mbr environmental impact

TRANSCRIPT

›› www.metalbulletinresearch.com

New for 2016

The cost of EU’s new environmental regulations on EU integrated producers out to 2021

Whitepapers

Whitepaper: MBR feature

Europe/Americas/MENA [email protected] +44(0) 20 7779 8174 Asia [email protected] +61 3 5222 61542

Across Europe – with the UK particularly affected, around 5,000 steel industry jobs alone were lost in October 2015. With the current impact of competitively priced imports, driven largely by Chinese exports which have exploded to around 110m tonnes this year, environmental legislation facing EU steelmakers is seen by many as a further burden to fall upon the industry over the coming years. .

This is another real threat to the 330,000 workers

in the steel sector, a headcount down 85,000 since

2008. According to Mr Axel Eggert, Director General of

EUROFER, “The EU needs to adapt trade, climate and

energy policies, in particular the review of the EU Emission

Trading Scheme, to keep our sector competitive. Best

performers in carbon leakage sectors like steel must not

be penalised by additional direct or indirect carbon costs

against extra-EU competitors”

It is against this context that Metal Bulletin Research (MBR)

has now published the highly topical research study

called “Impact of Environmental Policies on the Global

Steel Industry: Technical and Economic Performance

Assessment from the EU Perspective”*

Our new and independent study shows that the cost of

EU’s new environmental regulations could be as high as

€15/tonne on a crude steel basis for key EU integrated

producers out to 2021. Total cost of the carbon allowance

for the steelmakers will reach US$500 million by 2021.

These costs would represent 25-60% of average EBITDA

margins of the EU steel industry over the last few years.

This is significant as MBR’s continues to forecast global

overcapacity to feature out to 2020 from low-cost

emerging market steel producers. This casts doubts as

to whether the EU steel industry can really competitively

pass on any of these additional costs onto customers.

EU steel companies are competing more than ever before

on which are best positioned to adopt effective strategies

against the backdrop of even more environmental

pressure planned on EU steel mills. Our analysis shows

that EU steel companies have afforded to invest in

environment-related investments in profitable times. The

number of environmental initiatives translating into actual

investment projects skyrocketed in 2010-2011. However,

with steel prices and EBITDA margins declining since

then so have the total number of newly announced

environmental projects.

This has left some EU steel companies investing only

to assure their operations are merely compliant to EU

legislations, while others have progressed more and

manage to adopt a more holistic and forward looking

approach aimed at promoting long-term efficiency gains

beyond mere compliance. This has involved targeting

improvements to the efficiency of energy generation,

coking synthesis and the steelmaking process, switching

to less emissions-intensive fuel types etc.

ANAlysis

MBR feature: the cost of EU’s new environmental regulations could be as high as €15/tonne on a crude steel basis with the total cost for key EU integrated producers totalling US$ 500 million out to 2021

1 December 2015 - Roman Kucinskij, Research Analyst, Metal Bulletin Research

Europe/Americas/MENA [email protected] +44(0) 20 7779 8174 Asia [email protected] +61 3 5222 61543

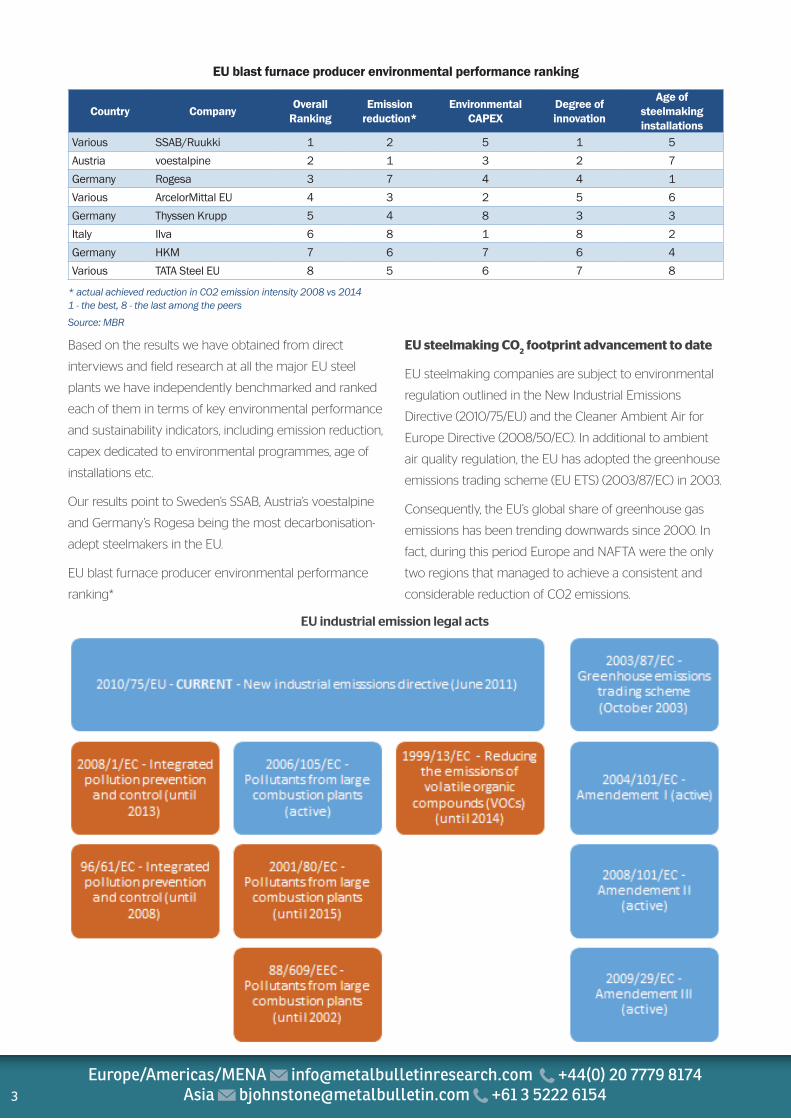

Based on the results we have obtained from direct

interviews and field research at all the major EU steel

plants we have independently benchmarked and ranked

each of them in terms of key environmental performance

and sustainability indicators, including emission reduction,

capex dedicated to environmental programmes, age of

installations etc.

Our results point to Sweden’s SSAB, Austria’s voestalpine

and Germany’s Rogesa being the most decarbonisation-

adept steelmakers in the EU.

EU blast furnace producer environmental performance

ranking*

EU steelmaking CO2 footprint advancement to date

EU steelmaking companies are subject to environmental

regulation outlined in the New Industrial Emissions

Directive (2010/75/EU) and the Cleaner Ambient Air for

Europe Directive (2008/50/EC). In additional to ambient

air quality regulation, the EU has adopted the greenhouse

emissions trading scheme (EU ETS) (2003/87/EC) in 2003.

Consequently, the EU’s global share of greenhouse gas

emissions has been trending downwards since 2000. In

fact, during this period Europe and NAFTA were the only

two regions that managed to achieve a consistent and

considerable reduction of CO2 emissions.

EU blast furnace producer environmental performance ranking

Country Company Overall Ranking

Emission reduction*

Environmental CAPEX

Degree of innovation

Age of steelmaking installations

Various SSAB/Ruukki 1 2 5 1 5Austria voestalpine 2 1 3 2 7Germany Rogesa 3 7 4 4 1Various ArcelorMittal EU 4 3 2 5 6Germany Thyssen Krupp 5 4 8 3 3Italy Ilva 6 8 1 8 2Germany HKM 7 6 7 6 4Various TATA Steel EU 8 5 6 7 8

* actual achieved reduction in CO2 emission intensity 2008 vs 20141 - the best, 8 - the last among the peersSource: MBR

EU industrial emission legal acts

Europe/Americas/MENA [email protected] +44(0) 20 7779 8174 Asia [email protected] +61 3 5222 61544

Global carbon emissions vs. GDP, 1983-2013

Europe

MENAOther As ia

CIS

NAFTA

China

0

250

500

750

1,000

1,250

1,500

1,750

2,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Glo

bal c

rude

ste

el p

rodu

ctio

n, M

tonn

es

Tota

l CO

2 em

issi

ons,

MTo

nnes

Latin America India Africa Global crude steel production (RHS), Mtonnes

Source: MBR, various

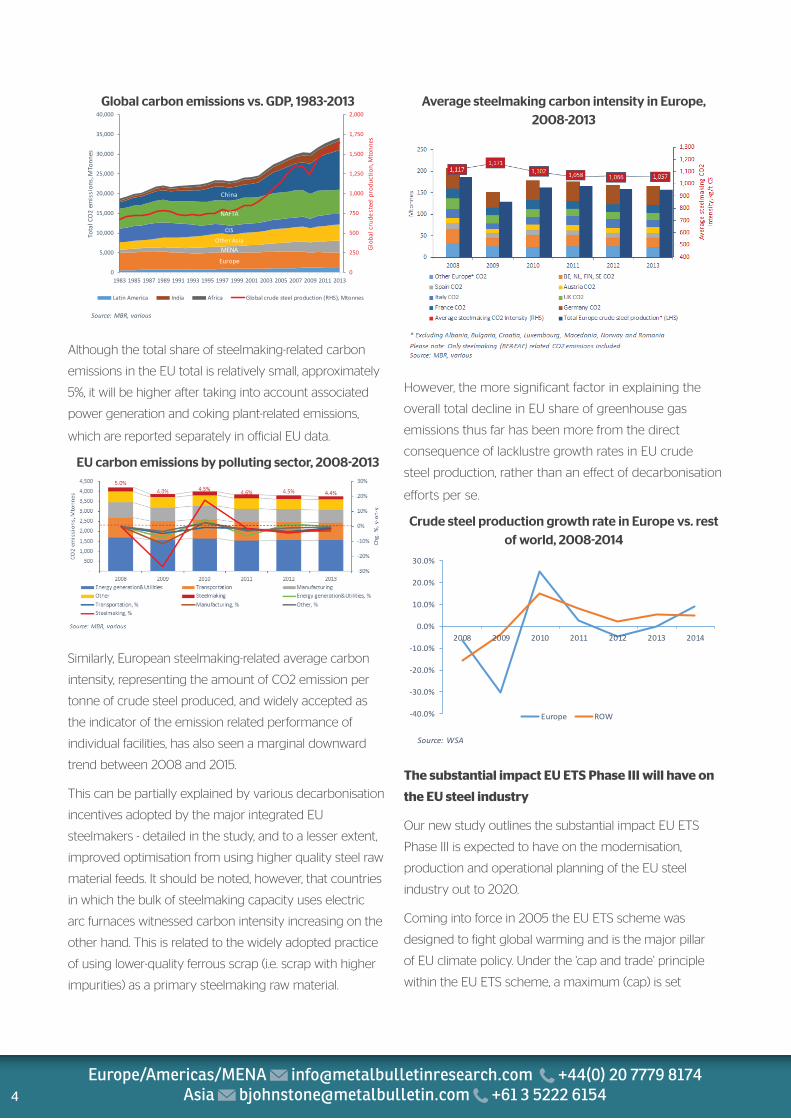

Although the total share of steelmaking-related carbon

emissions in the EU total is relatively small, approximately

5%, it will be higher after taking into account associated

power generation and coking plant-related emissions,

which are reported separately in official EU data.

EU carbon emissions by polluting sector, 2008-2013

Similarly, European steelmaking-related average carbon

intensity, representing the amount of CO2 emission per

tonne of crude steel produced, and widely accepted as

the indicator of the emission related performance of

individual facilities, has also seen a marginal downward

trend between 2008 and 2015.

This can be partially explained by various decarbonisation

incentives adopted by the major integrated EU

steelmakers - detailed in the study, and to a lesser extent,

improved optimisation from using higher quality steel raw

material feeds. It should be noted, however, that countries

in which the bulk of steelmaking capacity uses electric

arc furnaces witnessed carbon intensity increasing on the

other hand. This is related to the widely adopted practice

of using lower-quality ferrous scrap (i.e. scrap with higher

impurities) as a primary steelmaking raw material.

Average steelmaking carbon intensity in Europe, 2008-2013

However, the more significant factor in explaining the

overall total decline in EU share of greenhouse gas

emissions thus far has been more from the direct

consequence of lacklustre growth rates in EU crude

steel production, rather than an effect of decarbonisation

efforts per se.

Crude steel production growth rate in Europe vs. rest of world, 2008-2014

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

2008 2009 2010 2011 2012 2013 2014

Europe ROW

Source: WSA

The substantial impact EU ETs Phase iii will have on

the EU steel industry

Our new study outlines the substantial impact EU ETS

Phase III is expected to have on the modernisation,

production and operational planning of the EU steel

industry out to 2020.

Coming into force in 2005 the EU ETS scheme was

designed to fight global warming and is the major pillar

of EU climate policy. Under the ‘cap and trade’ principle

within the EU ETS scheme, a maximum (cap) is set

Europe/Americas/MENA [email protected] +44(0) 20 7779 8174 Asia [email protected] +61 3 5222 61545

on the total amount of greenhouse gases that can be

emitted by all participating installations. ‘Allowances’ for

emissions are then auctioned off or allocated for free, and

can subsequently be traded. Installations must monitor

and report their CO2 emissions, ensuring they hand

in enough allowances to the authorities to cover their

emissions. If emission exceeds what is permitted by its

allowances, an installation must purchase allowances from

others. Conversely, if an installation has performed well at

reducing its emissions, it can sell its leftover credits. This

allows the system to find the most cost-effective ways

of reducing emissions without significant government

intervention.

The scheme has been divided into a number of “trading

periods”. The first ETS trading period lasted three years,

from January 2005 to December 2007. The second

trading period ran from January 2008 until December

2012, coinciding with the first commitment period of the

Kyoto Protocol.

Starting in January 2013, and spanning until December

2020, Phase III of ETS sees a turn to auctioning a majority

of permits rather than allocating freely to each EU state;

harmonisation of rules for the remaining allocations; and

the inclusion of other greenhouse gases, such as nitrous

oxide and per fluorocarbons.

The problem was attempts to set up a market-driven

and viable emission trading scheme largely failed to

materialise. Insufficient demand, caused by excessive free

allocations and slower than expected industrial output in

the aftermath of the 2008/2009 crisis resulted in the free-

market carbon auction price crashing to almost zero on a

number of occasions.

However, now with the tightening of EU emissions limits

as defined in Phase III of the EU Emissions Trading

Scheme (ETS) this is now expected to result in the total

national free carbon emission allocations balance for EU

member countries turning negative from 2016 onwards.

Estimated shortfall in free carbon emissions

allowances under EU ETS Phase III out to 2020

This should re-establish the functionality of the ETS

trading market, at the same time as prompting industrial

carbon emitters, including steelmakers, to incur additional

costs as a result of increasing carbon prices to source

additional carbon allocations on a free market to cover

this shortfall. We detail our carbon price forecasts within

the study out to 2020.

Key obstacles for the steel sector in terms of new

environmental regulations

A new international climate agreement to replace the

Kyoto protocol is expected to be finalised and signed

in Paris during the United Nations Climate Change

Conference in December 2015.

We understand that the new agreement is unlikely to

introduce sectorial environmental targets, owing to a

lack of incentive to co-ordinate joint efforts between the

existing members and newly signing countries alike.

The EU ETS review process is also not expected to

yield any considerable innovations from which the steel

sector could benefit, apart from certain positive gains

in supporting “carbon leakage” prevention as a political

compromise on behalf of EU commissions.

MBR expects steel mill profitability to remain the driving

force behind adopting and investing in new environment

and sustainability projects going forwards. However, this

also represents the EU steel industries single most critical

challenge in Metal Bulletin Research’s view out to 2020.

Europe/Americas/MENA [email protected] +44(0) 20 7779 8174 Asia [email protected] +61 3 5222 61546

Contrary to the belief of some members within EUROFER,

we do not expect a widespread gradual shift towards EAF

steelmaking in the EU over the long time, as a response

to the ramp up in carbon emission allowance costs. This is

likely to be the case due to:

l ample supply of highly competitive steelmaking

capacities in other regions expected going forward

l the anticipated tightening in the EU energy balance

due to shifting weight away from conventional power

generation and ever more to renewable energy

sources

l Despite some trade protectionist measures being

adopted to protect the EU steel industry from unfairly-

priced foreign imports, we do not expect wholesale

state interventionist support for the EU steel industry

As such, MBR believes that the net effect of upcoming

environmental costs will be to act as yet another factor,

in a series of factors that most likely will see the gradual

long-term transformation of the EU steel industry.

We expect the EU to increasingly move away from

upstream steelmaking, via the BF route, to more

re-rolling and steel processing operations of imported

semis to produce high-value steel products serving EU’s

automotive, engineering, construction, as well as other

niche sectors in a just-in-time manner.

Methodology and coverage

Metal Bulletin Research’s brand new independent strategic

forecast study called ‘Impact of Environmental Policies

on the Global Steel Industry: Technical and Economic

Performance Assessment from the EU Perspective’, has

just been published.

The research programme involved three month’s worth of

site visits, face-to-face and phone interviews with major EU

integrated steelmakers and associated industry bodies.

The study offers independent and exclusive data on

the impact of EU environmental policies on European

integrated steel producers performance, as well as a

forward outlook.

For the first time, the study provides apparent CO2

emissions by steelmaking process in 2014, historic

carbon emission released and carbon intensity statistics,

forecast effect of the reduction in free carbon emissions

allowances on carbon prices (€/t) from 2016 out to 2020,

analysis of the direct economic impact environmental

investment projects have had on the cost of crude steel

production at each major EU integrated steelmaking site.

The study also features a detailed technical database

detailing sintering, coking coal, DRI/HBI, blast furnace,

BOF, vacuum degassing and ladle facilities for each

selected EU plant.

Roman Kucinskij, a consultant with Metal Bulletin

Research, is one of the authors of the report. Any

questions please contact on :

[email protected] or + 44 (0) 827 7827 6421

To download a free complimentary review of the report

click here:

Disclaimer: This Disclaimer is in addition to our Terms

and Conditions as available on our website and shall not

supersede or otherwise affect these Terms and Conditions.

Prices and other information contained in this publication

have been obtained by us from various sources believed

to be reliable. This information has not been independently

verified by us. There may be errors or defects in such

assumptions or methodologies that cause resultant

evaluations to be inappropriate for use. Your use or reliance

on any information published by us is at your sole risk.

Meet the EditorRoman Kucinskij

Having graduated from the University of Aberdeen with a M.Sc. in International Business Energy and Petroleum, Roman predominantly concentrated on MBR consultancy coverage of the global metals

& mining space. Furthermore, Roman is a MBA holder from the Vilnius Gediminas Technical University. Prior to joining MBR Roman worked as a research associate at the Australian Mineral Economics (AME) in Sydney and London covering CIS metals sector. From 2006 to 2009 Roman worked a Pan-Baltic Head of Marketing and Sales at Q-Vara, a leading investment company in Baltics. Roman is a native Russian speaker.

+44 (0) 20 7779 8000+44 (0) 20 7779 8090info@metalbulletinresearch.comwww.metalbulletinstore.comMetal Bulletin Research, 8 Bouverie Street, London, EC4Y 8AX

FIVE EASY WAYS TO ORDER

You are also able to request a brochure, sample extracts and detailed table of contents for more information

Impact of Environmental Policieson the Global Steel Industry: Technical and Economic PerformanceAssessment from the EU Perspective

What direct and indirect impact will Phase III of ETS have on the EU steel industry?

What impact will it have on EU steelmaking operating and total costs?

Which EU steel companies are the most environmentally advanced?

What is the future carbon emissions price for the steelmaking industry post 2016?

New&Exclusive

for 2016

REQUEST A DEMO

Yes I would like to order: Impact of Environmental Policies on the Global Steel Industry: Technical and Economic Performance Assessment from the EU Perspective

www.metalbulletinresearch.com

Call:+44 (0) 20 7779 7999

Fax this form to:+44 (0) 20 7779 8090

Five easy ways to orderE-mail:[email protected]

Online:www.metalbulletinstore.com

Mail this form to:Metal Bulletin Research SpecialReports, TDS, Pegasus Drive,Stratton Business Park, Biggleswade,Bedfordshire SG18 8TQ, UK

Select: Select: Select:

Hard copy

Electronic copies

Excel data

Access to analysts / consultants

Quarterly updates of the report

Please tick which packageyou would like to order:

Silver Package

$13,500£7,995€10,995

1 copy

1 user

1 user

4

8

Gold Package

$20,250£11,992€16,492

3 copies

Unlimited users in one office

Unlimited users in one office

4

8

Platinum Package

$27,000£15,990€21,990

Up to 5 copies

Unlimited users globally/Intranet access

Unlimited users/Intranet access

4

4

Other relevant Metal Bulletin Research publications include:• Steel Raw Materials: Weekly Market Tracker• Steel: Weekly Market Tracker• Steel Plate Market by Grade, Dimension and Application: Global Strategic Outlook to 2024

• Steel Rebars: A Market Technical and Plant Performance Feasibility Study• The Five Year Outlook for the Global OCTG Industry• Global Small-diameter Linepipe Market: The Five Year Strategic Outlook• The Five Year Strategic Outlook for the Global Large-diameter Linepipe Market

• Strategic Prospects for the Global Transmission Linepipe Market by Type,Size Range and Grade

• Global Steel Cost Service• Steelmaking Capacity and Capex Study

The service includes a hard copyand electronic access to the study,associated data spreadsheets, andconsultant support.

For more information please visit www.metalbulletinresearch.comor call +44 (0) 20 7779 7999 or email [email protected]

Get all current and upcomingStrategic Forecast Studies in ahandy portal, accessible for yourentire organisation

For more information [email protected] call +44 (0) 20 7779 7999

Strategic Forecast StudyLibrary License

Personal details

Name

Company

Job Title

Country

Telephone

Payment Method

ChequeInvoiceCredit Card*

*A representative will be in touch to arrange payment.

SUBMIT FORMUse of your information The information you provide on this form will be used by Euromoney Institutional Investor PLC and its group companies (“we” or “us”) to process your order and/or deliver relevant products/services and content. We may also monitor your use ofour website(s), including information you post and actions you take, to improve our services to you and track compliance with our terms of use. Except to the extent you indicate your objection below, we may also use your data (including data obtained from monitoring)(a) to keep you informed of our products and services; (b) occasionally to allow companies outside our group to contact you with details of their products/services; or (c) for our journalists to contact you for research purposes. As an international group, we may transferyour data on a global basis for the purposes indicated above, including to countries which may not provide the same level of protection to personal data as within the European Union. By submitting your details, you will be indicating your consent to the use of your data asidentified above. Further information on our use of your personal data is set out in our privacy policy, which is available at www.euromoneyplc.com or can be provided to you separately upon request. Marketing choices If you object to contact as identified above by telephoneq, fax q, or email q, or post q, please tick the relevant box. If you do not want us to share your information with our journalists q, or other companies q please tick the relevant box.

DATA PROTECTION NOTICE