mba urban farming sample business plan

DESCRIPTION

This report is prepared for the Social Purpose Business course at Schulich School of Business as a practice to apply the social entrepreneurship business model planning methods.TRANSCRIPT

NMLP6350 Team Project – Part 2 Business model valuation: “Aquaponic Hotspot Business Model”

Tuesday, March 20, 2012

By Group D: Miriam Aguilar (211991031)

Satyameet Ahuja (211334778) Suzanne Pragg (203062932) Hiroyasu Sudo (211145257) Peter Wambera (210611788)

2

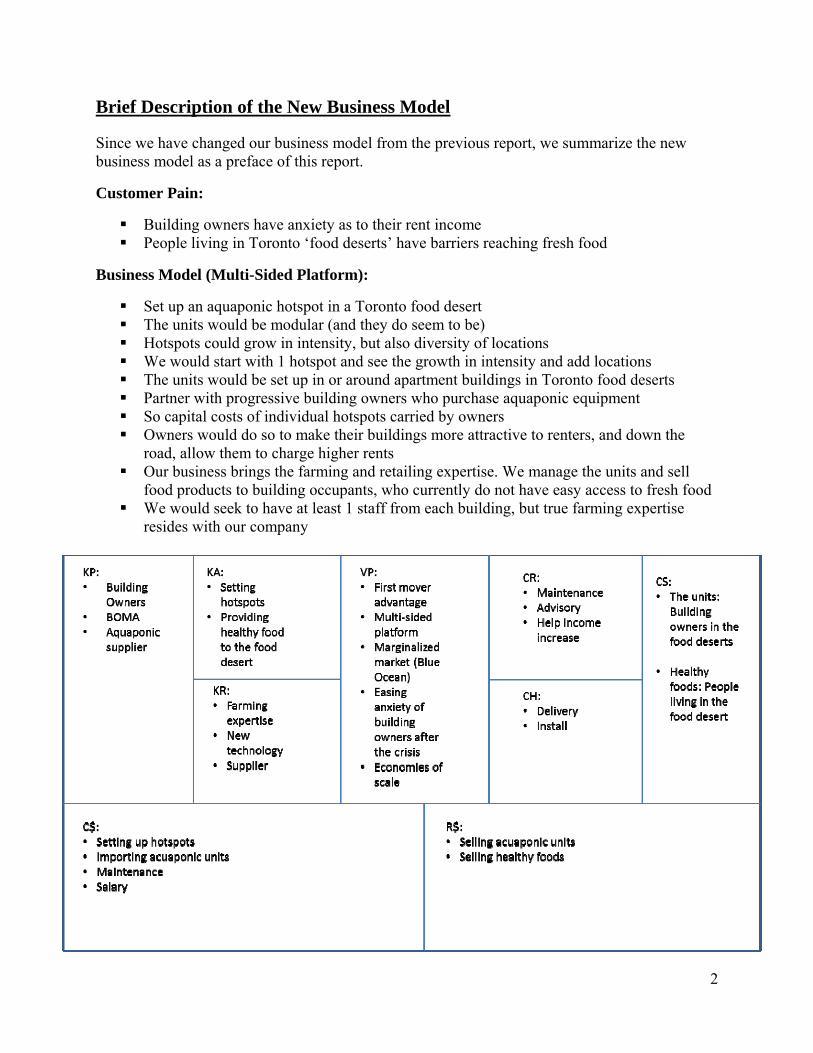

Brief Description of the New Business Model

Since we have changed our business model from the previous report, we summarize the new business model as a preface of this report.

Customer Pain:

Building owners have anxiety as to their rent income People living in Toronto ‘food deserts’ have barriers reaching fresh food

Business Model (Multi-Sided Platform):

Set up an aquaponic hotspot in a Toronto food desert The units would be modular (and they do seem to be) Hotspots could grow in intensity, but also diversity of locations We would start with 1 hotspot and see the growth in intensity and add locations The units would be set up in or around apartment buildings in Toronto food deserts Partner with progressive building owners who purchase aquaponic equipment So capital costs of individual hotspots carried by owners Owners would do so to make their buildings more attractive to renters, and down the

road, allow them to charge higher rents Our business brings the farming and retailing expertise. We manage the units and sell

food products to building occupants, who currently do not have easy access to fresh food We would seek to have at least 1 staff from each building, but true farming expertise

resides with our company

3

Contents Target Customer Analysis............................................................................................................... 4

Market Analysis .............................................................................................................................. 5

The Competition ............................................................................................................................. 6

Risk ................................................................................................................................................. 7

Market Strategies ............................................................................................................................ 8

Organizational Infrastructure .......................................................................................................... 9

Legal Considerations ...................................................................................................................... 9

Financials ...................................................................................................................................... 10

Exit Strategy: ................................................................................................................................ 11

Bibliography ................................................................................................................................. 12

4

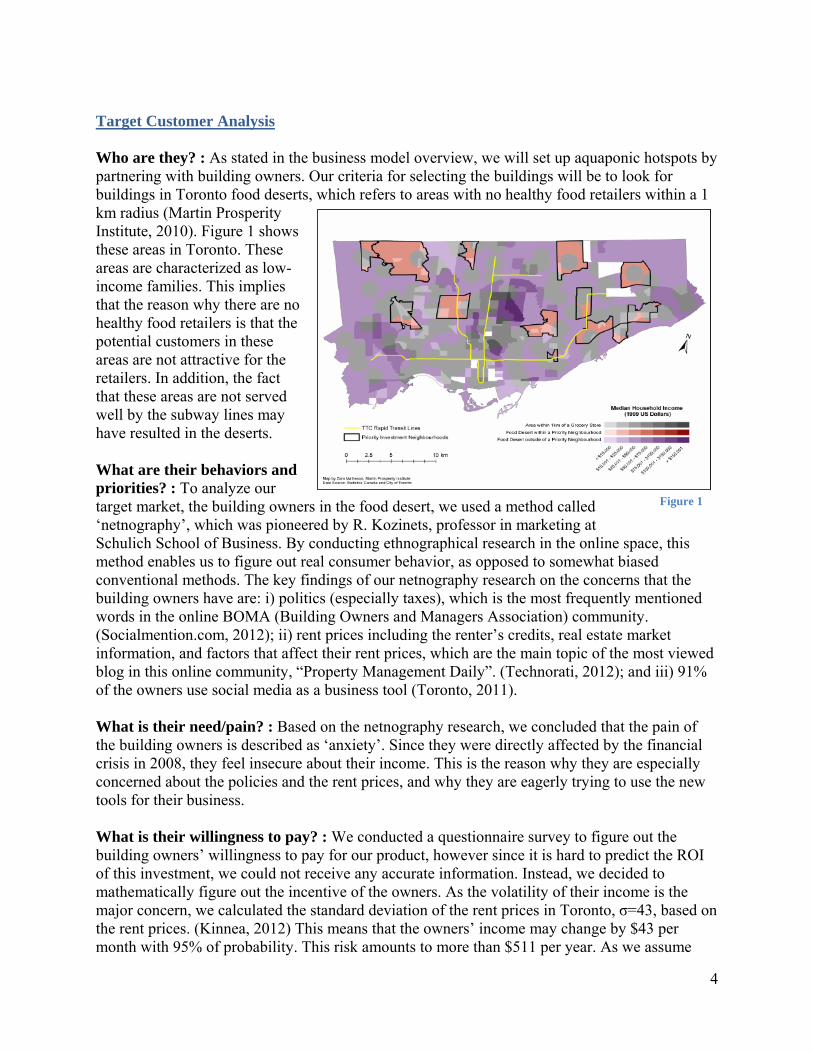

Target Customer Analysis Who are they? : As stated in the business model overview, we will set up aquaponic hotspots by partnering with building owners. Our criteria for selecting the buildings will be to look for buildings in Toronto food deserts, which refers to areas with no healthy food retailers within a 1 km radius (Martin Prosperity Institute, 2010). Figure 1 shows these areas in Toronto. These areas are characterized as low-income families. This implies that the reason why there are no healthy food retailers is that the potential customers in these areas are not attractive for the retailers. In addition, the fact that these areas are not served well by the subway lines may have resulted in the deserts. What are their behaviors and priorities? : To analyze our target market, the building owners in the food desert, we used a method called ‘netnography’, which was pioneered by R. Kozinets, professor in marketing at Schulich School of Business. By conducting ethnographical research in the online space, this method enables us to figure out real consumer behavior, as opposed to somewhat biased conventional methods. The key findings of our netnography research on the concerns that the building owners have are: i) politics (especially taxes), which is the most frequently mentioned words in the online BOMA (Building Owners and Managers Association) community. (Socialmention.com, 2012); ii) rent prices including the renter’s credits, real estate market information, and factors that affect their rent prices, which are the main topic of the most viewed blog in this online community, “Property Management Daily”. (Technorati, 2012); and iii) 91% of the owners use social media as a business tool (Toronto, 2011). What is their need/pain? : Based on the netnography research, we concluded that the pain of the building owners is described as ‘anxiety’. Since they were directly affected by the financial crisis in 2008, they feel insecure about their income. This is the reason why they are especially concerned about the policies and the rent prices, and why they are eagerly trying to use the new tools for their business. What is their willingness to pay? : We conducted a questionnaire survey to figure out the building owners’ willingness to pay for our product, however since it is hard to predict the ROI of this investment, we could not receive any accurate information. Instead, we decided to mathematically figure out the incentive of the owners. As the volatility of their income is the major concern, we calculated the standard deviation of the rent prices in Toronto, σ=43, based on the rent prices. (Kinnea, 2012) This means that the owners’ income may change by $43 per month with 95% of probability. This risk amounts to more than $511 per year. As we assume

Figure 1

5

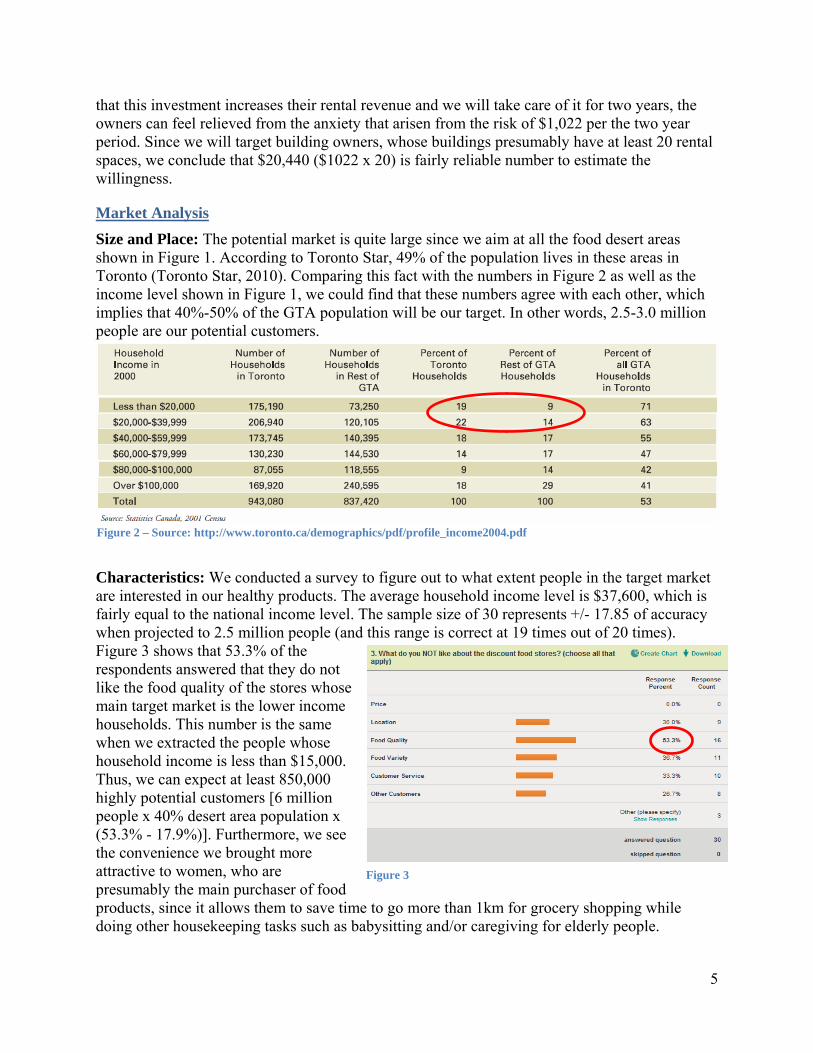

Figure 2 – Source: http://www.toronto.ca/demographics/pdf/profile_income2004.pdf

Figure 3

that this investment increases their rental revenue and we will take care of it for two years, the owners can feel relieved from the anxiety that arisen from the risk of $1,022 per the two year period. Since we will target building owners, whose buildings presumably have at least 20 rental spaces, we conclude that $20,440 ($1022 x 20) is fairly reliable number to estimate the willingness.

Market Analysis

Size and Place: The potential market is quite large since we aim at all the food desert areas shown in Figure 1. According to Toronto Star, 49% of the population lives in these areas in Toronto (Toronto Star, 2010). Comparing this fact with the numbers in Figure 2 as well as the income level shown in Figure 1, we could find that these numbers agree with each other, which implies that 40%-50% of the GTA population will be our target. In other words, 2.5-3.0 million people are our potential customers.

Characteristics: We conducted a survey to figure out to what extent people in the target market are interested in our healthy products. The average household income level is $37,600, which is fairly equal to the national income level. The sample size of 30 represents +/- 17.85 of accuracy when projected to 2.5 million people (and this range is correct at 19 times out of 20 times). Figure 3 shows that 53.3% of the respondents answered that they do not like the food quality of the stores whose main target market is the lower income households. This number is the same when we extracted the people whose household income is less than $15,000. Thus, we can expect at least 850,000 highly potential customers [6 million people x 40% desert area population x (53.3% - 17.9%)]. Furthermore, we see the convenience we brought more attractive to women, who are presumably the main purchaser of food products, since it allows them to save time to go more than 1km for grocery shopping while doing other housekeeping tasks such as babysitting and/or caregiving for elderly people.

6

List of Aquaponics System Providers • Aquaponic Gardening (Boulder, CO, USA) • Backyard Aquaponics (Success, W Australia) • DIY Aquaponics (Orange Park, FLA, USA) • Friendly Aquaponics (Honoka’a, HI, USA) • Growing Power (Milwaukee, WI, USA) • Nelson + Pade (Montello, WI, USA) • Practical Aquaponics (North Maclean, QLD, Australia)• S&S Aqua Farms (West Plains, MO, USA) • Urban Aquaponics (Bundamba, QLD, Australia)

Entry barriers/ substitutes: Barriers to entry is considered to be low. We will elaborate on this issue in the risk section. As shown above, people are seeking good quality substitutes to the currently available foods. Thus, the threat of substitutes is negligible.. Growth Trend: According to a community research conducted by University of Toronto, it is forecasted that the low income population, whose incomes are more than 20% below the average, will grow by 16.4% by 2020. (Hulchanski, 2007) This group is not an attractive segment for food retailers, or even if so, the quality of the products provided to this group will be questionable. Therefore, the food desert will continue to exist, and most likely to grow at a fast pace.

The Competition

In terms of an organization selling aquaponics systems to low-income, high-density buildings in Toronto, there would appear to be zero direct competition. Aquaponics is a relatively new concept, with little traction in Canada. There is no local aquaponics Toronto chapter. A self-help aquaponics website exists in Edmonton, www.edmontonaquaponics.org, however there is no similar Canadian site. At this website, almost all commercial (or retail) links suggested to purchase equipment are in the US or Australia (see Figure4).

To summarize, the commercial and retail aquaponics market is in nascent phase, with no Toronto or Ontario presence, and with a fractured US presence. There would be appeared to be no threat of any of these suppliers competing with our business.

Other urban farming organizations, such as Foodshare, or Young Urban Farmers, would also not post a serious competitive threat, as they would either welcome our entry into the market, or find themselves serving entirely different markets. Similarly, the issue of food security is so broad, the size of Toronto’s food deserts so large, that any solution will have hundreds of components. The likelihood of any one solution in the market completely addressing the social problem is essentially zero. Lastly, there would seem to be no credible competitive threat in terms of building improvement. A building owner looking to improve his/her building can do so in innumerable ways, so one improvement (e.g. better water pressure) does not preclude the addition of other improvements, such as an aquaponic system. In conclusion then, the key assumption would be that competition is either non-existent, too fractured or non-competitive, and research would support this assumption. If this business is to fail, it will not likely be because we are out-competed.

Figure 4

7

Risk

There are multiple kinds of risk associated with this business plan. It is important to be aware of all potential sources of risk before undertaking this venture so that every possible action can be taken to mitigate these risks and increase the viability of this business. Potential Entry: The first source of risk would be from the potential entry of firms using similar business models. Though aquaponics itself and this business model specifically are new in Toronto it can be easily replicated by those with access to the correct technology and the technical knowledge to be able to use and maintain the units adequately. Though the business model (and the aquaponic units themselves) is new in Toronto there is nothing proprietary about the technology and, as a result, there is not much our company could do to prevent another business from sourcing and selling their own units to interested parties within the same geographic market. Naturally, competition in the market would drive product prices down and, in fact, there is no way of ensuring our company is not undercut by those entering the same market. However, we should try to differentiate our business as much as possible. One way this is done is to utilize the first mover advantage. This allows us to tap into the ‘blue ocean’ in which we can expect high profitability and high growth. As long as we can grow rapidly, we can remain competitive to some extent even if there are low-price competitors since it is difficult for the building owners to replace the units once installed. In addition, we could switch our supplier to a more cost-effective supplier if the competition intensifies. Wrong Prediction: Another huge source of risk would be the chance that aquaponics – or the way we have presented it to potential customers through our business model – would not gain traction among Toronto consumers. This technology is unlike any that exists in the Toronto agriculture market currently and there is a chance that will not be embraced by building owners in general. If for whatever reason the technology is rejected, then the business model as it exists now would inevitably be a failure. In this case, we should immediately cease our business model. Therefore, we should constantly pay attention to the inventory level so as to sustain the liquidity. Supplier: At present, our business plans to import these aquaponic units from a supplier in either the US or Australia. The risk here is the chance of this supplier going out of business/bankrupt. Since the commercial and retail aquaponics market is in nascent phase, there is a chance that we may be left with no supplier in the case our supplier goes out of business on short notice. Any delay in sourcing these units (or parts or accessories for the units) could have a negative effect not only on sales but on customer relationships. Currency: As we purchase the aquaponic units from abroad, our procurement activity is always exposed to currency risk. Although a conventional wisdom tells us that we could entirely hedge this currency risk by using currency forward contracts, it is not easy for us to implement because we also need to keep the inventory level low. In other words, we would have to have so many long-positioned contracts that our labour cost increases. In addition, the labour would need to have a skill to settle these OTC contracts. This also adds up the labour cost. Instead, we could pursue cash transaction without incurring accounts payables. This way, we could at least negotiate purchasing price with the supplier even though we are still fully exposed to the risk.

8

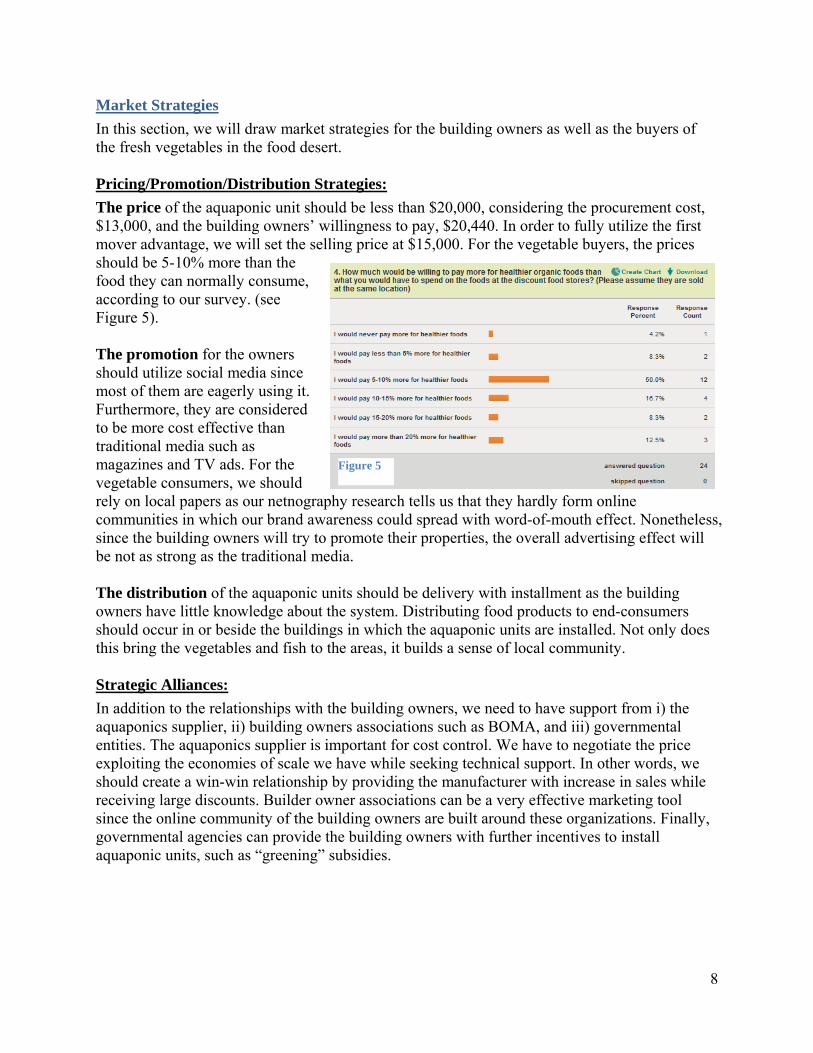

Figure 5

Market Strategies

In this section, we will draw market strategies for the building owners as well as the buyers of the fresh vegetables in the food desert. Pricing/Promotion/Distribution Strategies:

The price of the aquaponic unit should be less than $20,000, considering the procurement cost, $13,000, and the building owners’ willingness to pay, $20,440. In order to fully utilize the first mover advantage, we will set the selling price at $15,000. For the vegetable buyers, the prices should be 5-10% more than the food they can normally consume, according to our survey. (see Figure 5). The promotion for the owners should utilize social media since most of them are eagerly using it. Furthermore, they are considered to be more cost effective than traditional media such as magazines and TV ads. For the vegetable consumers, we should rely on local papers as our netnography research tells us that they hardly form online communities in which our brand awareness could spread with word-of-mouth effect. Nonetheless, since the building owners will try to promote their properties, the overall advertising effect will be not as strong as the traditional media. The distribution of the aquaponic units should be delivery with installment as the building owners have little knowledge about the system. Distributing food products to end-consumers should occur in or beside the buildings in which the aquaponic units are installed. Not only does this bring the vegetables and fish to the areas, it builds a sense of local community. Strategic Alliances:

In addition to the relationships with the building owners, we need to have support from i) the aquaponics supplier, ii) building owners associations such as BOMA, and iii) governmental entities. The aquaponics supplier is important for cost control. We have to negotiate the price exploiting the economies of scale we have while seeking technical support. In other words, we should create a win-win relationship by providing the manufacturer with increase in sales while receiving large discounts. Builder owner associations can be a very effective marketing tool since the online community of the building owners are built around these organizations. Finally, governmental agencies can provide the building owners with further incentives to install aquaponic units, such as “greening” subsidies.

9

Organizational Infrastructure

In order to carry out our business plan, there are four different functionalities required.

Management/Governance: Decision making, maintaining relationships with key partners, representing a company as a legal entity (compliance), and coordinating all the other functionalities. The CEO and the assistant will assume this task.

Sales and Marketing: Implementation of the promotional strategies described above and all the transactional activities including supplier negotiation. The sales person assumes this task.

Finance: Accounting, seeking investors (see the finance section), budget management, and risk hedging. The CEO and the assistant will assume this task.

Technical Operations: Aquaponic unit delivery, installation, maintenance, and advisory. Assistance in selling foods to building occupants. The technical staff will assume this task.

To fulfill these four areas of functionalities, we will need eight employees:

CEO (1): Undertakes the management/governance and the finance functionalities. Fair knowledge of management, strategy, and finance is required. In addition, strong passion for solving the food desert problem is required.

Assistant (1): Supports the CEO. Competitive communication skill and knowledge of accounting are necessary. Strong interest in the social problem is required.

Sales (2): Undertake the sales and marketing function as a team. Directly reports to the CEO. Experience in B2B sales, and knowledge of social media marketing and the real estate industry are required. Part of the salaries is commission-based to incentivize these staff.

Technical Staff (4): In charge of the technical operations and directly reports to the CEO as a team. Knowledge of agriculture (especially urban farming) is necessary. Passion to solve the social problem is required. At the inception, we will require two employees. After 6 months, we plan to add another two depending on the sales growth.

Since most of the clerical functions are done by the CEO and the Assistant, the employees will work from home, except the Assistant who will work at the CEO’s place.

Legal Considerations

Legal Framework: As a food business, there are several key legal considerations, which include but are not limited to:

Register our business with Ministry of Business and Consumer Services Gain a municipal license Obtain a provincial operating license Secure proper municipal zoning approvals for our farming units Obtain a business number from Revenue Canada Registering for the PST Prepare for being employers, in particular compliance with Ministry of Labour

regulations and Workers Safely Insurance Board rules Securing business insurance

10

Having regular health inspections Obtain a food handler’s certificate from Toronto Public Health

Our business will also require sufficient insurance for employee claims, and any food sales liabilities. Legal Structure: This business operates as a private for-profit company to minimize reporting requirements. Co-op could be another option because the building owners have an established community, however it may be difficult to ask them to be members without considerable support from the community leader such as the BOMA. Additionally, the somewhat hierarchical governance style may not fit the characteristic of co-op, which delegates voting share to each member regardless of the amounts of their investment. It is our assumption that we will require modest capital startup funds, as our business would start small and then scale up. If our organization could secure business development grants or external investors, we would ideally structure as a for-profit business. This would allow our organization to make quick decisions and retain maximum flexibility with decision making. Should start up capital come from a foundation or government granting agency, our organization may be forced to set up as non-profit, though not a registered charity. Forming as a non-profit is not desirable, as it limits the scope of activities the organization could undertake.

Financials

With Aquaponic units being installed in buildings with intent to sell the produce to the building occupants, we will be selling the largest size units called the deluxe (Backyard Aquaponics). In order to map out our financial forecast, we make the following assumptions:

1. While the retail price for these units (including installation) is $11,475, we believe that including the shipping costs we will be able to import this product at $13,000.

2. With limited time (30 minutes per aquaponic unit) and farming expertise required, we believe that on an average one technical staff will be able to cater to 12 aquaponic units a day in an 8 hour shift and will be paid at an hourly rate of $12 per hour.

3. We will require 2 technical staff for the first 6 months, and as number of units installed increases we will require 4 staff in all.

4. Due to economies of scale, cost of producing the vegetables and fish will be 5% lower than what it would cost an individual to produce the same yield.

5. Sales personnel will be paid $3000 per month and a 3% commission on each sale. 6. We will be able to sell 55 units in the first year. (6% of the BOMA members) 7. Any unsold produce will be sold to restaurants or local markets. 8. The rent for the hotspot is one-year contract.

The financial forecast is shown in Figure 6. Based on this forecast, we calculated the following:

Start-up Financial Need: $35,000 Net Profit Margin: Pessimistic = -35%, Baseline = 4%, Optimistic = 11% Break Even Units: 43 units Break Even Sales: $947,505

11

As explained in the risk section, we would have to withdraw from this business if the sales trajectory is similar to the pessimistic scenario. Therefore, we will provide the start-up cost in order to make the liquidation process simple in case of the withdrawal. Assuming no interest charge and no need to concern repayments, the business will be off the hook both from financing cost and a potential forced-bankruptcy.

Unit Price

$ per unit Pessimistic # Baseline # Optimistic # Pessimistic $ Baseline $ Optimistic $

Revenue

Aquaponic Unit Sales 15,000 20 55 80 300,000 825,000 1,200,000

Veggies and Fish per Unit 7,035 20 55 80 140,700 386,925 562,800

Total Revenue 440,700 1,211,925 1,762,800

Costs

<Startup>

Aquaponic unit for the hotspot 13,000 1 1 1 13,000 13,000 13,000

Rent for the hotspot (1yr contract) 1,000 12 12 12 12,000 12,000 12,000

Start Up Costs (Website/Social Media) 10,000 1 1 1 10,000 10,000 10,000

<Fixed>

CEO salary 5,000 1 1 1 60,000 60,000 60,000

Assistant salary 3,000 1 1 1 36,000 36,000 36,000

Tech. Staff salary for the first 6 months 2,880 2 2 2 34,560 34,560 34,560

Tech. Staff salary after 6 months 2,880 2 4 6 34,560 69,120 103,680

Sales Personnel salary (Fixed part) 36,000 2 2 2 72,000 72,000 72,000

Utilities and Miscellaneous 1,500 12 12 12 18,000 18,000 18,000

<Variable>

Procurement for Aquaponic 13,000 20 55 80 260,000 715,000 1,040,000

Veggies and Fish

(including util ities and seedlings costs)1,743 20 55 80 34,865 95,879 139,460

Sales Personnel (Commission) 450 20 55 80 9,000 24,750 36,000

Total Costs 593,985 1,160,309 1,574,700

Net Profit (Total Rev‐Total Cost) ‐153,285 51,616 188,100

Expected quantities Total amount of dollarsItems

Figure 6

Exit Strategy:

Up to one or two years from installation, the units already sold to building owners will be taken care of by the technical staff. After this period, our service will be limited to advisory, assuming that the owners can either learn the way to manage the units or find someone to take this job over at their expense. This model enables us to effectively and rapidly expand in the market without being over-staffed, in order to attain the first mover advantage. This will help us to withdraw from this business in case of sluggish sales. In addition, the “just in time” business model, which refers to the low-inventory strategy in which we import the units upon orders from the building owners, will make it even easier to exit.

12

Bibliography Backyard Aquaponics. (n.d.). Cost Benefit Analysis of Aquaponic Systems.

Hulchanski, J. D. (2007). Centre for Urban & Community Studies: Research Bulletin 41. Toronto: University of Toronto.

Kinnea, J. (2012, March 17). Toronto Real Estate Statistics Database. Retrieved March 17, 2012, from Toronto Real Estate Statistics Database: http://juliekinnear.com/toronto-real-estate-market-statistics

Martin Prosperity Institute. (2010). Food Deserts and Priority Neighbourhoods in Toronto. Toronto: Martin Prosperity Institute.

Socialmention.com. (2012, March 17). Mentions about "BOMA toronto". Retrieved March 17, 2012, from Socialmention.com: http://www.socialmention.com/search?t=all&q=%22BOMA+toronto%22&btnG=Search&start=15

Technorati. (2012, March 17). Blogs relating to “real estate owners”. Retrieved March 17, 2012, from Technorati: http://technorati.com/search?return=sites&authority=all&q=real+estate+owners&x=11&y=20

Toronto Star. (2010, June 14). A struggle to eat in Toronto’s food deserts. Retrieved March 18, 2012, from thestar.com: http://www.thestar.com/yourcitymycity/article/823514--a-struggle-to-eat-in-toronto-s-food-deserts

Toronto, B. (2011, July 22). BOMA Toronto @BOMATORONTO. Retrieved March 17, 2012, from Twitter: https://twitter.com/#!/BOMATORONTO