matthew boyle - cru - coal market outlook – tracking the trends

TRANSCRIPT

Coal market outlook – Tracking the

trends

Prepared for:

Mozambique Coal Conference,

Maputo, Mozambique

July 27, 2015

Matthew Boyle Principal Consultant - CRU Analysis

• This presentation is supplied on a private and confidential basis to the customer. It must not

be disclosed in whole or in part, directly or indirectly or in any other format to any other

company, organisation or individual without the prior written permission of CRU International

Limited.

• Permission is given for the disclosure of this report to a company’s majority owned

subsidiaries and its parent organisation. However, where the report is supplied to a client in

his capacity as a manager of a joint venture or partnership, it may not be disclosed to the

other participants without further permission.

• CRU International Limited’s responsibility is solely to its direct client. Its liability is limited to

the amount of the fees actually paid for the professional services involved in preparing this

presentation. We accept no liability to third parties, howsoever arising.

• Although reasonable care and diligence has been used in the preparation of this

presentation, we do not guarantee the accuracy of any data, assumptions, forecasts or other

forward-looking statements.

Disclaimer

2

The global presence of CRU

3

1. The opening of the Nacala Corridor and port, together with other infrastructure

improvements, will boost coal exports from Mozambique.

2. Chinese demand is still relevant, but the seaborne coal markets are now switching their

focus to India. India will be the dominant demand market for coal going forward.

3. Prices are expected to recover towards their equilibrium point, and therefore a balanced

market, in both metallurgical and thermal coal. However, the wait will be longer for thermal

coal.

Summary The future is brighter for Mozambican coal exports

4

Agenda

• Coal production in Mozambique – how does it fit in with global supply?

• Where are the demand markets for Mozambican metallurgical and thermal coal exports?

• How competitive are Mozambican costs compared to other supply markets?

Mozambique is not a Greenfield basin anymore

6

0

1

2

3

4

5

6

7

8

9

11 12 13 14 15

Metallurgical Thermal

Data: CRU.

Mozambique coal exports, Mt

0

1

2

3

4

5

6

7

8

9

11 12 13 14 15

Metallurgical Thermal

Data: CRU.

Mozambique coal production, Mt

Mozambique metallurgical coal is high ash, mid vol, high

CSR

7

0

10

20

30

40

50

60

70

80

Data: CRU.

CSR HCC

0%

2%

4%

6%

8%

10%

12%

Data: CRU.

Met. Coal Ash, % ad

New met. coal supply from Mozambique, Mongolia and

Russia will come online in the next five years

8

-4

-3

-2

-1

0

1

2

3

4

5

6

7

15 16 17 18 19

Mongolia Mozambique Russia

Met. coal exports change y/y, Mt

Data: CRU, GTIS, company reports.

Mozambique thermal coal has high CV, and a high ash

content

9

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Data: CRU.

Thermal Coal Energy, Kcal/kg NAR

0%

5%

10%

15%

20%

25%

30%

Data: CRU.

Thermal Coal Ash, % ad

Mozambique, Russia to be the predominant growth markets

for seaborne thermal coal supply

10

0

2

4

6

8

10

12

14

12 13 14 15 16 17 18 19

Mozambique Russia

Data: CRU.

Changes in thermal coal exports, Mt y/y

Data: CRU

South African thermal coal production, exports static

through to 2019

11

0

50

100

150

200

250

300

2012 2013 2014 2015 2016 2017 2018 2019

Domestic Demand Exports

Total thermal coal production and exports, 2012-2019 (Mt)

Agenda

• Coal production in Mozambique – how does it fit in with global supply?

• Where are the demand markets for Mozambican metallurgical and thermal coal

exports?

• How competitive are Mozambican costs compared to other supply markets?

No matter where you look, it is India

13 Images courtesy of domdeen at FreeDigitalPhotos.net

Indian hot metal production is expected to grow strongly

this year; production rose by 11% y/y in Q1

14

11.0

11.5

12.0

12.5

13.0

13.5

14.0

14.5

15.0

13Q1

13Q2

13Q3

13Q4

14Q1

14Q2

14Q3

14Q4

15Q1

Indian hot metal production, Mt

Data: CRU.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Indian coking coal imports, Mt

Robust met. Coal import demand growth from other

markets, including India, will help to offset Chinese decline

15

-2%

0%

2%

4%

6%

8%

10%

15 16 17 18 19

JKT India Europe Latin America

Data: CRU.

Met. coal seaborne import demand growth y/y, %

16

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

0

50

100

150

200

250

300

350

2014 2015 2016 2017 2018 2019

India seaborne demand South East Asia seaborne demand

Global seaborne imports excl. China Global seaborne imports

LHS: India and South East Asia seaborne imports, Mt

RHS: Growth, y/y %

Data: CRU.

Seaborne thermal coal supply to India and Southeast Asia

set to increase

Electricity generation demand to drive thermal coal

consumption in India

17

0

200

400

600

800

1,000

1,200Cement production coal demand

Other industrial coal demand

Electricity generation coal demand

Data: CRU.

Thermal coal demand by industry, Mt

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000Gross electricity generation

Electricity % of PE

Data: CRU.

LHS: Total gross electricity generation, TWh

RHS: Electricity percentage share of Primary Energy, %

18

0

200

400

600

800

1,000

1,200

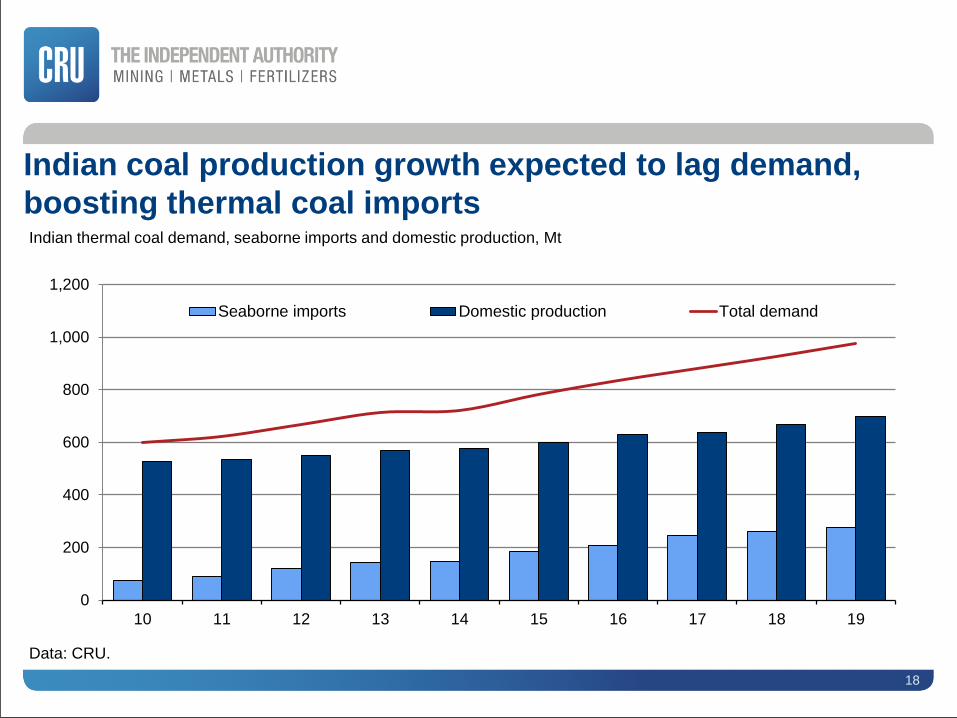

10 11 12 13 14 15 16 17 18 19

Seaborne imports Domestic production Total demand

Indian thermal coal demand, seaborne imports and domestic production, Mt

Data: CRU.

Indian coal production growth expected to lag demand,

boosting thermal coal imports

India to overtake China as major thermal coal import

market in 2015

19

0

50

100

150

200

250

300

10 11 12 13 14 15 16 17 18 19

China India

Seaborne thermal coal imports, Mt

Data: CRU.

Speaking of China’s demand: underlying versus apparent Imports continue despite slower power generation growth

20 Data: NBS, CRU Thermal Coal Market Service

Underlying SE generation demand growth (% YoY RHS) vs.

apparent demand, imports (Mt LHS)

-20%

-10%

0%

10%

20%

30%

Domestic coastal Volume Change% YoY

QHD 5500Kcal Price % YoY

China domestic coastal volume changes & Price %

YoY

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0

50

100

150

200

250

Seaborne Imports (Mt LHS)

Power generation in coastal area (% YoY RHS)

Data: CRU Analysis.

21

China has plenty of coal, in the wrong place China’s coal & power production surplus & deficits are expanding

XINJIANG

QINGHAI

INNER MONGOLIA

GANSU

NINGXIA

SHAANXI XIZANG

SICHUAN CHONGQING

YUNNAN GUIZHOU

GUANGXI

HAINAN

HUNAN JIANGXI ZHEJIANG

FUJIAN

GUANGDONG

MACAU

SHANGHAI

JIANGSU

ANHUI HUBEI

HENAN

SHANXI

SHANDONG

HEBEI LIAONING

JILIN

HEILONGJIANG

>350mt 100mt to 350mt 20mt to 100mt <20mt

XINJIANG

QINGHAI

INNER MONGOLIA

GANSU

NINGXIA

SHAANXI XIZANG

SICHUAN CHONGQING

YUNNAN

GUIZHOU

GUANGXI

HAINAN

HUNAN JIANGXI ZHEJIANG

FUJIAN

GUANGDONG

MACAU

SHANGHAI

JIANGSU

ANHUI HUBEI

HENAN

SHANXI

SHANDONG

HEBEI LIAONING

JILIN

HEILONGJIANG

Coal production in 2004 Coal production in 2014

Data: CRU Thermal Coal Market Service

Data: CRU, NDRC, CEC, NBS

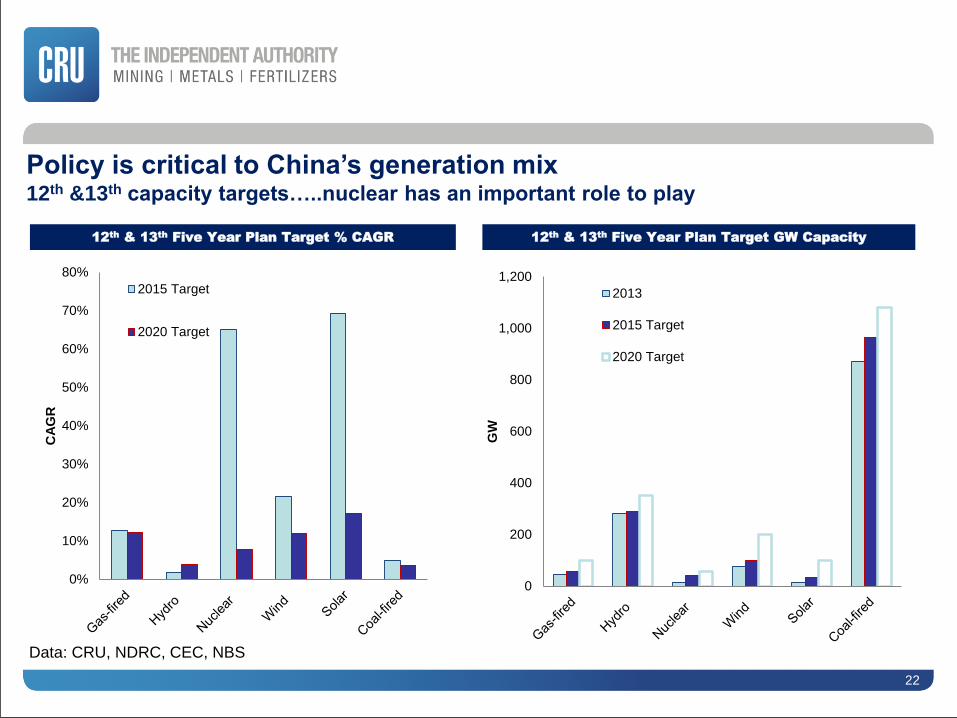

Policy is critical to China’s generation mix 12th &13th capacity targets…..nuclear has an important role to play

22

0

200

400

600

800

1,000

1,200

GW

2013

2015 Target

2020 Target

0%

10%

20%

30%

40%

50%

60%

70%

80%

CA

GR

2015 Target

2020 Target

12th

& 13th

Five Year Plan Target % CAGR 12th

& 13th

Five Year Plan Target GW Capacity

Power consumption growth has a long way to run But regional differences in intensity trajectory will impact growth rates.....

23

R² = 0.9643

0

0.002

0.004

0.006

0.008

0.01

0.012

0.014

0 10000 20000 30000 40000 50000 60000

Japan USA France

Germany China Average

Regression Line

Electricity demand / cap. vs GDP / cap. (1980-2011)

0

1

2

3

4

5

6

7

8

0 10000 20000 30000 40000 50000

MW

h/c

ap

ita

South-East Coastal South-East Coastal (f)

Rest of China Rest of China (f)

China electricity demand / cap. vs GDP / cap. (1995-

2035)

Rapid industrialisation

and increase in energy

consumption per capita…

Data: CRU Thermal Coal Market Service

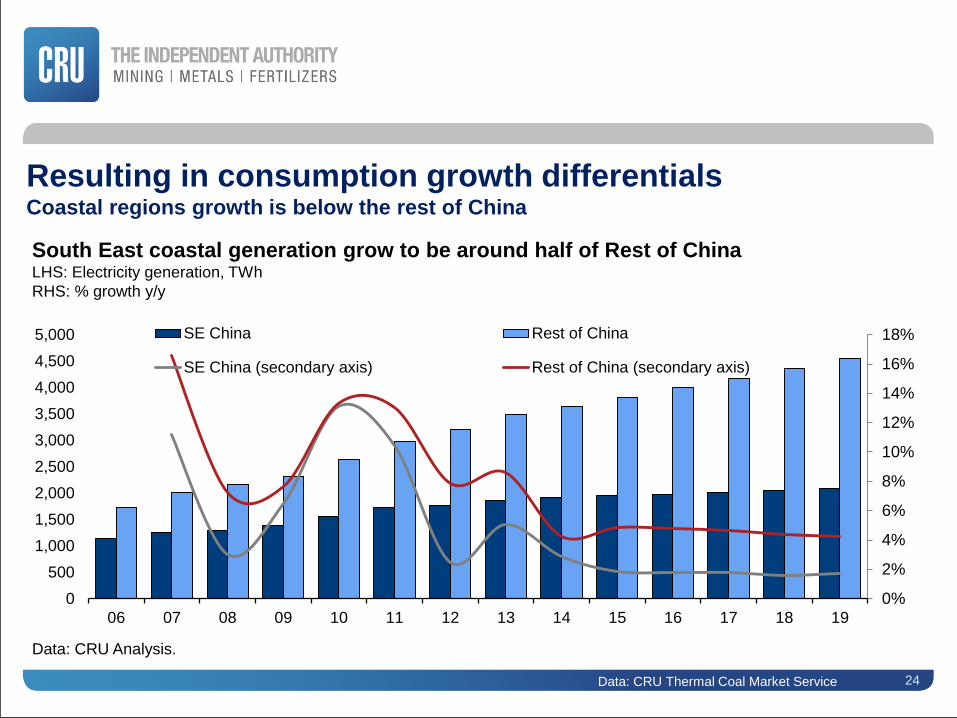

Resulting in consumption growth differentials Coastal regions growth is below the rest of China

24

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

06 07 08 09 10 11 12 13 14 15 16 17 18 19

SE China Rest of China

SE China (secondary axis) Rest of China (secondary axis)

South East coastal generation grow to be around half of Rest of China LHS: Electricity generation, TWh

RHS: % growth y/y

Data: CRU Analysis.

Data: CRU Thermal Coal Market Service

The Chinese steel industry has been flagging and domestic

steel prices tumbled in H1

25

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5Crude steel production change y/y EBITDA margin

Data: CRU.

LHS: China crude steel production change y/y, Mt

RHS: Average China steel mill EBITDA margin, %

The Chinese coal industry remains oversupplied; coke

exports continued to rise y/y in H1, while coal imports fell

26

China coke exports

rose by 25% y/y in

January-May

0

1

2

3

4

5

6

7

8

China met. coal imports, Mt

Data: CRU, GTIS.

0

200

400

600

800

1,000

1,200

1,400

China coke exports, '000 t

Agenda

• Coal production in Mozambique – how does it fit in with global supply?

• Where are the demand markets for Mozambican metallurgical and thermal coal exports?

• How competitive are Mozambican costs compared to other supply markets?

Supply regions have benefitted from depreciating local

currencies, aiding cost cutting efforts Hard coking coal business costs, y/y change, %

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

Russia Ukraine Australia Mozambique United States

14 vs. 13 15 vs 14

Data: CRU.

Macro-shifts and company actions are pushing the

Business Cost curve lower in 2015

2014 2015

X-axis: Seaborne HCC supply, Mt

Y-axis: Business Costs(1), $/t, FOB, nominal

Key 2015 macro assumptions:

• Energy:

• Brent oil: $61/bbl

• Diesel: $71/bbl

• Currency:

• AUD: 76 cents

• CAD: 81 cents

• RUB: 0.0169 cents

Data: CRU Metallurgical Coal Cost Model 2014. Note: (1) Cash costs including royalties, sustaining capital and adjustments to benchmark HCC price for

freight and quality differentials.

29

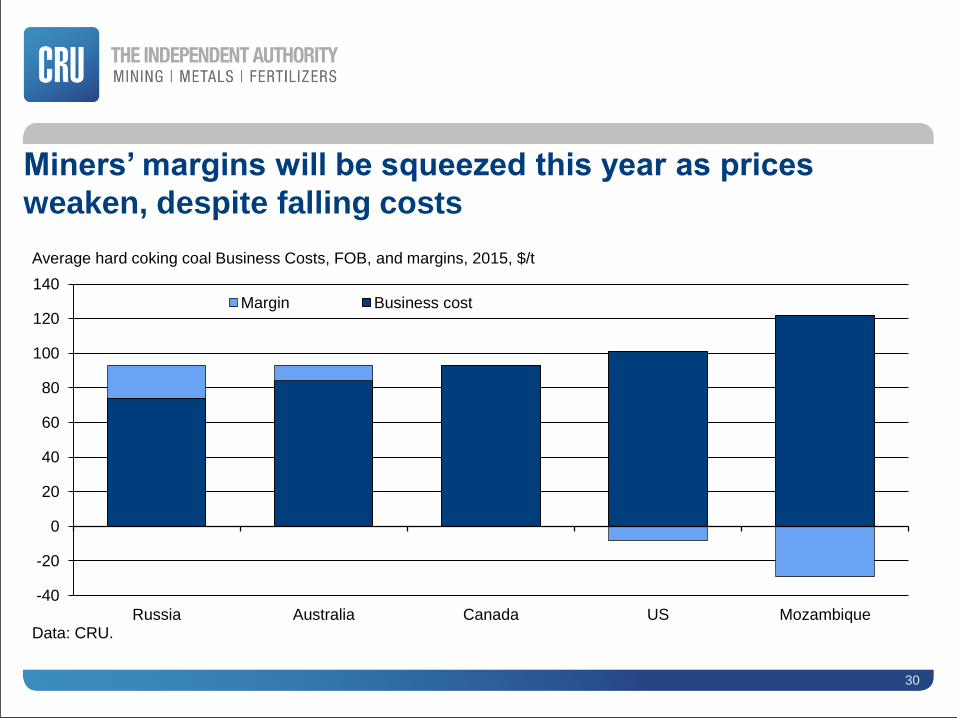

Miners’ margins will be squeezed this year as prices

weaken, despite falling costs

30

-40

-20

0

20

40

60

80

100

120

140

Russia Australia Canada US Mozambique

Margin Business cost

Average hard coking coal Business Costs, FOB, and margins, 2015, $/t

Data: CRU.

Further cost reductions will be very difficult in the years

ahead, as currencies and energy prices recover

50

75

100

125

60

80

100

120

14 15 16 17 18 19

Global average seaborne costs AUD CAD RUB Oil price

LHS: Global average seaborne HCC Business Costs, $/t, FOB, real 2014$

RHS: Key cost macro drivers, index 2014 = 100

Data: CRU Metallurgical Coal Cost Model. Note: (1) Cash costs including royalties, sustaining capital and adjustments to benchmark HCC price for

freight and quality differentials.

31

Data: CRU Thermal Coal Cost Model

Mixed operations are typically higher cost than either open

pit or underground mines Average Business Costs, 2014

0

20

40

60

80

100

120

Austr

alia

Ch

ile

Co

lom

bia

Ind

one

sia

Mo

za

mbiq

ue

Russia

Sou

th A

fric

a

Un

ited

Sta

tes

Ven

ezue

la

Vie

tna

m

Mixed Open Pit UndergroundLHS: Business Costs (US$/t)

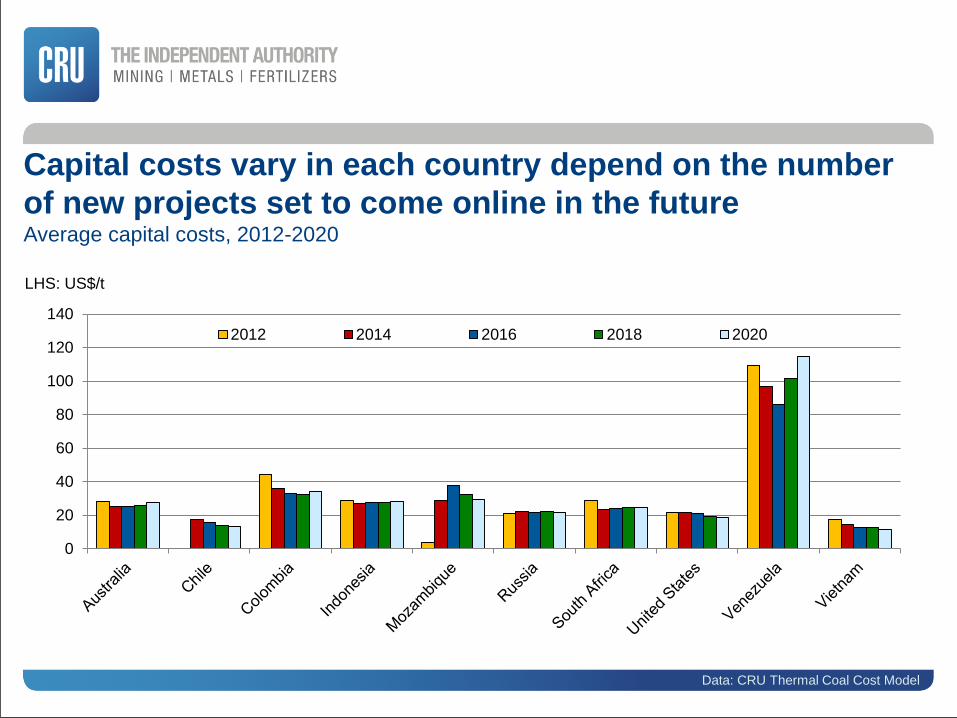

Capital costs vary in each country depend on the number

of new projects set to come online in the future Average capital costs, 2012-2020

Data: CRU Thermal Coal Cost Model

0

20

40

60

80

100

120

140

2012 2014 2016 2018 2020

LHS: US$/t

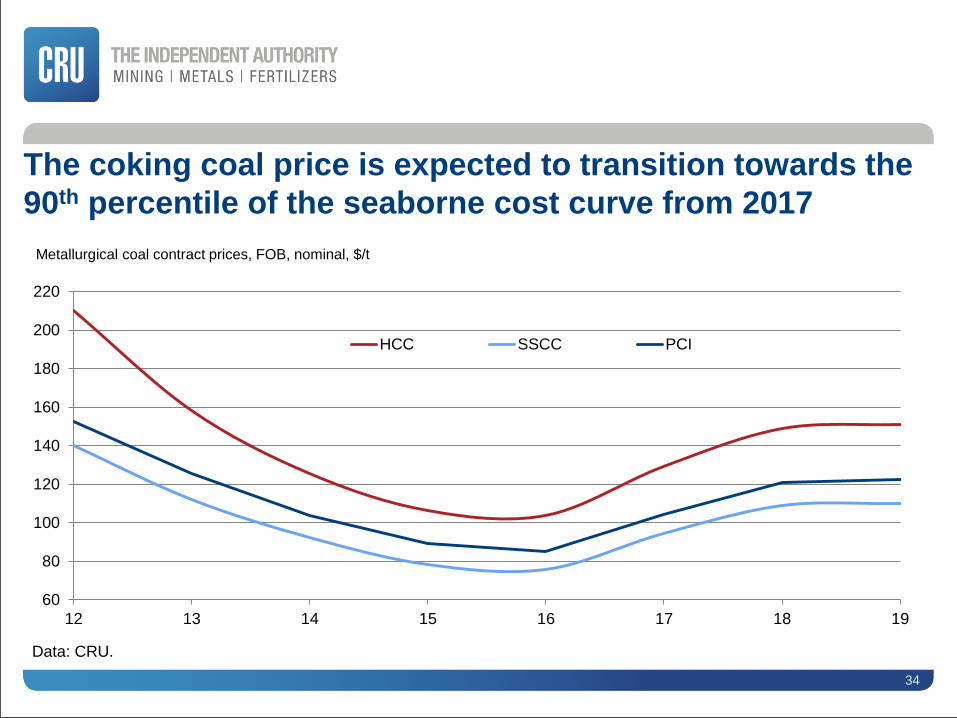

The coking coal price is expected to transition towards the

90th percentile of the seaborne cost curve from 2017

60

80

100

120

140

160

180

200

220

12 13 14 15 16 17 18 19

HCC SSCC PCI

Data: CRU.

Metallurgical coal contract prices, FOB, nominal, $/t

34

35

0

20

40

60

80

100

120

-40

-20

0

20

40

60

80

100

120

2014 2015 2016 2017 2018 2019

Change in domestic coastal trade CFR South China, 5,500 kg/kcal NAR

LHS: Change in Southeast China coastal trade, Mt

RHS: Benchmark thermal coal price, CFR China, 5,500 Kcal/kg NAR

Data: CRU.

Increased domestic coastal trade, costs, and stronger

demand excl.-China will support price rises going forward

1. The opening of the Nacala Corridor and port, together with other infrastructure

improvements, will boost coal exports from Mozambique.

2. Chinese demand is still relevant, but the seaborne coal markets are now switching their

focus to India. India will be the dominant demand market for coal going forward.

3. Prices are expected to recover towards their equilibrium point, and therefore a balanced

market, in both metallurgical and thermal coal. However, the wait will be longer for thermal

coal.

Conclusion The future is brighter for Mozambican coal exports

36

Thank you for listening www.crugroup.com

11

Matthew Boyle: Principal Consultant - Coal and Steel Raw Materials

Nick Collier: Business Development Manager

37

39