mbi - basel ii- unit ii

TRANSCRIPT

BASEL ACCORD• Basel is a city in Switzerland which is also the headquarters of

Bureau of International Settlement (BIS).• BIS fosters co-operation among central banks with a common goal

of financial stability and common standards of banking regulations. • Currently there are 27 member nations in the committee. Basel

guidelines refer to broad supervisory standards formulated by this group of central banks- called the Basel Committee on Banking Supervision (BCBS). The set of agreement by the BCBS, which mainly focuses on risks to banks and the financial system are called Basel accord.

• The purpose of the accord is to ensure that financial institutions have enough capital on account to meet obligations and absorb unexpected losses.

• India has accepted Basel accords for the banking system. BASEL capital adequacy norms were enacted in 1988

BASEL I• In 1988, BCBS introduced capital measurement system

called Basel capital accord, also called as Basel 1.• It focused almost entirely on credit risk.• It defined capital and structure of risk weights for banks.• The minimum capital requirement was fixed at 8% of

risk weighted assets (RWA). • RWA means assets with different risk profiles. For

example, an asset backed by collateral would carry lesser risks as compared to personal loans, which have no collateral. India adopted Basel 1 guidelines in 1999.

BASEL II• In 2004, Basel II guidelines were published by BCBS, which were

considered to be the refined and reformed versions of Basel I accord.

• The guidelines were based on three parameters.• Banks should maintain a minimum capital adequacy requirement

of 8% of risk assets, banks were needed to develop and use better risk management techniques in monitoring and managing all the three types of risks that is credit and increased disclosure requirements.

• Banks need to mandatorily disclose their risk exposure, etc to the central bank.

• Basel II norms in India and overseas are yet to be fully implemented.

BASEL III• In 2010, Basel III guidelines were released. • These guidelines were introduced in response to the

financial crisis of 2008.• A need was felt to further strengthen the system as

banks in the developed economies were under-capitalized, over-leveraged and had a greater reliance on short-term funding.

• Also the quantity and quality of capital under Basel II were deemed insufficient to contain any further risk. The guidelines aim to promote a more resilient banking system by focusing on four vital banking parameters viz. capital, leverage, funding and liquidity.

What is Basel II?• Basel II (also cited as Basel 2), also known as the

International Convergence of Capital Measurement and Capital Standards, helps international banks and financial institutions safeguard themselves against operational and financial risks.

• It does this by setting up rigorous risk and capital management requirements designed to ensure that a bank holds enough capital reserves on hand to offset its risks.

• With Basel II, each bank has to follow minimum risk methodology standards, develop their own risk management framework and ensure regulatory supervision.

OBJECTIVE

• The final version aims at:• Ensuring that capital allocation is more risk sensitive;• Enhance disclosure requirements which will allow

market participants to assess the capital adequacy of an institution;

• Ensuring that credit risk, operational risk and market risk are quantified based on data and formal techniques;

• Attempting to align economic and regulatory capital more closely to reduce the scope for regulatory arbitrage.

Basel II Implementation• Basel II Guidelines are based on a framework of 3 pillars.• Pillar 1: Minimum Capital Requirements – Identify risks,

quantitatively measure risks, mitigate risks, allocate minimum capital for each risk

• Pillar 2: Supervisory review – Provide visibility into the risk management infrastructure, support supervisory review of capital adequacy and internal risk measurement methodologies, determine ability to hold additional capital above and beyond Pillar 1

• Pillar 3: Market Discipline – Release relevant financial data to the public to help investors evaluate the bank's health

PILLAR I- Minimum Capital Requirements

• The main international effort to establish rules around capital requirements has been the Basel Accords, published by the Basel Committee on Banking Supervision housed at the Bank for International Settlements.

• This sets a framework on how banks and depository institutions must calculate their capital.

• In 1988, the Committee decided to introduce a capital measurement system commonly referred to as Basel I.

• This framework has been replaced by a significantly more complex capital adequacy framework commonly known as Basel II.

• After 2012 it will be replaced by Basel III.[

• In India, the Tier 1 capital is defined as "'Tier I Capital' means "owned fund“.

• Owned funds stand for paid up equity capital, preference shares which are compulsorily convertible into equity, free reserves, balance in share premium account and capital reserves representing surplus arising out of sale proceeds of asset, excluding reserves created by revaluation of asset, as reduced by accumulated loss balance, book value of intangible assets and deferred revenue expenditure, if any.

• Tier 2 capital, or supplementary capital, comprises undisclosed reserves, revaluation reserves, general provisions, hybrid instruments and subordinated term debt(debt which is repaid when all the other creditors are paid).

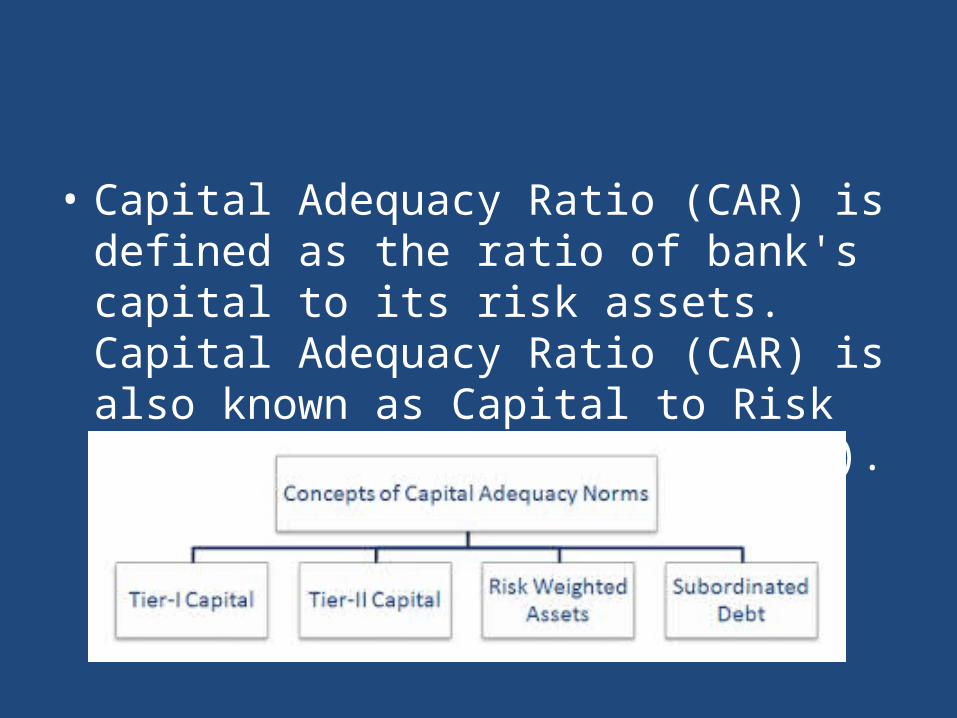

• Capital Adequacy Ratio (CAR) is defined as the ratio of bank's capital to its risk assets. Capital Adequacy Ratio (CAR) is also known as Capital to Risk (Weighted) Assets Ratio (CRAR).

CAPITAL ADEQUACY RATIO

• Basel I norms prescribed a minimum capital adequacy ratio (CRAR) [1] of 8 % for Banks which were signatories to the Basel Accord.

• Basel I framework was confined to the prescription of only minimum capital requirements for banks, the Basel II framework expands this approach not only to capture certain additional risks in the minimum capital ratio but also includes two additional areas, Supervisory Review Process and Market Discipline through increased disclosure

CAPITAL ADEQUACY RATIO

• The minimum capital to risk-weighted asset ratio (CRAR) in India is placed at 9%, one percentage point above the Basel II requirement. All the banks have their Capital to Risk

• Weighted Assets Ratio (CRAR) above the stipulated requirement of Basel guidelines (8%) and RBI guidelines (9%). As per Basel II norms, Indian banks should maintain tier I capital of at least 6%.

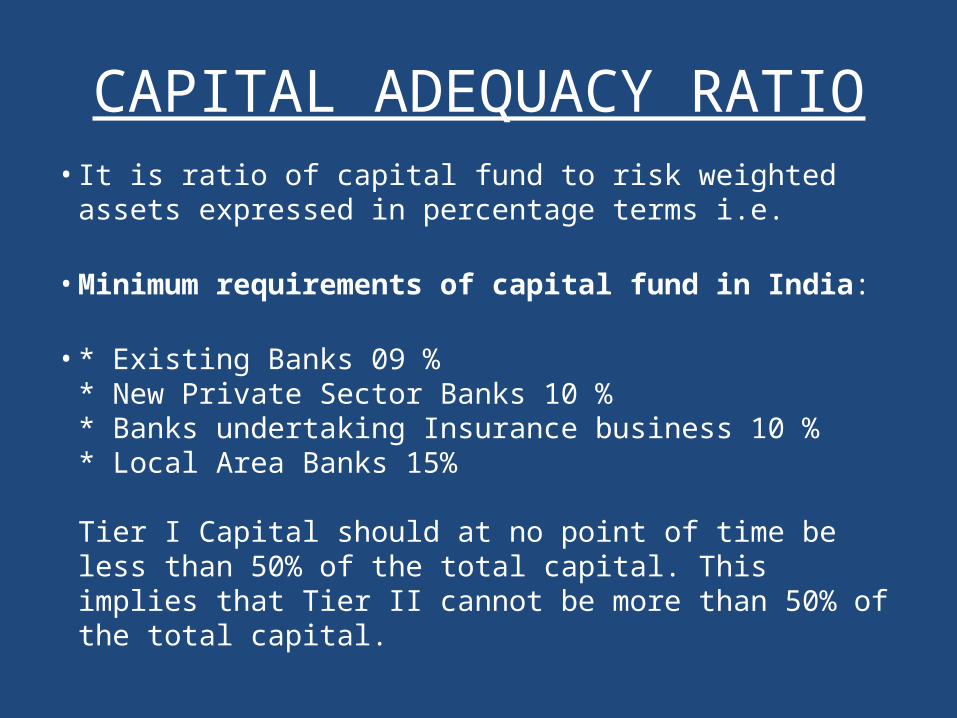

CAPITAL ADEQUACY RATIO• It is ratio of capital fund to risk weighted assets expressed in

percentage terms i.e.

• Minimum requirements of capital fund in India:

• * Existing Banks 09 % * New Private Sector Banks 10 % * Banks undertaking Insurance business 10 % * Local Area Banks 15%

Tier I Capital should at no point of time be less than 50% of the total capital. This implies that Tier II cannot be more than 50% of the total capital.

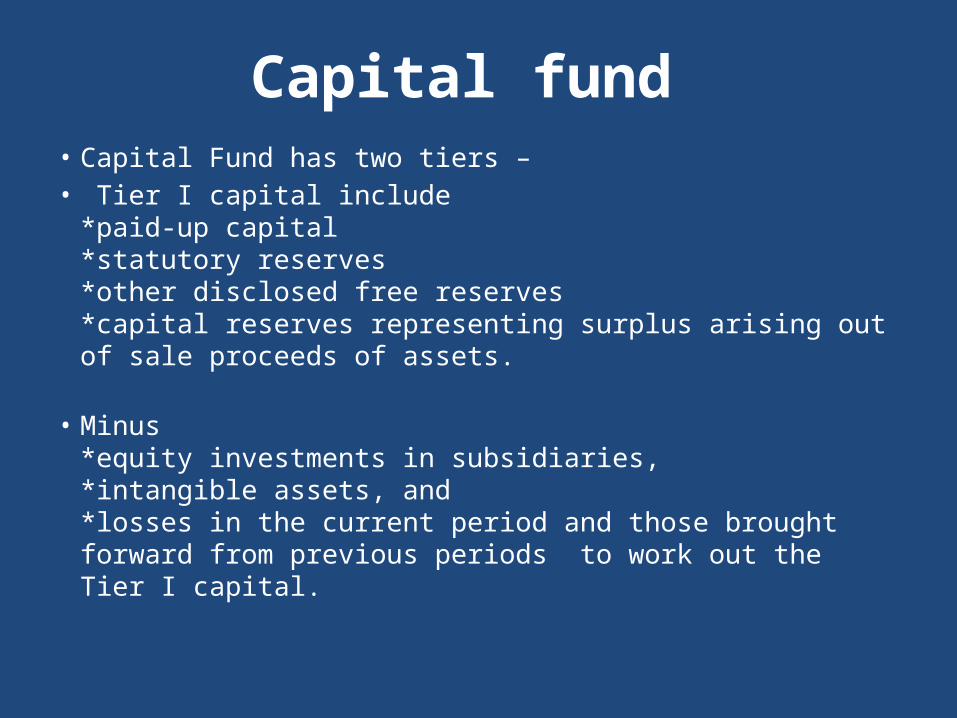

Capital fund • Capital Fund has two tiers –• Tier I capital include

*paid-up capital *statutory reserves *other disclosed free reserves *capital reserves representing surplus arising out of sale proceeds of assets.

• Minus *equity investments in subsidiaries, *intangible assets, and *losses in the current period and those brought forward from previous periods to work out the Tier I capital.

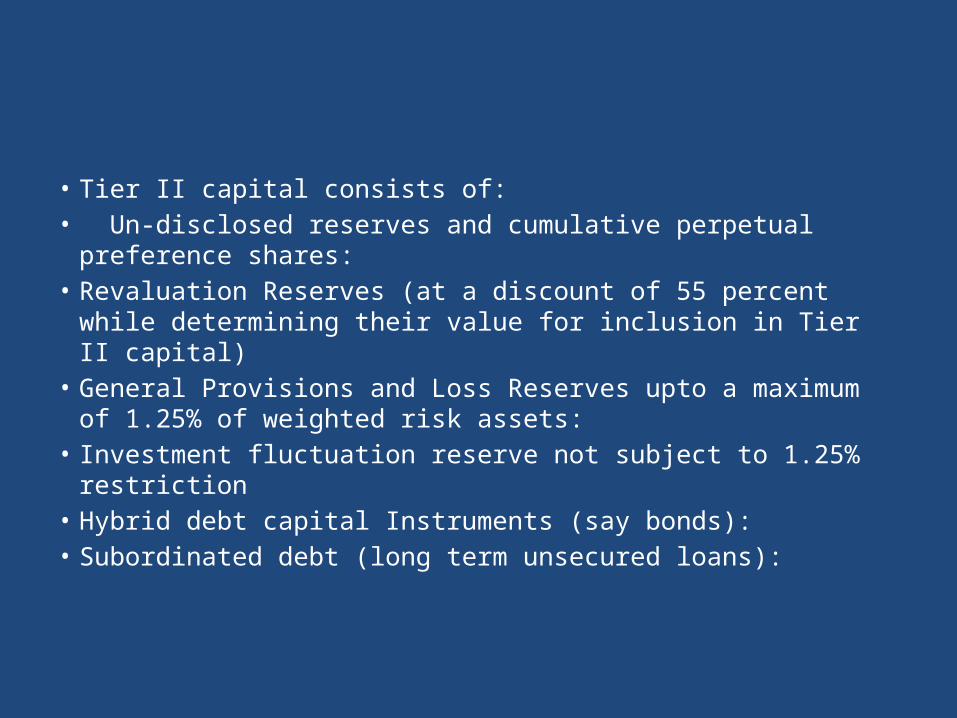

• Tier II capital consists of: • Un-disclosed reserves and cumulative perpetual preference

shares: • Revaluation Reserves (at a discount of 55 percent while

determining their value for inclusion in Tier II capital) • General Provisions and Loss Reserves upto a maximum of 1.25% of

weighted risk assets: • Investment fluctuation reserve not subject to 1.25% restriction • Hybrid debt capital Instruments (say bonds): • Subordinated debt (long term unsecured loans):

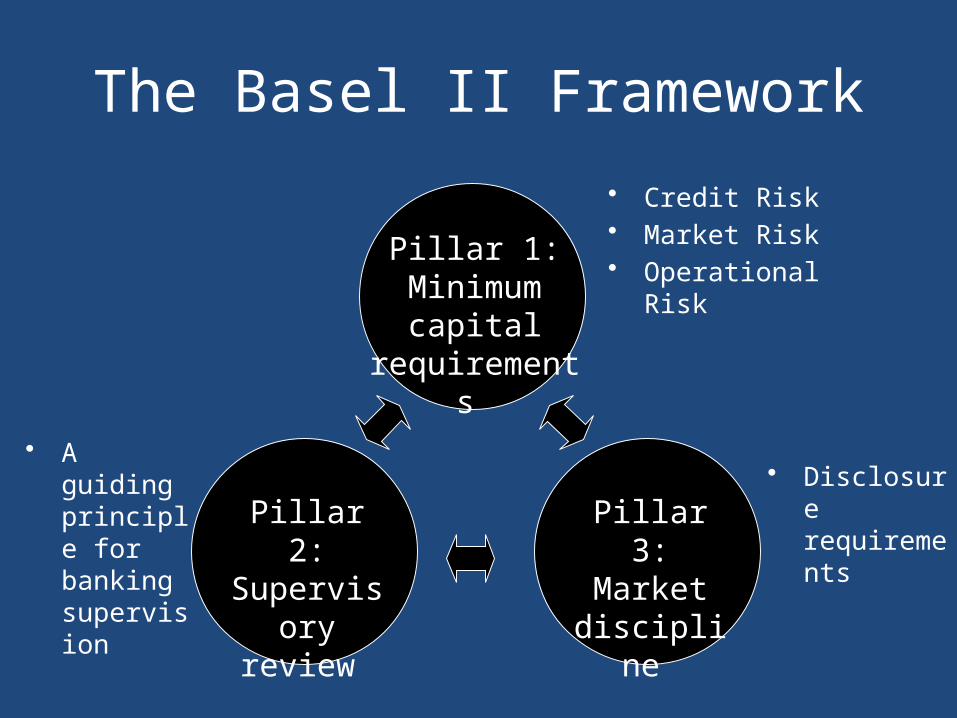

The Basel II Framework

Pillar 1: Minimum capital

requirements

Pillar 2: Supervisory

review

Pillar 3: Market

discipline

• A guiding principle for banking supervision

• Credit Risk• Market Risk• Operational Risk

• Disclosure requirements

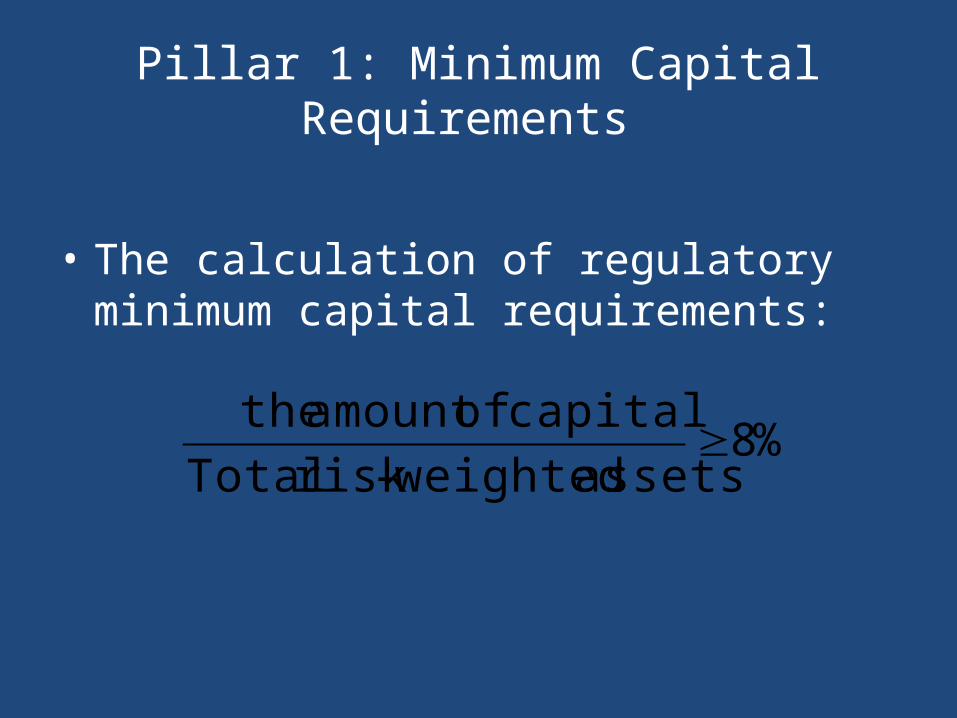

Pillar 1: Minimum Capital Requirements

• The calculation of regulatory minimum capital requirements:

%8assets weighted-risk Total

capital ofamount the

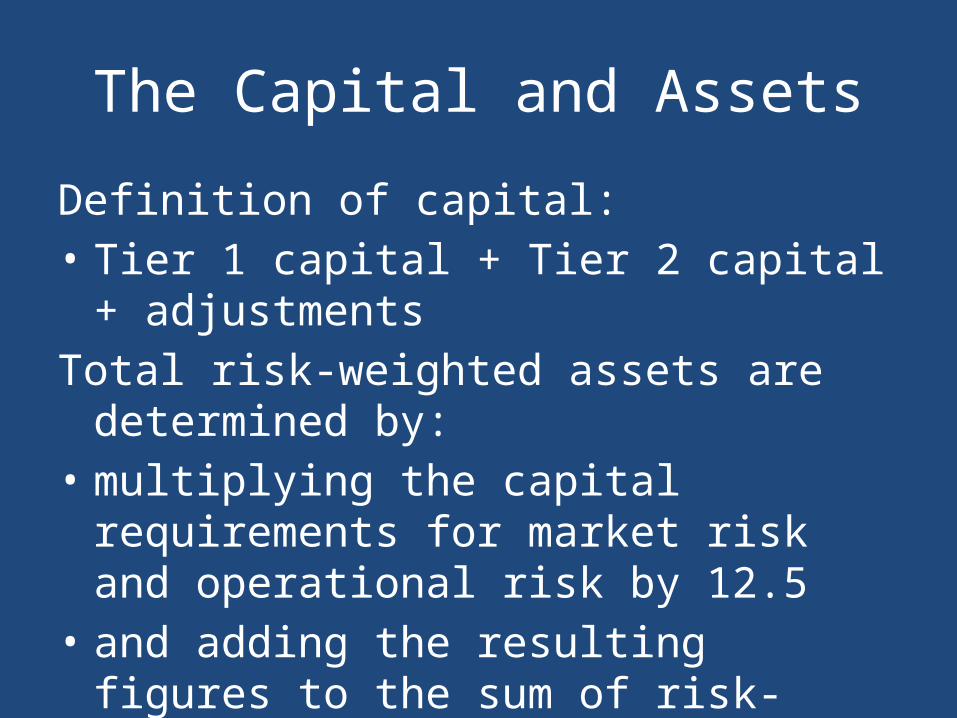

The Capital and Assets

Definition of capital:• Tier 1 capital + Tier 2 capital + adjustmentsTotal risk-weighted assets are determined by:• multiplying the capital requirements for

market risk and operational risk by 12.5• and adding the resulting figures to the sum of

risk-weighted assets for credit risk.

Credit risk

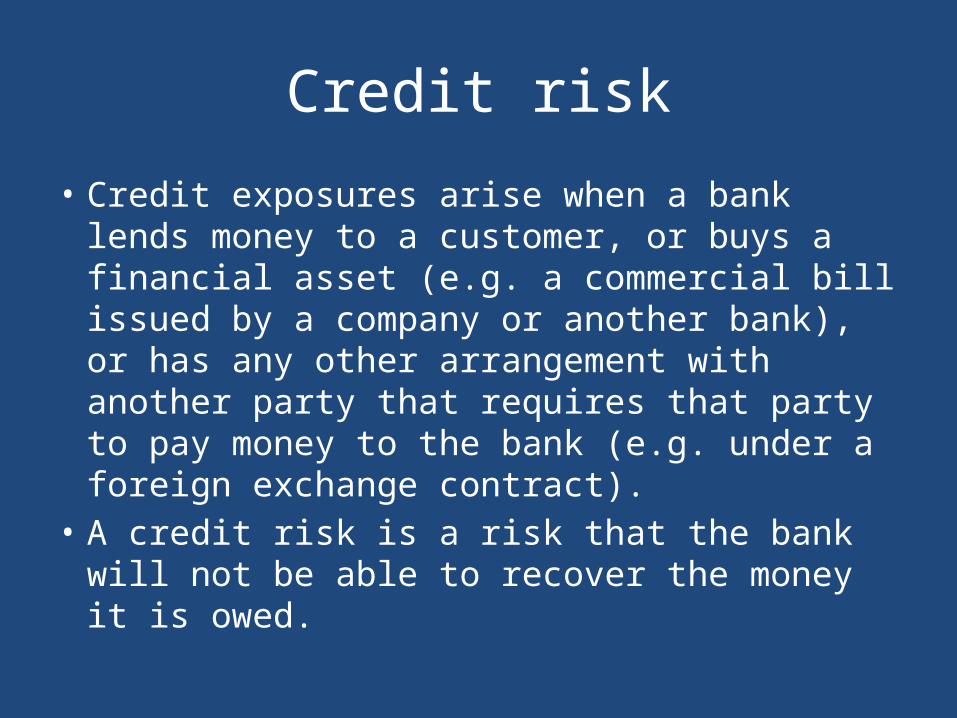

• Credit exposures arise when a bank lends money to a customer, or buys a financial asset (e.g. a commercial bill issued by a company or another bank), or has any other arrangement with another party that requires that party to pay money to the bank (e.g. under a foreign exchange contract).

• A credit risk is a risk that the bank will not be able to recover the money it is owed.

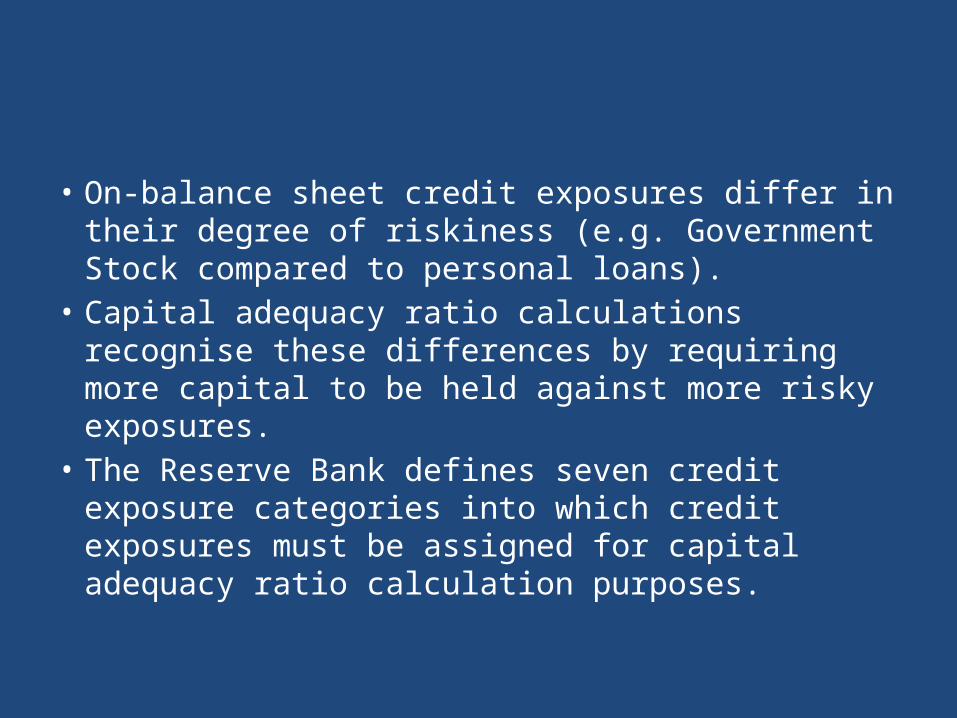

• On-balance sheet credit exposures differ in their degree of riskiness (e.g. Government Stock compared to personal loans).

• Capital adequacy ratio calculations recognise these differences by requiring more capital to be held against more risky exposures.

• The Reserve Bank defines seven credit exposure categories into which credit exposures must be assigned for capital adequacy ratio calculation purposes.

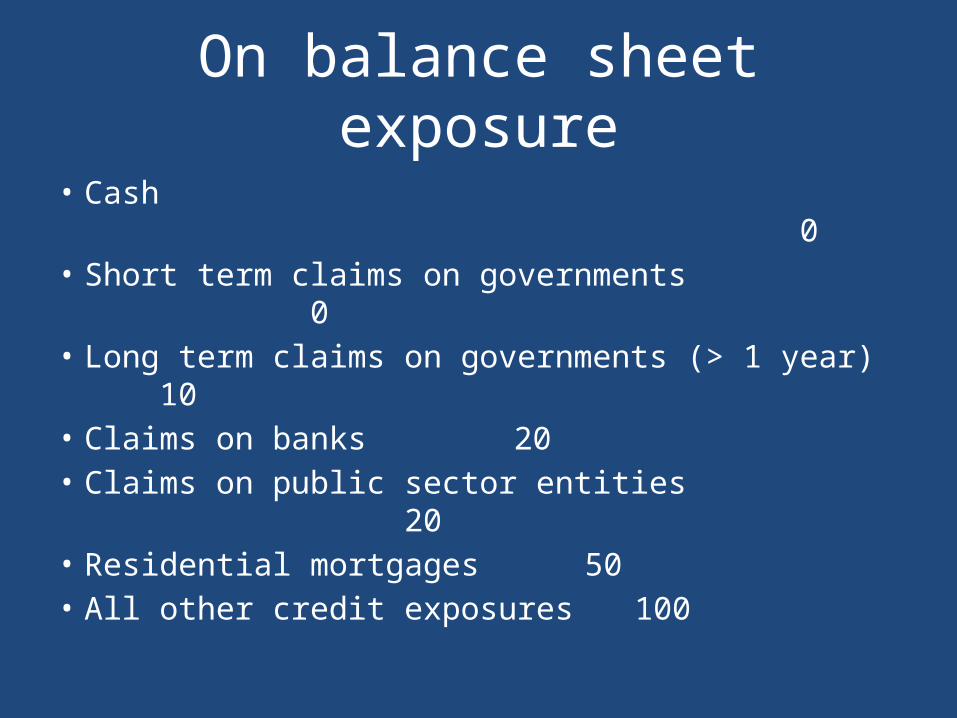

On balance sheet exposure

• Cash 0• Short term claims on governments 0• Long term claims on governments (> 1 year) 10• Claims on banks 20• Claims on public sector entities 20• Residential mortgages 50• All other credit exposures 100

Credit Risk

• Standardised Approach• Foundation IRB Approach• Advanced IRB Approach

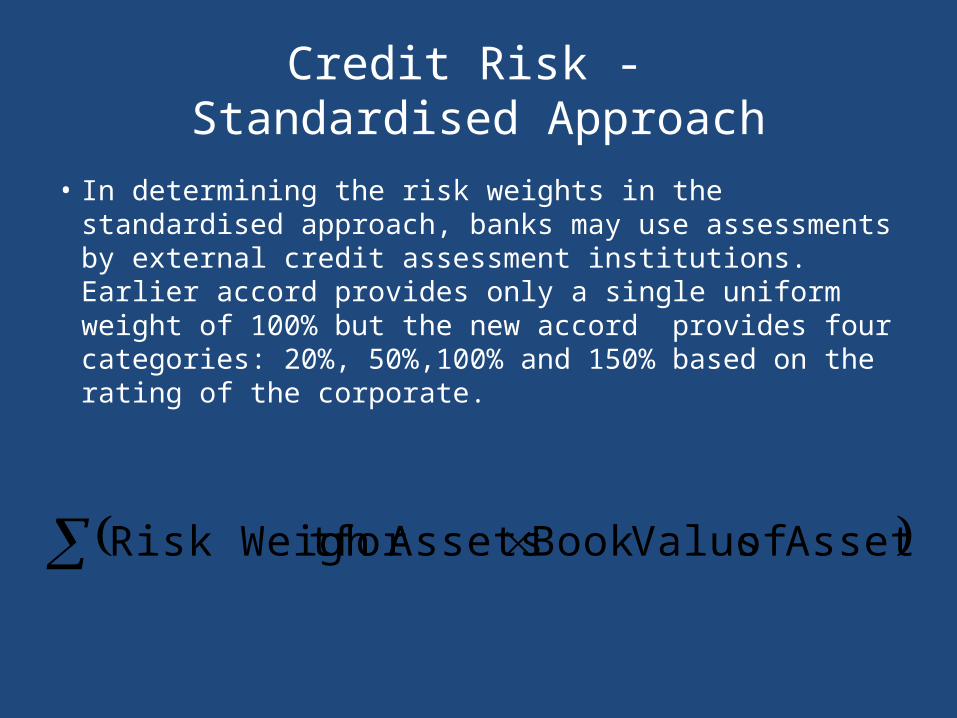

Credit Risk - Standardised Approach

• In determining the risk weights in the standardised approach, banks may use assessments by external credit assessment institutions. Earlier accord provides only a single uniform weight of 100% but the new accord provides four categories: 20%, 50%,100% and 150% based on the rating of the corporate.

Assets of ValusBook Assetsfor t Risk Weigh

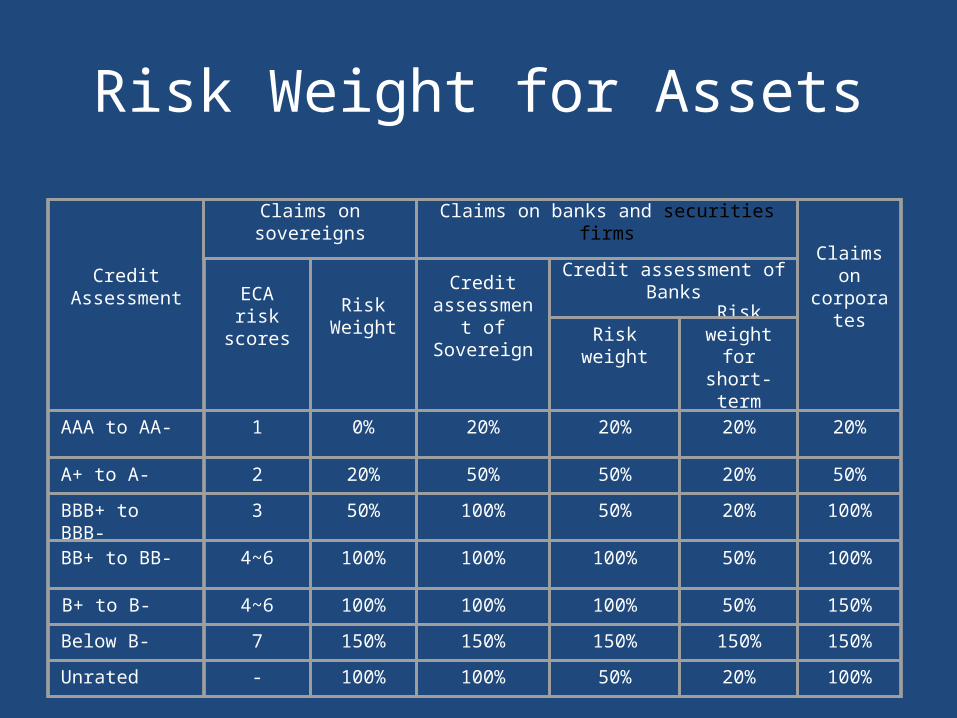

Risk Weight for Assets

Credit Assessment

Claims on sovereigns

Claims on banks and securities firms

Claims on corporatesECA risk

scoresRisk

Weight

Credit assessment of

Sovereign

Credit assessment of Banks

Risk weight

Risk weight

for short-term

AAA to AA- 1 0% 20% 20% 20% 20%

A+ to A- 2 20% 50% 50% 20% 50%

BBB+ to BBB- 3 50% 100% 50% 20% 100%

BB+ to BB- 4~6 100% 100% 100% 50% 100%

B+ to B- 4~6 100% 100% 100% 50% 150%

Below B- 7 150% 150% 150% 150% 150%

Unrated - 100% 100% 50% 20% 100%

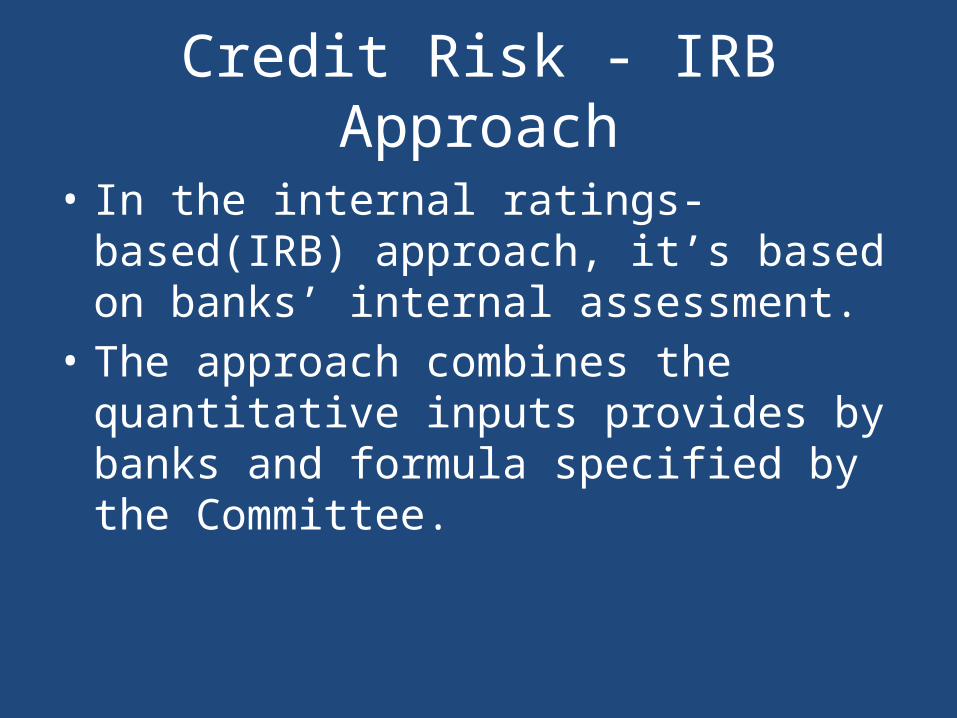

Credit Risk - IRB Approach

• In the internal ratings-based(IRB) approach, it’s based on banks’ internal assessment.

• The approach combines the quantitative inputs provides by banks and formula specified by the Committee.

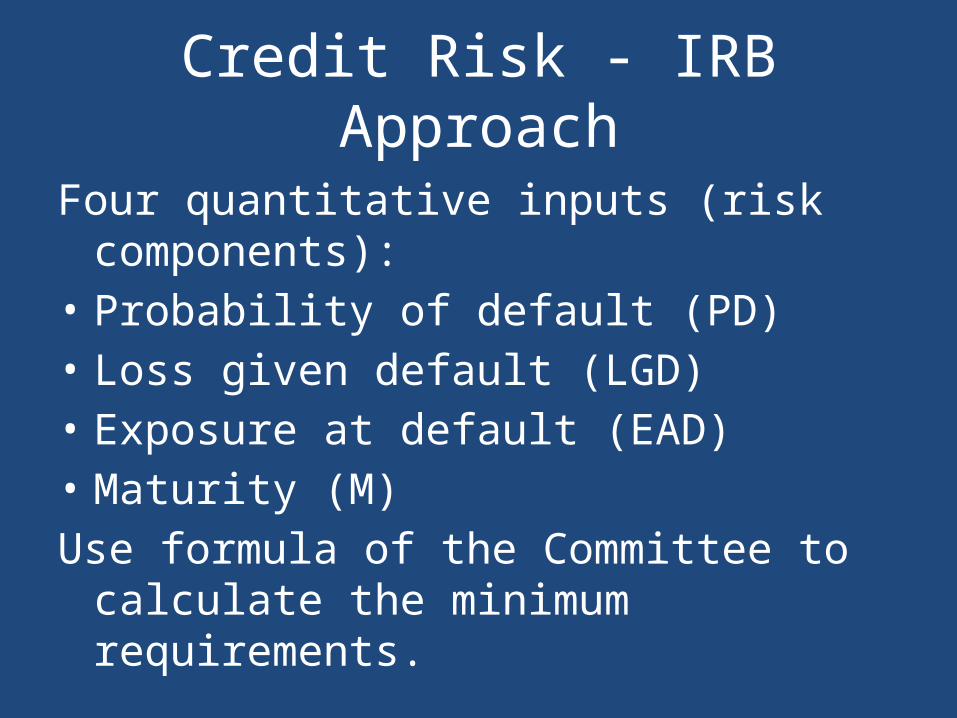

Credit Risk - IRB Approach

Four quantitative inputs (risk components):• Probability of default (PD)• Loss given default (LGD)• Exposure at default (EAD)• Maturity (M) Use formula of the Committee to calculate the

minimum requirements.

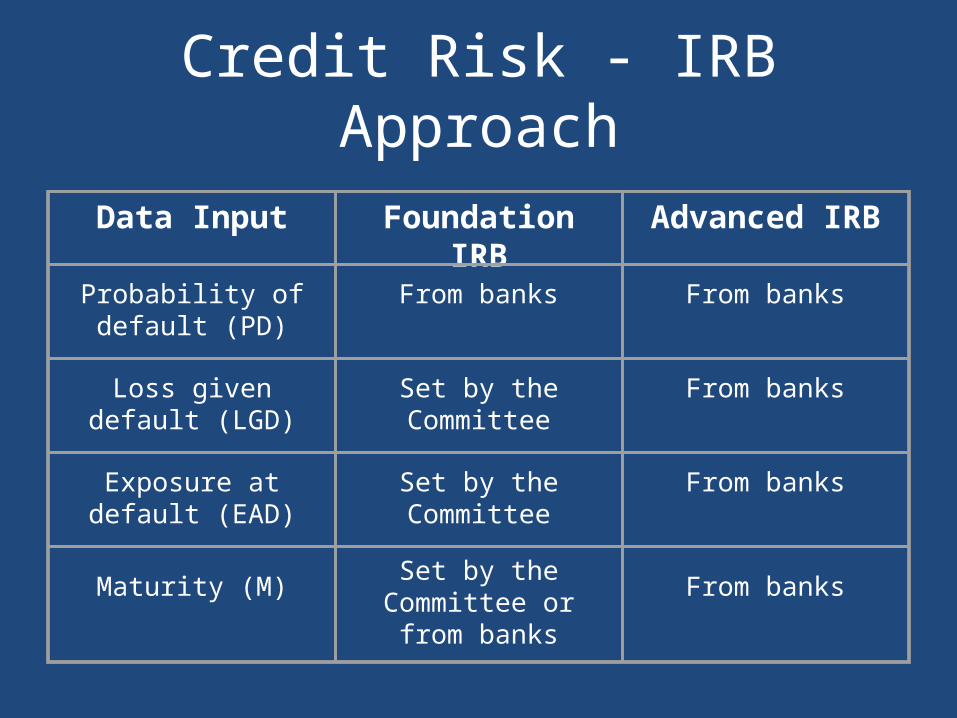

Credit Risk - IRB Approach

Data Input Foundation IRB Advanced IRB

Probability of default (PD)

From banks From banks

Loss given default

(LGD)

Set by the Committee

From banks

Exposure at default

(EAD)

Set by the Committee

From banks

Maturity (M)

Set by the Committee or from banks

From banks

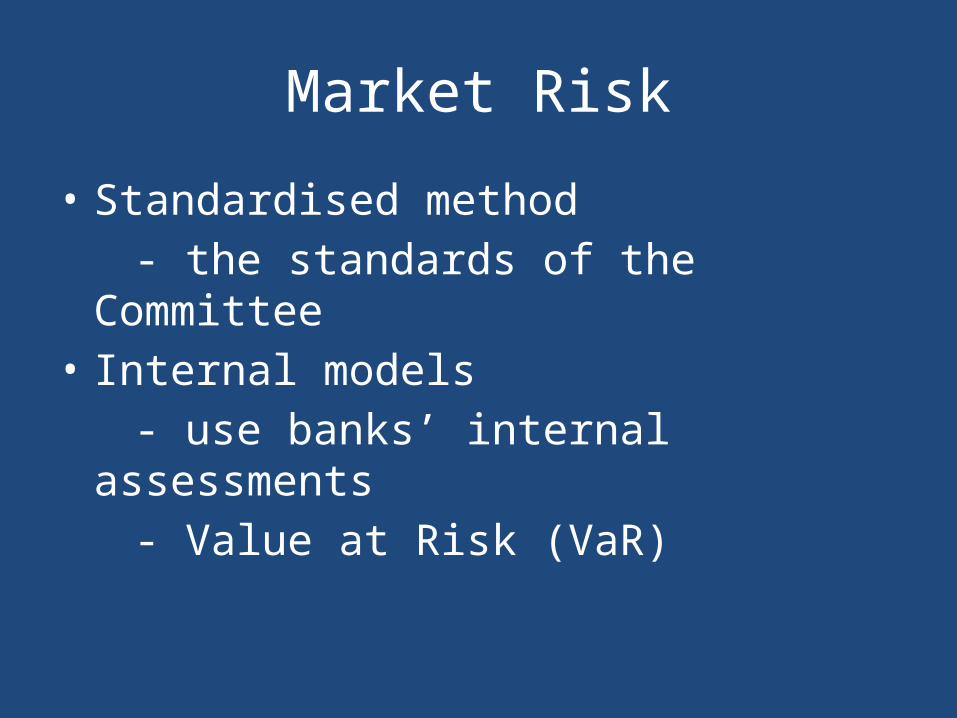

Market Risk

• Standardised method - the standards of the Committee• Internal models - use banks’ internal assessments - Value at Risk (VaR)

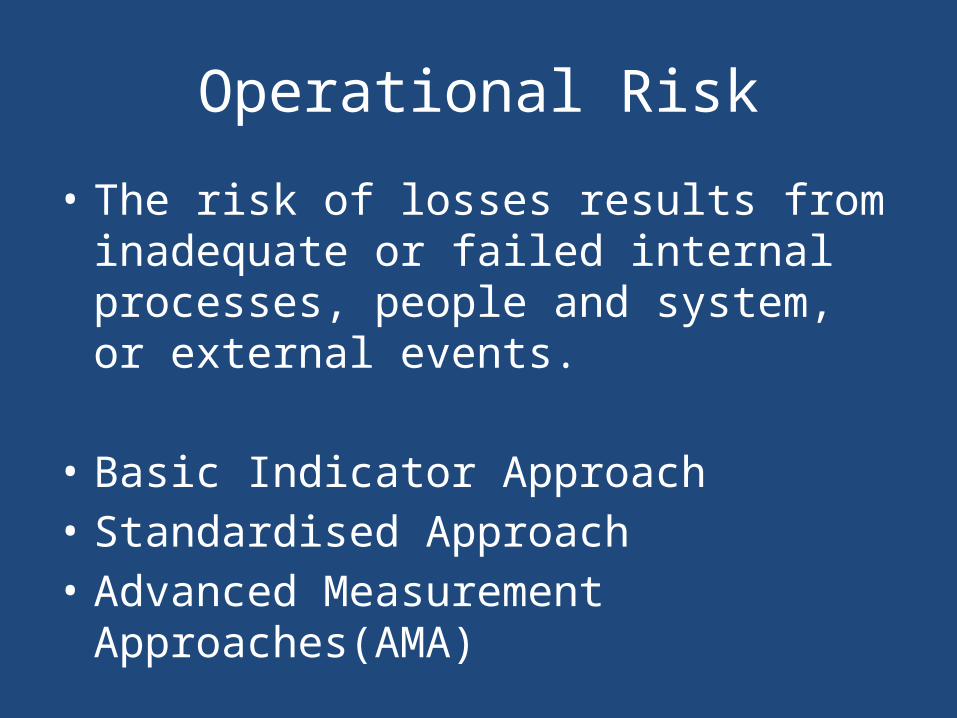

Operational Risk

• The risk of losses results from inadequate or failed internal processes, people and system, or external events.

• Basic Indicator Approach• Standardised Approach• Advanced Measurement Approaches(AMA)

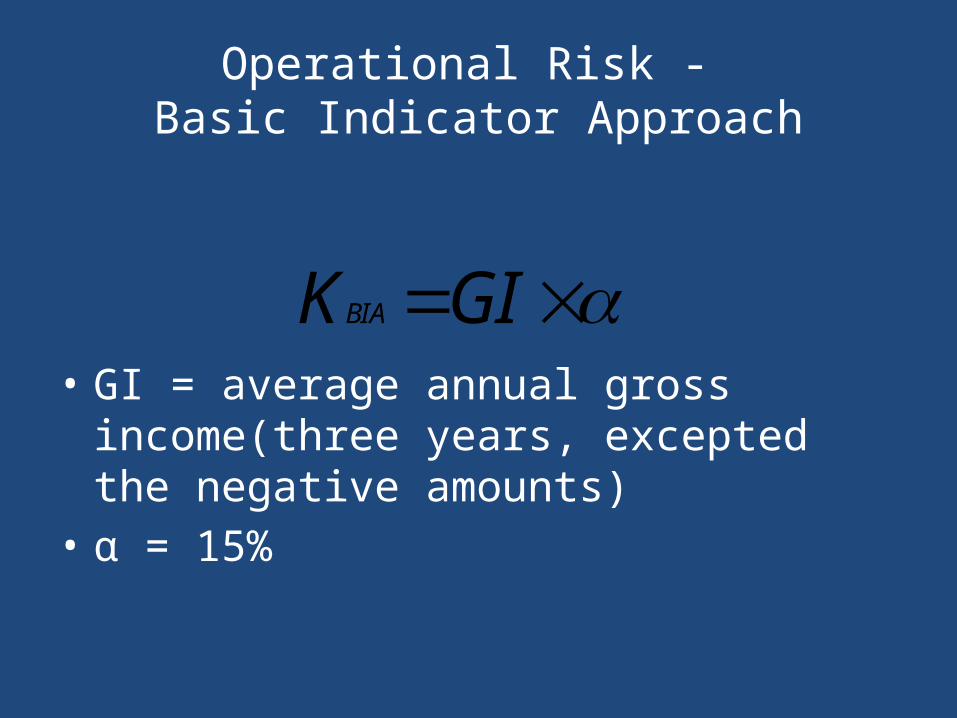

Operational Risk - Basic Indicator Approach

• GI = average annual gross income(three years, excepted the negative amounts)

• α = 15%

GIKBIA

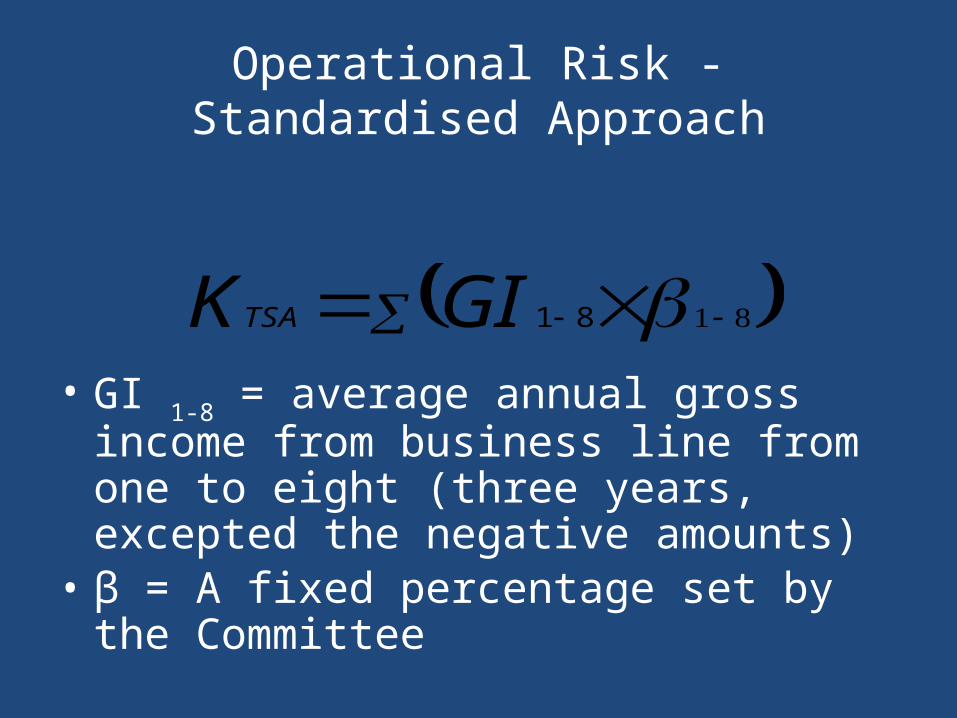

Operational Risk -Standardised Approach

• GI 1-8 = average annual gross income from business line from one to eight (three years, excepted the negative amounts)

• β = A fixed percentage set by the Committee

81GIKTSA

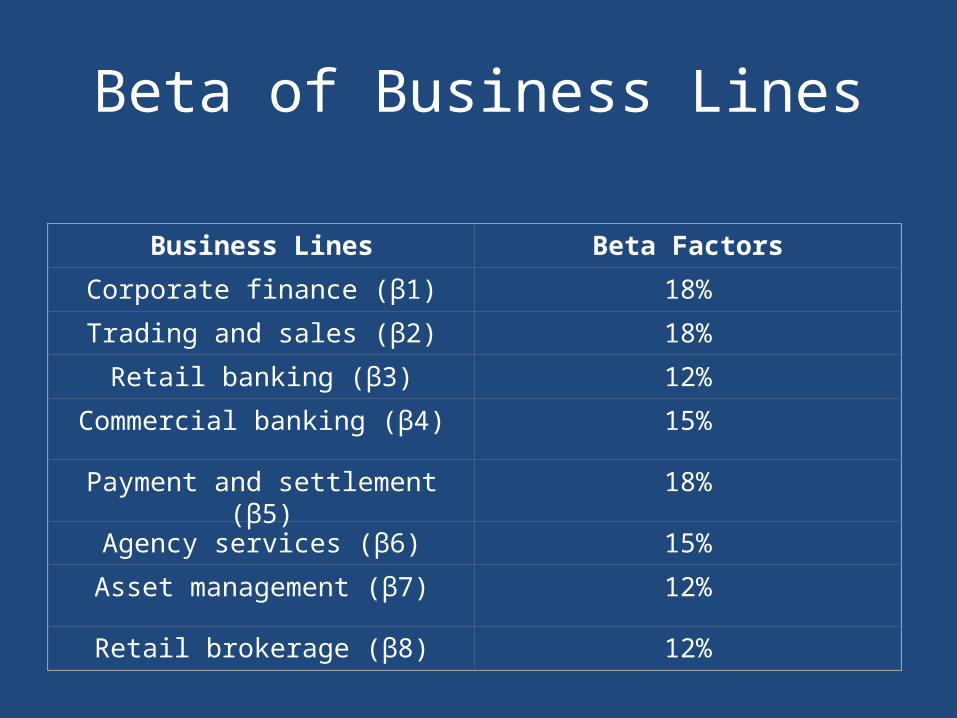

Beta of Business Lines

Business Lines Beta Factors

Corporate finance (β1) 18%

Trading and sales (β2) 18%

Retail banking (β3) 12%

Commercial banking (β4) 15%

Payment and settlement (β5) 18%

Agency services (β6) 15%

Asset management (β7) 12%

Retail brokerage (β8) 12%

Operational Risk - Advanced Measurement Approaches

• Under the AMA, the regulatory capital requirement will equal the risk measure generated by the bank’s internal operational risk measurement system using the quantitative and qualitative criteria for the AMA.

• Use of the AMA is subject to supervisory approval.

Pillar 2: Supervisory Review

• Principle 1: Banks should have a process for assessing and maintaining their overall capital adequacy.

• Principle 2: Supervisors should review and evaluate banks’ internal capital adequacy assessments and strategies.

• Supervisors would be responsible for evaluating how well the banks are assessing the capital adequacy needs relative to their risks.

Supervisory Review

• Principle 3: Supervisors should expect banks to operate above the minimum regulatory capital ratios.

• Principle 4: Supervisors should intervene at an early stage to prevent capital from falling below the minimum levels.

Board for Financial Supervision(BFS)

• BFS was constituted in Nov 1994 under RBI. The main instrument of supervision is “Inspection”.

• For the on-site supervision , the Inspecting officers concentrate on core assessment based on the CAMELS model(Capital adequacy, asset Quality, Management, Earnings, Liquidity(asset liability management), sensitivity(involves market risk particularly interest rate risk))

• Further by 2002, a revised rating model (CALCS)was developed that incorporates the component of ‘Liquidity’in the rating of foreign branches in India.

• The CAMELS ratings or Camels rating is a supervisory rating system originally developed in the U.S. to classify a bank's overall condition.

Pillar 3: Market Discipline

• The purpose of pillar three is to complement the pillar one and pillar two.

• Develop a set of disclosure requirements to allow market participants to assess information about a bank’s risk profile and level of capitalization.

Minimum Capital Adequacy Ratios

• Tier one capital to total risk weighted credit exposures to be not less than 4 %;

• Total capital (i.e. tier one plus tier two less certain deductions) to total risk weighted credit exposures to be not less than 8%

Calculation of Capital

Tier One Capital • the ordinary share capital (or equity) of the

bank; and • audited revenue reserves e.g.. retained

earnings; less • current year's losses; • future tax benefits; and • intangible assets, e.g. goodwill.

Calculation of Capital

Upper Tier Two Capital• Un-audited retained earnings; • revaluation reserves; • general provisions for bad debts; • perpetual cumulative preference shares (i.e.

preference shares with no maturity date whose dividends accrue for future payment even if the bank's financial condition does not support immediate payment);

• perpetual subordinated debt (i.e. debt with no maturity date which ranks in priority behind all creditors except shareholders).

Calculation of Capital

Lower Tier Two Capital • Subordinated debt with a term of at least 5

years; • Sedeemable preference shares which may not

be redeemed for at least 5 years.

Restrictions

• Tier two capital may not exceed 100% of tier one capital;

• Lower tier two capital may not exceed 50% of tier one capital;

• Lower tier two capital is amortized on a straight line basis over the last five years of its life.

Total Capital

This is the sum of tier 1 and tier 2 capital less the following deductions:

• equity investments in subsidiaries; • shareholdings in other banks that exceed 10

percent of that bank's capital; • unrealized revaluation losses on securities

holdings.