may, 1986 - tdl

TRANSCRIPT

PUBLIC EMPLOYEE RETIREMENT SYSTEM REPORTS: A STUDY

OF USER INFORMATION PROCESSING ABILITY

by

STEPHEN D. WILLITS, B.S., M.S. in Acct.

A DISSERTATION

IN

BUSINESS ADMINISTRATION

Submitted to the Graduate Faculty of Texas Tech University in Partial Fulfillment of the Requirements for

the Degree of

DOCTOR OF PHILOSOPHY

Approved

May, 1986

ACKNOWLEDGMENTS

I am forever Indebted to my committee chairman, Dr. Robert J.

Freeman, and to Dr. Donald K. Clancy for their careful and patient

guidance throughout the development of this work; to Dr. Paul H. Munter

for providing numerous helpful suggestions; and to Drs. Larry M. Austin

and James B. Wilcox for serving on my committee.

I am grateful to my wife Kris and my family for their patience,

support and encouragement during the years of my academic career.

11

CONTENTS

ACKNOWLEDGMENTS ii

ABSTRACT v

LIST OF TABLES vli

LIST OF FIGURES viii

1. INTRODUCTION 1

Nature of the Problem 1

General Pension Setting 3

GAAP Controversy 7

Actuarial Status 10

Specific Problem to be Addressed 12

Expected Contributions of the Study 15

Organization of the Study 16

2. LITERATURE ON PENSION PLAN REPORTING 18

Authoritative Statements 18

Previous Pension Research 26

Summary 34

3. FULL DISCLOSURE VS. FUNCTIONAL FIXATION 36

Support for "Full Disclosure" 37

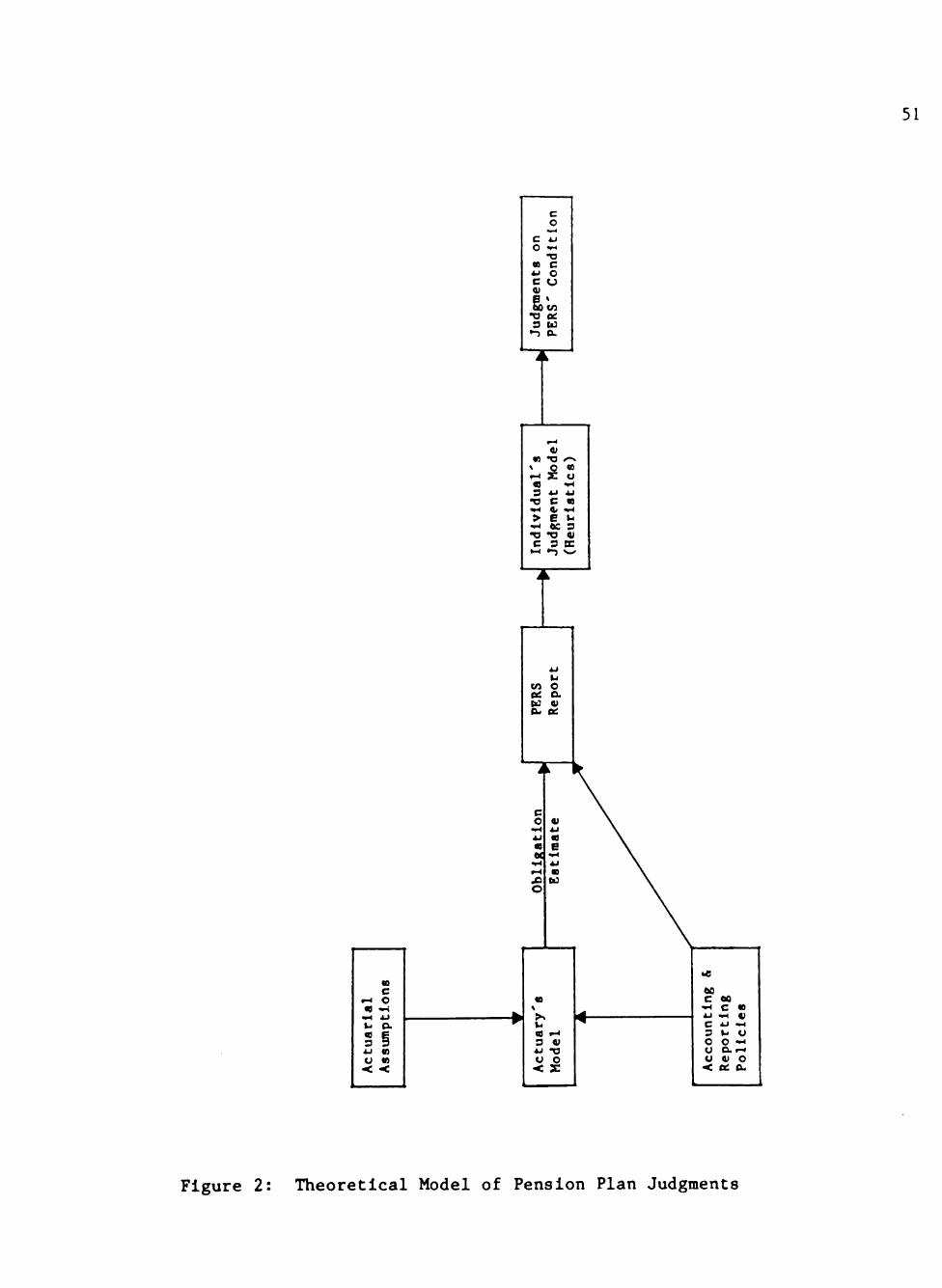

Support for "Functional Fixation" 44

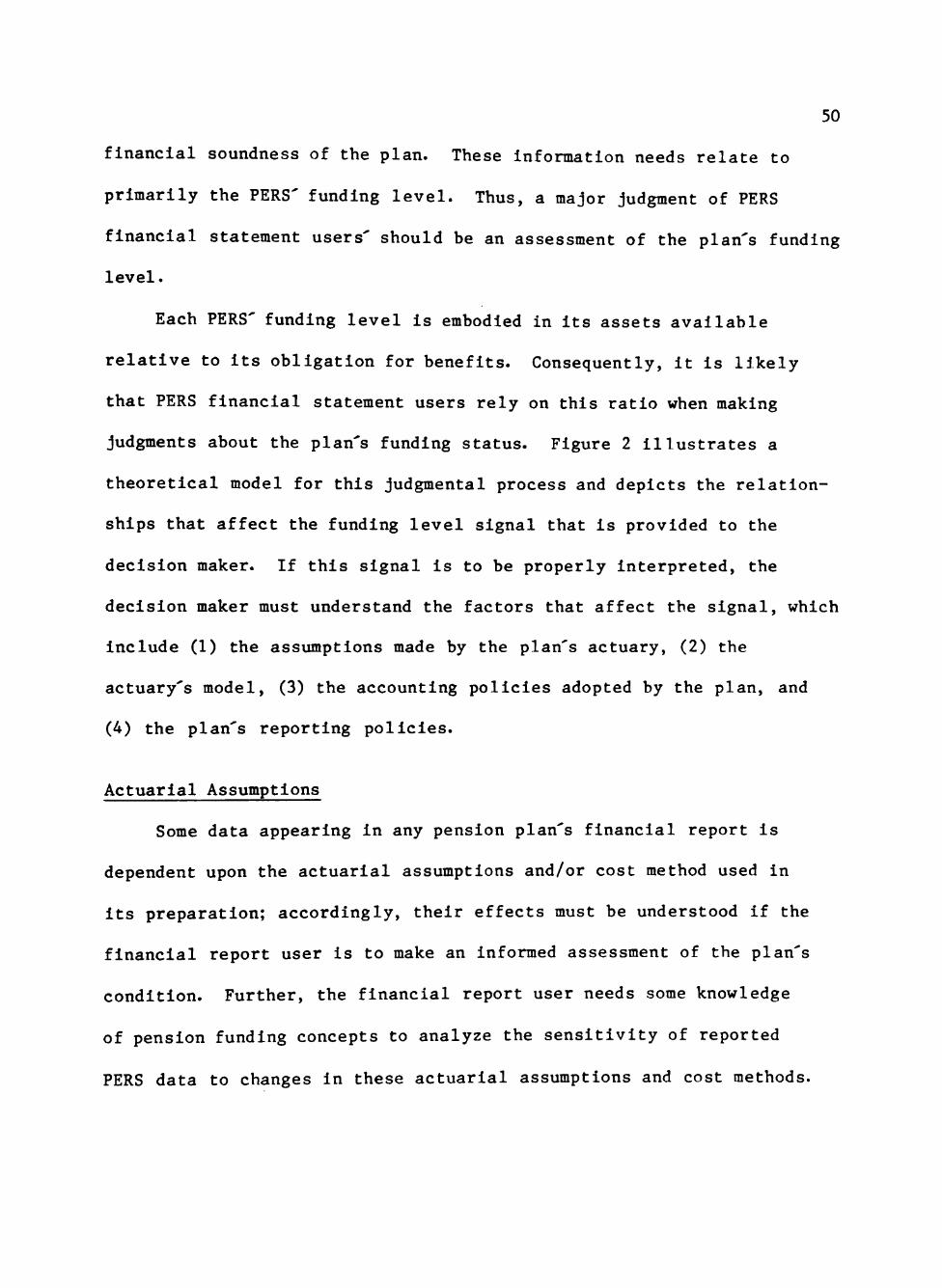

Theoretical Model of PERS Accounting 49

Summary 59

111

4. RESEARCH DESIGN 60

Human Judgment Research 60

Research Instrument and Hypotheses 75

Summary 80

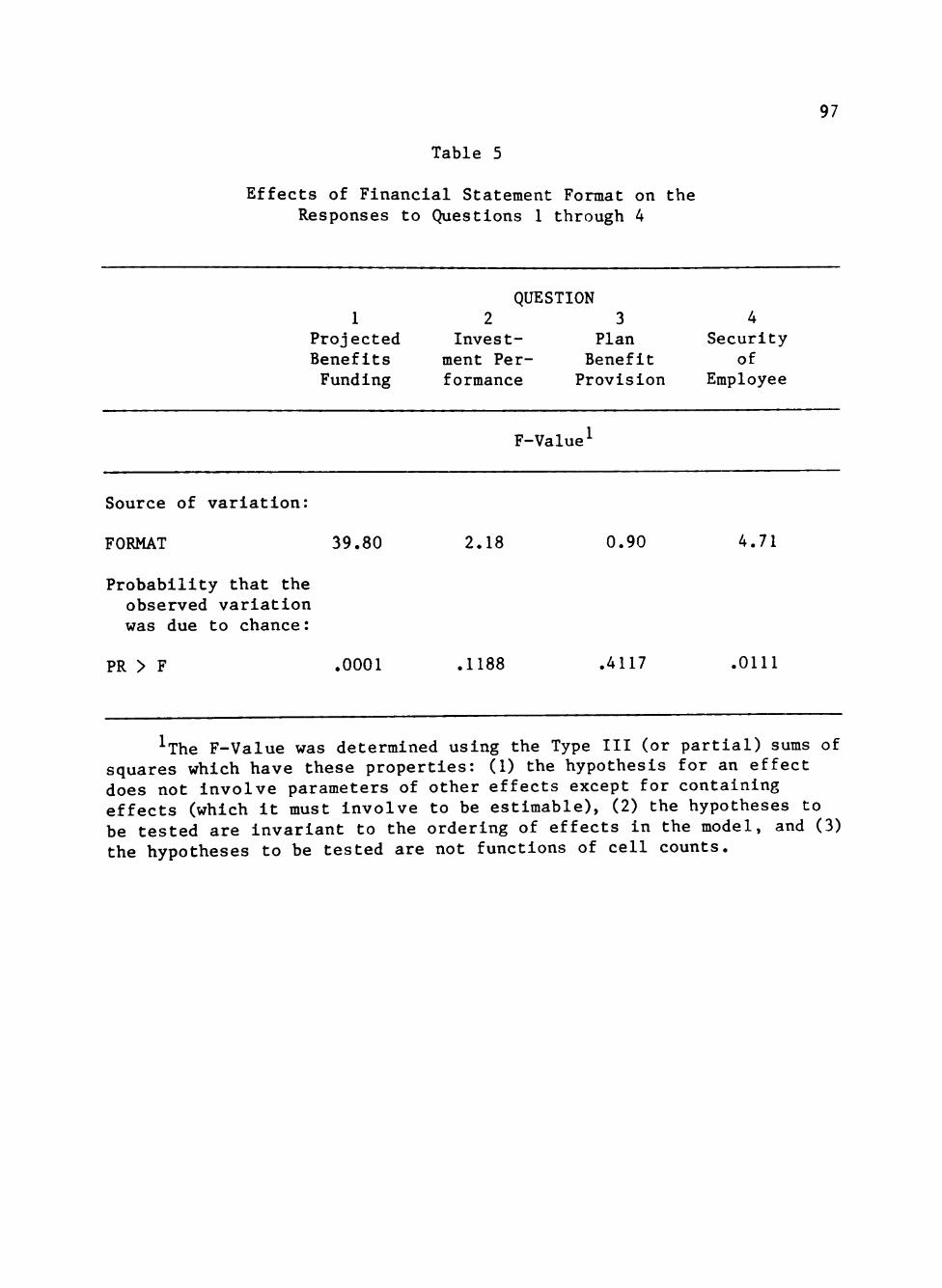

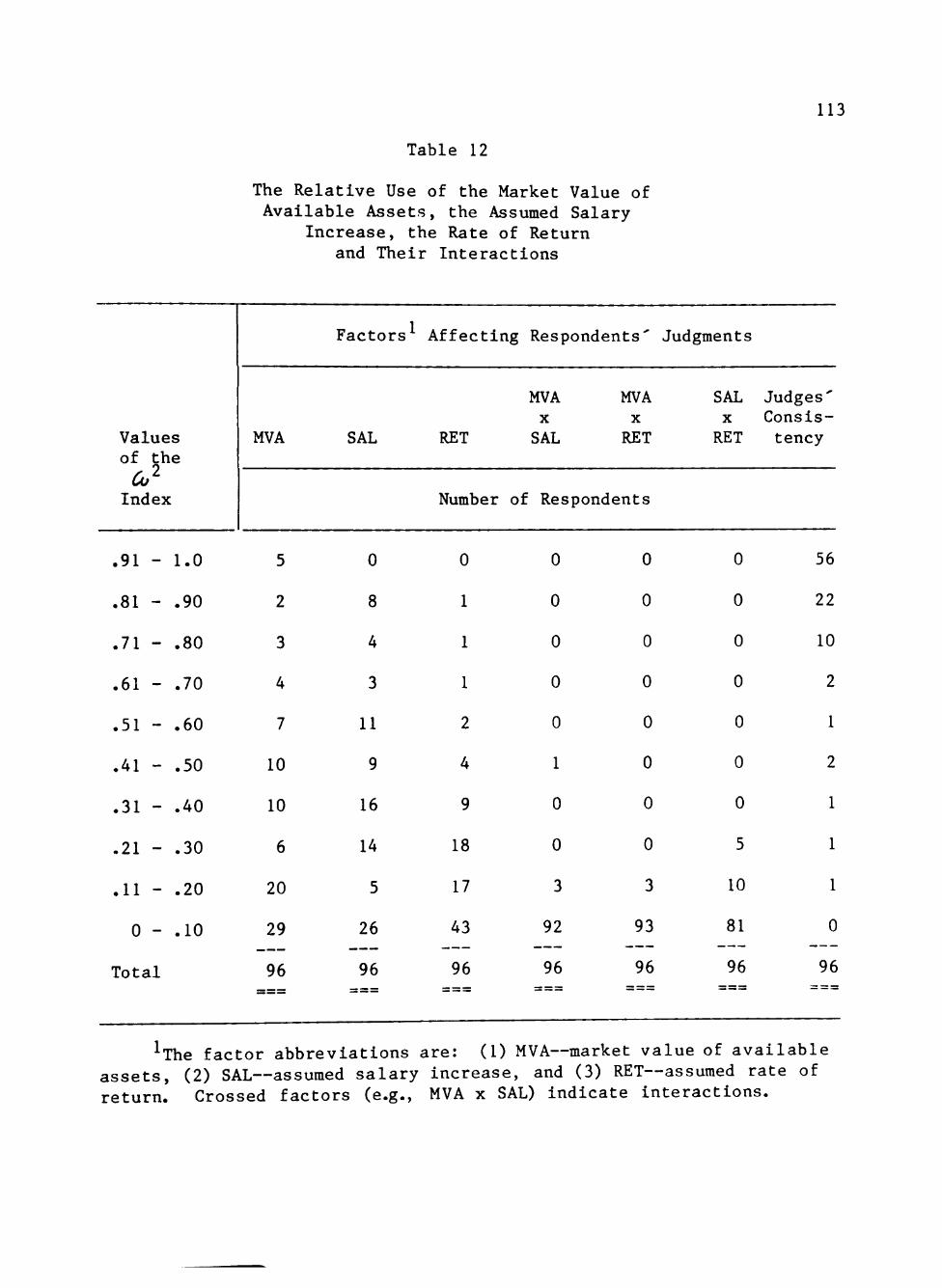

5. HYPOTHESES TESTS, RESULTS, AND IMPLICATIONS 82

Instrument Validation 82

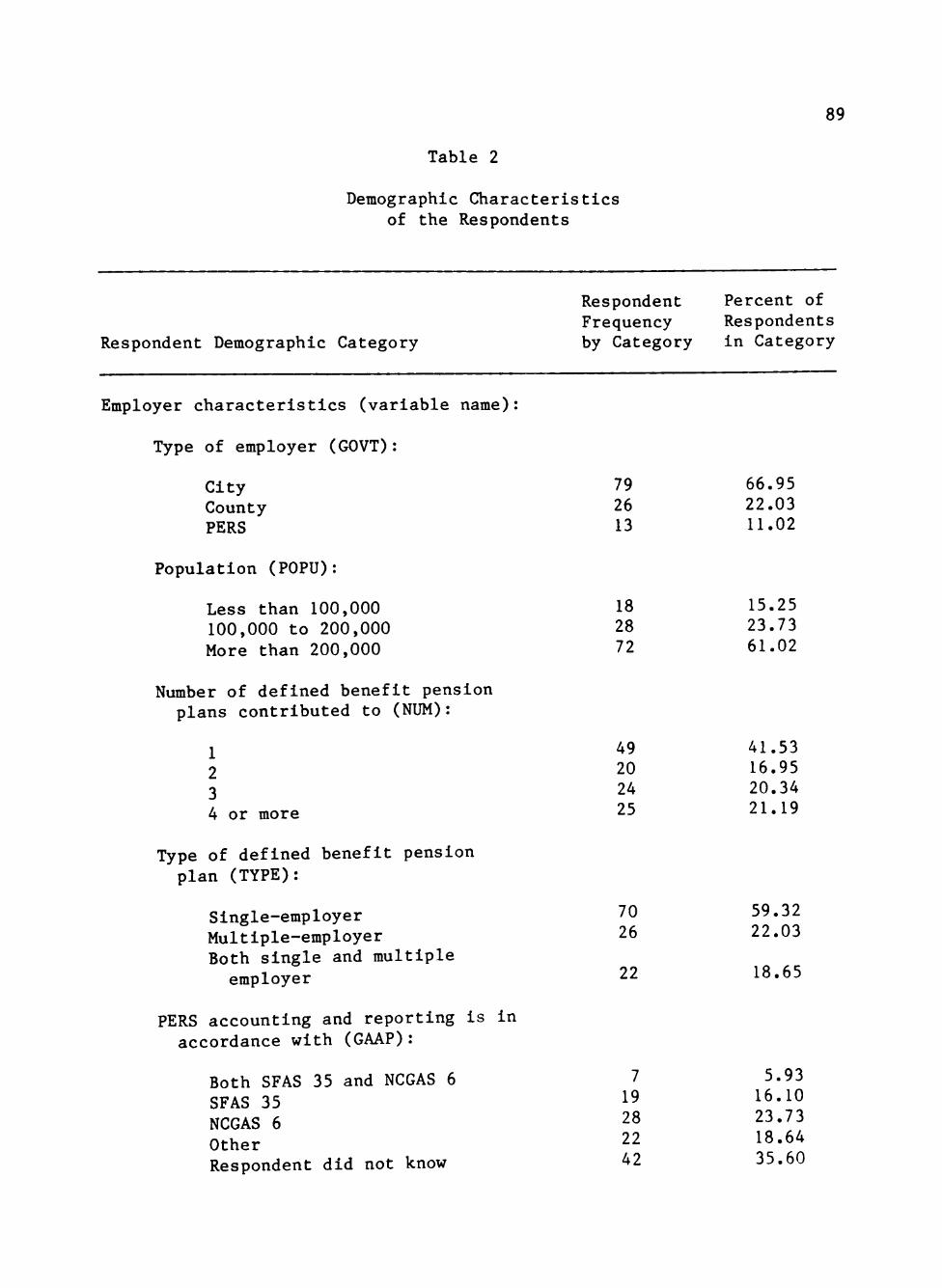

Respondent Demographics 85

Judgments About PERS 93

Judgment Consensus 114

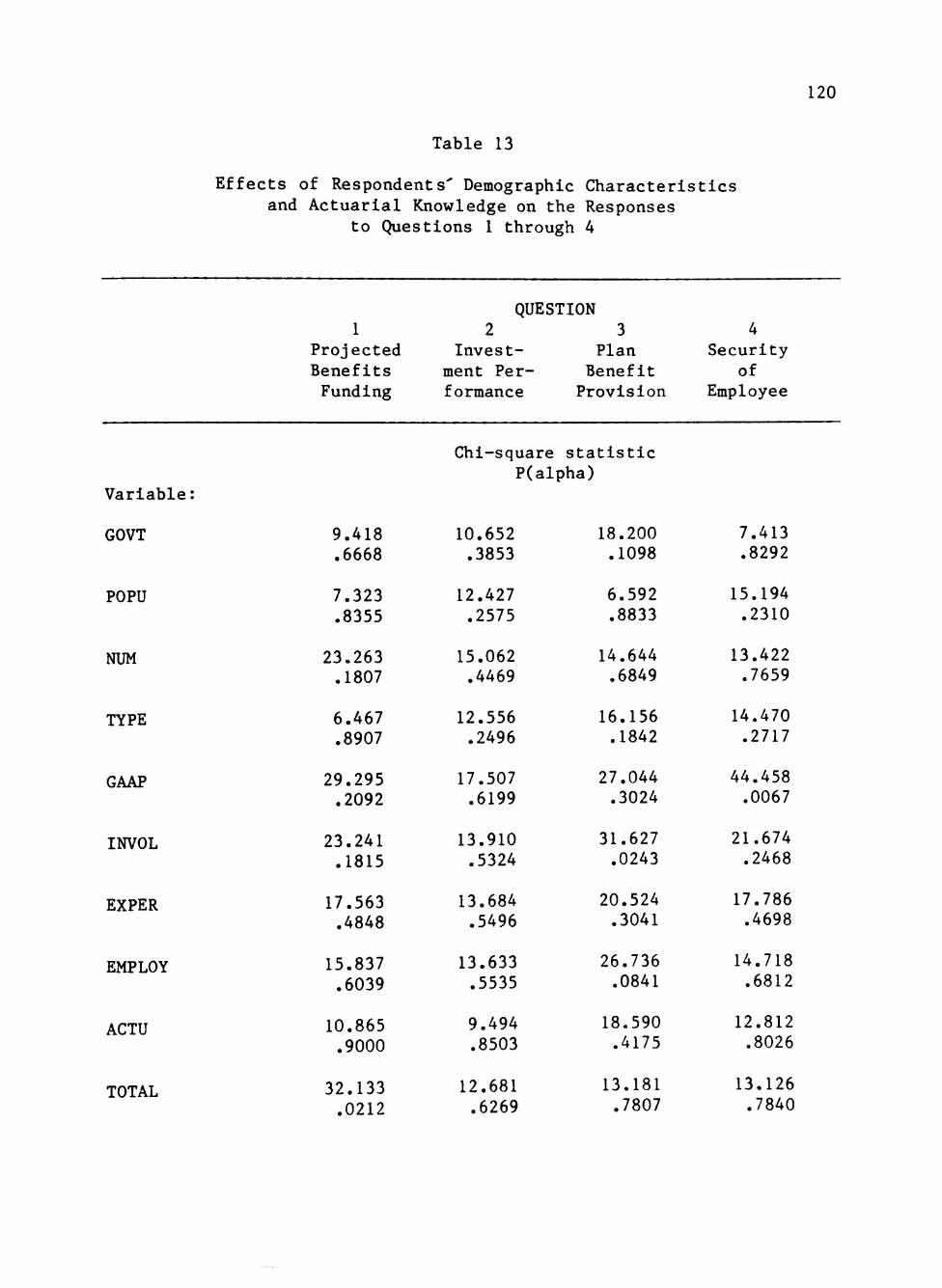

Effects on Judgments of Respondent Demographies . . . 119

Limitations 122

Summary 124

6. CONCLUSIONS 126

The Study: An Overview 126

The Research Results in Perspective 128

Changes in PERS Financial Reporting Practices

Suggested by the Results 129

Implications for Additional Research 137

BIBLIOGRAPHY 139

APPENDICES

A. COMPARISON OF SFAS 35 AND NCGAS 6 147

B. DESCRIPTION OF BRUNSWIK'S LENS MODEL 153

C. RESPONDENT PACKET—NCGAS 6 VERSION 157

D. RESPONDENT PACKET—SFAS 35 VERSION 174

iv

ABSTRACT

Improved accounting reports should result when standards setters

are provided with evidence regarding the ability of public employee

retirement system (PERS) financial report users to (1) interpret

reported pension information, and (2) Impound actuarial data. Accord

ingly, this study was conducted to gain insight into the decision making

process(es) of PERS financial report users and preparers.

A field experiment employing a simulated decision making situation

was used to gather data. Respondents made judgments about a fictitious

PERS and then completed two exercises that (1) measured their knowledge

of the effects of actuarial methods and assumptions on reported data,

and (2) tested their ability to properly consider these effects when

comparing the funding of the fictitious PERS to that of other pension

plans. Two general research questions were addressed: (1) does the

benefit-liability measure used for PERS financial reporting and/or the

amount of supplemental disclosure affect users' perceptions of the PERS

financial condition, and (2) do users of PERS financial statements

understand the effects that actuarial assumptions have on the reported

benefit-liability measure?

Analysis of the responses produced these findings: (1) respondents

appeared to be functionally fixated on the reported funding status of

the PERS and did not properly consider the underlying factors that

affect this status; (2) a significant percentage of respondents under

stood the effects of the assumed rates of (a) salary increase and (b)

return on plan assets on reported pension obligations, but did not

recognize the effects of the actuarial cost methods presented; (3) mean

responses were not affected by the presence of 10-year trend data;

however, the inclusion of 10-year data did result in improved judgment

consensus; (4) fixation on the reported funding status of the fictitious

PERS was not limited to those respondents that had limited actuarial

knowledge, but was found in all respondent groups; and (5) demographic

characteristics had only a limited effect on respondent's decision

models.

These findings indicate (1) that communication between PERS finan

cial report users and preparers needs Improvement, and (2) that

financial report users have difficulty incorporating actuarial

Information in their judgments. Accordingly, standards setters should

standardize PERS reporting practices and/or seek ways to improve PERS

disclosures.

VI

LIST OF TABLES

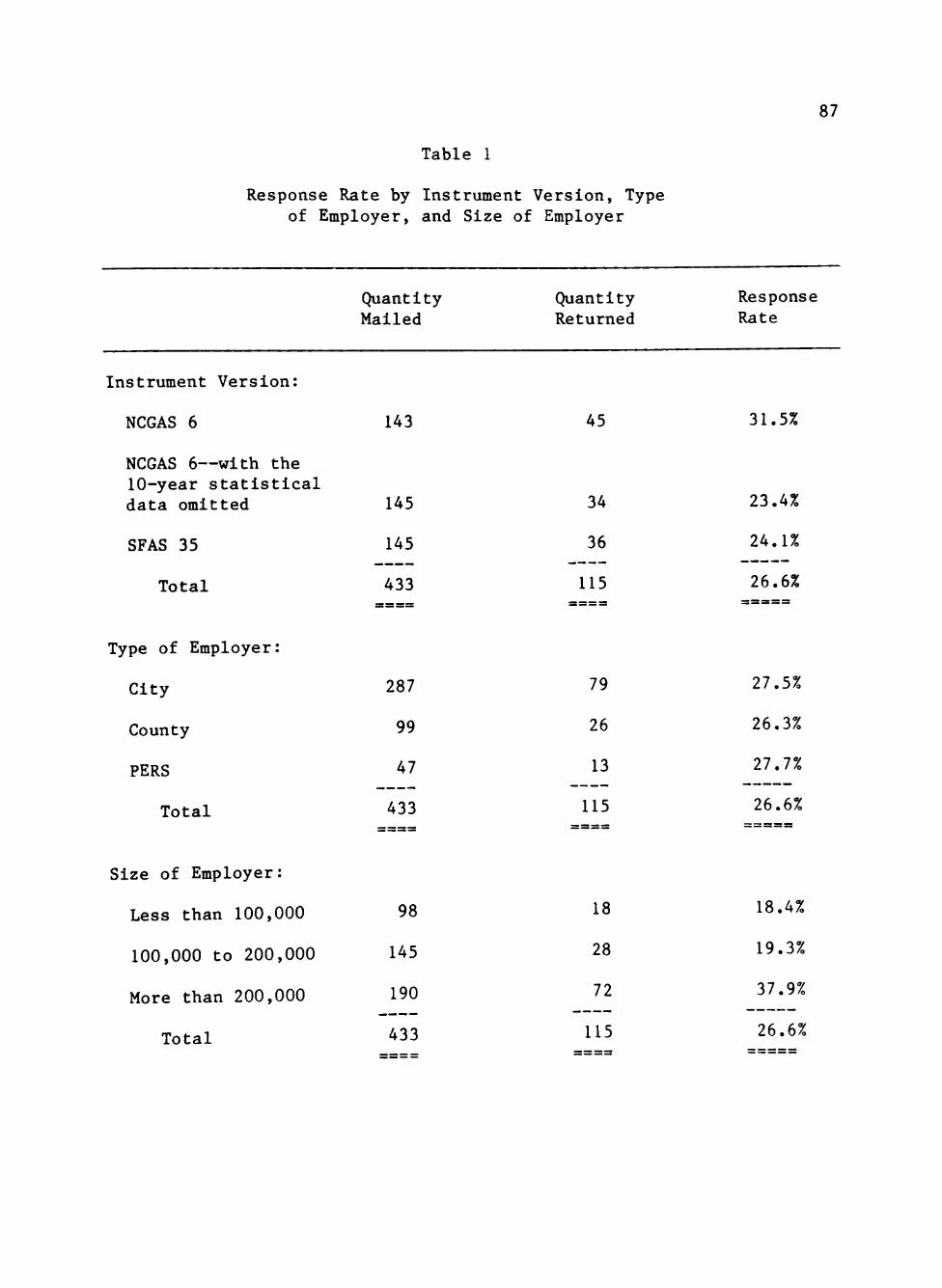

1. Response Rate by Instrument Version, Type of Employer, and

Size of Employer 87

2. Demographic Characteristics of the Respondents 89

3. Respondents' Knowledge of the Effects of Selected Actuarial Variables on the Reported Benefits Obligation of a PERS . . 92

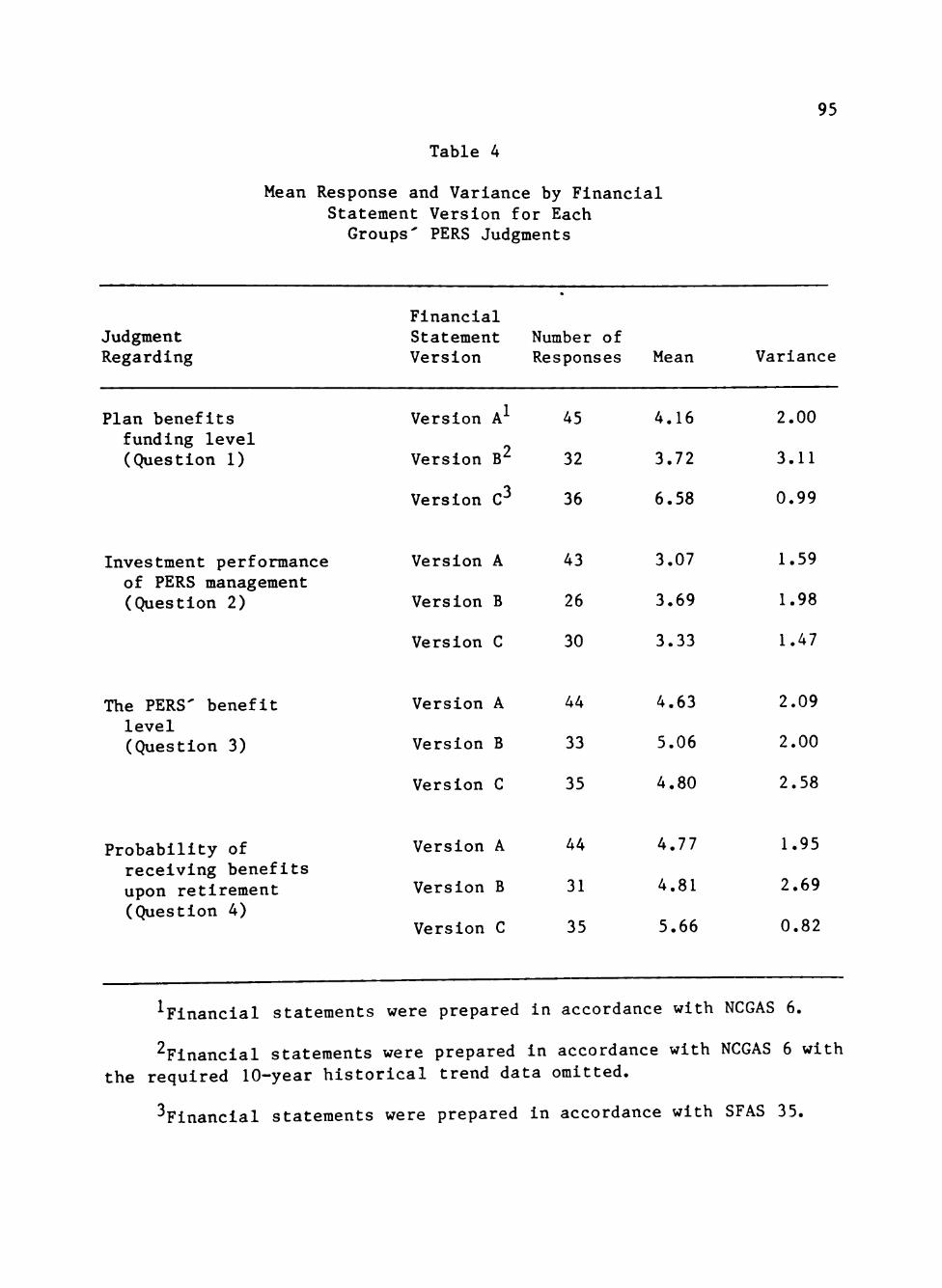

4. Mean Response and Variance by Financial Statement Version for Each Groups' PERS Judgments 95

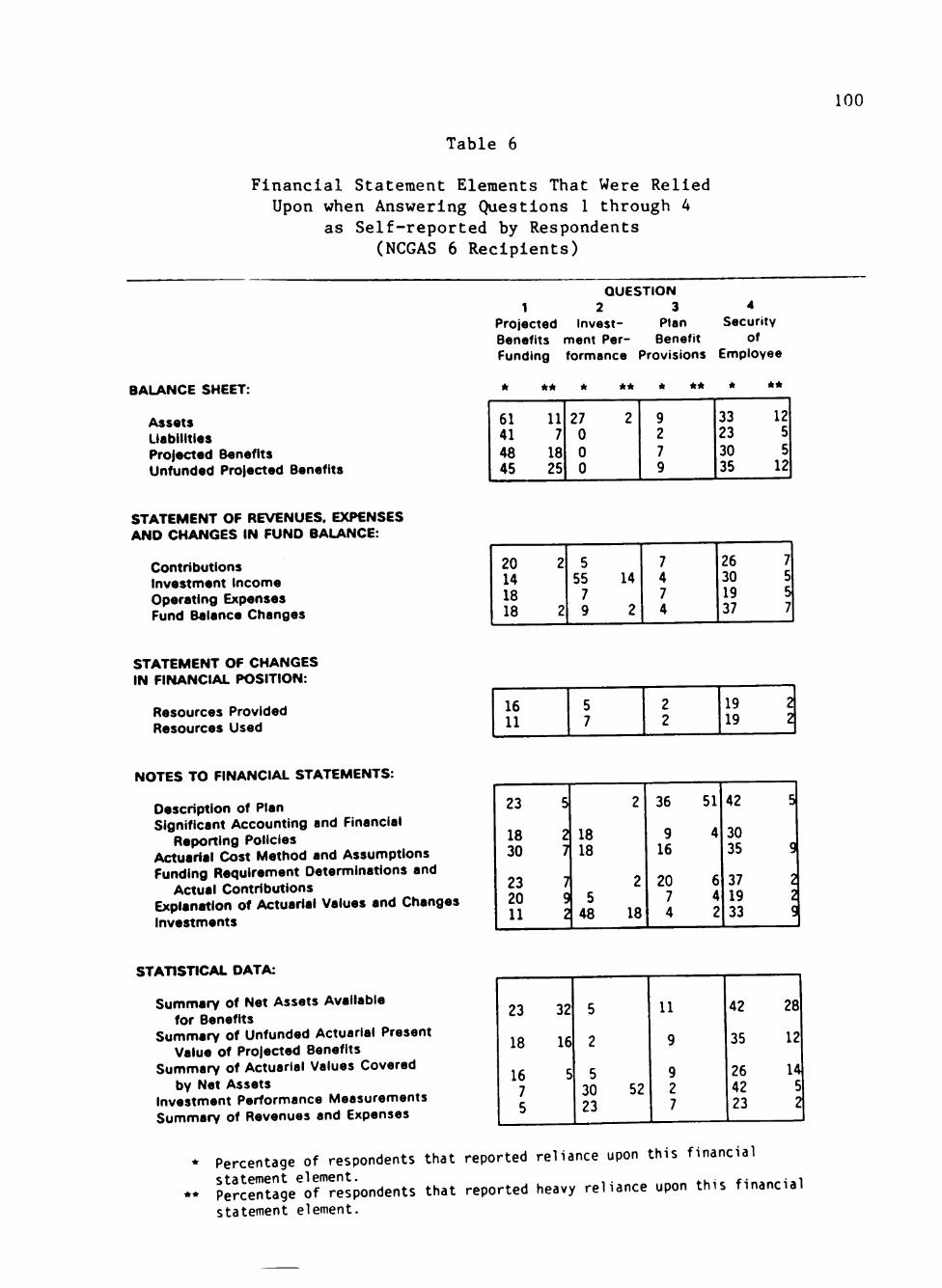

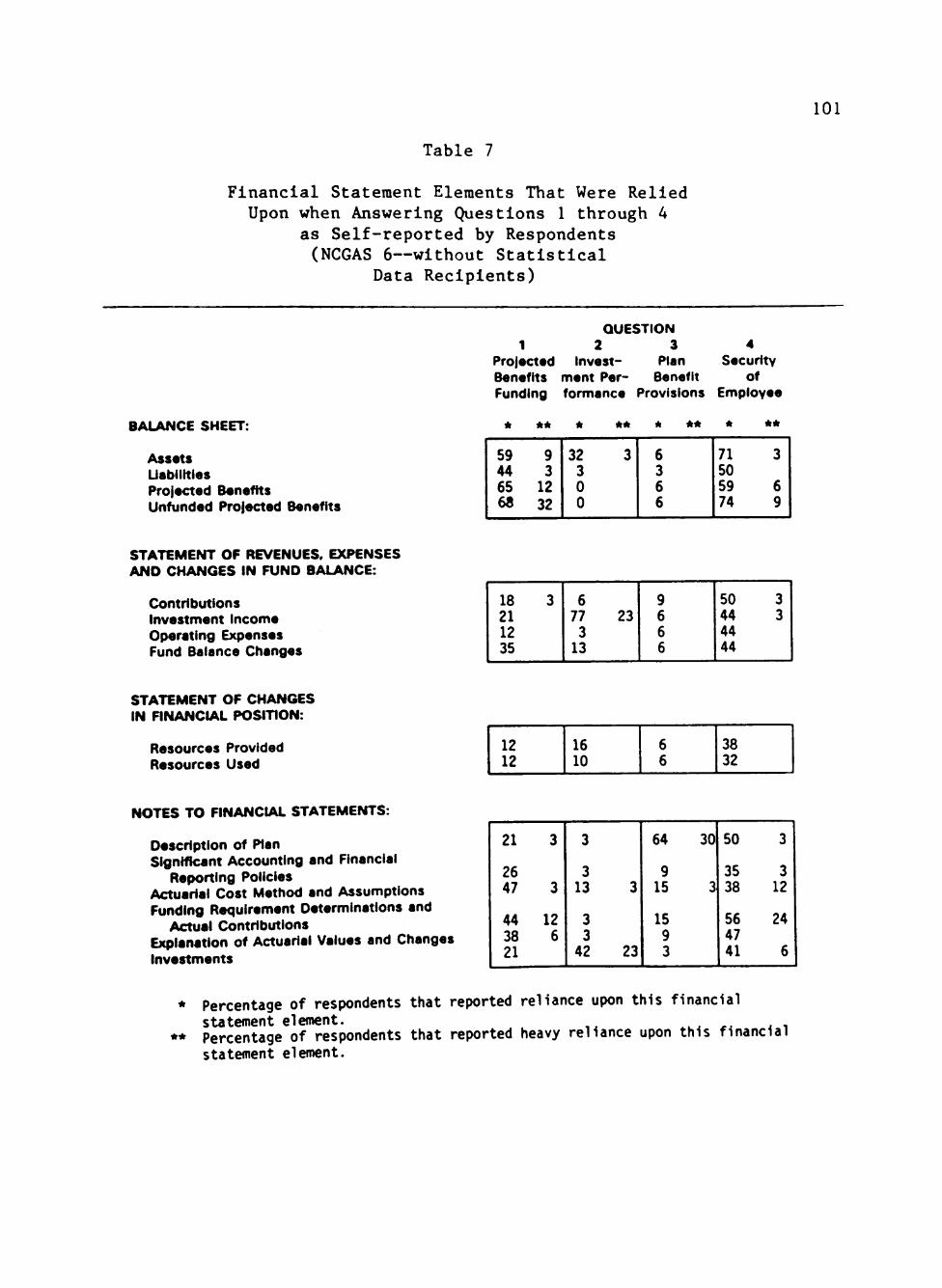

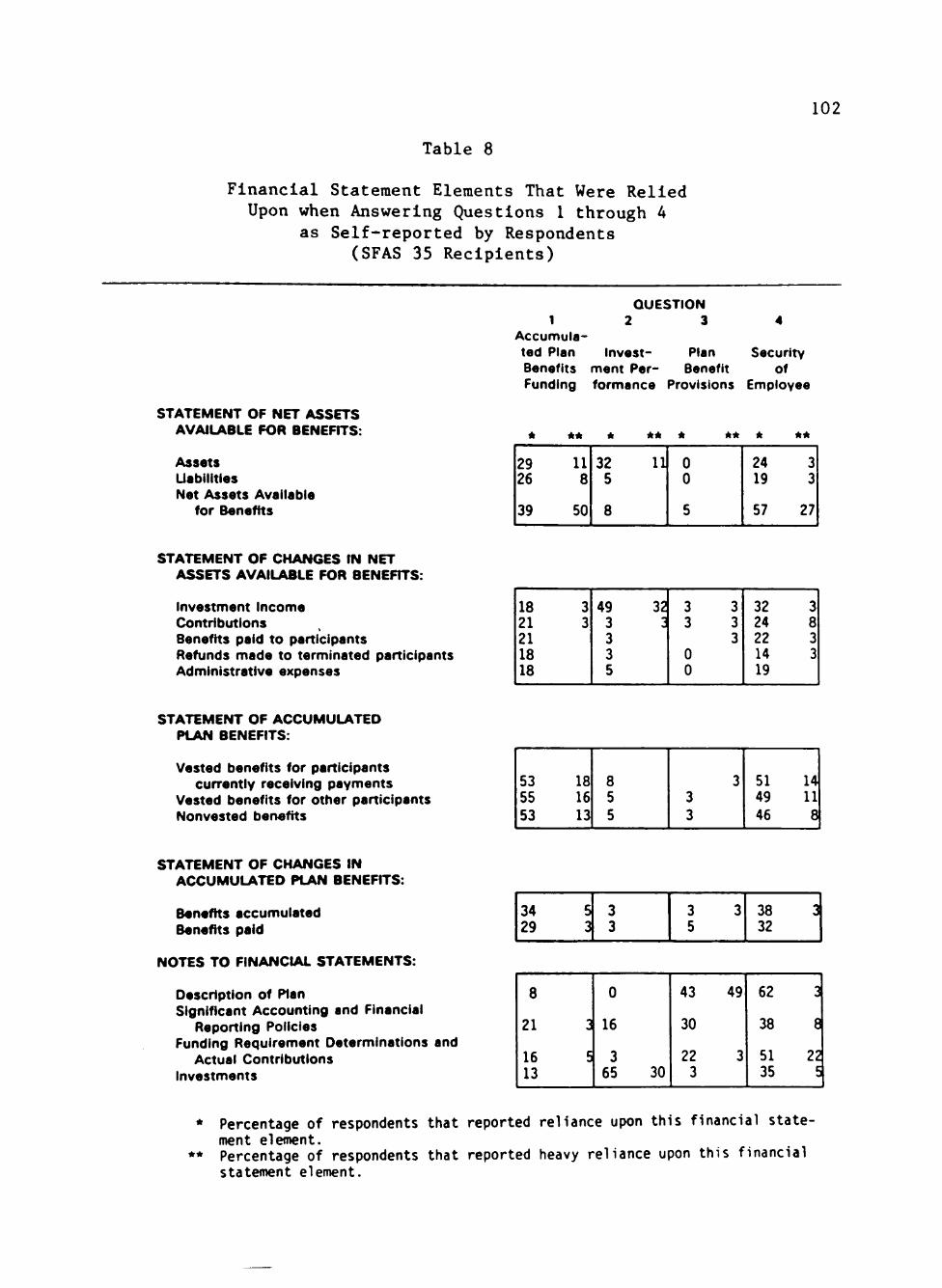

5. Effects of Financial Statement Format on the Responses to Questions 1 through 4 97

6. Financial Statement Elements That Were Relied Upon when Answering Questions 1 through 4 as Self-reported by Respondents (NCGAS 6 Recipients) 100

7. Financial Statement Elements That Were Relied Upon when Answering Questions 1 through 4 as Self-reported by Respondents (NCGAS 6—without Statistical Data Recipients) 101

8. Financial Statement Elements That Were Relied Upon when Answering Questions 1 through 4 as Self-reported by Respondents (SFAS 35 Recipients) 102

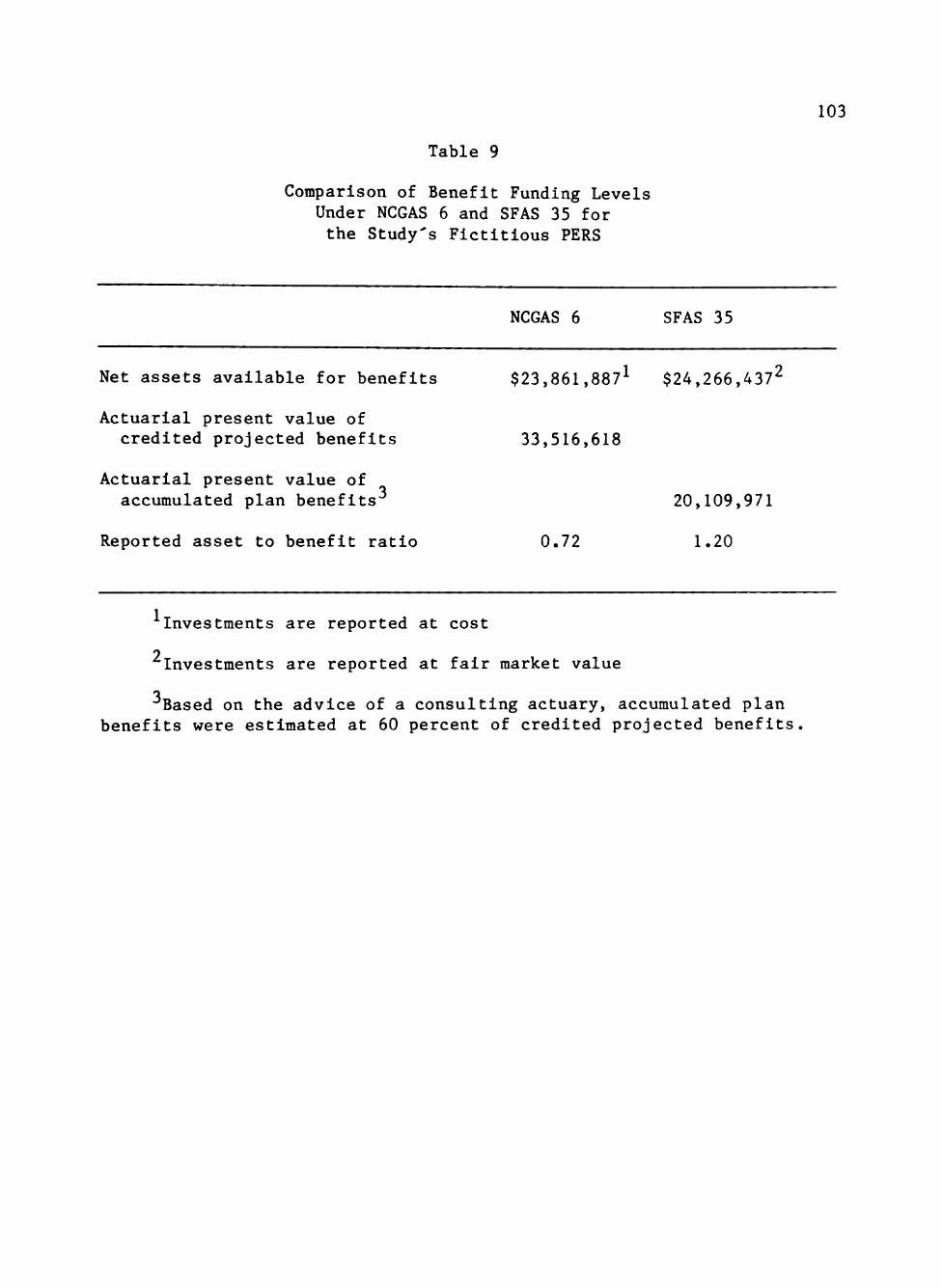

9. Comparison of Benefit Funding Levels Under NCGAS 6 and SFAS 35 for the Study's Fictitious PERS 103

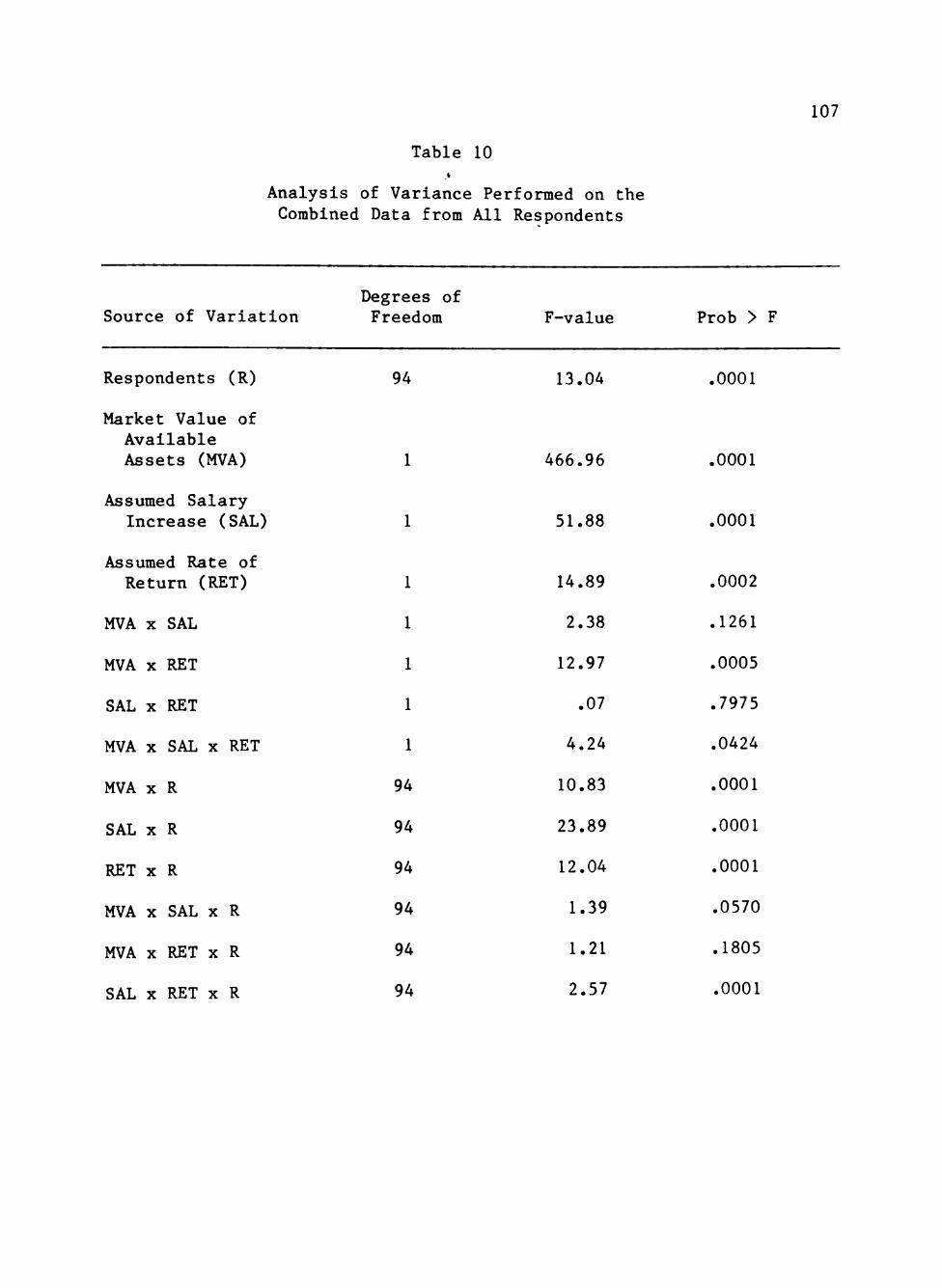

10. Analysis of Variance Performed on the Combined Data from All Respondents 107

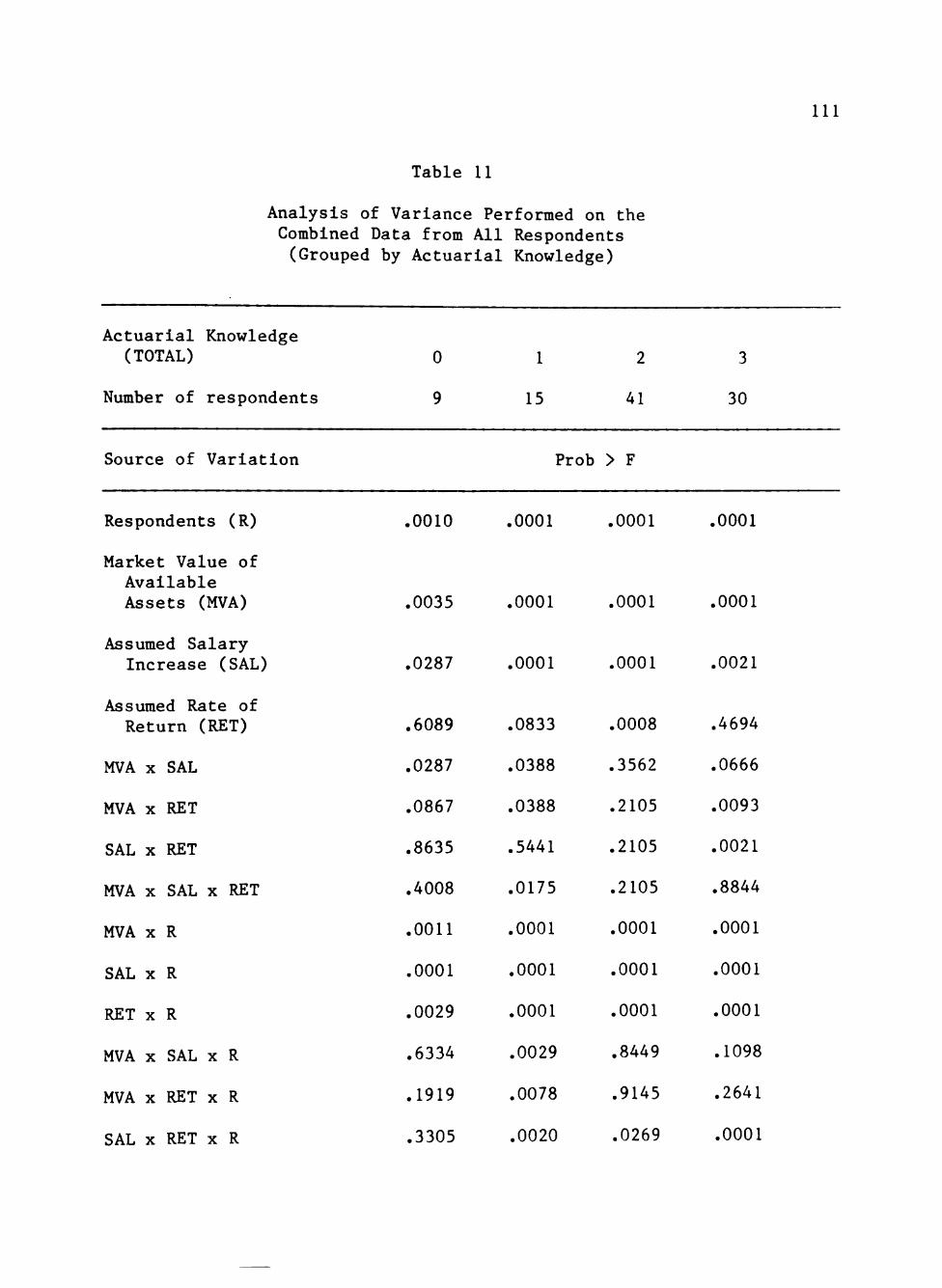

11. Analysis of Variance Performed on the Combined Data from All Respondents (Grouped by Actuarial Knowledge) Ill

12. The Relative Use of the Market Value of Available Assets, the Assumed Salary Increase, the Rate of Return and Their Interactions 113

13. Effects of Respondents' Demographic Characteristics and Actuarial Knowledge on the Responses to Questions 1 through 4 120

vli

LIST OF FIGURES

1. Pension Accounting Environment 4

2. Theoretical Model of Pension Plan Judgments 51

3. Hypothetical PERS Illustrative Asset Targets 53

4. Asset Target for a Hypothetical PERS Under Various Actuarial

Assumptions 55

5. Brunswik's Lens Model 62

6. Indices of Human Judgment 63

7. Research Design 68

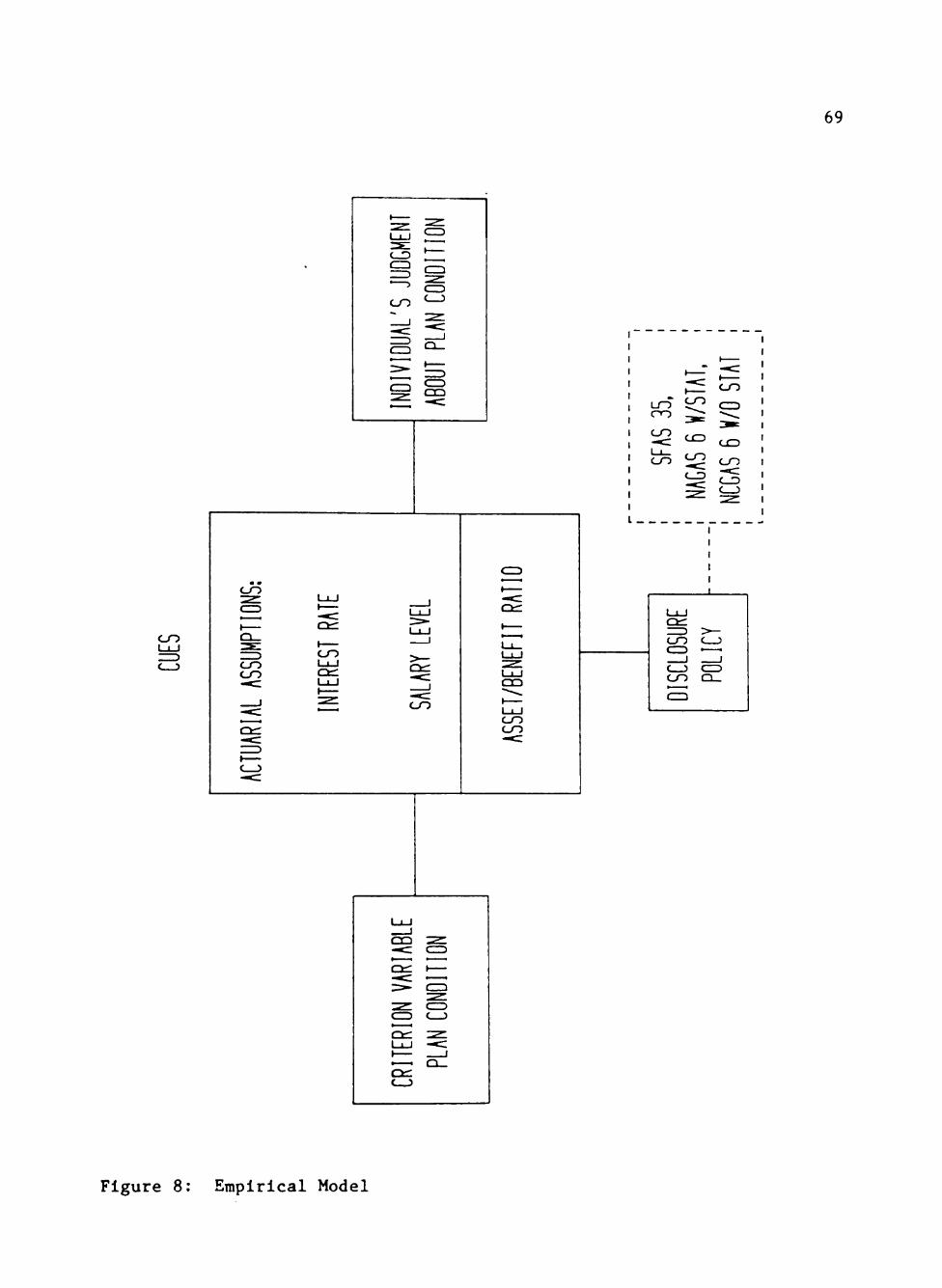

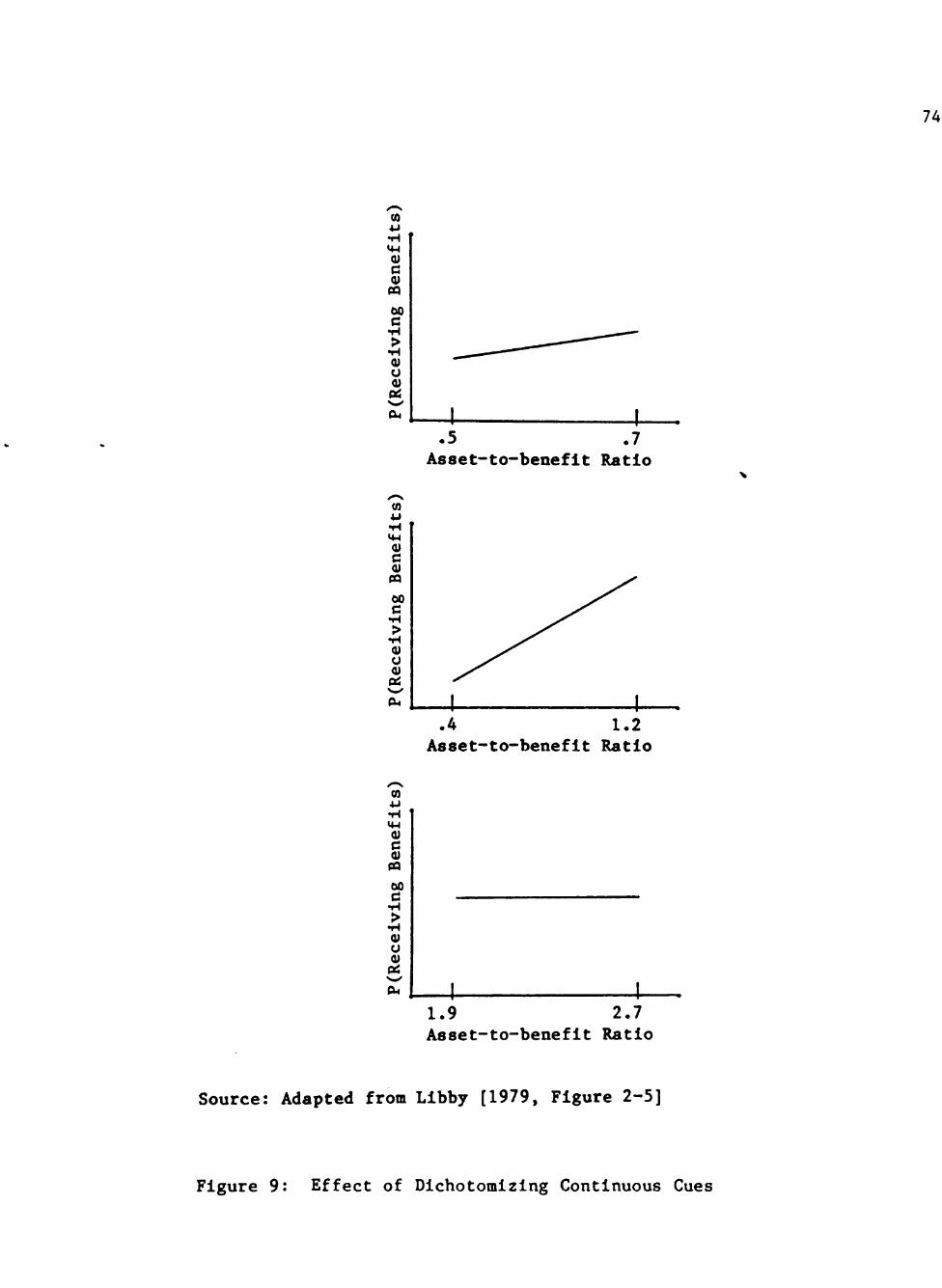

8. Empirical Model 69

9. Effect of Dichotomizing Continuous Cues 74

viii

CHAPTER 1

INTRODUCTION

Nature of the Problem

Concern about the relationship between (1) users' information

needs, and (2) the information content of accounting reports has pro

vided the impetus for accountants to re-examine both their perceptions

of users' Information needs and their ability to provide accounting

information that will serve these perceived needs. This concern is

evident throughout the Financial Accounting Standards Board's [FASB's]

conceptual framework project [e.g., FASB, 1976], and stems from observa

tions made by accounting researchers, and others, that may be

summarized:

1. Users of accounting information seek information that will

assist them in their decision making process.

2. The decision making process is complex, thus Implying a diverse

set of Information needs.

3. The accountant emphasizes the measurement of economic

phenomena; accordingly, the importance of relevant and reliable

(objective) information is stressed.

4. Accounting information may lack usefulness for some specific

decision models due to differences in orientation between users and

preparers.

The concern over the objectives of financial statements has not

been confined to the private sector. Both the FASB's Statement of

Financial Accounting Concepts No. 4, "Objectives of Financial Reporting

by Nonbusiness Organizations" [FASB, 1980], and National Council on

Governmental Accounting (NCGA) Concepts Statement 1, "Objectives of

Accounting and Financial Reporting for Governmental Units" [NCGA, 1982],

address the information content required by users of nonbusiness

financial statements.

Accounting researchers have studied the behavior of financial

statement users in an effort to (1) better understand htiman information

processing, and (2) develop some Insight into the more common decision

models. The ultimate objective of such research in accounting is to

Improve decision making [Ashton, 1982]. However, decision making must

be understood before it can be Improved. Thus, human Information

processing research in accounting concentrates on understanding, evalua

ting, and improving decisions based on accounting information.

Although previously published human Information processing studies

have been confined to the private sector [Libby, 1981, ch. 3-5; Ashton,

1982, ch. 7-8], the solution to several accounting and reporting prob

lems in the public sector may come from a better understanding of how

users of financial information make certain judgments. One of these

problems relates to the decision making process(es) of the users of

public employee retirement system (PERS) financial information and the

ability of these users to make judgments based on currently available

PERS financial statements.

General Pension Setting

PERS Growth

The provision of pension benefits is a matter of increasing concern

to many state and local governments because of the growth in PERS

enrollments and plan benefits. The General Accounting Office reports

that ". . . State and local plan enrollment and assets have increased at

an even faster rate than that of all pension plans" [1980, p. 1]. State

and local plan membership stood at 11.4 million persons in fiscal year

1982-83 [U.S. Department of Commerce, 1984]—up from 1.6 million in 1940

[General Accounting Office, 1980]. Further, the U.S. Department of

Commerce reports:

Total State and local government employee retirement system revenues for fiscal year 1982-83 amounted to $57.9 billion while their payments totaled $19.8 billion. In the last month of their 1982-83 fiscal year, these government agencies: . . . had amassed financial assets totaling $289.7 billion; paid recurrent benefits of $1.4 billion to 3.1 million persons for an average monthly payment of $464 per beneficiary. [1984, p. vi]

This growth in government pension plans has occurred, to some extent,

because of the promises of elected officials, as noted by Mautz:

Promises can be made in the present that escape accounting attention in the financial statements until much later. Promises of future pensions may get the waste hauled away or the transit system operating again right now, but those obligations may not be reported as obligations to be met by future taxpayers until much later, if ever. [1981, p. 56]

Pension Environment

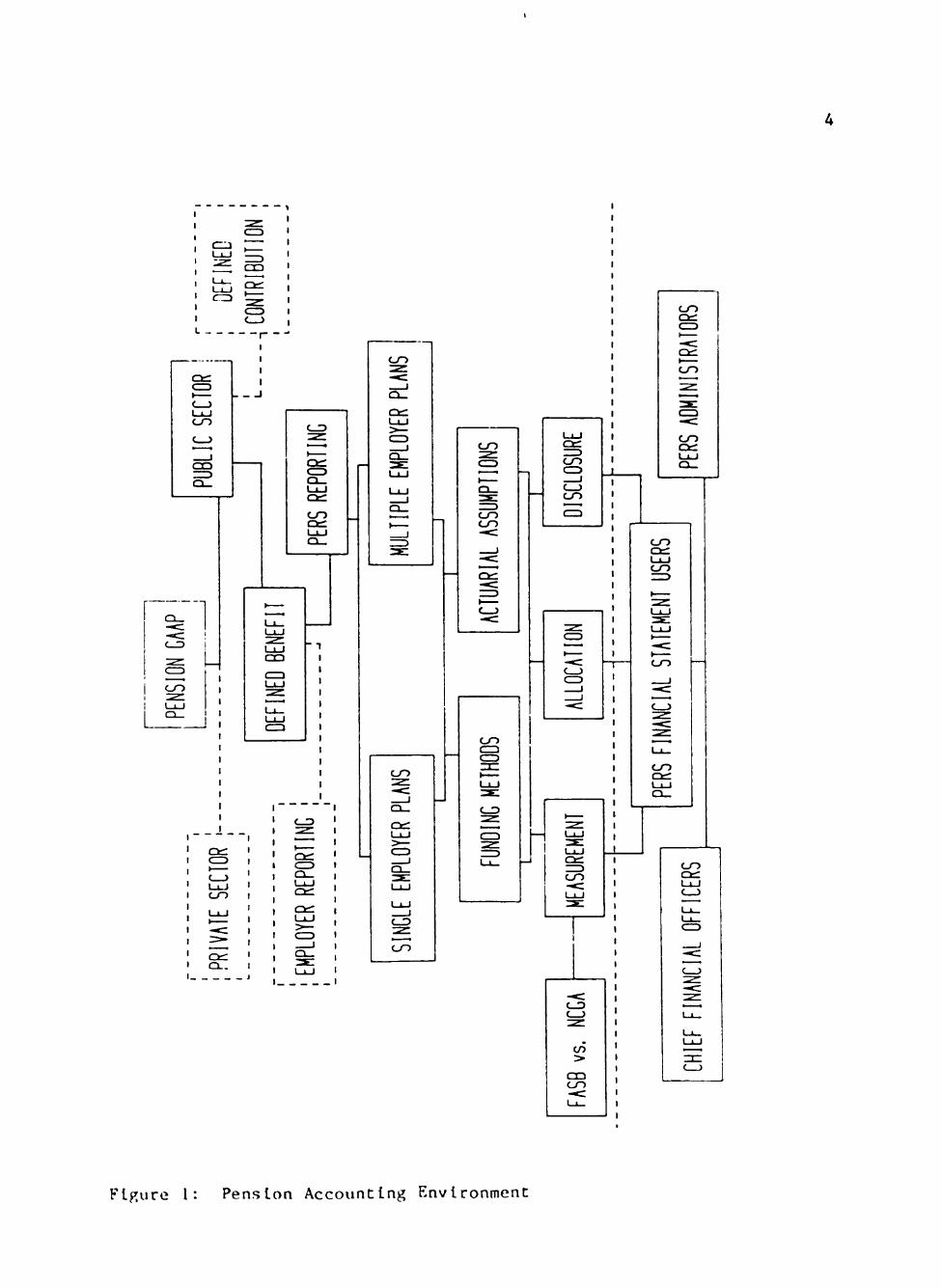

The pension reporting environment is complex—in part because of

the variety of pension arrangements used to provide employees with

retirement benefits. Figure 1 diagrams the PERS plan setting that

potentially affects pension accounting and financial reporting

Figure I: Pension Accounting Environment

techniques. In addition to the plan setting presented here, other

potentially material PERS environmental factors Include: legislative

mandates, pressures from public employee unions, legal actions, and the

political climate.

While both defined benefit and defined contribution pension plans

exist in the public sector, defined benefit plans are the most prevalent

in the public sector and are the focus of this study [Engstrom, 1984].

Under a defined benefit plan, each employee is entitled to the level of

benefits specified by the plan. Frequently, such benefits are based on

the length of employment and the employee's salary near the time of

retirement. In contrast, in a defined contribution plan, employee

retirement benefits are based on an allocated share of the plan's

available assets.

The existence of both single-employer and multiple-employer defined

benefit plans adds to the environmental complexity. As the name

Implies, single-employer PERS are sponsored by one employer (city,

county, or state) exclusively for its employees. When more than one

employer contributes to a plan, it is referred to as a multiple-employer

plan. A multiple-employer plan may serve as an Investment and admin

istrative agent for each participating employer or may be a pension

cost-sharing arrangement.

A final, and extremely Important, difference among PERS is the

method of financing the benefits provided by such systems. Unfortu

nately, some PERS are not funded on an actuarial basis [Wlnklevoss and

McGlll, 1979]. Instead, such plans employ either pay-as-you-go or

terminal funding methods, relying on uncertain and often inadequate

legislative appropriations to finance benefit payments during each

fiscal period [NCGA, 1968]. At the opposite end of the scale, a number

of PERS undergo periodic actuarial valuations and all liabilities,

present and prospective, are advance funded [Engstrom, 1984]. Between

these two extremes are numerous PERS that are designed to be actuarially

sound but have "manageable" unfunded actuarial liabilities resulting

from such circumstances as Inadequate provisions for prior service

costs, investment restrictions, or benefit increases too liberal to be

met with existing funding patterns.

The Nature of PERS Liabilities

Two fundamentally different approaches to benefit-liability

measures can be used in reporting the financial status of defined

benefit PERS. The plan-termination liability (PTL)—based on the

assumption that the plan will be terminated on the valuation date—is

the dollar value of each active member's accumulated plan benefit. The

actuarial assumptions used to calculate this liability may differ from

those used in the annual valuation. For example, the appropriate rate

of interest is the rate on which currently available annuity contracts

are based—which may not coincide with the actuarially assumed valuation

rate. Accumulated plan benefits are based on the employee's current

salary level and exclude consideration of ancillary benefits (e.g.,

disability, death, and early retirement benefits) since—if the plan

were actually to terminate—the only benefit the plan members would be

entitled to would be a deferred benefit starting at the plan's normal

retirement age. The PTL also Includes any contributions made by non-

vested employees.

The second approach to benefit-liability measures—termed the

plan-continuation liability (PCL)—Is predicated on the assumption of an

ongoing pension plan. Accordingly, PCL calculations are based on bene

fits allocated to date—including ancillary benefits—and use the

actuary's valuation assumptions. Typically, these allocated benefits

relate to each active member's projected benefit at retirement, and thus

are based on his expected future salary level. Under both approaches,

the liability for benefits attributable to nonactive members equals the

actuarial value of benefits payable to them.

Several arguments favor the PCL as the benefit-liability measure

to use for PERS reporting:

1. The PCL recognizes the effects on reported benefits of

ancillary benefits and future salary increases, both of which are

expected to occur in an ongoing plan.

2. The PCL is preferred by PERS administrators since it is more

conservative than the PTL approach and results in a larger unfunded

pension liability being reported. In turn, this larger reported

liability provides an Incentive for government officials to maintain or

increase levels of plan funding.

3. Few municipalities have defaulted on pension obligations, and

even in those cases the courts have upheld the rights of workers to

receive their benefits [Inman, 1982].

GAAP Controversy

Much of the controversy surrounding PERS accounting and financial

reporting is due to the existence of two conflicting sets of official

8

pronouncements on the topic—one by the FASB, the other by the NCGA.

The FASB and the NCGA disagree about (1) the user(s) and objectives of

PERS financial statements, (2) the amount of Information to provide to

users, and (3) the appropriate benefit-liability measure to use. The

FASB's pronouncement. Statement of Financial Accounting Standards

No. 35 (SFAS 35), "Accounting and Reporting by Defined Benefit Pension

Plans" [March, 1980], Is predicated on the PTL approach. Although

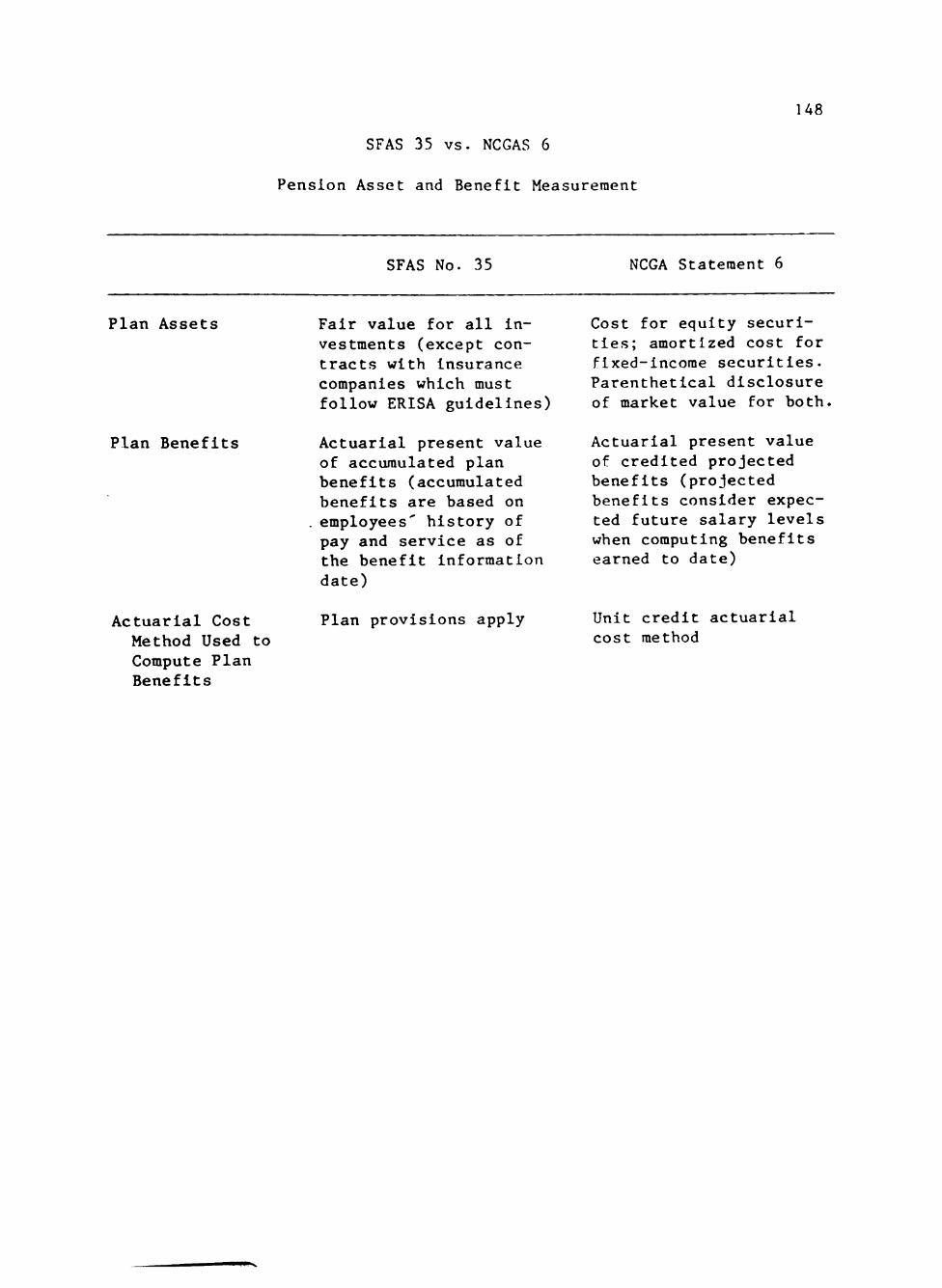

SFAS 35 states that "an assumption of an ongoing plan shall underlie the

other assumptions used . . ." [par. 20], its provisions appear to be

more consistent with a terminating plan assumption. For example, SFAS

35 requires that (1) accumulated plan benefits (based on current salary

levels) and (2) market values for plan investments be used for reporting

purposes; both are consistent with a PTL approach, as is the provision

that permits the use of actuarial assumptions that are Inherent in

commercially available Insurance contracts that could be purchased to

provide employee benefits.

In contrast, the NCGA's Statement 6 (NCGAS 6), "Pension Accounting

and Financial Reporting: Public Employee Retirement Systems and Local

Government Employers," [June, 1983], is predicated on the PCL approach.

For reporting purposes, NCGAS 6 requires (1) the use of credited pro

jected benefits (based on expected future salary levels) and (2) that

Investments be reported at cost (parenthetical disclosure of market

value is also required). NCGAS 6 also requires that the rate of

Interest and other actuarial assumptions used in the actuarial valuation

be disclosed. NCGAS 6 differs further from SFAS 35 in the level of

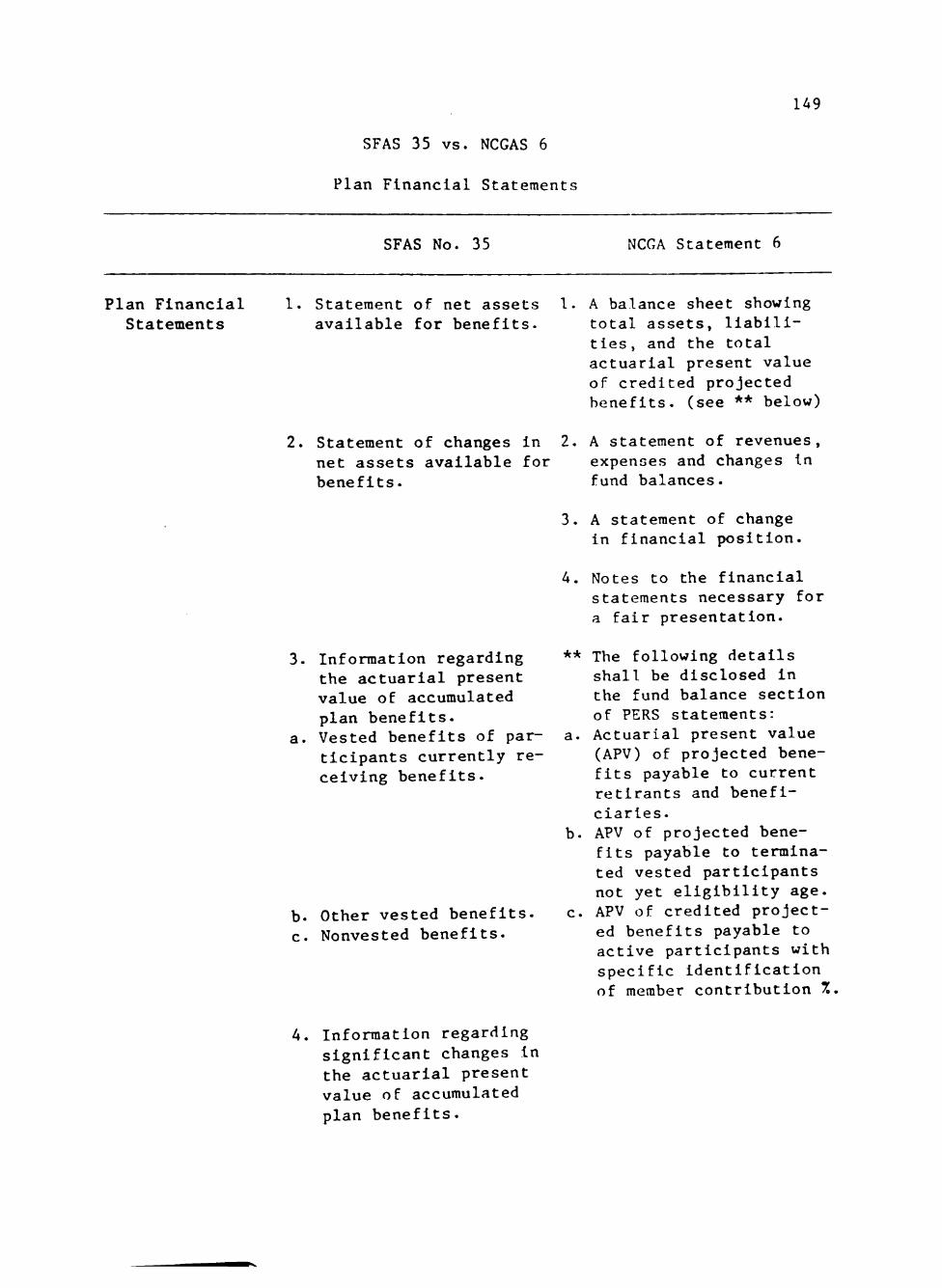

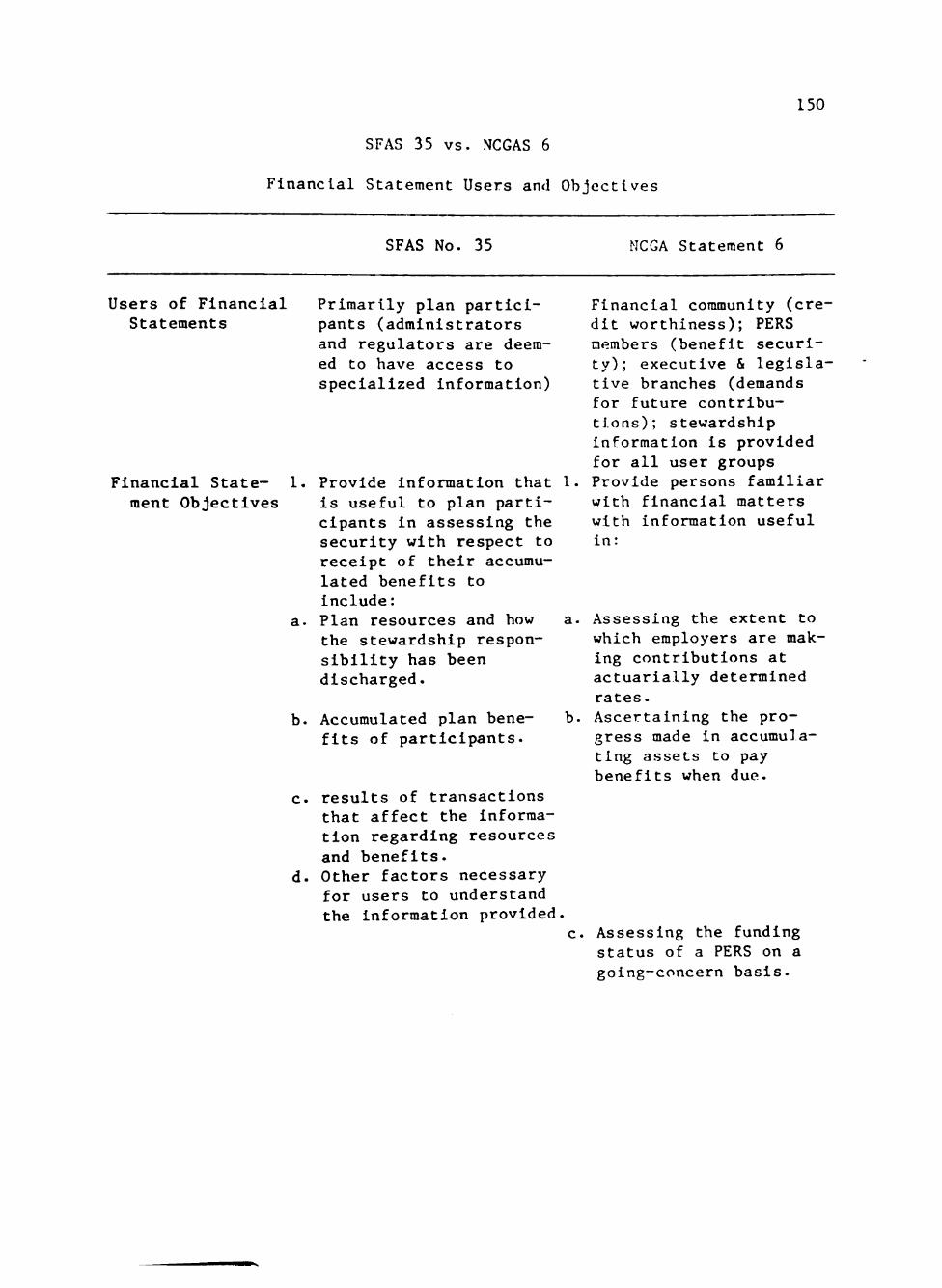

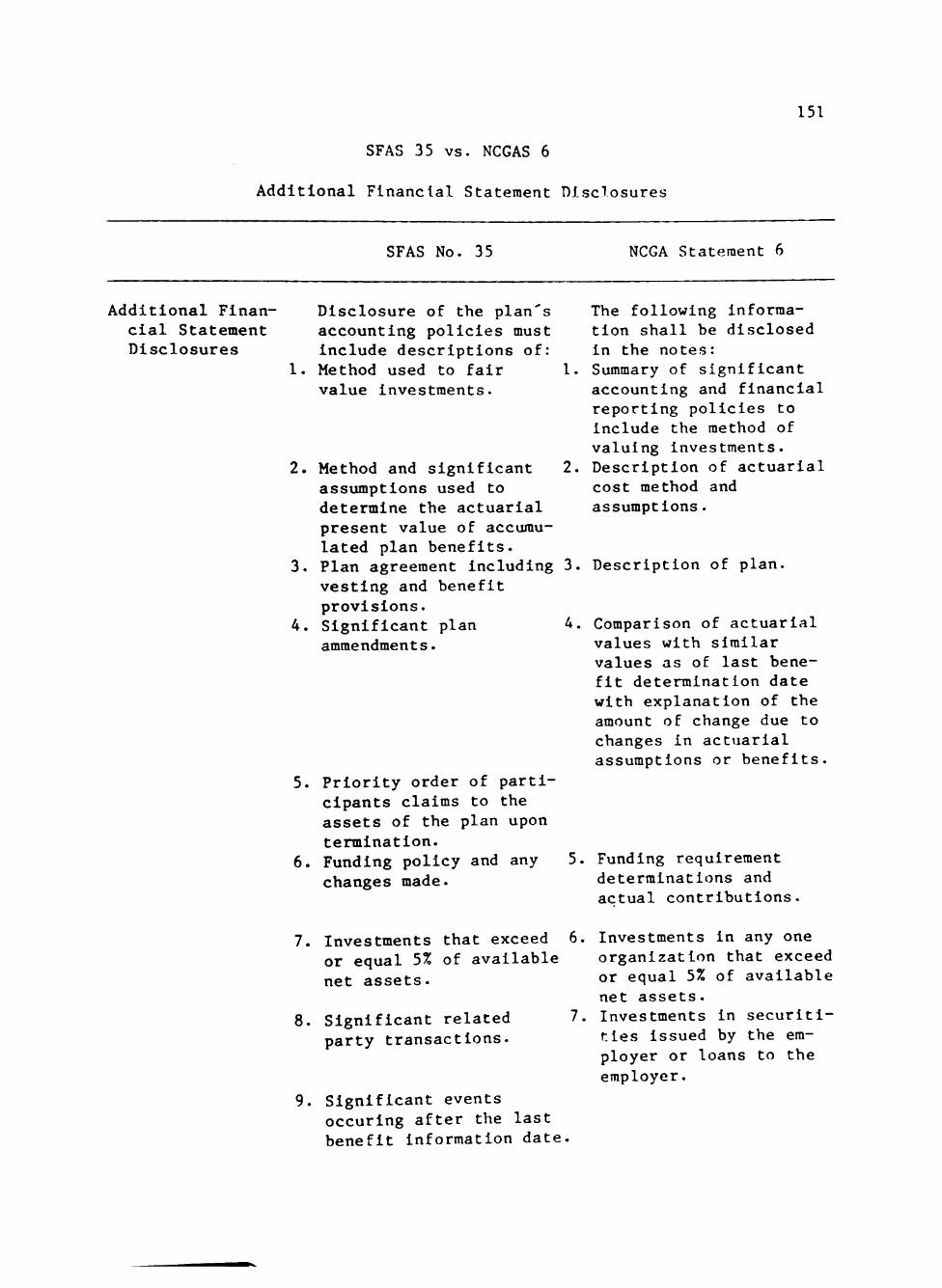

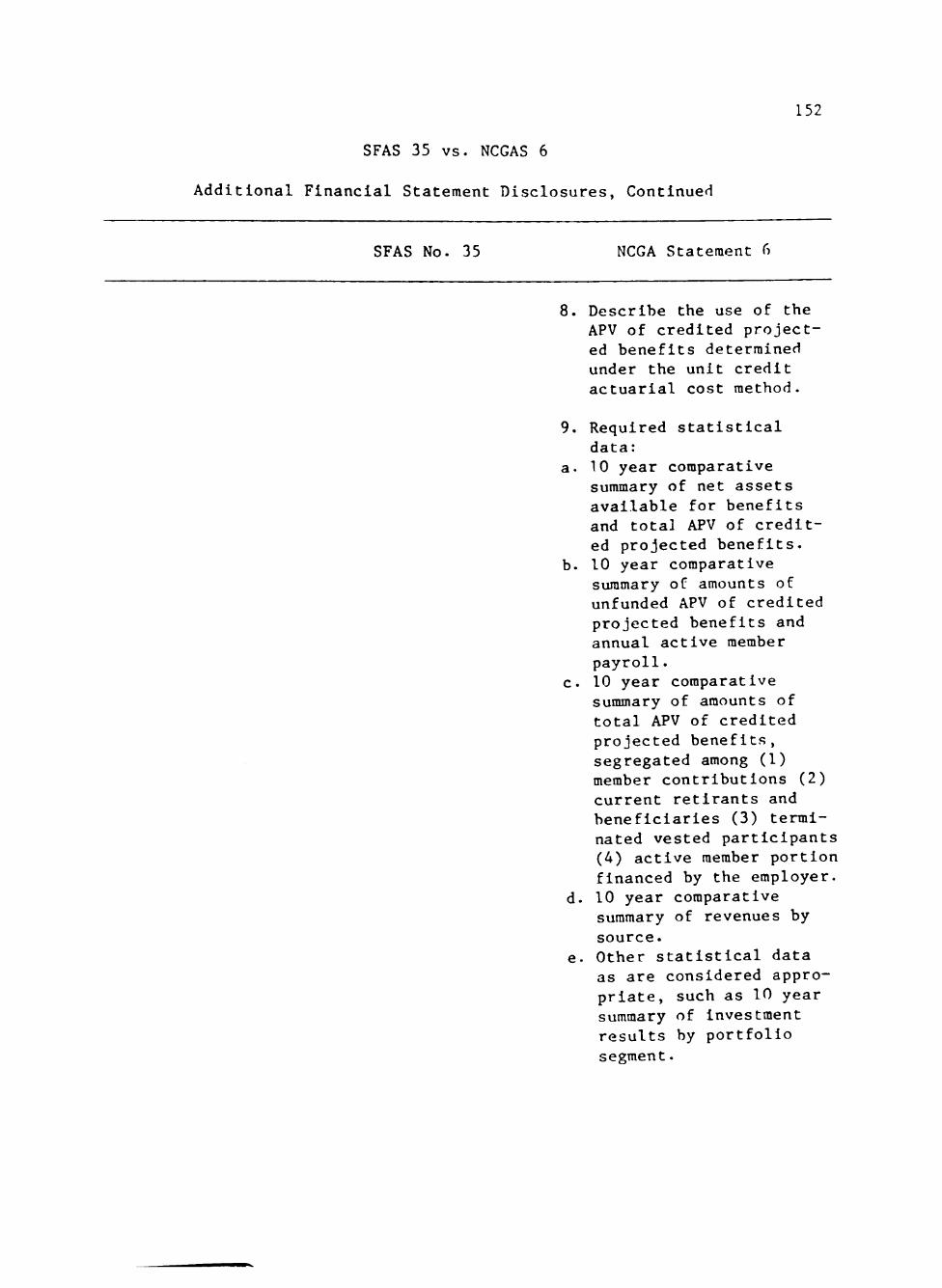

disclosure required. (Appendix A suimnarlzes the SFAS 35 and NCGAS 6

accounting and reporting requirements.)

As a temporary solution to the problem caused in the public sector

by conflicting official pronouncements, the NCGA and FASB agreed to

mutually defer the effective dates of their respective pronouncements

for PERS reporting. The newly formed Governmental Accounting Standards

Board (GASB) placed two pension projects on its initial agenda and,

until it issues a Statement(s) on the topic, has recognized both SFAS 35

and NCGAS 6 as acceptable sources of GAAP. The GASB also recognizes

Audits of State and Local Governmental Units (ASLGU) as authoritative,

thus potentially adding to the controversy since ASLGU recognizes

Governmental Accounting, Auditing, and Financial Reporting [1968]

(GAAFR68) as the primary source of GAAP for governments. Further, GASB

Statement 1, "Authoritative Status of NCGA Pronouncements and AICPA

Audit Guide" [July, 1984] (GASBS 1), recognizes NCGA Statement 1,

"Governmental Accounting and Financial Reporting Principles" [March,

1979] (NCGAS 1), as authoritative, and NCGAS 1 has been interpreted as

effectively recognizing the GAAFR68 method of pension accounting by

presenting that approach in its illustrative financial statements.

Accordingly, a third alternative exists for PERS accounting and finan

cial reporting. GAAFR68 contains guidance on pension accounting and

reporting that differs from both SFAS 35 and NCGAS 6, emphasizing the

trust fund nature of pension funds. GAAFR68 also provides no guidance on

acceptable (for reporting purposes) actuarial methods and requires no

disclosure of plan benefit provisions, accounting and funding methods,

or actuarial assumptions.

10

Actuarial Status

Actuaries determine the probable future benefits of a particular

plan and advise the PERS and sponsoring employer on the funding policy

to adopt. Thus, actuaries heavily Influence pension accounting and

financial reporting. Both economic assumptions (e.g.. Interest rate,

inflation rate, salary-level increases) and employee related assumptions

(e.g., termination rates, turnover, salary scale, survivor election)

must be made in the process of estimating plan benefits and determining

the required plan funding. These assumptions can materially affect both

reported pension information and plan funding [Wlnklevoss, 1977].

Walker [1984] notes that:

Actuarial assumptions are sensitive to small changes. Some assumptions, such as the interest rate assumption, are extremely sensitive. Even the small changes actuaries make in assumptions to provide safety margins can have a significant effect on pension costs [and PERS financial statements] for a given year. [p. 194]

The correct treatment of these assumptions is the basis for consi

derable controversy among accountants. Some contend that comparabil

ity in accounting and financial reporting will be enhanced if (1) all

PERS are required to use the same actuarial cost method, or (2) the

range of acceptable actuarial assumptions for accounting purposes is

narrowed [Wlnklevoss and McGlll, 1979; Walker, 1984; Schwartz and

Lorentz, 1984]. Schlpper and Weil [1982] state that: ". . . one cannot

measure the present value of future cash outflows for pensions from a

pension accounting that is based on some of the actuarial cost methods

that are allowed under currently accepted accounting principles"

[p. 807]. They also note that: "because the various actuarial methods

11

are based on data and assumptions that may preclude drawing inferences

about other methods not used, even sophisticated users of the data may

not be able to derive their own estimates of the future pension cash

flows" [p. 816]. Thus, they Imply that the range of permissible

actuarial cost methods should be narrowed—given the financial account

ing objective that information useful in assessing future cash flow

prospects should be provided [SFAC No. 1, par. 37]. Similar views were

adopted by the Federal Government.

Uniform reporting for the Federal Government's 50-plus pension

plans is required by Public Law 95-595. This law extends the annual

financial and actuarial reporting requirements of the Employee Retire

ment Income Security Act of 1974 [ERISA]—passed in response to the

rapid growth of the private pension system and concern over the funding

status of many plans [Schwartz and Lorentz, 1984]—to most Federal

pension plans. (However, Federal plans are not subjected to ERISA's

funding, minimum benefit level, or individual participant reporting

requirements.) Webster [1984] notes that:

. . . guidelines [for the Implementation of Public Law 95-595] were Issued that paralleled [SFAS 35]. The guidelines went further, however, specifying a rate of inflation to be used in actuarial computations, disclosing the computation of the unfunded actuarial accrued liability, disclosing the plan's normal cost, presenting a funding method whereby the unfunded liability is amortized in level dollar amounts over 40 years, presenting the future flow of plan assets, and requiring similar statistical data to that reported in ERISA Form 5500— Schedule B. The guidelines also require an opinion of an enrolled

actuary stating that actuarial assumptions used in preparing the report are reasonable and that the report is complete and accurate.

Others believe that the specification of actuarial assumptions or

accounting and reporting requirements similar to those of Public

12

Law 95-595 places an unnecessary burden on PERS and government employers

and would not achieve the desired comparability between plans [Buxbaum

and Quindlen, 1984].

Specific Problem to be Addressed

The amount and type(s) of actuarial reporting and/or disclosure to

require—and the best benefit-liability measure and reporting format—

should be determined only after considering the Information needs of

PERS financial statement users. NCGA Concepts Statement 1—based on a

research study of potential users of government financial statements and

the information necessary to support their decisions—identifies five

basic categories of relevant information:

1. Information concerning short-term financial resources.

2. Information concerning the financial condition of the

governmental unit.

3. Information concerning compliance with legal, contractual, and

fiduciary requirements.

4. Information useful for planning and budgeting.

5. Information concerning managerial and organizational

performance.

The GASB [1985b] enumerates similar uses of governmental financial

reports in its Statement of Governmental Accounting and Reporting

Objectives. In addition to this general discussion of the uses of

governmental financial reports, the GASB [1985a] specifically discusses

PERS reporting and states that:

the primary objectives of pension disclosures are to provide . . . information needed to assess (a) the funding status of a

13

PERS on a going-concern basis, (b) progress made in accumulating assets to pay benefits when due, and (c) whether employers are making actuarially determined contributions to plans, [par. 6]

However, no consensus has been reached regarding the PERS information

set that best meets these user needs.

Some would argue that these needs are best met when accounting and

reporting alternatives are severely limited. Implicit in such arguments

is the belief that users of pension reports benefit (i.e., are able to

make better decisions) if reported pension information is standardized

as to content, form, and underlying assumptions.

On the other hand, others take issue with pension reporting

requirements such as those specified by Public Law 95-595, believing

that "over-regulation" of this kind (1) is unduly expensive and (2)

precludes the selection of an accounting and reporting method that

mirrors the underlying economic aspects of the PERS. Implicitly, they

argue that—because the "market" is efficient—any one of several

pension accounting and reporting approaches should be permitted if the

selected approach is adequately described in the PERS financial

statements.

Those advocating "adequate disclosure" (in lieu of specifying

narrow standards) implicitly assume that users of pension information

are able to make better decisions once they are Informed of the under

lying actuarial assumptions and which of the several alternative

accounting and reporting approaches is being used. For this to be true,

users must have a sufficient grasp of actuarial methods and terminology

to be able to use the information provided in PERS financial statements.

This grasp of actuarial terminology and methods is particularly

14

important if users wish to compare various pension plans considering (1)

the wide variations in actuarial disclosures found in current reporting

practices [Engstrom, 1984], and (2) the differing benefit-liability

measures used by the NCGA and the FASB.

No empirical evidence has been found to indicate that users can, in

fact, identify the effects of actuarial assumptions on reported data. A

comment by Llvnat [1984]—based on a study of the information content of

reported pension liabilities—summarizes a common perception:

It was empirically found in many [business] studies that the earnings signal possesses information content and that it causes share price revisions. Yet, no comparable body of literature exists for pension disclosures. Furthermore, due to the numerous assumptions that are needed to derive pension liabilities, one may question whether the pension signal is sufficiently reliable, [p. 77]

In an effort to provide evidence regarding the ability of PERS

financial statement users to (1) Interpret reported pension information,

and (2) impound actuarial data, the following general research questions

are addressed:

1. Does the benefit-liability measure (i.e., PTL or PCL) and/or

the amount of supplemental disclosure affect users' perceptions of the

PERS' financial condition?

2. Do users of PERS financial statements understand the effects

that actuarial assumptions have on the reported benefit-liability

measure?

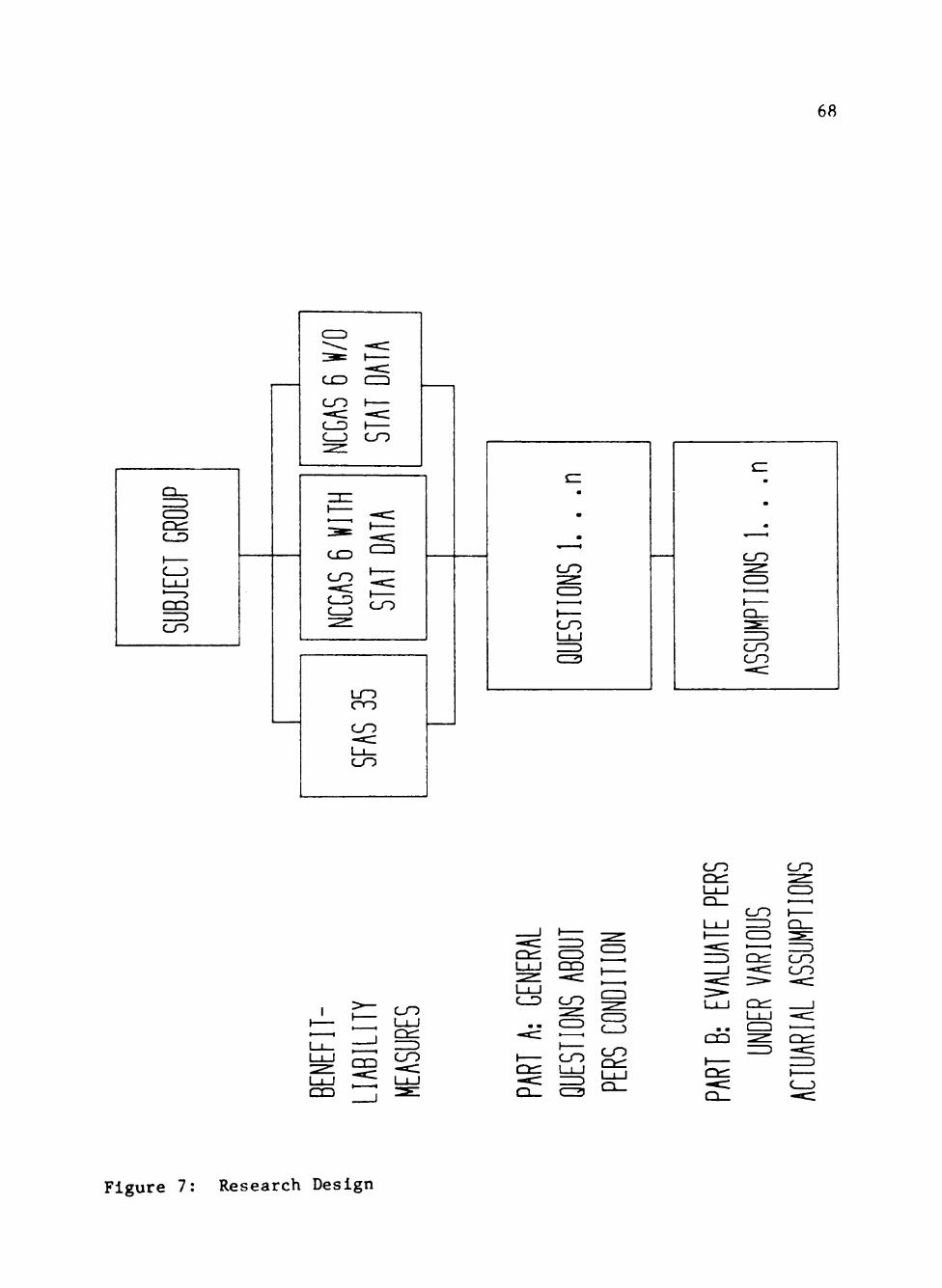

A field experiment was used to gather the necessary data. In the

experiment, each participant was given the financial statements of a

fictitious PERS and asked to (1) answer several questions about the

PERS, and (2) identify the financial statement Information that was

15

believed to be the basis for each response. The research design

utilized to answer the study's first question randomly divided the

sample into three groups and then provided each group with a different

version of the PERS' financial statements. Between group response

differences are considered indicative of an effect attributable to the

financial statement version, thus leading to the conclusion that

judgments about a PERS can be affected by the content of the PERS'

financial reports and the accounting methods used to generate the

reported data.

Each participant was also Instructed to complete two exercises

designed to measure (1) their knowledge of the effects of actuarial

methods and assumptions on reported data, and (2) their ability to

effectively consider these effects when making judgments regarding the

pension's financial condition.

Expected Contributions of the Study

This study should contribute to our understanding of the judgment

process employed by PERS financial statement users when analyzing

reported pension data. In turn, this knowledge should lead to financial

reports that are better able to meet the needs of those making decisions

about various PERS attributes.

The accounting profession cannot control an individual's knowledge

level or consistency, but it can affect the "quality" (i.e., Information

content) of PERS financial statements through the standard setting

process. This study provides empirical evidence about the ability of

pension information users to assimilate information about a PERS'

16

economic condition since current GAAP permits varying (1) benefit-

liability measures and/or disclosure levels, and (2) actuarial

assumptions and cost methods. In particular, the research findings

offer guidance to accounting standards setters by determining:

1. Whether the benefit-liability measure (among those in current

use) used by a PERS for financial reporting affects judgments regarding

its financial condition,

2. Whether the presence or absence in a PERS' financial report of

10-year statistical summaries affects users' (a) perceptions about the

PERS or (b) judgment consensus, and

3. Whether there is any basis for prescribing the actuarial

assumptions to use for PERS financial reporting.

Previous human information processing research in accounting has

been limited to the private sector and has principally relied, for

subjects, on (1) surrogates for financial statement users (usually

deemed to be investors), and (2) auditors. This study extends human

Information processing research techniques to the public sector via

research into the decision making of actual PERS financial statement

users and preparers.

Organization of the Study

The first part of the study briefly examines the authoritative

pronouncements that are relevant to PERS accounting and financial

reporting. Next, a review of the academic and professional studies

pertaining to this study is presented. Using these studies as bases,

the theoretical model that supports current PERS accounting and

17

financial reporting is described and conceptual and empirical support

for an alternative approach is given. The research methodology as well

as the operational hypotheses and variables is then developed. Finally,

the results are presented including the implications and limitations of

the study.

CHAPTER 2

LITERATURE ON PENSION PLAN REPORTING

Literature relevant to this study can be divided into two general

areas: (1) authoritative statements on the topic of pension accounting

and financial reporting, and (2) academic and professional studies. The

authoritative literature review traces the recent evolution of pro

nouncements on public employee retirement system (PERS) accounting and

financial reporting. It is followed by a review of several studies of

users' reactions to pension information.

Authoritative Statements

Little mention of pension accounting and financial reporting

appears in the early authoritative literature. Municipal Accounting and

Auditing [1951] briefly mentions pension accounting in the section

dealing with trust and agency funds, but the discussion is limited to a

comment that:

Pension funds should be set up on an actuarial basis and the reserve should equal the actuarial requirements of the fund at the date of the balance sheet. If the assets in the fund exceed the actuarial requirements the difference represents a surplus; if the actuarial requirements are greater than the assets in the fund, the difference represents a deficit. Surpluses and deficits should be reflected in the accounts and on the balance sheet, [p. 101]

GAAFR68

Governmental Accounting, Auditing, and Financial Reporting

(GAAFR68) [1968], issued by the National Committee on Governmental

Accounting, contains the first substantive discussion of PERS accounting

18

19

and financial reporting in the authoritative literature. GAAFR68 was

recognized as authoritative by the American Institute of Certified

Public Accountants (AICPA) in Audits of State and Local Governmental

Units (ASLGU) [1974] and gained widespread acceptance as the primary

authoritative statement on the application of generally accepted

accounting principles (GAAP) to state and local governments. Until

superseded, GAAFR68 provided the only authoritative guidance on

accounting and reporting for pension plans (as opposed to employer

pension costs) in either the private or public sectors.

Public employee retirement funds are a form of expendable trust

fund, i.e., the funds' principal and Income may be expended in the

course of its designated operations. A pension fund operates by

receiving money from general revenues, contributions, and Interest on

Investments and expending these monies on participant benefits, fund

operations (in some cases, expenditures for PERS operations are made

from the general fund), and refunds to terminated employees.

GAAFR68 required several financial statements for each PERS

(balance sheet, statement of cash receipts and disbursements, statement

of changes in fund balances, and analysis of changes in retirement

reserves). These statements were to be prepared on the "accrual"

(modified accrual) basis with revenues recognized when earned and expen

ditures recognized when current liabilities were incurred. The trust

fund nature of PERS resulted in (1) the absence of an income statement

from the required financial statements, and (2) the emphasis on cash

receipts and disbursements.

20

GAAFR68 recognized the Importance of actuarial valuations and

states:

The National Committee on Governmental Accounting recommends that appropriate reserve accounts be set up on the books [and reported on the balance sheet] to reflect not only compliance with applicable legal requirements and actual amounts set aside pursuant to such requirements for pajment of employee benefits but also the amount of assets which, on the basis of competent actuarial evaluation, should be in the fund if sufficient money is to be available to pay retirement annuities and other benefits to employees when they retire or otherwise become eligible, [p. 77]

Under this recommended approach, periodic adjustment of the accounts to

reflect actuarial requirements results in a credit balance in the Fund

Balance account when the retirement system is "fully funded" and a

deficit when an actuarial deficiency exists. A deficit must be financed

at some future date or retirement commitments cannot be met in full on

schedule.

The existence—and magnitude—of a pension plan's actuarial

deficiency, however, depends upon the various assumptions made by its

actuary. Unfortunately, GAAFR68 provided no guidance regarding

acceptable actuarial techniques (for financial reporting purposes). In

addition, it did not require disclosure of (1) the actuarial cost method

used for financial reporting (or funding) purposes, or (2) the actuarial

assumptions used in the valuation. Thus, financial statement users were

without the information needed to judge the reasonableness of the PERS'

apparent funding status.

NCGAS 1

National Council on Governmental Accounting Statement 1 (NCGAS 1),

"Governmental Accounting and Financial Reporting Principles," was issued

21

to "update, clarify, amplify, and reorder GAAFR" [NCGAS 1, 1979, p. 1].

However, the guidance on PERS accounting and financial reporting found

in NCGAS 1 is limited to (1) a statement that ". . . Pension Trust Funds

are accounted for in essentially the same manner as proprietary funds

[p» 6]," (2) a footnote mentioning "pension plan accounting and report

ing . . . is under study by the FASB [Financial Accounting Standards

Board], the AICPA State and Local Government Accounting Committee, and

the NCGA [p. 27]," and (3) the inclusion of a Pension Trust Fund in the

illustrative financial statements provided in Appendix A to the

statement. Although Appendix A was nonauthoritative, the fact that (1)

it illustrated the GAAFR68 approach to PERS financial reporting, and (2)

"GAAFR restatement" was the objective of NCGAS 1 led many governments to

continue to use the trust fund method of PERS financial reporting.

SFAS 35

In 1980, the FASB completed its study of accounting and reporting

by defined benefit pension plans and Issued Statement of Financial

Accounting Standards No. 35 (SFAS 35), "Accounting and Reporting by

Defined Benefit Pension Plans" [March, 1980]. Its release caused con

troversy in the public sector because—believing all pension plans are

similar and should report similarly—the FASB declared SFAS 35 to be

applicable to state and local government PERS. (Indeed, it is the first

measurement standard issued by the FASB or its predecessors made speci

fically applicable to state and local governmental units.) Public

sector pension accounting leaders generally disagree with several of its

provisions—primarily the provision requiring the reporting of an

22

accumulated plan benefit Instead of a projected plan benefit [e.g.,

Flndley, 1981; and NCGA 6].

NCGAI 4

NCGA Interpretation No. 4 (NCGAI 4), "Accounting and Financial

Reporting for Public Employee Retirement Systems and Pension Trust

Funds" [December, 1981], was Intended to "provide interim authoritative

guidance to the proper application of [NCGA] Statement 1 requirements to

PERS and to supplement Statement 1 guidance for pension trust funds"

[p. 1]. It differed from SFAS 35 primarily by requiring footnote

disclosure of "anticipated Increases in accumulated benefits based on

projected salary Increases from the current period to retirement" [p.

1—emphasis added]. Because of this difference, the effective dates for

state and local governments of SFAS 35 and NCGAI 4 were deferred to

fiscal years ending after June 15, 1983 by Statement of Financial

Accounting Standards No. 59, "Deferral of the Effective Date of Certain

Accounting Requirements for Pension Plans of State and Local Govern

mental Units," [April, 1982] and by NCGA resolution so that the two

standard setting bodies might have time to resolve their differences.

NCGA 6

The NCGA's pension project culminated with the issuance of

Statement 6 (NCGAS 6), "Pension Accounting and Financial Reporting:

Public Employee Retirement Systems and State and Local Government

Employers," [June, 1983]. As did NCGAI 4 (which it supersedes), NCGAS 6

intended to provide guidance not found in NCGAS 1 on pension accounting

and financial reporting.

23

NCGAS 6, like NCGAI 4, required that PERS report the effects of

projected salary Increases on plan benefit obligations. However,

NCGAS 6 changed the format of this reporting from a footnote to

disclosure of the actuarial present value of credited plan benefits^ in

the fund balance section of PERS financial statements. NCGAS 6 also

expanded the information required to be disclosed in the notes to PERS

financial statements. This prescribed disclosure includes (1) a

description of the plan, (2) a description of the actuarial cost method

and assumptions, (3) funding requirement determinations and actual con

tributions, (4) a summary of significant accounting and financial

reporting policies, (5) an explanation of actuarial values and changes,

and (6) Information regarding the PERS' investments. Further, 10-year

historical trend information must be presented to disclose progress in

accumulating assets to pay benefits when due. Appendix A more fully

details the reporting requirements of NCGAS 6 and compares them to those

of SFAS 35.

The significant differences between the respective FASB and NCGA

statements have yet to be resolved. These differences primarily regard

(1) the appropriate benefit-liability measure to use for PERS reporting,

(2) the amount of note disclosure to require, and (3) the accounting

treatment of pension obligations by governmental employers. Accord

ingly, the application dates to state and local government PERS of both

statements have been deferred indefinitely [SFAS 75, 1983; NCGAI 8,

1983].

These are the actuarial values determined under the unit credit actuarial cost method with benefits based on projected salary Increases [NCGAS 6, par. 22].

24

GASBS 1

Statement No. 1 of the Governmental Accounting Standards Board,

"Authoritative Status of NCGA Pronouncements and AICPA Industry Audit

Guide," [July, 1984] (GASBS 1) leaves present GAAP in effect until

". . . altered, amended, supplemented, revoked, or superseded by

subsequent GASB pronouncements [par. 8]." The GASB also states:

Pending issuance by the GASB of a Statement or Statements concerning pension accounting and financial reporting, the following pronouncements are considered by the GASB as sources of acceptable accounting and reporting principles for public employee retirement systems (PERS) and state and local government employers . . . : (a) [NCGAS 1] (b) [NCGAS 6] (c) [SFAS 35] [GASBS 1, par. 9].

Thus, PERS financial statements may be prepared in accordance with

either NCGAS 1, SFAS 35, or NCGAS 6. Note the lack of a definitive

article in the phrase "as sources of," thus implying that pension

accounting and financial reporting may be done in other ways as well.

This situation is likely to continue until at least early 1986—when

Section 5.1 of the GASB's pension project is tentatively scheduled for

completion.

GASB Pension Project Section 5.1: Pension Disclosures

This subproject deals with pension disclosure requirements. On

August 20, 1985, the GASB released an exposure draft, "Disclosure of

Defined Benefit Pension Information for Public Employee Retirement

Systems and State and Local Governmental Employers." This exposure

draft agrees with the NCGA's conclusions—expressed in NCGAS 6—

regarding the primary objectives of PERS financial reports. The expo

sure draft also reaffirms the NCGA's conclusions that these objectives

25

cannot be accomplished with current year financial statements alone.

Accordingly, 10-year dollar and ratio analysis historical trend data are

required to be presented. In addition the proposed Statement:

. . . requires standardized computation and disclosure of a measure of the accrued pension benefit obligation that may differ from that produced by the actuarial funding method used by the PERS to determine employer contribution requirements. The prescribed standardized obligation measure . . . considers both salary progressions and steprate benefits. Disclosures about significant actuarial assumptions and the sensitivity of the standardized obligation measure to changes in interest rate and salary projection assumptions are also required. [GASB Exposure Draft, 1985, summary]

GASB Pension Project Section 5.2: Pension Accounting and Reporting

This subproject covers accounting and reporting issues (other than

disclosure requirements) for PERS and governmental entitles from both

the pension plan and the employer perspectives. Among other things, it

is addressing the areas of difference between NCGAS 6 and SFAS 35, such

as the valuation of marketable securities and the valuation of the

pension benefit obligation. It also is dealing with such Issues as the

display of the pension benefit obligation on the employer balance sheet.

SFAS 87

In December 1985, the FASB issued Statement of Financial Accounting

Standards No. 87 (SFAS 87), "Employers' Accounting for Pensions." This

document represents a major milestone in the decade old FASB pension

project and provides financial statement users with improved information

about enterprises' pension costs and liabilities. This improved infor

mation takes the form of (1) enhanced footnote disclosure of pension

data and (2) the balance sheet recognition of at least a portion of

26

organizations' unfunded pension liabilities. Although SFAS 87 does not

require that 10-year historical trend data be reported, its disclosure

requirements are in many respects similar to those of the GASB's

exposure draft. However, there are two major differences between the

documents: (1) SFAS 87 addresses employer accounting Issues as well as

disclosure matters, and (2) SFAS 87 concerns employer—not PERS—

accounting. SFAS 35 would not be affected by its issuance.

Standard Setting in Perspective

Although the economic significance of pensions has steadily evolved

over the past half-century, pension accounting and reporting practices

remained relatively unchanged until recently. The past decade has

witnessed a considerable debate over PERS accounting and reporting

matters and the Issuance of more than several conflicting pronouncements

on the topic. Both the GASB and the FASB are working toward resolving

these conflicts and providing users of PERS financial reports with

Information that fulfills their needs. However, additional research is

needed in order to identify (1) these needs and (2) the information set

that best meets them. This study provides standards setters with

evidence regarding the ability of PERS financial statement users to

analyze the statements when underlying actuarial assumptions are not

prescribed.

Previous Pension Research

The pension accounting controversy has been accompanied by numerous

articles on the topic. Generally, these articles state the author's

position on the issue and present arguments and anecdotal evidence to

27

support that position. Although interesting reading (and relevant when

considering the politics of standard setting), they present little

empirical evidence that might assist standard setters to objectively

determine an appropriate approach to pension accounting. Several

studies were found, however, that are relevant to pension accounting and

financial reporting. Primarily, this research (1) concerns users'

reactions to reported pension information, or (2) identifies the infor

mation that users claim is necessary to support their decisions.

The Market's Reaction to Pension Disclosures

Llvnat

Research question. Llvnat [1984] addressed the question of whether

unfunded vested benefits and unfunded past service costs possess any

information content. He states that "... a signal is said to possess

information content when it changes the market transactors' beliefs

about the distribution of future returns" [p. 78].

Methodology. Llvnat used a research design similar to that

employed by Gonedes [1978], who tested the information content of earn

ings, extraordinary items, and dividend yields. Llvnat tested whether

the means of the returns were revised (i.e., does the signal have infor

mation content) by grouping the sample into portfolios according to

their realizations of the signals (unfunded vested benefits, unfunded

past service costs, and the earnings signal when supplemented by pension

plan signals) and constructing control portfolios with equivalent

degrees of risk. If market participants have not revised their assess

ment of mean returns upon receipt of the signal, the sample portfolios

28

should have the same expected return as the control portfolio since they

have the same degree of risk.

Findings/conclusions. Llvnat summarizes the results of his tests

as follows:

1. The joint earnings and unfunded vested benefits signal

possesses Information content.

2. The joint earnings and unfunded past service costs signal

possesses less information content than the joint earnings and unfunded

vested benefits signal.

3. The joint unfunded vested benefits and unfunded past service

costs signal does not possess information content.

4. Although the earnings signal possesses information content,

the unfunded vested benefits and the unfunded past service costs signals

make the earnings signal more informative, [p. 86]

Relevance to current study. Although Livnat's study was concerned

with employer pension reporting, his findings are relevant to this

study. Llvnat found that the amount reported as unfunded prior service

costs served as an information signal (albeit a weak signal) in the

presence of the earnings signal. Yet, this amount appears to possess

little real information content. The FASB commented that, "the amount

of past service costs can vary considerably or be non-existent depending

on the actuarial cost method selected without any differences in other

facts or circumstances" [SFAS 36, par. 2, emphasis added]. Accordingly,

users must know what actuarial cost method was used if reported unfunded

prior service costs (which may be zero) are to be meaningful. At the

time of Livnat's study, no disclosure was required of the actuarial cost

29

method used. Thus, doubt is cast on the ability of financial statement

users to Interpret the pension signal.

Unfunded vested benefits is reported by Llvnat to be a better

signal than unfunded prior service costs; however, the amount reported

as unfunded vested benefits depends upon which of a variety of actuarial

assumptions are used. Of these assumptions, the interest rate assump

tion is most critical. Webster [1984] notes that seemingly minor (i.e.,

1%) changes in the rate of return assumption result in large differences

in the reported unfunded actuarial accrued liability (of which unfunded

vested benefits is a major component). Further, studies indicate that a

wide range of interest rates are used in practice [Nichols and Morris,

1982; Tierney and Calder, 1985]. Although published in 1984, Livnat's

study covered the pre-1979 period—prior to any promulgation requiring

disclosure of actuarial interest rates. Accordingly, financial state

ment users appear to be basing decisions on a pension signal that could

be considered unreliable in the absence of disclosed actuarial

assumptions.

Daley

Research question. Daley [1984] studied the relationship between

several accounting measures of the cost of defined benefit pension plans

for sponsoring firms and the market value of their equity securities.

The measures considered were (1) unfunded vested benefits, (2) unfunded

prior service costs, (3) pension expense (which serves as an annualized

estimate of future cash flows associated with the pension benefit obli

gation), and (4) the actuarial assumption about Interest rates. He

attempted to determine whether, and to what extent, any of these

30

measures of pension cost are consistent with the value of the pension

cash flow Impounded within equity security prices.

Methodology. Daley used a cross-sectional equity valuation model

to analyze earnings before extraordinary items and total assets (from

the Compustat Annual Industrial File 1961-79) and monthly stock returns

and share prices (on the CRSP return file 1971-79). Actuarial interest

rate data came from Department of Labor filings, FASB's SFAS 36 data

tape. Form lOKs, and annual reports. The sample consisted of the 153

firms for which complete data were available for the years noted. Of

these firms, actuarial interest rate data were available for only 128;

thus, interest rate tests were performed on this subsample.

Findings/conclusions. Daley found that (1) the pension expense is

the "most consistent" measure of the equity market's aggregate pension

cost measure, and (2) cross-sectional differences in actuarially

selected discount rates are not used by the equity markets in evaluating

data on pension costs.

Relevance to current study. The reported pension expense—which

(1) Daley reports as being the "most consistent" measure of aggregate

pension costs, and (2) is a component of reported earnings—depends in

any given year on the actuarial cost method used. Schlpper and Well

[1982] note that:

A nonrandom sample of actuaries have Indicated that actuarial cost methods are chosen to suit the employer's wishes in some regards. One actuary offered a choice of patterns—one with smooth, relatively equal patterns of funding payments independent of earnings and another with smaller payments in years when the income was low and with larger payments in years when Income was high. [p. 816]

31

These observations are significant because financial statement

users (1) appear to be using pension data in an Inconsistent manner

(i.e., reported pension expense may not be a very consistent measure of

aggregate pension cost), and (2) seem to be making decisions about

economic phenomena based on reported pension data when, due to varia

tions in assumptions and actuarial cost methods, the reported data can

vary significantly without any differences in other facts or

circumstances, or vice versa. Again, doubt is cast on the ability of

financial statement users to properly Interpret the pension signal.

PERS Research

Van Daniker and Aldrldge

Research question. Van Daniker and Aldrldge (V&A) [1985] conducted

a study—authorized by the NCGA—to provide empirical data that can be

used in the development of financial reporting requirements for PERS.

V&A assert that a major reason for the controversy over PERS financial

reporting requirements is the difference of opinion as to the users of

PERS financial information and the needs of those users for information.

Accordingly, they attempted to ". . . first, identify some of the users

of PERS financial information; and second, determine the informational

needs of those Identified as users" [p. 14].

Methodology. Data were gathered via a questionnaire that was sent

to plan participants, plan administrators, and legislative/oversight

officials. Reliability tests were performed to determine the accuracy

of the questionnaire used in the study. A mean response and standard

deviation were determined for each question, by individual group and in

32

the aggregate, and were used to test for significant differences between

the groups' responses to each question.

Findings/conclusions. V&A determined that (1) plan participants,

(2) PERS administrators, and (3) legislative/oversight officials are

users of PERS financial Information. (Since PERS data are included in

the comprehensive annual financial report (CAFR) of the sponsoring

governmental employer, users of the CAFR can also be considered to be

users of PERS Information.)

The study found that not all user groups profess the same informa

tional needs. Plan participants are primarily Interested in assessing

the amount of future benefits and the risk associated with future bene

fits. PERS administrators and legislative/oversight officials—while

interested in the amount of future benefits—appear more interested in

information useful for assessing (1) the performance of plan administra

tors and (2) the need for future contributions. All three user groups

indicated a preference for plan reporting based on the same actuarial

method as used for plan funding. The user groups also requested disclo

sure of the actuarial assumptions used in the benefit determination and

disclosure of the actuarial cost method used to determine plan funding.

Relevance to current study. The V&A study makes a valuable contri

bution to this research. The study empirically identifies some of the

users of PERS financial statements and lists the financial information

items that these users state they need to make decisions about the PERS.

The current study draws its sample from among the user groups

identified by V&A, and their findings are the basis for this study's

questionnaire. However, the V&A study leads to the need for, and rele-

33

vance of, the current study. As noted by Abdel-khalik and Keller

[1979]:

The Inability to transfer conceptual knowledge about accounting changes to understanding as to the economic Impact on a firm Implies that questionnaires requesting users to specify information needs for decision making are not likely to be very productive, [p. 52]

This comment is reinforced by several studies of Individuals' judgments

which concluded that individuals typically overestimate (1) the amount

of information, and (2) the relative importance of information items

that actually serve as the basis for a decision [e.g., Ashton, 1974b;

Hofstedt and Hughes, 1977; Joyce, 1976]. Accordingly, it may be inap

propriate to rely on "self-reported" research findings such as those of

Van Daniker and Aldrldge. The current study seeks to determine whether

users of PERS financial information can assimilate the information they

requested when making decisions about a PERS' economic condition.

Engstrom

Research question. Engstrom [1984] studied the pension disclosure

practices of municipalities located in the United States in order to

". . . determine the extent of compliance with authoritative pronounce

ments for both employer and pension funds" [p. 198].

Methodology. Engstrom requested a Comprehensive Annual Financial

Report from each of the 180 cities that had Municipal Finance Officers

Association Certificates of Conformance as of September 1, 1980. The

116 reports that Engstrom received were analyzed and the following data

presented in tabular form: (1) various employee groups covered, (2)

types of pension plans reported, (3) reported unfunded pension liability

per capita, (4) reported unfunded pension liability/general fund assets,

34

(5) reported pension cost per capita, (6) disclosures of accounting and

funding status, and (7) method of reflecting the unfunded liability.

Findings/conclusions. Engstrom found that the cities he studied

made widely varying pension disclosures. For example, some reported

total unfunded liabilities, others reported vested liabilities, and

still others did not disclose whether or not a liability existed. His

frustration about the state of employer pension reporting is summed up

by his statement that, "a further limitation [of the study] is the

inability to extract Information from reports with such widely varying

pension disclosures" [p. 210].

Relevance to current study. Employer pension reporting is

generally reflective of PERS reporting since the latter serves as the

basis for the former. Accordingly, Engstrom's finding of considerable

variation in employer reporting indicates that considerable variation in

PERS reporting is likely. This variation poses a threat to financial

statement users wishing to make between PERS comparisons if, as Engstrom

notes, "financial analysts and others would have difficulty extracting

comparable pension information from the financial reports of U.S.

cities" [p. 210].

Summary

This chapter first discussed the evolution of authoritative state

ments on the topic of pension accounting and financial reporting. The

controversial nature of the subject is evident in (1) the pension

pronouncements Issued by the NCGA and the FASB (and their predecessor

35

organizations), and (2) the two pension projects placed on the GASB's

initial agenda.

Not only are pension accounting and reporting practices in ques

tion, but studies by Llvnat [1984] and Daley [1984] raise doubts about

the ability of PERS financial statement users to adequately evaluate the

pension data that are currently reported. The following chapter (1)

discusses the theoretical support for current pension accounting prac

tices, and (2) presents the results of research that—in conflict with

current practice—supports the findings of both Llvnat and Daley.

CHAPTER 3

FULL DISCLOSURE VS. FUNCTIONAL FIXATION

The theory that supports public employee retirement system (PERS)

financial reporting practices has yet to be clearly identified. State

ment of Financial Accounting Concepts No. 4 (SFAC 4), "Objectives of

Financial Reporting by Nonbusiness Organizations," established the

objectives of general purpose external financial reporting by

nonbusiness organizations. The Financial Accounting Standards Board

(FASB) stated that these objectives

together with the objectives set forth in FASB Concepts Statement No. 1, "Objectives of Financial Reporting by Business Enterprises," will serve as the foundation of the conceptual framework the [FASB] is developing for financial accounting and reporting. Based on its review of the similarities and differences between those two sets of objectives, the [FASB] has concluded that it is not necessary to develop an Independent conceptual framework for any particular category of entitles. [SFAC 4, 1980, par. 1]

Thus, PERS and other organizations share the same generalized conceptual

framework for accounting and financial reporting and have developed

similar reporting standards. However, some question exists as to

whether the pension Information produced in accordance with these

standards adequately meets the financial reporting objectives set forth

in the conceptual framework.

Llvnat [1984] and Daley [1984] found evidence which indicates that

the users of general purpose financial statements have difficulty inter

preting reported pension data. Their findings suggest either (1) that

the generalized conceptual framework developed for nonbusiness account

ing and financial reporting is Inappropriate for PERS use, or (2) that

36

37

PERS are unique entities that depend upon complex funding and actuarial

constructs; consequently, accounting and reporting practices developed

primarily for other categories of entities are not appropriate for PERS'

utilization. The latter alternative postulates—as does this study—

that the same conceptual framework is suitable for both PERS and other

nonbusiness entities. Thus, any financial reporting Inadequacies are

due to inappropriate reporting standards rather than to the objectives

of financial reporting.

This chapter discusses two hypotheses that have been widely tested

in the context of business financial reporting. First, the efficient

market hypothesis is discussed since it appears that current PERS

accounting and reporting standards are predicated on its implications.

Next, the phenomenon of functional fixation is considered since it seems

to offer a plausible explanation for the findings of both Llvnat and

Daley. The discourse considers the capacity of each hypothesis to

serve as a theory regarding how financial statement users process PERS

information. Knowledge of how this information is processed will assist

accounting standards setters to achieve the reporting objectives set

forth in the conceptual framework.

Support for "Full Disclosure"

The efficient market hypothesis [EMH] has important implications

for accounting practice [Deitrlck and Harrison, 1984]. As Ketz and

Wyatt [1983] note, "since the evidence for stock market efficiency seems

abundant, some accountants have argued that controversial topics should

be adjudicated in terms of efficient market theory" [p. 29]. The term

38

"efficient" refers to the way that security prices reflect information—

in an efficient market, security prices react as if they fully and

rapidly incorporate all existing information in an unbiased fashion.

Three forms of the EMH have been delineated:

1. The "weak form" of market efficiency implies that a security's

price at a particular time impounds the information contained in its

sequence of past prices.

2. The "semistrong form" holds that a security price fully

reflects all publicly available information.

3. The "strong form" asserts that all Information—including

information that is not publicly available, i.e., inside information—is

reflected in a security's price.

The EMH presumes that, in the aggregate, users of accounting

information (the securities markets) are (1) rational, and (2) able to

properly interpret accounting signals (and other information), thus

allocating resources to those entities providing the best rate of return

for a given level of risk. In other words, accounting information

serves as evidence regarding underlying economic phenomena.

Beaver [1973] states that EMH research has "several important

implications for accounting in general and for the FASB in particular"

[p. 52]. Although directed at the private sector, his "four major

Implications" of the EMH for the accounting profession are also appli

cable to the public sector. Accordingly, as summarized below, they have

been adapted. They are:

1. Many reporting issues are capable of a simple disclosure

solution and do not warrant an expenditure of standards setters time and

39

resources in attempting to resolve them.

2. The role of accounting data is to prevent superior returns

accruing from inside information and can be achieved by a policy of much

fuller disclosure than is currently required.

3. Financial statements should not be reduced to the level of

understanding of the naive Investor.

4. Standards setters should strive for policies that will

eliminate excessive costs of information.

Here, these implications are relevant in the context of pension

accounting. The objective of the following discussion is to demonstrate

that PERS reporting—as permitted by GASB Statement 1 (GASBS 1) and

proposed in the August 20, 1985 exposure draft, "Disclosure of Defined

Benefit Pension Information for Public Employee Retirement Systems and

State and Local Governmental Employers,"—is based on the presumed

validity of the EMH and its applicability to PERS accounting and finan

cial reporting.

Implications of the EMH for PERS Accounting

Accounting Alternatives

Beaver's first point is based on the assertion that many reporting

issues Involve alternatives, any of which can be adopted with essen

tially no difference in cost to the government. Further, these issues

are characterized as requiring essentially no cost to statement users in

adjusting from one method to another. In such cases, Beaver suggests a

"simple solution: report one method, with sufficient footnote disclo

sure to permit adjustment to the other" [p. 52]. This appears to be the

approach taken by the GASB. Although GASBS 1 does not require

40

disclosure of which pronouncement served as the basis for a PERS'

financial statements, differences in statement format, measurement

basis, and disclosure levels make apparent which standard was applied.

Further, it seems reasonable to presume that the enhanced disclosures

called for in the GASB's exposure draft are supposed to facilitate

comparisons of plans when different assumptions are used (since—under

the exposure draft—the actuarial cost method used for reporting has

been prescribed).

Disclosure Levels

The second implication of the EMH for accounting standards setters

applies when the "semi-strong form" of the EMH is valid—as is widely

held to be the case [Dyckman, Downes, and Magee, 1975]. As Beaver

notes, "merely because prices reflect publicly available information in

no way implies that they also fully reflect inside information" [p. 53].

Inside information has been perceived as a problem for persons inter

ested in the "real" cost of PERS. The conventional wisdom maintains

that an underfunded PERS results in intergenerational wealth transfers,

reduced savings, and future fiscal stress for the sponsoring government.

This view implies that taxpayers and employees are not fully aware of

deferred labor costs [Copeland and Wilson, 1985]. Some place part of

the blame for this "unawareness" on pension accounting practices [Mautz,

1981].

A government's annual pension contribution is normally determined

on the basis of a fixed percentage of total payroll or a fixed

percentage of projected benefits plus an amount sufficient to amortize

any unfunded pension liability [Wlnklevoss and McGlll, 1979]. But as

41

Copeland and Wilson observe, "especially for locally administered plans,

valuation of plan benefits, amortization period for the unfunded

liability, and timing of contributions may be subject to considerable

manipulation" [p. 5].

Beaver recommends that much fuller disclosure be required when

inside information is being used to secure "abnormal returns" for

Insiders (in this case, those responsible for establishing PERS bene

fits, funding policies, and accounting policies). The GASB's response

to this perceived problem has been to propose disclosure levels that are

greatly in excess of those currently found in typical PERS reports

[Engstrom, 1984].

Users' Knowledge Level

The EMH's third Implication for accounting standards setters

relates to the "traditional concern for the naive investor." Beaver

states, "we must stop acting as if all—or even most—individual inves

tors are literally involved in the process of interpreting the impact of

accounting information upon the security prices of firms" [p. 53]. In

the case of pension reporting, the role of the "naive investor" is

assumed by employees—and Indirectly, taxpayers. Unlike the naive

investor in securities, these two groups do not have the opportunity to

diversify. Thus, their eventual welfare is negotiated by plan

administrators and elected officials.

The GASB appears to have concurred with Beaver's conclusion. Para

graph 6 of the exposure draft states:

After considering the needs of users and related reporting objectives, the GASB has concluded that the primary objectives of pension disclosures are to provide persons

42

familiar with financial matters with information needed to assess (a) the funding status of a PERS on a going-concern basis, (b) progress made in accumulating assets to pay benefits when due, and (c) whether employers are making actuarially determined contributions to plans [emphasis added].

The meaning of the phrase "persons familiar with financial matters" is

not clear but does appear to rule out the "typical" PERS participant.

The level of required actuarial disclosure lends credence to this inter

pretation.

Information Costs

The final implication of the EMH pertains to the cost of infor

mation. There is considerable evidence that the EMH adequately

describes the workings of equity securities markets. These markets

react to all publicly available information, of which accounting data

are but a small portion. Given this plethora of data, it is unneces

sarily costly for organizations to act as if their financial reports

constitute the only source of Information about the organization.

Pension financial reports, on the other hand, may constitute the major

source of information about the PERS and its financial condition. If

so, the GASB's position of requiring more, rather than less information

to be disclosed is quite reasonable. In the case of pension reporting,

"underdisclosure" will lead to excessive Information costs since (1)

those Interested in a PERS are forced to obtain their own information—

which is not obtained without cost, or (2) the allocation of resources

in the economy will be suboptlmal.

The preceding discussion has focused on the parallels between

Beaver's EMH implications and the GASB's approach to PERS reporting.

43

However, evidence provided by Llvnat [1984] and Daley [1984]—which

raises questions about the ability of financial statement users to

properly Interpret the pension signal—fosters doubts about the

appropriateness of this theory for pension disclosures.

Does the EMH Apply to PERS?

The efficient market literature maintains that among alternative

methods of accounting or reporting, any are satisfactory to the market

so long as complete disclosure is made of the method used. To be

logically valid for pension reporting, a critical assertion must be

supported: the pension benefit "market" should be efficient; however,

certain market characteristics evoke questions concerning the ability of

this market to be efficient.

Unlike equity markets, the pension benefit market handles few

transactions involving "trades" of benefits. For example, suppose that

employees are given the option of PERS membership or having a contri

bution—equal in amount to the cost of their PERS membership—made to

their Individual retirement accounts. The pension market thus estab

lished permits an analysis of the perceived condition, management, etc.

of the PERS by examining the percentage of employees who opt for PERS

membership. Unfortunately, employees are seldom permitted to change

their plan memberships, and plan membership is usually mandatory thus

precluding any market evaluation of each PERS' perceived condition.

Relatively little information about a PERS may be publicly avail

able. In addition to the annual report. Investors in equity markets

typically have access to a variety of Information that is relevant to

44

their decisions, whereas the annual report is often the only PERS data

available to plan members and other Interested parties.

Adding to the difference between the equity and pension markets,

the latter is characterized by a lack of liquidity. PERS members cannot