mckinsey - mbb time for rationality

TRANSCRIPT

Mobile Data:Time For Rationality

McKinsey Telecom Extranet Webcast

September 23, 2010

1

How to exploitmobile data whileensuringprofitability?

How to exploitmobile data whileensuringprofitability?

Which emergingconsumer trendsin pricing andpackaging?

Which emergingconsumer trendsin pricing andpackaging?

▪ Provide transparencyabout mobile data costsand potential levers toreduce them as a keyenabler to profitability

▪ Review innovativepackaging schemes(pricing, branding,bundling, differentiation…)

▪ Discuss potentialcustomer managementand migration approachesto generate value

Objectives of today’s session

Objectives of today’ssession

What are theoptimal go-to-market strategiesfor dongles vs.smartphones?

What are theoptimal go-to-market strategiesfor dongles vs.smartphones?

Smartphones

Dongles

2

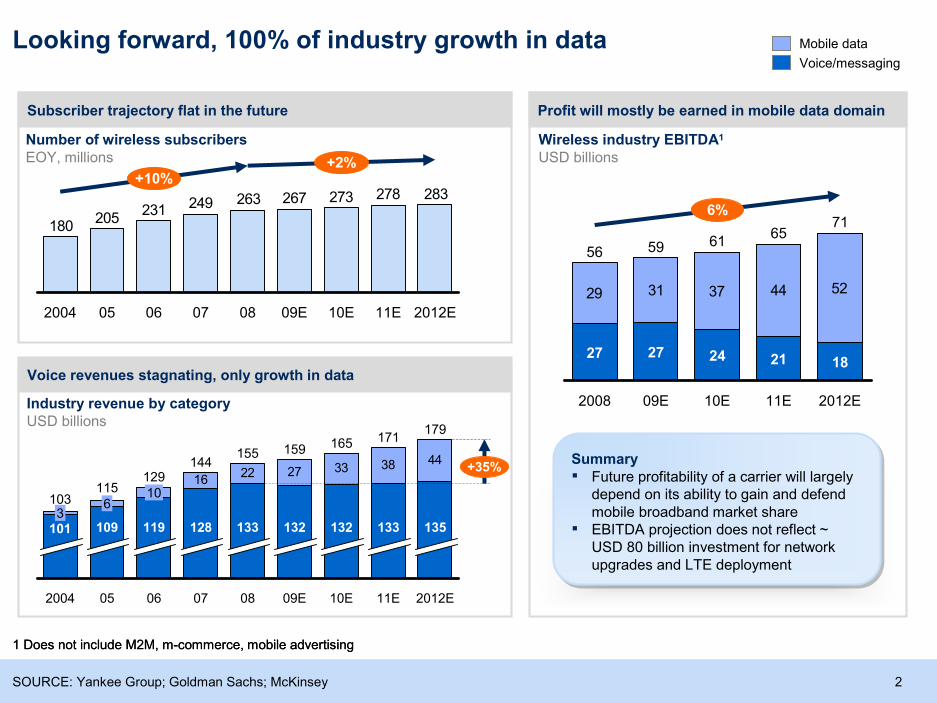

Profit will mostly be earned in mobile data domain

Looking forward, 100% of industry growth in data

SOURCE: Yankee Group; Goldman Sachs; McKinsey

Mobile data

Voice/messaging

1 Does not include M2M, m-commerce, mobile advertising

Subscriber trajectory flat in the future

Number of wireless subscribersEOY, millions

Industry revenue by categoryUSD billions

Wireless industry EBITDA1

USD billions

Voice revenues stagnating, only growth in data

1 Does not include M2M, m-commerce, mobile advertising

283278273267263249231205

180

10E

+2%+10%

2012E11E09E080706052004

22 27 33 38 44

16

133

07

144

133

179

06

129

119

10

05

115

109

6

2004

103

2012E

3

10E

165

135132

11E

128

171

09E

159

132

08

155

101

+35%

29 31 37 44 52

61

6%

2012E

24

71

18

09E

59

11E

27

65

21

2008

56

10E

27

Summary▪ Future profitability of a carrier will largely

depend on its ability to gain and defendmobile broadband market share

▪ EBITDA projection does not reflect ~USD 80 billion investment for networkupgrades and LTE deployment

3

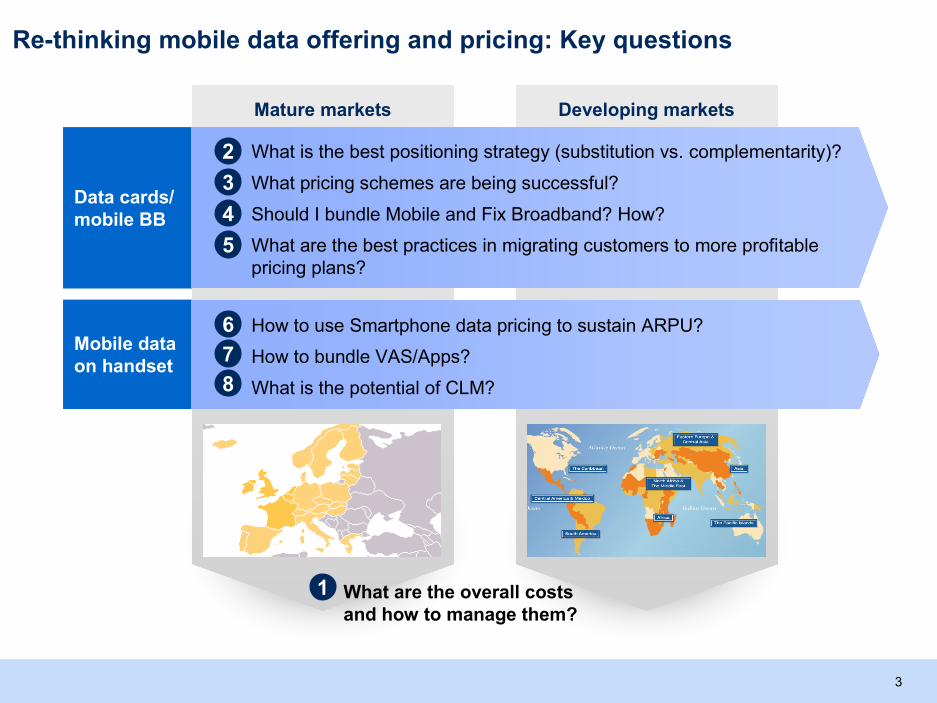

Re-thinking mobile data offering and pricing: Key questions

Developing marketsMature markets

What are the overall costsand how to manage them?

1

Mobile dataon handset

Data cards/mobile BB

What is the best positioning strategy (substitution vs. complementarity)?

What pricing schemes are being successful?

Should I bundle Mobile and Fix Broadband? How?

What are the best practices in migrating customers to more profitablepricing plans?

How to use Smartphone data pricing to sustain ARPU?

How to bundle VAS/Apps?

What is the potential of CLM?

2

3

4

5

6

7

8

4

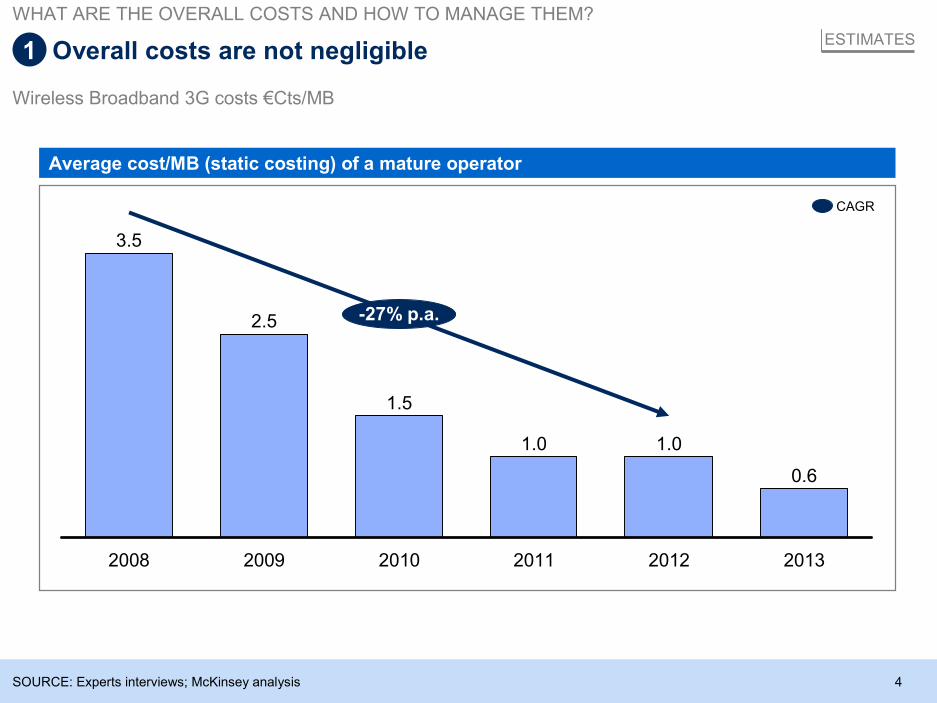

Average cost/MB (static costing) of a mature operator

ESTIMATES

Wireless Broadband 3G costs €Cts/MB

SOURCE: Experts interviews; McKinsey analysis

-27% p.a.

2013

0.6

2012

1.0

2011

1.0

2010

1.5

2009

2.5

2008

3.5

CAGR

Overall costs are not negligible

WHAT ARE THE OVERALL COSTS AND HOW TO MANAGE THEM?

1

5

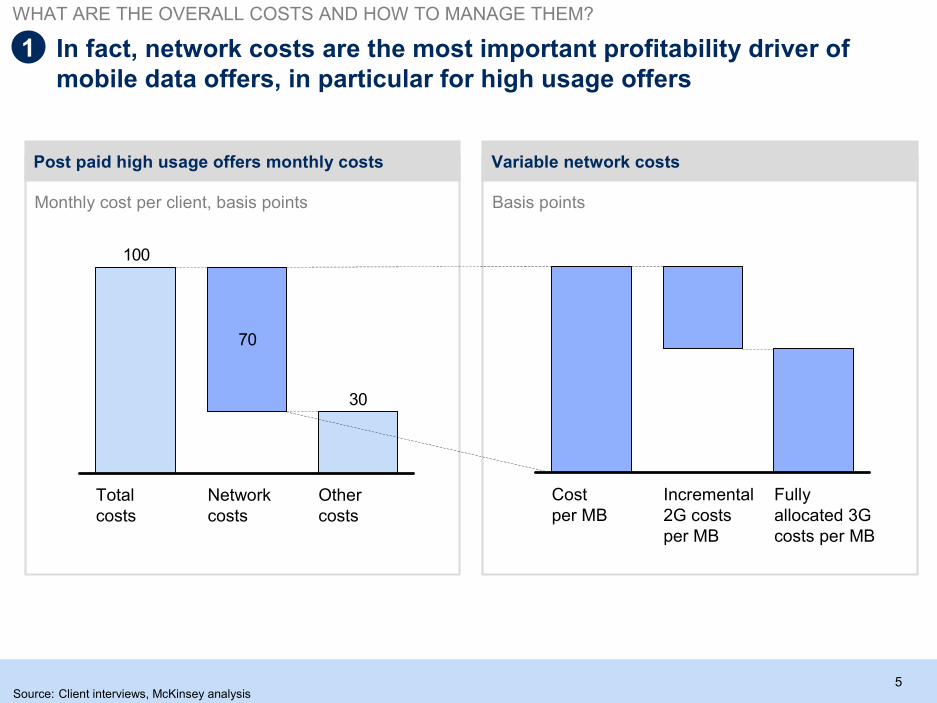

Post paid high usage offers monthly costs

Monthly cost per client, basis points

Variable network costs

Basis points

In fact, network costs are the most important profitability driver ofmobile data offers, in particular for high usage offers

30

70

100

Othercosts

Networkcosts

Totalcosts

Fullyallocated 3Gcosts per MB

Incremental2G costsper MB

Costper MB

Source: Client interviews, McKinsey analysis

1

WHAT ARE THE OVERALL COSTS AND HOW TO MANAGE THEM?

6

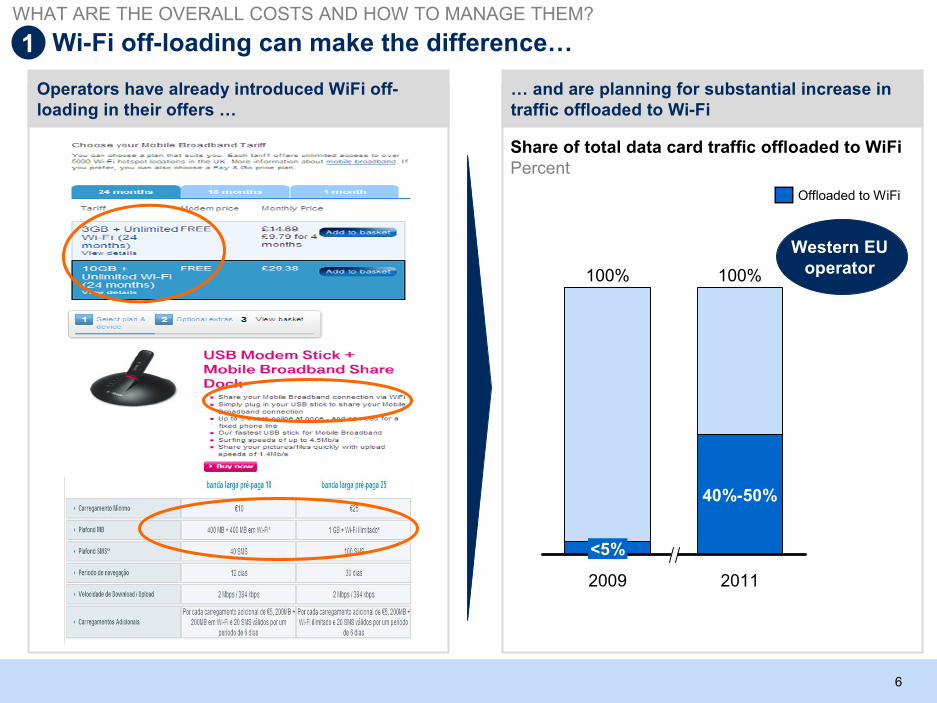

… and are planning for substantial increase intraffic offloaded to Wi-Fi

Operators have already introduced WiFi off-loading in their offers …

Wi-Fi off-loading can make the difference…

Share of total data card traffic offloaded to WiFiPercent

100%

2011

40%-50%

2009

100%

<5%

Western EUoperator

Offloaded to WiFi

1

WHAT ARE THE OVERALL COSTS AND HOW TO MANAGE THEM?

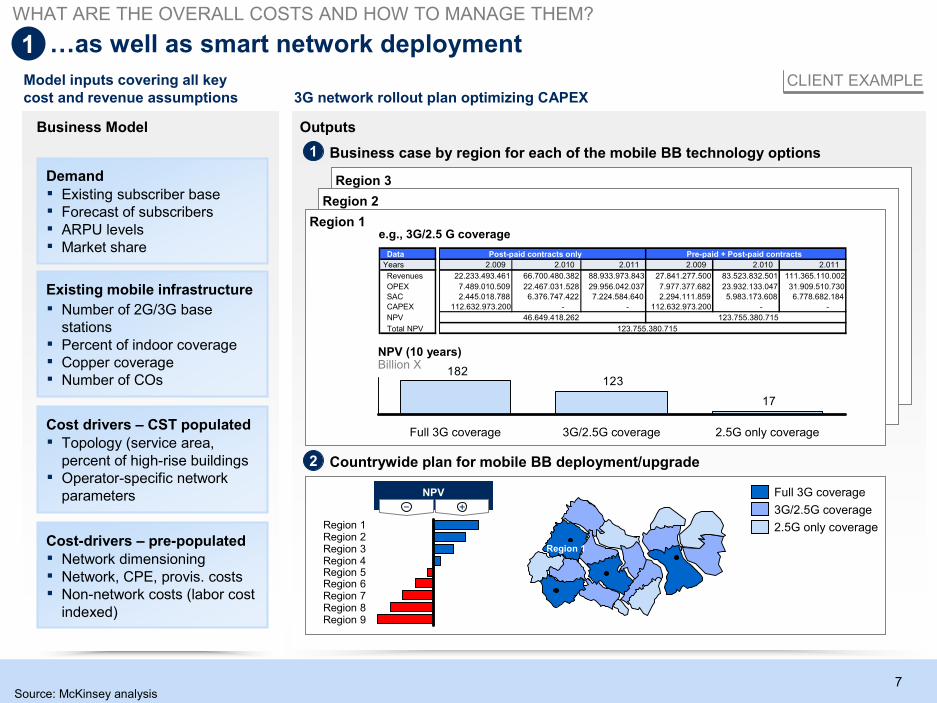

7

Business case by region for each of the mobile BB technology options

Countrywide plan for mobile BB deployment/upgrade

1

2

Region 3

Region 2

Region 1

…as well as smart network deployment

Source: McKinsey analysis

17

123182

NPV (10 years)Billion X

2.5G only coverage3G/2.5G coverageFull 3G coverage

Model inputs covering all keycost and revenue assumptions

Demand

▪ Existing subscriber base▪ Forecast of subscribers▪ ARPU levels▪ Market share

Existing mobile infrastructure

▪ Number of 2G/3G basestations

▪ Percent of indoor coverage▪ Copper coverage▪ Number of COs

Cost drivers – CST populated▪ Topology (service area,

percent of high-rise buildings▪ Operator-specific network

parameters

Cost-drivers – pre-populated▪ Network dimensioning▪ Network, CPE, provis. costs▪ Non-network costs (labor cost

indexed)

Business Model

e.g., 3G/2.5 G coverage

Data

Years 2.009 2.010 2.011 2.009 2.010 2.011

Revenues 22.233.493.461 66.700.480.382 88.933.973.843 27.841.277.500 83.523.832.501 111.365.110.002

OPEX 7.489.010.509 22.467.031.528 29.956.042.037 7.977.377.682 23.932.133.047 31.909.510.730

SAC 2.445.018.788 6.376.747.422 7.224.584.640 2.294.111.859 5.983.173.608 6.778.682.184

CAPEX 112.632.973.200 - - 112.632.973.200 - -

NPV 46.649.418.262 123.755.380.715

Total NPV

Post-paid contracts only Pre-paid + Post-paid contracts

123.755.380.715

3G network rollout plan optimizing CAPEX

Full 3G coverage

3G/2.5G coverage

2.5G only coverage

Region 1

Region 9Region 8Region 7Region 6Region 5Region 4Region 3Region 2Region 1

NPV

1

WHAT ARE THE OVERALL COSTS AND HOW TO MANAGE THEM?

CLIENT EXAMPLE

Outputs

8

MBB positioning will depend on the type of market and player

SOURCE: Interviews

-MatureEmerging “weak fixed” Developing

Market maturity

+

In all WestEuropecountries, offersophistication forcomplementaryusage:▪ Bundles▪ Pre-paid and

low usageoffers

▪ F/Mintegration foroffloadingcapacity

In Ukraine, operatorslaunching aggressiveUSB offer forsubstitution, even onCDMA

In Russia, fixed BBhigh-speed only in somehigh-end areas: mobilein others/rural

In Tanzania, MBBas main internetaccess technology

In South Africa,Vodacom and mobileplayers winning overfixed with MBB

In Turkey, incumbentcatching up in high-speed DSL diffusion,substitution becomingmore “selective”

In Czech Rep., mobileBB growing but oftencomplementary to fixed

In Saudi Arabia., mobileplayers playing aggressivevs. low-speed fixed

In Brazil, aggressiveMBB marketing bymobile only playersleveraging 2.5 assets

2

WHAT IS THE BEST POSITIONING STRATEGY (SUBSTITUTION VS COMPLEMENTARITY)?

CASE EXAMPLES

9

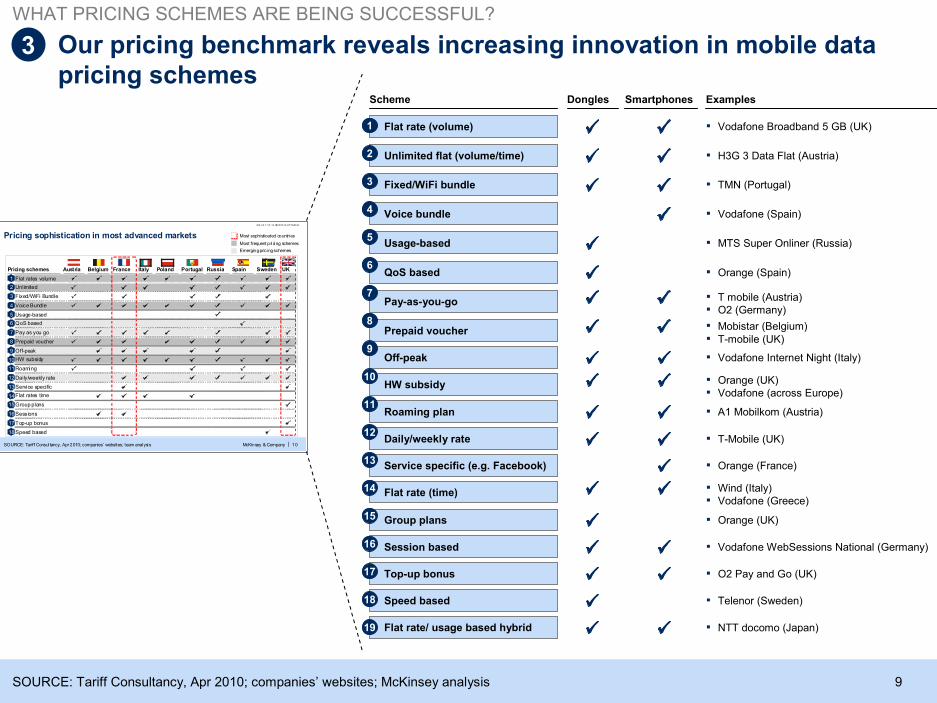

Our pricing benchmark reveals increasing innovation in mobile datapricing schemes

3

McKinsey & Company 10

M IL-24.1 /13 .12- 08022010 -67794/A B

|

Pricing sophistication in most advanced markets

SOURCE: Tariff Consul tancy, Apr 2010; companies’ websites; team analysis

Most sophisticated countries

Most frequent p ricing schemes

Emergingpricingschemes

Pricing schemes

1

Unlimited2

Fixed/WiFi Bundle3

Voice Bundle4

Usage-based5

Prepaid voucher8

Off-peak9

HW subsidy10

Roaming11

Daily/weekly rate12

Service specific13

Flat rates time14

Group plans15

Sessions16

Top-up bonus17

Speed based18

Pay as you go7

QoS based6

Belgium France Portugal RussiaPolandItalyAustria Spain Sweden

Flat rates volume

UK

WHAT PRICING SCHEMES ARE BEING SUCCESSFUL?

SOURCE: Tariff Consultancy, Apr 2010; companies’ websites; McKinsey analysis

▪ TMN (Portugal)

ExamplesSmartphones

▪ Vodafone Broadband 5 GB (UK)

▪ H3G 3 Data Flat (Austria)

▪ Orange (Spain)

▪ MTS Super Onliner (Russia)

▪ Vodafone (Spain)

▪ T mobile (Austria)▪ O2 (Germany)

▪ Mobistar (Belgium)▪ T-mobile (UK)

▪ Vodafone Internet Night (Italy)

▪ Orange (UK)▪ Vodafone (across Europe)

▪ A1 Mobilkom (Austria)

▪ T-Mobile (UK)

▪ Orange (France)

▪ Wind (Italy)▪ Vodafone (Greece)

▪ Orange (UK)

▪ Vodafone WebSessions National (Germany)

▪ O2 Pay and Go (UK)

▪ Telenor (Sweden)

▪ NTT docomo (Japan)

Scheme

Fixed/WiFi bundle

Dongles

Flat rate (volume)

Unlimited flat (volume/time)

QoS based

Usage-based

Voice bundle

Pay-as-you-go

Prepaid voucher

Off-peak

HW subsidy

Roaming plan

Daily/weekly rate

Service specific (e.g. Facebook)

Flat rate (time)

Group plans

Session based

Top-up bonus

Speed based

Flat rate/ usage based hybrid

3

1

2

6

5

4

7

8

9

10

11

12

13

14

15

16

17

18

19

10

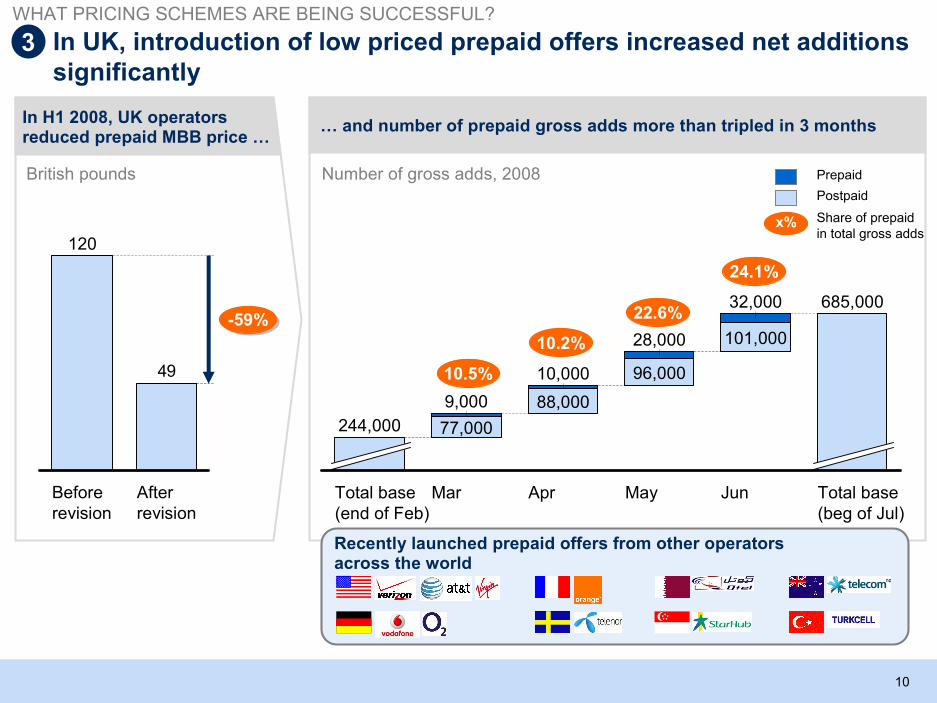

… and number of prepaid gross adds more than tripled in 3 months

In UK, introduction of low priced prepaid offers increased net additionssignificantly

Total base(beg of Jul)

685,000

Jun

101,000

32,000

May

96,000

28,000

Apr

88,000

10,000

Mar

77,000

9,000

Total base(end of Feb)

244,000

Prepaid

Postpaid

Share of prepaidin total gross adds

Number of gross adds, 2008

Recently launched prepaid offers from other operatorsacross the world

In H1 2008, UK operatorsreduced prepaid MBB price …

49

Beforerevision

120

Afterrevision

-59%-59%

British pounds

x%

10.2%

22.6%

24.1%

10.5%

3WHAT PRICING SCHEMES ARE BEING SUCCESSFUL?

11

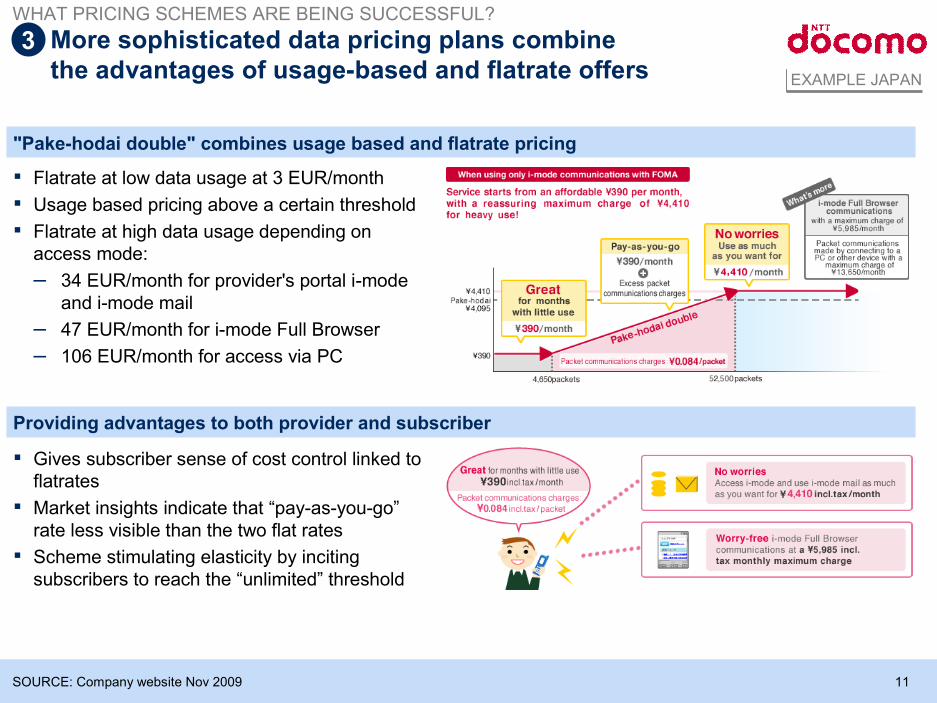

More sophisticated data pricing plans combinethe advantages of usage-based and flatrate offers

SOURCE: Company website Nov 2009

EXAMPLE JAPAN

"Pake-hodai double" combines usage based and flatrate pricing

Providing advantages to both provider and subscriber

▪ Flatrate at low data usage at 3 EUR/month

▪ Usage based pricing above a certain threshold

▪ Flatrate at high data usage depending onaccess mode:

– 34 EUR/month for provider's portal i-modeand i-mode mail

– 47 EUR/month for i-mode Full Browser

– 106 EUR/month for access via PC

▪ Gives subscriber sense of cost control linked toflatrates

▪ Market insights indicate that “pay-as-you-go”rate less visible than the two flat rates

▪ Scheme stimulating elasticity by incitingsubscribers to reach the “unlimited” threshold

3WHAT PRICING SCHEMES ARE BEING SUCCESSFUL?

12

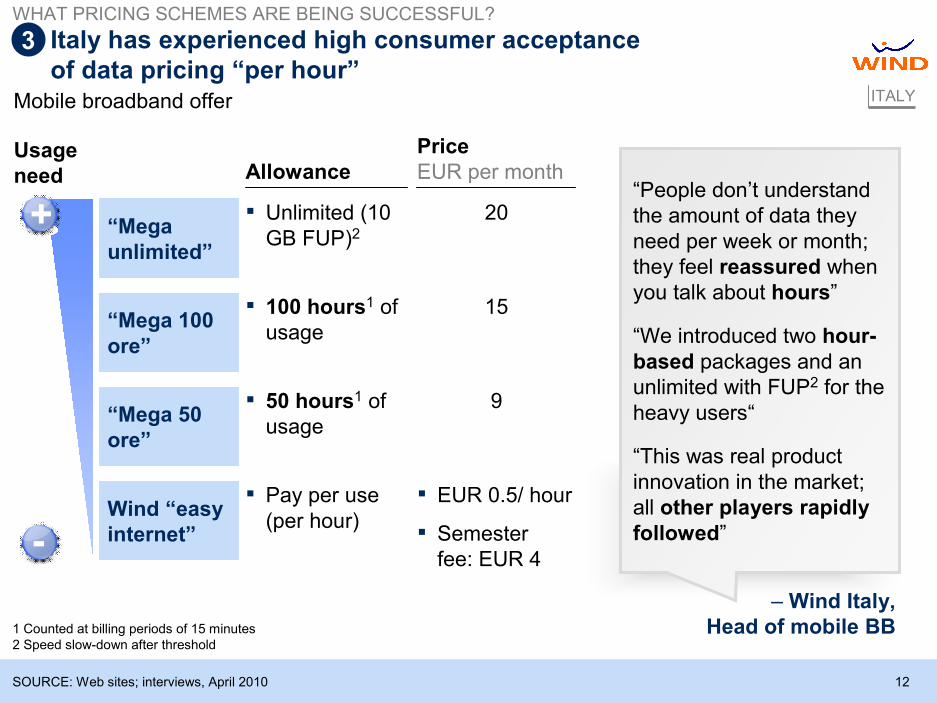

Italy has experienced high consumer acceptanceof data pricing “per hour”

1 Counted at billing periods of 15 minutes2 Speed slow-down after threshold

SOURCE: Web sites; interviews, April 2010

Mobile broadband offer ITALY

Usageneed Allowance

▪ 100 hours1 ofusage

“Mega 100ore”

▪ 50 hours1 ofusage

“Mega 50ore”

▪ Unlimited (10GB FUP)2“Mega

unlimited”

▪ Pay per use(per hour)

Wind “easyinternet”

“People don’t understandthe amount of data theyneed per week or month;they feel reassured whenyou talk about hours”

“We introduced two hour-based packages and anunlimited with FUP2 for theheavy users“

“This was real productinnovation in the market;all other players rapidlyfollowed”

– Wind Italy,Head of mobile BB

PriceEUR per month

15

9

20

▪ EUR 0.5/ hour

▪ Semesterfee: EUR 4

WHAT PRICING SCHEMES ARE BEING SUCCESSFUL?

3

-

+

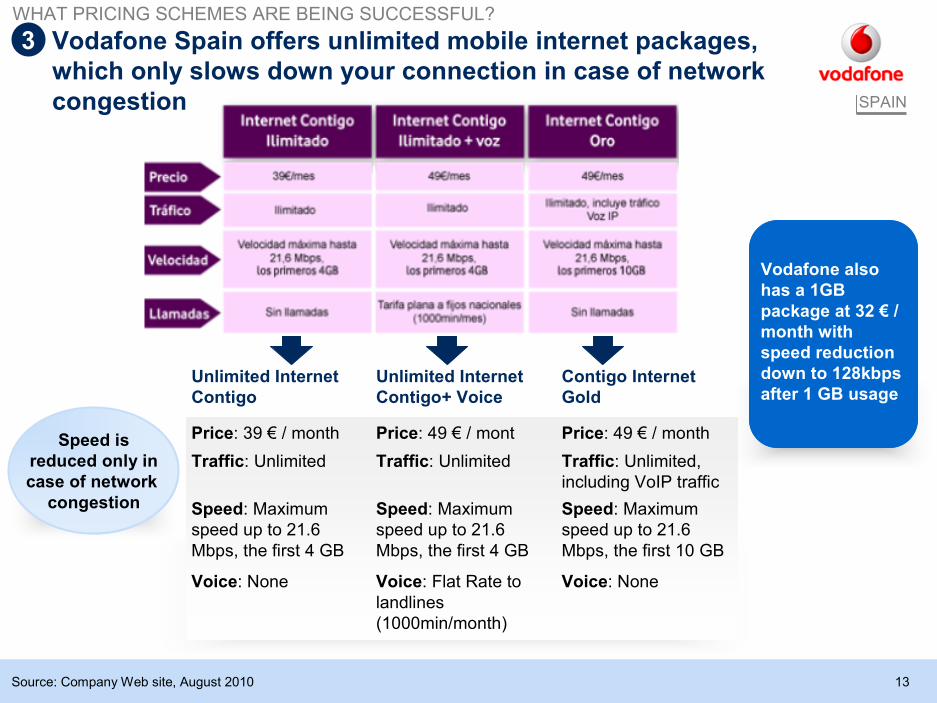

13Source: Company Web site, August 2010

SPAIN

Speed isreduced only incase of network

congestion

WHAT PRICING SCHEMES ARE BEING SUCCESSFUL?

Vodafone Spain offers unlimited mobile internet packages,which only slows down your connection in case of networkcongestion

Unlimited InternetContigo

Price: 39 € / month

Traffic: Unlimited

Speed: Maximumspeed up to 21.6Mbps, the first 4 GB

Voice: None

Unlimited InternetContigo+ Voice

Price: 49 € / mont

Traffic: Unlimited

Speed: Maximumspeed up to 21.6Mbps, the first 4 GB

Voice: Flat Rate tolandlines(1000min/month)

Contigo InternetGold

Price: 49 € / month

Traffic: Unlimited,including VoIP traffic

Speed: Maximumspeed up to 21.6Mbps, the first 10 GB

Voice: None

Vodafone alsohas a 1GBpackage at 32 € /month withspeed reductiondown to 128kbpsafter 1 GB usage

3

14

Maxis in Malaysia follows a more targeted communication strategyfor the heavy users of mobile broadbandMaxis USB modems covered with “cool” sleeves targeting the youth in the country

Maxis organizes musicfests and distributes smallgifts (e.g., goodie bags) to

its young customers

SOURCE: Web search; McKinsey analysis

3WHAT PRICING SCHEMES ARE BEING SUCCESSFUL?

15

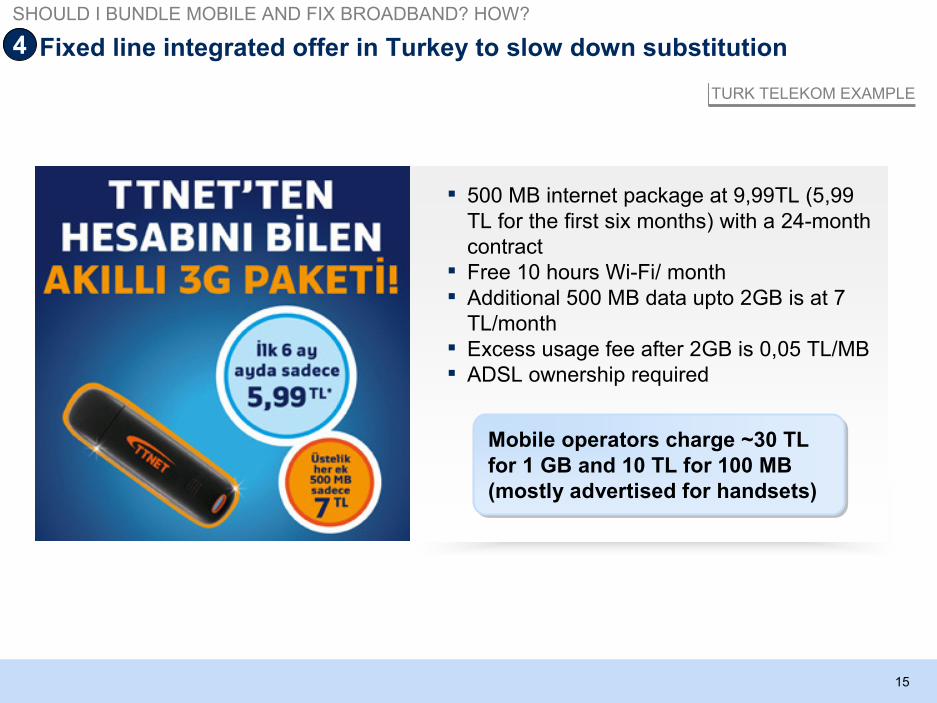

Fixed line integrated offer in Turkey to slow down substitution

▪ 500 MB internet package at 9,99TL (5,99TL for the first six months) with a 24-monthcontract

▪ Free 10 hours Wi-Fi/ month▪ Additional 500 MB data upto 2GB is at 7

TL/month▪ Excess usage fee after 2GB is 0,05 TL/MB▪ ADSL ownership required

Mobile operators charge ~30 TLfor 1 GB and 10 TL for 100 MB(mostly advertised for handsets)

TURK TELEKOM EXAMPLE

4

SHOULD I BUNDLE MOBILE AND FIX BROADBAND? HOW?

16

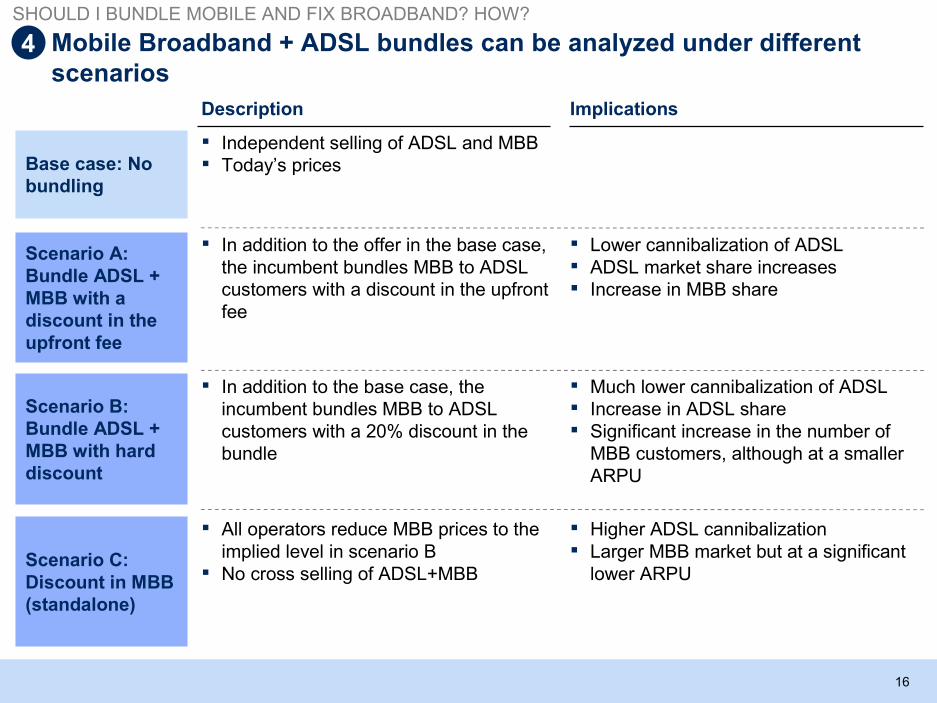

Mobile Broadband + ADSL bundles can be analyzed under differentscenarios

Scenario A:Bundle ADSL +MBB with adiscount in theupfront fee

▪ In addition to the offer in the base case,the incumbent bundles MBB to ADSLcustomers with a discount in the upfrontfee

▪ Lower cannibalization of ADSL▪ ADSL market share increases▪ Increase in MBB share

Description Implications

Scenario B:Bundle ADSL +MBB with harddiscount

▪ In addition to the base case, theincumbent bundles MBB to ADSLcustomers with a 20% discount in thebundle

▪ Much lower cannibalization of ADSL▪ Increase in ADSL share▪ Significant increase in the number of

MBB customers, although at a smallerARPU

Scenario C:Discount in MBB(standalone)

▪ All operators reduce MBB prices to theimplied level in scenario B

▪ No cross selling of ADSL+MBB

▪ Higher ADSL cannibalization▪ Larger MBB market but at a significant

lower ARPU

Base case: Nobundling

▪ Independent selling of ADSL and MBB▪ Today’s prices

4

SHOULD I BUNDLE MOBILE AND FIX BROADBAND? HOW?

17

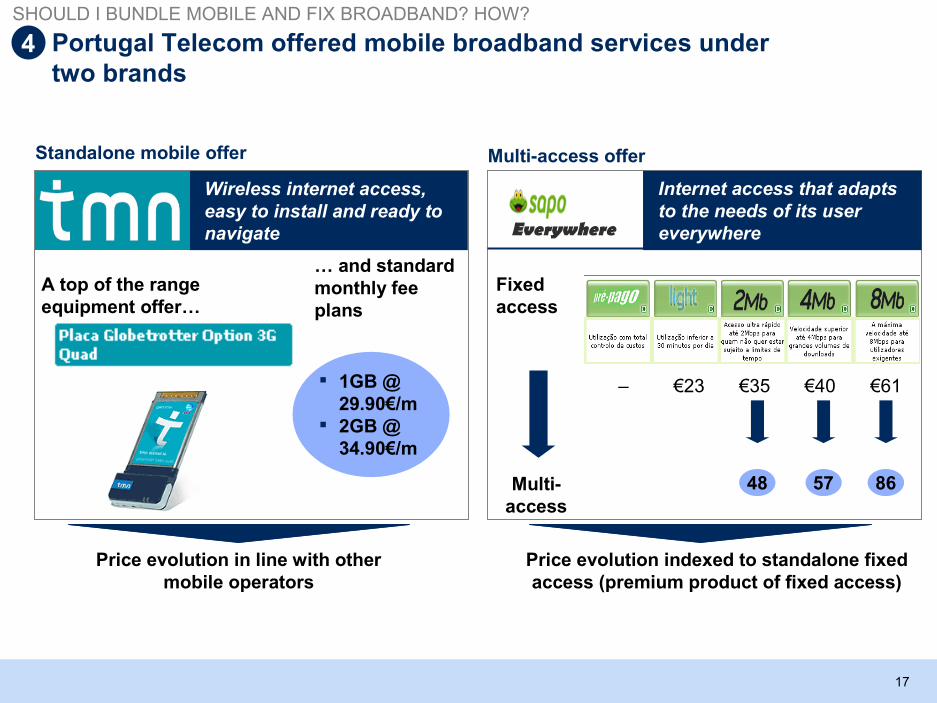

Portugal Telecom offered mobile broadband services undertwo brands

Standalone mobile offer Multi-access offer

Price evolution in line with othermobile operators

Price evolution indexed to standalone fixedaccess (premium product of fixed access)

Wireless internet access,easy to install and ready tonavigate Everywhere

▪ 1GB @29.90€/m

▪ 2GB @34.90€/m

Fixedaccess

– €61€40€35€23

Multi-access

48 57 86

Internet access that adaptsto the needs of its usereverywhere

A top of the rangeequipment offer…

… and standardmonthly feeplans

SHOULD I BUNDLE MOBILE AND FIX BROADBAND? HOW?

4

18

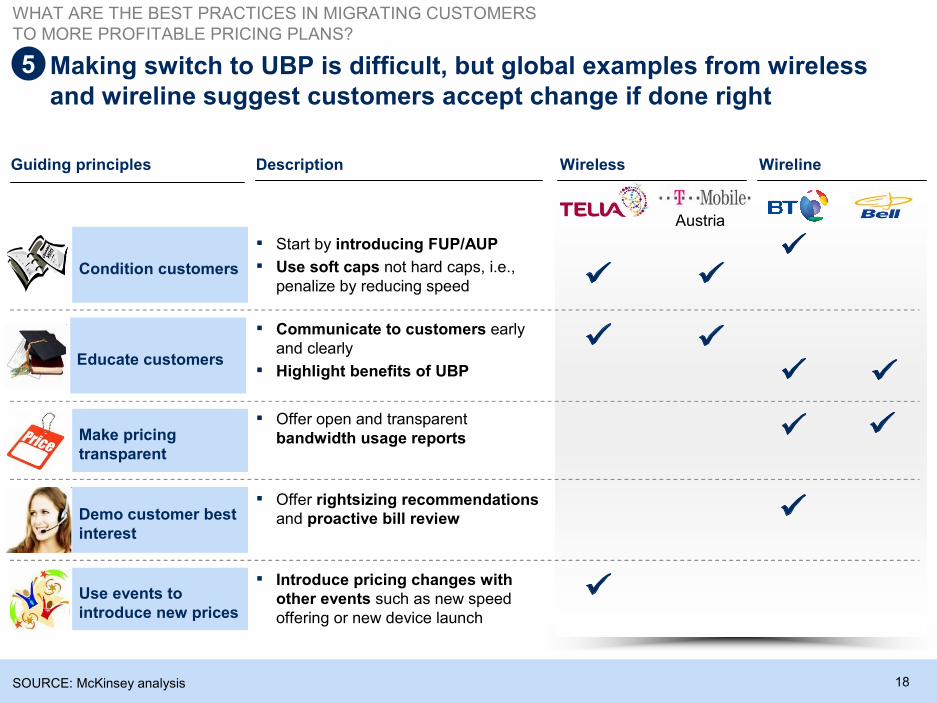

Making switch to UBP is difficult, but global examples from wirelessand wireline suggest customers accept change if done right

Guiding principles Wireless Wireline

Austria

Condition customers

▪ Start by introducing FUP/AUP

▪ Use soft caps not hard caps, i.e.,penalize by reducing speed

Educate customers

▪ Communicate to customers earlyand clearly

▪ Highlight benefits of UBP

Make pricingtransparent

▪ Offer open and transparentbandwidth usage reports

Demo customer bestinterest

▪ Offer rightsizing recommendationsand proactive bill review

Use events tointroduce new prices

▪ Introduce pricing changes withother events such as new speedoffering or new device launch

Description

SOURCE: McKinsey analysis

WHAT ARE THE BEST PRACTICES IN MIGRATING CUSTOMERSTO MORE PROFITABLE PRICING PLANS?

5

19

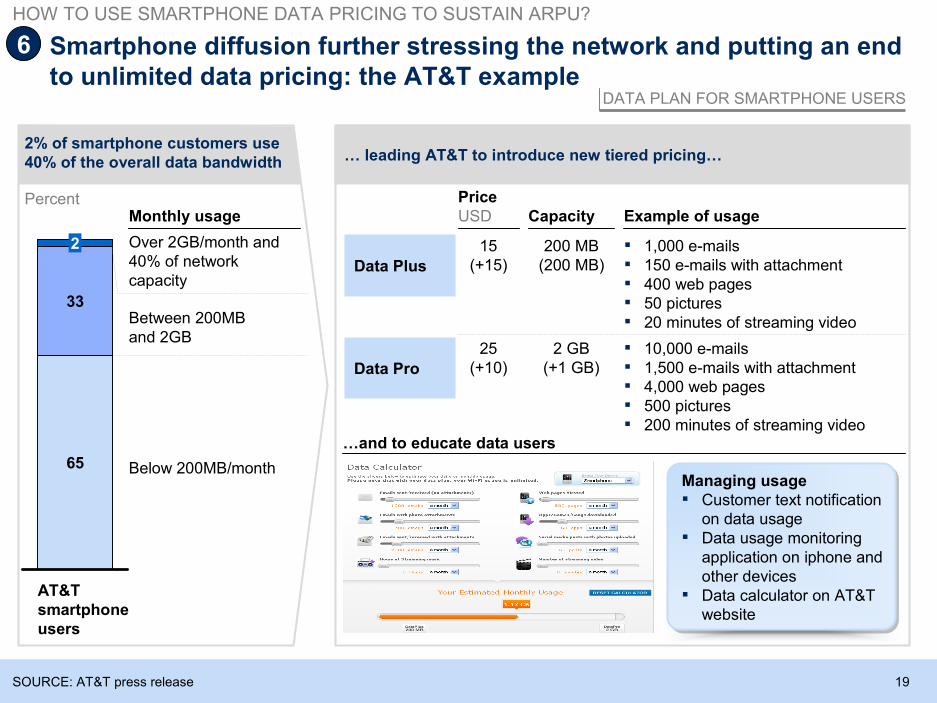

2% of smartphone customers use40% of the overall data bandwidth

Monthly usage

Over 2GB/month and40% of networkcapacity

Between 200MBand 2GB

Below 200MB/month

… leading AT&T to introduce new tiered pricing…

CapacityPriceUSD Example of usage

Data Plus

15(+15)

200 MB(200 MB)

▪ 1,000 e-mails▪ 150 e-mails with attachment▪ 400 web pages▪ 50 pictures▪ 20 minutes of streaming video

Data Pro

25(+10)

2 GB(+1 GB)

▪ 10,000 e-mails▪ 1,500 e-mails with attachment▪ 4,000 web pages▪ 500 pictures▪ 200 minutes of streaming video

…and to educate data users

Managing usage▪ Customer text notification

on data usage▪ Data usage monitoring

application on iphone andother devices

▪ Data calculator on AT&Twebsite

Smartphone diffusion further stressing the network and putting an endto unlimited data pricing: the AT&T example

SOURCE: AT&T press release

AT&Tsmartphoneusers

65

33

2

DATA PLAN FOR SMARTPHONE USERS

6

Percent

HOW TO USE SMARTPHONE DATA PRICING TO SUSTAIN ARPU?

20

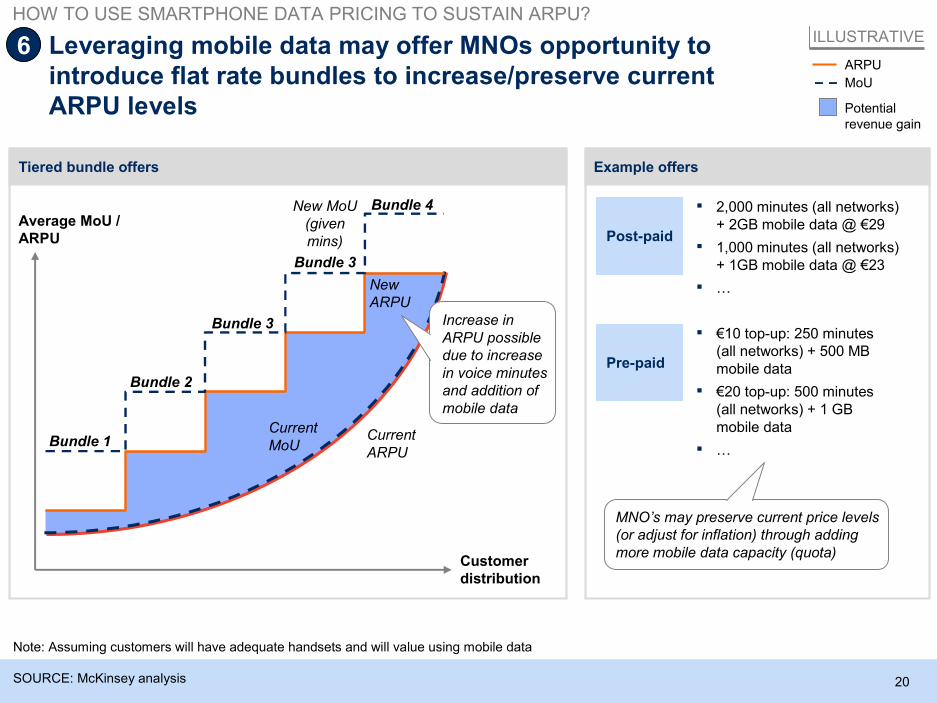

Example offersTiered bundle offers

Leveraging mobile data may offer MNOs opportunity tointroduce flat rate bundles to increase/preserve currentARPU levels

SOURCE: McKinsey analysis

Potentialrevenue gain

ARPU

MoU

ILLUSTRATIVE

▪ 2,000 minutes (all networks)+ 2GB mobile data @ €29

▪ 1,000 minutes (all networks)+ 1GB mobile data @ €23

▪ …

Post-paid

▪ €10 top-up: 250 minutes(all networks) + 500 MBmobile data

▪ €20 top-up: 500 minutes(all networks) + 1 GBmobile data

▪ …

Pre-paid

Average MoU /ARPU

Bundle 1

Bundle 2

Bundle 3

Bundle 4New MoU(givenmins)

CurrentMoU

CurrentARPU

NewARPU

Customerdistribution

Bundle 3

Increase inARPU possibledue to increasein voice minutesand addition ofmobile data

6

MNO’s may preserve current price levels(or adjust for inflation) through addingmore mobile data capacity (quota)

Note: Assuming customers will have adequate handsets and will value using mobile data

HOW TO USE SMARTPHONE DATA PRICING TO SUSTAIN ARPU?

21

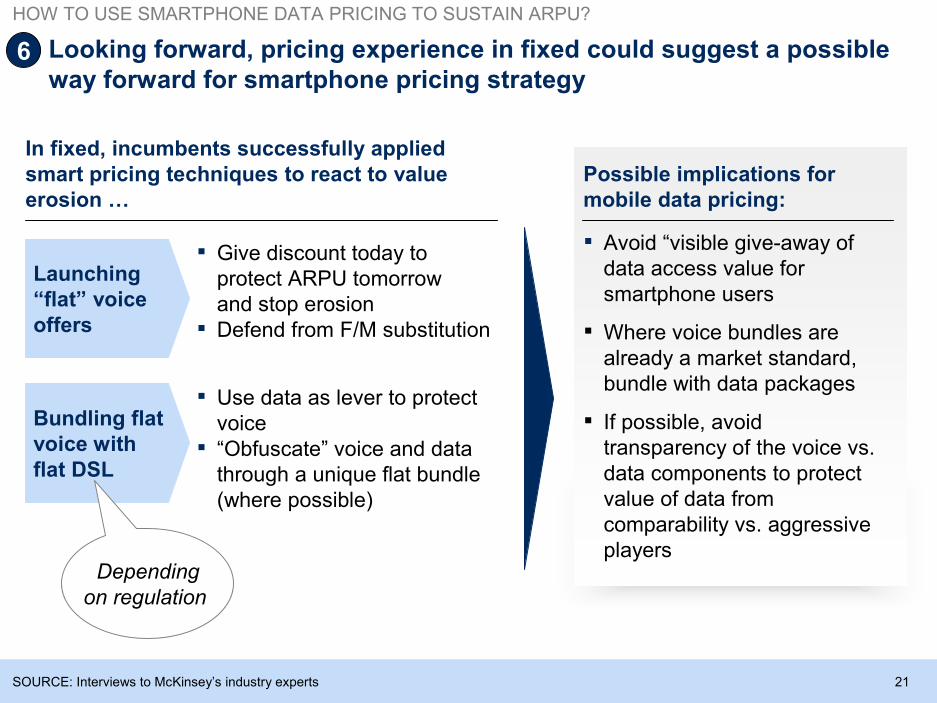

Looking forward, pricing experience in fixed could suggest a possibleway forward for smartphone pricing strategy

SOURCE: Interviews to McKinsey’s industry experts

Possible implications formobile data pricing:

▪ Avoid “visible give-away ofdata access value forsmartphone users

▪ Where voice bundles arealready a market standard,bundle with data packages

▪ If possible, avoidtransparency of the voice vs.data components to protectvalue of data fromcomparability vs. aggressiveplayers

In fixed, incumbents successfully appliedsmart pricing techniques to react to valueerosion …

Launching“flat” voiceoffers

▪ Give discount today toprotect ARPU tomorrowand stop erosion

▪ Defend from F/M substitution

Bundling flatvoice withflat DSL

▪ Use data as lever to protectvoice

▪ “Obfuscate” voice and datathrough a unique flat bundle(where possible)

Dependingon regulation

6

HOW TO USE SMARTPHONE DATA PRICING TO SUSTAIN ARPU?

22

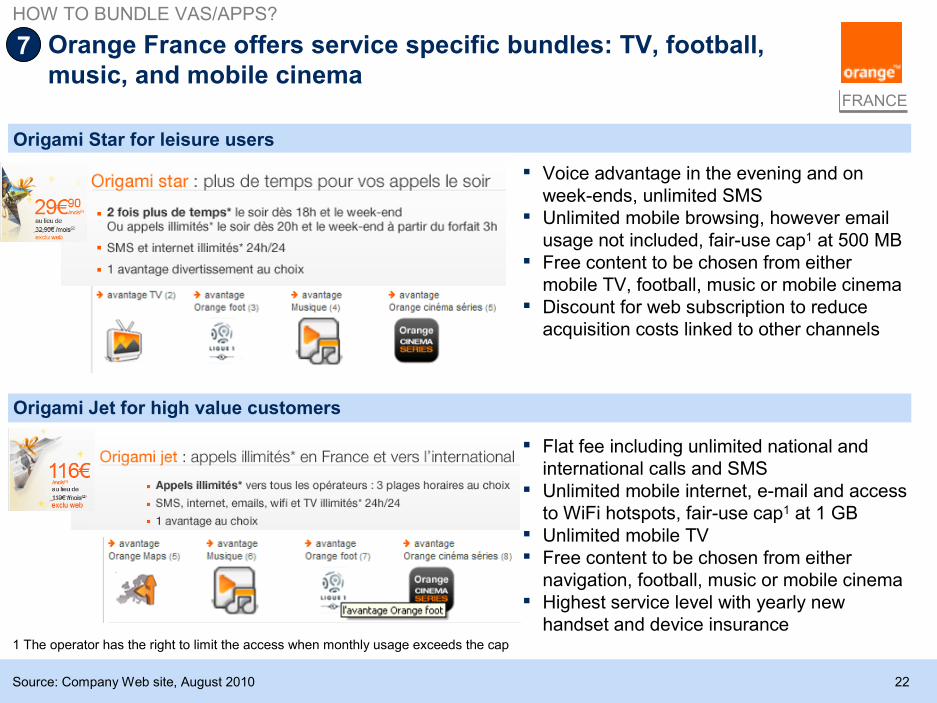

▪ Voice advantage in the evening and onweek-ends, unlimited SMS

▪ Unlimited mobile browsing, however emailusage not included, fair-use cap1 at 500 MB

▪ Free content to be chosen from eithermobile TV, football, music or mobile cinema

▪ Discount for web subscription to reduceacquisition costs linked to other channels

FRANCE

Origami Star for leisure users

Origami Jet for high value customers

▪ Flat fee including unlimited national andinternational calls and SMS

▪ Unlimited mobile internet, e-mail and accessto WiFi hotspots, fair-use cap1 at 1 GB

▪ Unlimited mobile TV▪ Free content to be chosen from either

navigation, football, music or mobile cinema▪ Highest service level with yearly new

handset and device insurance

Source: Company Web site, August 2010

1 The operator has the right to limit the access when monthly usage exceeds the cap

Orange France offers service specific bundles: TV, football,music, and mobile cinema

HOW TO BUNDLE VAS/APPS?

7

23

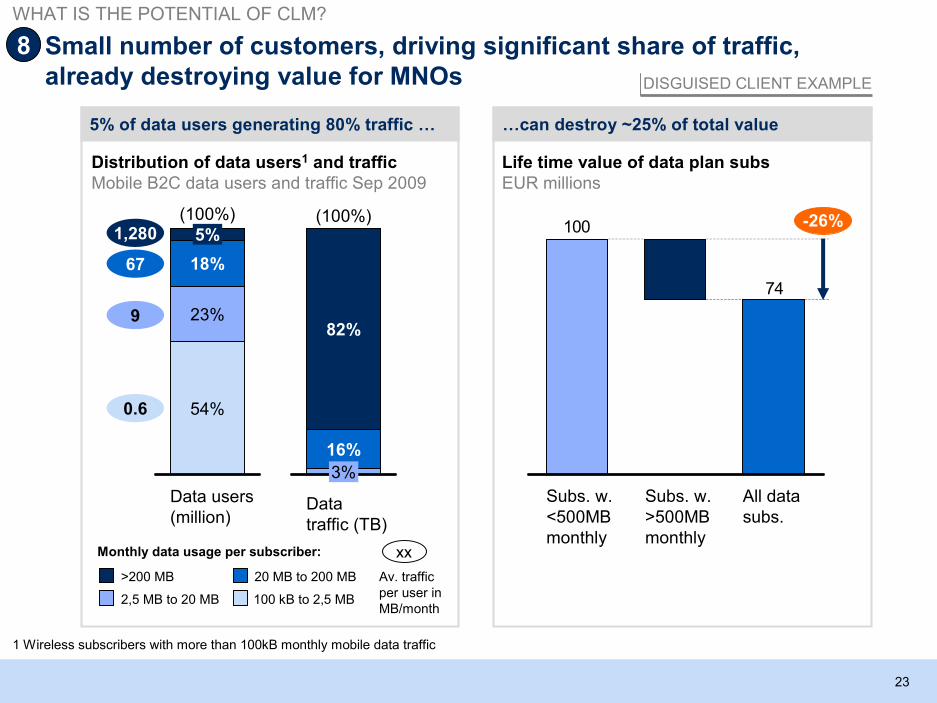

5% of data users generating 80% traffic … …can destroy ~25% of total value

Life time value of data plan subsEUR millions

Small number of customers, driving significant share of traffic,already destroying value for MNOs

74

100

All datasubs.

Subs. w.>500MBmonthly

Subs. w.<500MBmonthly

-26%

Distribution of data users1 and trafficMobile B2C data users and traffic Sep 2009

1,280

67

9

0.6

Data users(million)

(100%)

54%

23%

18%

5%

Datatraffic (TB)

(100%)

3%

16%

82%

Monthly data usage per subscriber:

2,5 MB to 20 MB

20 MB to 200 MB

100 kB to 2,5 MB

>200 MB

xx

Av. trafficper user inMB/month

1 Wireless subscribers with more than 100kB monthly mobile data traffic

DISGUISED CLIENT EXAMPLE

8

WHAT IS THE POTENTIAL OF CLM?

24

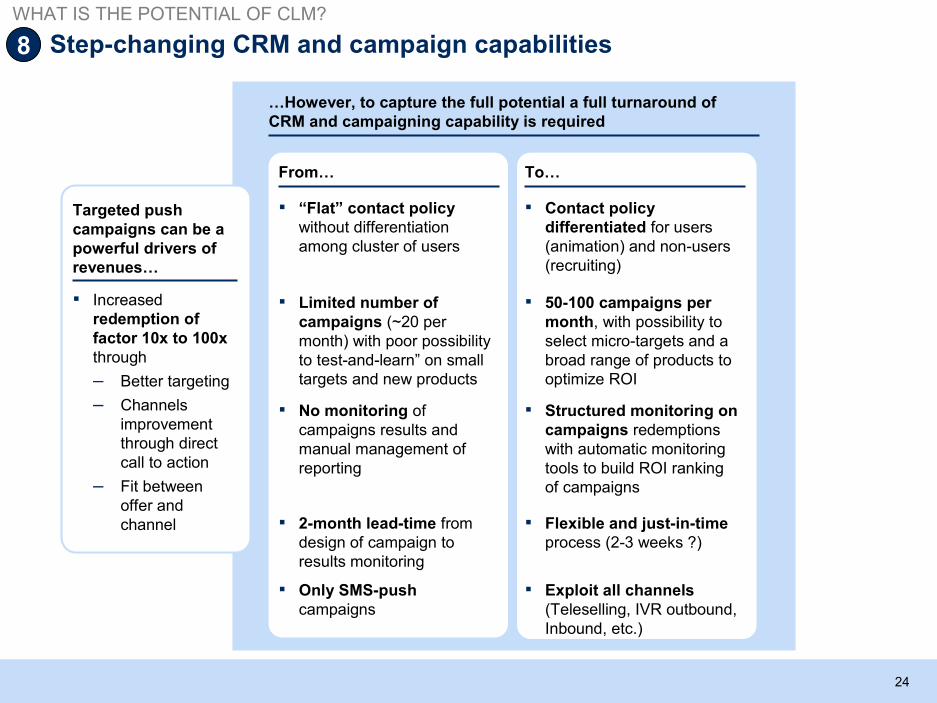

Step-changing CRM and campaign capabilities

WHAT IS THE POTENTIAL OF CLM?

8

…However, to capture the full potential a full turnaround ofCRM and campaigning capability is required

From… To…

▪ “Flat” contact policywithout differentiationamong cluster of users

▪ Contact policydifferentiated for users(animation) and non-users(recruiting)

▪ Limited number ofcampaigns (~20 permonth) with poor possibilityto test-and-learn” on smalltargets and new products

▪ 50-100 campaigns permonth, with possibility toselect micro-targets and abroad range of products tooptimize ROI

▪ No monitoring ofcampaigns results andmanual management ofreporting

▪ Structured monitoring oncampaigns redemptionswith automatic monitoringtools to build ROI rankingof campaigns

▪ 2-month lead-time fromdesign of campaign toresults monitoring

▪ Flexible and just-in-timeprocess (2-3 weeks ?)

▪ Only SMS-pushcampaigns

▪ Exploit all channels(Teleselling, IVR outbound,Inbound, etc.)

Targeted pushcampaigns can be apowerful drivers ofrevenues…

▪ Increasedredemption offactor 10x to 100xthrough

– Better targeting

– Channelsimprovementthrough directcall to action

– Fit betweenoffer andchannel

25

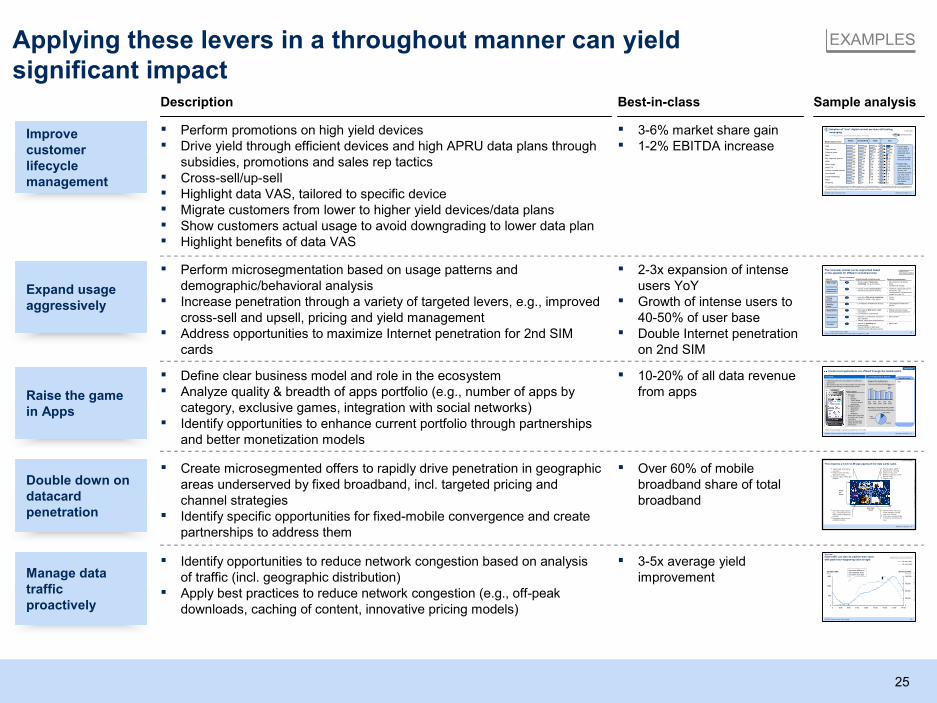

Applying these levers in a throughout manner can yieldsignificant impact

Description

Expand usageaggressively

Best-in-class

▪ Perform microsegmentation based on usage patterns anddemographic/behavioral analysis

▪ Increase penetration through a variety of targeted levers, e.g., improvedcross-sell and upsell, pricing and yield management

▪ Address opportunities to maximize Internet penetration for 2nd SIMcards

▪ 2-3x expansion of intenseusers YoY

▪ Growth of intense users to40-50% of user base

▪ Double Internet penetrationon 2nd SIM

Manage datatrafficproactively

▪ Identify opportunities to reduce network congestion based on analysisof traffic (incl. geographic distribution)

▪ Apply best practices to reduce network congestion (e.g., off-peakdownloads, caching of content, innovative pricing models)

▪ 3-5x average yieldimprovement

Raise the gamein Apps

▪ Define clear business model and role in the ecosystem▪ Analyze quality & breadth of apps portfolio (e.g., number of apps by

category, exclusive games, integration with social networks)▪ Identify opportunities to enhance current portfolio through partnerships

and better monetization models

▪ 10-20% of all data revenuefrom apps

Improvecustomerlifecyclemanagement

▪ Perform promotions on high yield devices▪ Drive yield through efficient devices and high APRU data plans through

subsidies, promotions and sales rep tactics▪ Cross-sell/up-sell▪ Highlight data VAS, tailored to specific device▪ Migrate customers from lower to higher yield devices/data plans▪ Show customers actual usage to avoid downgrading to lower data plan▪ Highlight benefits of data VAS

▪ 3-6% market share gain▪ 1-2% EBITDA increase

Sample analysis

EXAMPLES

56

Wo

rkin

gD

raft-L

ast

Mo

difie

d0

8/05/2

01

007

:27:4

7P

rinte

d0

7/0

5/201

01

7:0

9:06

3G voice trafficMinutes

75,000

50,000

25,000

100,000

0

3G data trafficMbps

500

1,500

1,000

00 12:00 24:0018:006:00 9:00 15:00 21:003:00

3G voice traffic

3G data traffic

DISGUISED CLIENT EXAMPLEData traffic can also be peakier than voice,with peak hour happening later at night

SOURCE: Client interv iews; Team analysis

Important differencealso between weekand week-end days

Short-term

45

Wo

rkin

gD

raft-L

ast

Mo

difie

d0

8/05/2

01

007

:36:1

1P

rinte

d0

7/0

5/201

01

7:0

9:06

Handsets

* France, Germany, U.K., Spain

Sources: Segmentation derived from Telecom Customer Insight Survey, 2008

CASE STUDY,WESTERN EUROPE

Share of consumers*%Segment Attitude toward content/services Other key characteristics

28“Web socials”▪ Strong usage of “Web social

networking”, IM, photo sharing,…▪ More “techies” and “fashion-

driven”▪ Younger than average

20 ▪ Utilizing mostly e-mails/calendars▪ Adverse to web social networking

▪ Traditional usage of devices (TV,fixed phone, etc.)

▪ Low penetration of entertainmentcontent (e.g., pay-TV)

“Conservativeprofessionals”

13 ▪ Keen about Web social networking▪ Appetite for music, video, games

▪ Young▪ Female

“Youngsocials”

12 ▪ Low utilization of fixed/home services ▪ Low utilization of fixed/homedevices

“Mobility-driven”

11 ▪ High usage of Web search, news,e-commerce

▪ Low interest for entertainment

▪ Slightly older than average▪ Somehow biased toward fixed

“Utility-driven”

11 ▪ Rejection of “professional ” services (e-mail, calendar)

▪ “Neutral” about other content/services

▪ Mostly female“Housewives”

▪ Appetite for gambling andringtones/logos

▪ Very low interest for Web socialnetworking and professional services

▪ Mostly male5“Frivolous”

The consumer market can be segmented basedon the appetite for different content/services

Double down ondatacardpenetration

▪ Create microsegmented offers to rapidly drive penetration in geographicareas underserved by fixed broadband, incl. targeted pricing andchannel strategies

▪ Identify specific opportunities for fixed-mobile convergence and createpartnerships to address them

▪ Over 60% of mobilebroadband share of totalbroadband

McKinsey & Company 6

Wo

rkin

gD

raft

-La

stM

od

ified

24/0

3/201

01

2:17:09

PM

Prin

ted

11

/02/2

010

13

:00:29

|

Aware Considered Tried UseMobile data service

▪ For pre-paidusers usage islower than forpost-paid users,howeverconversion ratesare quite similar

▪ Despite highawareness, trialrates continue tobe very lowacross the board.e.g. only 1 pre-paid user in 10has tried to usethe mobileinternet

SMS

Take pictures

Listen to music

Buy ringtones, games

MMS

Watch TV

93

92

97

Watch video

87

95

97

MSN

89

95

97

79

Search / browse internet

93

88

Send emails

Social Networking

Maps

82Shopping

54

59

69

72

83

29

31

36

44

48

36

42

49

62

57

42

77

39

13

14

18

22

27

19

29

24

6

7

8

9

10

12

13

13

20

20

43

48

5976%

XX% Conversion rate

77%

75%

47%

51%

46%

53%

64%

38%

41%

47%

48%

52%

Q72 - For each of the following mobile serv ices, please choose one of the following statements: (1) I have not heard of this serv ice, (2) I am aware of thisserv ice but have never considered using it, (3) I have considere d using this service on my phone but have not yet tried it, (4) I have tried this service onmy phone but rarely use it, or (5) I use this service regularly (e.g. few times a month) on my phone

PRE-PAID

SOURCE: LatAm mobile panel 2010

Adoption of “true” digital content services still trailingmessaging

2

% of respondents, post -paid users only, (N = 980)

McKinsey & Company 21|

The portals...

Content and applications are offered through the mobile portal

1 Based on surveys among x-y subscribers using internet on their mobile

SOURCE: Company website, interviews, Up-To-Data panelJune 2009

Aggregation

May2008

Nov2008

Aug2008

Feb2009

May2009

A

B

Usage of the mobile portalPercent of mobile data users1

Veryunlikely

Neutral

Very likely

Would you recommend the portal?% of mobile portal users1 - May 2009

...are not perceived as attractive

▪ Startpage:– News– Weather– Traffic update– Links to sites and

applications▪ Download section:

– Applications– Wallpapers– Music– Ringtones

▪ Email section with linksto emailing and instantmessaging

▪ Personal space withbilling and price planinformations

Portal content

▪ Partnership with xx for vast majority of content andapplications

▪ The company gets x% of revenue share from the partner▪ Billing is done through a company billing system

Key take-aways

▪ TBD

|McKinsey & Company 34

SPO-TFN386-20090206

Work

ingD

raft

-Last

Mo

dified

06/02

/200

90

9:02:0

0Prin

ted

7/2

/20

0901

:46:3

3

This requires a more CLM type approach for data cards sales

? Tighten data l imits and f air

use policy? Restr ict video and mus ic

application us ages

? Upsell to higher ARPU dataproducts

? Promote higher ARPU

products (e.g., roaming)

? Cross-sel l v oice and

WLAN t o maximise ov erallli fecycle value

? Target f or VAS

? Pus h dif ferentiated pricing

(e.g., cheap off-peak , best

effort speeds, limited hoursper day)

? Enc ourage higher use onprofitable products

? Seek out more users (e.g.,

senior managers, secondcard while roaming)

? Cros s-sel l v oic e and WLANto maximise overall lifecycle

value

Usage

per

month

L ow

Hi gh

Sp en d per

month

L ow Hig h

Upsel l to retai nContr ol & upsell

D rive for profitability Seek out & pr omote

26

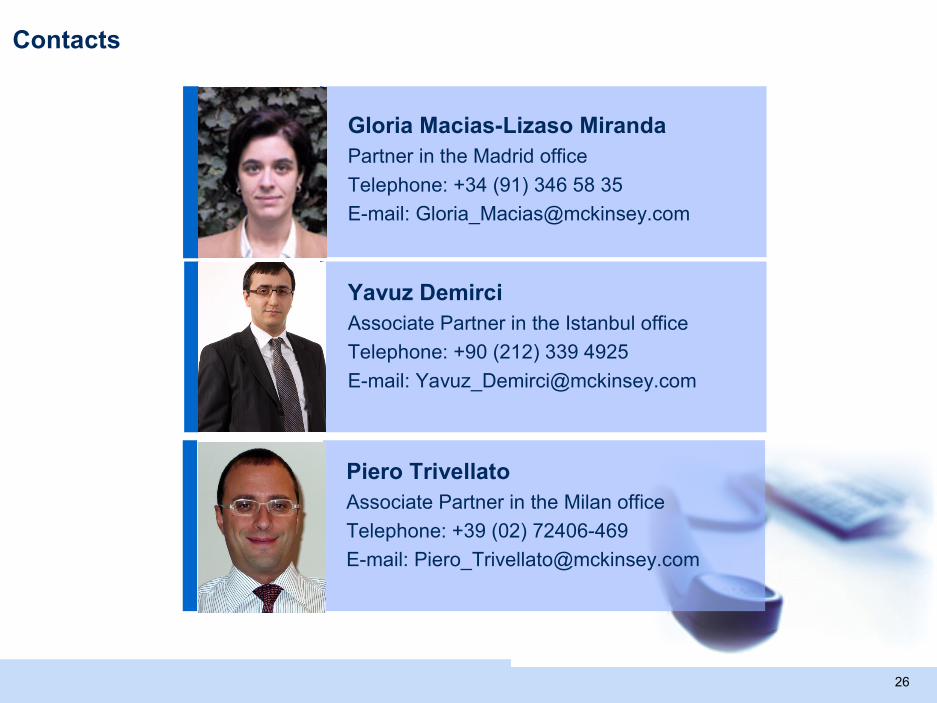

Contacts

Gloria Macias-Lizaso Miranda

Partner in the Madrid office

Telephone: +34 (91) 346 58 35

E-mail: [email protected]

Yavuz Demirci

Associate Partner in the Istanbul office

Telephone: +90 (212) 339 4925

E-mail: [email protected]

Piero Trivellato

Associate Partner in the Milan office

Telephone: +39 (02) 72406-469

E-mail: [email protected]

27

Have a question for thepresenters? Type it by

pressing the “Submit question”button – We will answer as

many as time permits