maruti suzuki india (maruti) | 6650 · maruti suzuki ltd (msil) reported steady performance in...

TRANSCRIPT

October 26, 2018

ICICI Securities Ltd | Retail Equity Research

Result Update

Near term headwinds, recovery in FY20E…

Maruti Suzuki Ltd (MSIL) reported steady performance in Q2FY19

with optical out-performance led by higher other operating income

(~| 200 crore) on account of income from services from its parent.

Total operating income in Q2FY19 stood at | 22,433 crore, up 3.1%

YoY. ASP for the quarter came in at | 4.44 lakh/unit, flat YoY.

Discounting however was aggressive at | 18,750/unit, up 23% YoY

Volumes for Q2FY19 stood at 484,848 units, down 1.5% YoY. Of

this, the domestic volumes de-grew by 0.4% YoY to 455,400 units,

while the exports were down 15.2% YoY to 29,448 units.

EBITDA in Q2FY19 stood at | 3,431 crore with corresponding EBITDA

margins at 15.3%. EBITDA margins are up 40 bps on QoQ basis

largely factoring in cost reduction efforts undertaken by company

which were partially offset by higher sales promotion expense and

adverse foreign exchange movement.

PAT in Q2FY19 stood at | 2,240 crore, down 9.8%YoY

Management commentary cautiously optimistic over H2FY19!

The management sounded cautious on rising cost of ownership of vehicle

owing to higher insurance (blended hike by ~| 9000/unit; ~2% of vehicle

costs), fuel (up nearly 17-25%) as well financing costs (up 35 bps) which

is leading somewhat postposing of purchase by consumers and

consequent slowdown in demand in the PV space domestically. Festive

season too is a lacklustre, resulting in largely flat sales at the retail level. In

the exports market the situation is no different wherein growth is a

challenge amidst currency headwinds and imposition of import tariffs in

key markets. The management however re-iterated its commitment

towards double digit volume growth for FY19E. Sensing the demand

slowdown as well as new launch by one of its key competitor in the

passenger car market we have revised downward our volume estimates

for MSIL going forward. We now expect volumes at MSIL to grow at a

CAGR of 9.0% (11.5% earlier) over FY18-20E to 21.2 lakh units in FY20E.

Market leadership maintained, across segments!

MSIL has been a market leader and outperformed industry in the past. Its

market share increased from ~47% in FY17 to ~50% in FY18 to further

~52% in H1FY19. It has been done by introducing new and impressive

models at an appropriate time suiting to the market needs. It enjoys

market leadership across segments namely- PC, UV and Vans. Currently

its top selling models include Swift, Dzire, Baleno among others and

possesses 7 models out of top 10 PV models sold domestically. Going

forward from the customer perspective it still remains a prominent brand

owing to: low cost of ownership & high dealer and servicing network;

which warrants it to be held in one’s portfolio on long term basis.

Margins to recover in FY20E, B/s positives persists, maintain HOLD!

Management commentary suggest margins to remain muted in H2FY19

primarily tracking impact of INR deprecation on input costs which comes

with a quarterly lag. This will be partially offsetted against cost cutting

undertaken by the company. Going forward, as INR stabilises in FY20E

and structural decline in royalty as well as operating leverage benefits we

expect margins to recover in FY20E. Revising our estimates, we now

expect Sales, EBITDA, PAT of 11,12,14% respectively over FY18-20E. We

value MSIL at | 7250 i.e. 22x P/E on FY20E EPS of | 330 and assign HOLD

rating on the stock. Key positives which remain with MSIL is its cash

surplus balance sheet (~15% market cap), negative working capital cycle,

healthy 20%+ RoCE, ~6% CFO yield and ~4% FCF yield.

Rating matrix

Rating : Hold

Target : | 7250

Target Period : 12 months

Potential Upside : 9%

What’s Changed?

Target Changed from | 9875 to | 7250

EPS FY19E Changed from | 318 to | 291

EPS FY20E Changed from | 380 to | 330

Rating Unchanged

Quarterly Performance

(| Crore) Q2FY19 Q2FY18 YoY (%) Q1FY18 QoQ (%)

Revenue 22,433.2 21,768.2 3.1 22,459.4 -0.1

EBITDA 3,431.3 3,677.5 -6.7 3,351.1 2.4

EBITDA (%) 15.3 16.9 -160 bps 14.9 37 bps

Reported PAT 2,240.4 2,484.3 -9.8 1,975.3 13.4

Key Financials

| Crore FY17 FY18 FY19E FY20E

Revenue 68,035 79,763 89,203 99,109

EBITDA 10,353.0 12,061.5 13,410.8 15,255.0

Net Profit 7,337.7 7,721.8 8,791.3 9,959.3

EPS (|) 242.9 255.6 291.0 329.7

Valuation summary

FY17 FY18 FY19E FY20E

P/E (x) 27.4 26.0 22.9 20.2

Target P/E (x) 29.8 28.4 24.9 22.0

EV/EBITDA (x) 16.8 13.8 12.2 10.3

P/BV (x) 5.6 4.8 4.2 3.8

RoNW (%) 20.3 18.5 18.6 18.6

RoCE (%) 20.3 21.1 21.1 21.1

Stock data

Particular Amount

Market Capitalization (| Crore) | 200883.2 Crore

Total Debt | 110.8 Crore

Cash & Investment | 34153.1 Crore

EV | 166840.9 Crore

52 week H/L (|) 10000 / 6625

Equity capital (| crore) | 151 Crore

Face value (|) | 5

Price performance (%)

1M 3M 6M 12M

M&M Ltd -17.8 -19.4 -14.1 7.5

Maruti Suzuki India -16.0 -31.1 -24.8 -14.6

Tata Motors -31.3 -35.9 -49.7 -60.8

Maruti Suzuki India (MARUTI) | 6650

Research Analyst

Shashank Kanodia, CFA

Vidrum Mehta

ICICI Securities Ltd | Retail Equity Research Page 2

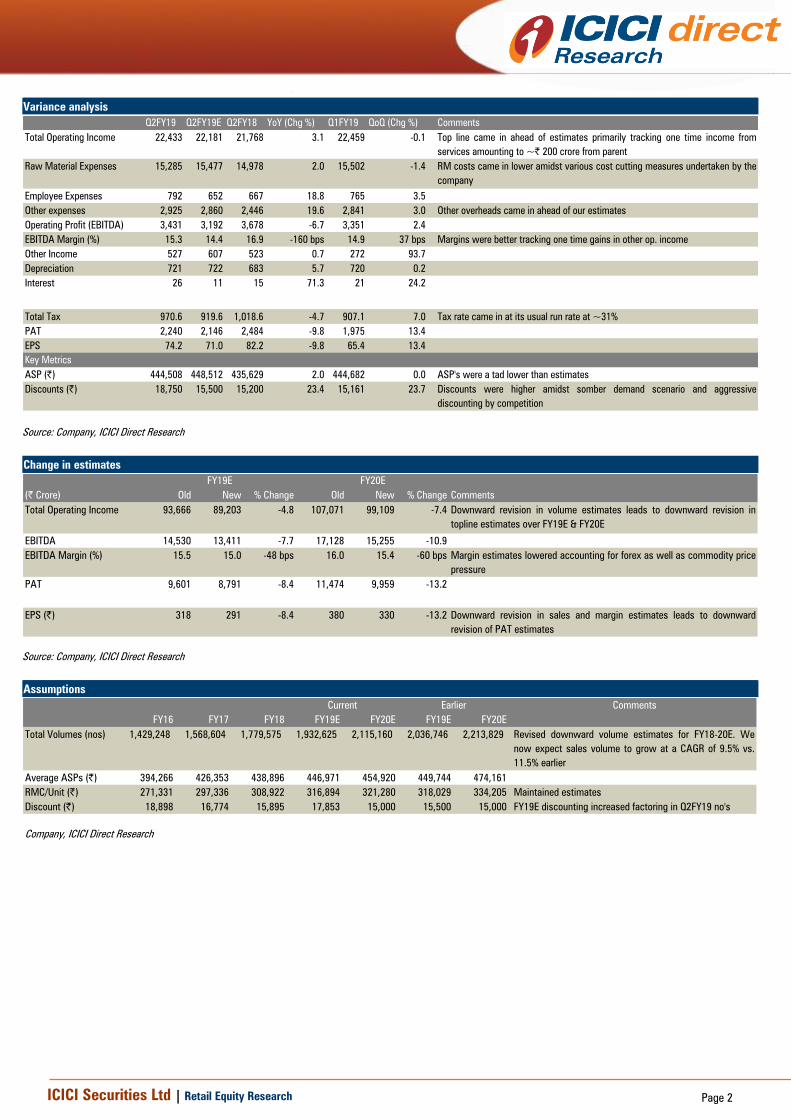

Variance analysis

Q2FY19 Q2FY19E Q2FY18 YoY (Chg %) Q1FY19 QoQ (Chg %) Comments

Total Operating Income 22,433 22,181 21,768 3.1 22,459 -0.1 Top line came in ahead of estimates primarily tracking one time income from

services amounting to ~| 200 crore from parent

Raw Material Expenses 15,285 15,477 14,978 2.0 15,502 -1.4 RM costs came in lower amidst various cost cutting measures undertaken by the

company

Employee Expenses 792 652 667 18.8 765 3.5

Other expenses 2,925 2,860 2,446 19.6 2,841 3.0 Other overheads came in ahead of our estimates

Operating Profit (EBITDA) 3,431 3,192 3,678 -6.7 3,351 2.4

EBITDA Margin (%) 15.3 14.4 16.9 -160 bps 14.9 37 bps Margins were better tracking one time gains in other op. income

Other Income 527 607 523 0.7 272 93.7

Depreciation 721 722 683 5.7 720 0.2

Interest 26 11 15 71.3 21 24.2

Total Tax 970.6 919.6 1,018.6 -4.7 907.1 7.0 Tax rate came in at its usual run rate at ~31%

PAT 2,240 2,146 2,484 -9.8 1,975 13.4

EPS 74.2 71.0 82.2 -9.8 65.4 13.4

Key Metrics

ASP (|) 444,508 448,512 435,629 2.0 444,682 0.0 ASP's were a tad lower than estimates

Discounts (|) 18,750 15,500 15,200 23.4 15,161 23.7 Discounts were higher amidst somber demand scenario and aggressive

discounting by competition

Source: Company, ICICI Direct Research

Change in estimates

(| Crore) Old New % Change Old New % Change Comments

Total Operating Income 93,666 89,203 -4.8 107,071 99,109 -7.4 Downward revision in volume estimates leads to downward revision in

topline estimates over FY19E & FY20E

EBITDA 14,530 13,411 -7.7 17,128 15,255 -10.9

EBITDA Margin (%) 15.5 15.0 -48 bps 16.0 15.4 -60 bps Margin estimates lowered accounting for forex as well as commodity price

pressure

PAT 9,601 8,791 -8.4 11,474 9,959 -13.2

EPS (|) 318 291 -8.4 380 330 -13.2 Downward revision in sales and margin estimates leads to downward

revision of PAT estimates

FY19E FY20E

Source: Company, ICICI Direct Research

Assumptions

Comments

FY16 FY17 FY18 FY19E FY20E FY19E FY20E

Total Volumes (nos) 1,429,248 1,568,604 1,779,575 1,932,625 2,115,160 2,036,746 2,213,829 Revised downward volume estimates for FY18-20E. We

now expect sales volume to grow at a CAGR of 9.5% vs.

11.5% earlier

Average ASPs (|) 394,266 426,353 438,896 446,971 454,920 449,744 474,161

RMC/Unit (|) 271,331 297,336 308,922 316,894 321,280 318,029 334,205 Maintained estimates

Discount (|) 18,898 16,774 15,895 17,853 15,000 15,500 15,000 FY19E discounting increased factoring in Q2FY19 no's

Current Earlier

Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 3

Conference Call Highlights

Management Outlook/Guidance & Demand

Company sounded guarded on earlier guidance of double digit

growth this year. While it was on track thus far in H1FY19,

H2FY19E has been impacted by issues surrounding cost of

ownership viz. fuel, insurance and financing.

Company is hopeful of pent-up demand emerging over next

couple of months in Kerala, UP, Uttrakhand and some other

eastern states which have been flood-affected in the recent past.

Retail side festive demand has been flat thus far. However,

company remains hopeful about the approaching Diwali season.

On a YoY basis urban centres including Mumbai and Gujarat have

experienced soft demand while rural pockets have registered 13%

growth on the back of higher disposable incomes and good

monsoons.

Company reported that 63% of domestic PV volumes were in the

petrol segment.

It will be an uphill task for the company to match last year’s

export growth due to higher relative currency depreciation of

other economies vis-à-vis Indian Rupee and rising trade

protectionism.

Company remains bullish on its LCV division where it is currently

the second largest player and has sizeable network strength in the

segment that it operates into.

Company sees CNG as an immediate agent for change while

remaining upbeat about electrification and hybridization prospects

as well.

Revenue & Margins

Company’s cost reduction efforts mitigated the combined ~350

bps impact of commodity prices (~120 bps), exchange rate

movement (~120 bps) and product discounts (~130 bps).

Company expects lesser impact of steel prices in H2FY19E than

what was seen in H1FY19. Forex impact however is likely to

impact earnings in H2FY19

Exports at | 1,427 crore for Q2FY19 amounted to ~7% of overall

sales.

Others

60% of the company’s royalty payments are made in Japanese

Yen while the rest are made in Indian Rupees.

Imports amounted to 18% of net sales, of which 5% were direct

and 13% were indirect.

Other operating income included some amount is respect of

recovery of engineering services fees from parent Suzuki. A figure

amounting to ~| 200 crore is a one-off. A variable quantum of

such fees will likely be earned per quarter going forward as well.

Gujarat plant produced ~67000 units in this quarter. Next line for

the plant will be commissioned in early 2019 and the third line in

mid-2020, each with a capacity of 2.5 lakh p.a. By 2020 at

~750,000 p.a. capacity and with ancillary set up being developed

in Gujarat, MSIL’s Gujarat plant is expected to nearly match

Haryana plant on localisation content levels.

ICICI Securities Ltd | Retail Equity Research Page 4

Company Analysis

Management commentary cautiously optimistic over H2FY19!

The management sounded cautious on rising cost of ownership of vehicle

owing to higher insurance (blended hike by ~| 9000/unit; ~2% of vehicle

costs), fuel (up nearly 17-25%) as well financing costs (up 350 bps) which

is leading somewhat postposing of purchase by consumers and

consequent slowdown in demand in the PV space domestically. Festive

season too is a lacklustre, resulting in largely flat sales at the retail level. In

the exports market the situation is no different wherein growth is a

challenge amidst currency headwinds and imposition of import tariffs in

key markets. The management however re-iterated its commitment

towards double digit volume growth for FY19E. Sensing the demand

slowdown as well as new launch by one of its key competitor in the

passenger car market we have revised downward our volume estimates

for MSIL going forward. We now expect volumes at MSIL to grow at a

CAGR of 9.0% (11.5% earlier) over FY18-20E to 21.2 lakh units in FY20E.

Consequently, we expect revenues to grow at a CAGR of 11.5 over FY18-

20E to | 99,109 crore in FY20E (| 79,763 crore in FY18). On the back of

near term headwinds, EBITDA margins are expected to taper to 15.0% in

FY19 and then recover to 15.4% as INR stabilises in FY20E. PAT at MSIL

is expected to grow at a CAGR of 13.6% to | 9,959 crore in FY20E.

Exhibit 1: Topline and bottomline trends

43588

43701

49874

57746

68035

79763

89203

99109

23922783

3711 4571

7338

7722

8791

9959

0

2000

4000

6000

8000

10000

12000

0

20000

40000

60000

80000

100000

120000

FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E

(| crore)

(| crore)

Topline Bottomline

Source: Company press release, ICICI Direct Research

Exhibit 2: Margins to recover in FY20E

5,089.9

6,605.9

8,978.6

10,353.0

12,061.5

13,410.8

15,255.0

11.6

13.2

15.5 15.2 15.1 15.0

15.4

-

2

4

6

8

10

12

14

16

18

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

FY14 FY15 FY16 FY17 FY18 FY19E FY20E

(%

)

(| crore)

EBITDA Margins (%)

Source: Company press release, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 5

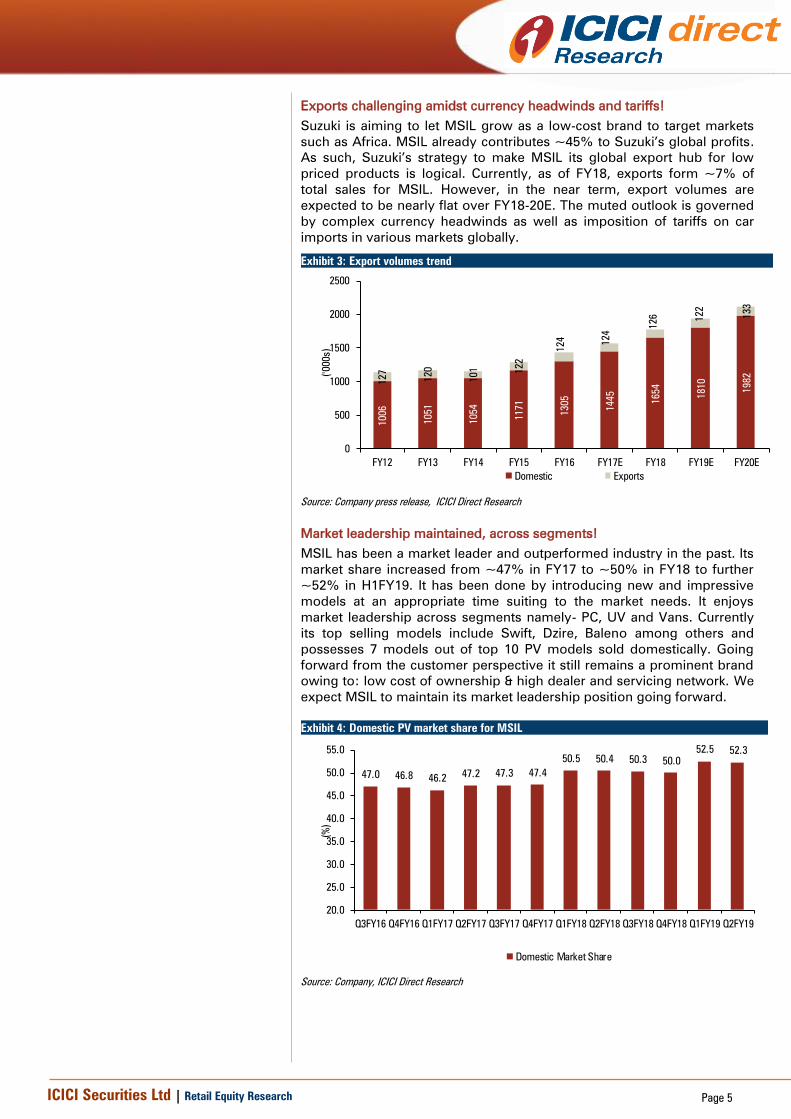

Exports challenging amidst currency headwinds and tariffs!

Suzuki is aiming to let MSIL grow as a low-cost brand to target markets

such as Africa. MSIL already contributes ~45% to Suzuki’s global profits.

As such, Suzuki’s strategy to make MSIL its global export hub for low

priced products is logical. Currently, as of FY18, exports form ~7% of

total sales for MSIL. However, in the near term, export volumes are

expected to be nearly flat over FY18-20E. The muted outlook is governed

by complex currency headwinds as well as imposition of tariffs on car

imports in various markets globally.

Market leadership maintained, across segments!

MSIL has been a market leader and outperformed industry in the past. Its

market share increased from ~47% in FY17 to ~50% in FY18 to further

~52% in H1FY19. It has been done by introducing new and impressive

models at an appropriate time suiting to the market needs. It enjoys

market leadership across segments namely- PC, UV and Vans. Currently

its top selling models include Swift, Dzire, Baleno among others and

possesses 7 models out of top 10 PV models sold domestically. Going

forward from the customer perspective it still remains a prominent brand

owing to: low cost of ownership & high dealer and servicing network. We

expect MSIL to maintain its market leadership position going forward.

Exhibit 4: Domestic PV market share for MSIL

47.0 46.8 46.247.2 47.3 47.4

50.5 50.4 50.3 50.0

52.5 52.3

20.0

25.0

30.0

35.0

40.0

45.0

50.0

55.0

Q3FY16 Q4FY16 Q1FY17 Q2FY17 Q3FY17 Q4FY17 Q1FY18 Q2FY18 Q3FY18 Q4FY18 Q1FY19 Q2FY19

(%

)

Domestic Market Share

Source: Company, ICICI Direct Research

Exhibit 3: Export volumes trend

1006

1051

1054

1171

1305

1445

1654

1810

1982

127

120

101 122

124

124

126 122

133

0

500

1000

1500

2000

2500

FY12 FY13 FY14 FY15 FY16 FY17E FY18 FY19E FY20E

('0

00s)

Domestic Exports

Source: Company press release, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 6

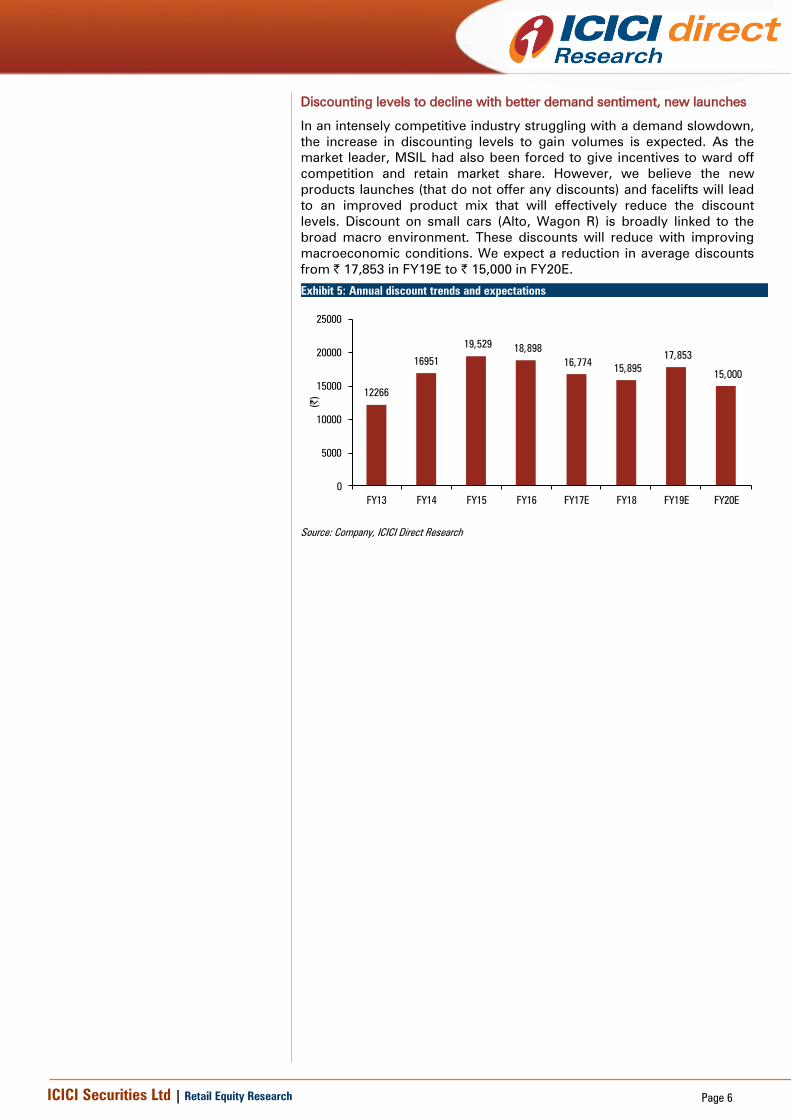

Discounting levels to decline with better demand sentiment, new launches

In an intensely competitive industry struggling with a demand slowdown,

the increase in discounting levels to gain volumes is expected. As the

market leader, MSIL had also been forced to give incentives to ward off

competition and retain market share. However, we believe the new

products launches (that do not offer any discounts) and facelifts will lead

to an improved product mix that will effectively reduce the discount

levels. Discount on small cars (Alto, Wagon R) is broadly linked to the

broad macro environment. These discounts will reduce with improving

macroeconomic conditions. We expect a reduction in average discounts

from | 17,853 in FY19E to | 15,000 in FY20E.

Exhibit 5: Annual discount trends and expectations

12266

16951

19,529 18,898

16,774 15,895

17,853

15,000

0

5000

10000

15000

20000

25000

FY13 FY14 FY15 FY16 FY17E FY18 FY19E FY20E

(|)

Source: Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 7

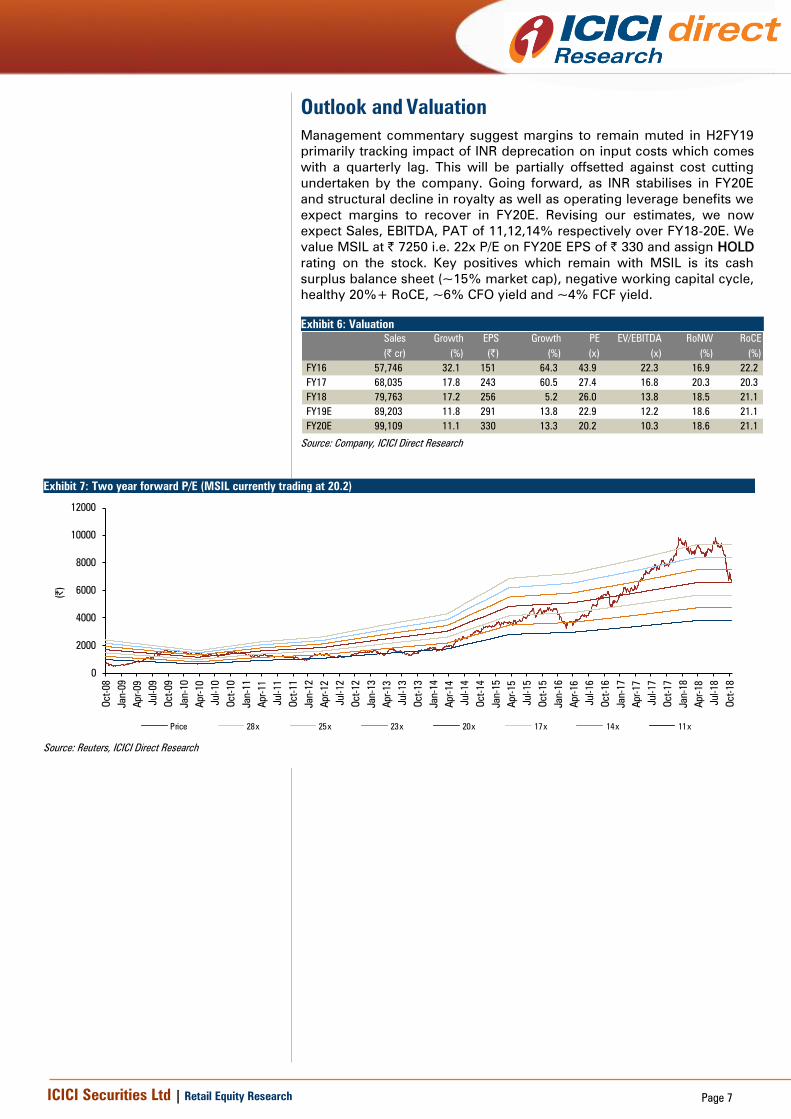

Outlook and Valuation

Management commentary suggest margins to remain muted in H2FY19

primarily tracking impact of INR deprecation on input costs which comes

with a quarterly lag. This will be partially offsetted against cost cutting

undertaken by the company. Going forward, as INR stabilises in FY20E

and structural decline in royalty as well as operating leverage benefits we

expect margins to recover in FY20E. Revising our estimates, we now

expect Sales, EBITDA, PAT of 11,12,14% respectively over FY18-20E. We

value MSIL at | 7250 i.e. 22x P/E on FY20E EPS of | 330 and assign HOLD

rating on the stock. Key positives which remain with MSIL is its cash

surplus balance sheet (~15% market cap), negative working capital cycle,

healthy 20%+ RoCE, ~6% CFO yield and ~4% FCF yield.

Exhibit 6: Valuation

Sales Growth EPS Growth PE EV/EBITDA RoNW RoCE

(| cr) (%) (|) (%) (x) (x) (%) (%)

FY16 57,746 32.1 151 64.3 43.9 22.3 16.9 22.2

FY17 68,035 17.8 243 60.5 27.4 16.8 20.3 20.3

FY18 79,763 17.2 256 5.2 26.0 13.8 18.5 21.1

FY19E 89,203 11.8 291 13.8 22.9 12.2 18.6 21.1

FY20E 99,109 11.1 330 13.3 20.2 10.3 18.6 21.1

Source: Company, ICICI Direct Research

Exhibit 7: Two year forward P/E (MSIL currently trading at 20.2)

0

2000

4000

6000

8000

10000

12000

Oct-08

Jan-09

Apr-09

Jul-09

Oct-09

Jan-10

Apr-10

Jul-10

Oct-10

Jan-11

Apr-11

Jul-11

Oct-11

Jan-12

Apr-12

Jul-12

Oct-12

Jan-13

Apr-13

Jul-13

Oct-13

Jan-14

Apr-14

Jul-14

Oct-14

Jan-15

Apr-15

Jul-15

Oct-15

Jan-16

Apr-16

Jul-16

Oct-16

Jan-17

Apr-17

Jul-17

Oct-17

Jan-18

Apr-18

Jul-18

Oct-18

(|)

Price 28x 25x 23x 20x 17x 14x 11x

Source: Reuters, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 8

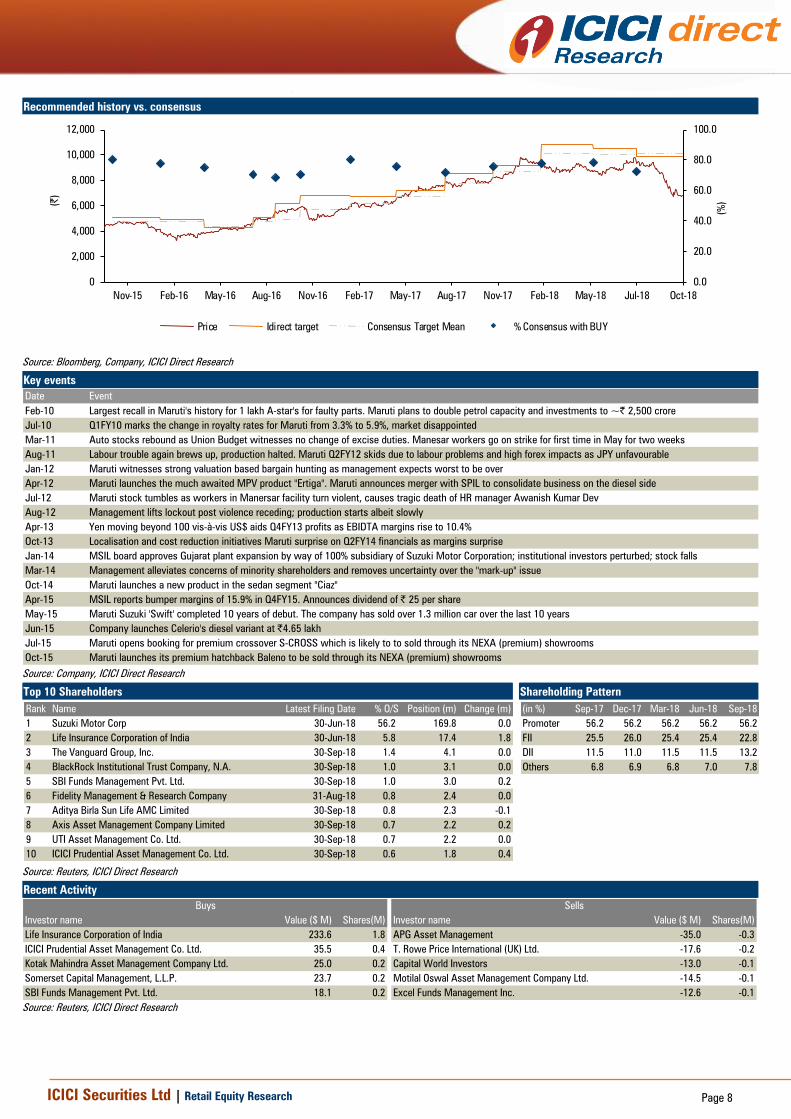

Recommended history vs. consensus

0.0

20.0

40.0

60.0

80.0

100.0

0

2,000

4,000

6,000

8,000

10,000

12,000

Oct-18Jul-18May-18Feb-18Nov-17Aug-17May-17Feb-17Nov-16Aug-16May-16Feb-16Nov-15

(%

)(|)

Price Idirect target Consensus Target Mean % Consensus with BUY

Source: Bloomberg, Company, ICICI Direct Research

Key events

Date Event

Feb-10 Largest recall in Maruti's history for 1 lakh A-star's for faulty parts. Maruti plans to double petrol capacity and investments to ~| 2,500 crore

Jul-10 Q1FY10 marks the change in royalty rates for Maruti from 3.3% to 5.9%, market disappointed

Mar-11 Auto stocks rebound as Union Budget witnesses no change of excise duties. Manesar workers go on strike for first time in May for two weeks

Aug-11 Labour trouble again brews up, production halted. Maruti Q2FY12 skids due to labour problems and high forex impacts as JPY unfavourable

Jan-12 Maruti witnesses strong valuation based bargain hunting as management expects worst to be over

Apr-12 Maruti launches the much awaited MPV product "Ertiga". Maruti announces merger with SPIL to consolidate business on the diesel side

Jul-12 Maruti stock tumbles as workers in Manersar facility turn violent, causes tragic death of HR manager Awanish Kumar Dev

Aug-12 Management lifts lockout post violence receding; production starts albeit slowly

Apr-13 Yen moving beyond 100 vis-à-vis US$ aids Q4FY13 profits as EBIDTA margins rise to 10.4%

Oct-13 Localisation and cost reduction initiatives Maruti surprise on Q2FY14 financials as margins surprise

Jan-14 MSIL board approves Gujarat plant expansion by way of 100% subsidiary of Suzuki Motor Corporation; institutional investors perturbed; stock falls

Mar-14 Management alleviates concerns of minority shareholders and removes uncertainty over the "mark-up" issue

Oct-14 Maruti launches a new product in the sedan segment "Ciaz"

Apr-15 MSIL reports bumper margins of 15.9% in Q4FY15. Announces dividend of | 25 per share

May-15 Maruti Suzuki 'Swift' completed 10 years of debut. The company has sold over 1.3 million car over the last 10 years

Jun-15 Company launches Celerio's diesel variant at |4.65 lakh

Jul-15 Maruti opens booking for premium crossover S-CROSS which is likely to to sold through its NEXA (premium) showrooms

Oct-15 Maruti launches its premium hatchback Baleno to be sold through its NEXA (premium) showrooms

Source: Company, ICICI Direct Research

Top 10 Shareholders Shareholding Pattern

Rank Name Latest Filing Date % O/S Position (m) Change (m)

1 Suzuki Motor Corp 30-Jun-18 56.2 169.8 0.0

2 Life Insurance Corporation of India 30-Jun-18 5.8 17.4 1.8

3 The Vanguard Group, Inc. 30-Sep-18 1.4 4.1 0.0

4 BlackRock Institutional Trust Company, N.A. 30-Sep-18 1.0 3.1 0.0

5 SBI Funds Management Pvt. Ltd. 30-Sep-18 1.0 3.0 0.2

6 Fidelity Management & Research Company 31-Aug-18 0.8 2.4 0.0

7 Aditya Birla Sun Life AMC Limited 30-Sep-18 0.8 2.3 -0.1

8 Axis Asset Management Company Limited 30-Sep-18 0.7 2.2 0.2

9 UTI Asset Management Co. Ltd. 30-Sep-18 0.7 2.2 0.0

10 ICICI Prudential Asset Management Co. Ltd. 30-Sep-18 0.6 1.8 0.4

(in %) Sep-17 Dec-17 Mar-18 Jun-18 Sep-18

Promoter 56.2 56.2 56.2 56.2 56.2

FII 25.5 26.0 25.4 25.4 22.8

DII 11.5 11.0 11.5 11.5 13.2

Others 6.8 6.9 6.8 7.0 7.8

Source: Reuters, ICICI Direct Research

Recent Activity

Investor name Value ($ M) Shares(M) Investor name Value ($ M) Shares(M)

Life Insurance Corporation of India 233.6 1.8 APG Asset Management -35.0 -0.3

ICICI Prudential Asset Management Co. Ltd. 35.5 0.4 T. Rowe Price International (UK) Ltd. -17.6 -0.2

Kotak Mahindra Asset Management Company Ltd. 25.0 0.2 Capital World Investors -13.0 -0.1

Somerset Capital Management, L.L.P. 23.7 0.2 Motilal Oswal Asset Management Company Ltd. -14.5 -0.1

SBI Funds Management Pvt. Ltd. 18.1 0.2 Excel Funds Management Inc. -12.6 -0.1

Buys Sells

Source: Reuters, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 9

.

Financial summary

Profit and loss statement | Crore

(Year-end March) FY17 FY18 FY19E FY20E

Total operating Income 68,035 79,763 89,203 99,109

Growth (%) 18 17 12 11

Raw Material Expenses 46,732 54,975 61,244 67,956

Employee Expenses 2,331 2,834 3,190 3,390

Marketing Expenses 0 0 0 0

Administrative Expenses 0 0 0 0

Other expenses 8,619 9,892 11,359 12,509

Total Operating Expenditure 57,682 67,701 75,793 83,854

EBITDA 10,353 12,062 13,411 15,255

Growth (%) 57 17 11 14

Depreciation 2,602 2,758 2,944 3,469

Interest 89 346 88 88

Other Income 2,280 2,046 2,346 2,736

PBT 9,941 11,003 12,725 14,434

Others 0 0 0 0

Total Tax 2,604 3,282 3,933 4,474

PAT 7,338 7,722 8,791 9,959

Growth (%) 98 5 14 13

EPS (|) 243 256 291 330

Source: Company, ICICI Direct Research

Cash flow statement | Crore

(Year-end March) FY17 FY18 FY19E FY20E

Profit after Tax 7,338 7,722 8,791 9,959

Add: Depreciation 2,602 2,758 2,944 3,469

(Inc)/dec in Current Assets -346 -50 -1,349 -343

Inc/(dec) in CL and Provisions 1,535 2,584 676 1,282

Others 89 346 88 88

CF from operating activities 11,219 13,359 11,150 14,455

(Inc)/dec in Investments -26,682 -6,527 -3,400 -6,180

(Inc)/dec in Fixed Assets -3,369 -3,701 -4,000 -4,000

Others 16,663 -218 -319 -311

CF from investing activities -13,388 -10,447 -7,719 -10,491

Issue/(Buy back) of Equity 0 0 0 0

Inc/(dec) in loan funds 406 -373 0 0

Dividend paid & dividend tax -2,727 -2,900 -3,262 -3,806

Inc/(dec) in Sec. premium 0 0 0 0

Others 4,464 419 -88 -88

CF from financing activities 2,143 -2,854 -3,350 -3,894

Net Cash flow -26 58 81 70

Opening Cash 39 13 71 152

Closing Cash 13 71 152 222

Source: Company, ICICI Direct Research

Balance sheet | Crore

(Year-end March) FY17 FY18 FY19E FY20E

Liabilities

Equity Capital 151 151 151 151

Reserve and Surplus 36,020 41,606 47,135 53,288

Total Shareholders funds 36,171 41,757 47,286 53,439

Total Debt 484 111 111 111

Deferred Tax Liability 464 559 559 559

Others Liabilties 1,127 1,612 1,652 1,692

Total Liabilities 38,246 44,039 49,608 55,801

Assets

Gross Block 18,656 21,424 26,550 31,050

Less: Acc Depreciation 5,367 8,065 11,009 14,477

Net Block 13,289 13,359 15,541 16,572

Capital WIP 1,252 2,126 1,000 500

Total Fixed Assets 14,542 15,485 16,541 17,072

Investments 28,228 35,290 38,940 45,370

Inventory 3,262 3,161 3,788 3,937

Debtors 1,199 1,462 1,955 1,901

Loans and Advances 3 3 9 10

Other Current Assets 2,119 2,007 2,230 2,478

Cash 13 71 152 222

Total Current Assets 6,596 6,704 8,134 8,547

Creditors 8,367 10,497 10,998 12,219

Provisions 449 560 550 611

Other current Liabilities 3,931 4,274 4,460 4,460

Total Current Liabilities 12,748 15,331 16,008 17,290

Net Current Assets -6,152 -8,627 -7,873 -8,743

Other Assets 1,627 1,891 2,000 2,101

Application of Funds 38,246 44,039 49,608 55,801

Source: Company, ICICI Direct Research

Key ratios

(Year-end March) FY17 FY18 FY19E FY20E

Per share data (|)

EPS 242.9 255.6 291.0 329.7

Cash EPS 329.0 346.9 388.5 444.5

BV 1,197.4 1,382.3 1,565.3 1,769.0

DPS 75.0 80.0 90.0 105.0

Cash Per Share 0.4 2.4 5.0 7.3

Operating Ratios

EBITDA Margin (%) 15.2 15.1 15.0 15.4

PBIT / Net sales (%) 11.4 11.7 11.7 11.9

PAT Margin (%) 10.8 9.7 9.9 10.0

Inventory days 17.5 14.5 15.5 14.5

Debtor days 6.4 6.7 8.0 7.0

Creditor days 44.9 48.0 45.0 45.0

Return Ratios (%)

RoE 20.3 18.5 18.6 18.6

RoCE 20.3 21.1 21.1 21.1

RoIC 66.1 91.7 77.9 85.6

Valuation Ratios (x)

P/E 27.4 26.0 22.9 20.2

EV / EBITDA 16.8 13.8 12.2 10.3

EV / Net Sales 2.6 2.1 1.8 1.6

Market Cap / Sales 3.0 2.5 2.3 2.0

Price to Book Value 5.6 4.8 4.2 3.8

Solvency Ratios

Debt/EBITDA 0.0 0.0 0.0 0.0

Debt / Equity 0.0 0.0 0.0 0.0

Current Ratio 0.7 0.6 0.7 0.6

Quick Ratio 0.4 0.3 0.4 0.3

Source: Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 10

ICICI Direct Research coverage universe (Auto & Auto Ancillary)

CMP M Cap

(|) TP(|) Rating (| Cr) FY18E FY19E FY20E FY18E FY19E FY20E FY18E FY19E FY20E FY18E FY19E FY20E FY18E FY19E FY20E

Amara Raja (AMARAJ) 760 875 Hold 12977 27.6 32.8 41.6 27.5 23.1 18.3 15.9 13.3 10.7 23.3 23.5 25.3 16.0 16.3 17.5

Apollo Tyre (APOTYR) 211 325 Buy 12070 12.7 19.5 25.0 16.7 10.8 8.5 8.4 8.4 7.2 7.8 10.7 12.6 7.4 10.4 12.0

Ashok Leyland (ASHLEY) 117 135 Buy 33010 5.3 6.6 8.2 21.9 17.7 14.3 10.2 8.8 6.8 28.5 31.2 33.0 21.9 23.4 24.2

Bajaj Auto (BAAUTO) 2567 2410 Hold 74271 140.6 153.3 169.5 17.6 16.2 14.6 11.8 10.4 8.9 22.9 22.4 22.3 21.5 20.7 20.4

Balkrishna Ind. (BALIND) 1039 1250 Buy 20085 38.2 50.2 59.2 31.2 23.8 20.2 21.0 14.8 12.1 22.4 25.8 25.9 18.1 25.8 25.9

Bharat Forge (BHAFOR) 565 720 Buy 26302 16.2 24.1 28.1 34.9 23.5 20.1 17.4 14.2 12.0 23.0 27.0 26.1 17.5 23.8 21.7

Bosch (MICO) 18601 20000 Hold 58407 449.1 585.3 645.5 43.0 33.0 29.9 26.8 21.9 19.1 14.4 16.2 16.0 21.4 24.2 23.9

Eicher Motors (EICMOT) 22165 32900 Buy 59868 725.5 989.1 1214.6 30.5 22.4 18.2 26.5 20.6 16.4 39.1 37.0 35.1 29.9 28.7 27.1

Exide Industries (EXIIND) 263 300 Buy 22389 8.2 10.1 12.3 31.9 26.1 21.4 18.3 14.7 12.2 19.1 20.7 22.2 13.0 14.2 15.4

Hero Moto (HERHON) 2832 3350 Buy 56547 185.1 186.6 209.6 15.3 15.2 13.5 9.5 9.2 7.9 42.4 41.0 41.3 31.4 29.0 29.1

JK Tyre & Ind (JKIND) 97 120 Hold 2202 2.9 15.7 22.1 33 6.2 4.4 10.3 5.9 4.8 7.8 13.2 15.3 3.7 16.6 18.8

Mahindra CIE (MAHAUT) 264 280 Buy 9994 9.5 14.5 17.7 27.9 18.2 15.0 13.7 9.9 8.2 9.8 12.9 13.7 11.2 15.0 17.1

Maruti Suzuki (MARUTI) 6650 7250 Hold 200032 255.6 291.0 329.7 26.0 22.9 20.2 13.8 12.2 10.3 21.1 21.1 21.1 18.5 18.6 18.6

Motherson (MOTSUM) 250 335 Hold 52583 7.6 11.2 14.4 32.9 22.3 17.3 14.0 10.7 8.5 16.3 22.5 27.0 17.4 23.0 24.8

Tata Motors (TELCO) 183 200 Hold 54829 26.8 7.0 28.4 6.9 26.2 6.5 2.0 2.8 2.5 10.5 6.9 9.1 10.3 5.9 11.0

Wabco India (WABTVS) 6500 7200 Hold 12350 143.8 175.3 205.8 45.2 37.1 31.6 30.6 26.3 21.6 17.9 18.3 17.9 25.1 25.8 24.9

Sector / Company

RoE (%)EPS (|) P/E (x) EV/EBITDA (x) RoCE (%)

Source: Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 11

RATING RATIONALE

ICICI Direct endeavours to provide objective opinions and recommendations. ICICI Direct assigns ratings to its

stocks according to their notional target price vs. current market price and then categorises them as Strong

Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional target price is

defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICI Direct Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities Ltd | Retail Equity Research Page 12

ANALYST CERTIFICATION

We /I, Shashank Kanodia, CFA MBA (Capital Markets) and Vidrum Mehta, MBA (Finance) Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed

in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific

recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities Limited Sebi Registration is INZ000183631 for stock Broker. ICICI Securities is a wholly-owned

subsidiary of ICICI Bank which is India’s largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture

capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving Shashank Kanodia, CFA MBA (Capital Markets) and Vidrum Mehta, MBA (Finance) this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation

that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make

their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment

by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other

reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors

are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-

looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Shashank Kanodia, CFA MBA (Capital Markets) and Vidrum Mehta, MBA (Finance) Research Analysts of this report have not received any compensation from the companies mentioned

in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.