mbs basics - mark adelson | · pdf filembs basics mark h. adelson director–head of...

TRANSCRIPT

Fixed Income Research

© Nomura Securities International, Inc.

MBS Basics

Mark H. Adelson Director–Head of Structured Finance Research

Nomura Securities International, Inc.

Thacher Proffitt & Wood New York, Tuesday, 11 April 2006

Fixed Income Research

2 © Nomura Securities International, Inc.

Key Theme: Prepayments

Prepayment risk distinguishes MBS

Comes from prepayment option in residential mortgage loans

Gives MBS undesirable "negative convexity"

Gives MBS higher yields than securities without prepayment risk

Ginnie Mae MBS Spread

to 5-Year Treasuries(basis points)

0

50

100

150

200

250

300

20

00

20

01

20

02

20

03

20

04

20

05

20

06

Source: Bloomberg MTGEGNSF, GT5

Fixed Income Research

3 © Nomura Securities International, Inc.

Why Focus on MBS

Mortgages are a big slice of all U.S. debt

MBS are a big slice of the bond market

MBS are the biggest slice of the securitization

market

MBS is the original source of securitization

technology

Understanding MBS is helpful (often essential) to

understanding other types of securitizations

Fixed Income Research

4 © Nomura Securities International, Inc.

Debt Outstanding: Domestic Non-financial Sectors as of 31 Dec 2005 ($ trillions)

4.70

1.86

9.15

2.35

5.35

2.98

Federal Gov't

State & Local Gov't

Home Mortgage

Other Household

Corporate

Other Business

Source: Federal Reserve

Fixed Income Research

5 © Nomura Securities International, Inc.

Fixed Income Capital Markets Outstanding Bond Market Debt ($ trillions)

0

5

10

15

20

25

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Municipal Treasuries

MBS Corporates

Agency Debt Money Market

ABS Housing

Stocks

Treasuries

MBSCorporates

Munis

Money

Market

ABS

Agencies

Sources: Bond Market Association, Federal Reserve, NYSE, NASD

Fixed Income Research

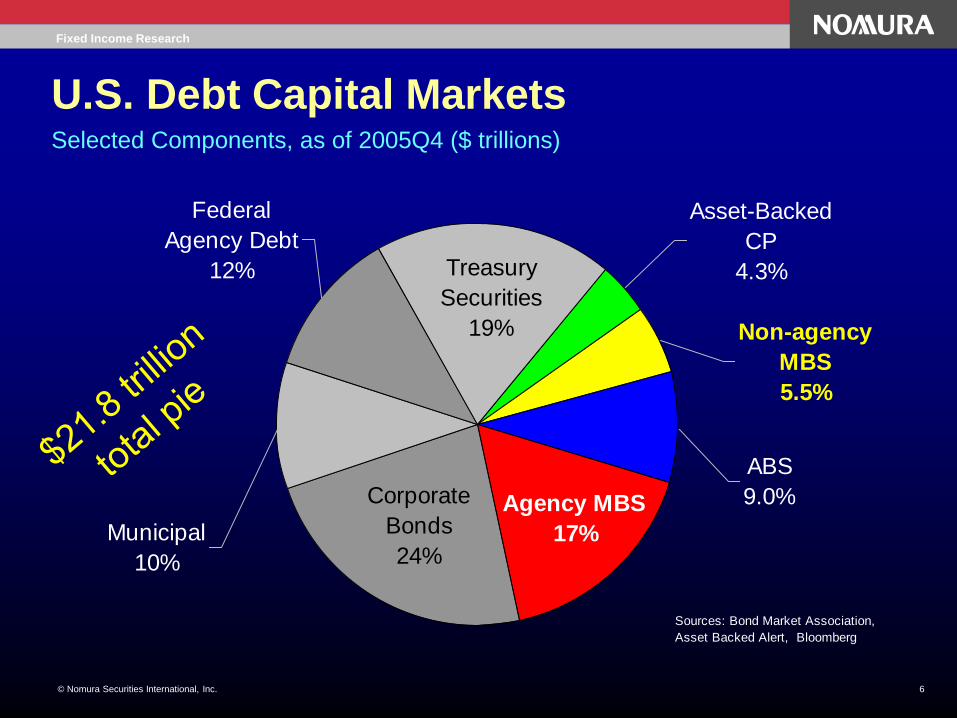

6 © Nomura Securities International, Inc.

U.S. Debt Capital Markets Selected Components, as of 2005Q4 ($ trillions)

Federal

Agency Debt

12%

Corporate

Bonds

24%

Agency MBS

17%Municipal

10%

Asset-Backed

CP

4.3%

Non-agency

MBS

5.5%

ABS

9.0%

Treasury

Securities

19%

Sources: Bond Market Association,

Asset Backed Alert, Bloomberg

Fixed Income Research

7 © Nomura Securities International, Inc.

Securitization Marketplace Outstandings as of 31 Dec 2005

Mobile Homes

Student Loans

Credit Cards

Other

ABS

CMBS

CDOs

GN

MA

FHLMC

Agency-backed

CMOs/REMICs

(double counting)

Non-

agency

MBS

AB

CP

Home Eq(sub-prime)

FNMAVehicles

Sources: Bond Market Association, Asset Backed Alert, Bloomberg, Trepp

Fixed Income Research

8 © Nomura Securities International, Inc.

MBS Issuance Volume

0.3

9

0.5

5

0.7

1

0.3

7

0.3

9

0.5

3 0.7

2

1.2

0

0.5

3

0.4

8

0.4

1

0.5

9

0.8

6

1.1

8

.27

0.0

0.5

1.0

1.5

2.0

2.5

3.01

98

5

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

$ T

rilli

on

s

Non-Agency MBS/ABS

Fannie Mae MBS

Freddie Mac PCs

Ginnie Mae MBS

Sources: Inside MBS & ABS 1/6/06. Note: Non-Agency MBS/ABS includes jumbo, alt-A, and subprime mortgage products.

Fixed Income Research

9 © Nomura Securities International, Inc.

Public ABS Issuance Volume

94 147 208

475

445

65

49

65

67

58

108

82

83

88

86

94

0

100

200

300

400

500

600

700

8001990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

$ B

illio

ns

Other

Vehicles

Credit Cards

Mfd. Housing

Home Equity

Sources: Moody’s, Bloomberg, Asset Securitization Report

Fixed Income Research

10 © Nomura Securities International, Inc.

Mortgage Loan Basics

Traditional loan is 30-year, fixed rate, fully amortizing,

payable monthly, and prepayable at any time

Variations

15-year, 20-year

adjustable interest rate (ARMs)

index

caps

hybrid (fixed/adjustable)

Affordability features: interest only, negative am., 40-year

Specialty mortgage products: alt-A, sub-prime

Fixed Income Research

11 © Nomura Securities International, Inc.

Refinancing: A Valuable Option

Fixed rate loans

When interest rates fall, a borrower can refinance his loan at a

lower interest rate

When interest rates rise, a borrower has the benefit of having

locked-in a lower rate in the past

Floating rate loans

When hybrid loan resets borrower can refinance to new hybrid or

to fixed

When interest rates fall, a borrower has the ability to "permanently"

lock-in the benefit of the low rates by refinancing into a fixed rate

loan

Fixed Income Research

12 © Nomura Securities International, Inc.

Mortgage Loan = A Bond minus an Option

Bond portion: obligation to pay principal and interest in

monthly installments

Option portion: opportunity to "call" (purchase) the bond at

a price of par, at any time

Lender is long the bond and short the option

Borrower is short the bond and long the option

Jargon: Mortgage loan contains an embedded short option

Value of a mortgage loan is the value of the bond minus

the value of the option

Valuing the option is hard to do

Fixed Income Research

13 © Nomura Securities International, Inc.

MBS Basic Features (GSE MBS)

Pass-through security

Monthly collections of interest and principal, including prepayments, "passed through" to investors

Servicer collects payments from borrowers (for a fee)

GSE guarantee protects investors from credit risk on loans

Pass-through rate is like an interest rate on the MBS

Lower than the interest rates on the loans

Difference is the servicing fee plus the guarantee fee

Loans backing an MBS are generally similar

Interest rates

Loan maturities

Fixed Income Research

14 © Nomura Securities International, Inc.

Basic MBS Cash Flow

Homeowners

Servicer

Investors

Monthly P&I at

the mortgage

rate (e.g. 6.5%)

Monthly P&I at

the pass-through

rate (e.g. 6.0%)

Homeowners make monthly

payments of principal and

interest at the mortgage rate.

The servicer retains a portion

of the interest component of

each monthly payment as the

"servicing fee."

The pass-through rate is the

mortgage rate net of the

servicing fee rate.

$

$

Fixed Income Research

15 © Nomura Securities International, Inc.

Ginnie Mae – GNMA

Guarantees securities issued by banks and mortgage

banks that participate in Ginnie Mae programs

Part of HUD

Loans have federal insurance or guarantees (e.g. FHA or

VA; usually low- or moderate income borrowers)

Full faith and credit guarantee

0% risk weight for bank capital

GN I: All loans have same interest rate

GN II: Loan rates in 0.75% band

Competes with sub-prime mortgage ABS for loans

Fixed Income Research

16 © Nomura Securities International, Inc.

Fannie Mae (FNMA) & Freddie Mac (FHLMC)

Private corporations, federally chartered & regulated

Directly issue MBS

Accept conventional mortgage loans < $417,000

Cash and swap programs for lenders

Regular and special servicing

with and without recourse; most sellers choose without

Guarantees its own MBS against credit losses on the underlying loans

Guarantee is not backed by the government

20% risk weight

Loan Interest rates usually in 1.75% band

Fixed Income Research

17 © Nomura Securities International, Inc.

Private-Label MBS

Issued by private companies

No GSE guarantee

Rated securities w/ credit support

Subordinate tranches absorb losses before senior tranches

Mortgage loan credit quality:

Collateral – loan-to-value ratio (LTV)

Credit – credit score (FICO)

Capacity – debt-to-income ratio (DTI)

Jumbo: loans above conforming limit

Alt-A: loans that contain non-standard features but which have borrowers of "A" creditworthiness

Securities backed by sub-prime mortgage loans are classified as "home equity ABS" rather than MBS

Fixed Income Research

18 © Nomura Securities International, Inc.

Reallocating Credit Risk – Tranching

Pool of

Loans

Residual - NR

Class D - Baa2

Class C - A2

Class B -

Aa2

Class A -

Aaa

Underlying Assets Securities

Fir

st L

oss A

lloca

tio

n L

ast

Hig

he

st R

isk L

ow

est

Fixed Income Research

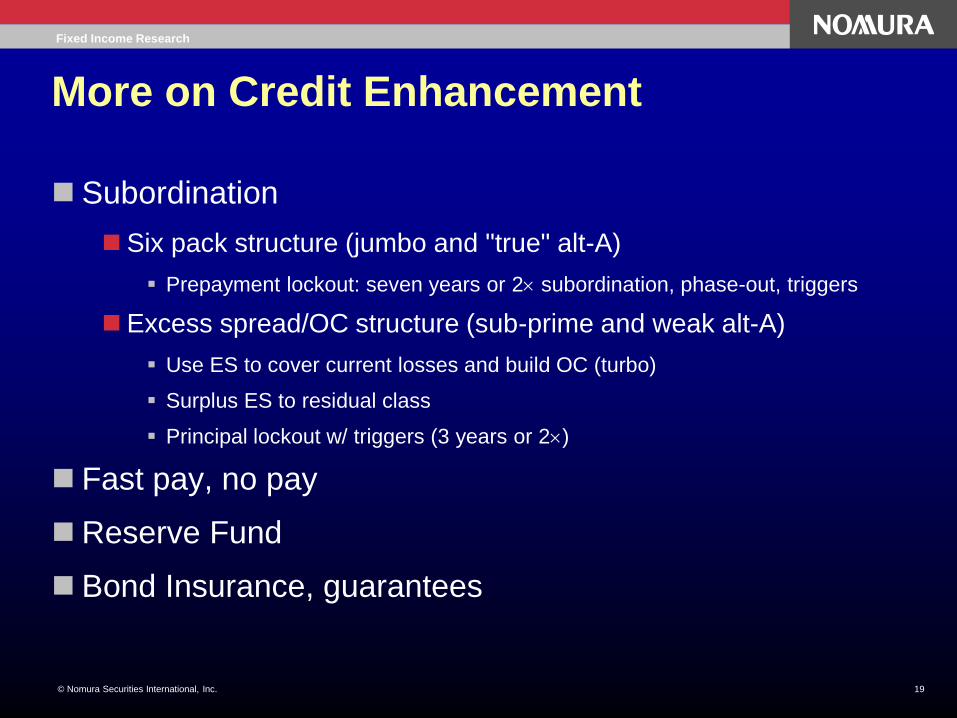

19 © Nomura Securities International, Inc.

More on Credit Enhancement

Subordination

Six pack structure (jumbo and "true" alt-A)

Prepayment lockout: seven years or 2 subordination, phase-out, triggers

Excess spread/OC structure (sub-prime and weak alt-A)

Use ES to cover current losses and build OC (turbo)

Surplus ES to residual class

Principal lockout w/ triggers (3 years or 2)

Fast pay, no pay

Reserve Fund

Bond Insurance, guarantees

Fixed Income Research

20 © Nomura Securities International, Inc.

MBS Trading

TBA (to be announced) pools traded generically

Coupon stack

Cheapest to deliver strategy

Specified pools – investor knows exactly what he will get

but he must pay more and can pick only from what is

available

BloombergSM system provides much information

The whole GSE MBS market settles trades according to a

fixed monthly cycle

Fixed Income Research

21 © Nomura Securities International, Inc.

MBS Valuation

Dynamic analysis

Prepayment models and assumptions

Interest rate simulations

Option adjusted spread (OAS) analysis:

Applies a fixed spread over benchmark interest rates to calculate a

simulated price for the security under each scenario, as well as the

average of the simulated prices across all scenarios

Adjusts the fixed spread and repeats the calculation process until the

average of the simulated prices across all scenarios converges to the

actual market price

Reported OAS is the fixed spread that equates the average of the

simulated prices to the actual market price of the security

MBS values falls when interest rates are more volatile

Private label also must consider credit risk

Fixed Income Research

22 © Nomura Securities International, Inc.

Positive vs. Negative Convexity

$700

$900

$1,100

$1,300

$1,500

$1,700

2% 3% 4% 5% 6% 7% 8% 9% 10%

Market Yields

Price

5 Yr. Bond 10 Yr. Bond

30 Yr. Bond MBS

Fixed Income Research

23 © Nomura Securities International, Inc.

Structure: Prepayments (1) Basic Cash Flows, 30 Year, 7% Mortgage Loan

No Prepayments

Time

Money

Interest

Principal

Fixed Income Research

24 © Nomura Securities International, Inc.

Structure: Prepayments (2) Principal Cash Flows, 30 Year, 7% Mortgage Loan

No Prepayments

Time

Money

Principal

Fixed Income Research

25 © Nomura Securities International, Inc.

Structure: Prepayments (3) Principal Cash Flows, 30 Year, 7% Mortgage Loans

6% CPR 3% CPR

12% CPR 24% CPR

Time

Money

Fixed Income Research

26 © Nomura Securities International, Inc.

Structure: Prepayments (4) Principal Cash Flows, 30 Year, 7% Mortgage Loans

100% PSA 50% PSA

200% PSA 400% PSA

Time

Money

Fixed Income Research

27 © Nomura Securities International, Inc.

Structure: Prepayments (5) Interest Cash Flows, 30 Year, 7% Mortgage Loan

No Prepayments

Time

Money

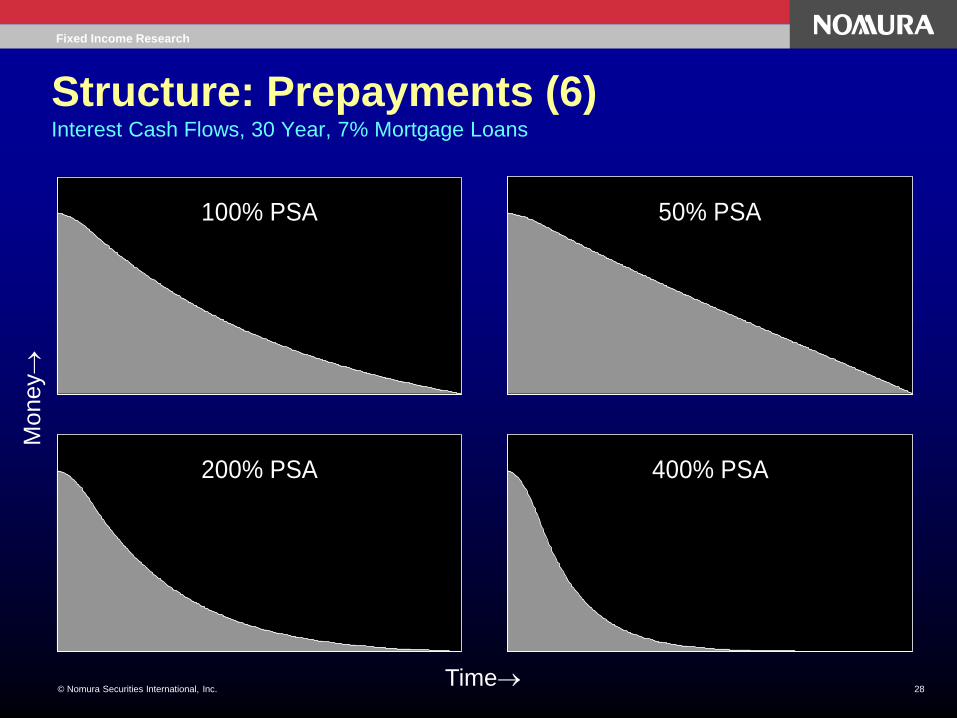

Fixed Income Research

28 © Nomura Securities International, Inc.

Structure: Prepayments (6) Interest Cash Flows, 30 Year, 7% Mortgage Loans

100% PSA 50% PSA

200% PSA 400% PSA

Time

Money

Fixed Income Research

29 © Nomura Securities International, Inc.

CMOs/REMICs

Time-tranching of cash flows

Underlying assets can be GSE MBS, raw mortgage loans,

or other REMIC securities

GSEs issue CMOs/REMICs

Private MBS issuers typically structure all their deals as

CMOs/REMICs

Fixed Income Research

30 © Nomura Securities International, Inc.

Structure: Prepayments (7) Slicing Principal Cash Flows over Time: Building a CMO

165% PSA 165% PSA

350% PSA 75% PSA

Time

Money

Fixed Income Research

31 © Nomura Securities International, Inc.

Treasury Yield Curves

0

1

2

3

4

5

0 5 10 15 20 25 30

Maturity (years)

Yie

ld

12/31/2003

12/31/2004

12/31/2005

03/20/2006

Fixed Income Research

32 © Nomura Securities International, Inc.

Example of Complexity (GM 4L65-E)

Fixed Income Research

33 © Nomura Securities International, Inc.

Structure: Prepayments (8) Shifting Prepayment Risk: Building PAC Classes in a CMO

Defining PAC Cash Flow

The area under both curves

represents the principal cash flow

available at any constant PSA

prepayment rate between the rate of

the upper PAC band and the rate of

the lower PAC band.

165% PSA

PAC A PAC C

PAC E PAC FCompanions

350% PSA 75% PSA

Time

Money

Fixed Income Research

34 © Nomura Securities International, Inc.

Structure: Prepayments (9) Shifting Prepayment Risk: Sensitivity of Companion Classes

165% PSA 165% PSA

Companion G

Companion D

Companion B

PACs

350% PSA 75% PSA

Time

Money

Fixed Income Research

35 © Nomura Securities International, Inc.

Recent Times Have Been Good…

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

-25%

-15%

-5%

5%

15%

25%

Recession

Unemployment %

HY Default Rate

CPI % Change

GNP % Change

Fixed Income Research

36 © Nomura Securities International, Inc.

…But House Prices Are Overheated

-10

-5

0

5

10

15

20

25

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

Ye

ar-

ove

r-Y

ea

r C

ha

ng

e (

%)

USA

Pacific

New England

Mid-Atlantic

South Atlantic

Source: Bloomberg (HPI)

Fixed Income Research

37 © Nomura Securities International, Inc.

Annualized Total Returns by Sector from Citigroup Fixed Income Indices

2.4

%

3.5

%

3.5

% 5.6

%

4.5

%

4.8

%

10

.8%

2.8

%

2.5

%

2.6

%

2.7

%

2.1

%

0.4

%

-0.2

%

0.1

%

2.1

%

2.1

%

2.0

%

1.9

%

-2.2

%

11

.4%

-3%

-1%

1%

3%

5%

7%

9%

11%

13%

ABS Treasury GSE Corporate Inv. Grade MBS High Yield

2004

2005

2006 YTD (3/17/06)

Source: Bloomberg SBCAAB <index>, SBGT <index>, SBGS <index>,

SBCRP <index>, SBBIG <index>, SBMT <index>, SBHYMI <index>.

Fixed Income Research

38 © Nomura Securities International, Inc.

Conclusion

Prepayments are the key to understanding MBS cash

flows, performance and valuations

MBS represent a large portion of all fixed income activity in

the U.S.

MBS represent the largest portion of securitization activity

in the U.S.

No fixed income professional can afford to be ignorant

about MBS

Fixed Income Research

56 © Nomura Securities International, Inc.