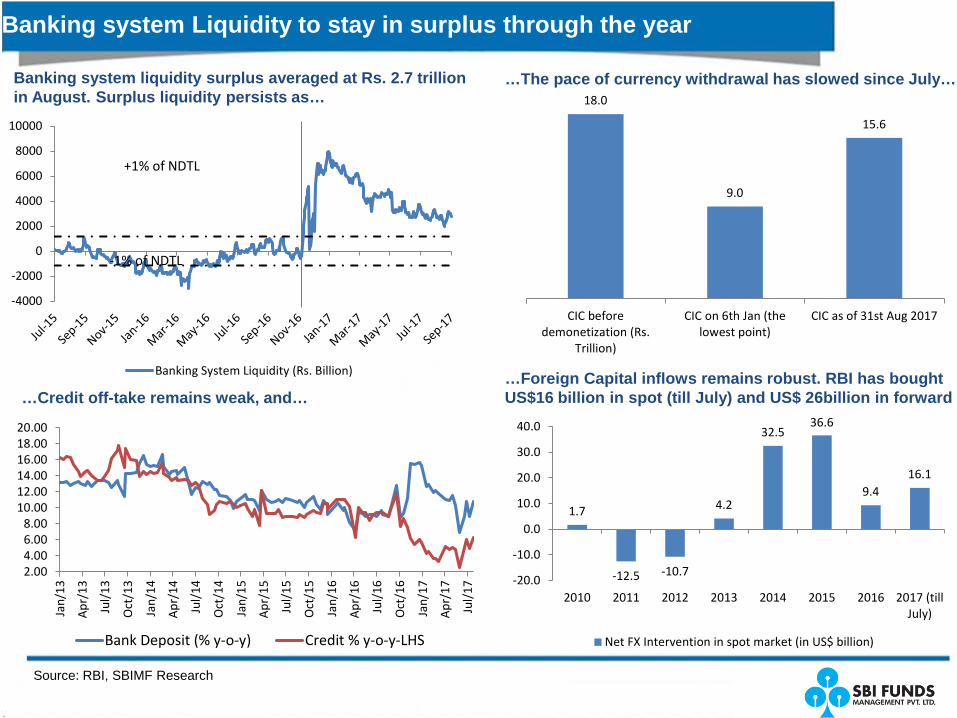

Banking system Liquidity to stay in surplus through the year

Source: RBI, SBIMF Research

Banking system liquidity surplus averaged at Rs. 2.7 trillion in August. Surplus liquidity persists as…

…The pace of currency withdrawal has slowed since July…

-4000

-2000

0

2000

4000

6000

8000

10000

Banking System Liquidity (Rs. Billion)

+1% of NDTL

-1% of NDTL

18.0

9.0

15.6

CIC beforedemonetization (Rs.

Trillion)

CIC on 6th Jan (thelowest point)

CIC as of 31st Aug 2017

2.004.006.008.00

10.0012.0014.0016.0018.0020.00

Jan/

13

Apr

/13

Jul/

13

Oct

/13

Jan/

14

Apr

/14

Jul/

14

Oct

/14

Jan/

15

Apr

/15

Jul/

15

Oct

/15

Jan/

16

Apr

/16

Jul/

16

Oct

/16

Jan/

17

Apr

/17

Jul/

17

Bank Deposit (% y-o-y) Credit % y-o-y-LHS

…Credit off-take remains weak, and…

1.7

-12.5 -10.7

4.2

32.536.6

9.416.1

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

2010 2011 2012 2013 2014 2015 2016 2017 (tillJuly)

Net FX Intervention in spot market (in US$ billion)

…Foreign Capital inflows remains robust. RBI has bought US$16 billion in spot (till July) and US$ 26billion in forward

Source: Bloomberg, SBIMF Research,

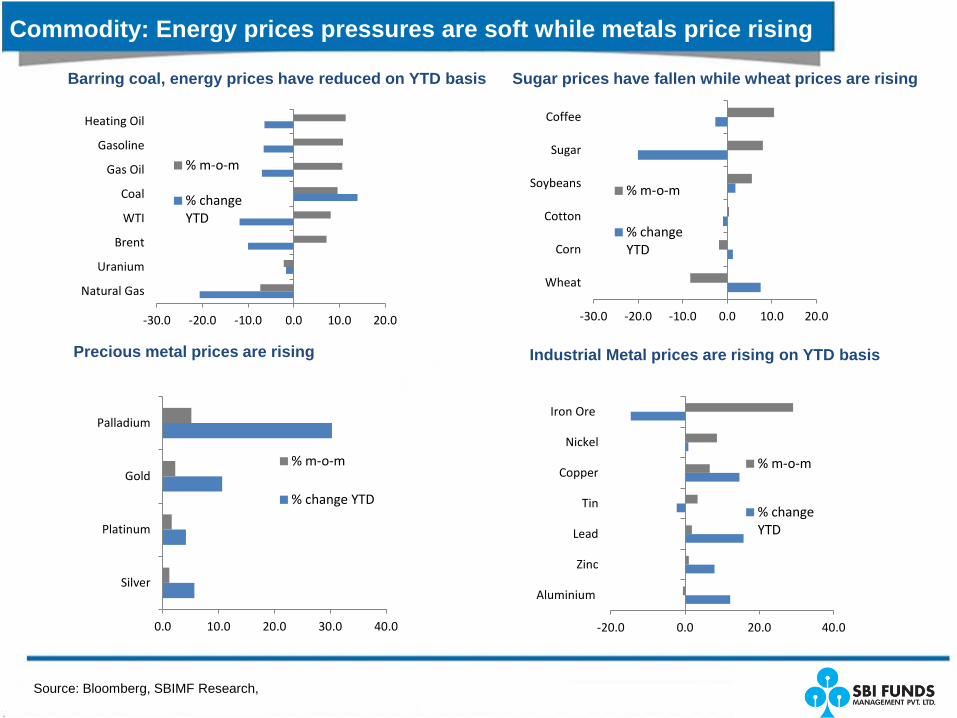

Commodity: Energy prices pressures are soft while metals price rising

Barring coal, energy prices have reduced on YTD basis

Precious metal prices are rising Industrial Metal prices are rising on YTD basis

-30.0 -20.0 -10.0 0.0 10.0 20.0

Natural Gas

Uranium

Brent

WTI

Coal

Gas Oil

Gasoline

Heating Oil

% m-o-m

% changeYTD

-30.0 -20.0 -10.0 0.0 10.0 20.0

Wheat

Corn

Cotton

Soybeans

Sugar

Coffee

% m-o-m

% changeYTD

0.0 10.0 20.0 30.0 40.0

Silver

Platinum

Gold

Palladium

% m-o-m

% change YTD

-20.0 0.0 20.0 40.0

Aluminium

Zinc

Lead

Tin

Copper

Nickel

Iron Ore

% m-o-m

% changeYTD

Sugar prices have fallen while wheat prices are rising

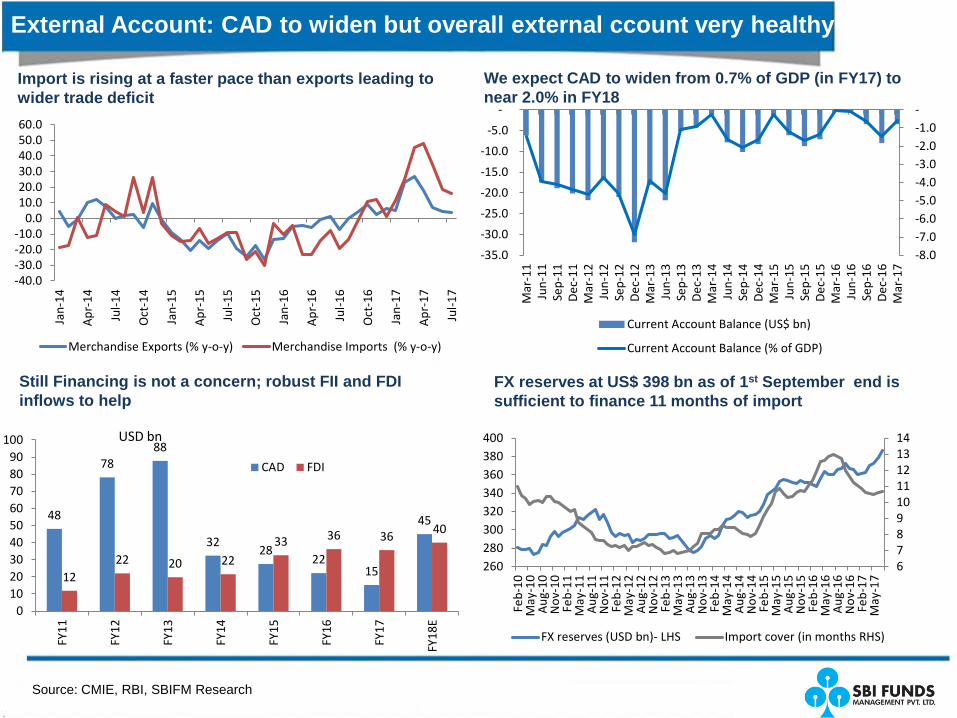

External Account: CAD to widen but overall external ccount very healthy

Import is rising at a faster pace than exports leading to wider trade deficit

Source: CMIE, RBI, SBIFM Research

We expect CAD to widen from 0.7% of GDP (in FY17) to near 2.0% in FY18

Still Financing is not a concern; robust FII and FDI inflows to help

FX reserves at US$ 398 bn as of 1st September end is sufficient to finance 11 months of import

67891011121314

260280300320340360380400

Feb-

10M

ay-1

0A

ug-1

0N

ov-1

0Fe

b-11

May

-11

Aug

-11

Nov

-11

Feb-

12M

ay-1

2A

ug-1

2N

ov-1

2Fe

b-13

May

-13

Aug

-13

Nov

-13

Feb-

14M

ay-1

4A

ug-1

4N

ov-1

4Fe

b-15

May

-15

Aug

-15

Nov

-15

Feb-

16M

ay-1

6A

ug-1

6N

ov-1

6Fe

b-17

May

-17

FX reserves (USD bn)- LHS Import cover (in months RHS)

-40.0-30.0-20.0-10.0

0.010.020.030.040.050.060.0

Jan-

14

Apr

-14

Jul-1

4

Oct

-14

Jan-

15

Apr

-15

Jul-1

5

Oct

-15

Jan-

16

Apr

-16

Jul-1

6

Oct

-16

Jan-

17

Apr

-17

Jul-1

7

Merchandise Exports (% y-o-y) Merchandise Imports (% y-o-y)

-8.0 -7.0 -6.0 -5.0 -4.0 -3.0 -2.0 -1.0 -

-35.0

-30.0

-25.0

-20.0

-15.0

-10.0

-5.0

-

Mar

-11

Jun-

11Se

p-11

Dec

-11

Mar

-12

Jun-

12Se

p-12

Dec

-12

Mar

-13

Jun-

13Se

p-13

Dec

-13

Mar

-14

Jun-

14Se

p-14

Dec

-14

Mar

-15

Jun-

15Se

p-15

Dec

-15

Mar

-16

Jun-

16Se

p-16

Dec

-16

Mar

-17

Current Account Balance (US$ bn)

Current Account Balance (% of GDP)

48

7888

3228

2215

45

1222 20 22

33 36 36 40

0102030405060708090

100

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

E

CAD FDI

USD bn

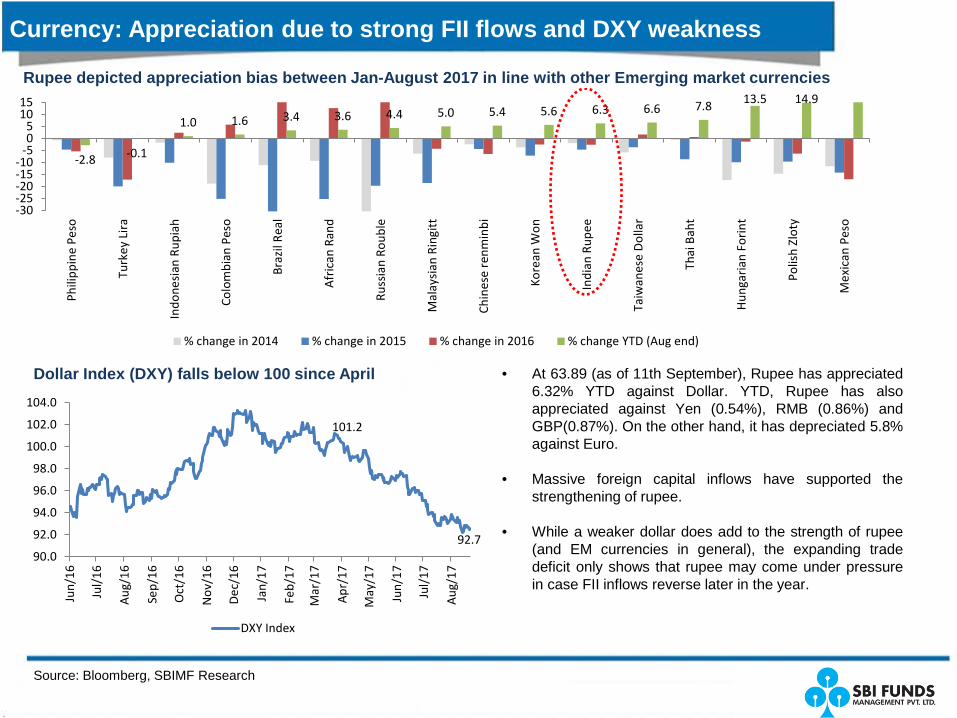

Rupee depicted appreciation bias between Jan-August 2017 in line with other Emerging market currencies

Currency: Appreciation due to strong FII flows and DXY weakness

Source: Bloomberg, SBIMF Research

Dollar Index (DXY) falls below 100 since April • At 63.89 (as of 11th September), Rupee has appreciated6.32% YTD against Dollar. YTD, Rupee has alsoappreciated against Yen (0.54%), RMB (0.86%) andGBP(0.87%). On the other hand, it has depreciated 5.8%against Euro.

• Massive foreign capital inflows have supported thestrengthening of rupee.

• While a weaker dollar does add to the strength of rupee(and EM currencies in general), the expanding tradedeficit only shows that rupee may come under pressurein case FII inflows reverse later in the year.

101.2

92.790.0

92.0

94.0

96.0

98.0

100.0

102.0

104.0

Jun/

16

Jul/

16

Aug

/16

Sep/

16

Oct

/16

Nov

/16

Dec

/16

Jan/

17

Feb/

17

Mar

/17

Apr

/17

May

/17

Jun/

17

Jul/

17

Aug

/17

DXY Index

-2.8 -0.1

1.0 1.6 3.4 3.6 4.4 5.0 5.4 5.6 6.3 6.6 7.8 13.5 14.9

-30-25-20-15-10

-505

1015

Phili

ppin

e Pe

so

Turk

ey L

ira

Indo

nesi

an R

upia

h

Colo

mbi

an P

eso

Braz

il Re

al

Afr

ican

Ran

d

Russ

ian

Roub

le

Mal

aysi

an R

ingi

tt

Chin

ese

renm

inbi

Kore

an W

on

Indi

an R

upee

Taiw

anes

e D

olla

r

Thai

Bah

t

Hun

gari

an F

orin

t

Polis

h Zl

oty

Mex

ican

Pes

o

% change in 2014 % change in 2015 % change in 2016 % change YTD (Aug end)

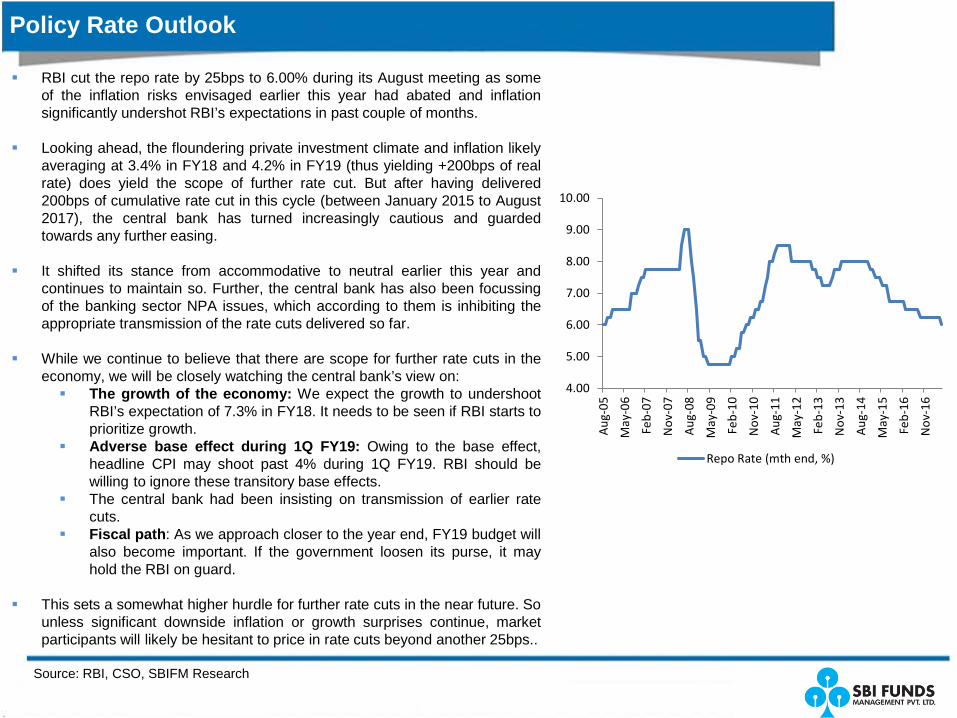

RBI cut the repo rate by 25bps to 6.00% during its August meeting as someof the inflation risks envisaged earlier this year had abated and inflationsignificantly undershot RBI’s expectations in past couple of months.

Looking ahead, the floundering private investment climate and inflation likelyaveraging at 3.4% in FY18 and 4.2% in FY19 (thus yielding +200bps of realrate) does yield the scope of further rate cut. But after having delivered200bps of cumulative rate cut in this cycle (between January 2015 to August2017), the central bank has turned increasingly cautious and guardedtowards any further easing.

It shifted its stance from accommodative to neutral earlier this year andcontinues to maintain so. Further, the central bank has also been focussingof the banking sector NPA issues, which according to them is inhibiting theappropriate transmission of the rate cuts delivered so far.

While we continue to believe that there are scope for further rate cuts in theeconomy, we will be closely watching the central bank’s view on: The growth of the economy: We expect the growth to undershoot

RBI’s expectation of 7.3% in FY18. It needs to be seen if RBI starts toprioritize growth.

Adverse base effect during 1Q FY19: Owing to the base effect,headline CPI may shoot past 4% during 1Q FY19. RBI should bewilling to ignore these transitory base effects.

The central bank had been insisting on transmission of earlier ratecuts.

Fiscal path: As we approach closer to the year end, FY19 budget willalso become important. If the government loosen its purse, it mayhold the RBI on guard.

This sets a somewhat higher hurdle for further rate cuts in the near future. Sounless significant downside inflation or growth surprises continue, marketparticipants will likely be hesitant to price in rate cuts beyond another 25bps..

Policy Rate Outlook

Source: RBI, CSO, SBIFM Research

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Aug

-05

May

-06

Feb-

07

Nov

-07

Aug

-08

May

-09

Feb-

10

Nov

-10

Aug

-11

May

-12

Feb-

13

Nov

-13

Aug

-14

May

-15

Feb-

16

Nov

-16

Repo Rate (mth end, %)

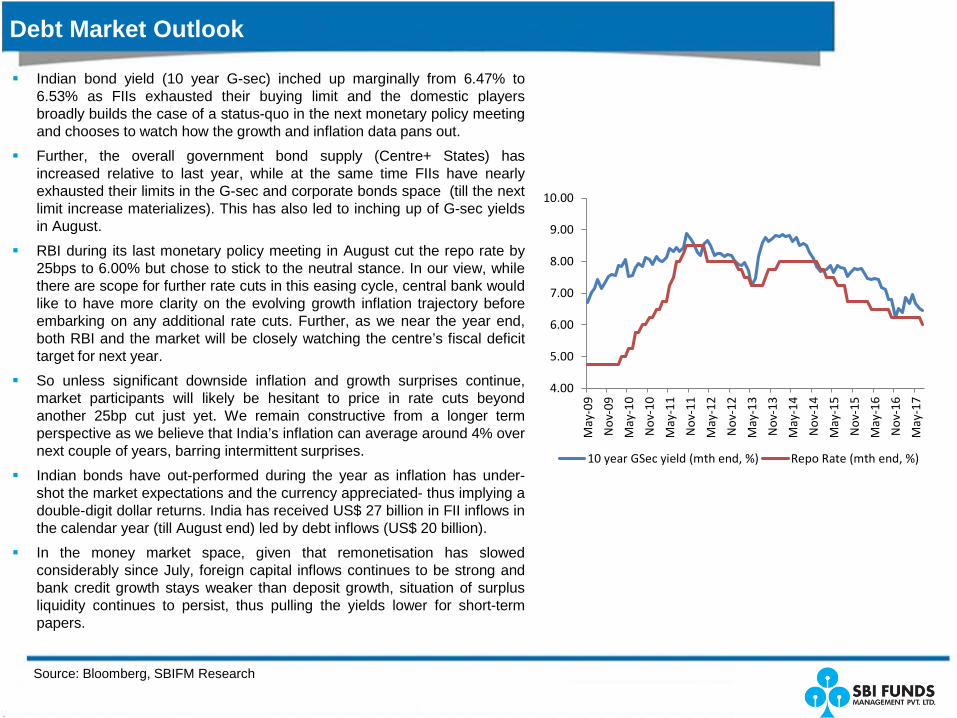

Indian bond yield (10 year G-sec) inched up marginally from 6.47% to6.53% as FIIs exhausted their buying limit and the domestic playersbroadly builds the case of a status-quo in the next monetary policy meetingand chooses to watch how the growth and inflation data pans out.

Further, the overall government bond supply (Centre+ States) hasincreased relative to last year, while at the same time FIIs have nearlyexhausted their limits in the G-sec and corporate bonds space (till the nextlimit increase materializes). This has also led to inching up of G-sec yieldsin August.

RBI during its last monetary policy meeting in August cut the repo rate by25bps to 6.00% but chose to stick to the neutral stance. In our view, whilethere are scope for further rate cuts in this easing cycle, central bank wouldlike to have more clarity on the evolving growth inflation trajectory beforeembarking on any additional rate cuts. Further, as we near the year end,both RBI and the market will be closely watching the centre’s fiscal deficittarget for next year.

So unless significant downside inflation and growth surprises continue,market participants will likely be hesitant to price in rate cuts beyondanother 25bp cut just yet. We remain constructive from a longer termperspective as we believe that India’s inflation can average around 4% overnext couple of years, barring intermittent surprises.

Indian bonds have out-performed during the year as inflation has under-shot the market expectations and the currency appreciated- thus implying adouble-digit dollar returns. India has received US$ 27 billion in FII inflows inthe calendar year (till August end) led by debt inflows (US$ 20 billion).

In the money market space, given that remonetisation has slowedconsiderably since July, foreign capital inflows continues to be strong andbank credit growth stays weaker than deposit growth, situation of surplusliquidity continues to persist, thus pulling the yields lower for short-termpapers.

Debt Market Outlook

Source: Bloomberg, SBIFM Research

4.00

5.00

6.00

7.00

8.00

9.00

10.00

May

-09

Nov

-09

May

-10

Nov

-10

May

-11

Nov

-11

May

-12

Nov

-12

May

-13

Nov

-13

May

-14

Nov

-14

May

-15

Nov

-15

May

-16

Nov

-16

May

-17

10 year GSec yield (mth end, %) Repo Rate (mth end, %)

Thank you

Disclaimer

This presentation is for information purposes only and is not an offer to sell or a solicitation to buy anymutual fund units/securities. These views alone are not sufficient and should not be used for thedevelopment or implementation of an investment strategy. It should not be construed as investmentadvice to any party. All opinions and estimates included here constitute our view as of this date and aresubject to change without notice. Neither SBI Funds Management Private Limited, nor any personconnected with it, accepts any liability arising from the use of this information. The recipient of thismaterial should rely on their investigations and take their own professional advice.

Mutual Funds investments are subject to market risks, read all scheme related documentscarefully.

Asset Management Company: SBI Funds Management Private Limited (A joint venture with SBI andAMUNDI). Trustee Company: SBI Mutual Fund Trustee Company Private Limited.

Contact Details

SBI Funds Management Private Limited

(A joint venture between SBI and AMUNDI)

Corporate Office:9th Floor, Crescenzo, C-38 & 39, G Block,Bandra Kurla Complex,Bandra (East), Mumbai - 400 051Tel: +91 22 6179 3000Fax: +91 22 6742 5687/88/89/90/91Website: www.sbimf.com

Call: 1800 425 5425

Visit us @ www.youtube.com/user/sbimutualfund

SMS: “SBIMF” to 56161

Email: [email protected]

Visit us @ www.facebook.com/SBIMF