massy united insurance ltd. united insurance company limited to massy united insurance ltd. on june...

TRANSCRIPT

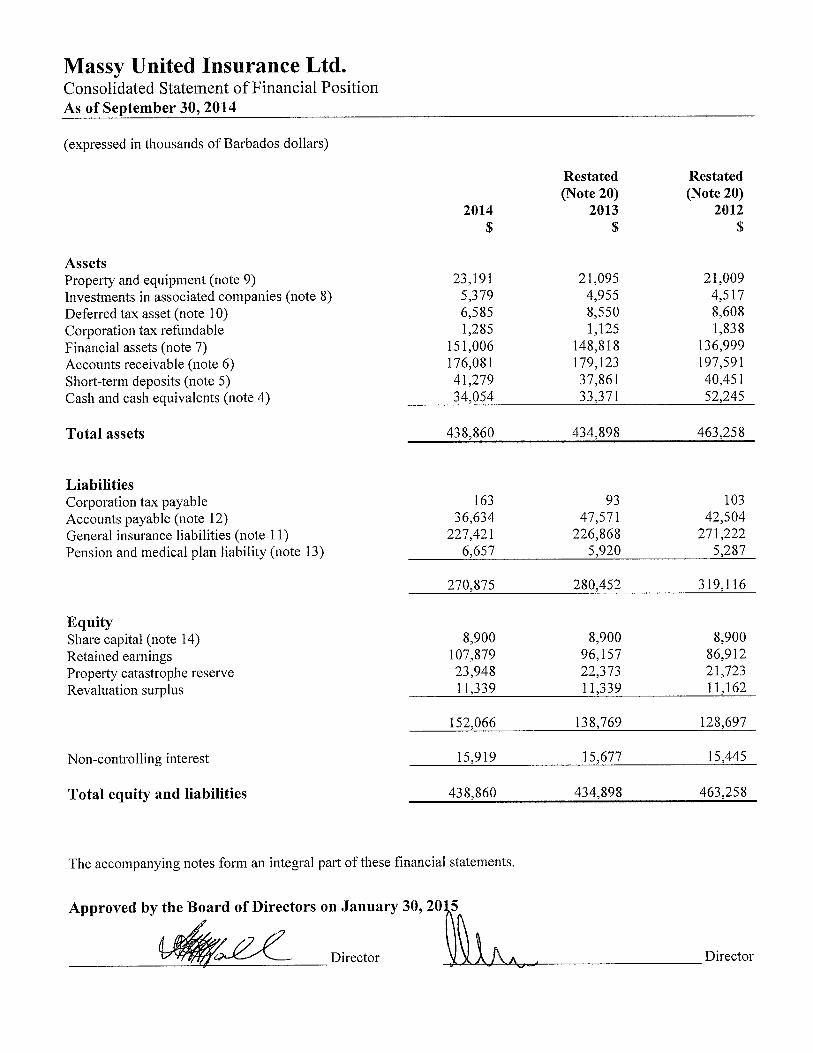

Massy United Insurance Ltd.

Consolidated Financial StatementsSeptember 30, 2014(expressed in thousands of Barbados dollars)

Massy United Insurance Ltd.Corporate Information

Directors

E. G. Warner - ChairmanD. N. O’BrienG. A. A. KingP. G. SymmondsJ. I. O’ConnellH. H. H. HallP. D. RajkumarsinghF. F. DelmasC. de Caires (appointed - February 1, 2014 - resigned - July 14, 2014)R.P. Young (resigned - October 3, 2013)

Secretary

Natalie. M. Brace

Auditor

PricewaterhouseCoopers SRL

Attorneys-at-Law

Carrington & Sealy

Bankers

CIBC FirstCaribbean International Bank

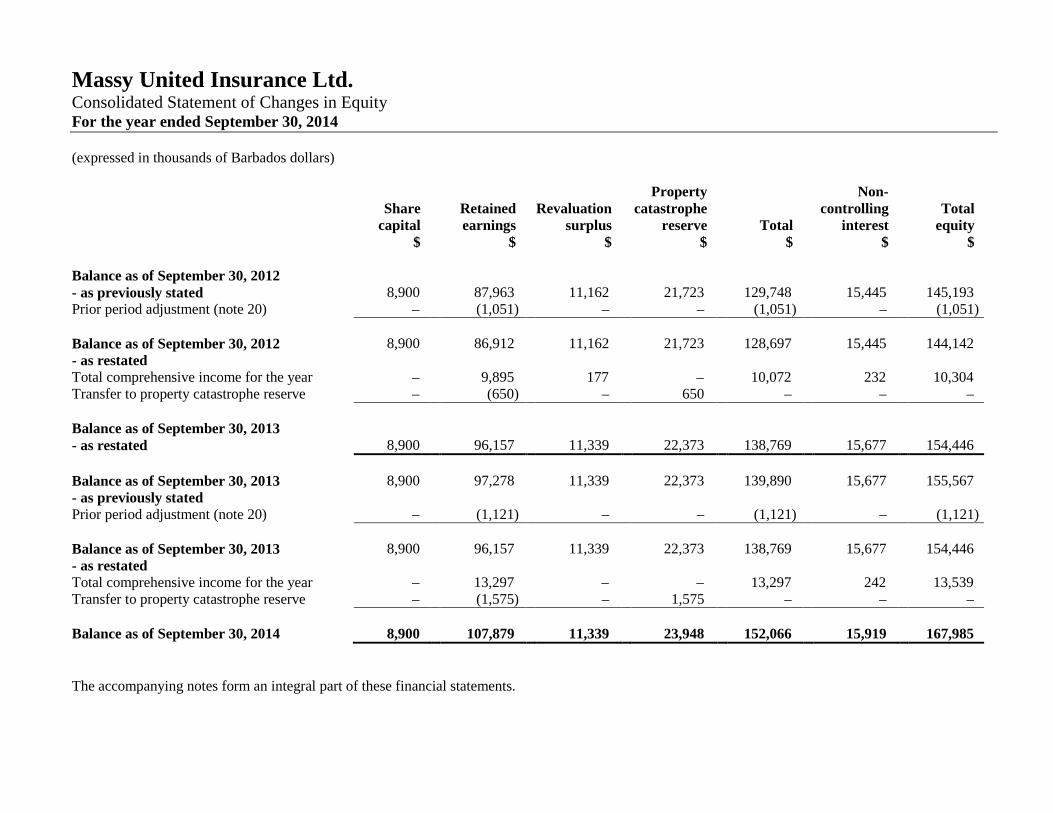

Massy United Insurance Ltd.Consolidated Statement of Changes in EquityFor the year ended September 30, 2014

(expressed in thousands of Barbados dollars)

Sharecapital

$

Retainedearnings

$

Revaluationsurplus

$

Propertycatastrophe

reserve$

Total$

Non-controlling

interest$

Totalequity

$

Balance as of September 30, 2012- as previously stated 8,900 87,963 11,162 21,723 129,748 15,445 145,193Prior period adjustment (note 20) – (1,051) – – (1,051) – (1,051)

Balance as of September 30, 2012 8,900 86,912 11,162 21,723 128,697 15,445 144,142- as restatedTotal comprehensive income for the year – 9,895 177 – 10,072 232 10,304Transfer to property catastrophe reserve – (650) – 650 – – –

Balance as of September 30, 2013- as restated 8,900 96,157 11,339 22,373 138,769 15,677 154,446

Balance as of September 30, 2013 8,900 97,278 11,339 22,373 139,890 15,677 155,567- as previously statedPrior period adjustment (note 20) – (1,121) – – (1,121) – (1,121)

Balance as of September 30, 2013 8,900 96,157 11,339 22,373 138,769 15,677 154,446- as restatedTotal comprehensive income for the year – 13,297 – – 13,297 242 13,539Transfer to property catastrophe reserve – (1,575) – 1,575 – – –

Balance as of September 30, 2014 8,900 107,879 11,339 23,948 152,066 15,919 167,985

The accompanying notes form an integral part of these financial statements.

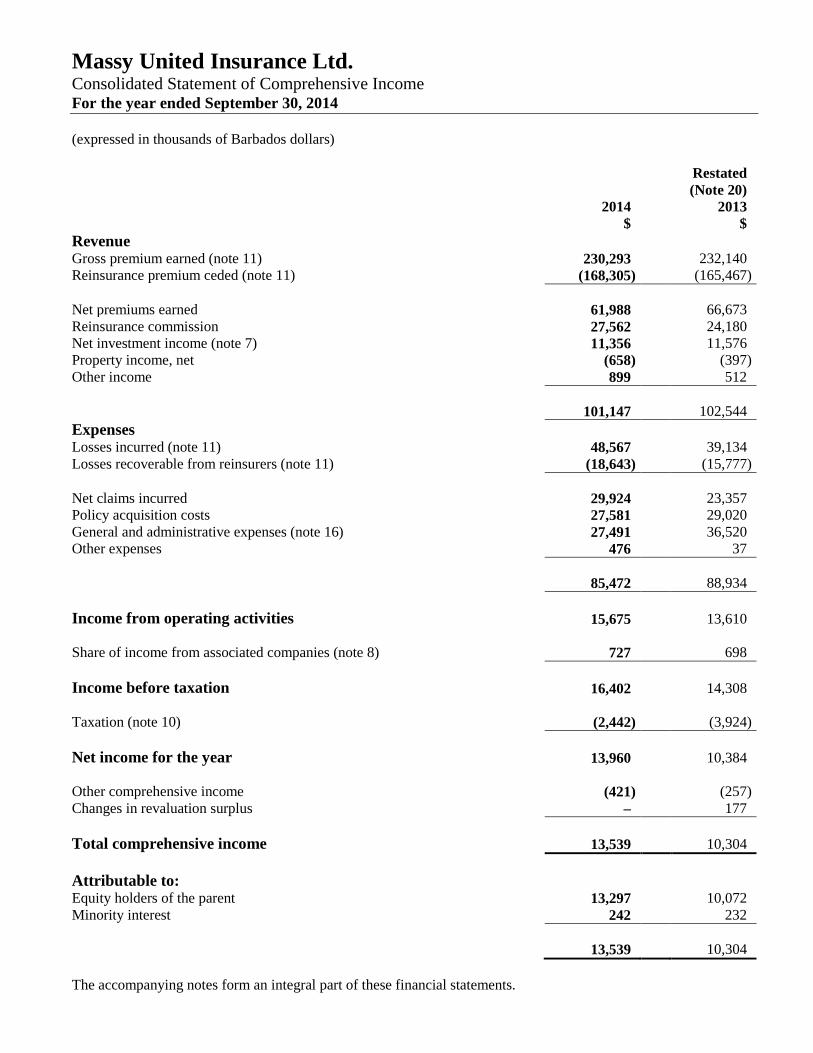

Massy United Insurance Ltd.Consolidated Statement of Comprehensive IncomeFor the year ended September 30, 2014

(expressed in thousands of Barbados dollars)

2014$

Restated(Note 20)

2013$

RevenueGross premium earned (note 11) 230,293 232,140Reinsurance premium ceded (note 11) (168,305) (165,467)

Net premiums earned 61,988 66,673Reinsurance commission 27,562 24,180Net investment income (note 7) 11,356 11,576Property income, net (658) (397)Other income 899 512

101,147 102,544

ExpensesLosses incurred (note 11) 48,567 39,134Losses recoverable from reinsurers (note 11) (18,643) (15,777)

Net claims incurred 29,924 23,357Policy acquisition costs 27,581 29,020General and administrative expenses (note 16) 27,491 36,520Other expenses 476 37

85,472 88,934

Income from operating activities 15,675 13,610

Share of income from associated companies (note 8) 727 698

Income before taxation 16,402 14,308

Taxation (note 10) (2,442) (3,924)

Net income for the year 13,960 10,384

Other comprehensive income (421) (257)Changes in revaluation surplus – 177

Total comprehensive income 13,539 10,304

Attributable to:Equity holders of the parent 13,297 10,072Minority interest 242 232

13,539 10,304

The accompanying notes form an integral part of these financial statements.

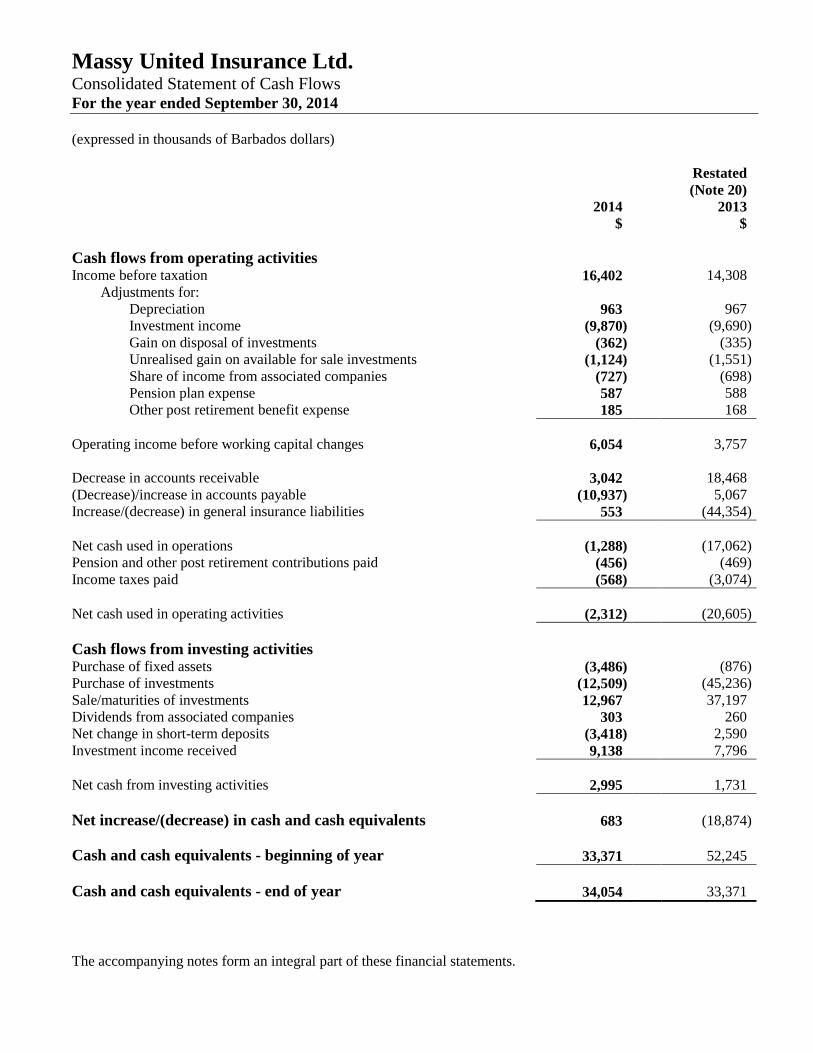

Massy United Insurance Ltd.Consolidated Statement of Cash FlowsFor the year ended September 30, 2014

(expressed in thousands of Barbados dollars)

2014$

Restated(Note 20)

2013$

Cash flows from operating activitiesIncome before taxation 16,402 14,308

Adjustments for:Depreciation 963 967Investment income (9,870) (9,690)Gain on disposal of investments (362) (335)Unrealised gain on available for sale investments (1,124) (1,551)Share of income from associated companies (727) (698)Pension plan expense 587 588Other post retirement benefit expense 185 168

Operating income before working capital changes 6,054 3,757

Decrease in accounts receivable 3,042 18,468(Decrease)/increase in accounts payable (10,937) 5,067Increase/(decrease) in general insurance liabilities 553 (44,354)

Net cash used in operations (1,288) (17,062)Pension and other post retirement contributions paid (456) (469)Income taxes paid (568) (3,074)

Net cash used in operating activities (2,312) (20,605)

Cash flows from investing activitiesPurchase of fixed assets (3,486) (876)Purchase of investments (12,509) (45,236)Sale/maturities of investments 12,967 37,197Dividends from associated companies 303 260Net change in short-term deposits (3,418) 2,590Investment income received 9,138 7,796

Net cash from investing activities 2,995 1,731

Net increase/(decrease) in cash and cash equivalents 683 (18,874)

Cash and cash equivalents - beginning of year 33,371 52,245

Cash and cash equivalents - end of year 34,054 33,371

The accompanying notes form an integral part of these financial statements.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(1)

1 Incorporation, ownership and registered office

Massy United Insurance Ltd. is incorporated under the laws of Barbados, with its registered office located atThe AutoDome, Warrens, St. Michael. The principal activities of the Company and its subsidiaries (“theGroup”) are primary insurance, reinsurance and management services. The name of the Company was changedfrom United Insurance Company Limited to Massy United Insurance Ltd. on June 27, 2014.

The Company is a subsidiary of Massy (Barbados) Limited, the ultimate parent being Massy Holdings Ltd., aCompany incorporated in Trinidad and Tobago.

The Board of Directors have the power to amend the financial statements after the date of issue.

2 Summary of significant accounting policies

a) Basis of preparation

The consolidated financial statements have been prepared on a historical cost basis, except for land andbuildings and financial assets classified as fair value through profit or loss which are measured at fairvalue.

These financial statements have been prepared in accordance with International Financial ReportingStandards ("IFRS"). The preparation of financial statements in accordance with IFRS requires the use ofcertain critical accounting estimates. The areas involving a higher degree of judgment or complexity orareas where assumptions and estimates are significant to the consolidated financial statements aredisclosed in Note 3.

Standards, and amendments and interpretations to existing standards effective in the 2014 financialyear

The following standards have been adopted by the Group in the 2014 financial year:

Revision to IAS 19 Employee benefits. The changes on the Group’s accounting policies has been asfollows: to immediately recognise all past service costs; and to replace interest cost and expected return onplan assets with a net interest amount that is calculated by applying the discount rate to the net definedbenefit liability (asset). See note 20 for the impact on the financial statements.

IFRS 12 Disclosures of interests in other entities - includes the disclosure requirements for all forms ofinterests in other entities, including joint arrangements, associates, structured entities and other off balancesheet vehicles.

IFRS 13 Fair value measurement - aims to improve consistency and reduce complexity by providing aprecise definition of fair value and a single source of fair value measurement and disclosure requirementsfor use across IFRSs. The requirements, which are largely aligned between IFRSs and US GAAP, do notextend the use of fair value accounting but provide guidance on how it should be applied where its use isalready required or permitted by other standards within IFRSs. This standard has no significant impact onthe Group’s financial results.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(2)

2 Summary of significant accounting policies …continued

a) Basis of preparation …continued

Standards, and amendments and interpretations to existing standards effective in the 2014 financialyear …continued

Amendment to IAS 1 Financial statement presentation regarding other comprehensive income. Themain change resulting from these amendments is a requirement for entities to group items presented inother comprehensive income on the basis of whether they are potentially reclassifiable to profit or losssubsequently.

New standards, and amendments and interpretations to published standards that are not yet effectiveand have not been early adopted

Management has reviewed the new standards, amendments and interpretations to existing standards thatare not yet effective and have determined that the following are relevant to the Group’s operations. TheGroup has not early adopted the new standards, amendments and interpretations.

Amendments to IAS 36 (effective January 1, 2014) - Impairment of assets on the recoverableamount disclosures for non-financial assets. This amendment removes certain disclosures of therecoverable amount of cash generating units which were included in IAS 36 by the issue of IFRS 13.

IFRS 9 Financial instruments (effective January 1, 2018) - addresses the classification, measurementand recognition of financial assets and financial liabilities requiring financial assets to be classified intotwo measurement categories: those measured as at fair value and those measured at amortised costdepending on the entity’s business model for managing its financial instruments and the contractual cashflow characteristics of the instrument.

IFRS 10 Consolidated financial statements - builds on existing principles by identifying the concept ofcontrol as the determining factor in whether an entity should be included within the consolidated financialstatements of the parent company. The standard provides additional guidance to assist in thedetermination of control where this is difficult to assess.

New standards and interpretations to existing standards effective in the 2014 financial year, but notrelevant

Amendment to IFRS 7 Financial instruments: Disclosures on asset and liability offsetting. Thisamendment includes new disclosures to facilitate comparison between those entities that prepare IFRSfinancial statements to those that prepare financial statements in accordance with US GAAP.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(3)

2 Summary of significant accounting policies …continued

a) Basis of preparation …continued

New standards and interpretations to existing standards effective in the 2014 financial year, but notrelevant …continued

IFRS 11 Joint arrangements - focuses on the rights and obligations of the parties to the arrangementrather than its legal form. There are two types of joint arrangements: joint operations and joint ventures.Joint operations arise where the investors have rights to the assets and obligations for the liabilities of anarrangement. A joint operator accounts for its share of the assets, liabilities, revenue and expenses. Jointventures arise where the investors have rights to the net assets of the arrangement; joint ventures areaccounted for under the equity method. Proportional consolidation of joint arrangements is no longerpermitted.

b) Consolidation

Subsidiaries are all entities over which the Group has the power to govern the financial and operatingpolicies generally accompanying a shareholding of more than one half of the voting rights. The existenceand effect of potential voting rights that are currently exercisable or convertible are considered whenassessing whether the Group controls another entity. Subsidiaries are fully consolidated from the date onwhich control is transferred to the Group. They are deconsolidated from the date that control ceases.

Inter-company transactions, balances and unrealised gains on transactions between Group companies areeliminated. Unrealised losses are also eliminated. Accounting policies of subsidiaries have been changedwhere necessary to ensure consistency with the policies adopted by the Group.

The Group consist of the following subsidiary and associated companies:

Equity Country of Incorporation

United Reinsurance ICC Inc. 100% St. LuciaUnited Insurance Management Inc. 60% BarbadosUnited Services Inc. 100% BarbadosUnited Insurance Company N.V. 100% ArubaUnited Insurance (Grenada) Co. Ltd. 20% GrenadaCSGK Finance Holdings Limited 20% Barbados

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(4)

2 Summary of significant accounting policies …continued

b) Consolidation …continued

Transactions and non-controlling interest

The Group treats transactions with non-controlling interests as transactions with equity owners of theGroup. For purchases from non-controlling interests, the difference between any consideration paid andthe relevant share acquired of the carrying value of the net assets of the subsidiary is recorded in equity.Gains or losses on disposals to minority interests are also recorded in equity.

When the Group ceases to have control or significant influence, any retained interest in the entity is re-measured to its fair value, with the change in carrying amount recognised in the statement ofcomprehensive income. The fair value is the initial carrying amount for the purposes of subsequentlyaccounting for the retained interest as an associate, joint venture or financial asset. In addition, anyamounts previously recognised in other comprehensive income in respect of that entity are accounted foras if the Group had directly disposed of the related assets or liabilities. This may mean that amountspreviously recognised in other comprehensive income are reclassified to the statement of income.

If the ownership interest in an associate is reduced but significant influence is retained, only aproportionate share of the amounts previously recognised in other comprehensive income are reclassifiedto the statement of income where appropriate.

Non-controlling interest includes $15,000 of capital issued to United Reinsurance ICC Inc. by Massy(Barbados) Limited. This capital has no voting or distribution rights.

Associates

Associates are all entities over which the Group has significant influence but not control, generallyaccompanying a shareholding between 20% and 50% of the voting rights. Investments in associates areaccounted for using the equity method of accounting and are initially recognised at cost. The Group’sinvestment in associates includes goodwill indentified on acquisition, net of accumulated impairment loss.

The Group’s share of its associates’ post-acquisition profits or losses is recognised in the statement ofcomprehensive income, and its share of post acquisition movements in other comprehensive income isrecognised in other comprehensive income. The cumulative post-acquisition movements are adjustedagainst the carrying amount of the investment. When the Group’s share of losses in an associate equals orexceeds its interest in the associate, including any other unsecured receivables, the Group does notrecognise further losses, unless it has incurred obligations or made payments on behalf of the associate.

Unrealised gains on transactions between the Group and its associates are eliminated to the extent of theGroup’s interest in the associates. Unrealised losses are also eliminated unless the transaction providesevidence of an impairment of the asset transferred. Accounting policies of associates have been changedwhere necessary to ensure consistency with the policies adopted by the Group.

Dilution gains or losses arising in investments in associates are recognised in the statement ofcomprehensive income.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(5)

2 Summary of significant accounting policies …continued

c) Cash and cash equivalents

Cash and cash equivalents comprise cash at bank and in hand and short-term deposits with an originalmaturity date of three months or less. Cash and cash equivalents are shown net of bank overdrafts wherethe right of offset exists.

d) Financial assets

The Group determines the classification of its investments at initial recognition, into the categories of fairvalue through profit and loss, held to maturity or loans and receivables.

Held to maturity

Held-to-maturity financial assets are non-derivative financial instruments with fixed or determinablepayments and fixed maturities that management has both the intent and ability to hold maturity.

Held to maturity assets are carried at amortised cost less provision for impairment.

Investments at fair value through profit or loss

Financial assets at fair value through profit or loss are so designated on acquisition where they are part of aportfolio of investments whose performance is evaluated on a fair value basis in accordance withdocumented investment strategies. For investments that are actively traded in organized financial markets,fair value is determined by reference to stock exchange quoted market prices at the close of business onthe balance sheet date.

For securities where there is no quoted market price, fair value has been estimated by management on thebasis of recent trades of the same investment or by reference to the current market value of otherinstruments with similar attributes. All marketable security transactions are recognized on the trade date.Realized and unrealized gains and losses adjustments are recorded in the income statement.

Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are notquoted in an active market.

Loans and receivables are carried at amortised cost less provision for impairment.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(6)

2 Summary of significant accounting policies …continued

e) Impairment of assets

The Group assesses at each reporting date whether there is an indication that an asset may be impaired. Ifsuch indication exists, or when annual impairment testing for an asset is required, the Group estimates theasset’s recoverable amount. An asset’s recoverable amount is the higher of fair value less costs to sell orits value in use. The recoverable amount is determined for an individual asset, unless the asset does notgenerate cash inflows that are largely independent of those from other assets.

For assets excluding goodwill, an assessment is made at each reporting date as to whether there is anyindication that previously recognized impairment losses may no longer exist or may have decreased.

If such indication exists, the Group makes an estimate of the recoverable amount. A previous impairmentloss is reversed only if there has been a change in the estimates used to determine the asset’s recoverableamount since the last impairment loss was recognized. If that is the case, the carrying amount of the assetis increased to its recoverable amount. That increased amount cannot exceed the carrying amount thatwould have been determined, net of depreciation, had no impairment loss been recognized for the asset inprior years. Such reversal is recognized in the income statement unless the asset is carried at revaluedamount, in which case the reversal is treated as a revaluation increase.

f) Derecognition of financial assets

A financial asset is derecognized when:

The rights to receive cash flows from the asset have expired; The Group retains the right to receive cash flows from the asset, but has assumed an obligation to pay

them in full without material delay to a third party under a ‘pass-through’ arrangement; The Group has transferred its rights to receive cash flows from the asset and either has transferred

substantially all the risks and rewards of the asset, or has neither transferred nor retained substantiallyall the risks and rewards of the asset, but has transferred control of the asset.

When the Group has transferred its right to receive cash flows from an asset and has neither transferrednor retained substantially all the risks and rewards of the asset nor transferred control of the asset, the assetis recognized to the extent of the Group’s continuing involvement in the asset. Continuing involvementthat takes the form of a guarantee over the transferred asset is measured at the lower of the originalcarrying amount of the asset and the maximum amount of consideration that the Group could be requiredto repay.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(7)

2 Summary of significant accounting policies …continued

g) Revenue recognition

Premium income:

Premiums written are recognized on policy inception and earned on a pro rata basis over the term of therelated policy coverage. Estimates of premiums written as at the balance sheet date but not yet received,are assessed based on estimates from underwriting or past experience and are included in premiumsearned. Premiums ceded are expensed on a pro-rata basis over the term of the respective policy.

Investment income:

Interest income is recognized in the income statement for all interest bearing instruments on an accrualbasis using the effective yield method based on the initial transaction price.

Investment income also includes dividends when the right to receive payment is established.

h) Insurance and reinsurance contracts

Insurance and reinsurance contracts are defined as those containing significant insurance risk at theinception of the contract, or those where at the inception of the contract there is a scenario withcommercial substance where the level of insurance risk may be significant. The significance of insurancerisk is dependent on both the probability of an insured event and the magnitude of its potential effect.Once a contract has been classified as an insurance contract, it remains an insurance contract for theremainder of its lifetime, even if the insurance risk reduces significantly during the period.

At each balance sheet date a liability adequacy test is performed to ensure the adequacy of insuranceliabilities. If the test indicates that the provision for claims and claims expenses is inadequate theliabilities are adjusted to correct the deficiency with the resulting charge being included in the statement ofcomprehensive income.

In the normal course of business, the Group seeks to reduce the losses to which it is exposed that maycause unfavorable underwriting results by reinsuring a certain level of risk with reinsurance companies.Reinsurance premiums are accounted for on a basis consistent with that used in accounting for the originalpolicies issued and or the terms of the reinsurance contracts. The Group may receive a ceding commissionin connection with ceded reinsurance, which is earned in a manner consistent with the premiums ceded.

Reinsurance contracts ceded do not relieve the Group from its obligations to policyholders. The Groupremains liable to its policyholders for the portion reinsured, to the extent that the reinsurers do not meet theobligations assumed under the reinsurance agreements.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(8)

2 Summary of significant accounting policies …continued

i) Unearned premium reserve

Written premiums in respect of direct insurance business and reinsurance contracts assumed are reflectedin the financial statements evenly over the terms of the insurance or reinsurance policies. Unearnedpremiums represent the unearned portion of the premiums written on policies in force at the end of theyear.

At each balance sheet date, a liability adequacy test is performed, to ensure the adequacy of unearnedpremiums net of related deferred acquisition costs. In performing the test, current best estimates of futurecontractual cash flows, claims handling and policy administration expenses, as well as investment incomefrom assets backing such liabilities, are used. Any inadequacy is immediately charged to the incomestatement by establishing an unexpired risk provision.

j) Outstanding claims reserve and property catastrophe reserve

Outstanding claims consist of estimates of the ultimate cost of claims incurred that have not been settled atthe balance sheet date, whether reported or not, together with related claims handling costs. Significantdelays may be experienced in the notification and settlement of certain types of general insurance claims,such as general liability business. Outstanding claims reserves are not discounted for the time value ofmoney.

Estimates are calculated using methods and assumptions considered to be appropriate to the circumstancesof the Group and the business undertaken. This provision, while believed to be adequate to cover theultimate cost of losses incurred, may ultimately be settled for a different amount. It is continuallyreviewed and any adjustments are recorded in operations in the period in which they are determined.

Unallocated loss adjustment expenses (ULAE) are included in the outstanding claims reserve at year end.The estimate of the reserve is arrived at by examining the overhead expenses allocated to the claimsfunction. This estimate is reviewed by the actuary annually.

The principal assumption underlying the estimates is past claims development experience. This includesassumptions in respect of average claim costs and claim numbers for each accident year. In addition,larger claims are separately assessed by loss adjusters. Judgment is used to assess the extent to whichexternal factors such as judicial decisions and government legislation affect the estimates. The ultimateliabilities will vary as a result of subsequent developments. Differences resulting from reassessment of theultimate liabilities are recognized in subsequent periods.

In addition to the above reserves, the Group transfers from its retained earnings, as permitted inSection 155 of the Insurance Act, 1996 - 32, 25% of net premium income earned arising from its propertybusiness into a reserve established to cover claims made by the Group’s policyholders arising from acatastrophic event, which is included as a separate component of equity.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(9)

2 Summary of significant accounting policies …continued

k) Amounts receivable from reinsurance companies

Amounts receivable from reinsurance companies consist primarily of amounts due in respect of cededinsurance liabilities. Recoverable amounts are estimated in a manner consistent with the outstandingclaims reserve or settled claims associated with the reinsured policies and in accordance with the relevantreinsurance contract.

If amounts receivable from reinsurance companies are impaired, the Group reduces the carrying amountaccordingly and recognizes an impairment loss in the statement of income. A reinsurance asset isimpaired if there is objective evidence that the Group may not receive all, or part, of the amounts due to itunder the terms of the reinsurance contract.

l) Deferred acquisition costs

Deferred acquisition costs, which is reflected net of unearned premium reserve on the balance sheet,relates to commissions and other costs of acquiring insurance which vary with, and are primarily relatedto, the production of new and renewal business. Acquisition costs on premiums written and reinsurancecommissions vary with and are directly related to the production of business. These costs and revenuesare deferred and recognised over the period of the policies to which they relate.

m) Currency

Functional and presentation currency

These financial statements are expressed in Barbados dollars which in the Group’s presentationalcurrency.

The results and financial position of the various agents and branches that have a functional currency otherthan the Group’s presentational currency are translated as follows:

i) Income, other comprehensive income, movements in equity and cash flows are translated at averageexchange rates for the year.

ii) Assets and liabilities are translated at the exchange rates ruling on December 31.iii) Resulting exchange differences are recognised in other comprehensive income.

Transactions and balances

Foreign currency transactions are translated into the functional currency using the exchange ratesprevailing at the date of the transactions. Foreign exchange gains and losses resulting from the settlementof such transactions and from the translation at year-end exchange rates of monetary assets and liabilitiesdenominated in foreign currencies are recognised in the statement of comprehensive income.

Translation differences on non-monetary financial assets and liabilities carried at fair value such asequities held at fair value through profit or loss are recognised as part of the fair value gain or loss in thestatement of comprehensive income.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(10)

2 Summary of significant accounting policies …continued

n) Premium and other receivables

Premium and other receivables are initially recognised at fair value and subsequently measured atamortised cost using the effective interest method, less provision for impairment. A provision forimpairment of receivables is established when there is objective evidence that the Group will not be able tocollect all amounts due according to the original terms of receivables. Significant financial difficulties ofthe debtor, probability that the debtor will enter bankruptcy or financial reorganisation, and default ordelinquency in payments are considered indicators that the trade receivable is impaired. The amount ofthe provision is the difference between the asset’s carrying amount and the present value of estimatedfuture cash flows, discounted at the effective interest rate. The amount of the provision is recognised inthe statement of income within ‘selling, general and administration expenses’.

o) Property, plant and equipment

Property, plant and equipment including freehold land and buildings are recognised initially at cost. Landand buildings are revalued periodically to reflect market conditions based on directors’ valuations takinginto consideration current replacement cost and land tax valuations, and which are reviewed forreasonableness by a qualified independent valuer.

Increases in the carrying amount arising on revaluation of land and buildings are credited to othercomprehensive income and shown as revaluation surplus in equity. Decreases that offset previousincreases of the same asset are charged as other comprehensive income and debited against revaluationsurplus directly in equity, all other decreases are charged directly to income. Any accumulateddepreciation at the date of revaluation is eliminated against the gross carrying amount of the asset, and thenet amount is restated to the revalued amount of the asset. Upon disposal, any revaluation surplus relatingto the particular asset being sold is transferred to retained earnings.

Plant and equipment is stated at cost, excluding the costs of day-to-day servicing, less any accumulateddepreciation and accumulated impairment in value. Subsequent expenditure related to repairs andmaintenance is expensed during the financial period in which they are incurred. The carrying values ofplant and equipment are reviewed for impairment when events or changes in circumstance indicate that thecarrying amount may not be recoverable. Gains and losses on disposals are computed as the differencebetween carrying amounts and proceeds received and are included in the statement of comprehensiveincome.

Depreciation is provided on buildings on a straight line basis over a period of 50 years. Depreciation ofgeneral equipment is provided on a straight-line basis at rates varying from 10% to 25% to write off thecost of the assets over their estimated useful lives.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(11)

2 Summary of significant accounting policies …continued

p) Current and deferred income tax

The current income tax charge is calculated on the basis of the tax laws enacted or substantively enacted atthe balance sheet date in the countries where the Group operates and generates taxable income.

Deferred income tax is provided in full, using the liability method, on temporary differences arisingbetween the tax bases of assets and liabilities and their carrying amounts in the financial statements.Deferred income tax is determined using tax rates (and laws) that have been enacted or substantiallyenacted by the balance sheet date and are expected to apply when the related deferred income tax asset isrealised or the deferred income tax liability is settled.

The principal temporary differences arise from depreciation on property, plant and equipment and taxlosses carried forward. Deferred tax assets relating to the carry forward of unused tax losses arerecognised to the extent that it is probable that future taxable profit will be earned against which theunused tax losses can be utilised.

q) Pension plan

Pension obligations

The Group’s pension scheme is generally funded through payments to insurance companies or trustee-administered funds, determined by periodic actuarial calculations. The Group has both defined benefit anddefined contribution plans. A defined contribution plan is a pension plan under which the Group paysfixed contributions into a separate entity. The Group has no legal or constructive obligations to payfurther contributions if the fund does not hold sufficient assets to pay all employees the benefits relating toemployee service in the current and prior periods. A defined benefit plan is a pension plan that is not adefined contribution plan. Typically defined benefit plans define an amount of pension benefit that anemployee will receive on retirement, usually dependent on one or more factors such as age, years ofservice and compensation.

Defined benefit plans define an amount of pension benefit that an employee will receive on retirement,usually dependent on one or more factors such as age, years of service and compensation. The liabilityrecognised in the consolidated statement of financial position in respect of defined benefit pension plans isthe present value of the defined benefit obligation at the consolidated financial statement date less the fairvalue of plan assets. The defined benefit obligation is calculated annually by independent actuaries usingthe projected unit credit method. The present value of the defined benefit obligation is determined bydiscounting the estimated future cash outflows using interest rates of long-term government securities thatare denominated in the currency in which the benefit will be paid, and that have terms to maturityapproximating the terms of the related pension liability. All actuarial gains and losses arising fromexperience adjustments and changes in actuarial assumptions are charged or credited to equity in othercomprehensive income in the period in which they arise. Past service costs are recognised immediately inthe consolidated statement of income.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(12)

2 Summary of significant accounting policies …continued

q) Pension plan …continued

Pension obligations …continued

For defined contribution plans, the Group pays contributions to administered pension insurance plans. TheGroup has no further payment obligations once the contributions have been paid. The contributions arerecognised as employee benefit expense when they are due. Prepaid contributions are recognised as anasset to the extent that a cash refund or a reduction in the future payments is available.

Other post-employment obligations

The Group provides post-retirement healthcare benefits through the Massy Barbados Medical Scheme totheir retirees and registered dependants. The entitlement to these benefits is usually conditional on theemployee remaining in service up to retirement age and the completion of a minimum service period. Theexpected costs of these benefits are accrued over the period of employment using the same accountingmethodology as used for defined benefit pension plans. Actuarial gains and losses arising from experienceadjustments and changes in actuarial assumptions are charged or credited to the statement ofcomprehensive income in the period in which they arise. These obligations are valued by independentqualified actuaries.

Bonus plans

The Group recognises a liability and an expense for bonuses when at least one of the following conditionsis met:

There is a formal plan and the amounts to be paid are determined before the time of issuing thefinancial statements; or

Past practice has created a valid expectation by employees that they will receive a bonus and theamount can be determined before the time of issuing the financial statements.

Liabilities for bonus plans are expected to be settled within 12 months and are measured at the amountsexpected to be paid when they are settled.

r) Leases

Leases in which a significant portion of the risks and rewards of ownership are retained by the lessor areclassified as operating leases. Payments made under operating leases (net of any incentives received fromthe lessor) are charged to the statement of comprehensive income on a straight line basis over the period ofthe lease.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(13)

2 Summary of significant accounting policies …continued

s) Dividend distributions

Dividend distributions on the Group’s common shares are recorded in the period in which the directorsapproved the declaration of the dividend.

t) Provisions

Provisions are recognised when: the Group has a present legal or constructive obligation as a result of pastevents; it is more likely than not that an outflow of resources will be required to settle the obligation; andthe amount has been reliably estimated. Provisions are not recognised for future operating losses.

Where there are a number of similar obligations, the likelihood that an outflow will be required insettlement is determined by considering the class of obligations as a whole. A provision is recognisedeven if the likelihood of an outflow with respect to any one item included in the same class of obligationsmay be small.

Provisions are measured at the present value of the expenditures expected to be required to settle theobligation using a pre-tax rate that reflects current market assessments of the time value of money and therisks specific to the obligation. The increase in the provision due to passage of time is recognised asinterest expense.

3 Significant accounting judgments, estimates and assumptions

The preparation of the Group’s financial statements requires management to make judgments, estimates andassumptions that affect the reported amounts of revenues, expenses, assets and liabilities, and the disclosure ofcontingent liabilities, at the reporting date. However, uncertainty about these assumptions and estimates couldresult in outcomes that could require a material adjustment to the carrying amount of the asset or liabilityaffected in the future.

Liabilities on insurance contracts

The estimation of the ultimate liability arising from claims made under insurance contracts is a criticalaccounting estimate. There are several sources of uncertainty that need to be considered in the estimate of theliability that the Group will ultimately pay for such claims.

Claim liabilities are based on estimates due to the fact that the ultimate disposition of claims incurred prior tothe date of the financial statements, whether reported or not, is subject to the outcome of events that may notyet have occurred. The estimated cost of claims include direct expenses to be incurred in settling claims, net ofthe expected subrogation value and other recoveries. Significant delays are experienced in the notification andsettlement of certain types of claims, particularly in respect of casualty contracts. Events which may affect theultimate outcome of claims include inter alia, jury decisions, court interpretations, legislative changes andchanges in the medical condition of claimants.

Management engages an independent actuary to assist in the computation of the estimate of claim liabilities.The ultimate liability arising from claims may be mitigated by recovery arising from reinsurance contracts held.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(14)

3 Significant accounting judgements, estimates and assumptions …continued

Post- retirement benefits

The cost of the defined benefit pension plan and other post employment medical benefits is determined usingactuarial valuations. These actuarial valuations involve making assumptions about discount rates, expectedrates of return on assets of the plan, future pension increases, future salary increases, proportion of employeesopting for early retirement, future changes in the NIS ceiling and inflation. Due to the long-term nature of theplan, such estimates are subject to significant uncertainty. Assumptions used are disclosed in Note 13.

Revaluation of property, plant and equipment

The Group carries its land and buildings at fair value, with changes in fair value being recognized in othercomprehensive income. The Group utilizes independent valuers, but the nature of the process is such that it issubject to significant judgment, for example through the use of valuation techniques where there is a lack ofcomparable market data.

4 Cash and cash equivalents

2014$

2013$

Cash on hand 69 22Cash at bank 33,985 33,349

34,054 33,371

The cash and short-term deposits with an original maturity of less than 90 days earned interest at varying ratesbetween 0.05% and 2.0% (2013 - 0.05% and 2.00%) per annum.

The cash and short-term deposits are held across countries in which the Group conducts its business.

5 Short-term deposits

The majority of these deposits mature after 90 days, and within one year of the financial statement date, exceptfor a few held as statutory deposits which have maturity dates more than one year but less than three years. Theinterest rates on these deposits ranged from 0.20% and 5.50% (2013 - 0.20% to 5.50%) per annum.

The Group’s deposits are held at financial institutions throughout the Caribbean region.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(15)

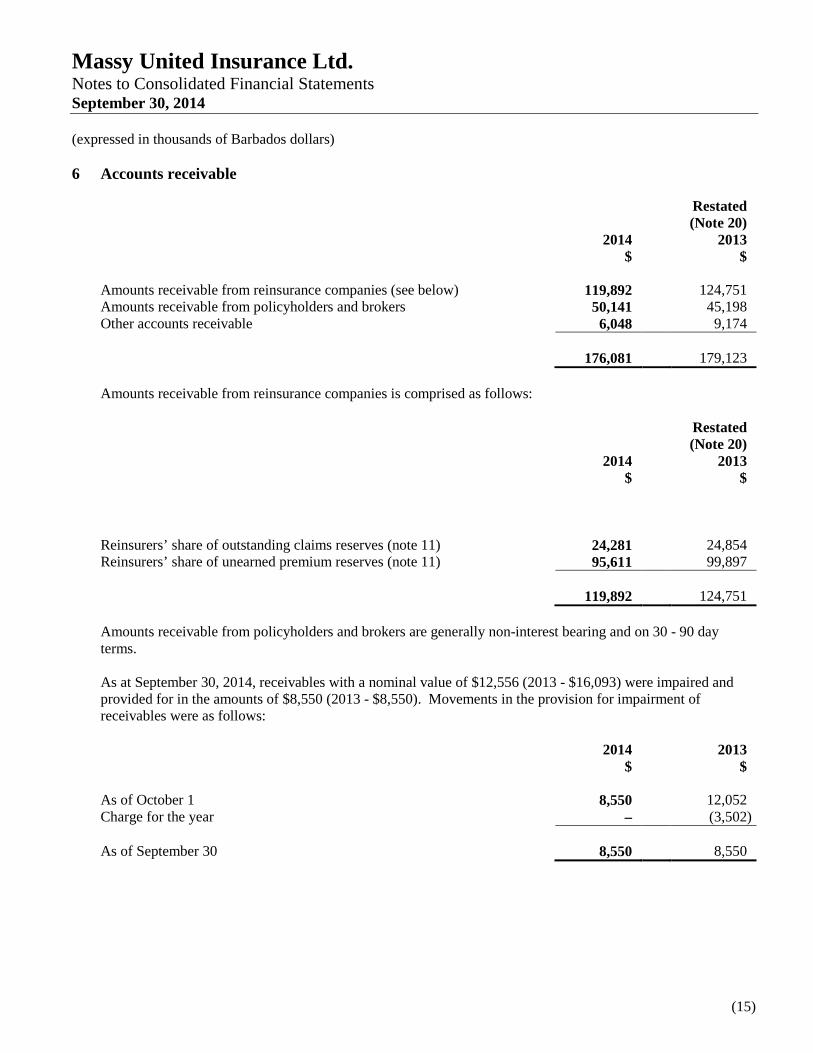

6 Accounts receivable

2014$

Restated(Note 20)

2013$

Amounts receivable from reinsurance companies (see below) 119,892 124,751Amounts receivable from policyholders and brokers 50,141 45,198Other accounts receivable 6,048 9,174

176,081 179,123

Amounts receivable from reinsurance companies is comprised as follows:

2014$

Restated(Note 20)

2013$

Reinsurers’ share of outstanding claims reserves (note 11) 24,281 24,854Reinsurers’ share of unearned premium reserves (note 11) 95,611 99,897

119,892 124,751

Amounts receivable from policyholders and brokers are generally non-interest bearing and on 30 - 90 dayterms.

As at September 30, 2014, receivables with a nominal value of $12,556 (2013 - $16,093) were impaired andprovided for in the amounts of $8,550 (2013 - $8,550). Movements in the provision for impairment ofreceivables were as follows:

2014$

2013$

As of October 1 8,550 12,052Charge for the year – (3,502)

As of September 30 8,550 8,550

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(16)

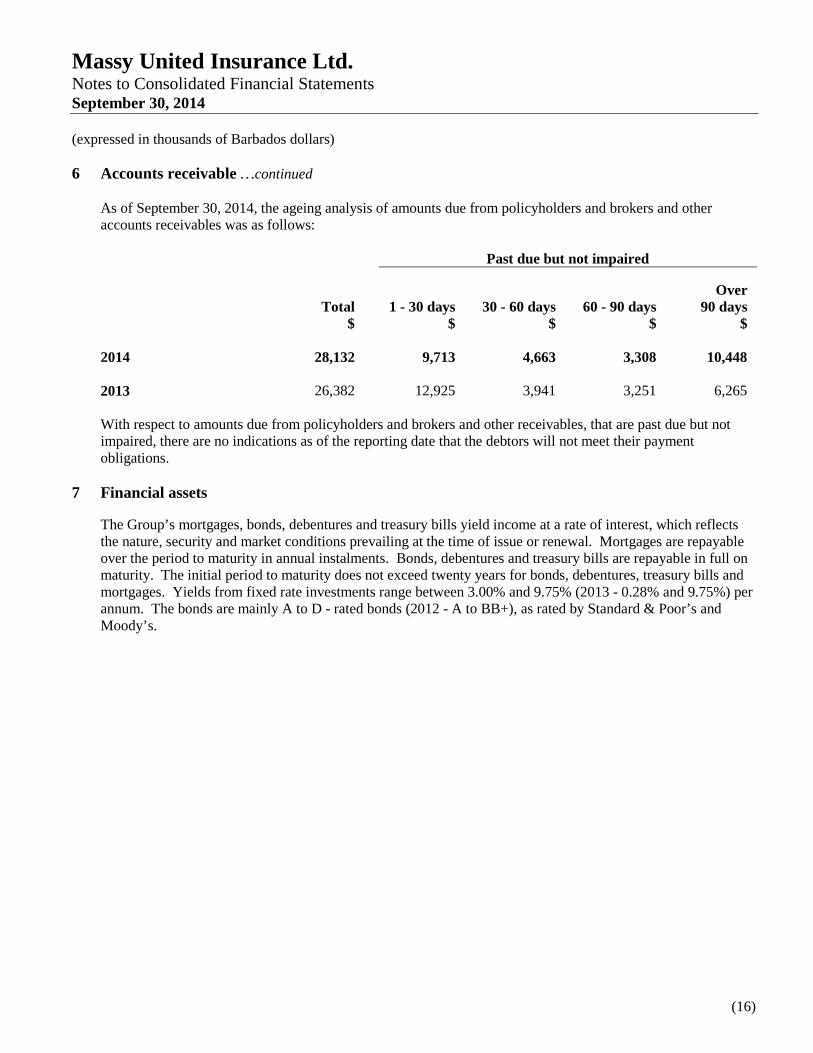

6 Accounts receivable …continued

As of September 30, 2014, the ageing analysis of amounts due from policyholders and brokers and otheraccounts receivables was as follows:

Past due but not impaired

Total$

1 - 30 days$

30 - 60 days$

60 - 90 days$

Over90 days

$

2014 28,132 9,713 4,663 3,308 10,448

2013 26,382 12,925 3,941 3,251 6,265

With respect to amounts due from policyholders and brokers and other receivables, that are past due but notimpaired, there are no indications as of the reporting date that the debtors will not meet their paymentobligations.

7 Financial assets

The Group’s mortgages, bonds, debentures and treasury bills yield income at a rate of interest, which reflectsthe nature, security and market conditions prevailing at the time of issue or renewal. Mortgages are repayableover the period to maturity in annual instalments. Bonds, debentures and treasury bills are repayable in full onmaturity. The initial period to maturity does not exceed twenty years for bonds, debentures, treasury bills andmortgages. Yields from fixed rate investments range between 3.00% and 9.75% (2013 - 0.28% and 9.75%) perannum. The bonds are mainly A to D - rated bonds (2012 - A to BB+), as rated by Standard & Poor’s andMoody’s.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(17)

7 Financial assets …continued

Investments are comprised as follows:

Carryingvalue

$Fair value

$

September 30, 2014

Fair value through income statement:Marketable securities 38,337 38,337

Loans and receivables:Government debentures, guaranteed bonds, deposits,treasury bills and notes 90,754 110,956Corporate bonds and debentures 12,341 14,890Mortgage loans 2,796 2,796

105,891 128,642Held to maturity:

Corporate bonds and debentures 1,657 1,694

Accrued interest 5,121 5,121

151,006 173,794

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(18)

7 Financial assets …continued

Investments are comprised as follows:

Carryingvalue

$Fair value

$

September 30, 2013

Fair value through income statement:Marketable securities 36,505 36,505

Loans and receivables:Government debentures, guaranteed bonds, deposits, 89,107 92,533treasury bills and notesCorporate bonds and debentures 12,447 12,483Mortgage loans 2,954 2,954

104,508 107,970Held to maturity:

Government debentures, guaranteed bonds, deposits,treasury bills and notes 802 825Corporate bonds and debentures 2,250 2,362

3,052 3,187

Accrued interest 4,753 4,753

148,818 152,415

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(19)

7 Financial assets …continued

Effectiveyield

Current$

1 to 5years

$

Over 5years

$Total

$

September 30, 2014

Interest bearing assets:Debentures 5.88 - 8.5% – 13,000 11,500 24,500Treasury bills, notes anddeposits 3.00 - 8.95% 12,997 5,106 10,578 28,681Bonds 3.50 - 9.75% 2,869 17,894 30,808 51,571Mortgages 6.00 - 8.50% – 371 2,425 2,796

15,866 36,371 55,311 107,548

September 30, 2013

Interest bearing assets:Debentures 5.25 - 8.50% 1,000 13,000 11,500 25,500Treasury bills, notes anddeposits 0.28 - 8.50% 7,455 13,272 10,307 31,034Bonds 4.25 - 9.75% 2,268 15,870 29,934 48,072Mortgages 6.00 - 8.50% – 393 2,561 2,954

10,723 42,535 54,302 107,560

Investment income is comprised as follows:

2014$

2013$

Interest on deposits 1,285 1,345Interest on bonds, debentures and notes 7,375 6,993Interest on mortgages 191 186Interest on term payments for premium policies 687 797Dividends received 125 156Bank interest 186 163Discount on debentures 21 49Impairment loss on investments – 1Unrealized gain on investments 1,124 1,551Realised gain/ (loss) on disposal of investments 362 335

11,356 11,576

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(20)

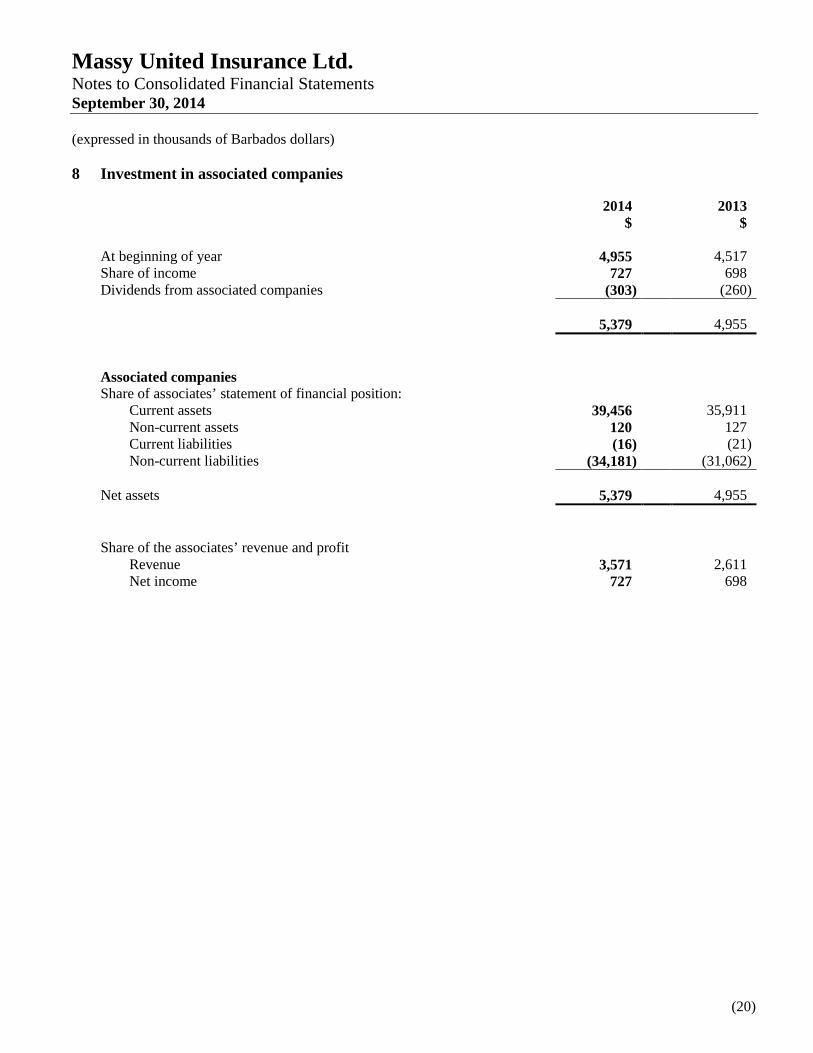

8 Investment in associated companies

2014$

2013$

At beginning of year 4,955 4,517Share of income 727 698Dividends from associated companies (303) (260)

5,379 4,955

Associated companiesShare of associates’ statement of financial position:

Current assets 39,456 35,911Non-current assets 120 127Current liabilities (16) (21)Non-current liabilities (34,181) (31,062)

Net assets 5,379 4,955

Share of the associates’ revenue and profitRevenue 3,571 2,611Net income 727 698

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(21)

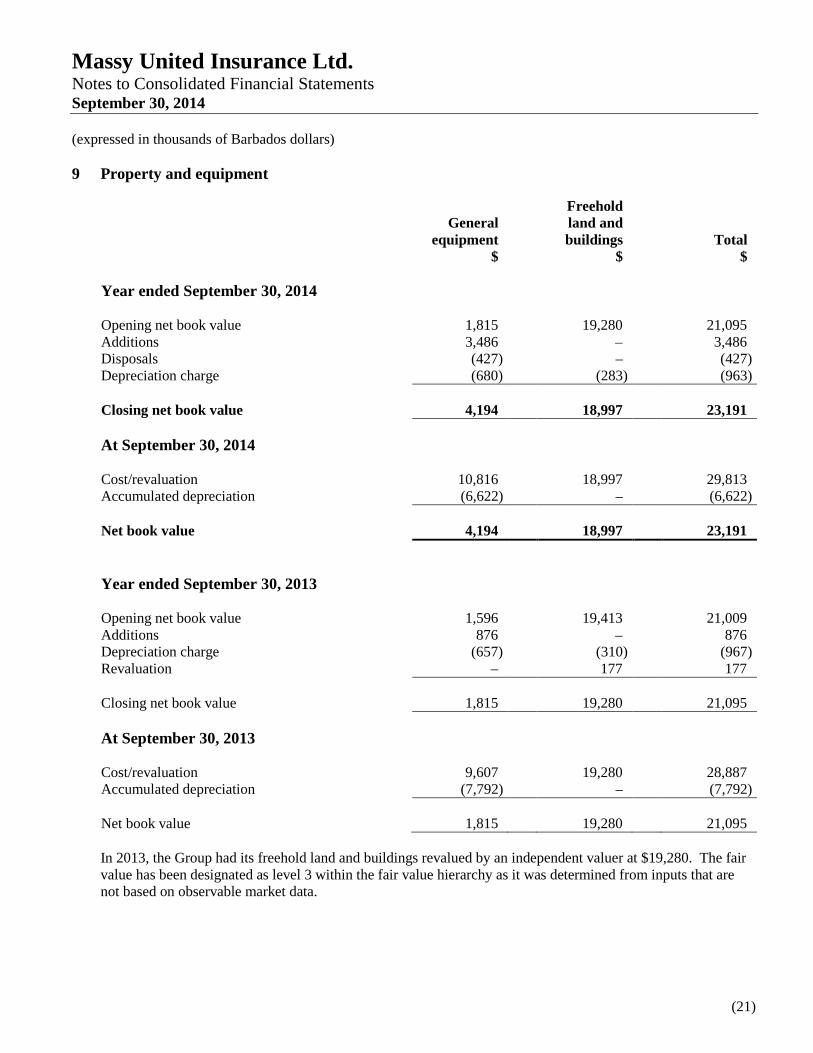

9 Property and equipment

Generalequipment

$

Freeholdland andbuildings

$Total

$

Year ended September 30, 2014

Opening net book value 1,815 19,280 21,095Additions 3,486 – 3,486Disposals (427) – (427)Depreciation charge (680) (283) (963)

Closing net book value 4,194 18,997 23,191

At September 30, 2014

Cost/revaluation 10,816 18,997 29,813Accumulated depreciation (6,622) – (6,622)

Net book value 4,194 18,997 23,191

Year ended September 30, 2013

Opening net book value 1,596 19,413 21,009Additions 876 – 876Depreciation charge (657) (310) (967)Revaluation – 177 177

Closing net book value 1,815 19,280 21,095

At September 30, 2013

Cost/revaluation 9,607 19,280 28,887Accumulated depreciation (7,792) – (7,792)

Net book value 1,815 19,280 21,095

In 2013, the Group had its freehold land and buildings revalued by an independent valuer at $19,280. The fairvalue has been designated as level 3 within the fair value hierarchy as it was determined from inputs that arenot based on observable market data.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(22)

9 Property and equipment …continued

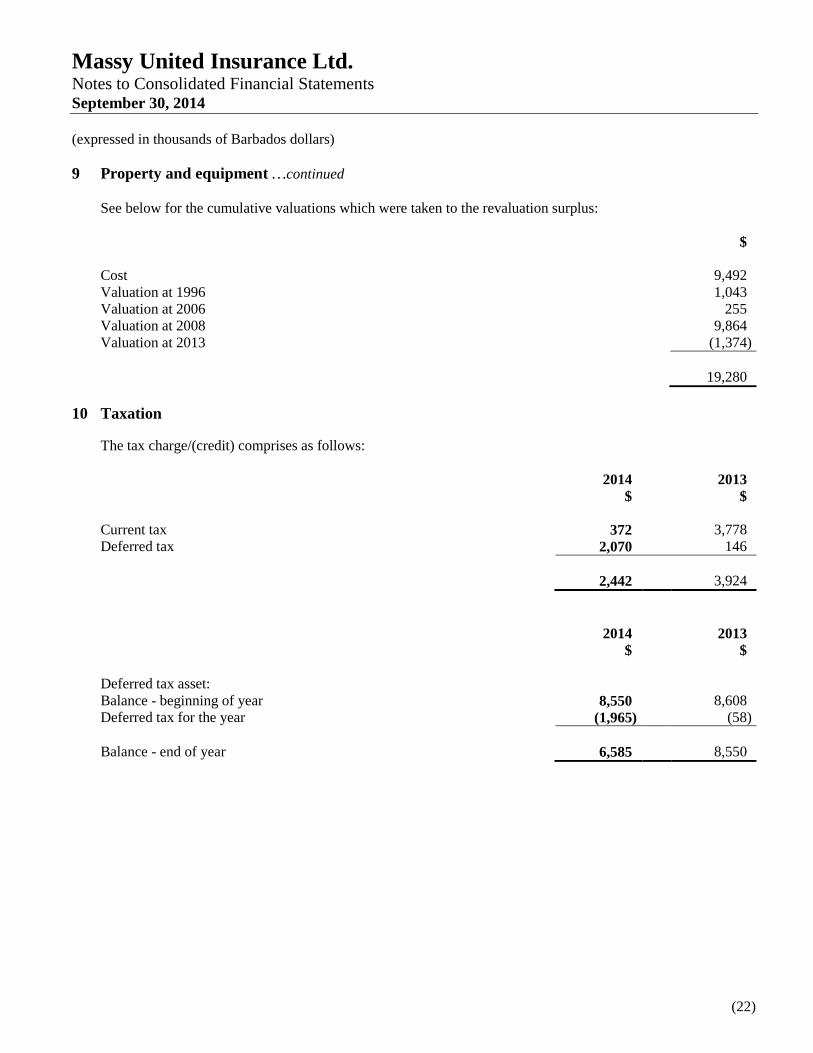

See below for the cumulative valuations which were taken to the revaluation surplus:

$

Cost 9,492Valuation at 1996 1,043Valuation at 2006 255Valuation at 2008 9,864Valuation at 2013 (1,374)

19,280

10 Taxation

The tax charge/(credit) comprises as follows:

2014$

2013$

Current tax 372 3,778Deferred tax 2,070 146

2,442 3,924

2014$

2013$

Deferred tax asset:Balance - beginning of year 8,550 8,608Deferred tax for the year (1,965) (58)

Balance - end of year 6,585 8,550

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(23)

10 Taxation …continued

The deferred tax asset comprises:

2014$

2013$

Accelerated depreciation 313 30Pension liability 1,664 1,669Provisions 502 314Unutilized tax losses 4,106 6,537

6,585 8,550

Tax losses of the Group which are available for set off against future taxable income for corporation taxpurposes are as follows:

Incomeyear

Broughtforward

$Adjustments

$Utilised

$

Carriedforward

$Expiry

date

2009 8,218 (1,744) (6,474) – 20142010 824 – (824) – 20152011 12,737 – (2,936) 9,801 20162012 6,905 (281) – 6,624 2017

28,684 (2,025) (10,234) 16,425

These losses are as computed by the Group in its corporation tax returns and have yet neither been confirmednor disputed by the Commissioner of Inland Revenue.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(24)

10 Taxation …continued

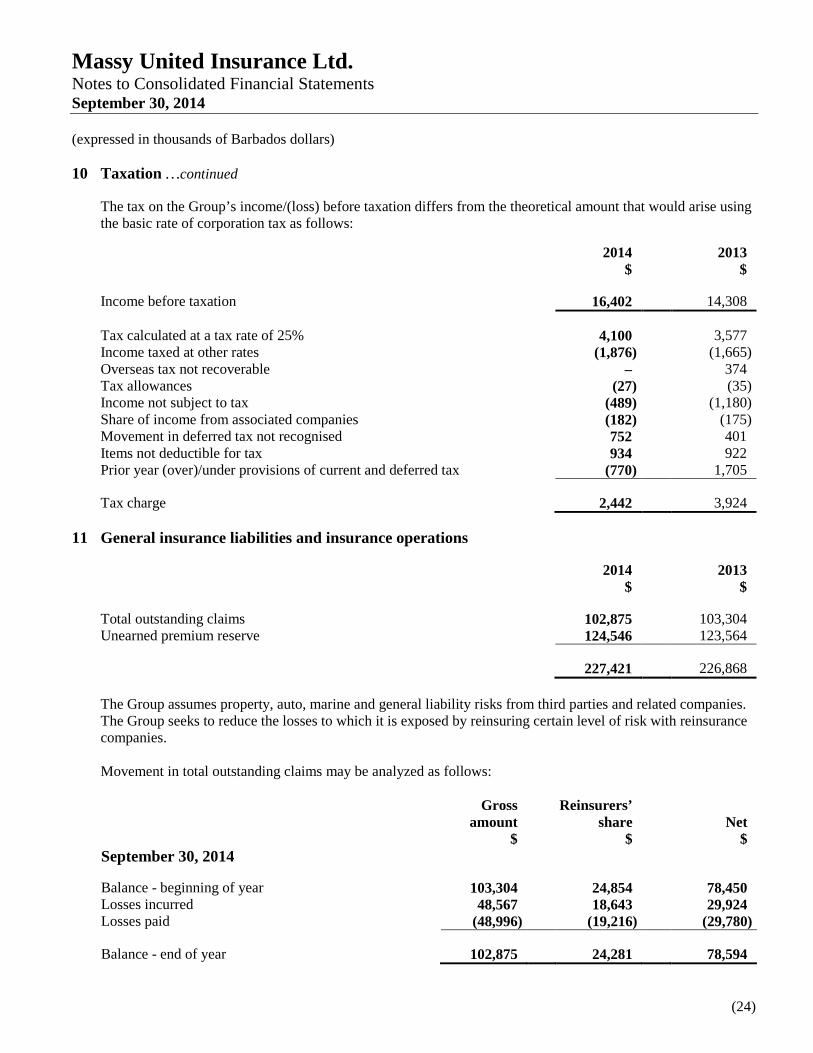

The tax on the Group’s income/(loss) before taxation differs from the theoretical amount that would arise usingthe basic rate of corporation tax as follows:

2014$

2013$

Income before taxation 16,402 14,308

Tax calculated at a tax rate of 25% 4,100 3,577Income taxed at other rates (1,876) (1,665)Overseas tax not recoverable – 374Tax allowances (27) (35)Income not subject to tax (489) (1,180)Share of income from associated companies (182) (175)Movement in deferred tax not recognised 752 401Items not deductible for tax 934 922Prior year (over)/under provisions of current and deferred tax (770) 1,705

Tax charge 2,442 3,924

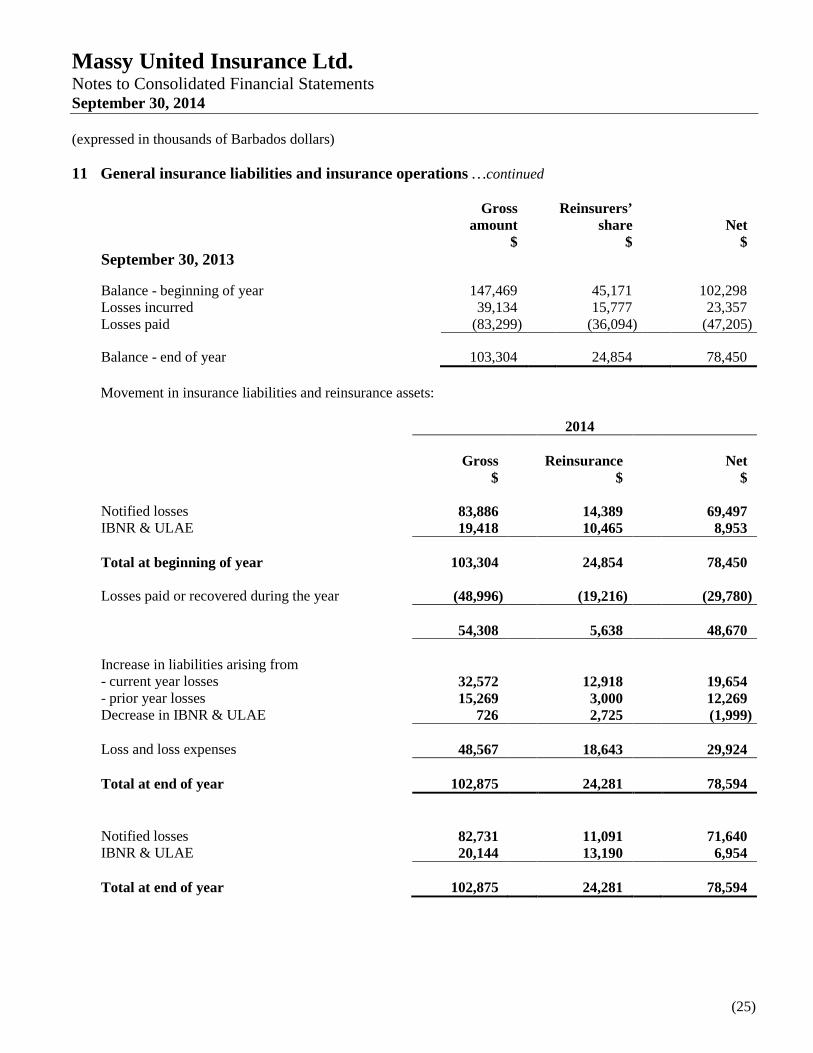

11 General insurance liabilities and insurance operations

2014$

2013$

Total outstanding claims 102,875 103,304Unearned premium reserve 124,546 123,564

227,421 226,868

The Group assumes property, auto, marine and general liability risks from third parties and related companies.The Group seeks to reduce the losses to which it is exposed by reinsuring certain level of risk with reinsurancecompanies.

Movement in total outstanding claims may be analyzed as follows:

Grossamount

$

Reinsurers’share

$Net

$September 30, 2014

Balance - beginning of year 103,304 24,854 78,450Losses incurred 48,567 18,643 29,924Losses paid (48,996) (19,216) (29,780)

Balance - end of year 102,875 24,281 78,594

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(25)

11 General insurance liabilities and insurance operations …continued

Grossamount

$

Reinsurers’share

$Net

$September 30, 2013

Balance - beginning of year 147,469 45,171 102,298Losses incurred 39,134 15,777 23,357Losses paid (83,299) (36,094) (47,205)

Balance - end of year 103,304 24,854 78,450

Movement in insurance liabilities and reinsurance assets:

2014

Gross$

Reinsurance$

Net$

Notified losses 83,886 14,389 69,497IBNR & ULAE 19,418 10,465 8,953

Total at beginning of year 103,304 24,854 78,450

Losses paid or recovered during the year (48,996) (19,216) (29,780)

54,308 5,638 48,670

Increase in liabilities arising from- current year losses 32,572 12,918 19,654- prior year losses 15,269 3,000 12,269Decrease in IBNR & ULAE 726 2,725 (1,999)

Loss and loss expenses 48,567 18,643 29,924

Total at end of year 102,875 24,281 78,594

Notified losses 82,731 11,091 71,640IBNR & ULAE 20,144 13,190 6,954

Total at end of year 102,875 24,281 78,594

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(26)

11 General insurance liabilities and insurance operations …continued

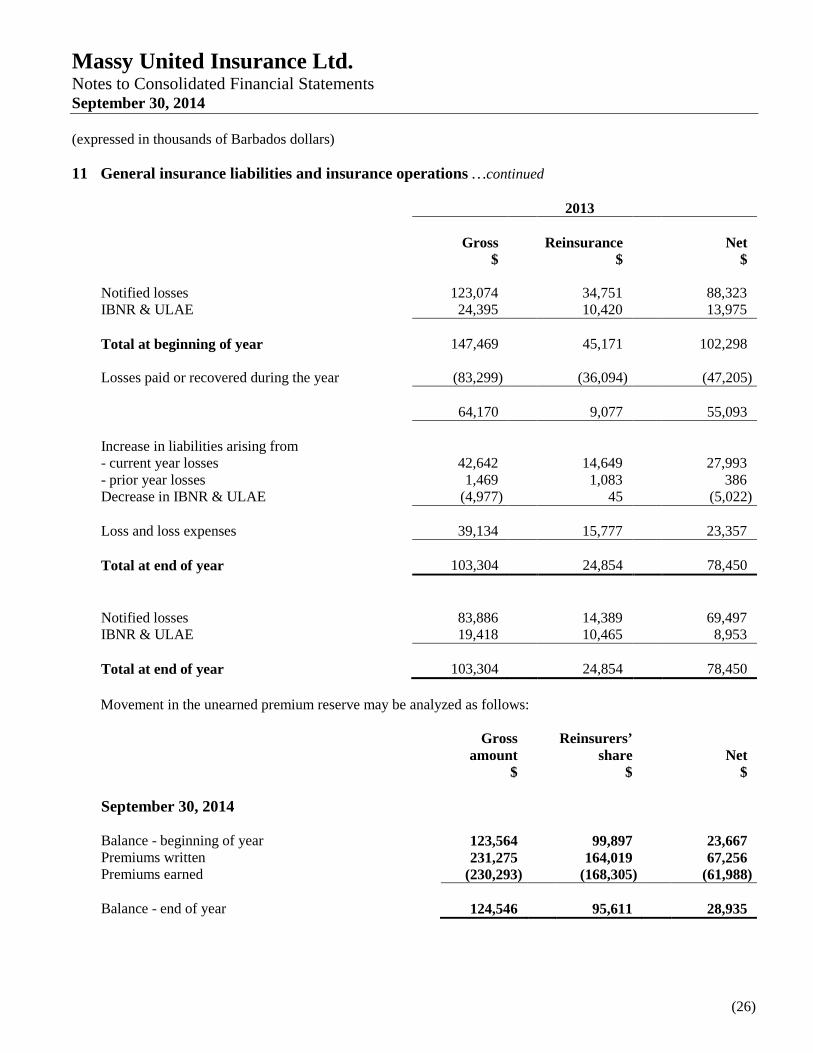

2013

Gross$

Reinsurance$

Net$

Notified losses 123,074 34,751 88,323IBNR & ULAE 24,395 10,420 13,975

Total at beginning of year 147,469 45,171 102,298

Losses paid or recovered during the year (83,299) (36,094) (47,205)

64,170 9,077 55,093

Increase in liabilities arising from- current year losses 42,642 14,649 27,993- prior year losses 1,469 1,083 386Decrease in IBNR & ULAE (4,977) 45 (5,022)

Loss and loss expenses 39,134 15,777 23,357

Total at end of year 103,304 24,854 78,450

Notified losses 83,886 14,389 69,497IBNR & ULAE 19,418 10,465 8,953

Total at end of year 103,304 24,854 78,450

Movement in the unearned premium reserve may be analyzed as follows:

Grossamount

$

Reinsurers’share

$Net

$

September 30, 2014

Balance - beginning of year 123,564 99,897 23,667Premiums written 231,275 164,019 67,256Premiums earned (230,293) (168,305) (61,988)

Balance - end of year 124,546 95,611 28,935

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(27)

11 General insurance liabilities and insurance operations …continued

Grossamount

$

Reinsurers’share

$Net

$

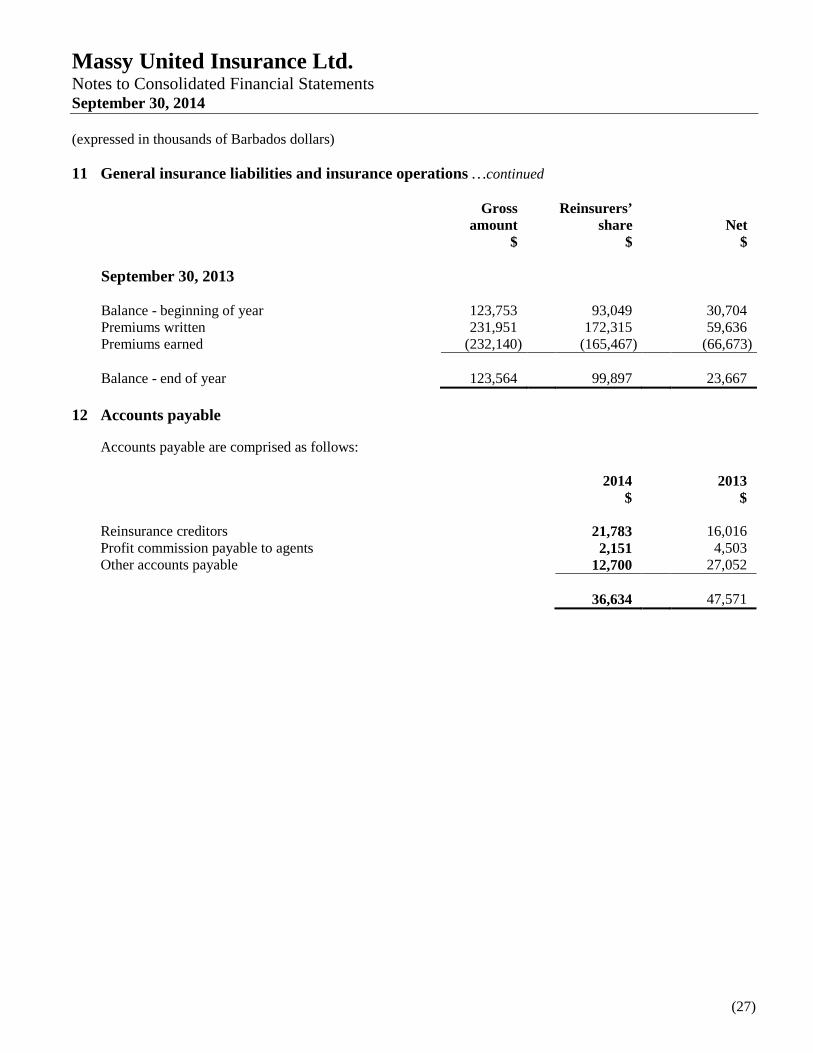

September 30, 2013

Balance - beginning of year 123,753 93,049 30,704Premiums written 231,951 172,315 59,636Premiums earned (232,140) (165,467) (66,673)

Balance - end of year 123,564 99,897 23,667

12 Accounts payable

Accounts payable are comprised as follows:

2014$

2013$

Reinsurance creditors 21,783 16,016Profit commission payable to agents 2,151 4,503Other accounts payable 12,700 27,052

36,634 47,571

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(28)

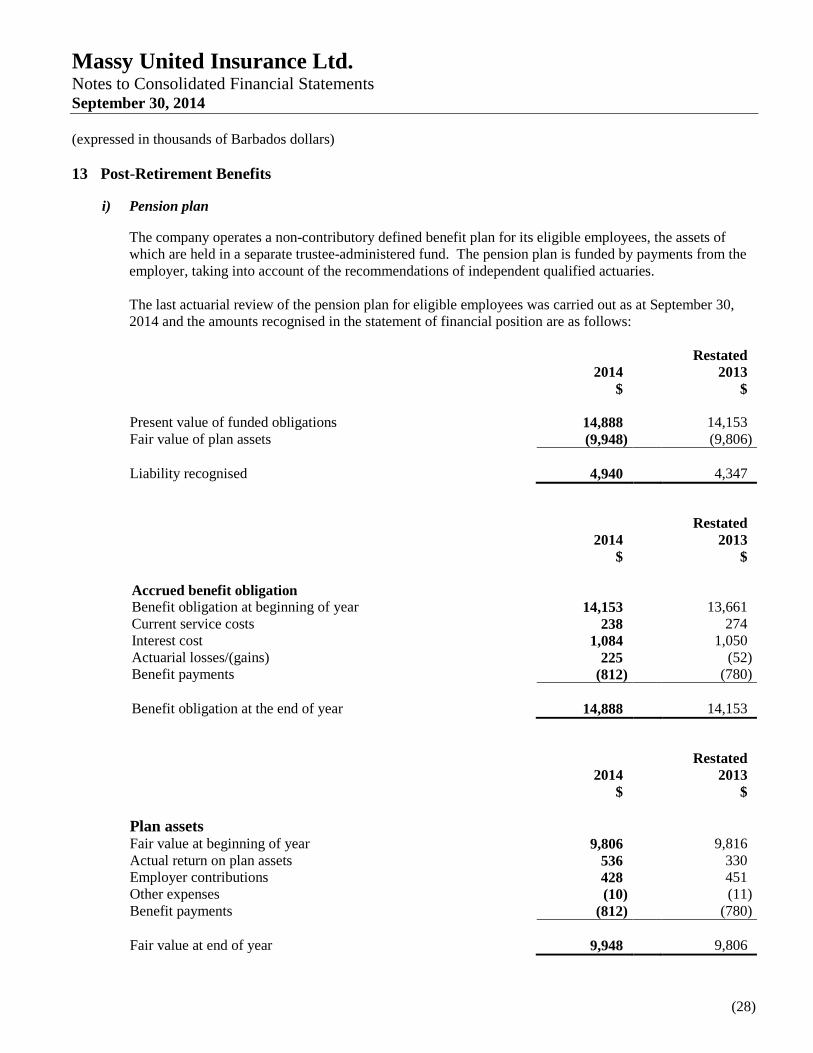

13 Post-Retirement Benefits

i) Pension plan

The company operates a non-contributory defined benefit plan for its eligible employees, the assets ofwhich are held in a separate trustee-administered fund. The pension plan is funded by payments from theemployer, taking into account of the recommendations of independent qualified actuaries.

The last actuarial review of the pension plan for eligible employees was carried out as at September 30,2014 and the amounts recognised in the statement of financial position are as follows:

2014$

Restated2013

$

Present value of funded obligations 14,888 14,153Fair value of plan assets (9,948) (9,806)

Liability recognised 4,940 4,347

2014$

Restated2013

$

Accrued benefit obligationBenefit obligation at beginning of year 14,153 13,661Current service costs 238 274Interest cost 1,084 1,050Actuarial losses/(gains) 225 (52)Benefit payments (812) (780)

Benefit obligation at the end of year 14,888 14,153

2014$

Restated2013

$

Plan assetsFair value at beginning of year 9,806 9,816Actual return on plan assets 536 330Employer contributions 428 451Other expenses (10) (11)Benefit payments (812) (780)

Fair value at end of year 9,948 9,806

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(29)

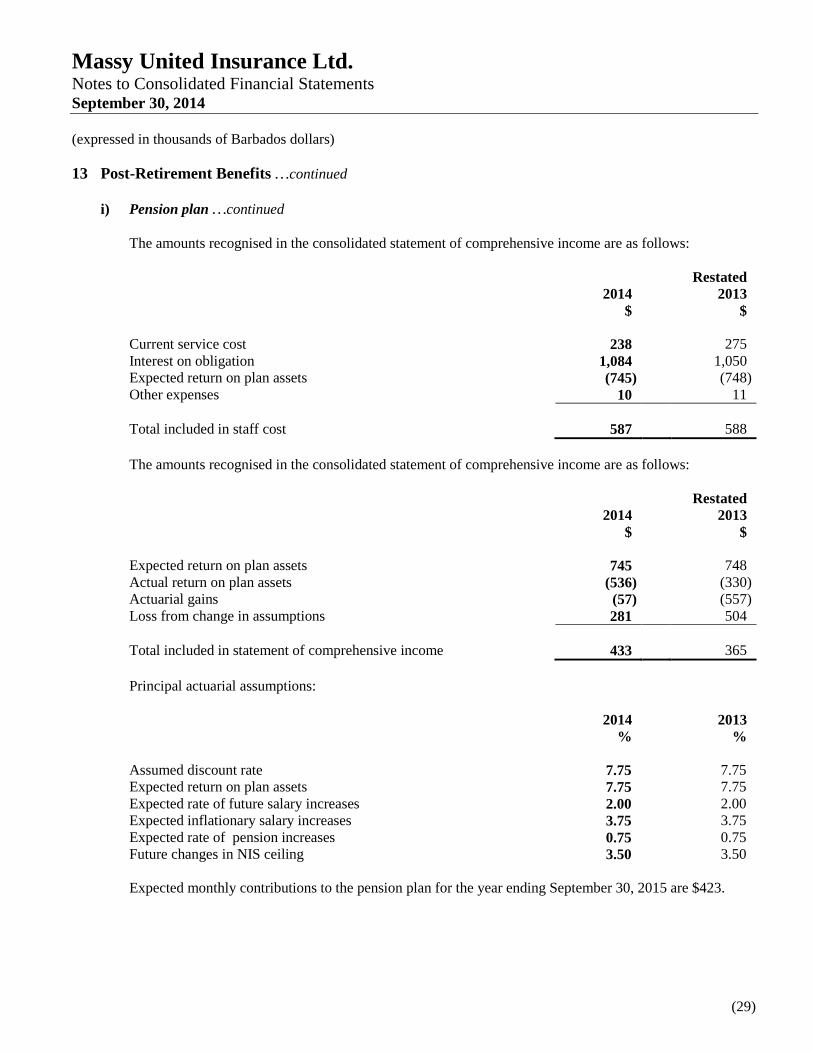

13 Post-Retirement Benefits …continued

i) Pension plan …continued

The amounts recognised in the consolidated statement of comprehensive income are as follows:

2014$

Restated2013

$

Current service cost 238 275Interest on obligation 1,084 1,050Expected return on plan assets (745) (748)Other expenses 10 11

Total included in staff cost 587 588

The amounts recognised in the consolidated statement of comprehensive income are as follows:

2014$

Restated2013

$

Expected return on plan assets 745 748Actual return on plan assets (536) (330)Actuarial gains (57) (557)Loss from change in assumptions 281 504

Total included in statement of comprehensive income 433 365

Principal actuarial assumptions:

2014%

2013%

Assumed discount rate 7.75 7.75Expected return on plan assets 7.75 7.75Expected rate of future salary increases 2.00 2.00Expected inflationary salary increases 3.75 3.75Expected rate of pension increases 0.75 0.75Future changes in NIS ceiling 3.50 3.50

Expected monthly contributions to the pension plan for the year ending September 30, 2015 are $423.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(30)

13 Post-Retirement Benefits …continued

i) Pension plan …continued

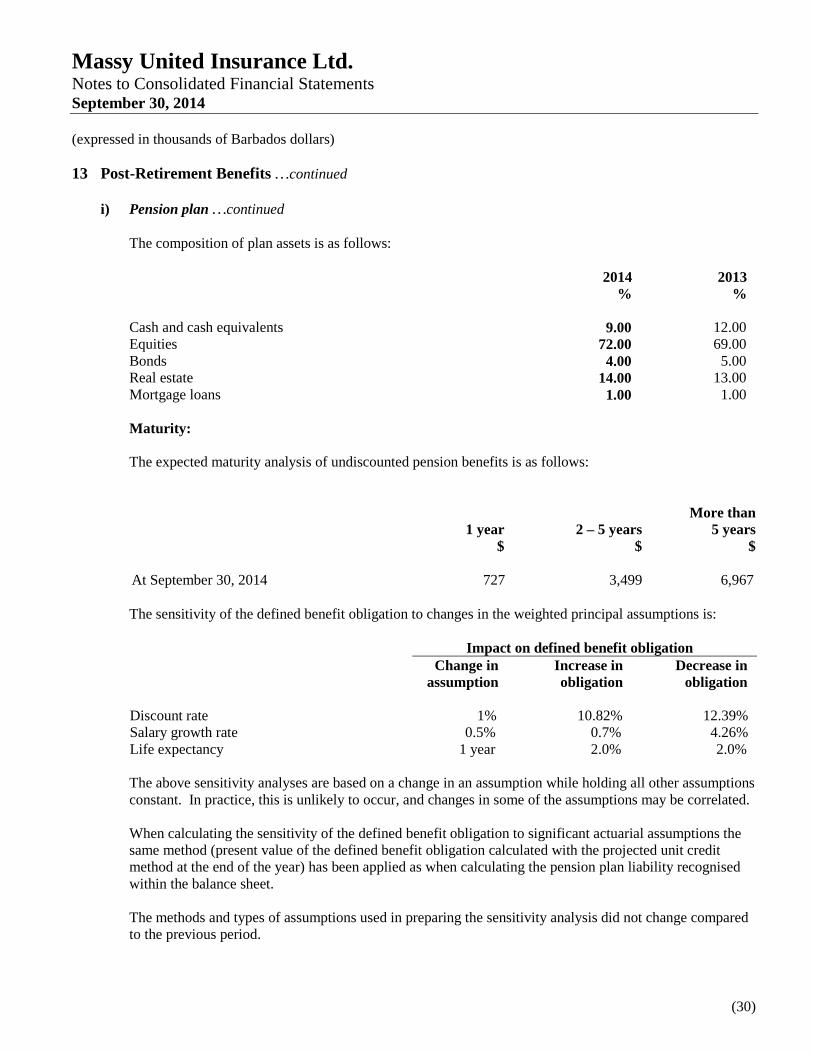

The composition of plan assets is as follows:

2014%

2013%

Cash and cash equivalents 9.00 12.00Equities 72.00 69.00Bonds 4.00 5.00Real estate 14.00 13.00Mortgage loans 1.00 1.00

Maturity:

The expected maturity analysis of undiscounted pension benefits is as follows:

1 year$

2 – 5 years$

More than5 years

$

At September 30, 2014 727 3,499 6,967

The sensitivity of the defined benefit obligation to changes in the weighted principal assumptions is:

Impact on defined benefit obligationChange in

assumptionIncrease inobligation

Decrease inobligation

Discount rate 1% 10.82% 12.39%Salary growth rate 0.5% 0.7% 4.26%Life expectancy 1 year 2.0% 2.0%

The above sensitivity analyses are based on a change in an assumption while holding all other assumptionsconstant. In practice, this is unlikely to occur, and changes in some of the assumptions may be correlated.

When calculating the sensitivity of the defined benefit obligation to significant actuarial assumptions thesame method (present value of the defined benefit obligation calculated with the projected unit creditmethod at the end of the year) has been applied as when calculating the pension plan liability recognisedwithin the balance sheet.

The methods and types of assumptions used in preparing the sensitivity analysis did not change comparedto the previous period.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(31)

13 Post-Retirement Benefits …continued

i) Pension plan …continued

Mortality:

Assumptions regarding future mortality are set based on actuarial advice in accordance with publishedstatistics and experience

At September 30, 2014, a male aged 65 retiring has a life expectancy of 19.84 years while a female aged65 retiring has a life expectancy of 22.17 years.

ii) Other Post-Retirement Benefits

The Company offers post-retirement medical benefits to its employees, pensioners and their dependants.These medical benefits are offered under a scheme, which is insured with the Company.

The last actuarial review of the medical plan for eligible employees was carried out as at September 30,2014 and the amounts recognised in the balance sheet are determined as follows:

Post retirement medical plan

2014$

Restated2013

$

Present value of funded obligations 1,717 1,573Fair value of planned assets – –

Liability recognised on balance sheet 1,717 1,573

2014$

Restated2013

$

Accrued benefit obligationBenefit obligation at beginning of year 1,573 1,443Current service cost 55 50Interest cost 125 115Past service cost 1 2Actuarial gains (12) (14)Benefit payments (25) (22)

Benefit Obligation September 30 1,717 1,573

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(32)

13 Post-Retirement Benefits …continued

ii) Other Post-Retirement Benefits …continued

2014$

Restated2013

$

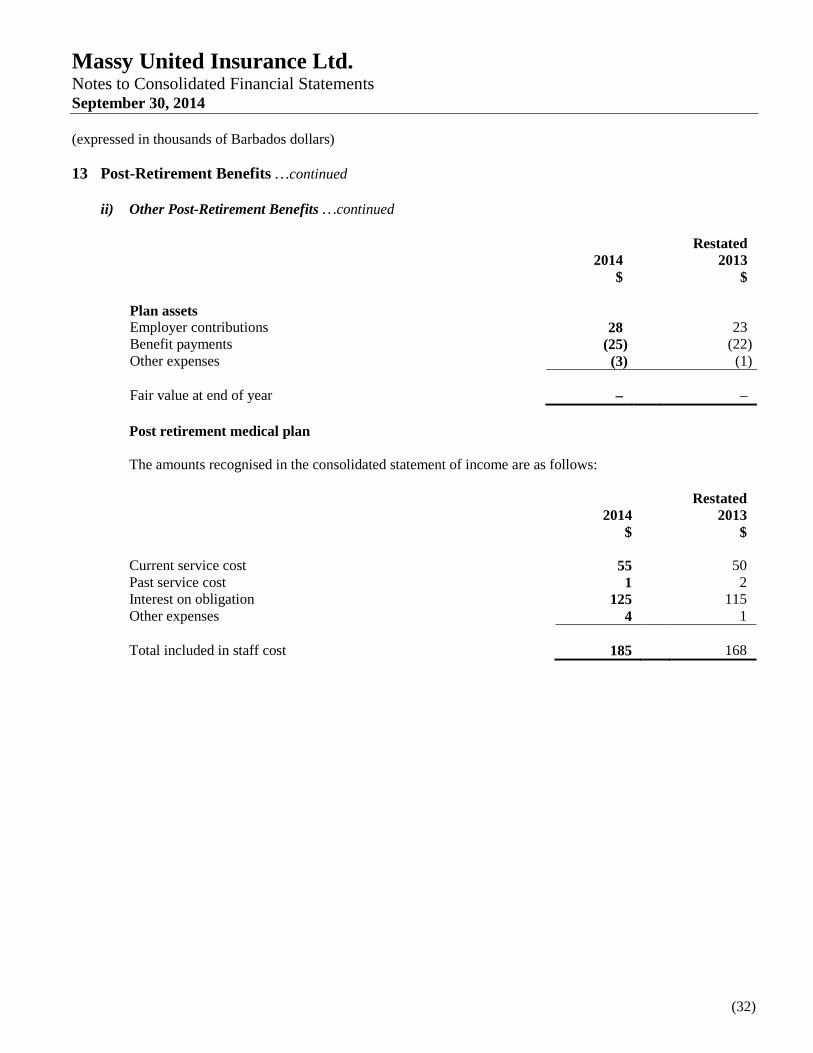

Plan assetsEmployer contributions 28 23Benefit payments (25) (22)Other expenses (3) (1)

Fair value at end of year – –

Post retirement medical plan

The amounts recognised in the consolidated statement of income are as follows:

2014$

Restated2013

$

Current service cost 55 50Past service cost 1 2Interest on obligation 125 115Other expenses 4 1

Total included in staff cost 185 168

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(33)

13 Post-Retirement Benefits …continued

ii) Other Post-Retirement Benefits …continued

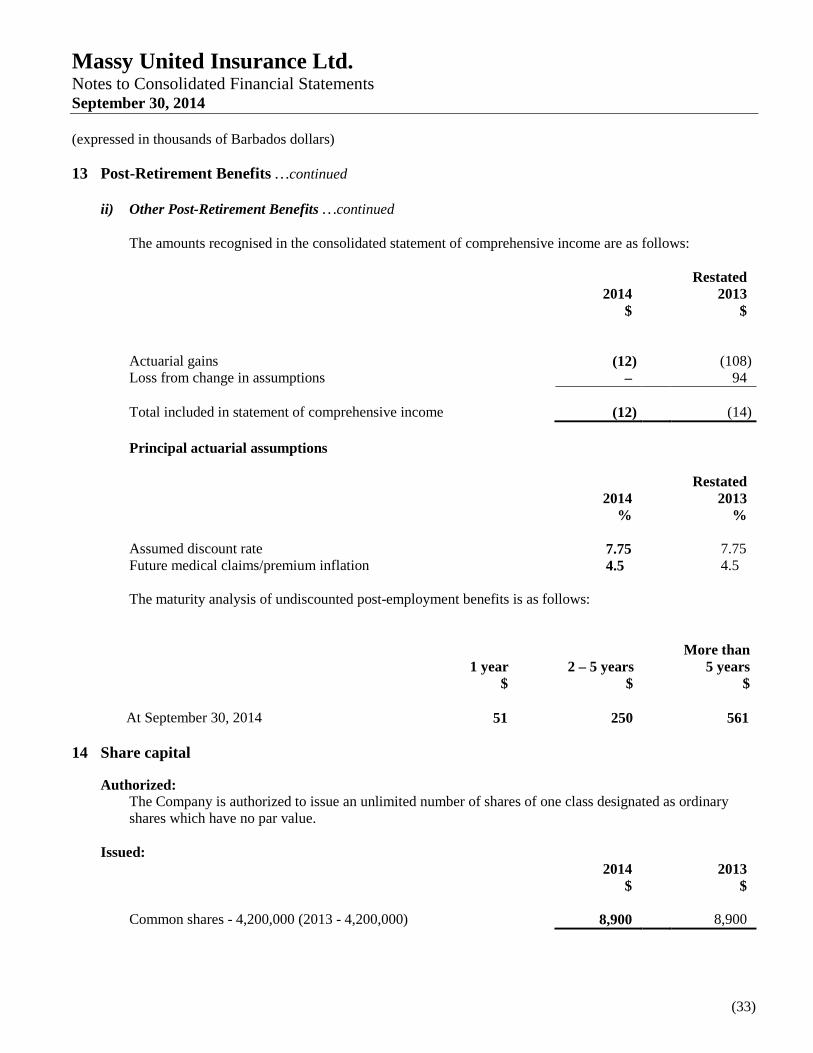

The amounts recognised in the consolidated statement of comprehensive income are as follows:

2014$

Restated2013

$

Actuarial gains (12) (108)Loss from change in assumptions – 94

Total included in statement of comprehensive income (12) (14)

Principal actuarial assumptions

2014%

Restated2013

%

Assumed discount rate 7.75 7.75Future medical claims/premium inflation 4.5 4.5

The maturity analysis of undiscounted post-employment benefits is as follows:

1 year$

2 – 5 years$

More than5 years

$

At September 30, 2014 51 250 561

14 Share capital

Authorized:The Company is authorized to issue an unlimited number of shares of one class designated as ordinaryshares which have no par value.

Issued:2014

$2013

$

Common shares - 4,200,000 (2013 - 4,200,000) 8,900 8,900

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(34)

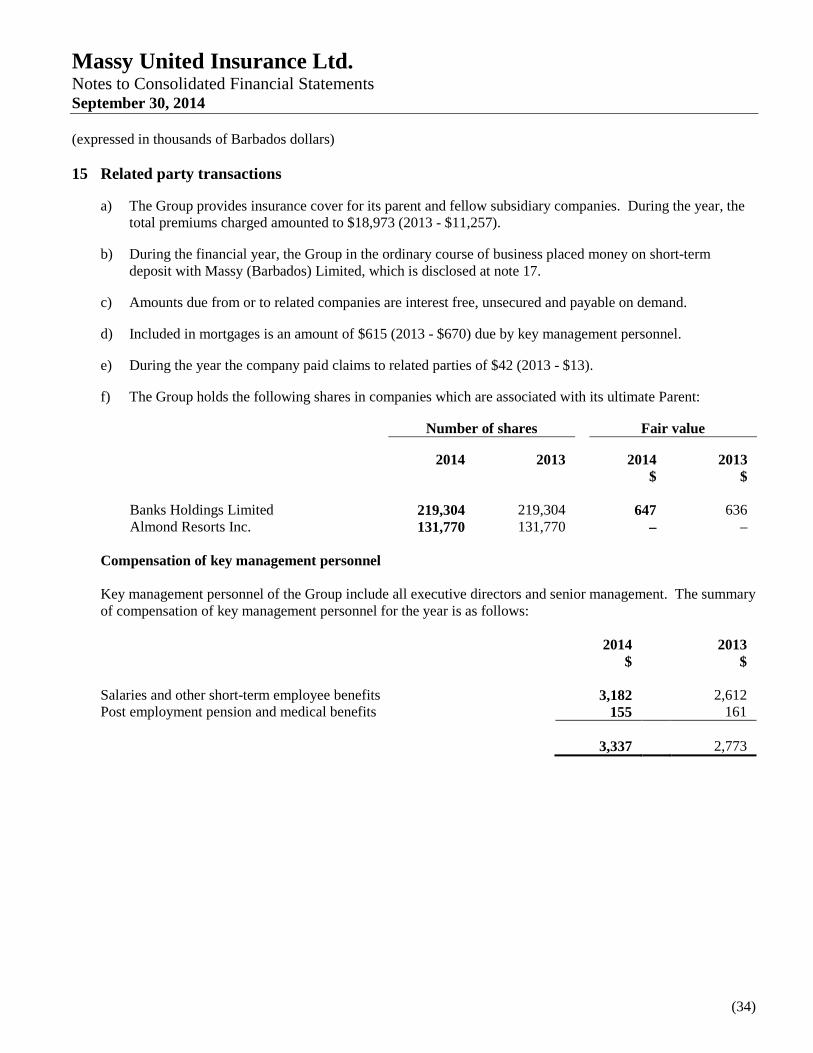

15 Related party transactions

a) The Group provides insurance cover for its parent and fellow subsidiary companies. During the year, thetotal premiums charged amounted to $18,973 (2013 - $11,257).

b) During the financial year, the Group in the ordinary course of business placed money on short-termdeposit with Massy (Barbados) Limited, which is disclosed at note 17.

c) Amounts due from or to related companies are interest free, unsecured and payable on demand.

d) Included in mortgages is an amount of $615 (2013 - $670) due by key management personnel.

e) During the year the company paid claims to related parties of $42 (2013 - $13).

f) The Group holds the following shares in companies which are associated with its ultimate Parent:

Number of shares Fair value

2014 2013 2014$

2013$

Banks Holdings Limited 219,304 219,304 647 636Almond Resorts Inc. 131,770 131,770 – –

Compensation of key management personnel

Key management personnel of the Group include all executive directors and senior management. The summaryof compensation of key management personnel for the year is as follows:

2014$

2013$

Salaries and other short-term employee benefits 3,182 2,612Post employment pension and medical benefits 155 161

3,337 2,773

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(35)

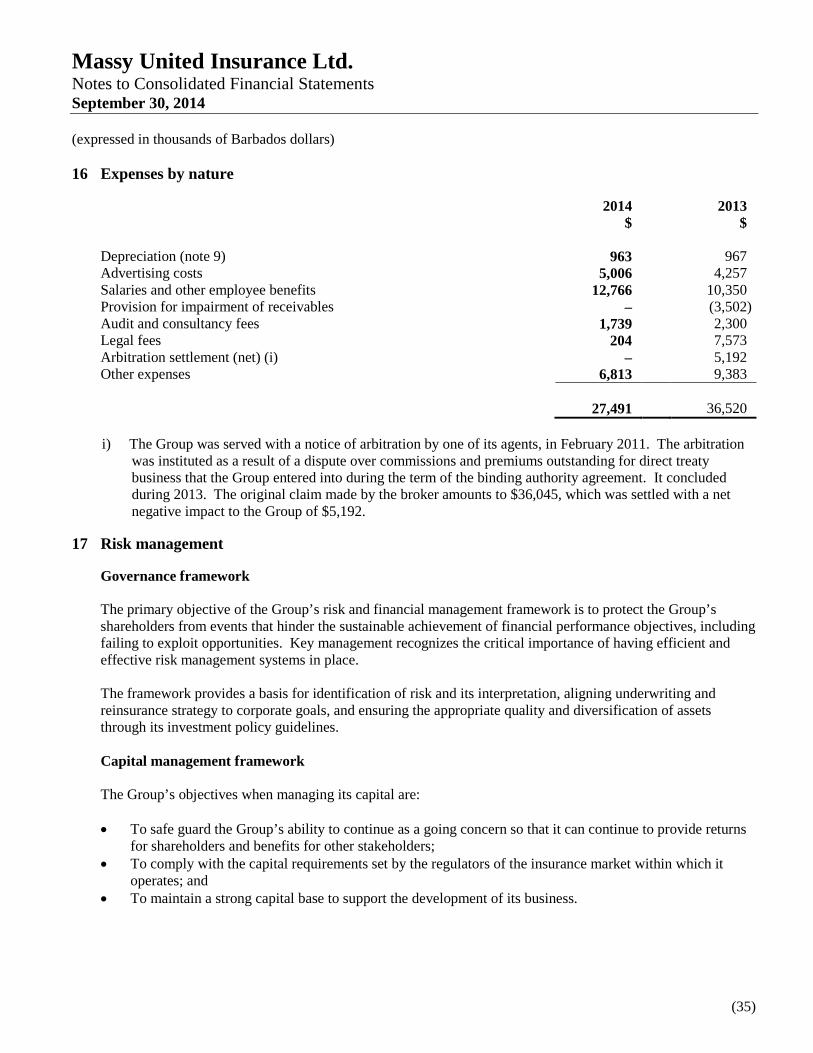

16 Expenses by nature

2014$

2013$

Depreciation (note 9) 963 967Advertising costs 5,006 4,257Salaries and other employee benefits 12,766 10,350Provision for impairment of receivables – (3,502)Audit and consultancy fees 1,739 2,300Legal fees 204 7,573Arbitration settlement (net) (i) – 5,192Other expenses 6,813 9,383

27,491 36,520

i) The Group was served with a notice of arbitration by one of its agents, in February 2011. The arbitrationwas instituted as a result of a dispute over commissions and premiums outstanding for direct treatybusiness that the Group entered into during the term of the binding authority agreement. It concludedduring 2013. The original claim made by the broker amounts to $36,045, which was settled with a netnegative impact to the Group of $5,192.

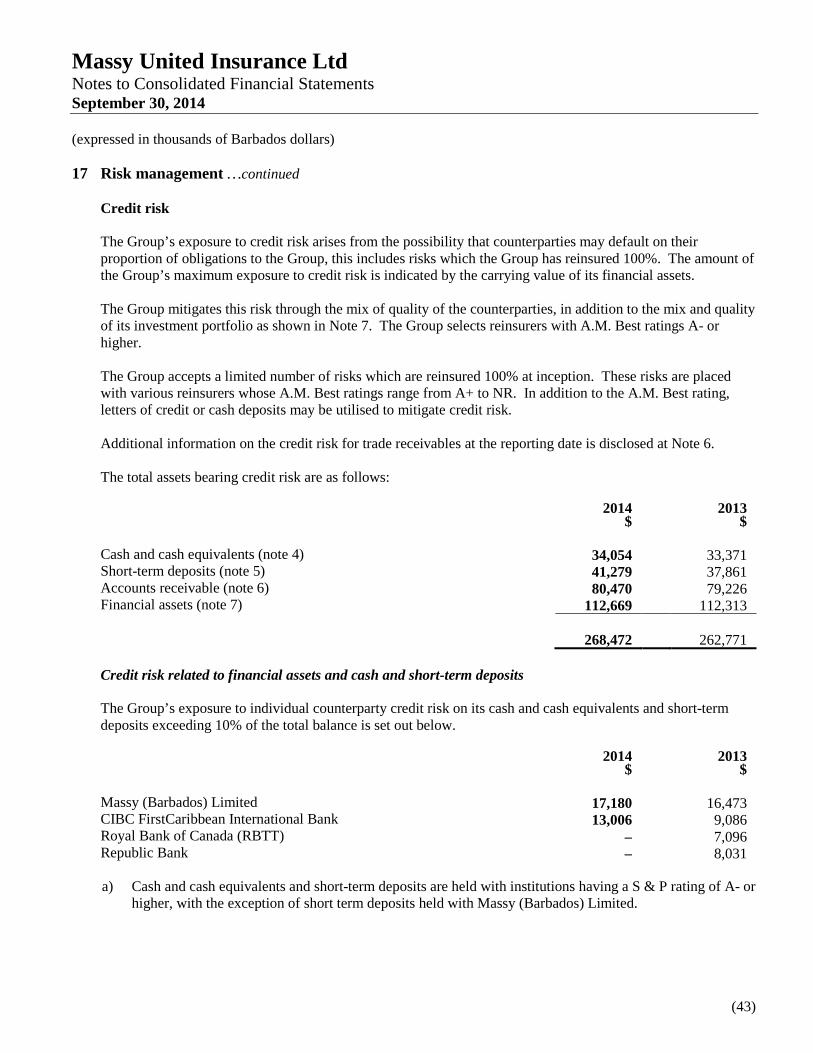

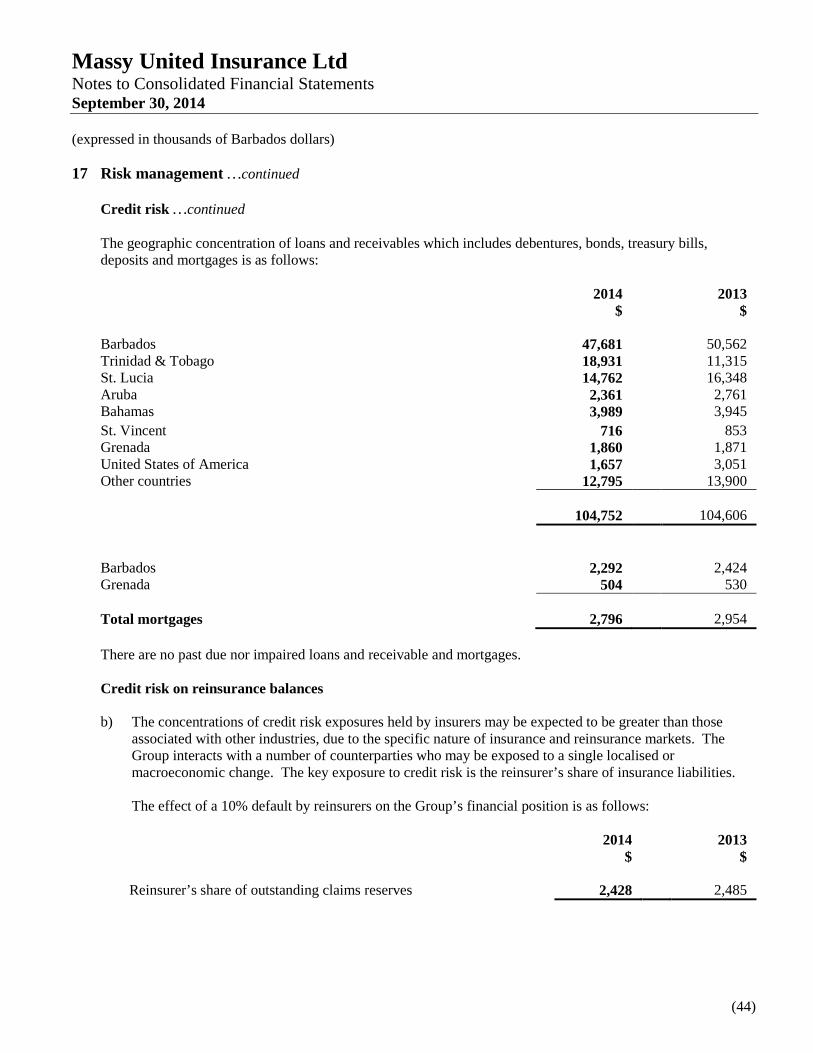

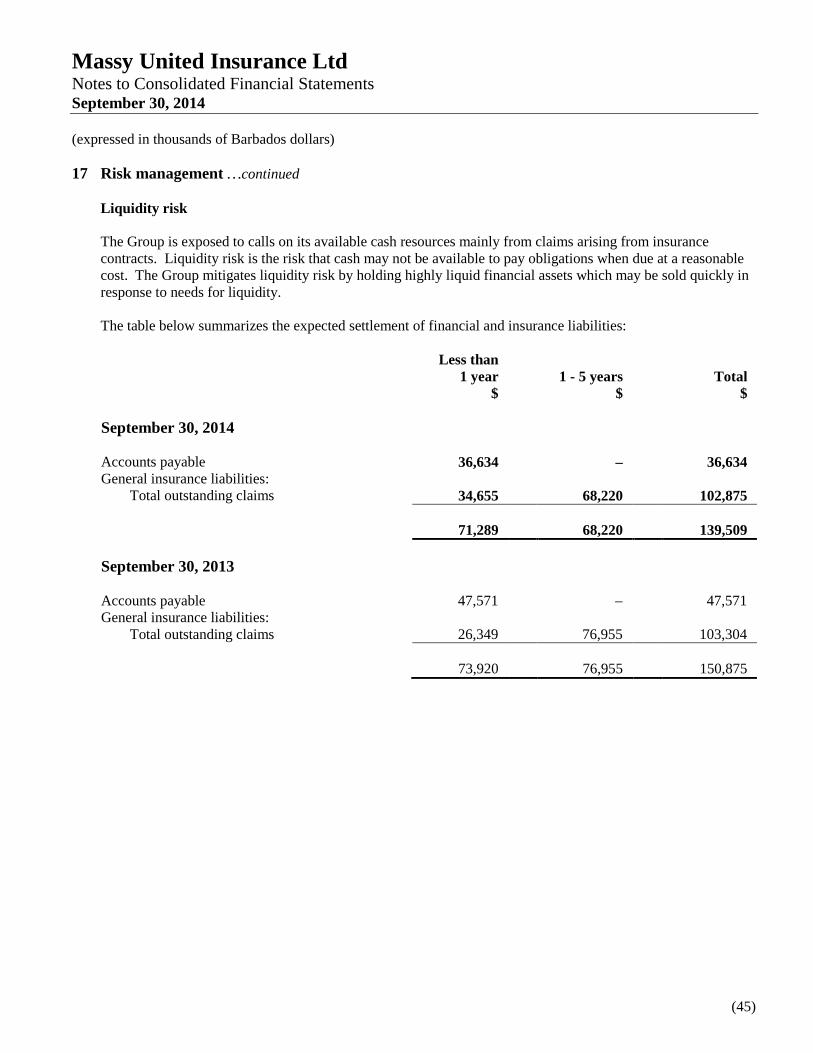

17 Risk management

Governance framework

The primary objective of the Group’s risk and financial management framework is to protect the Group’sshareholders from events that hinder the sustainable achievement of financial performance objectives, includingfailing to exploit opportunities. Key management recognizes the critical importance of having efficient andeffective risk management systems in place.

The framework provides a basis for identification of risk and its interpretation, aligning underwriting andreinsurance strategy to corporate goals, and ensuring the appropriate quality and diversification of assetsthrough its investment policy guidelines.

Capital management framework

The Group’s objectives when managing its capital are:

To safe guard the Group’s ability to continue as a going concern so that it can continue to provide returnsfor shareholders and benefits for other stakeholders;

To comply with the capital requirements set by the regulators of the insurance market within which itoperates; and

To maintain a strong capital base to support the development of its business.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(36)

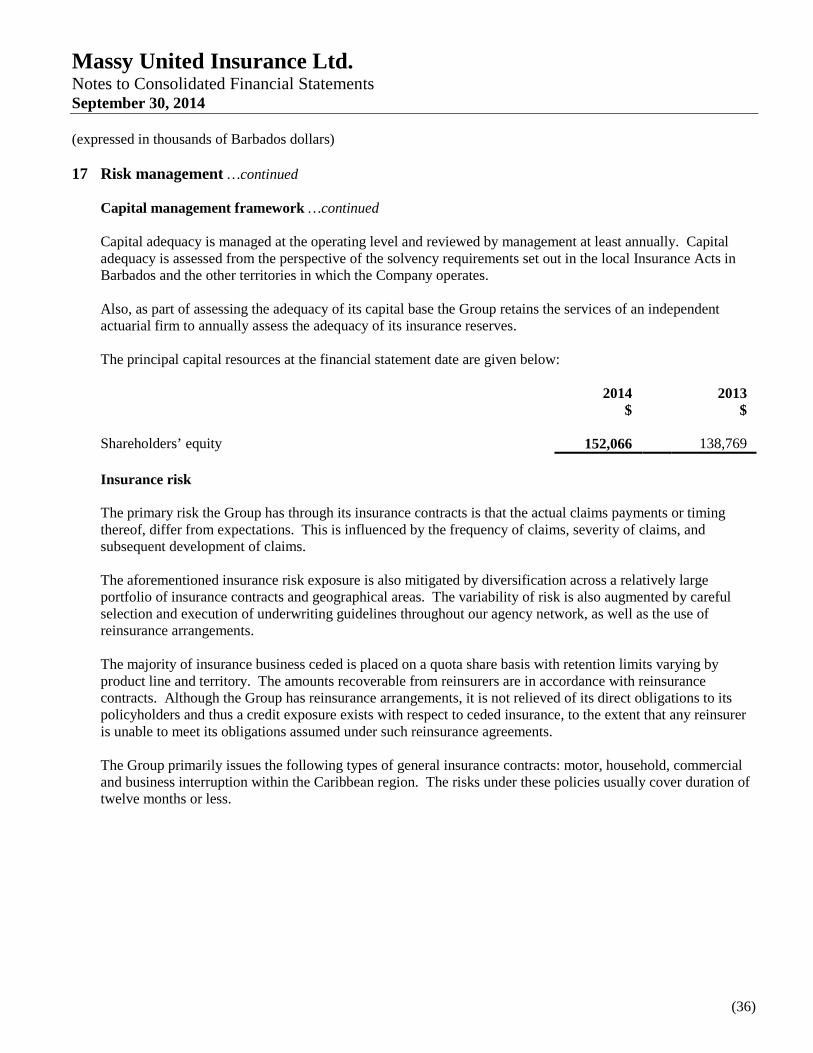

17 Risk management …continued

Capital management framework …continued

Capital adequacy is managed at the operating level and reviewed by management at least annually. Capitaladequacy is assessed from the perspective of the solvency requirements set out in the local Insurance Acts inBarbados and the other territories in which the Company operates.

Also, as part of assessing the adequacy of its capital base the Group retains the services of an independentactuarial firm to annually assess the adequacy of its insurance reserves.

The principal capital resources at the financial statement date are given below:

2014$

2013$

Shareholders’ equity 152,066 138,769

Insurance risk

The primary risk the Group has through its insurance contracts is that the actual claims payments or timingthereof, differ from expectations. This is influenced by the frequency of claims, severity of claims, andsubsequent development of claims.

The aforementioned insurance risk exposure is also mitigated by diversification across a relatively largeportfolio of insurance contracts and geographical areas. The variability of risk is also augmented by carefulselection and execution of underwriting guidelines throughout our agency network, as well as the use ofreinsurance arrangements.

The majority of insurance business ceded is placed on a quota share basis with retention limits varying byproduct line and territory. The amounts recoverable from reinsurers are in accordance with reinsurancecontracts. Although the Group has reinsurance arrangements, it is not relieved of its direct obligations to itspolicyholders and thus a credit exposure exists with respect to ceded insurance, to the extent that any reinsureris unable to meet its obligations assumed under such reinsurance agreements.

The Group primarily issues the following types of general insurance contracts: motor, household, commercialand business interruption within the Caribbean region. The risks under these policies usually cover duration oftwelve months or less.

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(37)

17 Risk management …continued

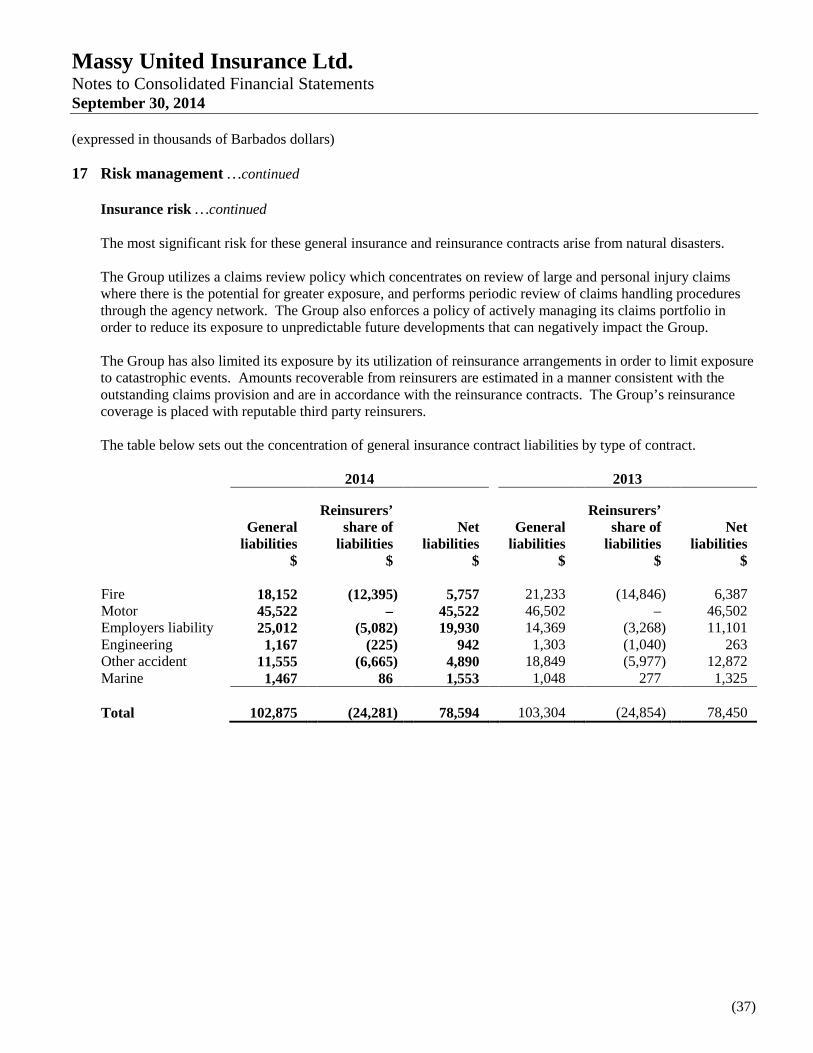

Insurance risk …continued

The most significant risk for these general insurance and reinsurance contracts arise from natural disasters.

The Group utilizes a claims review policy which concentrates on review of large and personal injury claimswhere there is the potential for greater exposure, and performs periodic review of claims handling proceduresthrough the agency network. The Group also enforces a policy of actively managing its claims portfolio inorder to reduce its exposure to unpredictable future developments that can negatively impact the Group.

The Group has also limited its exposure by its utilization of reinsurance arrangements in order to limit exposureto catastrophic events. Amounts recoverable from reinsurers are estimated in a manner consistent with theoutstanding claims provision and are in accordance with the reinsurance contracts. The Group’s reinsurancecoverage is placed with reputable third party reinsurers.

The table below sets out the concentration of general insurance contract liabilities by type of contract.

2014 2013

Generalliabilities

$

Reinsurers’share of

liabilities$

Netliabilities

$

Generalliabilities

$

Reinsurers’share of

liabilities$

Netliabilities

$

Fire 18,152 (12,395) 5,757 21,233 (14,846) 6,387Motor 45,522 – 45,522 46,502 – 46,502Employers liability 25,012 (5,082) 19,930 14,369 (3,268) 11,101Engineering 1,167 (225) 942 1,303 (1,040) 263Other accident 11,555 (6,665) 4,890 18,849 (5,977) 12,872Marine 1,467 86 1,553 1,048 277 1,325

Total 102,875 (24,281) 78,594 103,304 (24,854) 78,450

Massy United Insurance Ltd.Notes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(38)

17 Risk management …continued

Insurance risk …continued

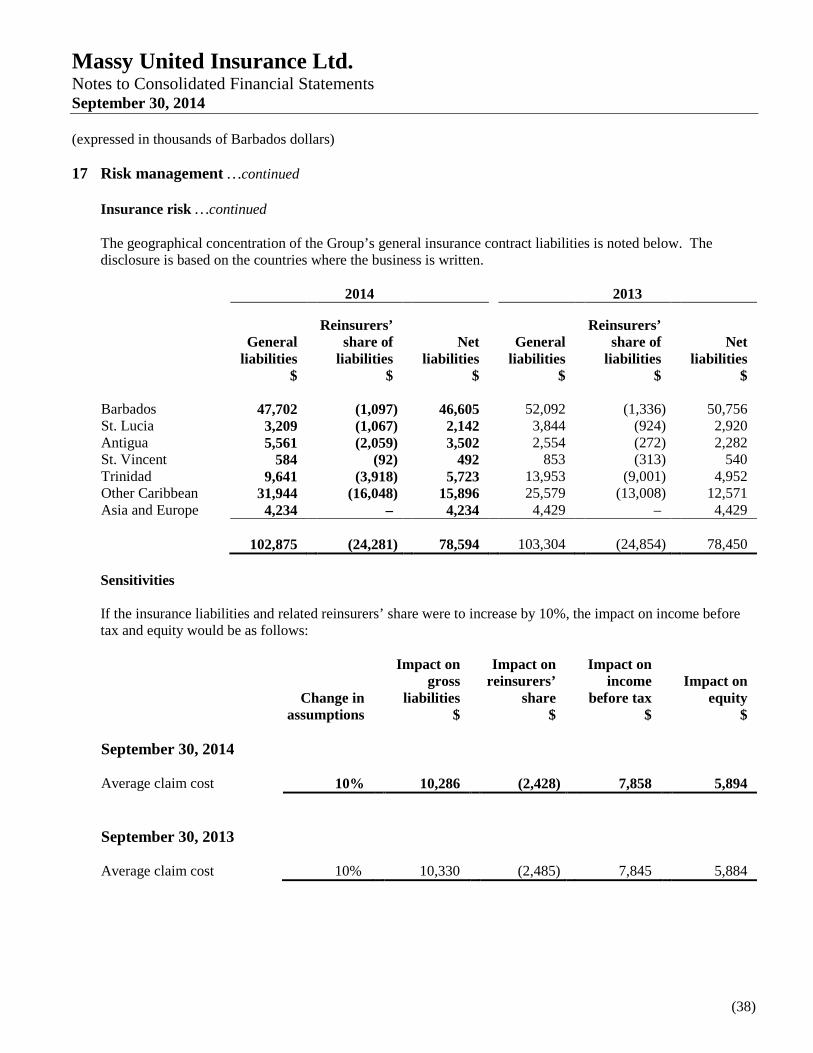

The geographical concentration of the Group’s general insurance contract liabilities is noted below. Thedisclosure is based on the countries where the business is written.

2014 2013

Generalliabilities

$

Reinsurers’share of

liabilities$

Netliabilities

$

Generalliabilities

$

Reinsurers’share of

liabilities$

Netliabilities

$

Barbados 47,702 (1,097) 46,605 52,092 (1,336) 50,756St. Lucia 3,209 (1,067) 2,142 3,844 (924) 2,920Antigua 5,561 (2,059) 3,502 2,554 (272) 2,282St. Vincent 584 (92) 492 853 (313) 540Trinidad 9,641 (3,918) 5,723 13,953 (9,001) 4,952Other Caribbean 31,944 (16,048) 15,896 25,579 (13,008) 12,571Asia and Europe 4,234 – 4,234 4,429 – 4,429

102,875 (24,281) 78,594 103,304 (24,854) 78,450

Sensitivities

If the insurance liabilities and related reinsurers’ share were to increase by 10%, the impact on income beforetax and equity would be as follows:

Change inassumptions

Impact ongross

liabilities$

Impact onreinsurers’

share$

Impact onincome

before tax$

Impact onequity

$

September 30, 2014

Average claim cost 10% 10,286 (2,428) 7,858 5,894

September 30, 2013

Average claim cost 10% 10,330 (2,485) 7,845 5,884

Massy United Insurance LtdNotes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(39)

17 Risk management …continued

Insurance risk …continued

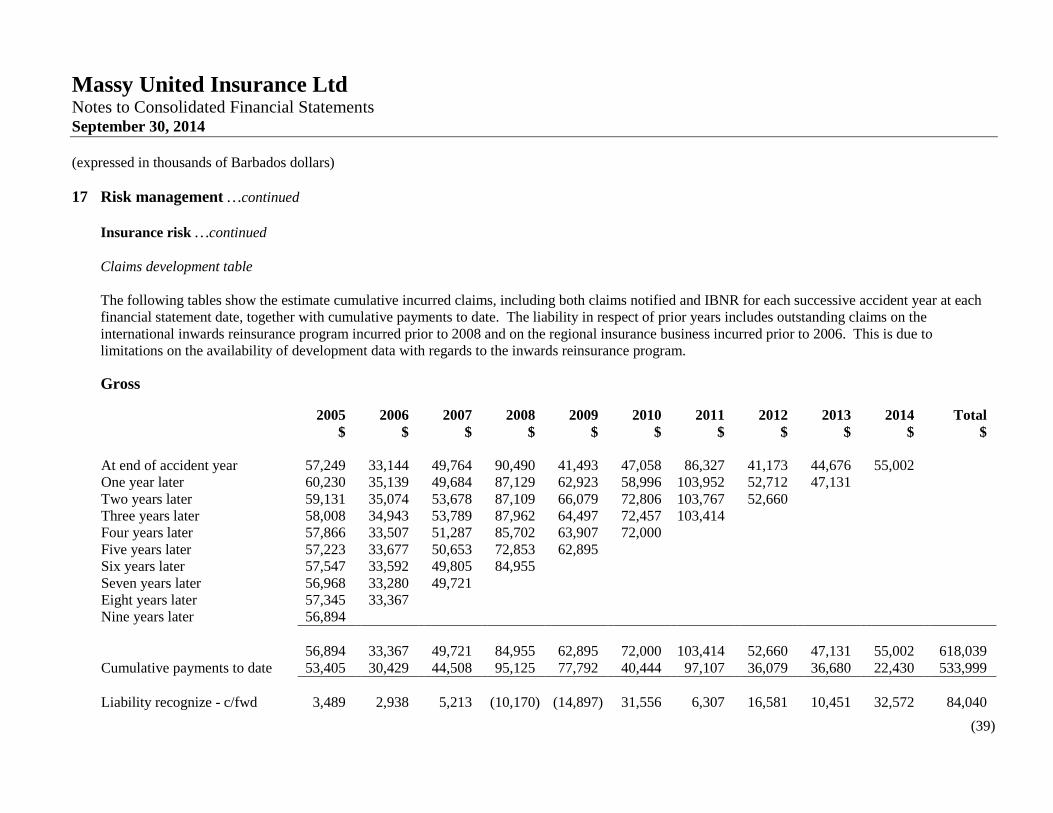

Claims development table

The following tables show the estimate cumulative incurred claims, including both claims notified and IBNR for each successive accident year at eachfinancial statement date, together with cumulative payments to date. The liability in respect of prior years includes outstanding claims on theinternational inwards reinsurance program incurred prior to 2008 and on the regional insurance business incurred prior to 2006. This is due tolimitations on the availability of development data with regards to the inwards reinsurance program.

Gross

2005$

2006$

2007$

2008$

2009$

2010$

2011$

2012$

2013$

2014$

Total$

At end of accident year 57,249 33,144 49,764 90,490 41,493 47,058 86,327 41,173 44,676 55,002One year later 60,230 35,139 49,684 87,129 62,923 58,996 103,952 52,712 47,131Two years later 59,131 35,074 53,678 87,109 66,079 72,806 103,767 52,660Three years later 58,008 34,943 53,789 87,962 64,497 72,457 103,414Four years later 57,866 33,507 51,287 85,702 63,907 72,000Five years later 57,223 33,677 50,653 72,853 62,895Six years later 57,547 33,592 49,805 84,955Seven years later 56,968 33,280 49,721Eight years later 57,345 33,367Nine years later 56,894

56,894 33,367 49,721 84,955 62,895 72,000 103,414 52,660 47,131 55,002 618,039Cumulative payments to date 53,405 30,429 44,508 95,125 77,792 40,444 97,107 36,079 36,680 22,430 533,999

Liability recognize - c/fwd 3,489 2,938 5,213 (10,170) (14,897) 31,556 6,307 16,581 10,451 32,572 84,040

Massy United Insurance LtdNotes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(40)

17 Risk management …continued

Insurance risk …continued

Claims development table …continued

Gross …continued

2005$

2006$

2007$

2008$

2009$

2010$

2011$

2012$

2013$

2014$

Total$

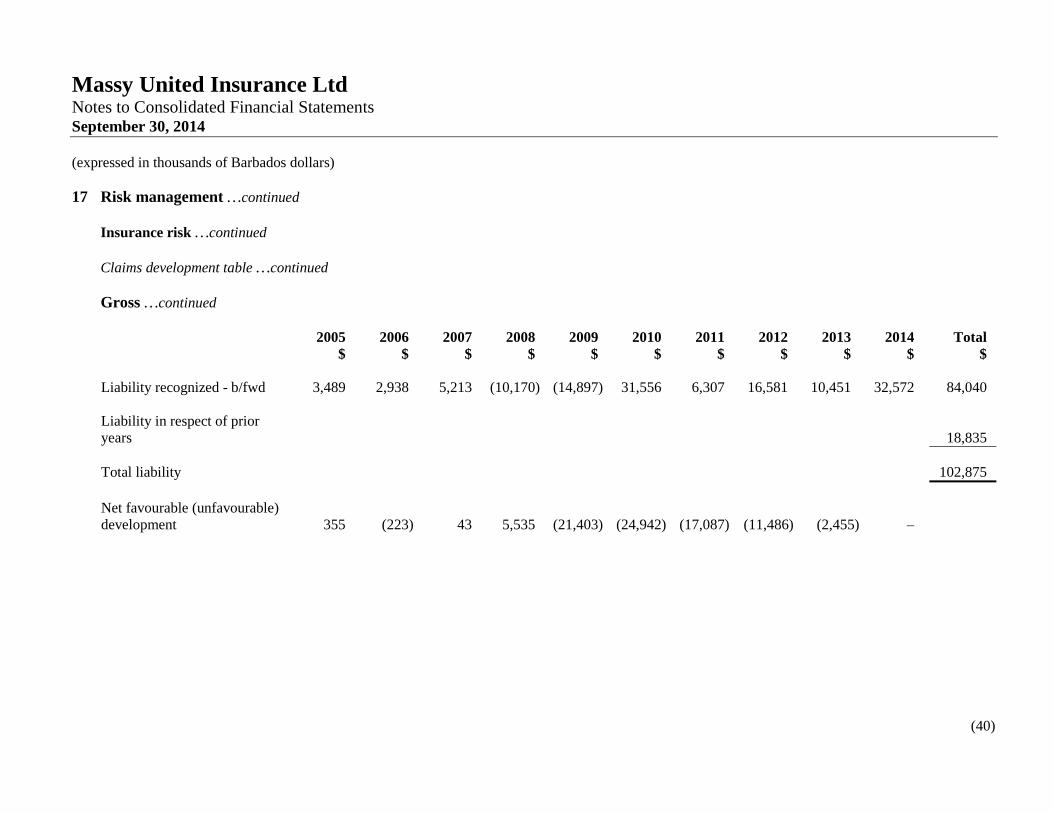

Liability recognized - b/fwd 3,489 2,938 5,213 (10,170) (14,897) 31,556 6,307 16,581 10,451 32,572 84,040

Liability in respect of prioryears 18,835

Total liability 102,875

Net favourable (unfavourable)development 355 (223) 43 5,535 (21,403) (24,942) (17,087) (11,486) (2,455) –

Massy United Insurance LtdNotes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(41)

17 Risk management …continued

Insurance risk …continued

Claims development table …continued

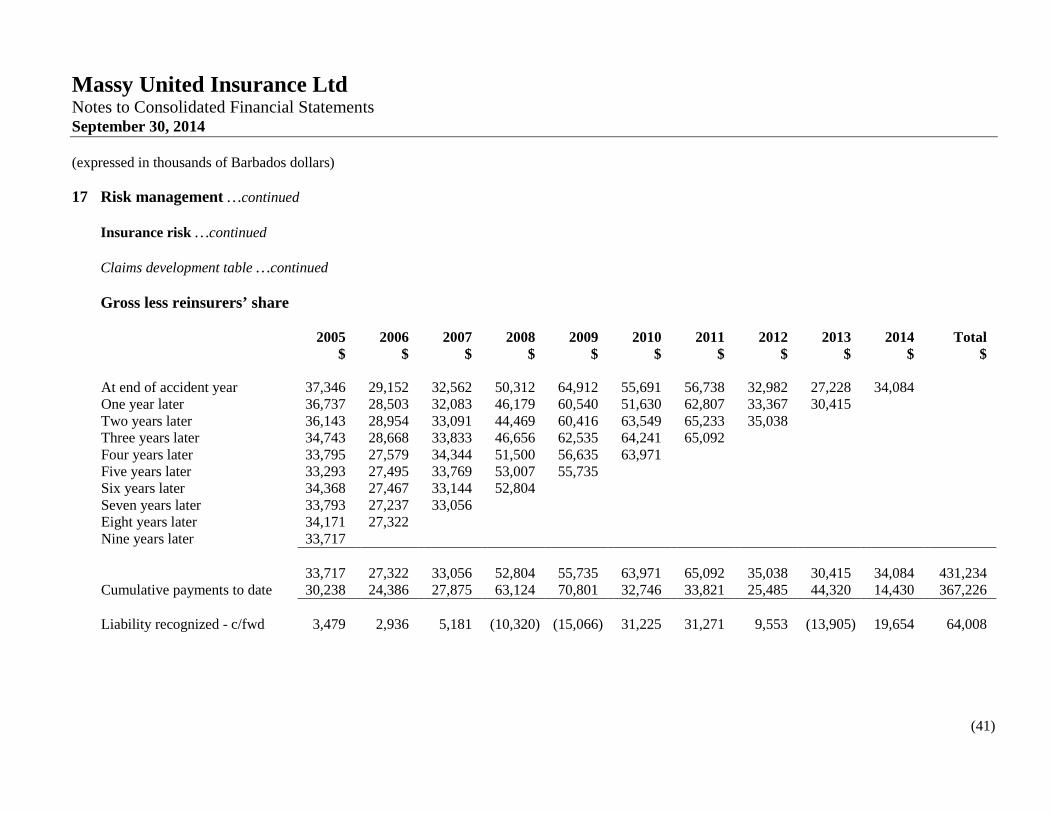

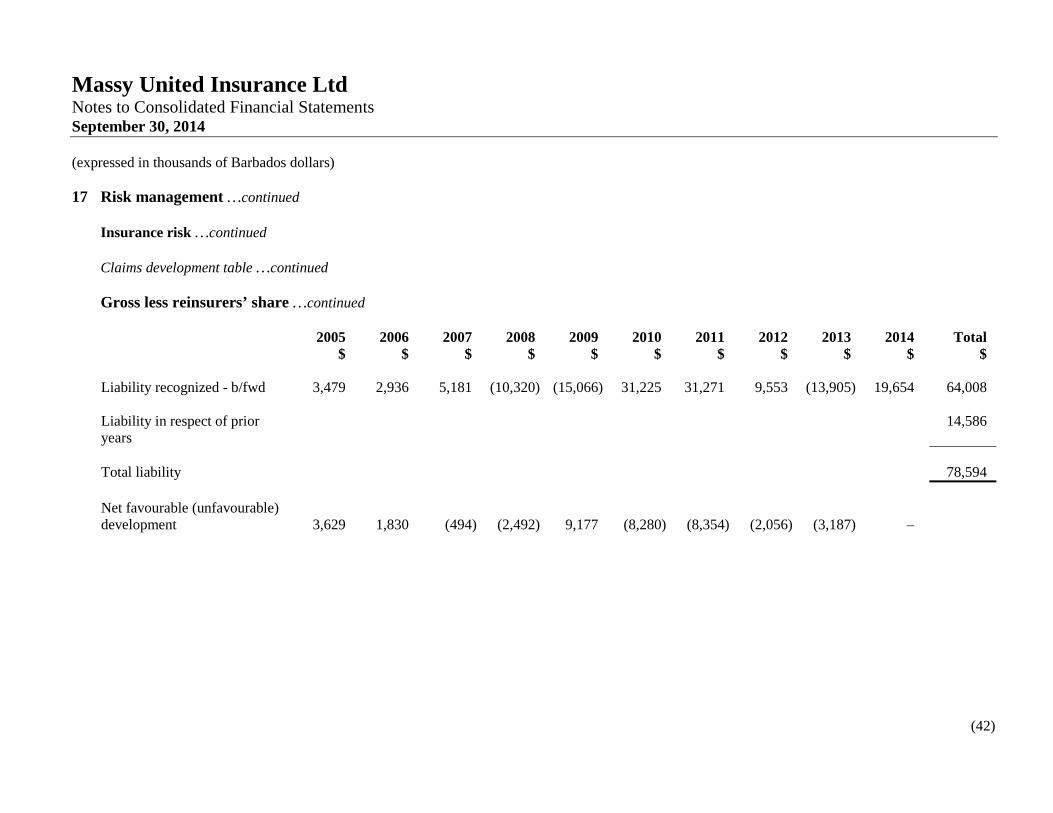

Gross less reinsurers’ share

2005$

2006$

2007$

2008$

2009$

2010$

2011$

2012$

2013$

2014$

Total$

At end of accident year 37,346 29,152 32,562 50,312 64,912 55,691 56,738 32,982 27,228 34,084One year later 36,737 28,503 32,083 46,179 60,540 51,630 62,807 33,367 30,415Two years later 36,143 28,954 33,091 44,469 60,416 63,549 65,233 35,038Three years later 34,743 28,668 33,833 46,656 62,535 64,241 65,092Four years later 33,795 27,579 34,344 51,500 56,635 63,971Five years later 33,293 27,495 33,769 53,007 55,735Six years later 34,368 27,467 33,144 52,804Seven years later 33,793 27,237 33,056Eight years later 34,171 27,322Nine years later 33,717

33,717 27,322 33,056 52,804 55,735 63,971 65,092 35,038 30,415 34,084 431,234Cumulative payments to date 30,238 24,386 27,875 63,124 70,801 32,746 33,821 25,485 44,320 14,430 367,226

Liability recognized - c/fwd 3,479 2,936 5,181 (10,320) (15,066) 31,225 31,271 9,553 (13,905) 19,654 64,008

Massy United Insurance LtdNotes to Consolidated Financial StatementsSeptember 30, 2014

(expressed in thousands of Barbados dollars)

(42)

17 Risk management …continued

Insurance risk …continued

Claims development table …continued

Gross less reinsurers’ share …continued

2005$

2006$

2007$

2008$

2009$

2010$

2011$

2012$

2013$

2014$

Total$