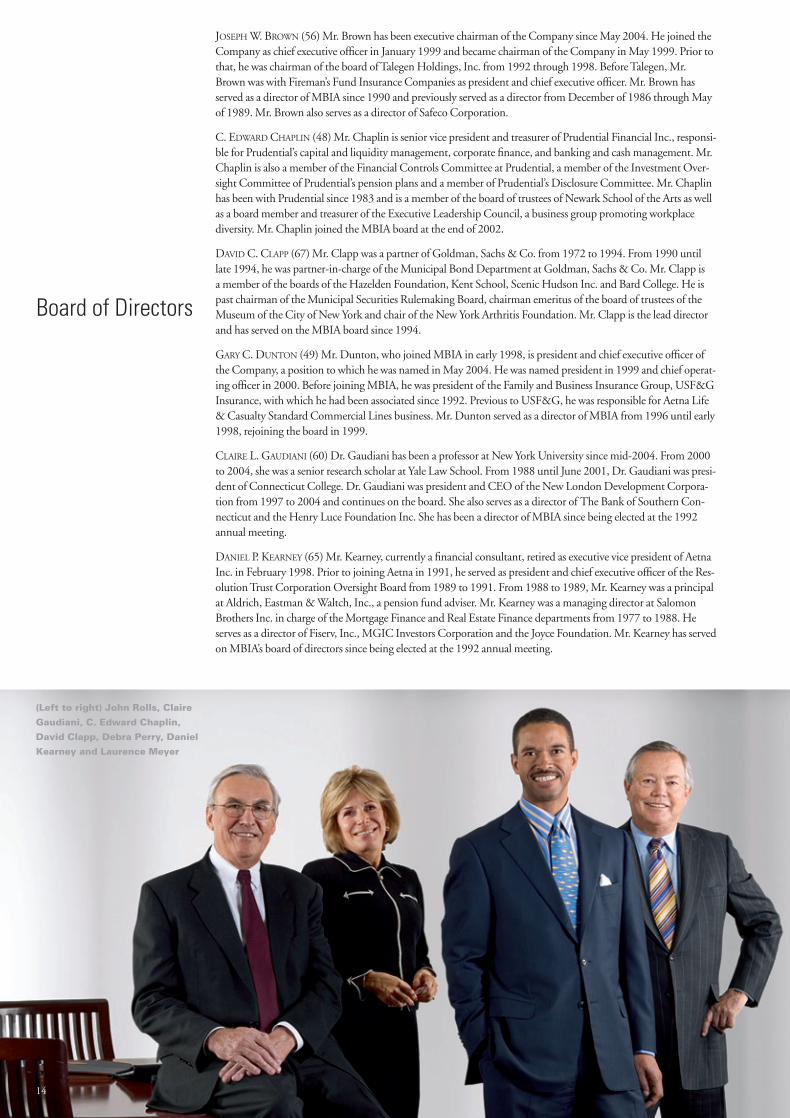

mbia annual report 2004 · baiocco, michael ballinger, frances banuelos, ann barbara, mary barbara,...

TRANSCRIPT

Baiocco, Michael Ballinger, Frances Banuelos, Ann Barbara, Mary Barbara, Lorraine Barg, Steve Barney, Jason Bathauer, Barry Baughier, Michael Baumkirchner, Jennifer Beaton, Natacha Beauboeuf, Brad Beck, Marguerite Beirne, Tom Bell, Lajuanda Bell, Dinah Bellis, Regina Bello, Jim Berger, Adam Bergonzi, Beth Berman, Paul Bernier, Gerry

an, Amy Brown, Jay Brown, Kevin Brown, Taresha Bryant, Karen Brylle, Neil Budnick, Mark Bunyea, Joe Buonadonna, Danny Burdiez, Nicole Byrd, Christine Calvao, Jason Cameron, Lisa Campbell, Lori Candarelli, Lisa Carinha, Linda Carpenter, Bill Carson, Adam Carta, Bill Carta, Mike Castracan, Judy Cavino, Jason Celente, Kevin Cerutti, Chris

ce Clark, Robyn Clarke, Miriam Cleary, Tom Cochran, William Cody, Robert Cole, Madelyn Coleman, Rosemaria Collorafi, Jeffrey Concepcion, Steve Cooke, Brian Cooney, Christie Corbett, Marti Correa, Cliff Corso, Irene Cortez, Jonathan Costello, Kenneth Couch, Thomas Cousins, David Craparo, Celinda Creighton, Jim Cronin, Ian Crooke, David

Laura DeLena, Carole Delorme, Nils Demme, Maureen Denyssenko, Lauren Desharnais, Charles Deutsch, William DeVane, Tom Devine, Ed DeVito, Jamie Di Orio, Greg Diamond, James DiChiaro, Wendy Dinsmore, Sharon Dittrich, Andrew Dixon, Michelle Dixon, Stephen Dixon, Christie Dixon, Everlena Dolman, Adriana Dominguez, Michelle

Ferguson, Gregg Ferguson, Nick Ferreri, Denise Feulner, Peter Fiala, Claus Fintzen, Sara Fischer, Anna Fischetti, Minnie Fitchben, Rosanne Fleury, Barbara Flickinger, Kimberlee Florin, Mary Flynn, Jesse Fogarty, Alison Fong, Karen Foxhall, Carol Fraundorfer, Dan Frisch, Max Gabriel, Julie Galante, Theodore Galgano, Rich Garay, James Garelick,

Greene, Aeneas Griffin, Jin Gu, Marsha Gumbs, Deirdre Guppy, John Hall, Traci Hall, John Hallacy, Steve Halpert, Christina Halvorsen, Doug Hamilton, Christine Hammond, Joanne Han, Melanie Haniph, Bret Harmon, Roger Harris, Andre Harris, Donald Harrison, Dana Hartman, Emete Hassan, Eugene Havel, Oddette Haynes, Bob Heller, Irene

es, Ahmed Ibrahim, Felicia Ivey, Rosalie Jackson, Lynn Jacobs, Lori Jalomo, Liz James, Ed Janson, Douglas Jensen, Janet Johnson, Adrian Jones, Joanne Jontz, Michael Joos, John Jordan, Tom Jordan, Deirdre Jordan-Coleman, Chris Jumper, Esther Kain, Maria Kang, Una Kearns, Liz Keese-Blasius, Rosemary Kelley, Brian Kelly, Patrick Kelly,

kin, Corinne Larson, Andy Laterza, Linda Latta, Gaddi Layden, Beatrice Le, Leon Leborgne Jr., David Lee, Jackie Lee, Jae Lee, Michael Lee, Poh Choo Lee, Andrew Leggio, Hannes Leifsson, Jane Lence, Jim Lennon, Lynn Leone, Maria Levin, Larry Levitz, Shella Lieberman, John Lilly, Sonya Linder-Silidjian, Linda Lindh, Eleanor Lipsey, Sandra

n, Amy Mauer-Litos, Thomas Mauk, Eric McAlley, Lisa McCall, Ellen McCarthy, Shaun McClelland, David McCollum, Martin McDermott, Jean McGovern, Noeleen McGovern, Jim McGrane, Tim McKeon, Anthony McKiernan, Tom McLoughlin, Linda McManus, Sadie McSwain, Jennifer Melle, Eugenio Mendoza, Ani Mensuroglu, Graham Metcalf,

y, Stephen Murray, Theresa Murray, Michael Murtagh, Joan Musselbrook, Brenda Narayan, Salvatore Narciso, Dan Nash, Eric Neglia, Bob Nevin, Julie Ng, Deb Nickel, Ann Nicoletti, Laurie Nicoletti, Stig Nielsen, Petya Nikolova, Mike Norris, Oliver North, Gerhard Oberholzer, Gonzalo Obregon, Michael O'Brien, Frances Ochoa, Lauren Oliaro, Pat

ndrew Porges, Scot Post, Cynthia Praschnik, Andrea Preftes, Bevin Presutti, Daniel Primavera, Armand Principato, Clifford Pritchard, Christopher Przymylski, Jim Pugh, Binu Punnoose, Kerrie Radoor, Beverly Raine, Ed Rajsteter, Andrea Randolph, Kathleen Reagan, Kevin Regan, Christopher Reid, Chip Reilly, Sue Reilly, David Rey, Loretta Rivera,

, Eric Savino, Kristie Scafidi, Colleen Scaglione, Steve Scanlan, Joe Schachinger, Tom Scherer, Laura Schneider, Patrick Scott, Louie Sedano, Lawrence Selik, Joe Sevely, Sherman Sham, Steven Sherman, Roger Shields, Cheryl Sholl, Abhishek Shukla, Carol Siefermann, Patricia Sielengiewicz, Kara Silva, Kevin Silva, Don Simon, Rebecca Simonian,

n Strayer, John Sulin, Phil Sullivan, Jane Sun, Kalyani Sundaram, Suhrid Swaminarayan, Dave Sweet, Richard Talmadge, Greg Tarrant, Tricia Taxter, Carrie Taylor, Joanne Taylor, Amber Taylor, Juliet Telford, Eva Thein, Helen Thomas, Susan Thomas, Laura Thorne-Trawinski, Thomas Tight, James Tilkes, Laura Tirado, Carrie Toomey, Rosanna Traina,

f Wark, Randy Warman, Antoinette Watson, Neil Waud, Carl Webb, Chris Weeks, Debbie Weeks, Irene Weidelman, Nancy Weiss, Ram Wertheim, Rebecca Werther, Linda Wessel, Ellen West, Ruth Whaley, Lori White, James Whitford Jr., Bettina Whyte, Charlie Williams, Eric Williamson, Dave Wilson, Henry Wilson, Dave Witthohn, Raymond

o, John Antonazzo, Gina Antonelli, Ana Areal, John Ariola, George Armonaitis, Craig Armstrong, Errol Arne, Linda Artis, Suresh Arumilli, Greer Avery, Dan Avitabile, Judy Baiocco, Michael Ballinger, Frances Banuelos, Ann Barbara, Mary Barbara, Lorraine Barg, Steve Barney, Jason Bathauer, Barry Baughier, Michael Baumkirchner, Jennifer Beaton,

m Boeheim, David Boisselle, Lisa Boland, Keith Borelli, Terry Bowens, Fiona Brady, David Brancale, Marty Braunstein, Melissa Brice-Johnson, Nelly Briggs, Pat Brosnan, Amy Brown, Jay Brown, Kevin Brown, Taresha Bryant, Karen Brylle, Neil Budnick, Mark Bunyea, Joe Buonadonna, Danny Burdiez, Nicole Byrd, Christine Calvao, Jason Cameron,

Choyke, David Christiansen, Deirdre Christiansen, Len Chubinsky, Lili Chueng, Lori Church, Stephanie Ciavarello, JoAnne Ciralli, Steve Citron, Robert Claiborne, Joyce Clark, Robyn Clarke, Miriam Cleary, Tom Cochran, William Cody, Robert Cole, Madelyn Coleman, Rosemaria Collorafi, Jeffrey Concepcion, Steve Cooke, Brian Cooney, Christie

Daniels, John Dare, Paul David, Gary Davis, Leslie Davis, Joshua Davis, Suzanne Davis, Michael de Nigris, Emmanuel Deblanc, Joanne DeGennaro, Sandy DeKoubia, Laura DeLena, Carole Delorme, Nils Demme, Maureen Denyssenko, Lauren Desharnais, Charles Deutsch, William DeVane, Tom Devine, Ed DeVito, Jamie Di Orio, Greg Diamond,

on, Tressa Earl, Scott Eckman, Teri Eckman, Barbara Edelmann, Gay Eichhoff, Bruce Ely, Jeff Esraelian, Lori Evangel, Felicia Fanelli, Carl Favelukes, Sharon Fera, Emily Ferguson, Gregg Ferguson, Nick Ferreri, Denise Feulner, Peter Fiala, Claus Fintzen, Sara Fischer, Anna Fischetti, Minnie Fitchben, Rosanne Fleury, Barbara Flickinger, Kimberlee

lly Goldberg, Sandy Goldstein, Amy Gonch, Roberto Gonzalez, Esther Gonzalez, Andrew Goodale, Michael Goss, Jen Gosselin, Kirby Gravance, Kelli Greene, Robert Greene, Aeneas Griffin, Jin Gu, Marsha Gumbs, Deirdre Guppy, John Hall, Traci Hall, John Hallacy, Steve Halpert, Christina Halvorsen, Doug Hamilton, Christine Hammond, Joanne

Patricia Howell, Barry Howsden, Peter Hughes, Garth Hughes, Scott Hughes, Roz Hume, Travis Humphries, Tim Hunt, David Huntley, Christina Hwang, Brian Hynes, Ahmed Ibrahim, Felicia Ivey, Rosalie Jackson, Lynn Jacobs, Lori Jalomo, Liz James, Ed Janson, Douglas Jensen, Janet Johnson, Adrian Jones, Joanne Jontz, Michael Joos, John

Michael Knopf, Megan Korson, Kathy Kruse, Nick Krzemienski, Linda Labelle, Matt Lagana, Richard Langberg, Rosalie Langschultz, Cara Sue LaPicola, Cheryl Larkin, Corinne Larson, Andy Laterza, Linda Latta, Gaddi Layden, Beatrice Le, Leon Leborgne Jr., David Lee, Jackie Lee, Jae Lee, Michael Lee, Poh Choo Lee, Andrew Leggio, Hannes

ancia, Joanne Mancuso, Paul Mansour, Huriya Manzar, Sabina Marino, Anne Marquart, Angel Martin, Anel Martinez, Yvette Martinez, Maryann Martini, Samira Mattin, Amy Mauer-Litos, Thomas Mauk, Eric McAlley, Lisa McCall, Ellen McCarthy, Shaun McClelland, David McCollum, Martin McDermott, Jean McGovern, Noeleen McGovern, Jim

Michael Morrell, John Morris, Marc Morris, Nancy Moua, Sudip Mukherjee, Imelda Muniz, Cindia Munoz, Michael Murphy, Thomas Murphy, Cathleen Murray, Gerry Murray, Stephen Murray, Theresa Murray, Michael Murtagh, Joan Musselbrook, Brenda Narayan, Salvatore Narciso, Dan Nash, Eric Neglia, Bob Nevin, Julie Ng, Deb Nickel, Ann

ercio, Giri Pawar, Alan Pearlman, Roger Pearson, Gerald Peeler, Charlie Pena, Art Perlowitz, Nik Petrika, Ian Petrillo, Gillian Pettit, Amelito Pilande, Pascale Pinte, Eric Popejoy, Andrew Porges, Scot Post, Cynthia Praschnik, Andrea Preftes, Bevin Presutti, Daniel Primavera, Armand Principato, Clifford Pritchard, Christopher Przymylski, Jim Pugh,

mans, Eric Rosensweig, Ted Ruddock, Christina Rundbaken, Stacey Russell, Steven Ruterman, Chris Ryff, Tom Saccardi, Shari Sacks, Nazima Saleem, Ridwan Sasmita, Jessica Sato, Eric Savino, Kristie Scafidi, Colleen Scaglione, Steve Scanlan, Joe Schachinger, Tom Scherer, Laura Schneider, Patrick Scott, Louie Sedano, Lawrence Selik, Joe

ula Solimine, Jeny Song, Jocelyn Songco, Mitchell Sonkin, Lori Soper, Donna Soto, Victor Soto, Nick Sourbis, Lisa Spano, Chris Staab, Matthew Starr, Robin Steward, Judy Stone, Karleen Strayer, John Sulin, Phil Sullivan, Jane Sun, Kalyani Sundaram, Suhrid Swaminarayan, Dave Sweet, Richard Talmadge, Greg Tarrant, Tricia Taxter, Carrie Taylor,

, Frank Venuti, Maria Vero-Magnan, Ines Vieira, Pamela Vieira, Ronnie Vilardo, Joan Vita, Sue Voltz, Karen Wagner, Todd Wall, Jeannine Walpole, Maggie Walsh, Rich Walz, Jing Wang, Jeff Wark, Randy Warman, Antoinette Watson, Neil Waud, Carl Webb, Chris Weeks, Debbie Weeks, Irene Weidelman, Nancy Weiss, Ram Wertheim, Rebecca

e Zureiqi, Deborah Zurkow, Pat Abt, Connie Accordino, Neil Ackerman, Joseph Adelizzi, Asli Aksuyek, Seth Albert, Angelique Allen, Mike Alter, Nancy Andreassi, Peter Andreou, Hector Angulo, John Antonazzo, Gina Antonelli, Ana Areal, John Ariola, George Armonaitis, Craig Armstrong, Errol Arne, Linda Artis, Suresh Arumilli, Greer Avery, Dan

erman, Paul Bernier, Gerry Berrigan, James Binette, Dennis Bird, Sabrina Biscardi, Cheri Bivings, Max Blackler, Bruce Blackwell, Carol Blair, Robert Blair, Rob Blake, Amy Block, Matthew Bodo, Kim Boeheim, David Boisselle, Lisa Boland, Keith Borelli, Terry Bowens, Fiona Brady, David Brancale, Marty Braunstein, Melissa Brice-Johnson, Nelly

elente, Kevin Cerutti, Chris Chafizadeh, Steve Chaloux, David Chappell, Nicole Chassey, Alex Chavarria, Helen Cheng, Charlotte Cheong, Sammy Cheung, Manuel Chevalier, Andrew Chintz, Richard Choyke, David Christiansen, Deirdre Christiansen, Len Chubinsky, Lili Chueng, Lori Church, Stephanie Ciavarello, JoAnne Ciralli, Steve Citron, Robert

m Cronin, Ian Crooke, David Crowle, Jacquelyn Cruz, Derrin Culp, Celia Culpan, Lucy Cusworth, Luigi Stefano Cuttica, Sal D'Addio, Ron Dadina, Jenn Dalton, John Danaher, Katie D'Angio, Jeffrey Daniels, John Dare, Paul David, Gary Davis, Leslie Davis, Joshua Davis, Suzanne Davis, Michael de Nigris, Emmanuel Deblanc, Joanne DeGennaro,

driana Dominguez, Michelle Donaldson, Mary Donovan, Tanya Dooley, Gloria D'Ottavio, Stephanie Dougherty, Randy Dryden, Dave Dubin, Maureen Duffy, Mohinder Dugal, Matt Dugan, Gary Dunton, Tressa Earl, Scott Eckman, Teri Eckman, Barbara Edelmann, Gay Eichhoff, Bruce Ely, Jeff Esraelian, Lori Evangel, Felicia Fanelli, Carl Favelukes,

o, Rich Garay, James Garelick, Michelle Garricks, Francois Gaudeul, Catherine Geddes, Wayne Gee, Byron Gehlhardt, Ethel Geisinger, Randall Gerardes, Stephen Gibson, Patri Ginas, Mark Gold, Kelly Goldberg, Sandy Goldstein, Amy Gonch, Roberto Gonzalez, Esther Gonzalez, Andrew Goodale, Michael Goss, Jen Gosselin, Kirby Gravance, Kelli

aynes, Bob Heller, Irene Hendricks, Jennifer Hendrix, Marc Herman, Ana Hernandez, Rick Hess, Sandra Heuer, Leslie Hickey, Willard Hill, Severin Hiller, Yujiro Hirayama, David Hoak, Ed Holden, Patricia Howell, Barry Howsden, Peter Hughes, Garth Hughes, Scott Hughes, Roz Hume, Travis Humphries, Tim Hunt, David Huntley, Christina Hwang,

an Kelly, Patrick Kelly, Patricia Kemsley, Riaz Khandwala, Gautam Khanna, Charles Khoo, Jake Kim, Danny King, Amir Kirkwood, Jason Kissane, Douglas Kitchen, JoAnn Klatskin, Jane Klemmer, Michael Knopf, Megan Korson, Kathy Kruse, Nick Krzemienski, Linda Labelle, Matt Lagana, Richard Langberg, Rosalie Langschultz, Cara Sue LaPicola,

eanor Lipsey, Sandra Lisanti, Brian Lo, Susan Lockwood, Kevin Loescher, Angelo Lovallo, John Lucas, Christa Luckenbach, Bertha Lui-McKee, Jennifer MacKay, Andrea Madden, Francesco Mancia, Joanne Mancuso, Paul Mansour, Huriya Manzar, Sabina Marino, Anne Marquart, Angel Martin, Anel Martinez, Yvette Martinez, Maryann Martini,

uroglu, Graham Metcalf, Marsha Miclat, Helen Miksits, Howard Miller, Diane Miller, Frank Minerva, Jairo Molina, Heather Molloy, Kathy Moon, James Moore, David Moriarty, Chris Moros, Michael Morrell, John Morris, Marc Morris, Nancy Moua, Sudip Mukherjee, Imelda Muniz, Cindia Munoz, Michael Murphy, Thomas Murphy, Cathleen Murray,

choa, Lauren Oliaro, Pat Olin, Stephanie Ontiveros, Kimberly Osgood, Nicole Ossun, Randy Palomba, Brett Parker, Kelli Parker, Eric Parsons, Fred Pastore, David Patashnik, Nancy Paulercio, Giri Pawar, Alan Pearlman, Roger Pearson, Gerald Peeler, Charlie Pena, Art Perlowitz, Nik Petrika, Ian Petrillo, Gillian Pettit, Amelito Pilande, Pascale Pinte,

y, David Rey, Loretta Rivera, Angel Rivera, Stephanie Rivera, Pascual Rizzo, Emmeline Rocha-Sinha, Glenn Roder, Lisa Rodia, Omar Rodriguez, Jaime Rojas Jr., Leo Roland, Doreen Romans, Eric Rosensweig, Ted Ruddock, Christina Rundbaken, Stacey Russell, Steven Ruterman, Chris Ryff, Tom Saccardi, Shari Sacks, Nazima Saleem, Ridwan

Silva, Don Simon, Rebecca Simonian, Adithi Singh, Arvind Singh, Joanne Sinopoli, Matthew Sleight, Marina Sloan, Beth Smayda, Deborah Smith, Jerry Socci, Fran Sofo, Gloria Solerti, Ursula Solimine, Jeny Song, Jocelyn Songco, Mitchell Sonkin, Lori Soper, Donna Soto, Victor Soto, Nick Sourbis, Lisa Spano, Chris Staab, Matthew Starr, Robin

Tirado, Carrie Toomey, Rosanna Traina, Mark Trench, Alan Trinh, Patrick Tucci, Anton Unger III, Bertha Valdovinos, Frederic Vallon, Tom Vandermark, Lisa Varalli, Eileen Vardilli, Janis Varney, Frank Venuti, Maria Vero-Magnan, Ines Vieira, Pamela Vieira, Ronnie Vilardo, Joan Vita, Sue Voltz, Karen Wagner, Todd Wall, Jeannine Walpole, Maggie Walsh,

nry Wilson, Dave Witthohn, Raymond Wosinski, Greg Wright, Melissa Wright, Jamie Xiong, Jim Yang, Christopher Young, Mingwei Yuan, Kim Zottola, Gail Zubradt, Mark Zucker, Leslie Zureiqi, Deborah Zurkow, Pat Abt, Connie Accordino, Neil Ackerman, Joseph Adelizzi, Asli Aksuyek, Seth Albert, Angelique Allen, Mike Alter, Nancy Andreassi,

Michael Baumkirchner, Jennifer Beaton, Natacha Beauboeuf, Brad Beck, Marguerite Beirne, Tom Bell, Lajuanda Bell, Dinah Bellis, Regina Bello, Jim Berger, Adam Bergonzi, Beth Berman, Paul Bernier, Gerry Berrigan, James Binette, Dennis Bird, Sabrina Biscardi, Cheri Bivings, Max Blackler, Bruce Blackwell, Carol Blair, Robert Blair, Rob Blake,

icole Byrd, Christine Calvao, Jason Cameron, Lisa Campbell, Lori Candarelli, Lisa Carinha, Linda Carpenter, Bill Carson, Adam Carta, Bill Carta, Mike Castracan, Judy Cavino, Jason Celente, Kevin Cerutti, Chris Chafizadeh, Steve Chaloux, David Chappell, Nicole Chassey, Alex Chavarria, Helen Cheng, Charlotte Cheong, Sammy Cheung, Manuel

epcion, Steve Cooke, Brian Cooney, Christie Corbett, Marti Correa, Cliff Corso, Irene Cortez, Jonathan Costello, Kenneth Couch, Thomas Cousins, David Craparo, Celinda Creighton, Jim Cronin, Ian Crooke, David Crowle, Jacquelyn Cruz, Derrin Culp, Celia Culpan, Lucy Cusworth, Luigi Stefano Cuttica, Sal D'Addio, Ron Dadina, Jenn Dalton, John

e, Ed DeVito, Jamie Di Orio, Greg Diamond, James DiChiaro, Wendy Dinsmore, Sharon Dittrich, Andrew Dixon, Michelle Dixon, Stephen Dixon, Christie Dixon, Everlena Dolman, Adriana Dominguez, Michelle Donaldson, Mary Donovan, Tanya Dooley, Gloria D'Ottavio, Stephanie Dougherty, Randy Dryden, Dave Dubin, Maureen Duffy, Mohinder

sanne Fleury, Barbara Flickinger, Kimberlee Florin, Mary Flynn, Jesse Fogarty, Alison Fong, Karen Foxhall, Carol Fraundorfer, Dan Frisch, Max Gabriel, Julie Galante, Theodore Galgano, Rich Garay, James Garelick, Michelle Garricks, Francois Gaudeul, Catherine Geddes, Wayne Gee, Byron Gehlhardt, Ethel Geisinger, Randall Gerardes, Stephen

, Doug Hamilton, Christine Hammond, Joanne Han, Melanie Haniph, Bret Harmon, Roger Harris, Andre Harris, Donald Harrison, Dana Hartman, Emete Hassan, Eugene Havel, Oddette Haynes, Bob Heller, Irene Hendricks, Jennifer Hendrix, Marc Herman, Ana Hernandez, Rick Hess, Sandra Heuer, Leslie Hickey, Willard Hill, Severin Hiller, Yujiro

ian Jones, Joanne Jontz, Michael Joos, John Jordan, Tom Jordan, Deirdre Jordan-Coleman, Chris Jumper, Esther Kain, Maria Kang, Una Kearns, Liz Keese-Blasius, Rosemary Kelley, Brian Kelly, Patrick Kelly, Patricia Kemsley, Riaz Khandwala, Gautam Khanna, Charles Khoo, Jake Kim, Danny King, Amir Kirkwood, Jason Kissane, Douglas Kitchen,

, Poh Choo Lee, Andrew Leggio, Hannes Leifsson, Jane Lence, Jim Lennon, Lynn Leone, Maria Levin, Larry Levitz, Shella Lieberman, John Lilly, Sonya Linder-Silidjian, Linda Lindh, Eleanor Lipsey, Sandra Lisanti, Brian Lo, Susan Lockwood, Kevin Loescher, Angelo Lovallo, John Lucas, Christa Luckenbach, Bertha Lui-McKee, Jennifer MacKay,

Jean McGovern, Noeleen McGovern, Jim McGrane, Tim McKeon, Anthony McKiernan, Tom McLoughlin, Linda McManus, Sadie McSwain, Jennifer Melle, Eugenio Mendoza, Ani Mensuroglu, Graham Metcalf, Marsha Miclat, Helen Miksits, Howard Miller, Diane Miller, Frank Minerva, Jairo Molina, Heather Molloy, Kathy Moon, James Moore,

, Bob Nevin, Julie Ng, Deb Nickel, Ann Nicoletti, Laurie Nicoletti, Stig Nielsen, Petya Nikolova, Mike Norris, Oliver North, Gerhard Oberholzer, Gonzalo Obregon, Michael O'Brien, Frances Ochoa, Lauren Oliaro, Pat Olin, Stephanie Ontiveros, Kimberly Osgood, Nicole Ossun, Randy Palomba, Brett Parker, Kelli Parker, Eric Parsons, Fred Pastore,

ard, Christopher Przymylski, Jim Pugh, Binu Punnoose, Kerrie Radoor, Beverly Raine, Ed Rajsteter, Andrea Randolph, Kathleen Reagan, Kevin Regan, Christopher Reid, Chip Reilly, Sue Reilly, David Rey, Loretta Rivera, Angel Rivera, Stephanie Rivera, Pascual Rizzo, Emmeline Rocha-Sinha, Glenn Roder, Lisa Rodia, Omar Rodriguez, Jaime Rojas

t, Louie Sedano, Lawrence Selik, Joe Sevely, Sherman Sham, Steven Sherman, Roger Shields, Cheryl Sholl, Abhishek Shukla, Carol Siefermann, Patricia Sielengiewicz, Kara Silva, Kevin Silva, Don Simon, Rebecca Simonian, Adithi Singh, Arvind Singh, Joanne Sinopoli, Matthew Sleight, Marina Sloan, Beth Smayda, Deborah Smith, Jerry Socci,

Greg Tarrant, Tricia Taxter, Carrie Taylor, Joanne Taylor, Amber Taylor, Juliet Telford, Eva Thein, Helen Thomas, Susan Thomas, Laura Thorne-Trawinski, Thomas Tight, James Tilkes, Laura Tirado, Carrie Toomey, Rosanna Traina, Mark Trench, Alan Trinh, Patrick Tucci, Anton Unger III, Bertha Valdovinos, Frederic Vallon, Tom Vandermark, Lisa Varalli,

ancy Weiss, Ram Wertheim, Rebecca Werther, Linda Wessel, Ellen West, Ruth Whaley, Lori White, James Whitford Jr., Bettina Whyte, Charlie Williams, Eric Williamson, Dave Wilson, Henry Wilson, Dave Witthohn, Raymond Wosinski, Greg Wright, Melissa Wright, Jamie Xiong, Jim Yang, Christopher Young, Mingwei Yuan, Kim Zottola, Gail

is, Suresh Arumilli, Greer Avery, Dan Avitabile, Judy Baiocco, Michael Ballinger, Frances Banuelos, Ann Barbara, Mary Barbara, Lorraine Barg, Steve Barney, Jason Bathauer, Barry Baughier, Michael Baumkirchner, Jennifer Beaton, Natacha Beauboeuf, Brad Beck, Marguerite Beirne, Tom Bell, Lajuanda Bell, Dinah Bellis, Regina Bello, Jim Berger,

n, Melissa Brice-Johnson, Nelly Briggs, Pat Brosnan, Amy Brown, Jay Brown, Kevin Brown, Taresha Bryant, Karen Brylle, Neil Budnick, Mark Bunyea, Joe Buonadonna, Danny Burdiez, Nicole Byrd, Christine Calvao, Jason Cameron, Lisa Campbell, Lori Candarelli, Lisa Carinha, Linda Carpenter, Bill Carson, Adam Carta, Bill Carta, Mike Castracan,

oAnne Ciralli, Steve Citron, Robert Claiborne, Joyce Clark, Robyn Clarke, Miriam Cleary, Tom Cochran, William Cody, Robert Cole, Madelyn Coleman, Rosemaria Collorafi, Jeffrey Concepcion, Steve Cooke, Brian Cooney, Christie Corbett, Marti Correa, Cliff Corso, Irene Cortez, Jonathan Costello, Kenneth Couch, Thomas Cousins, David Craparo,

l Deblanc, Joanne DeGennaro, Sandy DeKoubia, Laura DeLena, Carole Delorme, Nils Demme, Maureen Denyssenko, Lauren Desharnais, Charles Deutsch, William DeVane, Tom Devine, Ed DeVito, Jamie Di Orio, Greg Diamond, James DiChiaro, Wendy Dinsmore, Sharon Dittrich, Andrew Dixon, Michelle Dixon, Stephen Dixon, Christie Dixon,

elicia Fanelli, Carl Favelukes, Sharon Fera, Emily Ferguson, Gregg Ferguson, Nick Ferreri, Denise Feulner, Peter Fiala, Claus Fintzen, Sara Fischer, Anna Fischetti, Minnie Fitchben, Rosanne Fleury, Barbara Flickinger, Kimberlee Florin, Mary Flynn, Jesse Fogarty, Alison Fong, Karen Foxhall, Carol Fraundorfer, Dan Frisch, Max Gabriel, Julie Galante,

sselin, Kirby Gravance, Kelli Greene, Robert Greene, Aeneas Griffin, Jin Gu, Marsha Gumbs, Deirdre Guppy, John Hall, Traci Hall, John Hallacy, Steve Halpert, Christina Halvorsen, Doug Hamilton, Christine Hammond, Joanne Han, Melanie Haniph, Bret Harmon, Roger Harris, Andre Harris, Donald Harrison, Dana Hartman, Emete Hassan, Eugene

David Huntley, Christina Hwang, Brian Hynes, Ahmed Ibrahim, Felicia Ivey, Rosalie Jackson, Lynn Jacobs, Lori Jalomo, Liz James, Ed Janson, Douglas Jensen, Janet Johnson, Adrian Jones, Joanne Jontz, Michael Joos, John Jordan, Tom Jordan, Deirdre Jordan-Coleman, Chris Jumper, Esther Kain, Maria Kang, Una Kearns, Liz Keese-Blasius,

ngschultz, Cara Sue LaPicola, Cheryl Larkin, Corinne Larson, Andy Laterza, Linda Latta, Gaddi Layden, Beatrice Le, Leon Leborgne Jr., David Lee, Jackie Lee, Jae Lee, Michael Lee, Poh Choo Lee, Andrew Leggio, Hannes Leifsson, Jane Lence, Jim Lennon, Lynn Leone, Maria Levin, Larry Levitz, Shella Lieberman, John Lilly, Sonya Linder-Silidjian,

nez, Maryann Martini, Samira Mattin, Amy Mauer-Litos, Thomas Mauk, Eric McAlley, Lisa McCall, Ellen McCarthy, Shaun McClelland, David McCollum, Martin McDermott, Jean McGovern, Noeleen McGovern, Jim McGrane, Tim McKeon, Anthony McKiernan, Tom McLoughlin, Linda McManus, Sadie McSwain, Jennifer Melle, Eugenio Mendoza,

phy, Cathleen Murray, Gerry Murray, Stephen Murray, Theresa Murray, Michael Murtagh, Joan Musselbrook, Brenda Narayan, Salvatore Narciso, Dan Nash, Eric Neglia, Bob Nevin, Julie Ng, Deb Nickel, Ann Nicoletti, Laurie Nicoletti, Stig Nielsen, Petya Nikolova, Mike Norris, Oliver North, Gerhard Oberholzer, Gonzalo Obregon, Michael O'Brien,

lande, Pascale Pinte, Eric Popejoy, Andrew Porges, Scot Post, Cynthia Praschnik, Andrea Preftes, Bevin Presutti, Daniel Primavera, Armand Principato, Clifford Pritchard, Christopher Przymylski, Jim Pugh, Binu Punnoose, Kerrie Radoor, Beverly Raine, Ed Rajsteter, Andrea Randolph, Kathleen Reagan, Kevin Regan, Christopher Reid, Chip Reilly,

a Saleem, Ridwan Sasmita, Jessica Sato, Eric Savino, Kristie Scafidi, Colleen Scaglione, Steve Scanlan, Joe Schachinger, Tom Scherer, Laura Schneider, Patrick Scott, Louie Sedano, Lawrence Selik, Joe Sevely, Sherman Sham, Steven Sherman, Roger Shields, Cheryl Sholl, Abhishek Shukla, Carol Siefermann, Patricia Sielengiewicz, Kara Silva,

ew Starr, Robin Steward, Judy Stone, Karleen Strayer, John Sulin, Phil Sullivan, Jane Sun, Kalyani Sundaram, Suhrid Swaminarayan, Dave Sweet, Richard Talmadge, Greg Tarrant, Tricia Taxter, Carrie Taylor, Joanne Taylor, Amber Taylor, Juliet Telford, Eva Thein, Helen Thomas, Susan Thomas, Laura Thorne-Trawinski, Thomas Tight, James Tilkes,

pole, Maggie Walsh, Rich Walz, Jing Wang, Jeff Wark, Randy Warman, Antoinette Watson, Neil Waud, Carl Webb, Chris Weeks, Debbie Weeks, Irene Weidelman, Nancy Weiss, Ram Wertheim, Rebecca Werther, Linda Wessel, Ellen West, Ruth Whaley, Lori White, James Whitford Jr., Bettina Whyte, Charlie Williams, Eric Williamson, Dave

er, Nancy Andreassi, Peter Andreou, Hector Angulo, John Antonazzo, Gina Antonelli, Ana Areal, John Ariola, George Armonaitis, Craig Armstrong, Errol Arne, Linda Artis, Suresh Arumilli, Greer Avery, Dan Avitabile, Judy Baiocco, Michael Ballinger, Frances Banuelos, Ann Barbara, Mary Barbara, Lorraine Barg, Steve Barney, Jason Bathauer, Barry

bert Blair, Rob Blake, Amy Block, Matthew Bodo, Kim Boeheim, David Boisselle, Lisa Boland, Keith Borelli, Terry Bowens, Fiona Brady, David Brancale, Marty Braunstein, Melissa Brice-Johnson, Nelly Briggs, Pat Brosnan, Amy Brown, Jay Brown, Kevin Brown, Taresha Bryant, Karen Brylle, Neil Budnick, Mark Bunyea, Joe Buonadonna, Danny

y Cheung, Manuel Chevalier, Andrew Chintz, Richard Choyke, David Christiansen, Deirdre Christiansen, Len Chubinsky, Lili Chueng, Lori Church, Stephanie Ciavarello, JoAnne Ciralli, Steve Citron, Robert Claiborne, Joyce Clark, Robyn Clarke, Miriam Cleary, Tom Cochran, William Cody, Robert Cole, Madelyn Coleman, Rosemaria Collorafi, Jeffrey

enn Dalton, John Danaher, Katie D'Angio, Jeffrey Daniels, John Dare, Paul David, Gary Davis, Leslie Davis, Joshua Davis, Suzanne Davis, Michael de Nigris, Emmanuel Deblanc, Joanne DeGennaro, Sandy DeKoubia, Laura DeLena, Carole Delorme, Nils Demme, Maureen Denyssenko, Lauren Desharnais, Charles Deutsch, William DeVane, Tom

Duffy, Mohinder Dugal, Matt Dugan, Gary Dunton, Tressa Earl, Scott Eckman, Teri Eckman, Barbara Edelmann, Gay Eichhoff, Bruce Ely, Jeff Esraelian, Lori Evangel, Felicia Fanelli, Carl Favelukes, Sharon Fera, Emily Ferguson, Gregg Ferguson, Nick Ferreri, Denise Feulner, Peter Fiala, Claus Fintzen, Sara Fischer, Anna Fischetti, Minnie Fitchben,

s, Stephen Gibson, Patri Ginas, Mark Gold, Kelly Goldberg, Sandy Goldstein, Amy Gonch, Roberto Gonzalez, Esther Gonzalez, Andrew Goodale, Michael Goss, Jen Gosselin, Kirby Gravance, Kelli Greene, Robert Greene, Aeneas Griffin, Jin Gu, Marsha Gumbs, Deirdre Guppy, John Hall, Traci Hall, John Hallacy, Steve Halpert, Christina Halvorsen,

er, Yujiro Hirayama, David Hoak, Ed Holden, Patricia Howell, Barry Howsden, Peter Hughes, Garth Hughes, Scott Hughes, Roz Hume, Travis Humphries, Tim Hunt, David Huntley, Christina Hwang, Brian Hynes, Ahmed Ibrahim, Felicia Ivey, Rosalie Jackson, Lynn Jacobs, Lori Jalomo, Liz James, Ed Janson, Douglas Jensen, Janet Johnson, Adrian

Kitchen, JoAnn Klatskin, Jane Klemmer, Michael Knopf, Megan Korson, Kathy Kruse, Nick Krzemienski, Linda Labelle, Matt Lagana, Richard Langberg, Rosalie Langschultz, Cara Sue LaPicola, Cheryl Larkin, Corinne Larson, Andy Laterza, Linda Latta, Gaddi Layden, Beatrice Le, Leon Leborgne Jr., David Lee, Jackie Lee, Jae Lee, Michael Lee, Poh

cKay, Andrea Madden, Francesco Mancia, Joanne Mancuso, Paul Mansour, Huriya Manzar, Sabina Marino, Anne Marquart, Angel Martin, Anel Martinez, Yvette Martinez, Maryann Martini, Samira Mattin, Amy Mauer-Litos, Thomas Mauk, Eric McAlley, Lisa McCall, Ellen McCarthy, Shaun McClelland, David McCollum, Martin McDermott, Jean

oore, David Moriarty, Chris Moros, Michael Morrell, John Morris, Marc Morris, Nancy Moua, Sudip Mukherjee, Imelda Muniz, Cindia Munoz, Michael Murphy, Thomas Murphy, Cathleen Murray, Gerry Murray, Stephen Murray, Theresa Murray, Michael Murtagh, Joan Musselbrook, Brenda Narayan, Salvatore Narciso, Dan Nash, Eric Neglia, Bob

tore, David Patashnik, Nancy Paulercio, Giri Pawar, Alan Pearlman, Roger Pearson, Gerald Peeler, Charlie Pena, Art Perlowitz, Nik Petrika, Ian Petrillo, Gillian Pettit, Amelito Pilande, Pascale Pinte, Eric Popejoy, Andrew Porges, Scot Post, Cynthia Praschnik, Andrea Preftes, Bevin Presutti, Daniel Primavera, Armand Principato, Clifford Pritchard,

>>>

MBIA Annual Report 2004

87091_CoverforPDFonly.qxp 4/1/05 11:34 AM Page 1

Contents

1 Financial Highlights2 Letter to Shareholders14 Board of Directors16 Senior Officers17 Financial Review77 Locations78 Shareholder Information

MBIA is a world leader in credit enhancement services and a global provider of fixed-income assetmanagement services, listed on the New York Stock Exchange under the symbol MBI. The Company has approximately 600 employees located in 12 offices around the world.

MBIA’s financial strength, underwriting performance and record of service are reflected in the Triple-A rating of MBIA's claims-paying resources by Moody's Investors Service, Standard & Poor'sRatings Services, Fitch Ratings, and Rating and Investment Information, Inc. For more information, visit our Web site: www.mbia.com.

321 Henderson, Aareal Bank AG, Abington SD, ACA ABS 2003-2 Class A1SD, ACACIA CDO 5, LTD, ACACIA CDO VI, Acton Twn, Adams Co SD, Adams State Col, Addison Twn, Adel-DeSoto-Minburn Comm SD, AFC Trust Series 2000-2-3-4, Afton Central SD, Aiken Co, Airlines Repackaged Trust Secuities Ltd., AK HFC Collaterlized Bonds

Hsg Dev, AK Muni Bond Bank Auth, AK Univ, Akbank Remittance Trust Securitization, Akbank T.A.S. 2001-A Receivables Trust, AL Pub Schl & Col Auth, AL Univ Brd of Trustees, Alabaster City Sewer Rev, Alaska Student Loan Corp Moral Oblig, Albany Co, Albany Unified SD, Albuquerque City Airport, Alden Central SD, Allegheny Co Port

Auth Spc Dist LSE, Allegheny Valley SD, Allen Ind SD, Allen Park Pub Schls, Almont Pub Schls, Alvin Ind SD, Ambridge Area SD, AmerenUE, American Home Mtg Investment Trust, American Museum Natural History NY City Trust, AmeriCredit Automobile Receivables Trust 2004-B-M, AmeriCredit MTN Receivables Trust IV, Ames Comm

SD, Amherst Twn, Amortizing Residential Collateral Trust 2004-1 Class A2, Anaheim Pub Financing Auth Elec, Anchor Bay SD, Anchorage Muni, Anchorage Muni WasteWtr, Anchorage Muni Wtr, Andover City, Angelina Co Jr Col Dist, Ann Arbor Pub Schls, Annandale City, Antelope Valley Union High SD, Antietam SD, Apache, Aphrodite,

Appleton City Sewer, AR Dev Fin Auth Sewer, Arapahoe Co E-470 Toll Road, Archbold Area Lcl SD, Ardsley Union Free SD, ARG Funding Corp, Arizona Brd of Regents Arizona State Univ, Arlington City, Arlington Heights Village, Ashland City W&S Rev, Ashley Comm Schls, Atlanta City, Atlantic Beach City Utility Sys W&S, Atlantic Co,

Auburn City, Audrain Co Pub Facilities Corp LSE, Audubon Boro BOE, Aurora City Wtr, Austin Area SD, Austin City Airport, Austin City, Austin Comm Col Dist, Autopista Central S.A., Autopista del Maipo Sociedad Concesionaria S.A., Avon Twn, Ayer Twn, AZ State LSE, Azle City W&S, Bad Axe Pub Schls, Baltimore Co LSE, Bancomer

Receivables Master Trust, Bangor SD, Bangor Twnship SD, Bank of America Mtg PT Cert. 2004-4, Bank of America Mtg Securites 2004-7, Baptist Health Sys of Montgomery, Barnstable Twn, Barrington Boro BOE, Barrington Comm Unit SD #220, Barstow Unified SD, Barton Co Unified SD #428, Batavia City SD, Bath Charter Twnship,

Bath City, Bear Stearns ABS 2004-HE6, Beaufort Co SD, Beaufort Co, Beauregard Parishwide SD, Becker Ind SD #726, Bedford ASD, Bedford City, Bedford Heights City, Beekmantown Central SD, Bel Aire City, Bell City, Bellefontaine City, Bellefonte ASD, Bellevue City, Bellevue City W&S, Bellingham City, Bellingham City W&S, Berkeley

Co LSE, Berkeley Unified SD, Bernalillo Co Sales Tax, Bessemer City, Bethel Twn, Bethlehem City, Bethpage UFSD, Bettendorf City, Bexar Co, BHW Bausparkasse AG, Bicentennial Union High SD #76 96, Birmingham City Wtr Works & Sewer Brd, Black Hills State Univ Hsg & Aux Rev, Bladen Co, Bloomfield Charter Twnship,

Bloomington City, Blount Co Wtr, Bogota Boro, Bonita Unified SD, Boone Twp M.S.D. Bldg Corp, Boston City, Bowling Green City, Bowling Green State Univ, Boyd Co, Boyne Falls Pub Schls, Boynton Beach City Utility Sales Tax, Bradesco, Bradford Co, Brazil City Sewer, Brazoria Co Muni Utility Dist #6, Brazos River Auth Temple-Belton

Reg Sewerage, Bremer Co, Brentwood Union Elem SD, Briarcliff Manor Village, Brick Twnship, Bridgeport City, BridgeWtr-Raynham Reg SD, Bristol City, Bristol Co Wtr Auth, Bristol Twnship, Bristol Warren Reg SD, Broadlands Metro Dist #2, Brockway Area SD, Brook Park City, Brookfield CSD, Brookhaven Twn, Brooklyn Park City,

Broward Co LSE, Brown Co, Brown Univ, Brush SD #RE-2J, Buckeye Union High SD #201, Buellton Union SD, Buffalo City, Buffalo City Sales Tax, Bullitt Co SD Fin Corp LSE, Burleson City, Burlingame Elem SD, Burlington Area SD, Burlington City, Burlington Co, Burlington-Edison SD #100, Burrell SD, Business Loan Express Convention

loan 2004-A, Butler Boro BOE, Butler Univ, Byron City, CA Dept of Wtr Ress Power Supply Rev, CA Dept of Trans Fed Highway Grant Ant, CA Dept of Wtr Ress Central Valley, CA Econ Recovery Sales Tax, CA, CA Hsg Fin Ag Single Family Mtg, CA State Pub Works Brd LSE, CA Univ Regents, CA Univ Regents LSE, Cabrillo Comm Col

Dist, Cachuma Operation and Maintenance Brd Wtr, Caddo Parish Parishwide SD, Calaveras Co Wtr Dist W&S, Calcasieu Parish SD #33, Caledonia Charter Twnship, Caledonia Twn, Calexico Unified SD, Callaway City WasteWtr Sys, Cameron Co, Canal Winchester Village, Canaseraga CSD, Canby City Wtr, Canton Twn, Capital One Auto

Fin Trust 2004-B, Capitol Area Dev Auth Tax Allocation, Carbon Co, Carbondale Comm High SD #165, CareGroup, Inc., Carle Place Union Free SD, Carlsbad Muni SD#1, Carmel City LSE Rev, Carmel Clay Parks Bldg Corp LSE Rev, Carmel CSD, Carmel Schl Bldg Corp LSE, Carrollton-Farmers Ind SD, Cash Special Utility Dist Wtr, Castle

2003-2 Trust, Catawba Co COP, Catholic Healthcare West, Cattaraugus Co, Cazenovia CSD, C-BASS CBO X, C-BASS CDO XI, C-BASS XII, Cecil Twnship, Cedar Grove-Belgium Area SD, Cedar Hill City, Cedar Hill City W&S, Cedar Hill Ind SD, Celina City SD, Cendant Timeshare 2004-1 Receivables Funding Co., Cntr Line Pub Schls, Cntr

Twnship, Cntrville City, Centex Home Equity Certificates 2004-2, CENTEX HOME EQUITY TRUST 2004-D, AV-5, Centinela Valley Union High SD, Centra Health Sys, Central Arkansas Wtr, Central Columbia SD, Central Islip Union Free SD, Central Square Central SD, Cerritos Comm Col Dist, Chabot-Las Positas Comm Col Dist,

Chambersburg Boro, Charles Stewart Mott Comm Col, Charleston Co, Charleston Co LSE, Charlestown Twn, Charlotte City Airport, Charlotte City StormWtr Rev, Chaska City, Chaska Ind SD #112, Chautauqua Co, Chelmsford Twn, Chelsea City, Cheltenham Twnship, Cheltenham Twnship SD, Chemung Co, Chenango Forks Central SD,

Cherry Hill Twnship, Cherry Valley Village, Chester Rgl SD#4, Chester Wtr Auth, Chicago City Brd of Ed, Chicago City, Chicago City WasteWtr Transmission Sewer, Chicago City Wtr, Chicago O'Hare Int'l General Airport, Childrens Hosp Orange Co, Chino Basin Desalter Auth Wtr, Chiswell Fin Ltd, Chula Vista City LSE, Chula Vista Elem

SD, Chula Vista Elem SD LSE, Citicorp Mtg Loan Trust 2004-OPT1, Citicorp Mtg Securities Inc 2004-1 Class IA-3, Citicorp Mtg Secs Inc 2004-2 Class A-6, Citizens Property Insurance Corp, Citrus Comm Col Dist, Claremont Unified SD, Clark Co, Clark Co Las Vegas-McCarran Int'l Airport, Clark Co SD, Clarkston Comm Schls, Clarkstown

Twn, Clay Co Schl Brd LSE, Clever Reorganized SD # R-V, Clifton Brd of Ed, Clifton City, Clinton Prairie Schl Corp, Closter Boro BOE, CO Dept of Trans LSE, Cobb Co Dev Auth Kennesaw St. Univ Found Stu Hsg, Cobb Co Dev Auth Kennesaw St. Univ Found LSE, Cobb Co Dev Auth Kennesaw St. Univ Found Prkg Rev, Cocke Co, Cohoes

City SD, Coleman Comm Schls, Colgate Univ, Col Comm SD, Col Elem SD, Col of the Mainland, Col Park City, Col Station City, Colona City, Colorado Mountain Jr Col Dist, Colorado River Muni Wtr Dist, Colorado Springs City Cmbnd Utility, Columbia City Wtr & Elec Cmbnd Utility, Columbia-Brazoria Ind SD, Columbus City, Columbus SD,

Compton Comm Col Dist, Compton Unified SD, Concord City, Concord City Joint Powers Fin Auth WasteWtr, Concord Comm Schl Bldg, Conewago Valley SD, Conneaut SD, Consumers Energy Company, Contra Costa Comm Col Dist, Cook Co, Coopersville Area Pub Schls, Copper Mountain Cnsldtd Metro Dist Wtr, Coronado Fin Auth

Sewer, Cottonwood Union SD, Council Bluffs City, Countrywide ABS 2004-10, COUNTRYWIDE ABS 2004-12, Countrywide Alternate Loan Trust 2004-J4 Class A5 & A6, Countrywide Asset backed Cert Series 2004-5, Countrywide Asset Backed Cert 2004-8, Countrywide Asset Backed Sec 2004-7 Class 2-AV-3, Countrywide Home Loan

Mtg Pass-Thru Trust 2004-10, Countrywide Home Loans, Inc., Countrywide Mtg Pass Thru Trust 2004-9, Class A5, Covington City, Covington Comm Schl Corp, Crawfordsville Pub Library Bld & Preservation Corp Lse, Crest Exeter Street Solar 2004-1, Crest Hill W&S, Crestwood SD, Croton/Harmon UFSD, Crow Wing Co, CT Dev Auth

LSE Rev, CT, CT Muni Elec Energy Cooperative, CT Reg SD #13 (Durham & Middlefield), Cumberland Co, Cumberland Twn, Cutler-Orosi Joint Unified SD, Cuyahoga Falls City LTD, Dallas Cntr-Grimes Comm SD, Dallas City, Dallas-Fort Worth Int'l Airport, Daly City Wtr, Damon IG CDO, Danbury City, Daniel Boone Area SD, Dansville Central

SD, Dauphin Co, Davenport City, Dayton SD #8, De Soto Unified SD #232, Dearborn SD, Decatur City, DeForest Area SD, Dekalb Co W&S, Delaware City SD, Delaware Co Rgl Wtr Quality Control Auth Swr Rev, Delaware Co, Delaware River Joint Toll Bridge Commission, Delray Beach City, Denton City Utility Sys Cmbnd Utility, Denver

City and Co, Depew Village, Derry Twnship, Des Moines Area Comm Col, Des Moines City Wtr, Des Moines Metro WasteWtr Reclamation Auth Sewer, Des Plaines City, Deschutes Co, Desert Comm Col Dist, DeSoto City, Desoto Co SD LSE, Detroit City, Detroit City Wtr Sys, Detroit Edison Company, Detroit Lakes Ind SD #22, DFS

Receivables Funding Corp, Diamond Lake SD#76, Dinwiddie Co LSE Rev, Dodge City, Dolton Village, Douglas Co, Douglas Co Pub Utility Dist #1 Distribution Sys, Douglas Co Sales and Use Tax, Downey Unified SD, Drive Auto Receivables Trust 2004-1, Drive Time Auto Owner Trust 2004-B, Dryden Comm Schls, Dudley Twn, Dunellen

Boro Brd of Ed, Dunlap Comm Unit SD#323, Dunn City, Dutchess Co, Dutchess Co Wtr & WasteWtr Auth, East Cherry Creek Vly Wtr & San Dist Wtr, East Grand Rapids City, East Greenbush Central SD, East Greenwich Twn, East Greenwich Twnship SD, East Irondequoit Central SD, East Islip Union Free SD, East Penn SD, East Syracuse-

Minoa Central SD, East Wenatchee Wtr Dist, East Windsor, Eastern Iowa Comm Col Dist, Eastern Kentucky Univ, Eastern Lebanon Co SD, Eastern Snyder Co Reg Auth Sewer Rev, Eau Claire Area SD, Edgemont Union Free SD, Edina Ind SD #273, El Paso Co SD #22, Elgin City, Elizabeth City, Elkhart Co, Elmhurst City, Emporia City,

Energy Northwest Pub Power, Englewood City, Englewood City Wtr, Enterprise SD, Erie Co, Erie Twn Wtr Rev, Escambia Co Sch Bd Lse, Essex Co, Essex Co, Euclid City, Euclid City SD, Euless City W&S, Evanston/Skokie Comm Cnsldtd SD#65, Evansville City Redeveloment Dist, Evansville City Redev Auth LSE, Evergreen SD #114,

Evesham Muni Util Auth W&S, Fairfax City, Fairfax Co LSE, Fairfield-Suisun Unified SD, Fairport CSD, Fairview Health Servs, Fairview SD #72, Falls Twnship Auth, Fargo City, Fargo Pub SD #1, Farmers Branch City, Fayette Co SD Fin Corp Lse, Fenton City COP LSE, FHB Land Credit and Mtg Bank Ltd., Fife City W&S, Findlay City, First

Horizan ABS Closed End 2nd Lien Trust 2004-4, First Horizon ABS Trust 2004-HE2, First Horizon Mtg Pass Thru Trust 2004-3, 1-A3, First Horizon Series 2004-04, Fishhawk Comm Dev Dist, Fitchburg City, FL Brd of Ed Capital Outlay, FL Dept Natural Ress Preserv 2000 Sales Tax, FL Hsg Fin Ag, Flemington Boro, Florence City, Florence,

Florence Twnship Brd of Ed, Florence Twnship, Florida Int'l Univ, Florida Muni Loan Council Local Sales Tax, Folsom Boro BOE, Folsom Cordova Unified SD Fac Improv Dist #1, Fonda/Fultonville CSD, Fontana Unified SD, Foothills Park & Rec Dist Bldg Auth COP, Forest Hills Pub Sch, Fort Bend Co Wtr Control & Improv Dist #2, Fort Lee

Boro, Fort Scott City, Fort Smith W&S, Fort Zumwalt SD, Fortress CBO Investment I, Fortress Credit Opportunities I &II LP, Foxborough Twn, Fraikin Assets SAS, Framingham Twn, Francis Marion Univ Aux Ent, Franklin Auto Trust 2004-1, Franklin Auto Trust 2004-2, Franklin City W&S, Franklin Co SD Fin Corp Lse, Franklin Lakes Boro

BOE, Franklin Reg SD, Franklin Twn, Frazee-Vergas Ind SD #23, Freedom Forum, Freehold Twp, Fremont Co SD #RE-1, Fresno Unified SD, Frio Co Pub Facility Corp, Frisco City, Fulham Road Fin Ltd, Gallatin City, Gallup City Joint Utility, Garanti Bank, Garden City, Gastonia City, Gateway Twnship BOE, Gaylord Comm Sch, General Health

FHA, Genesee Co, Genesee Co Sewer Sys, Genesee SD, Genesee Wtr & San Dist, Geneseo City, Geneva City, Georgia Tech Fac Inc Fulton Co Dev Auth, Gilroy Unified SD COP LSE, Gladwin Comm Schls, Glassboro Boro Brd of Ed, Glendale City, Gloucester City, Gloucester Co, Gloucester Twnship SD, GMAC 2004-J4, GMAC Mtg Corp,

GMAC MTG LOAN TRUST 2004-J1, A-4-A13, GMACM Home Equity Loan Trust 2000-HE4, GMACM Home Equity Notes 2004 Variable Fund Trust, Gonzaga Univ, Gorham Twn, Gorham/Middlesex CSD, Goshen Muni Sewage Works, Goshen Twnship, Grafton Twn, Graham Co, Grand Chute Twn, Grand Fire Protection Dist #1, Grand Island

CSD, Grand Prairie City, Grand Prairie City W&S, Grand Rapids Pub Schls, Grand Traverse Co, Grant Comm High SD#124, Grant Co Fire Protection Dist #3, Grant PSD, Granville Exempted Village SD, Grayson Co Jr Col Dist Cmbnd Fee, Greater Cleveland Reg Trans Auth, Greater Latrobe SD, Greater Orlando Aviation Auth Airport, Greater

Rochester Airport, Greece CSD, Green City, Green Oak Twnship, Greencastle Boro, Greenville City, GS Mtg Securities II 1999-C1 A-2, G-Star 2004-4 Ltd, Guadalupe-Blanco River Auth Lockhart City Comb Utl, Guadalupe-Blanco River Auth Wtr, Guilford Twn, Gwinnett Co SD LSE Rev, Haldane Central SD, Half Hollow Hills CSD, Halifax

ASD, Hamilton Co Sewer Sys, Hammond Multi Schl Bldg Corp, Hampton City, Hampton Roads Reg Jail Auth, Hancock Pub Sch, Hanford Joint Union High SD, Hanover Comm Schl Bldg Corp, Hanover Twn, Hardin Co Sch Dist Fin Corp LSE, Hardin Co Wtr Dist #2, Harpeth Valley Util Dist W&S, Harris Co Fresh Wtr Supply Dist #61, Harris

87091_CoverforPDFonly.qxp 4/1/05 11:34 AM Page 2

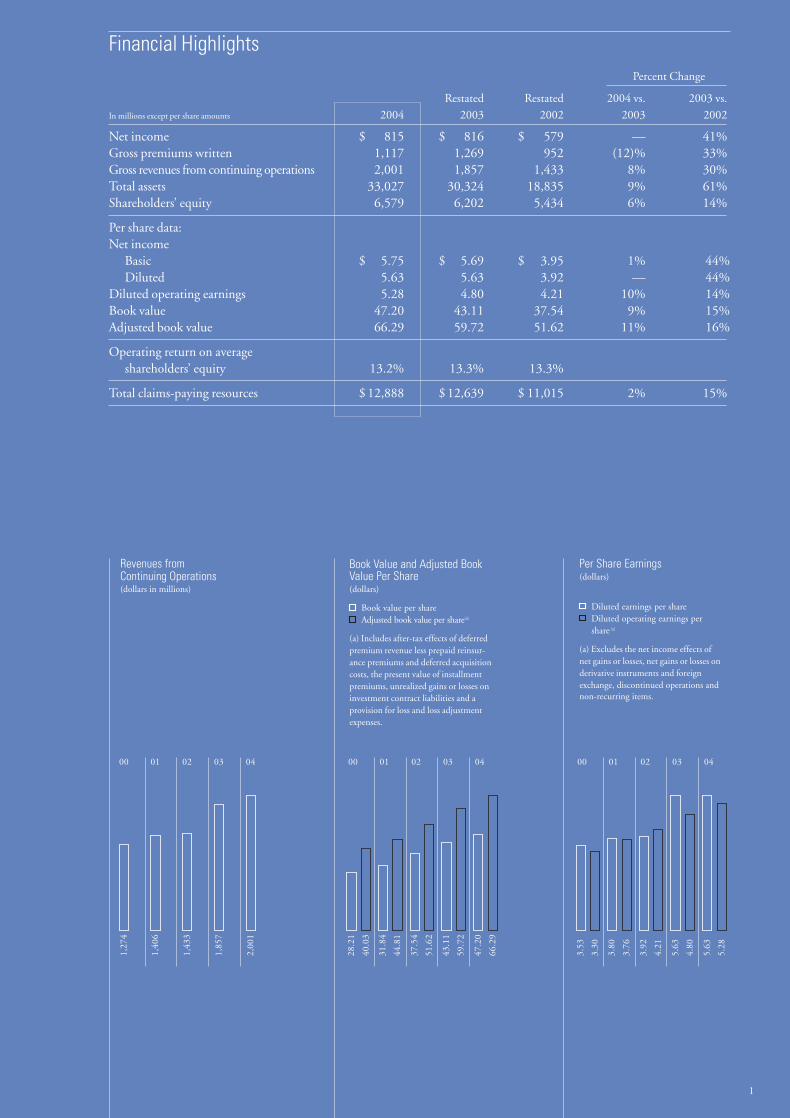

Financial HighlightsPercent Change

Restated Restated 2004 vs. 2003 vs.In millions except per share amounts 2004 2003 2002 2003 2002

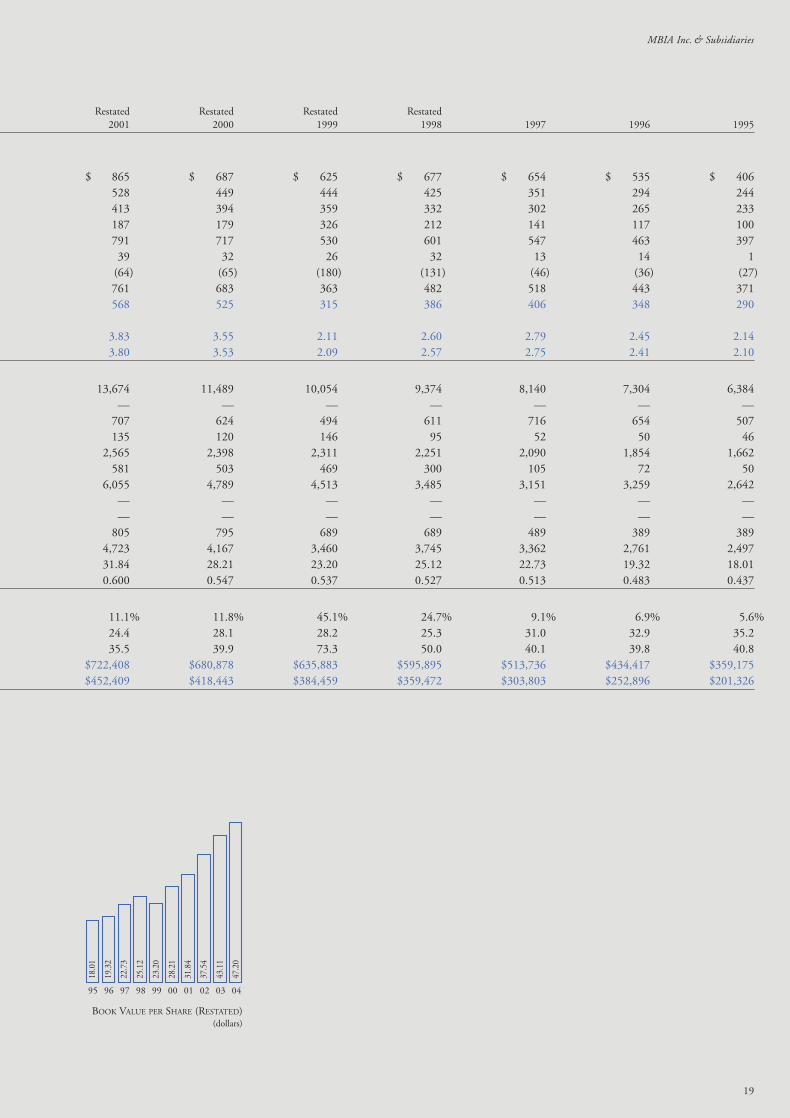

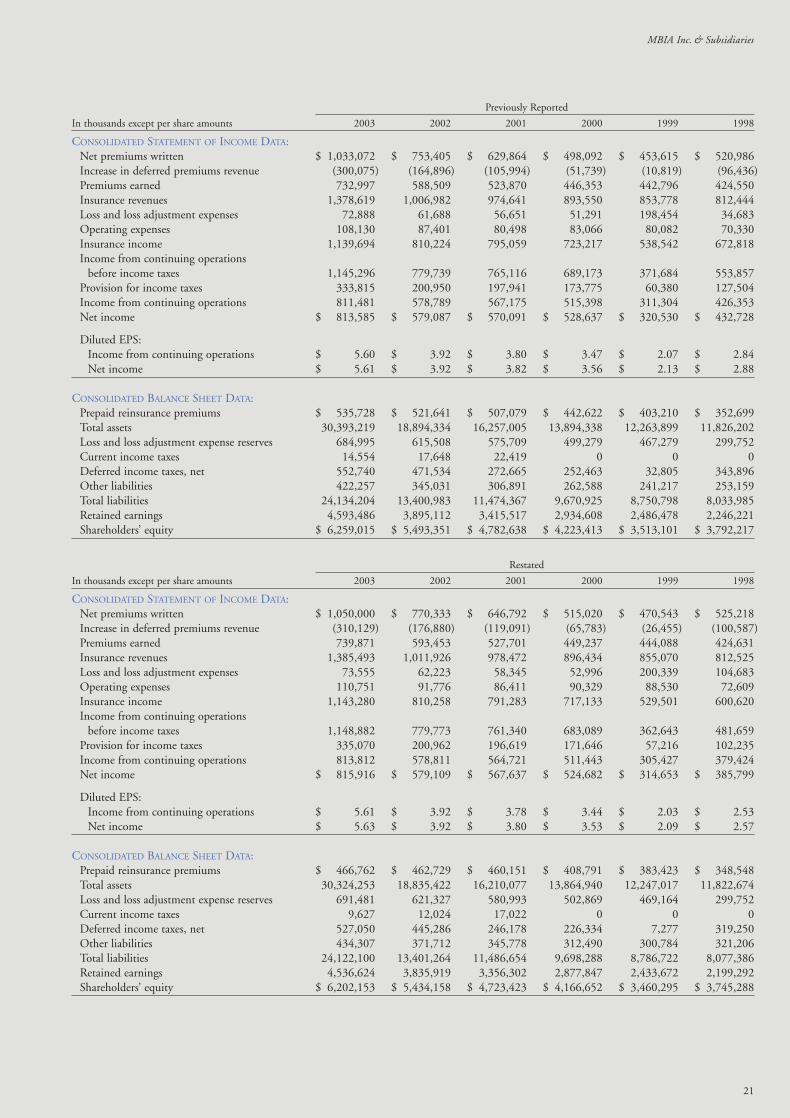

Net income $ 815 $ 816 $ 579 — 41%Gross premiums written 1,117 1,269 952 (12)% 33%Gross revenues from continuing operations 2,001 1,857 1,433 8% 30%Total assets 33,027 30,324 18,835 9% 61%Shareholders’ equity 6,579 6,202 5,434 6% 14%

Per share data: Net income

Basic $ 5.75 $ 5.69 $ 3.95 1% 44%Diluted 5.63 5.63 3.92 — 44%

Diluted operating earnings 5.28 4.80 4.21 10% 14%Book value 47.20 43.11 37.54 9% 15%Adjusted book value 66.29 59.72 51.62 11% 16%

Operating return on average shareholders’ equity 13.2% 13.3% 13.3%

Total claims-paying resources $ 12,888 $ 12,639 $ 11,015 2% 15%

66.2

9

47.2

0

59.7

2

43.1

1

51.6

2

37.5

4

44.8

1

31.8

4

40.0

3

28.2

1

2,00

1

1,85

7

1,43

3

1,40

6

1,27

4

Revenues from Continuing Operations(dollars in millions)

Book Value and Adjusted BookValue Per Share(dollars)

Book value per shareAdjusted book value per share(a)

(a) Includes after-tax effects of deferredpremium revenue less prepaid reinsur-ance premiums and deferred acquisitioncosts, the present value of installmentpremiums, unrealized gains or losses oninvestment contract liabilities and a provision for loss and loss adjustmentexpenses.

Per Share Earnings(dollars)

Diluted earnings per shareDiluted operating earnings pershare (a)

(a) Excludes the net income effects ofnet gains or losses, net gains or losses onderivative instruments and foreignexchange, discontinued operations and non-recurring items.

5.28

5.63

4.80

5.63

4.21

3.92

3.76

3.80

3.30

3.53

00 01 02 03 0400 01 02 03 04 00 01 02 03 04

1

87091_MBIA_Editorial.qxp 3/28/05 6:09 PM Page 1

Letter to Shareholders

2

To Our Owners,

Last year at this time we reported record results across most of our financial measures due inpart to a very favorable operating and economic environment. This year, we are reporting good,but not exceptional, financial results. While 2004 presented a distinctly more challengingmarketplace for our industry, every year does not need to be a record-breaker for us to turn in asolid performance, as we did again last year. The race we are running is a marathon and not asprint. We are buyers and holders of long-term credit risk, and our results must be judged overtime. As I will outline in the comments that follow, we continued to build MBIA franchisestrength in 2004 despite difficult market conditions and increased regulatory scrutiny, and webelieve the long-term trends in the global capital markets favor our industry.

There is no question that 2004 was a challenging year from a production viewpoint, with theforces of supply and demand significantly different than in 2003. On the supply side, we sawincreased competition from both the uninsured market and other traditional monolines, as wellas from new market entrants who were eager to earn their stripes in this difficult market.European banks have also become involved in our markets, especially in large publicinfrastructure financings. This led to pricing pressure and narrower margins throughout theyear across virtually every sector.

While supply of our product was increasing, overall demand was moving in the oppositedirection, reflecting a change in market sentiment from fear to greed. Credit spreads continuedto tighten throughout the year, effectively limiting what price we could charge issuers. Forexample, spreads between Triple-A and Triple-B corporates compressed 36%, going from 72 to46 basis points in 12 months. Corporate defaults were at a cyclical low, which was good for ourexisting portfolio but contributed to an increasing comfort level with and demand foruninsured bonds among investors. And despite the increase in the Fed funds rate, longer-terminterest rates remained low, with 10-year Treasuries beginning the year at 4.25% and ending theyear virtually unchanged. For all these reasons, 2004 was characterized by the perception of lowrisk in the marketplace, where investors, flush with cash and hungry for yield, were lessinterested in buying insurance, particularly in the asset-backed market.

Letter to Shareholders

Gary Dunton

87091_MBIA_Editorial.qxp 3/28/05 6:09 PM Page 2

3Letter to Shareholders

Bottom line – there was more supply of the financial guarantee product and muted demandboth here and abroad. Traditionally, we have our best years when the perception of risk isgreater than the real risk – the opposite of today’s market environment. The encouraging aspectof where we are today is that, like many things in life, there is a reversion to the mean, and webelieve economic conditions that favor our business will return in the near future.

The Year’s Accomplishments Considering the context of 2004’s challenges, our financial results were strong. We generatedsatisfactory growth in pre-tax operating earnings, with all three business lines (insurance, assetmanagement and municipal services) producing solid results. Pre-tax operating income in ourinsurance business topped the $1 billion mark for the first time in the Company’s history. Netoperating earnings per share grew 10% to $5.28, further demonstrating our ability to produceconsistent, steady earnings growth even in challenging times. Book value per share grew 10% to$43.05, excluding unrealized gains in our portfolio. Net income declined $1 million to $815million, primarily due to the small 2004 mark-to-market net gain on derivative exposure of$1.6 million, compared with a $100 million gain in 2003. And Adjusted Direct Premium(ADP) reached $1.1 billion – our third highest year ever.

The overall strength of our franchise and balance sheet improved in 2004. Our total claims-paying resources are now approaching $13 billion – a record level – and underpin a strongclaims-paying ratio of 81:1. The credit quality of our portfolio continues to improve, with over80% of the total book of business now rated Single-A or higher, demonstrating one of thebenefits of consistent, rigorous underwriting. We also expanded our global footprint as weopened a new office in Milan, Italy, and as we converted our U.K. office into a fully licensed,Triple-A-rated insurance company. Both events allow us to better meet the growing demand for our products throughout Europe, as issuers seek improved market access and a broaderinvestor base.

Other important achievements occurred in risk management: MBIA, along with partnersRenaissance Re, Partner Re and Koch Financial, launched Channel Re, a valuable and durablesource of Triple-A-rated reinsurance. Channel Re assumed $26 billion of in-force business from MBIA, which came from previously commuted treaties with other lesser rated insurers.This effectively increases our reinsurance capacity. Another form of risk transfer we executed in 2004 was an innovative capital markets transaction called Kirkwood. This transactionprovides an economic hedge for credit and market risk concentrations in our insured syntheticCDO portfolio.

Our portfolio shaping continued with the successful closure of ASIA Ltd, in which theCompany had acquired a minority interest as a result of its 1998 merger with CapMACHoldings. In this transaction, MBIA assumed the outstanding book of business, consisting of23 issues with outstanding par of $369 million. We also assumed $9 million of unearnedpremium reserves, $19 million of case reserves and $33 million of unallocated loss reserves.Overall, it was a very profitable exchange.

A very important silver lining of slower growth (amplified by our increasing credit quality) isthat we continue to be a net generator of capital, leading to greater strength in our capitalposition. We significantly exceed the rating agencies’ requirements with respect to our Triple-Aratings as well as regulatory capital requirements. In 2004, some of our capital cushion wasreturned to our shareholders through the repurchase of shares. During the third quarter, ourboard of directors authorized the Company to repurchase up to 15 million shares ofoutstanding common stock. As you may remember, we received a similar board authorizationin 1999 to repurchase up to 11.25 million shares, all of which were repurchased by July 2004.With our stock trading below adjusted book value for much of the year, we bought back a totalof 5.8 million shares at very attractive prices. At year-end 2004, approximately 10.9 millionshares remained in the Company’s latest buyback program.

87091_MBIA_Editorial.qxp 3/28/05 6:09 PM Page 3

In December, MBIA Insurance Corporation paid a special dividend of $375 million plus its regular quarterly dividend of $82 million to MBIA Inc., our holding company, afterreceiving approval from the New York State Department of Insurance. As of year-end, there was over $700 million of capital at our holding company. We plan to use these funds over time for additional share repurchases, strategic initiatives, general liquidity and other corporate purposes.

Throughout the year, we strengthened our employee base and built bench strength at all levels,including a refortified Executive Policy Committee (EPC), which is the policy-making team at the Company. As has been the case over the past few years, we continued to develop ourhuman capital with world class training and development programs in 2004, addressingsubjects such as negotiation, leadership and fraud detection. We also continued our focus onstrong corporate controls and governance, and this past year we implemented the newSarbanes-Oxley requirements without a hitch. Again in 2004, we received high rankings incorporate governance from organizations such as Institutional Shareholder Services (ISS),GovernanceMetrics International and Moody’s Investors Service.

We refocused our Asset Management Division around our fixed-income capabilities and sold our equity unit, 1838 Investment Advisors, for a modest $3 million profit. And finally, we had a $77 million pre-tax gain on the sale of a common stock investment the Companypurchased in 2002.

The Year’s DisappointmentsThe year’s disappointments certainly were led by the scarcity of attractive transactions that metour profitability goals and credit standards, due to both the pricing pressure mentioned earlierand to generally softer credit terms than we have seen in the past several years. Despite ourremediation efforts, we had losses on two transactions from the mid- to late-1990s: thePhiladelphia Authority for Industrial Development Tax Claim Collateralized Revenue Bondsand the Fort Worth Osteopathic Hospital. Higher interest rates also did not materialize as wehad anticipated 18 months ago, so the shortening of our investment portfolio duration back in2003 cost us some $40 million in foregone operating income. However, the other (better) sideof this story is that we have protected our economic capital base in what we still believe will bean increasing interest rate environment. Right decision, wrong timing.

In October, we initiated an investigation of reinsurance arrangements the Company hadentered into in 1998 in connection with the bankruptcy of Pittsburgh-based Allegheny Health,Education and Research Foundation (AHERF). The Audit Committee of the board of directorsand outside counsel led the examination. As a result of this investigation, MBIA decided torestate its financial statements for 1998 and subsequent years to correct the accounting for twoof the reinsurance agreements entered into with Converium Re. The restatement, whichamounts to a $57 million net reduction in profit from 1998 to 2003, results in an 11% decreasein net income for 1998, a 2% reduction in 1999, a decline of less than 1% in both 2000 and2001, and an increase of less than 1% in 2002 and 2003.

>>

4 Letter to Shareholders

Jay Brown

87091_MBIA_Editorial.qxp 3/28/05 6:09 PM Page 4

>

5Letter to Shareholders

In November, we received subpoenas from the Securities and Exchange Commission and theNew York State Attorney General’s Office that covered these 1998 AHERF reinsuranceagreements. In early March 2005, after we announced the restatement, we received a subpoenafrom the U.S. Attorney’s Office for the Southern District of New York. Needless to say, we arecooperating fully with these investigations.

Results by Business UnitOur insurance business was affected by the market conditions we have described; in particular,tight credit spreads squeezing global structured business volume, increased competition from uninsured executions, aggressive banking bids in Europe, and both reinvigorated old and aggressive new monoline competitors. Maintaining underwriting and pricing discipline in this environment led to lower volume across the board, in both plain vanilla and large “one-off” transactions.

We saw pricing pressure throughout the year. Standard & Poor’s profitability ratio reports forthe first half of 2004 indicated that in the domestic public and structured finance markets,industry profitability declined by 10% and 25%, respectively, demonstrating the extent ofpricing pressure. Our results were marginally better in the public finance business andmarginally worse on the structured side. While this is not the trend MBIA or the industry waslooking for, it’s worth noting that from 1999 through 2003, profitability in these two sectorshad doubled. The recent declines suggest the industry has given up only a portion of the groundit had gained.

On the international front, profitability trends are largely driven by “one-off” transactions, andtherefore can be uneven. In 2004, MBIA’s international public finance profitability was upconsiderably, primarily due to our lucrative and innovative guarantee of a toll road betweenSantiago and Talca, Chile. The flip side of this was evident in decreased international structuredfinance profitability, which was down due to tight spreads and competitive pressures. However,it is worth noting that our profitability levels are higher in international markets than indomestic markets.

These conditions contributed to a 29% decline in total ADP for our insurance operations to$1.1 billion, compared with the record $1.6 billion in 2003. Credit quality, however, remainedstrong, with 76% of net par insured rated Single-A or better, causing the quality of our overallbook to remain high. The percentage of our insurance portfolio rated non-investment-gradealso continues to improve, and was below 2% at year-end. While it is true that overall pricingcame under pressure, our expected returns on new business booked continued to meet orexceed our target hurdle rates.

Industry trends in public finance also reflected the challenging market conditions. For example,the domestic new issue market in 2004 was down 6% to $361 billion, compared with $384billion in 2003.

Despite the decline in new issuance, the domestic insured new issue market actually increasedslightly in 2004 to $194 billion, as insured penetration climbed to 54%, an all-time high.

87091_MBIA_Editorial.qxp 3/28/05 6:10 PM Page 5

Insured penetration levels remained high, even in the current environment, due to strong retaildemand for insurance and, to a lesser degree, greater issuance of auction-rate debt, which tendsto use more insurance.

In our domestic public finance business, the year’s production declined 27%, to $457 millionfrom $627 million in 2003, reflecting lower market issuance and pricing pressure. Internationalpublic finance production dropped more sharply, down 36% to $262 million from $409million in 2003, largely due to fewer large infrastructure projects coming to market in 2004, aswell as several transactions being delayed. Globally, we insured over $61 billion in publicfinance par, down 18% from $74 billion in 2003. Increased competition did result in somedownward pricing pressure, but overall returns remained respectable, while our capital chargesremained very much under control, improving slightly from 2003.

Encouraging notes in public finance include our robust activity in Australia and Latin America.One particularly interesting transaction this year was a toll road in the Mexican state of NuevoLeon. This 16-year-old road has been owned and operated by a state agency since opening. The $200 million securitization of the toll road’s future collections was the country’s firstinsured financing for a state infrastructure asset and utilized a non-recourse private trust forrevenue collections. Named “Infrastructure Deal of the Year for the Americas” by ProjectFinance International, this transaction is a template for the involvement of global monolines instate and local infrastructure finance, a trend we expect to see more of in Mexico and the rest of Latin America.

Turning to MBIA’s structured finance business, a combination of tight spreads and greaterdemand for uninsured transactions reduced the number of attractive opportunities available tous this year. Overall, there was lower insured penetration in the asset-backed market, as issuers favored senior-subordinated structures over bond insurance, given unabated investordemand for higher yielding uninsured paper. In addition, fewer large, blockbuster-typeEuropean transactions came to market, and the volume of CDO issuance was lower due tonarrow credit spreads.

Our performance in this sector was affected by increased competitive pricing and weaker creditstandards in bids from European banks. As a result, production declined 27% to $427 millionin 2004, from a record $585 million in 2003, although par increased by 8% to $51 billion,reflecting both shifts in product mix and downward pricing pressure. Although returns onbusiness written during 2004 were down from the prior year, they remained more thanacceptable. Credit quality of structured deals insured declined this year with 64% rated Single-A or higher, due mostly to reduced volume in Triple-A CDOs.

The Structured Finance Division executed some landmark transactions in 2004, including awhole company lease securitization for the Fraikin Group, which is controlled by Eurazeo, aleading French private-equity investor. This €600 million transaction was a first for MBIA anda first for France. The Fraikin Group, which is France’s leading truck and commercial vehiclerental company, offers a full range of transportation solutions including contract hire, truckrental and fleet management. MBIA guaranteed secured-loan facilities for Fraikin Assets, a

Neil Budnick

> >

6 Letter to Shareholders

87091_MBIA_Editorial.qxp 3/28/05 6:10 PM Page 6

Mark Zucker, Chris Weeks, Tom McLoughlin

>

7Letter to Shareholders

bankruptcy remote special purpose vehicle, which allows the company to acquire new trucksand complete new lease contracts. The transaction was named “European Corporate Deal ofthe Year” by International Securitisation Review, and is representative of the growing trend inEurope where businesses turn to the capital markets as alternatives to banking facilities.

Stepping back to look at our overall insurance business, total earned premiums were up 11% in2004, driven by new business writings over the past few years as well as the high level ofrefundings in our municipal book. Earned premiums from refundings increased 10% to $140million for the year, against very strong refunding activity in 2003.

We continue to make progress on lowering our GAAP expense ratio, which declined to 22.0%in 2004 from 22.8% in 2003. As we look back over the past 5 years, we have seen our grossinsurance expenses (before any deferrals) grow at an average annual rate of 7%. We arecommitted to controlling our expense growth, keeping it at a lower rate than growth in our netrevenues over the long term.

Moving beyond the insurance operations, MBIA’s institutional investment managementbusiness had a breakthrough year. Pre-tax operating income increased 31% to $61 million from$47 million in 2003, and assets under management reached $39 billion compared with $34billion the previous year. As part of the transformation of this business into a fixed-income-onlyplatform, we integrated the Conduit Group into the Asset Management Group, where it canleverage additional expertise for new deal generation in addition to strengthening back officeoperations. Since then, the Conduit Group has already closed two deals for over $1 billion innew issuance. Finally, the division strengthened its managed CDO capabilities, expanding intothe asset-backed sector and closing a $500 million CDO.

Our third and final business line, MuniServices, met all of its financial targets this year,generating a small pre-tax operating profit of nearly $2 million in 2004, up from $1 million in2003. The business expanded its tax discovery, collections, audit and other revenue enhancingservices to a number of new public-sector clients nationwide. While we are pleased withMuniServices’ growth in 2004, we believe this business is not consistent with MBIA’s corebusiness of risk management, and we will explore opportunities to sell the company in 2005.

To summarize, certainly the new business environment was not as favorable as in recent years, but short-term market cycles are part of our long-term business model, and the market pendulum eventually swings back. Even if current market conditions persist, we will continue to pursue proactively all appropriate business opportunities while maintaining pricing and underwriting standards. As market conditions change, we will respond swiftly and appropriately.

Risk Management PhilosophyMBIA’s true constant – our North Star, if you will – is our commitment to protecting ourTriple-A ratings, the keystone of our franchise. Our ratings are built on the foundation of topquality risk management with a no-loss underwriting standard. As you know, we will always actin the best interest of our shareholders, consistent with our commitment to both our standard

87091_MBIA_Editorial.qxp 3/28/05 6:10 PM Page 7

of underwriting excellence and our Triple-A ratings. If markets are good, we will competevigorously for growth. If markets are poor, we’ll still seek to compete vigorously for profitablebusiness, but we are fully willing to pick up our marbles and go home, conserving our capital for another day or returning excess capital to our owners by repurchasing shares. And if there are opportunities to thoughtfully expand our global franchise through strategicmergers or acquisitions, we will consider them as well. In all cases, we will adhere to our no-loss underwriting standards, disciplined pricing approach and careful, prudent expense management.

Let’s remember that anything truly worthwhile is not built easily or quickly. So it is with MBIA.Our model of underwriting low risk transactions that generate premium earnings over a longterm provides relative stability – stability in growth in earnings and in book value due to thefinancial and accounting underpinnings of our business model. Although we expect toexperience relatively attractive growth in our business platform over time, results in anyindividual quarter or single year – or even a couple of years – may well deviate from the mean.This includes both top line revenues and also actual losses. We are constrained in our ability tocreate short-term growth due to our underwriting standards and their importance to our long-term business success. We work hard to generate new business across all economic conditions,but ultimately can only do what the market allows at any point in time.

One of the intended consequences of no-loss underwriting is that losses are rare, and are bydefinition very difficult, if not impossible, to anticipate precisely. Over time we will inevitablyhave losses in amounts that are sometimes more than our quarterly reserving formula andsometimes less. There is no way to predict the exact amount of our losses over the short run. Atall times, we will seek to maintain total loss reserves to cover estimated losses in the existingportfolio. Note that in 30 years of business, with over $1.8 trillion of guaranteed debt service,we have only incurred $586 million of net losses. Put another way, since our inception in 1974,our underwriting decisions have been right 99.97% of the time!

But the .03% of losses we have incurred have taught us some key lessons. Losses will occur andwe need to price to ensure that we have sufficient capital to pay them, while at the same timeproviding a good return for our shareholders. We need adequate capital – we have around $13billion of claims-paying resources to ensure our Triple-A ratings are protected, and to guaranteethat under almost any possible economic scenario, our insured bondholders will not experiencelosses. We maintain adequate reserves in the form of both specific-case and unallocated reserves.We aggressively remediate credits at the first sign of trouble. Our underwriting criteria favorhigher underlying deal ratings where we strive to keep at least 75% of our in-force insuranceportfolio rated Single-A or better, and keep our non-investment-grade exposures to under 2%.We’ve learned that issuer or seller/servicer bankruptcies don’t necessarily equate to losses. Andthe securitizations we insure are structured to give us substantial first-loss protection andsignificant control rights for early action.

In 2004, we experienced two notable losses, which were fully covered by a portion of ourunallocated loss reserve.

Ruth Whaley, Mitch Sonkin, Kevin Silva

>

8 Letter to Shareholders

87091_MBIA_Editorial.qxp 3/28/05 6:10 PM Page 8

>

9Letter to Shareholders

The first loss occurred during the second quarter, when MBIA paid a $46 million claim – theremaining principal balance – on the Philadelphia Authority for Industrial Development TaxClaim Collateralized Revenue Bonds. The bonds were backed by a pool of delinquent propertytax liens that significantly underperformed, resulting in a shortfall. MBIA will vigorouslypursue collection of the remaining liens, and estimates that approximately $20 million can berecouped, resulting in a loss of $23 million, net of previous reserves and reinsurance.

Our second loss occurred in the third quarter, when we established a case loss reserve ofapproximately $49 million against $71 million net par exposure to Fort Worth OsteopathicHospital. While our Insured Portfolio Management team worked very closely with the hospitalto avoid a loss, the credit deteriorated to an irrecoverable degree, and substantially all of thehospital’s property was sold at auction in February 2005.

In addition, a new case reserve was established in the fourth quarter for a manufactured housingexposure in the amount of $10 million. This exposure has experienced higher-than-expectedlosses, and we continue to actively monitor it. This sector, unlike most others in our portfolio,has not benefited materially from the positive market credit trends of the last few years.

A Strong and Vital OrganizationOne of the most important responsibilities I have is to ensure that MBIA’s leadership team andemployees are the most highly trained, productive, motivated and challenged workforce in theindustry. This is why we stress internal training and development programs so much, why weinvest significantly in information technology and why we continue to make organizationaladjustments to fine-tune our business and market effectiveness.

2004 was no different, as we managed through process and leadership changes that had beenplanned over the prior years. In our underwriting process, we implemented comprehensive newfraud detection standards and assessment systems for use throughout our New Business,Underwriting and Insured Portfolio Management teams. We expanded our range of trainingprograms to include a multi-year leadership development program focused on our core values,business ethics and many elements of overall enterprise management. And we reorganized ourGlobal Public Finance Division along product lines, rather than geography, to align better withour client needs and with our own global operations.

The senior leadership team at MBIA – the Executive Policy Committee – was also reinvigoratedby a number of strategic changes in 2004. All of these changes but one were part of a multi-yearplanning process, and all were executed smoothly. We are pleased that we found all these seniormanagement replacements within our company, with the exception of Mitch Sonkin.

In May, Neil Budnick became President of MBIA Insurance Corporation. Neil returned to thenew business side of the house to lead our global public and structured finance businesses afterserving ably as Chief Financial Officer for the past 5-plus years.

87091_MBIA_Editorial.qxp 3/28/05 6:10 PM Page 9

Nick Ferreri was named Chief Financial Officer, succeeding Neil. Nick brings a rock-solidfinancial and accounting background together with considerable management experience to thejob, and he’s proving to be a valuable contributor to the EPC.

In our insurance operations, two key changes occurred. After a decade of circling the globe as hehelped build our international franchise, Chris Weeks was named head of the InternationalDivision and a member of the EPC, based out of our London office. Chris succeeded JackCaouette, who retired in December. Jack made many contributions to MBIA since joining uswith the CapMAC merger in 1998. He jumpstarted our international business and cut a widepathway into the global marketplace for MBIA. Under his guidance, ADP for non-U.S. publicand structured finance reached over 35% of MBIA’s business production. I am grateful to himfor his leadership and contributions, and I wish him all the best.

Tom McLoughlin was named head of our Global Public Finance Division, and a member of theEPC. Tom replaced John Pizzarelli, who left MBIA to pursue other interests after 20 years ofservice. Recently head of Global Transportation and Infrastructure, Tom spent a decadebuilding our public finance business in the western U.S., and he brings a wealth of industry andpublic-sector experience to this position. He has a proven track record that bodes well for futuresuccess in his new role.

Turning to our Asset Management Division, Cliff Corso, who is doing a superb job as MBIA’sChief Investment Officer and head of fixed-income asset management, was named a member ofthe EPC and president of MBIA Asset Management, LLC in June, following Thacher Brown’sretirement. Thacher took our asset management franchise to a new level after joining theCompany in 1998 following MBIA’s merger with 1838. We are indebted to him for hiscontribution to the business, and I wish him well in his future endeavors.

Earlier, Andrea Randolph was named Chief Technology Officer, and Mitch Sonkin was namedhead of Insured Portfolio Management and Government Relations. Although fairly recentadditions to our EPC, they have quickly and successfully integrated into the MBIA seniormanagement team.

Finally, in May, I became Chief Executive Officer, assuming the role from Jay Brown whoremains our Executive Chairman. I want to express my special appreciation to Jay, whosecounsel, support and encouragement have made it possible for me to grow into my currentposition. MBIA is indeed fortunate to have had such a knowledgeable, disciplined and high-integrity leader at the helm for the past five years.

Our board of directors also experienced somewhat of a transformation in 2004. Our twolongest-serving directors, Freda Johnson, with 15 years of service, and Jim Lebenthal, with 17,retired at year-end. Both Freda and Jim served faithfully and tirelessly during their time on ourboard and helped shape MBIA’s success from its early days. MBIA is unusually fortunate tohave had the benefit of their dedication all these years. It was a privilege to work with them, andI wish them every success.

>>Ram Wertheim, Cliff Corso

10 Letter to Shareholders

87091_MBIA_Editorial.qxp 3/28/05 6:10 PM Page 10

>Nick Ferreri, Andrea Randolph

11Letter to Shareholders

Just as Freda and Jim helped shape our past, we look to Debra Perry and Laurence Meyer tohelp chart our future. Debra, elected to our board in May, was most recently a Senior ManagingDirector at Moody’s where she was responsible for Moody’s Americas Corporate Finance,Leveraged Finance and Public Finance departments.

Elected to the board in August, Larry is currently Vice Chairman of Macroeconomic Advisers, adistinguished scholar at the Center for Strategic and International Studies and a board memberof the National Bureau of Economic Research. He also serves as a senior adviser to the G-7Group and is a fellow of the National Association of Business Economists.

The combination of insight, strength and experience in our senior leadership team and board of directors is formidable. They are the right team to guide us forward as we continue our pushinto the global capital markets.

The Opportunities AheadWe are very optimistic about our future prospects. We have a solid pipeline of businessopportunities to work on, our global franchise grows stronger every day, and the macro trendsfavor our industry as globalization, financial deregulation, bank disintermediation andprivatization continue to define the capital markets. For example, key infrastructure projectsaround the world, such as toll roads and utilities, are being privatized, particularly in Europe, asgovernments recognize that partnering with the private sector can lead to more efficient andeffective financing and management of large-scale projects. Another trend is thedisintermediation of banks in Europe, as banks struggle to compete with the more efficient,transparent and liquid capital markets. In fact, much of our business in Europe comes frombanks themselves who are looking for either capital or regulatory relief via the capital markets.

In the U.S., where the public finance market is mature, we expect to see continued modest butsteady growth in the 8% range. The major growth in public finance is occurring ininternational markets where opportunities abound, but where growth is not evenly paced.MBIA will benefit from a number of important, long-term trends such as Public PrivatePartnerships and Public Finance Initiatives (PPP/PFI), particularly in the U.S. and the U.K.PPP and PFI transactions are typically very complex, and involve private-sector involvement inthe funding, construction and management of large-scale public works such as roads, hospitalsand stadiums. Many foreign markets have recently developed legal and economic frameworksfor these transactions, and more will do so in time. With MBIA’s guarantee on these deals,investor confidence and demand for the securities naturally increase.

Essential infrastructure transactions, some of which have structured finance aspects to them, areeven larger drivers of the global markets. These are large-scale public projects such as airports,toll roads, rail and tunnel projects, and utilities such as water, gas and electric plants. Militaryhousing is another growing category, in which we lead the market today. This sector issupported by a strong governmental obligor, and it leverages our deep knowledge of housingand other key disciplines required to execute these transactions successfully.

87091_MBIA_Editorial.qxp 3/28/05 6:10 PM Page 11

Another important global trend is pension reform, in Europe and elsewhere. In Italy, Germanyand France in particular, there exist huge and unfunded pension liabilities, which will need tobe funded over time as their populations age. Many of the plan sponsors want a risk-managedfixed-income solution, as investors are not accustomed to taking cross-border and other creditrisk. Triple-A-rated insured bonds will help address this need.

In contrast to public finance, the structured finance market still shows strong growth in thelow- to mid-teens in the U.S., and even higher in the international arena. A particularly strongarea for us – one that shows significant expansion potential – is the future flow sector, especiallyin emerging market countries. In these transactions, we guarantee a security backed by expectedfuture receivables from credit card cash flows, bank remittances, or from exports of naturalresources such as oil, iron ore and copper. We’ve recently applied this technique to an additionalasset class – intellectual property. To date, we’ve insured film financings from the Australianproduction company Village Roadshow, and a transaction secured by royalty streams fromseveral drug patents issued by Royalty Pharma Finance Trust.