market study of digital financial services in india...

TRANSCRIPT

0

Market Study of Digital Financial Services in

India - Summary Report Study by Amarante Consulting

Sponsored by Amdocs

June 2014

1

Preface

This report provides an objective assessment on the current status of Digital

Financial Services (DFS) in India, future insights into the development of the

industry and market conclusions based on global best practices.

Amarante Consulting, a boutique firm specializing in DFS across emerging

markets has produced this report in partnership with Amdocs, a provider of

customer care, billing and order management systems for telecommunications

carriers and internet services providers.

www.amaranteconsulting.com www.amdocs.com

2

Acknowledgements

We would like to thank all the people who took out time for us during this study.

Their immense support and contributions is much appreciated, without which

compiling this report would not have been possible.

Our interview list spans across the following sectors* :

– Government and National Organisations

– Mobile Network Operators

– Commercial Banks

– Microfinance Institutions and Foundations

– Business Correspondent Entities

– Mobile Wallet Providers

– Prepaid Card Providers

– Other Innovative Technology Start-ups

This report is destined for a limited publication and is being emailed directly to

the intended readers with whom we interacted during the study.

*In the interest of keeping anonymity requested by some interviewees, this report does not make reference to any particular

individual or organization encountered during the study.

3

Methodology

This report analyzes the Digital Financial Services (DFS) landscape and related

opportunities in the Indian sub-continent, compiled through research and

analysis involving:

- Desktop studies

- Phone interviews

- On-field visits to key implementation sites and meetings with key

stakeholders

- In-house knowledge on global DFS best practices, challenges and

opportunities

- Observation of customer and agent journeys and distribution and overall

ecosystem dynamics

4

Report contents

Snapshot of the market context for Digital Financial Services in India

Snapshot of the regulatory environment

Opportunity for Digital Financial Services in the country

Business models, uses cases and customer profiles

Conclusions

Some Digital Financial Services industry best practices & examples

Snapshot of the market context for Digital

Financial Services in India

6

India’s population is over 1.2 billion; 60% of whom are under-banked, whilst 75% have mobile

phone access. Around 67% of payments are still made in cash. Card penetration (debit and credit)

is less than 10% and sending money through informal and expensive channels e.g. hawalas is

commonplace. Given this context, the country presents a huge opportunity to tackle financial

inclusion through the adoption of innovative digital financial services.

For a while now, the government has initiated a crackdown on cash, encouraging the use of digital

payments, and especially mobile, as a cost effective, secure and reliable channel.

Since the enactment of mobile banking regulation in 2008, mobile payments have scaled

significantly. The acceleration of mobile transactions has been attributed to the introduction of

IMPS (Immediate Payments Service) in 2010 which allows for interoperability between banks and

Mobile Network Operators. In 2013, RBI registered 20 million users for financial transactions over

the mobile and 1,194 million in transaction volumes.

By 2020, it is estimated that the mobile will have the potential to serve 250 million people for

financial services in India. However, there is still a long way to go and a number of challenges to

overcome. These largely pertain to the regulatory environment, service proposition, customer

awareness, ecosystem dynamics and agent network management.

This report presents a snapshot of the current digital financial industry in the country and also

provides examples of global industry best practices that players can benefit from.

Context

7

India: Overview

Total population: 1.2 billion

‐ 70% rural population

‐ 30% urban population

‐ 69% under poverty line

‐ 60% below 25 years

$3,910 GNI/Capita

73% literacy rate (35% women)

40% access to financial services

11.38 commercial bank branches / 11.21

ATMs per 100,000 habitants

12 MNOs (10 private players representing

88% of the sector)

‐ 75% mobile penetration

‐ 900 million mobile connections

200 banks with 65 banks licenced for mobile

banking and 59 banks live

14 MFS Solutions (excluding mobile banking

solutions)

Source: World CIA Factbook, Global Findex 2012 , GSMA, TRAI, CGAP, World Bank – 2012, 2013

8

Business is currently driven by complex array of factors/players

Regulation

Regulatory framework

drives what is permissible

and possible in terms of

players and products these

players offer in a given

market.

Payment Instruments

Cash

Linked

bank account

Pre-paid

card

Channels/Access Points

Integration of retail agents with existing financial

infrastructures (ATMs /POS) leads to more rapid uptake

Retail

Outlet Phones ATM

E-Payments

Platform/Switch

Initial single entity-led models being replaced by joint

ventures and collaborations across players

PSP MNO Bank

POS Online

Service Providers

Mobile account

Debit card

Credit card

The payment industry in India is very mature with a multitude of payment instruments available…

…However, while there are wide options for transactions and fungibility of channels for the urban

banked, the unbanked and rural populations often have access to one channel (mostly cash), if at all.

9

Progression of payment initiatives and digital channels in the country

2006: Business Correspondent

Banking, a network “accredited”

by banks to engage individuals,

and for-profit or non-profit

organisations as banking agents

for the performance of some of

the core banking functions

2010: The Immediate Mobile

Payment Service (IMPS), an

instant interbank electronic fund

transfer service allowing bank

transfers to be instructed on

mobile phones

2012: White Label ATMs (WL-

ATMs) offered by non-bank

entities who recognise that

investments in ATMs can be

leveraged for delivery of a wide

variety to customers and

expanded the scope of banking

to anytime, anywhere banking

through interoperable platforms

Electronic Payment

Processing

2004: The Real Time Gross

Settlement (RTGS) system

which is similar to NEFT but

operates in real-time on a

transaction to transaction

basis and is primarily meant

for large value transactions. In

2013, RTGS system and

regulations updated

2005: The National Electronic

Funds Transfer (NEFT)

payment system to facilitate

(in a batch-mode with netting)

one-to-one funds transfer from

an account in any bank

branch to an account in any

other bank branch in the

country.

2012: The National Electronic

Clearing Service (NECS) to

facilitate centralised

processing for repetitive and

bulk payment instructions

Prepaid Payment Instruments

& Mobile Money

Internet & Mobile

Banking

Branchless Banking &

White Label ATMs

2009: Prepaid Payments

Instruments (PPIs), a

payments system for the

issuance and operations of

prepaid Instruments that

can be issued by licensed

banks and non-banks

2009: Mobile Money: A

system permitting banks

and non banks to offer

services to their customer

over mobile phones

1996: Internet Banking,

offered primarily by

banks for customers to

access their accounts

and make transactions

over the net

2008: Mobile Banking

RBI published Mobile

Banking regulations

where banks could use

the mobile as a channel

for existing customers.

Back office electronic systems

for transaction processing

Non banks entering payments market & New payment channels emerging

and maturing

Expansion of channels,

including mobile

10

Started in: February 2009 under United Identification Authority of India (Government Department)

Purpose: Provide every Indian resident a digital ID (from toddler to senior citizens)

Method: Fingerprint and Iris scan identification along with a 12 digit number

Goal: All residents of India to be enrolled by 2016

Status so far: 650 Million people enrolled, many of them low income, street kids etc. 1 Million people

being enrolled a day

Enables:

‐ An individual to have an ID proof

‐ Signing up for a bank account while enrolling

‐ Linking 12 digit Aadhaar number to an existing bank account

‐ E-KYC

Role of mobile phone:

‐ Optional field in Aadhaar enrollment form

‐ Used by Aadhaar to communicate with Aadhaar card holder

Population reaction: Though take-up is good, petition is being fought in Supreme Court

The Government is focusing on getting everyone connected

through enrollment for a digital ID called Aadhaar

RBI and Money Laundering

Act declare Aadhaar

sufficient for KYC

Aadhaar is a 12 digit individual identification number issued by the Unique Identification

Authority of India to serve as a proof of identity and address, for any one residing in the country.

11

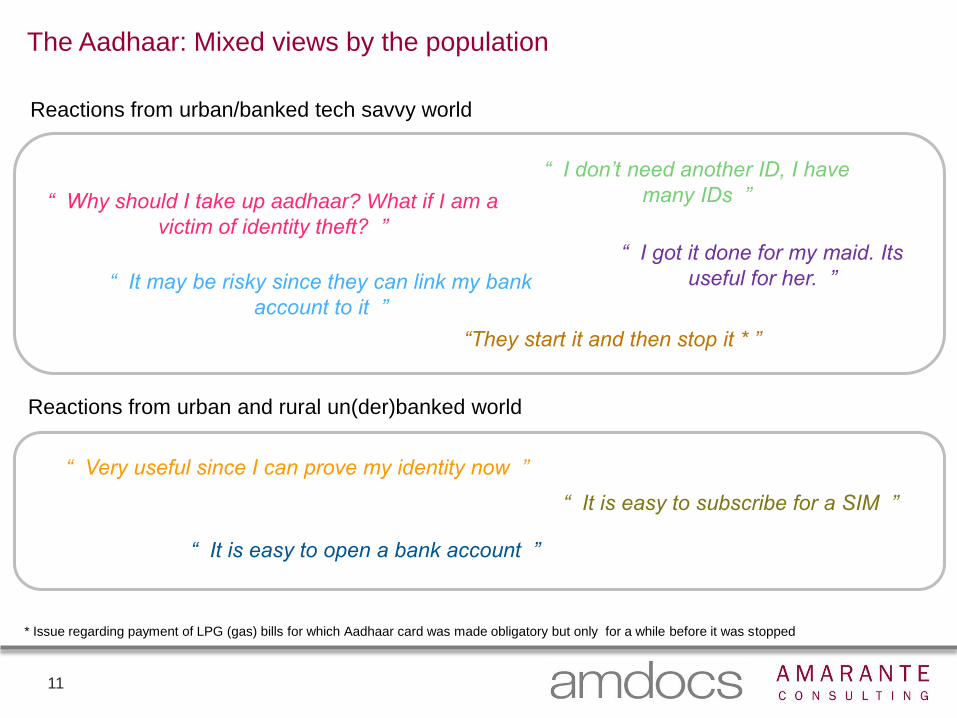

The Aadhaar: Mixed views by the population

“ Why should I take up aadhaar? What if I am a

victim of identity theft? ”

Reactions from urban/banked tech savvy world

“ It may be risky since they can link my bank

account to it ”

“ I don’t need another ID, I have

many IDs ”

“ I got it done for my maid. Its

useful for her. ”

Reactions from urban and rural un(der)banked world

“ Very useful since I can prove my identity now ”

“They start it and then stop it * ”

* Issue regarding payment of LPG (gas) bills for which Aadhaar card was made obligatory but only for a while before it was stopped

“ It is easy to open a bank account ”

“ It is easy to subscribe for a SIM ”

12

Aadhaar and Digital Financial Services

• Using a unified national identity system, such as Aadhaar, for KYC, assures

regulators and all stakeholders that the service provider is dealing with the

legitimate holder of an account.

• The Aadhaar Enabled Payment System allows Aadhaar card holder to carry out

financial transactions on a micro ATM terminal at a Business Correspondent.

• The Aadhaar number along with an individuals mobile number and an electronic

bank account number can revolutionize the way people access and transact

with financial products and services

• Aadhaar has the potential to become the universal linkage for disbursing

government payments in a more secure, streamlined, efficient and cost

effective way

• Deployment of Aadhaar-compliant biometric fingerprint devices at hundreds of

thousands of agents can be a costly and complex proposition,. This can make

it challenging for the system to be adopted quickly and on a large-scale.

Implications for

Aadhaar for DFS

Status of Aadhaar

(as of Q1 2014)

• As of March 2014, around 650 million people have been enrolled into the

Aadhaar program.

• Currently, the lead time between enrollment and card reception is less than two

months. Effort is being made to reduce this time to 30 days. (At worst of times, it

has taken a year to get the card to the people.)

13

A fragmented Digital Financial Services market: Examples of some providers

Telcos

Banks /

MFIs

Third

Parties

Snapshot of the regulatory environment

15

Regulatory environment – evolution of events

2011 2012 2014 so far 2006 - 2010

Mobile banking

regulations modified to

allow banks to facilitate

funds transfer both for

personal remittances

and purchase of goods

without any ceiling.

Banks free to decide on

the limits.

Small value transactions

fund transfers up to Rs.

5,000/- can be effected

through the mobile

phone without the need

for end-to-encryption.

Domestic Money

Transfer guidelines

issued

- Remittance from a bank

account and cash out for

unbanked beneficiary at

BC allowed (up to Rs.

10,000/- per transaction

subject to a monthly cap

of Rs.25,000)

BC status opened up

to include “for profit”

MNOs and mobile

payment providers as

well

BC interoperability

agreed, in principle

(no operational

guidelines yet)

MNOs can provide

prepaid instruments

and licensed as PPIs

TRAI set a ceiling

price for outgoing

USSD-based mobile

banking service:

INR 1.50 per

session

RBI allows non bank

holders to withdraw

funds received from

bank account

holders, through

ATMs

Licensing of non

financial institutions

as commercial

banks (lead time of

18 months to prove

readiness.)

2006: RBI allows banks to expand

beyond bank branches through

non profit BCs (but within 15 km

radius of branch)

2008: Mobile banking regulation

published

2009:

- E-money regulation published

- Prepaid instruments (PPI) license

introduced

‐ ‘For profits’ allowed to be

appointed as business

correspondents and can apply

fees

‐ Branch – BC radius increased to

30 km

‐ Transaction limit raised to Rs. 50K

per customer per day for mobile

banking transactions

2010: NPCI created mobile micro

transaction switch and interbank

mobile payment services (IMPS)

allowing bank holders to remit to

other bank holders via mobile

2013

RBI authorizes fully

enabled electronic

KYC (e-KYC),

based on the

Unique ID initiative

“Aadhaar Card” as

a valid process for

KYC verification

under the RBI’s

Prevention of

Money Laundering

Rules

RBI sets up

Financial Inclusion

Committee

Setting the Stage Initial relaxation on

limits

Focus on

reach

Facilitation & Fin

Inclusion

Further opening up

of sector

Market hopeful for:

- Restrictions lifted on cash out for PPIs

- Authorization of a new type of player:

Payment Banks, although recent media

coverage has pointed to doubts about its

realization, now pending due to the

recent change in government

16

Key elements of regulation impacting DFS in India

Bank led

model

MNOs can be

BCs and PPIs

Banks liable

not BCs

Switch for m-

banking

Fixed tariff/

limits

“Payment

Banks”

expected

Aadhaar

based KYC

Mobile banking regulation formalized in October 2008 and e-money regulations were published in 2009

RBI reserves the right to authorize non financial institutions (MNOs/others) to work with banks to offer

services under the Payment and Settlement Act 2007 (any issuer wishing to offer MFS without a bank

needs to seek authorization directly from the RBI as stated in the Act)

For profits, including MNOs, can be Business Correspondents (BCs) and use their retail points as customer

service points (CSPs), managing delivery channels and applying service fees

MNOs, like other non financial institutions, can be licensed Prepaid Payment Instruments (PPIs) and offer

prepaid or stored wallet accounts but clients are not allowed to perform cash withdrawals and accounts

cannot earn interest.

Banks remain liable for all transactions done through BCs and CSPs

In 2014, RBI is expected to license a new market player, called ‘payment bank’ which PPIs can upgrade to.

This will lift current restrictions revolving bank liability, settlements, etc.

The Banks are responsible for KYC, AML and CFT and must meet any RBI charges for any breach.

However, KYC requirements are less sophisticated to open simple accounts and wallets.

Unique Identification Authority of India issued Aadhaar; a 12 digit individual identification number that will

facilitate access to banking and digital financial services through a more efficient KYC process

IMPS allows interoperability for mobile banking transactions between banks.

Standard fee of Rs 1.50 for outgoing USSD mobile banking transactions

Remittance from a bank account for cash out to a non bank account at an ATM/BC outlet up to Rs 10,000

per transaction subject to a monthly cap of Rs 25,000

Maximum limit of Rs.50 K on prepaid wallet accounts

17

Implications of regulations 1/2

Issues Possible Solutions

Legislation for BCs to be no more than 30

KMs far from a bank branch hinders the

expansion of financial services

3rd party agents cannot perform complete

account opening and are restricted to only

certain processes

Cumbersome KYC requirements make it

difficult to fully offer financial inclusion

products/service to the (un)der banked

Government regulation of charges and

fees e.g. mandating fixed tariffs

Remove restriction to expand financial

services Into rural areas and increase

availability of touch points

Pass greater control and decrease

dependency on banks whilst improving

fraud monitoring

Make KYC proportionate to the level of

customers and services required. KYC

process for SIM card registration should

be used to open a mobile money

account

Allow market based and competitive

pricing to incentivise investment in DFS

Source: Amarante Research, GSMA “Mobile Money, the opportunity for India” 2013

18

Issues Possible Solutions

.

Only banks are licensed deposit takers

and authorised to pay interest. Non banks

are forbidden to take deposits.

Non FIs can offer prepaid stored value

accounts but clients cannot perform cash

withdrawals from these accounts

Regulatory concerns around consumer

protection and customers losing money

Interbank interoperability exists but not for

wallet to wallet which requires a lengthy

pre approval procedure to be followed by

non Financial Institutions

Change rules on deposit taking to enable

mobile money providers to pay interest on

stored value accounts for un(der)banked

Allow cash out from mwallets provided by

non FIs to limit dependency on banks and

improve usability

Cash backing mobile money should

always be held in a regulated institution,

whatever market evolution takes place

IMPs should integrate wallet to wallet

interoperability to expand the DFS

ecosystem

Source: Amarante Research, GSMA “Mobile Money, the opportunity for India” 2013

Implications of regulations 2/2

Opportunity for Digital Financial Services in

the country

20

Overview

The Indian payments market is complex and represented by a diverse range of channels, cash,

prepaid/debit/credit cards, virtual and mobile accounts; which in turn has led to the formation of

partnerships in cross industry sectors. Yet the omni channels, are limited largely to the urban and

connected world, with less options available to the under served and unbanked, (especially in rural

areas) whom are often restricted to one channel. However, the advent of business correspondent

banking, which has resulted in the integration of retail agents within the existing financial services

infrastructure (ATMs and POS) aims to deepen financial access. Moreover, joint ventures and

collaborations amongst players to launch digital financial services is increasing to further maximize

the distribution of financial services to those currently restricted. Initially, the Reserve Bank of India

stated that only banks could offer the full breadth of DFS and any player entering the market must tie

up with a bank. However, non-banks licensed as Prepaid Payment Instruments (PPIs) can offer

money transfer services, but customers are prohibited from cash out. Thus, mobile network operators

and third parties have been limited in scope with the services they can provide, which has prompted

collaborations with banks, such as; the case with Vodafone and ICICI Bank, Airtel and Axis Bank.

However, if new regulation comes into force allowing these non banks to become payment banks,

they will have a greater role to play in payments’ and deposits’ activities.

Recently, the government has agreed to license a couple of non financial institutions as commercial

banks provided they go through a period of transformation, over 18 months, to be ready in

accordance with RBIs’ standards. Clearly, the government has played an instrumental role in

providing the framework for what is and is not permissible in terms of products and stakeholders. It

will be interesting to see how business models and the payments market at large will develop under

the new government in power.

21

Opportunity to increase access to financial services

India faces a major financial exclusion challenge:

‐ 60% of population lacks access to basic financial services

‐ 90 per cent of small businesses have no links with formal financial institutions

‐ ~ 67% of total payments are still made in cash

‐ Less than 10% credit and debit cards penetration

‐ ~ 20% of the unbanked avail credit from local lenders

‐ ~ 30% of the population have access to savings

‐ 100 million Indians have insurance cover

India has one fifth of the world’s young population, a large majority of whom are tech-savvy

Indian domestic remittances market is valued at Rs.630 Bn (10 Bn USD) but only 30% of migrants

(300 million migrant population) have bank accounts and many still remit money informally, e.g.

hawalas

Government benefits payment market is worth $55 billion (mostly transferred in cash to

beneficiaries; a costly and inefficient process)

Across regions, financial exclusion is more acute in Central, Eastern and North-Eastern regions

Source: CGAP, Yale School of Management “Mobile Banking in India: Barriers and Adoption Triggers”, 2013, The Hindu “Vodafone to take mpesa pan

india next year”, Dec 2013 , Reserve Bank of India, Nachiket More Report, 2013, Munich Re Foundation & GIZ, The Landscape of Microinsurance in

Asia and Oceania” published at the Conference, 2013.

22

Opportunity for financial inclusion and financial deepening

There is a wide disparity across

the nation. The six largest cities

in India have 11% of the country’s

bank branches. Meanwhile, the

50 poorest districts have 4,068

loan accounts per 100,000

people, compared with the

national average of 11,680.

These districts have just 3

branches per 100,000 people,

which is less than half the all-

India average of 7.6.

The Southern areas of the

country have higher levels of

financial inclusion in comparison

to the North

The South also has better credit

penetration, the number of loan

accounts per 100,000 of

population at 17,142 which is

nearly twice that of the all-India

average.

Source: Crisil, http://www.crisil.com/about-crisil/crisil-inclusix.html#findings, 2013

Financial inclusion and financial

deepening remain poorly developed

and uneven on a regional basis

23

Opportunity with regards to the youth segment

India has a fifth of the world’s young population

Youth are most likely to adopt smartphones and mobile applications driven by a demand to be

connected 24/7and the availability of low cost smartphones

- 5% of 16-18 years old owned smartphones in 2012 which jumped to 22% in 2013, a four fold

increase

- 92% of 21-35 year olds in urban areas use smartphones, and 44% use their phones more

than laptops or computers to access the internet

- Popular uses includes: social networking, mobile TV, banking, sports, news and emails

Educational institutes may collaborate with portal and mobility solutions to get more engagement

with students in both urban and rural areas.

Preference of Indian youth to have advanced phones has resulted in intense competitiveness

amongst manufacturers and this is being seen as an important engine of growth for the telecom

industry.

Source: Smartphone Incidence Study, Nielsen 2013, The Economist 2013, India Onward, July 2013, India On Demand, June 2013, Slums, Youth and the

Mobile Internet in Urban India 2012

24

Opportunity with regards to government payments

In India, the government benefits transfer market is worth $55 billion (mostly transferred in cash to

unbanked beneficiaries, a process that is costly and inefficient)

Branchless banking and mobile technology can make G2P payments more accessible while

simultaneously decreasing costs and increasing the efficiency of the payment process

G2P Payments on the mobile channel will reduce funding leakages, procedural delays and

corruption (transaction costs are likely to decrease from 12%-15% to 2%)

Aadhaar, the national digital identification system can provide the universal linkage for disbursing

government transfers and will ensure they reach the intended beneficiary in a secure manner

Customer service points of business correspondents can serve as delivery agents for G2P

Payments. They can use mobile phones and biometric devices to capture beneficiaries’ data and

authenticate payments

Source: CGAP, Yale School of Management “Mobile Banking in India: Barriers and Adoption Triggers”, 2013, The Hindu “Vodafone to take mpesa pan india

next year”, Dec 2013 and MicroSave, “What Will It Take To Deliver ‘Direct Benefits / Cash Transfer Programmes Successfully”, 2013

25

Opportunity with regards to credit, savings & insurance

Close to 90% of small businesses have no links with formal financial institutions and 60 % of the

rural and urban population do not have a bank account

Bank credit to GDP ratio in the country stands at 70%, but in large states such as; Bihar, it can be

as low as 16%. A large part of the economy is dependent on the informal sector for meeting its

credit needs.

Difficulties in accessing finance, and gaining a positive return on financial savings coupled with ill-

adapted financial products has led the un(der)banked to a move away from savings in formal

financial institutions to more unregulated and informal means.

Savings as a proportion to GDP has fallen from 36.8% in 2007-08 to 30.8% in 2011-12. The

financial savings of households have declined from 11.6% of GDP to 8%.

Micro-insurance can serve as a powerful safety net for the poor to protect against illness, death,

disability, property damage, catastrophes, weather and natural disasters. However, only 10% of the

population have some form of insurance in the country

RBI proposes that by 2016, each district would have a total deposits and investments to GDP ratio

of 15% and a total term life insurance sum assured to GDP ratio of at least 30%. Credit to GDP ratio

is aimed at about 10%.

Mobile and branchless banking can increase distribution of much needed credit, savings and

insurance products to low income households and businesses whilst reducing interest rates and

premiums

Source: RBI, Nachiket More Committee Report, 2013, Journal of Business Management & Social Sciences, Micro-Insurance in India Protecting the Poor,

2013

26

Average cost of a typical domestic remittance of

Rs.2,000 through a hawala is 4.6% of the transfer

amount, including formal fees and indirect costs,

such as paying a bribe or traveling to the nearest

payment outlet.

Sending and receiving money through India Post is

expensive: in addition to paying 5% of the total

transfer amount, 1% is spent in bribes, tips, and

other indirect costs

Banks offer the cheapest method for sending money

but are difficult to travel to, require high KYC and

take up a lot of time in travel and queuing

Mobile and branchless banking channels are

significantly less expensive, especially for lower

transaction values

Alternative channels to cash are not only more

affordable, (especially for low income providers) but

are secure, reliable and allow proximity payments,

saving customers time and money

Percentage costs per remitted amount per channel

Source: Centre Microfinance (IFMR Research), CGAP Blog, “How do migrant workers move money in India”, 2011

0

1

2

3

4

5

6

Bank Post Office HawalaCourier

CashCourier

Friends

1.5

5.5

3.8 3.2

1.5

0.5

0.8

0.2

0.3

IndirectCosts

% o

f R

em

itte

d a

mo

un

t

0

20

40

60

80

0 500 1000 1500 2000

Tra

nsa

ction

Fe

e (

INR

)

Transaction Size (INR)

Mobile Banking Branchless Banking

Note: Remittances through mobile and branchless banking channels has not fully

taken off and the market is quite fragmented in terms of service providers compared

to other domestic remittance markets. The information provided in the bottom graph

may not be wholly accurate as the total market share of remittances per service

provider is unavailable. For the purpose of the graph (bottom) tiered pricing has been

converted into single pricing.

Opportunity for domestic remittances

Business models, uses cases and

customer profiles

28

Central Bank Telecom Regulator

Business Correspondents

Customer Service Points

Branches

NPCI

Regulators

Mobile Network

Operators Service Providers

Banks/Financial

Institutions

Prepaid Payment

Instruments (PPIs)

Technology

Handset/Equipment

Manufacturers

mWallet Providers ATM/POS/Card

Networks

MNO recharge

stores

Other Customer facing

channels

Final customer facing

outlets

Traditional Customer

facing channel

Communication

Infrastructure

Providers

Snapshot of the Digital Money Ecosystem India

29

Banks/MFIs Telecom Operators* Third Parties*

Motivation • Fulfilling RBI

obligations

• Deposit

Mobilization

• Outreach

• Reducing churn

• Increasing

revenues

• Penetrating a new

market

• Good revenue

generating business

• Offer value

proposition to banks

who want outreach

• Build innovative

technology to make

business model

viable

Likely

partners

Required

partners

• Distribution

Network

• Banks/MFIs

• Technology

providers

• Banks/MFIs**

• Technology

providers

*These entities have a PPI license and usually have access to a distribution network **Largely due to Regulatory compulsion

• Technology

providers

Key Stakeholders

30

Banks/MFIs Telecom Operators Third Parties

Model

• Use Telco distribution,

communication infrastructure

and wallet platform to open

bank accounts

• Cash in possible at bank

accepted telco CSPs

• Cash out possible at

branch/ATM or at bank

accepted telco CSPs

Equipment

• Account opening: form filling

+ KYC doc collection

• Cash in/Cash out: Retailer’s

mobile phone with preloaded

menu/app

Model

• Use PSP distribution and

platform to open bank

accounts

• Cash in possible at bank

accepted BC CSPs

• Cash out possible at

branch/ATM or at bank

accepted BC CSPs

Equipment

• Account opening on the

computer with front end

interface that syncs to the

CBS + form filling + KYC doc

collection (sometimes e-kyc)

• Cash in/Cash out:

Computer/tablete/phone

and/or camera/phone camera

+ biometric device

Main Model for Digital Financial Services in the Country – Bank Led Model

31

Bank Account Based

Model

Open Loop Prepaid

Wallet Semi Closed Prepaid

Wallet

• Requires the client to have

a bank account

• Mobile/Digital channel can

be used to access and

transact from the bank

account

• Allows inter-bank transfers

and cash outs (though

some transaction limits

may apply)

• Examples:

• ICICI imobile or Axis

Bank’s mobile

banking application

• All banks that are

active via IMPS

• Provided by third party

players (MNOs, Distribution

networks,…) in liaison with

banks

• KYC must be performed

(max a/c limit INR 50 K)

• Cash out is allowed at

business correspondents of

the concerned banks

• This service may allow for

transactions across across

banks, merchants and billers

and uses of payment

processors like Visa and

MasterCard.

• Example:

• Airtel Money (Super

Account)

• A mobile wallet offering

where cash in is allowed

but cash out is prohibited

• Requires clients to have

concerned mobile

operator’s SIM

subscription

• Bank partner not needed

• Full KYC needed in order

to use the account for

remittance and payments

(max a/c limit INR 50 K)

• No KYC if wallet used only

for bill payments (max a/c

limit INR 10 K)

• Examples:

• Airtel Money

(Express and Power

Accounts)

There are currently three main types of account offering in Digital

Financial Services in India

32

Digital Financial Services Use Cases

Key drivers for mobile payments

‐ Availability of 3G/4G network

‐ Increasing mobile phone penetration

‐ Lack of access to formal financial services

‐ Demand from MNOs and banks to improve stickiness and revenues

‐ Cheaper channel to send and access money

‐ Government pushing for Financial Inclusion

Current Use Cases Future Potential Use Cases

1. Prepaid airtime top up

2. Utility payments (DSTV

recharge and utilities)

3. Remittances

4. Merchant Payments

1. Remittances

2. G2P Payments

3. Merchant and Utility Payments

4. Savings/deposits

5. B2B (MME/SME) payments

By 2015, mobile money transfers in India could total $350 billion annually

Financial inclusion, G2P payments and remittances are expected to be the biggest drivers for digital

money adoption

Merchant payments services are expected to grow as middle class and youth become more tech

savvy and the availability of adapted handsets increases at a more affordable cost.

Source: CGAP, Deloitte M-Banking & M-Payments: The Next Frontier, 2013, GSMA “Mobile Economy India” 2013, Amarante Consulting

33

Potential Customer Profiles: Primarily un(der)banked people 1/2

Migrant

workers

Around 500 M workers in India of which

94% in unorganized sector (2012).

The min wage as of 2011 = 115 Rs./ day

• Come in to the cities to find work

• Feel there are better opportunities in

the city

• Usually engaged on

manual/seasonal work

• Earn weekly, fortnightly, monthly

• Share lodging with many others

Need:

• A safe place to store/save

money

• Have money accessible

• Transfer money bank to

family in the villages

• May need loans etc., (but

MFI offerings usually target

micro entrepreneurs)

Source: http://en.wikipedia.org/wiki/Labour_in_India; http://en.wikipedia.org/wiki/2011_census_of_India; Amarante interviews

People in

the villages

Around 835 M people live in around 640

different villages. (census 2011)

• All age groups

• For income/ livelyhood, they depend

on:

• Agriculture, household

enterprises, small businesses

for revenue

• Remittances

• Government payments

Main expenditures:

• Household maintenance

• Electricity bill (home and

farm)

• Farm input: fertilizers,

grains, etc.

• Children school fees

Need:

• Access to formal finance

• Savings, loans, insurance

• …

34

Informal

retailers

Small scale shops, usually less that 500 sq

ft in size. 14M outlet in India of which only

4% are shops >500 sq ft (2010).

• Usually pay for their stock in cash

• Do not systematically use bank

accounts for their business (although

they may have one for savings)

• Many do not keep any registrars of

inventory to stock purchases and sales

• Usually work on revolving credit offered

by the wholesaler

• Cash at the end of the day it either

reinvested in stock or taken home for

expenses/savings

Potentially would like to:

• Encourage more foot traffic

• Have credit facility

• Have secure ways to conduct

payments

However:

• Would not like to pay for

having to use or provide a

service (e.g. paying for POS

transaction etc.)

• Would be motivated to help

their community

Source: http://en.wikipedia.org/wiki/Labour_in_India, http://en.wikipedia.org/wiki/2011_census_of_India, World CIA Factbook, Amarante Interviews

Non

earning

tech savvy

Youth

18% of the population (222 M) between

the ages 15 to 24. (2014 est.)

• Young, tech savvy segment

• Have no bills to pay or earning of

their own

• Get pocket money/spending power

from parents

• Interested in hanging out,

entertainment, content, apps etc.

Main spending on:

• Eating out

• P2P among peers

• Downloading content, music

etc. / online merchant

payments

• Cinema tickets, rock shows,

other events etc.

Potential Customer Profiles: Primarily un(der)banked people 2/2

Conclusions

36

Challenges and opportunities for banks and MFIs

Banks MFIs

Challenges

Not motivated to serve low income customers

Opening up bank accounts on Core Banking Systems

(CBS) for low value balances and transactions makes it

expensive

Cumbersome sign up process for customers. Customers

need to open bank accounts and many times need to go to

the bank branch at least once (e.g. to pick up ATM card).

Moreover, some customers also do not have the requisite

KYC documents

Lead time is long between application form filling/account

opening at a business correspondent and customers

actually being able to transact full fledged on the account

(sometimes more than a week)

Opportunities

e-KYC with Aadhaar will make account opening easier

Remote validation of bank account opening based on a

scanned electronic copy can also ease the KYC burdens

Abridged CBS platforms (or payment bank platforms, if

approved by the sponsor bank/RBI) can lower processing

costs for healthy transaction volumes and providing real

time transaction processing

White label business correspondents can be added to

banks’ distribution network and generate more transaction

volumes

Challenges

Not enough financial muscle to invest in technology on

their own

Mobile phone (SMS / USSD / Application) based

instructions are still a challenge for poorer, uneducated or

non tech savvy people

Cards infrastructure can get expensive

Opportunities

• A good partner with viable technology and adequate reach

can facilitate substantial customer take up

37

Challenges and opportunities for MNOs and third parties

MNOs Third Parties

Challenges

Set up and management of a sufficiently large distribution

network is tough

Cash & liquidity management and monitoring & risk

management is not an easy task and it is indispensable

for this business

There is often not enough push and commitment from the

partner involved (especially if it’s a bank)

Opportunities

Should the RBI approve the Payment Bank License, service

providers can offer more adapted services to the clients e.g.

deposits and cash out

Incentives can be offered to distributors and retailers. For

example, processing transactions on behalf of illiterate

customers can earn agents commission instead of them

having to take time to educate the customer. Agents can

also be offered credit at attractive rates depending on the

volume of their activity

Opportunities

MNOs have the capability to process low value

transactions in a more economical and efficient way. Once

consumer trust is built, more transaction volumes will lead

to more revenues

Status of a payment bank will allow more freedom to offer

extensive products and services related to payments and

deposits, thus, improving the client value proposition

White Label Business Correspondents can complement

existing networks and be more economically viable to

increase out reach and therefore transaction volumes

Challenges

Current regulations do not allow MNOs to offer cash out

through mobile wallets unless the offer is tied to opening a

bank account (which needs a bank partner)

Telco distributors and retailers do not see value in mobile

money services due to low commission (0.5-1% for mobile

money transactions vs 1-2.5% for normal top ups)

On-time float/support is not provided by distributors in a

timely manner and this causes service disruption at the

customer service point

Customer awareness is low

Clients and retailers are more reassured when they see a

bank logo as opposed to a MNO logo on its own

38

Overall market SWOT analysis

Strengths Weaknesses

- The government is largely proactive and is driving

digital and mobile financial initiatives.

- The national payments corporation focuses on mobile

and digital financial initiatives and provides a strong

switch with nation wide reach

- Large populations can be brought on board with the

right ecosystem and customer message/education

- The mobile channel offers a cost effective, secure and

convenient alternative to access financial services

- Technology is evolving to meet the needs of low end

to high end consumers, and is already accessible

through USSD, IVR, SMS, web and apps.

- Despite the market opportunity, the number of actual

customers is still low, largely due to regulatory constraints and

weak business models.

- Banks still need to do more to extend financial services to

un(der) banked segments

- Service providers need to invest more time and money to

make digital financial services a viable business. It cannot just

be an ‘add on’ to an existing business line.

- More marketing and awareness campaigns need to be

developed to educate consumers

- Even though technology is progressive, there are still

incompatibility issues between handsets and required

applications/software to access services

Opportunities Threats

- The regulatory environment is becoming more

enabling, as the government looks to further leverage

mobile channels for financial inclusion

- The Aadhaar ID should make it easier to sign up to

services and become more financially included

- India is a huge market with many potential markets

segments standing to benefit from digital financial

services (migrants, poor, youth, women, recipient of

government disbursements, middle income, high

earners and micro/small businesses,…)

- Risks exist around fraud and there have been some instances

of agents in Customer Service Points running away with

customers’ funds

- The huge costs associated with spectrum could mean that

Telcos are not able to prioritize digital financial services.

Moreover, bureaucracy and policy transparency do not

provide the best environment in this regard.

- Technology doesn’t seem to be a differentiator given the wide

range of technology solutions available. Customer and agent

journeys and ecosystem viability (in terms of commissions,

margins etc.) will make the difference

39

Main conclusions

By linking Aadhaar numbers to Know Your Customer (KYC) norms, RBI has already paved the way for universalising bank

accounts and removing one of the most important barriers to financial access. Given this, one of the main inhibitors to digital

financial services will be lowered if business correspondent outlets are equipped with the right devices and if all clients are

is asked to use their Aadhaar number for registration and transactions

Relaxing the distance criteria (5KM to 30 KM) between the BC and the sponsor bank’s nearest branch, which is a major

obstacle of Business Correspondent (BC) distribution in rural areas, can encourage Digital Financial Services (DFS) and be

immensely beneficial especially given the lack bank branches in those areas.

Introducing Payment Bank license and allowing existing PPIs to upgrade so that these players can introduce expansion in

the DFS product and services offering will enhance and facilitate more access to finance. Their services would then include

deposits into accounts, transfers and withdrawal from accounts. This will ultimately drive consumer transactions and

adoption and cater to a more complete offer rather than just remittance and payments.

The National Payment Corporation’s IMPS initiative allows transactions to be instructed between bank account numbers

and phone numbers but the next step is to permit transactions between MNOs, other providers and also the different

Business Correspondent (BC) networks in order to create a fully inclusive ecosystem.

Greater investment in developing the telecommunications infrastructure in rural areas is needed and will ensure a good

provision of services that is not inhibited by poor network coverage.

Good agent management is absolutely critical for the business. Motivated and trained agents will provide a good level of

customer service which in turn will create trust and credibility that is crucial for service take up. With a strong BC/agent

network in place, offering more services will naturally increase transaction volumes and reduce account dormancy

Service providers should consider offering incentives on customer activity and not just on registration: The distribution sales

force should have strong incentives to register customers that might actually use the service. With proper incentives, the

sales force will take more care with each customer interaction and encourage clients to use the service frequently.

Through the research and analysis conducted, the following are the main conclusions and

facilitating factors for digital financial services to take off in India:

Some Digital Financial Services industry

best practices & examples

41

Client acquisition

Use appropriate and relevant market study results in order to design a value

proposition adapted to the customer demand

– Familiarize the customer with the product and promote the value proposition

to the customer

– Ensure easy registration process and a good customer experience

– Activate account immediately after a registration to encourage the use of

product / service

– Ensure that the distribution network is capable of handling operations

– Ensure effective customer service

A good experience, especially during the first use of the service will create

positive publicity and will go a long way to motivate agents too!

42

Example of good customer experience

Orange Money is available in 13 countries in Africa and the Middle East

Orange Money has experienced high customer take up; in Senegal there are 10 million customers; in Ivory Coast and

Madagascar more than 40% of Orange customers are registered with mobile money accounts

Much of Orange’s success can be attributed to their strong emphasis on the customer experience

From a marketing perspective, Orange Madagascar emphasize three key aspects: the first is understanding the market

through a full customer segmentation; the second is preparing new products by testing the value proposition through focus

groups and the third is testing the customer experience before launch. Each of these approaches puts the user, and their

needs, at the centre of the process.

Orange has invested resources in the end user experience and created a strong brand image by partnering with

established companies e.g. utility companies. In Ivory Coast, it has built a network of ATMs, which allows customers to

access cash at any time without the assistance of an agent.

In Madagascar, they focus internally on aligning the marketing and distribution sides of the business to be able to rapidly

adapt to customer demand, reacting quickly in order to roll out new products.

In terms of customer service, Orange conducts regular training with customer support to ensure active responsiveness and

monitors agents closely to ensure customers receive a good experience

By meeting the needs of customers and linking the brand with trusted and credible associations, Orange has become

recognized as a reliable and secure service.

Source: Orange, GSMA

In Africa, Orange Telecom enjoys a healthy volume of clients adoption

thanks to the good customer experience it provides

43

The marketing campaign…

Have a marketing campaign that is:

• Clear, simple, with one or two specific messages

• Transparent on pricing per transaction

• In a language spoken by all, easy to understand and in

the local/popular language

• Educative and formative

• In proximity to the target client

“M-pesa Man”, the M-

pesa mascot in Tanzania

44

… with below-the-line (BTL) and above-the-line (ATL) marketing

1. Create the « buzz »: (BTL/proximity marketing)

• Flyers

• Posters

• Road shows

• Educative sessions

• Street marketing

• Signs and boards at agent sites

• …

2. Leverage on ATL marketing (high value, high reach marketing)

• Radio spots, Television ads …

• Billboards

• …

45

Look for a mix of Operational Efficiency, Geographical Coverage

& Overall Control

Key considerations when setting up an agent network

• Have a concrete channel management structure and plan: Ensure flexibility in plan to accommodate

for market feedback and evolution

• Select agents with potential : This must fit with your business objective, be adapted to end customer

context and be easily set up with required equipment

• Determine an appropriate policy on commission: No one will work for free

• Have a distribution plan that is aligned with customer take up of the business and is split by

region/area to be covered.

• Implement best practices for liquidity management and other relevant support: The service is going to

considerably impact the agents’ cash management and business size

• Provide comprehensive training: Enable the agents to perform tasks needed

• Divide roles and responsibilities between three key tasks: Agent recruitment, documentation & process

and overall agent management

• Establish mechanisms for monitoring and evaluation of performance: Always ensure adequate control

46

The role of the agent (at the very least)

Verify client identity

• Ensure KYC process (if any)

• Safeguard against fraud

Handle client’s transaction request

• Offer clients easy access to perform their transaction (cash-in, cash-out etc.)

Be the customer’s point of contact

• Educate the client about the service

• Provide first level support to the client

Alert MM provider on all suspicions

transactions

• Ensure all transactions are made according to set norms

47

Example of good agent network management

- Strong recruitment criteria for agents

- Managing agent performance closely

- Increasing support of agent liquidity

Initiatives have accelerated agent activity levels and contributed to agent profitability multiplying four fold

Agents have become more motivated and provide better service to customers at the point of sale

MTN Côte d’Ivoire now has one of the highest agent activity rates in the world, with over 95% of its agents

active on a 30-day basis.

In Uganda, MTN communicates with its network of 15,000 agents through Agent Forums, which complement the

traditional means of communication via bulk SMS and on-site interaction. These forums are held in key

communities across the country on a quarterly basis. Over 25 key towns within Uganda are touched and over

8000 agents are accessed. These forums enjoy high level participation by agents because of the easy access to

the centres and the content of the conventions. Content discussed is related to Fraud Awareness & Prevention,

Liquidity Management, Product Awareness, Customer Service Practices, Agent Experience Sharing and Q & A.

Source:GMSA, MTN, MobileMoneyAfrica

MTN has built a strong agent network and employed good agent network

management techniques across many African countries.

MTN has deployed a very successful agent management, recruitment and

training programme across its operations in Africa through:

48

Example of successful product and service delivery through multiple

channels

First National Bank is one of the largest banks in South Africa, and one of the country’s mobile money pioneers, 51%

of mobile money users are FNB eWallet customers.

In October 2009, the bank launched its first eWallet mobile money solution and since then has become the largest

mobile money service in South Africa with over 2.5 million recipients and has processed transactions for over USD 499

million. FNB has also rolled out the eWallet in Botswana, Lesotho, Namibia, Swaziland and Zambia.

Part of the eWallet’s success is that it is network agnostic, not relying on any one of the MNOs.

Customers can place funds in the wallets through online banking or through the phones, whilst the receiver can use

the money in various ways e.g. pay bills, buy airtime or transfer money.

As a bank, it has relied on its own network of 4000 ATMs and has also partnered with retailers to complement the

network’s reach. In rural areas, the bank has deployed 1000 mini ATMs (which are small touch-screen terminals

installed in a retailer’s shop) allowing anyone to withdraw cash and FNB customers to check their account balances.

Also in rural areas, the bank has opened ‘lower-cost” branches. Typically staffed by two people, these are located

around townships, offer simple products and use automated deposit machines so they can limit the handling of cash.

The bank also has a mobile application and site which work on all internet enabled cell phones, including feature

phones.

Source: FNB, GSMA

In South Africa, First National Bank is an example of successful

product and service delivery through a network of ATMs and retailers

49

Example of good partnership dynamics

Partnerships are important to successfully grow and scale businesses.

Mobile money providers can work with stakeholders from a variety of sectors and common tie ups occur with financial

institutions, government/NGOs, MFIs, merchants and schools/universities.

bKash, a joint venture between Brac Bank and Money In Motion in Bangladesh, is one example of a service provider who

has continuously focussed on partnership development. IFC and Bill & Melinda Gates Foundation have also provided

support to bKash.

BRAC Bank, a SME focused private commercial bank in Bangladesh, works closely with its parent organization, BRAC,

which has a presence all over Bangladesh. Money in Motion, provides the technology and brings together investors and

mobile network, mobile money and mobile commerce operators. IFC and Gates Foundation, along with the capital, bring

global governance practices and knowledge on financial inclusion.

bKash has created a strong value proposition which has enabled it to successfully expand and diversify across industry

sectors

bKash is now widely accepted across Bangladesh and has become the largest payments service provider. Its service is

interoperable with each MNO: Robi Axiata, Grameenphone, Banglalink and Airtel which has allowed Bkash to serve

almost 100% of the population and even those using the most basic handsets.

Initially focussing on serving the poor, bKash now services a vast majority of the population.

Source: bKash, Amarante Consulting, efse

In Bangladesh, bKash is an example of good ecosystem expansion

through partnerships

50

Example of a successful interoperable ecosystem

The operators were able to develop and launch a solution quickly by setting up teams with members from each

department covering legal, customer care and IT that would be especially be affected by mobile money

interoperability.

Challenges that needed to be overcome included: How to route transactions between the different schemes, enabling

communication across platforms, managing AML/CFT and handling financial processes related to reconciliation and

settlement.

Cash-in and cash-out are handled by agents of the mobile money schemes of which the customer is a member or to

which the customer belongs

Sending money across networks costs customers IDR 2,000 (less than USD 0.20). This fee is shared between the

originating and receiving schemes. Transferring money within a particular mobile money scheme is, however, free of

charge.

Source: AFI, GSMA

In Indonesia, three of the largest MNOs, Telkomsel, Indosat and

XL have allowed customers to send and receive money across

each other's networks to any account or mobile wallet

Each of the three operators had established payments systems on their own, but in a

geographically dispersed country like Indonesia, isolated payments schemes are

unlikely to have enough reach to drive significant usage. With a new enabling

regulator, connecting their platforms would allow them to capitalise on the potential of

the payments market, strengthen the value proposition for their customers, and

become more competitive overall in the payments market

51

Constant feedback collection and service improvement is key

Client feedback Agent Feedback Market evolution

Improvement and

expansion of the service

52

Other useful reading material

• CGAP, Yale School of Management “Mobile Banking in India: Barriers and Adoption

Triggers”, 2013

• GSMA, “State of the Industry: Mobile Money”, 2013

• Nielsen, “Smartphone Incidence Study”, 2013

• The Economist, “India Onward”, 2013; “India On Demand” 2013: “Slums, Youth and the

Mobile Internet in Urban India”, 2012

• Centre Microfinance (IFMR Research), CGAP Blog, “How do migrant workers move money

in India”, 2011

• GSMA, “Mobile Economy India” 2013

• Deloitte, “M-Banking & M-Payments: The Next Frontier”, 2013

• Reserve Bank of India, “Nachiket More: Financial Inclusion Committee Report”, 2013

• GSMA, “Mobile Money, the opportunity for India” 2013

• IFC, “Market Scoping India”, 2013

• MicroSave, “What Will It Take To Deliver ‘Direct Benefits / Cash Transfer Programmes

Successfully”, 2013

• CRISIL, http://www.crisil.com/about-crisil/crisil-inclusix.html#findings

53

Thank you

Digital Financial Services Design and Implementation