measuring rate and return

TRANSCRIPT

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 1/45

MEASURING RISK AND RETURN

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 2/45

I. PORTFOLIO THEORY

´ How does investor decide among group of

assets?

´

assume: investors are risk averse« additional compensation for risk

« tradeoff between risk and expected return

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 3/45

GOAL

´ efficient or optimal portfolio

« for a given risk, maximize exp. return

«

OR« for a given exp. return, minimize the risk

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 4/45

TOOLS

´ measure risk, return

´ quantify risk/return tradeoff

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 5/45

return = R =change in asset value + income

initial value

MEASURING RETURN

´ R is ex post

« based on past data, and is known

´ R is typically annualized

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 6/45

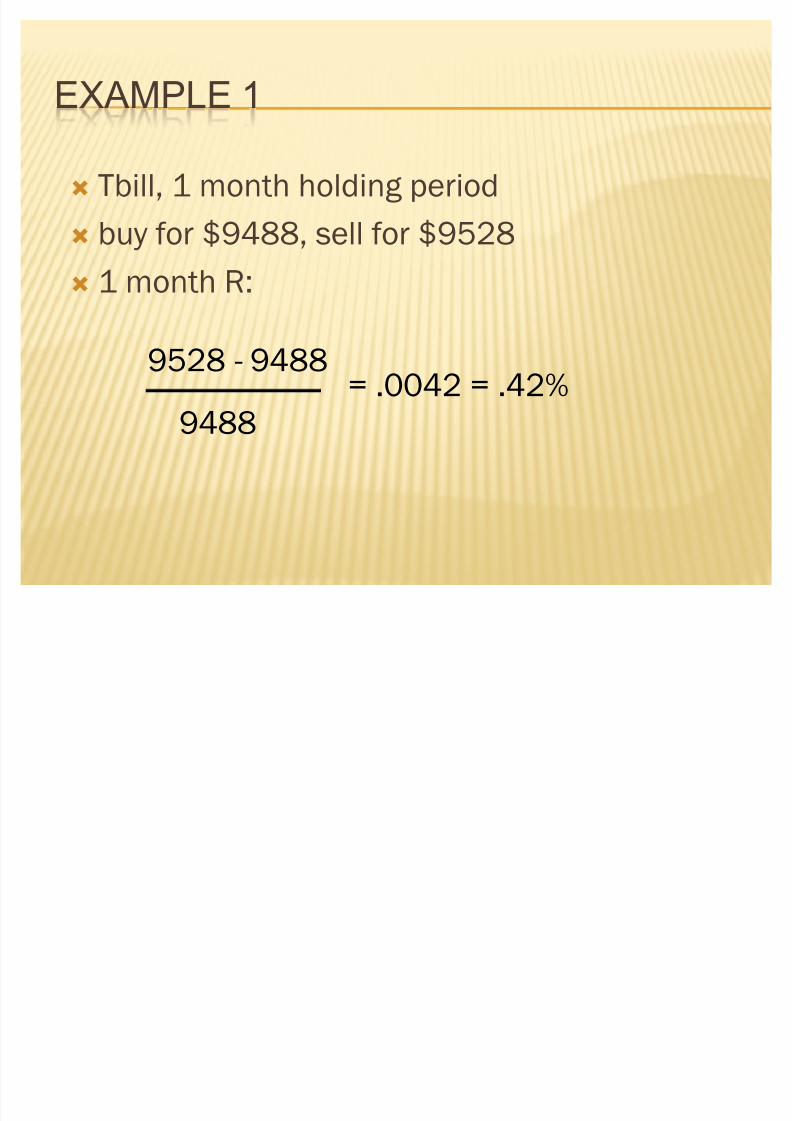

EXAMPLE 1

´ Tbill, 1 month holding period

´ buy for $9488, sell for $9528

´ 1 month R:

9528 - 9488

9488

= .0042 = .42%

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 7/45

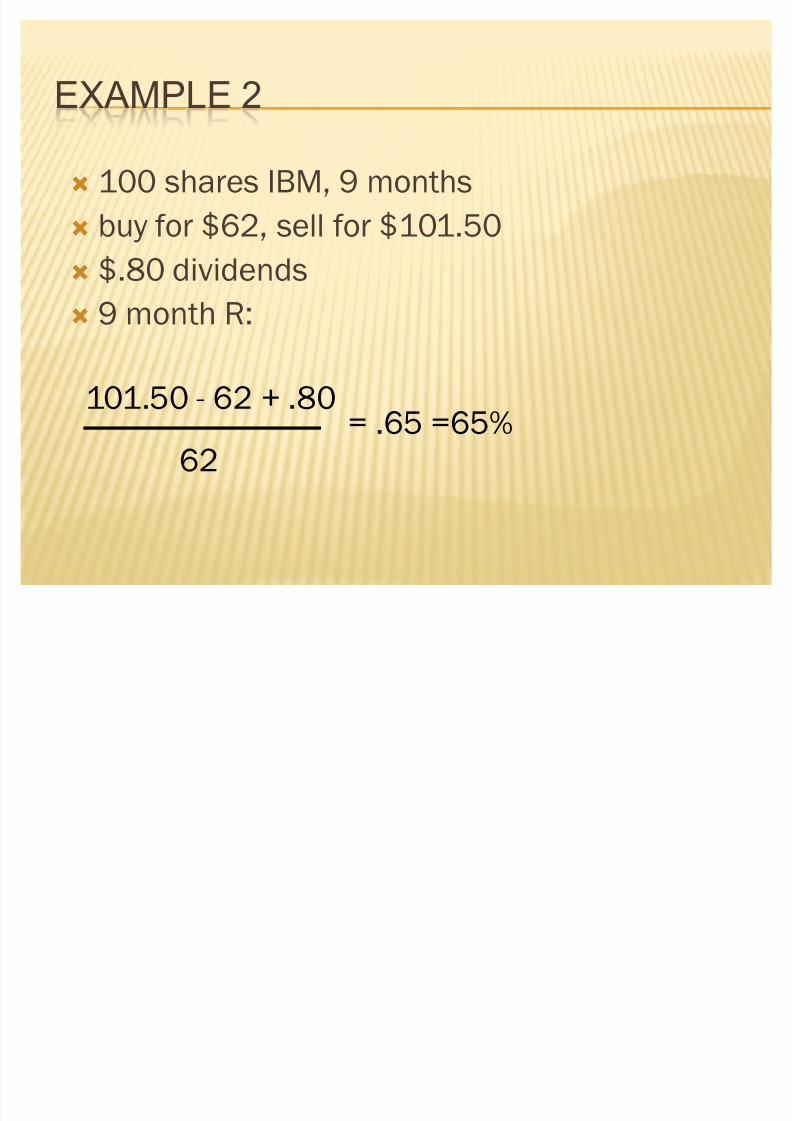

EXAMPLE 2

´ 100 shares IBM, 9 months

´ buy for $62, sell for $101.50

´ $.80 dividends´ 9 month R:

101.50 - 62 + .8062

= .65 =65%

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 8/45

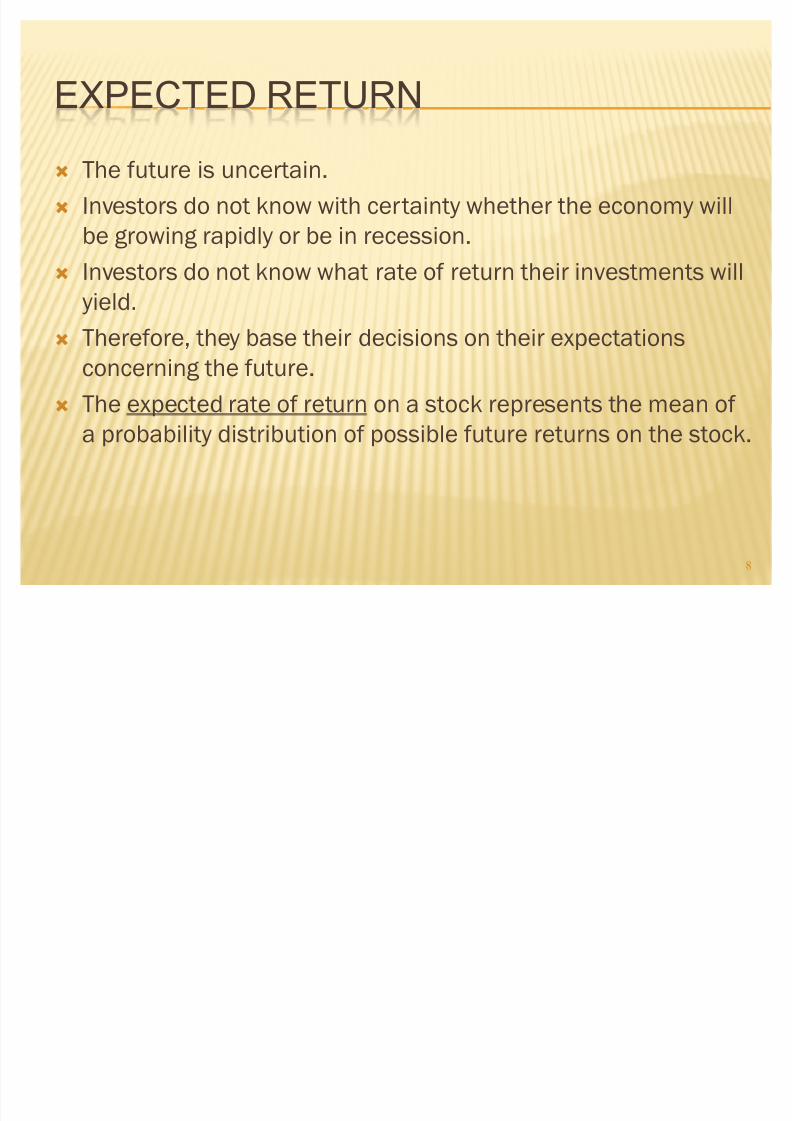

EXPECTED RETURN

´ The future is uncertain.

´ Investors do not know with certainty whether the economy will

be growing rapidly or be in recession.

´ Investors do not know what rate of return their investments willyield.

´ Therefore, they base their decisions on their expectations

concerning the future.

´ The expected rate of return on a stock represents the mean of a probability distribution of possible future returns on the stock.

8

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 9/45

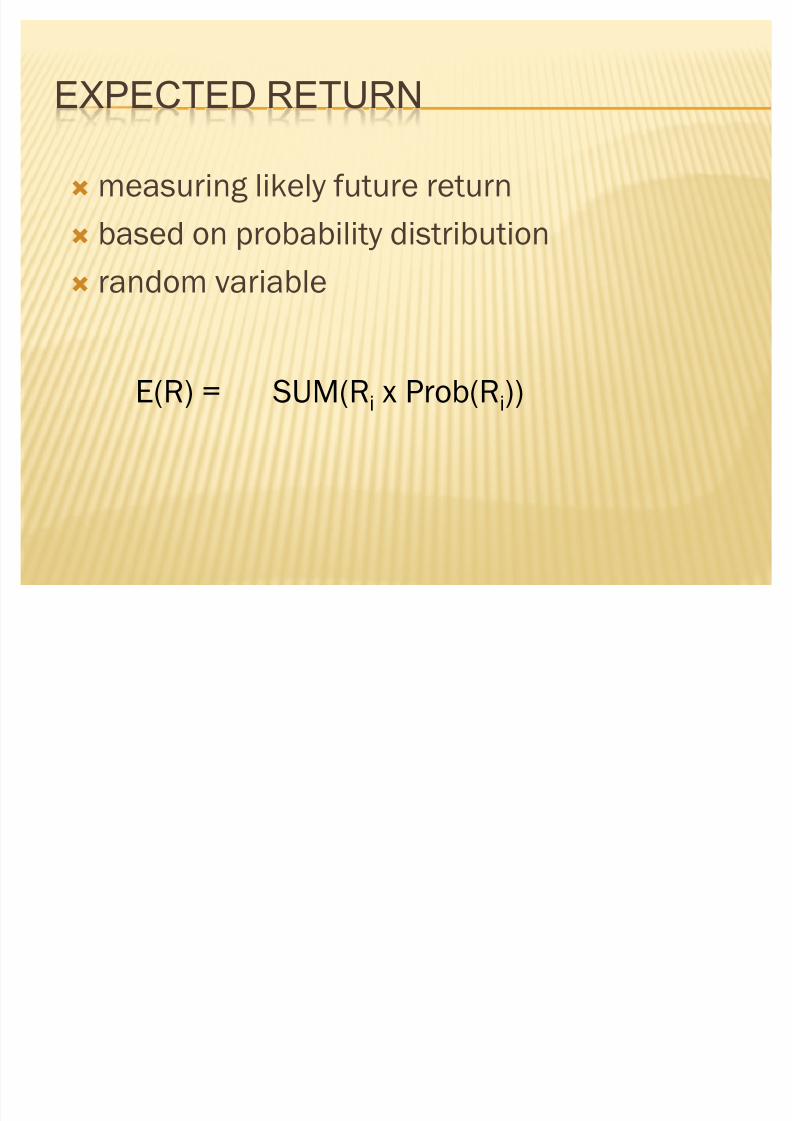

EXPECTED RETURN

´ measuring likely future return

´ based on probability distribution

´ random variable

E(R) = SUM(Ri x Prob(Ri))

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 10/45

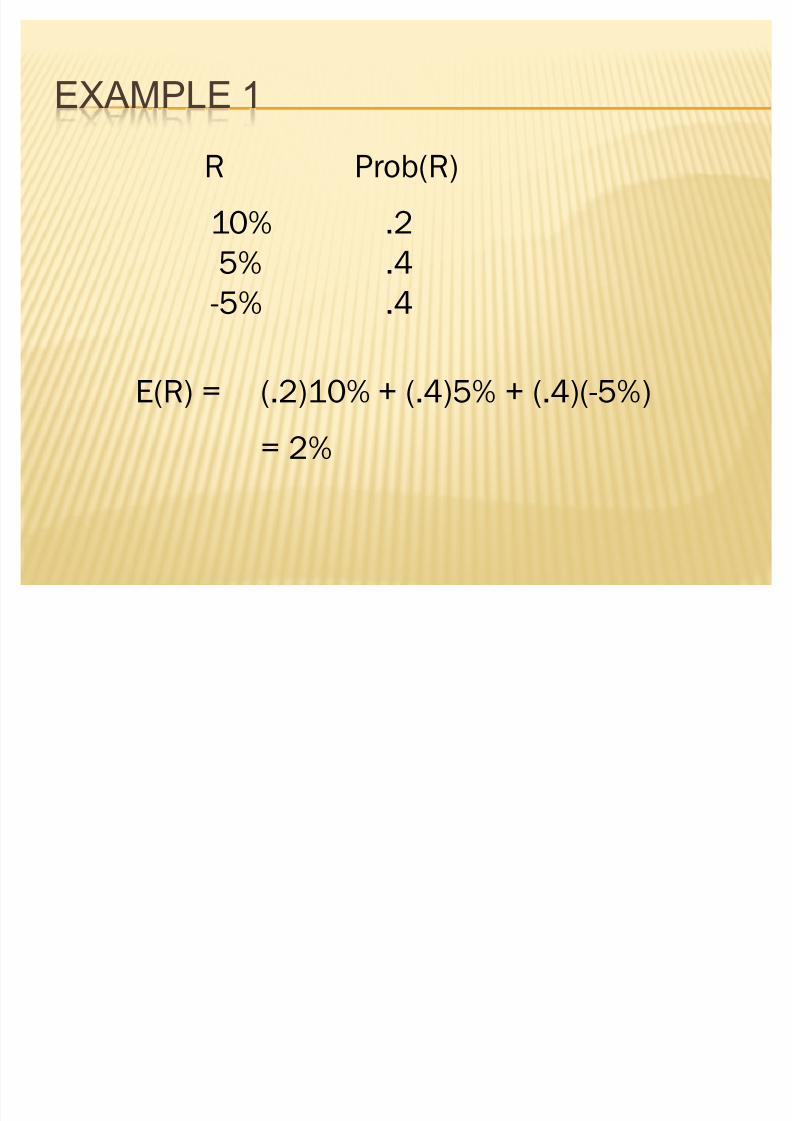

EXAMPLE 1

R Prob(R)

10% .2

5% .4-5% .4

E(R) = (.2)10% + (.4)5% + (.4)(-5%)

= 2%

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 11/45

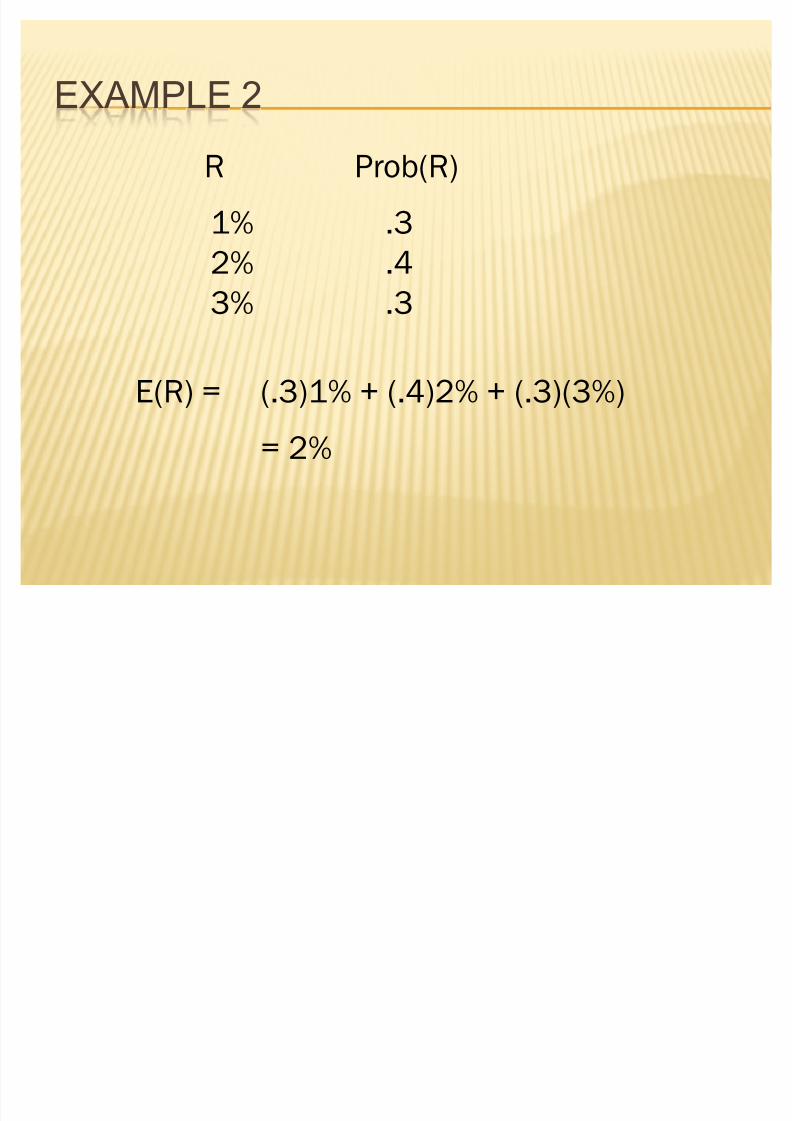

EXAMPLE 2

R Prob(R)

1% .3

2% .43% .3

E(R) = (.3)1% + (.4)2% + (.3)(3%)

= 2%

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 12/45

EXAMPLES 1 & 2

´ same expected return

´ but not same return structure

«

returns in example 1 are more variable

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 13/45

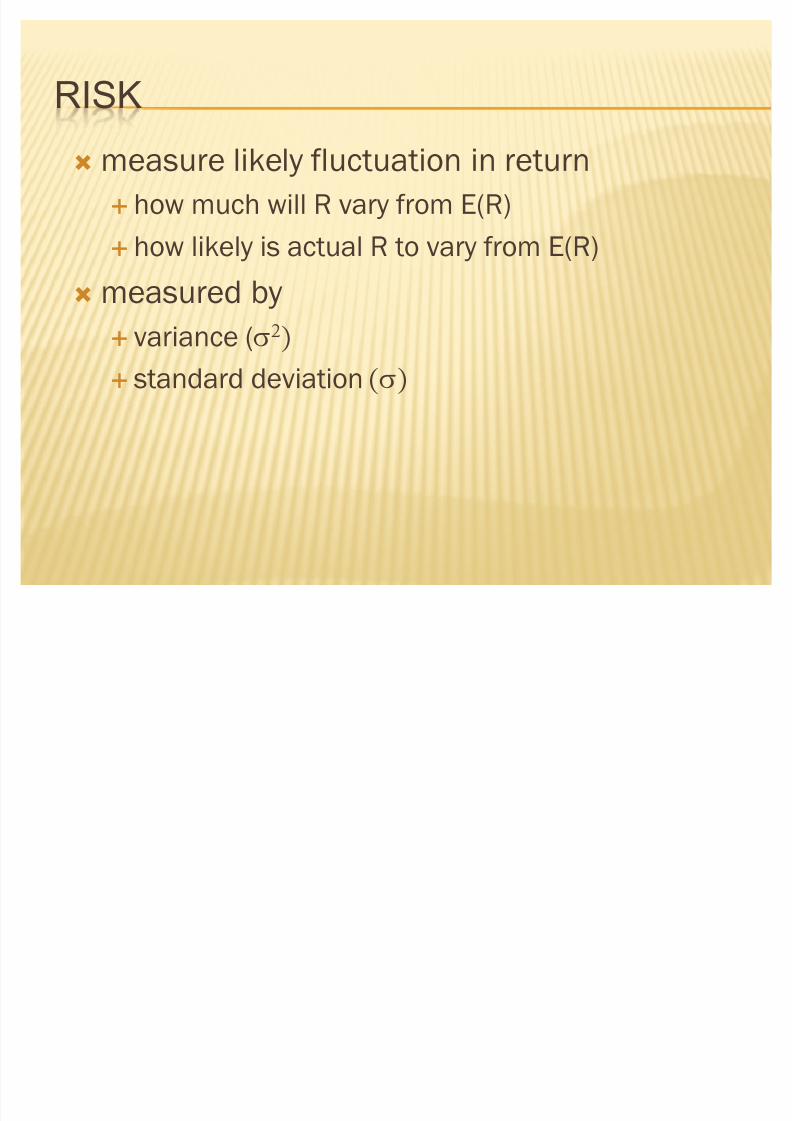

RISK

´measure likely fluctuation in return

« how much will R vary from E(R)

« how likely is actual R to vary from E(R)

´measured by

« variance (W

« standard deviation W

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 14/45

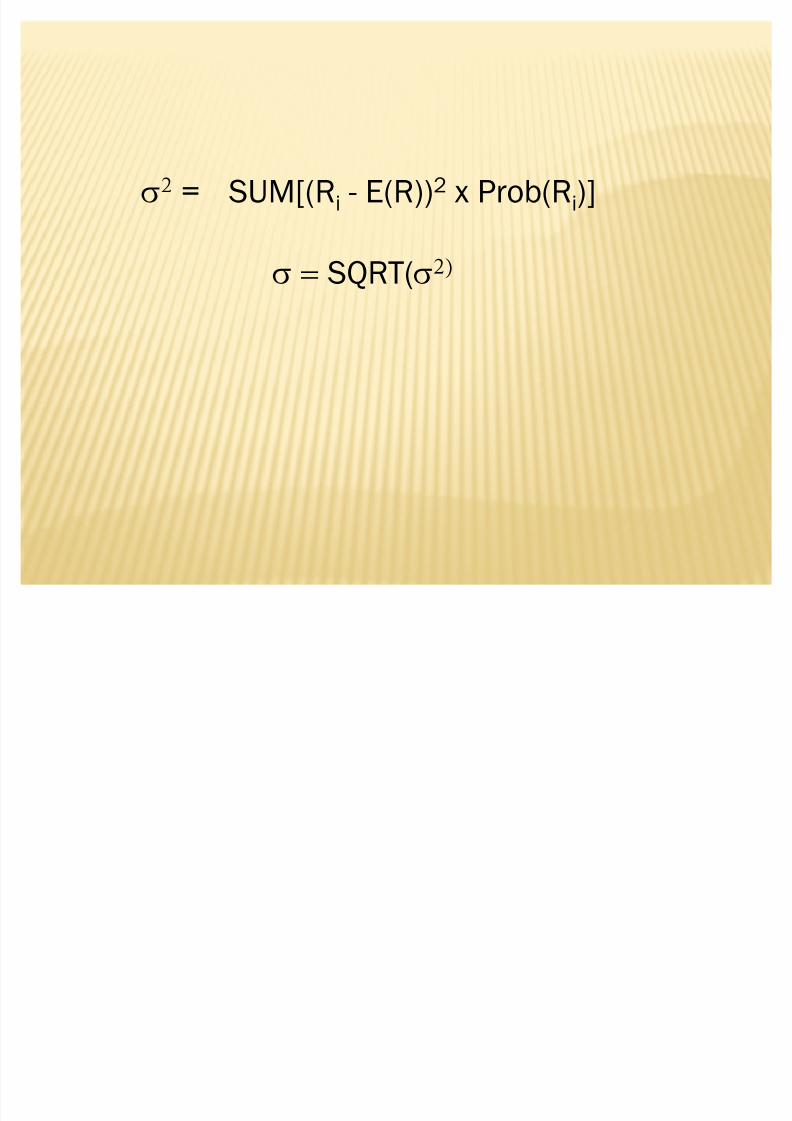

W = SUM[(Ri - E(R))2 x Prob(Ri)]

W!SQRT(W

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 15/45

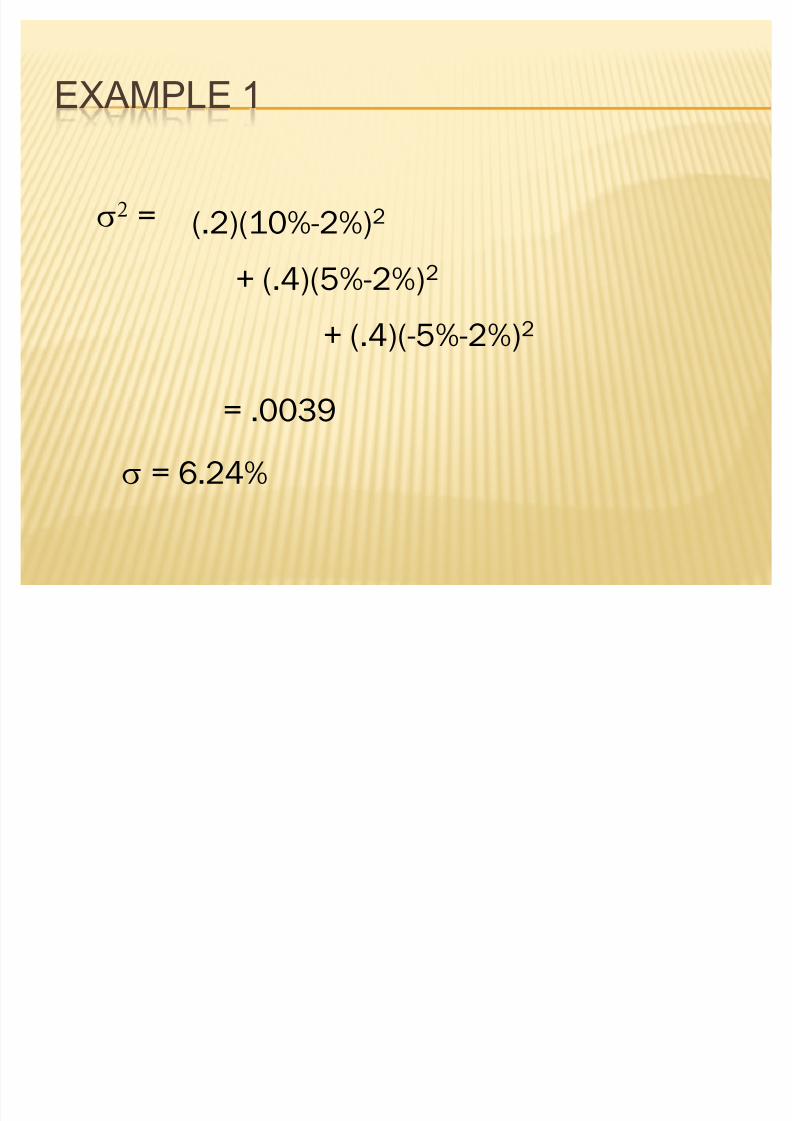

EXAMPLE 1

W = (.2)(10%-2%)2

= .0039

+ (.4)(5%-2%)2

+ (.4)(-5%-2%)2

W = 6.24%

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 16/45

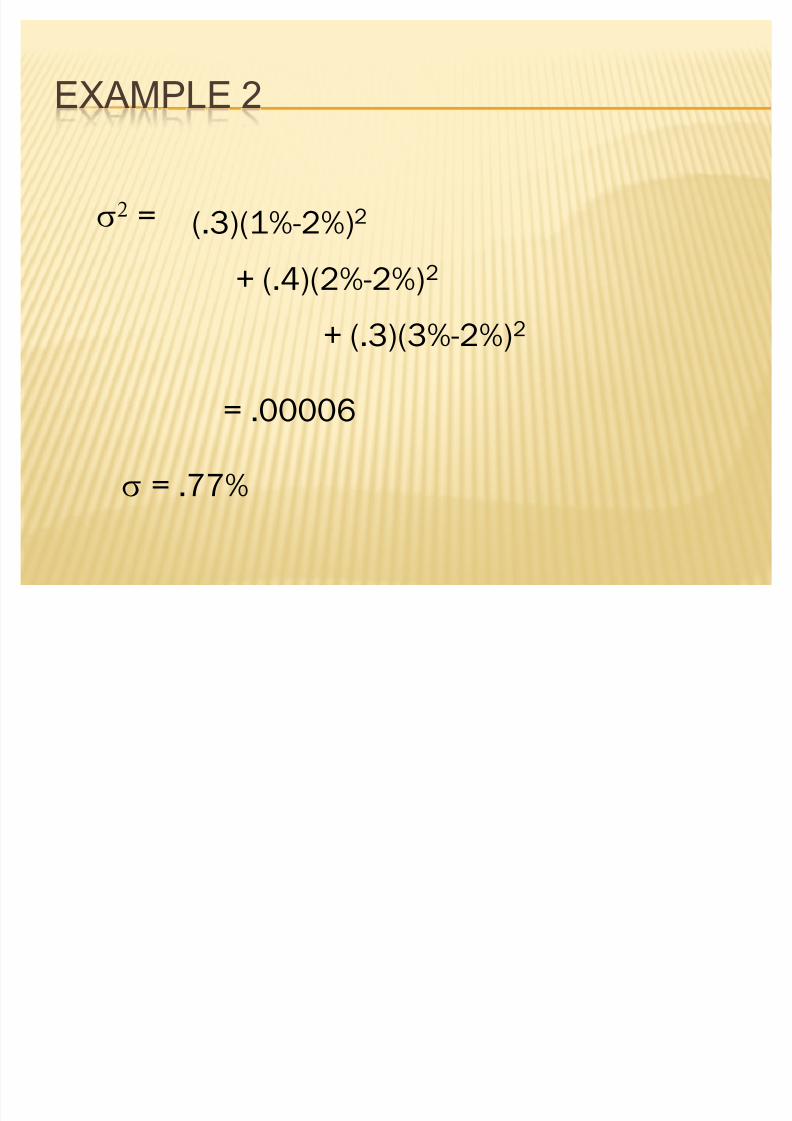

EXAMPLE 2

W = (.3)(1%-2%)2

= .00006

+ (.4)(2%-2%)2

+ (.3)(3%-2%)2

W = .77%

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 17/45

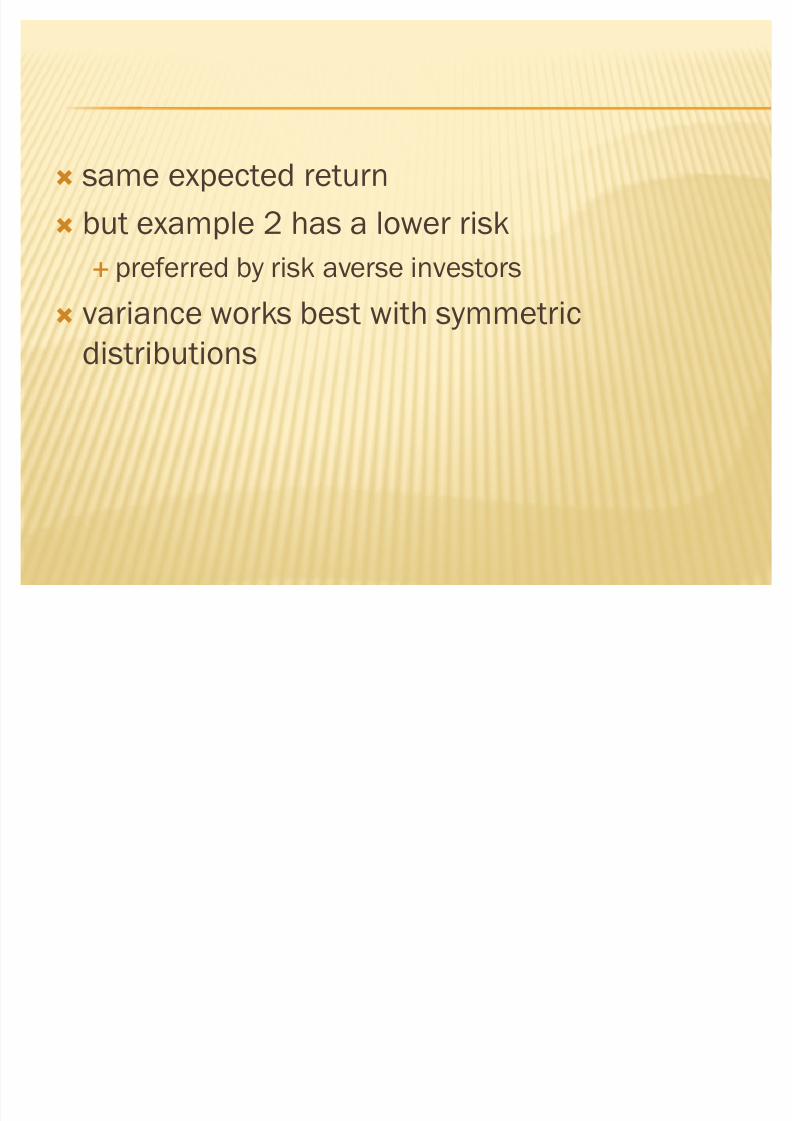

´ same expected return

´ but example 2 has a lower risk

«

preferred by risk averse investors´ variance works best with symmetric

distributions

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 18/45

EXPECTED RETURN

´ The table below provides a probability distribution for the returns on stocks

A and B

State Probability Return On Return On

Stock A Stock B

1 20% 5% 50%

2 30% 10% 30%

3 30% 15% 10%

4 20% 20% -10%

´ The state represents the state of the economy one period in the future i.e.

state 1 could represent a recession and state 2 a growth economy.

´ The probability reflects how likely it is that the state will occur. The sum of

the probabilities must equal 100%.

´ The last two columns present the returns or outcomes for stocks A and B

that will occur in each of the four states.

18

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 19/45

EXPECTED RETURN

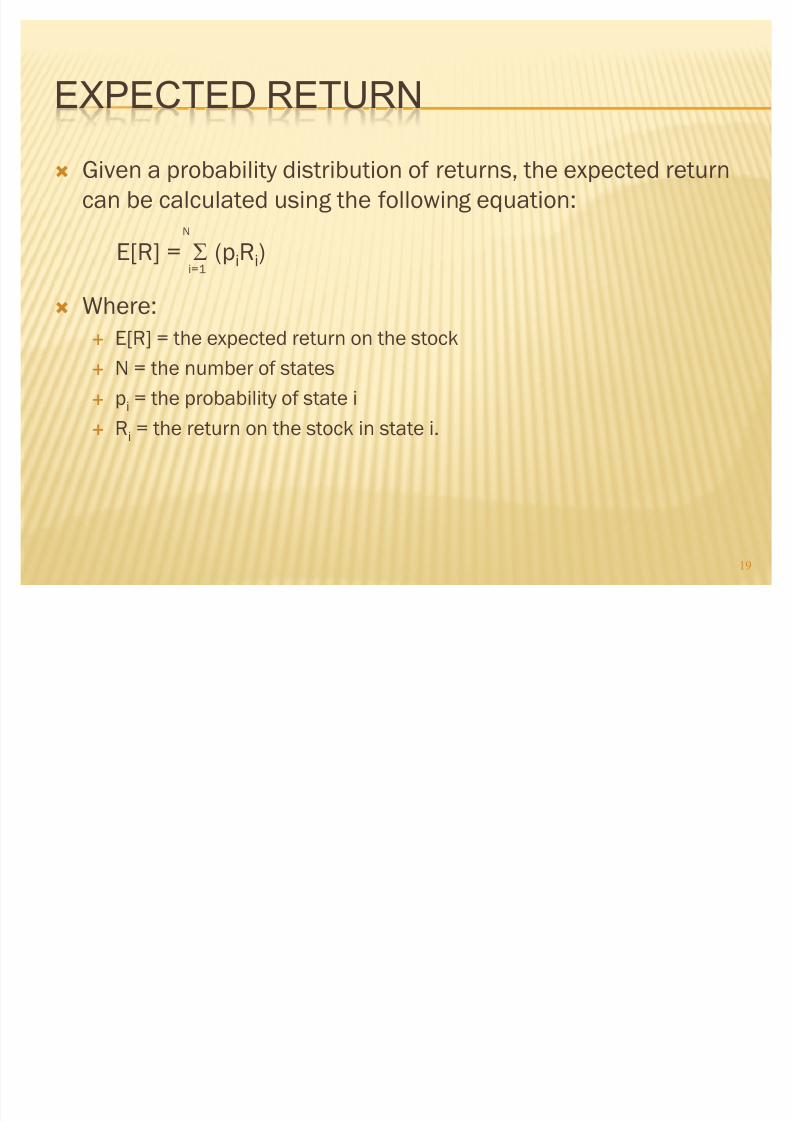

´ Given a probability distribution of returns, the expected return

can be calculated using the following equation:N

E[R] = 7(piRi)i=1

´ Where:

« E[R] = the expected return on the stock

« N = the number of states

« pi = the probability of state i

« Ri = the return on the stock in state i.

19

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 20/45

EXPECTED RETURN

´ In this example, the expected return for stock A would

be calculated as follows:

E[R]A = .2(5%) + .3(10%) + .3(15%) + .2(20%) = 12.5%

20

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 21/45

EXPECTED RETURN

the expected return for stock B would be calculated as follows:

E[R]B = .2(50%) + .3(30%) + .3(10%) + .2(-10%) = 20%

´ Stock B offers a higher expected return than Stock A.

´ However, that is only part of the analysis; risk werenot considered.

21

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 22/45

MANAGING RISK

´ Diversification

« holding a group of assets

« lower risk w/out lowering E(R)

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 23/45

´Why?

« individual assets do not have same return pattern

« combining assets reduces overall return variation

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 24/45

TWO TYPES OF RISK

´ unsystematic risk

« specific to a firm

« can be eliminated through diversification

« examples:

-- Safeway and a strike

-- Microsoft and antitrust cases

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 25/45

´ systematic risk

«market risk« cannot be eliminated through diversification

« due to factors affecting all assets

-- energy prices, interest rates, inflation,business cycles

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 26/45

EXAMPLE

´ choose stocks from NSE listings

´ go from 1 stock to 20 stocks

«

reduce risk by 40-50%

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 27/45

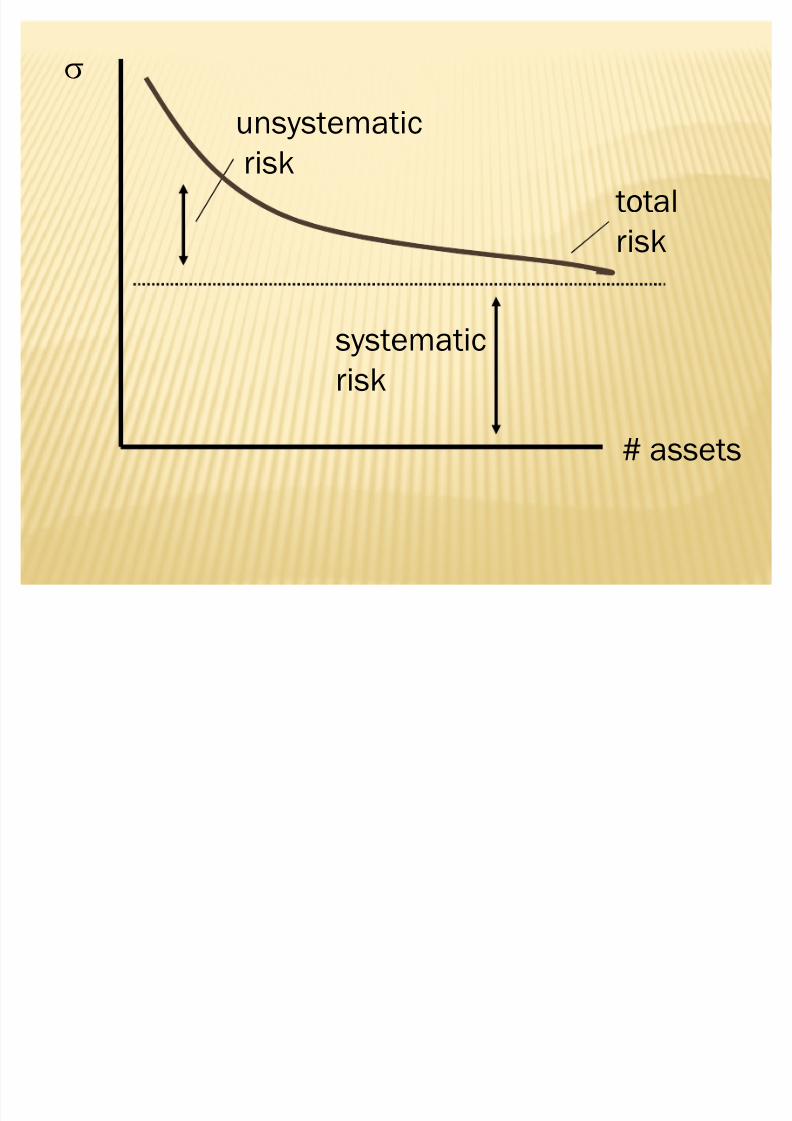

W

# assets

systematic

risk

unsystematic

risktotal

risk

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 28/45

MEASURES OF RISK

´ Risk reflects the chance that the actual return on an

investment may be different than the expected return.

´ One way to measure risk is to calculate the variance and

standard deviation of the distribution of returns.

28

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 29/45

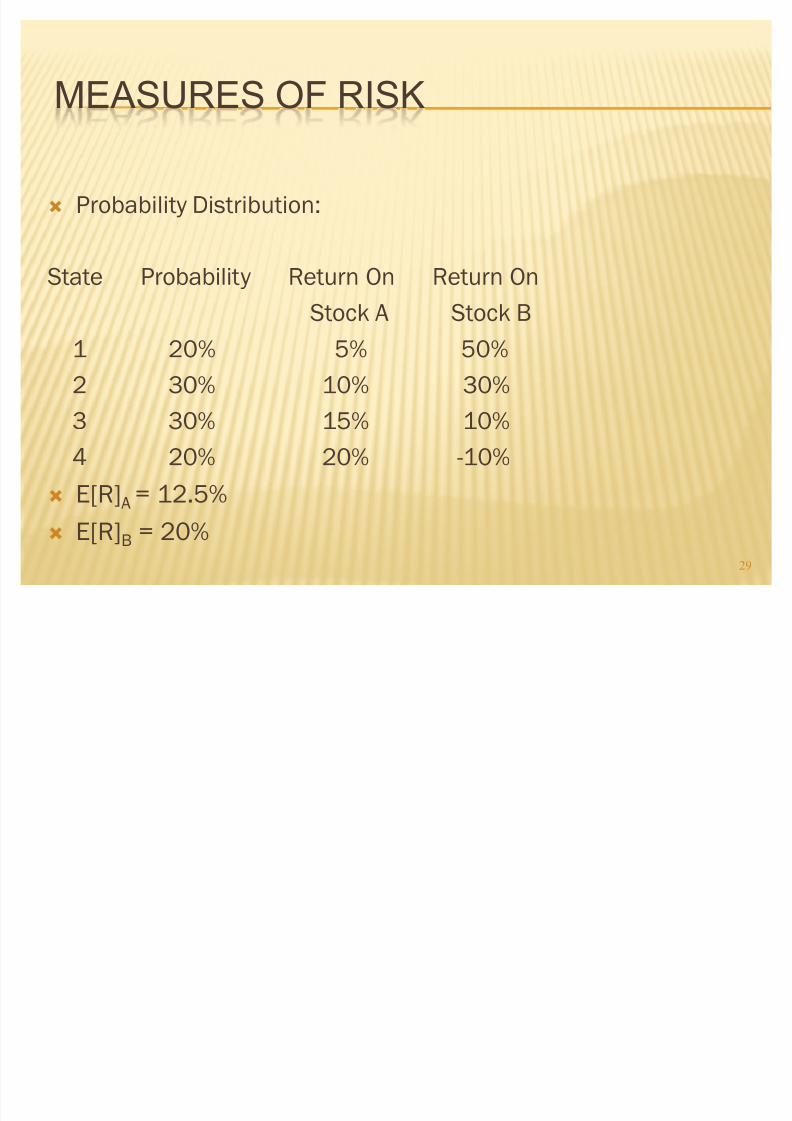

MEASURES OF RISK

´ Probability Distribution:

State Probability Return On Return OnStock A Stock B

1 20% 5% 50%

2 30% 10% 30%

3 30% 15% 10%4 20% 20% -10%

´ E[R]A = 12.5%

´ E[R]B = 20%29

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 30/45

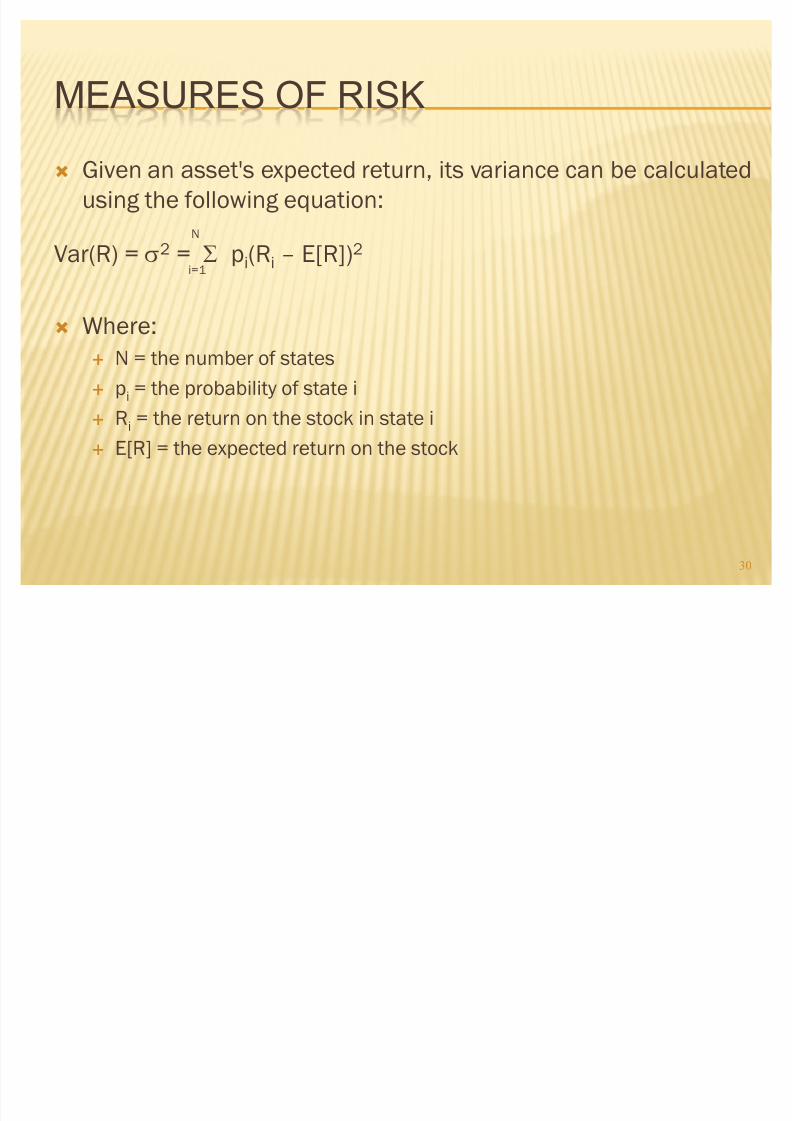

MEASURES OF RISK

´ Given an asset's expected return, its variance can be calculated

using the following equation:

N

Var(R) = W2 = 7 pi(Ri ² E[R])2

i=1

´ Where:

« N = the number of states

« pi = the probability of state i

« Ri = the return on the stock in state i« E[R] = the expected return on the stock

30

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 31/45

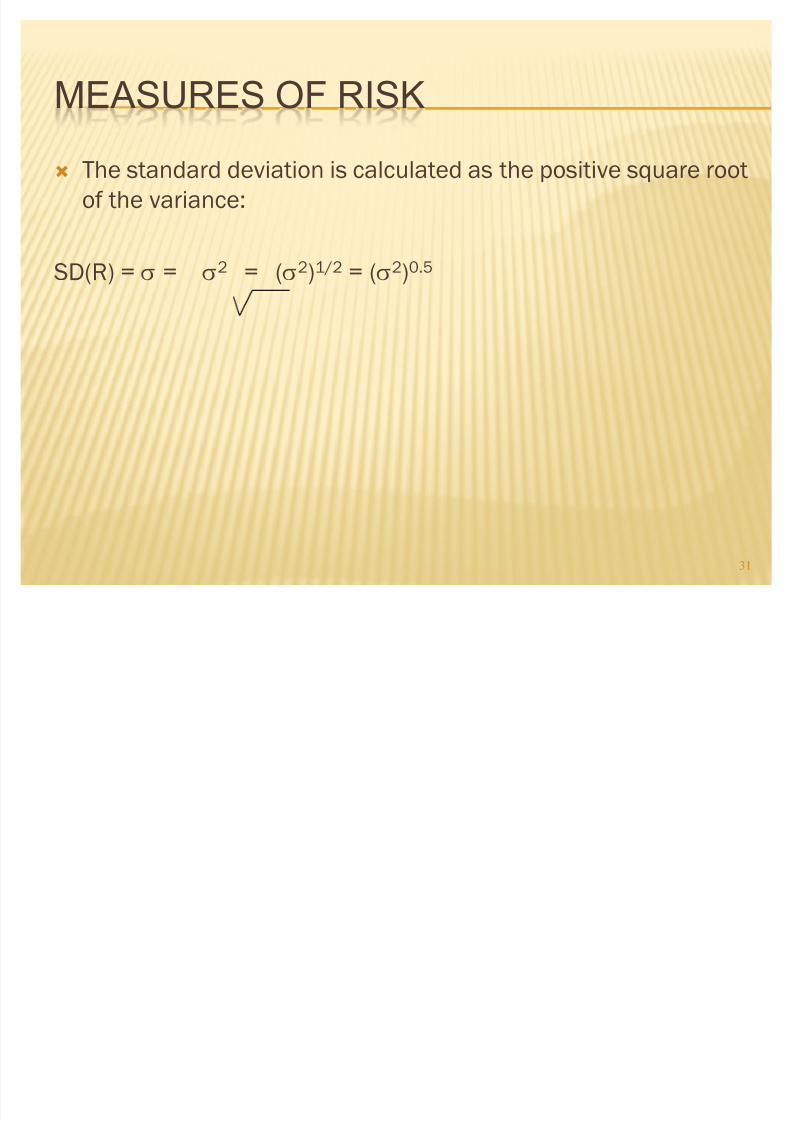

MEASURES OF RISK

´ The standard deviation is calculated as the positive square root

of the variance:

SD

(R) = W = W2

= (W2

)1/2

= (W2

)0.5

31

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 32/45

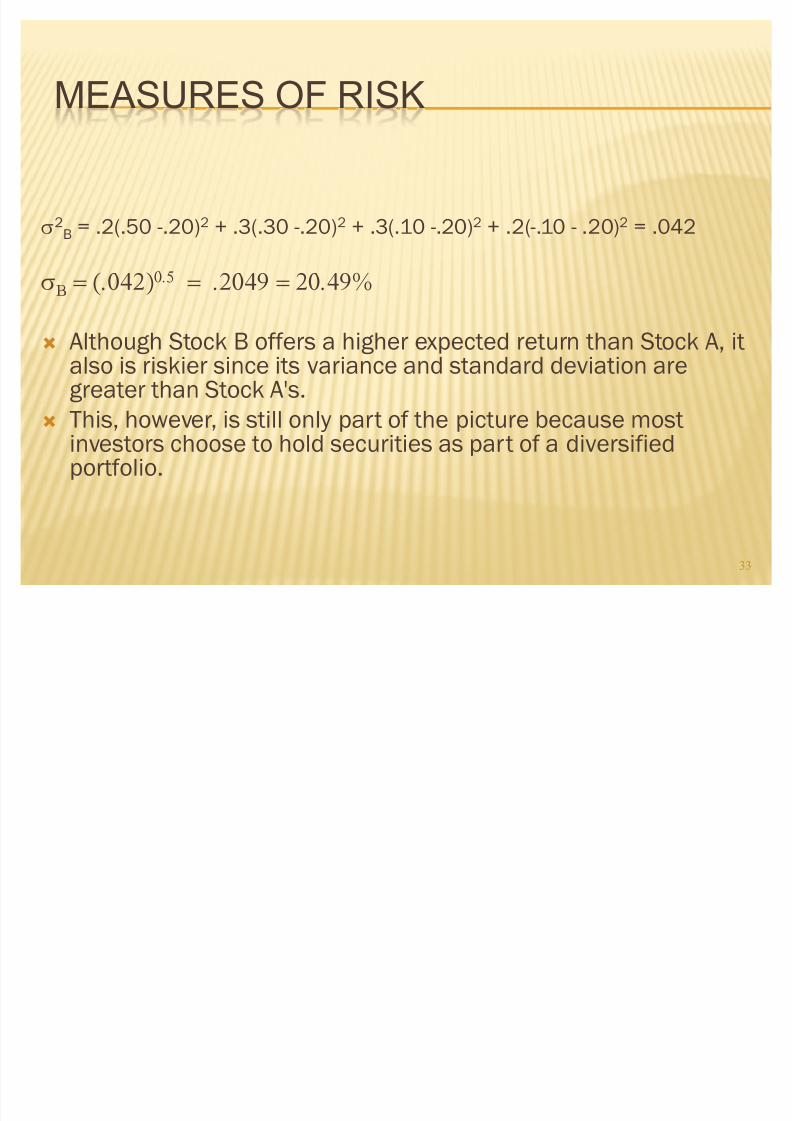

MEASURES OF RISK

´ The variance and standard deviation for stock A is calculated as

follows:

W2A = .2(.05 -.125)2 + .3(.1 -.125)2 + .3(.15 -.125)2 + .2(.2 -.125)2 = .002625

W% ! !!

32

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 33/45

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 34/45

PORTFOLIO RISK AND RETURN

´ Most investors do not hold stocks in isolation.

´ Instead, they choose to hold a portfolio of several stocks.

´ When this is the case, a portion of an individual stock'srisk can be eliminated, i.e., diversified away.

´ From our previous calculations, we know that:« the expected return on Stock A is 12.5%

« the expected return on Stock B is 20%

«

the variance on Stock A is .00263« the variance on Stock B is .04200

« the standard deviation on Stock A is 5.12%

« the standard deviation on Stock B is 20.49%

34

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 35/45

PORTFOLIO RISK AND RETURN

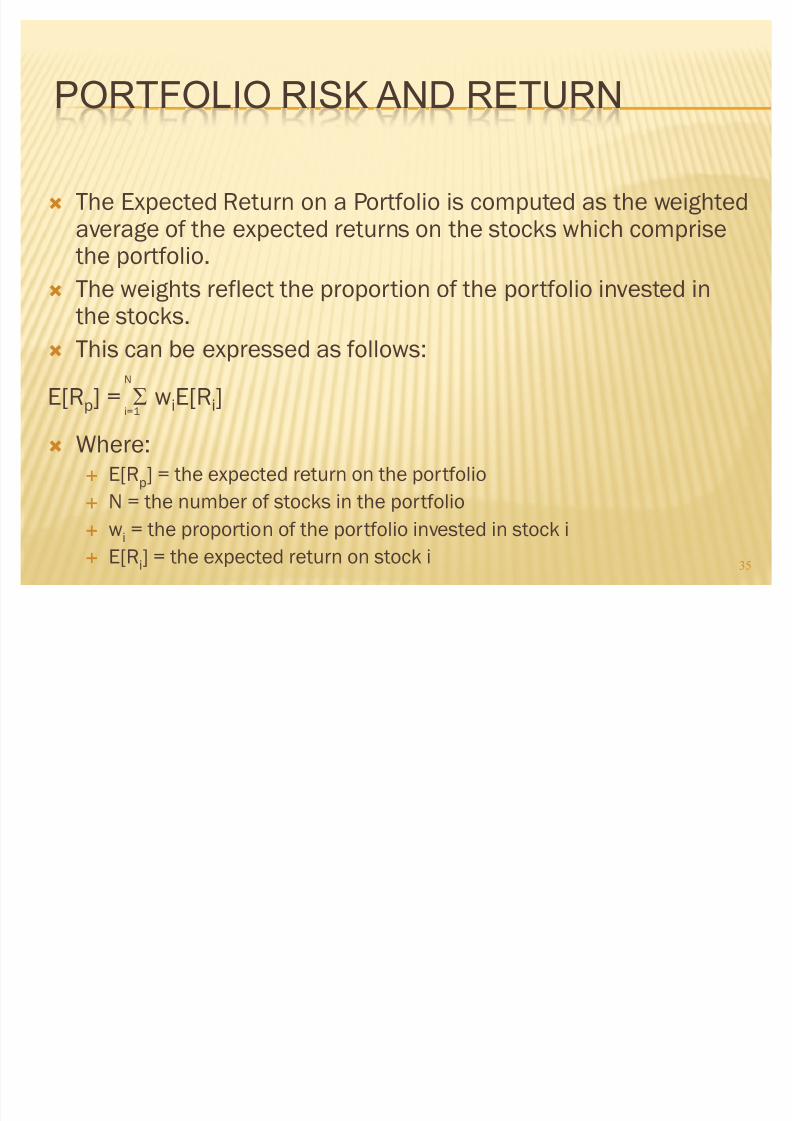

´ The Expected Return on a Portfolio is computed as the weightedaverage of the expected returns on the stocks which comprisethe portfolio.

´ The weights reflect the proportion of the portfolio invested inthe stocks.

´ This can be expressed as follows:N

E[Rp] = 7 wiE[Ri]i=1

´ Where:« E[Rp] = the expected return on the portfolio

« N = the number of stocks in the portfolio

« wi = the proportion of the portfolio invested in stock i

« E[Ri] = the expected return on stock i 35

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 36/45

PORTFOLIO RISK AND RETURN

´ For a portfolio consisting of two assets, the above equation can

be expressed as:

E[Rp] = w1E[R1] + w2E[R2]

´ If we have an equally weighted portfolio of stock A and stock B

(50% in each stock), then the expected return of the portfolio

is:

E[Rp] = .50(.125) + .50(.20) = 16.25%

36

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 37/45

PORTFOLIO RISK AND RETURN

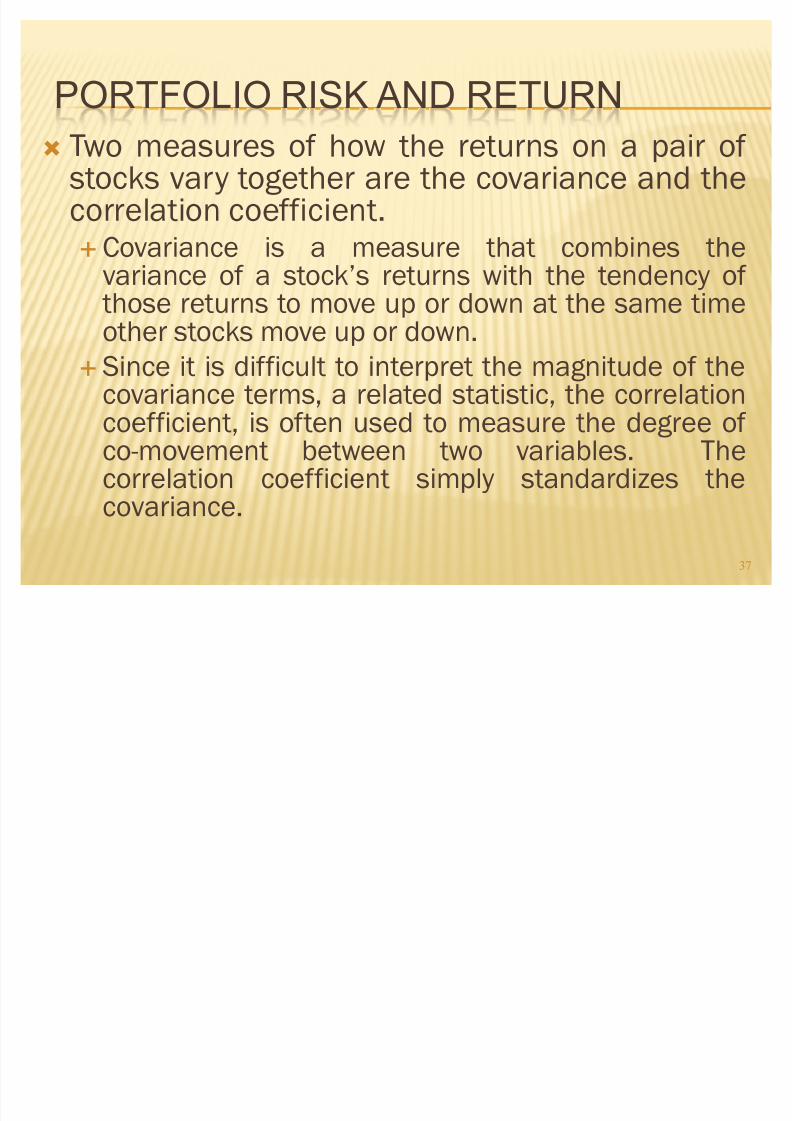

´ Two measures of how the returns on a pair of stocks vary together are the covariance and thecorrelation coefficient.«Covariance is a measure that combines the

variance of a stock·s returns with the tendency of those returns to move up or down at the same timeother stocks move up or down.

« Since it is difficult to interpret the magnitude of thecovariance terms, a related statistic, the correlation

coefficient, is often used to measure the degree of co-movement between two variables. Thecorrelation coefficient simply standardizes thecovariance.

37

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 38/45

PORTFOLIO RISK AND RETURN

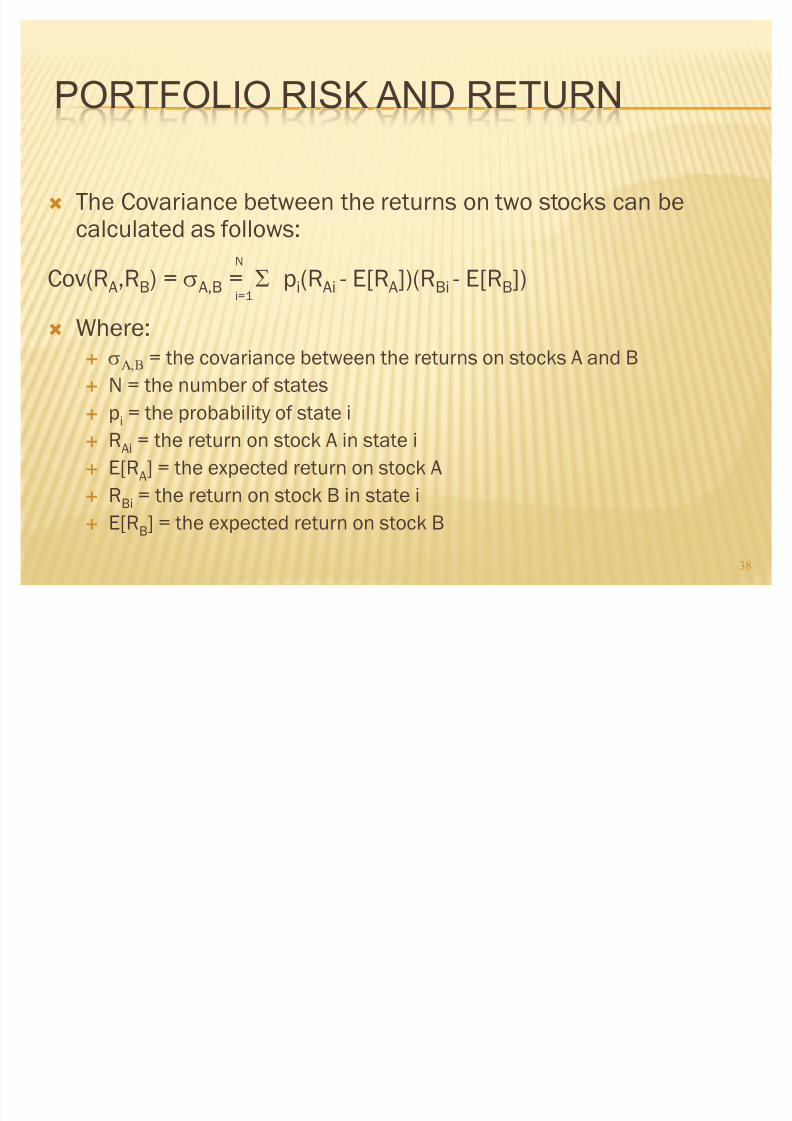

´ The Covariance between the returns on two stocks can becalculated as follows:

N

Cov(RA,RB) = WA,B = 7 pi(RAi - E[RA])(RBi - E[RB])i=1

´ Where:« W%& = the covariance between the returns on stocks A and B

« N = the number of states

«

pi = the probability of state i« RAi = the return on stock A in state i

« E[RA] = the expected return on stock A

« RBi = the return on stock B in state i

« E[RB] = the expected return on stock B

38

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 39/45

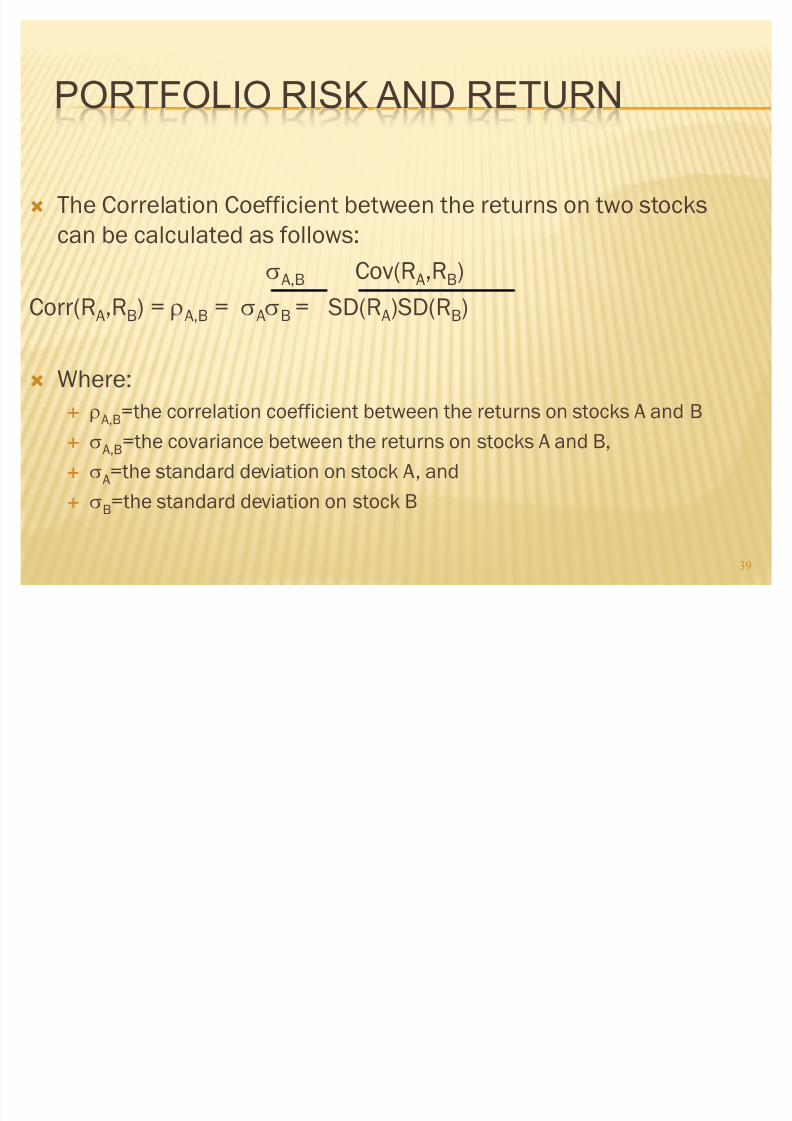

PORTFOLIO RISK AND RETURN

´ The Correlation Coefficient between the returns on two stocks

can be calculated as follows:

WA,B Cov(RA,RB)Corr(RA,RB) = VA,B = WAWB = SD(RA)SD(RB)

´ Where:

«

VA,B=the correlation coefficient between the returns on stocks A and B« WA,B=the covariance between the returns on stocks A and B,

« WA=the standard deviation on stock A, and

« WB=the standard deviation on stock B

39

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 40/45

PORTFOLIO RISK AND RETURN

´ The covariance between stock A and stock B is as follows:

WA,B = .2(.05-.125)(.5-.2) + .3(.1-.125)(.3-.2) +.3(.15-.125)(.1-.2) +.2(.2-.125)(-.1-.2) = -.0105

´ The correlation coefficient between stock A and stock B is as

follows:

-.0105

VA,B = (.0512)(.2049) = -1.00

40

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 41/45

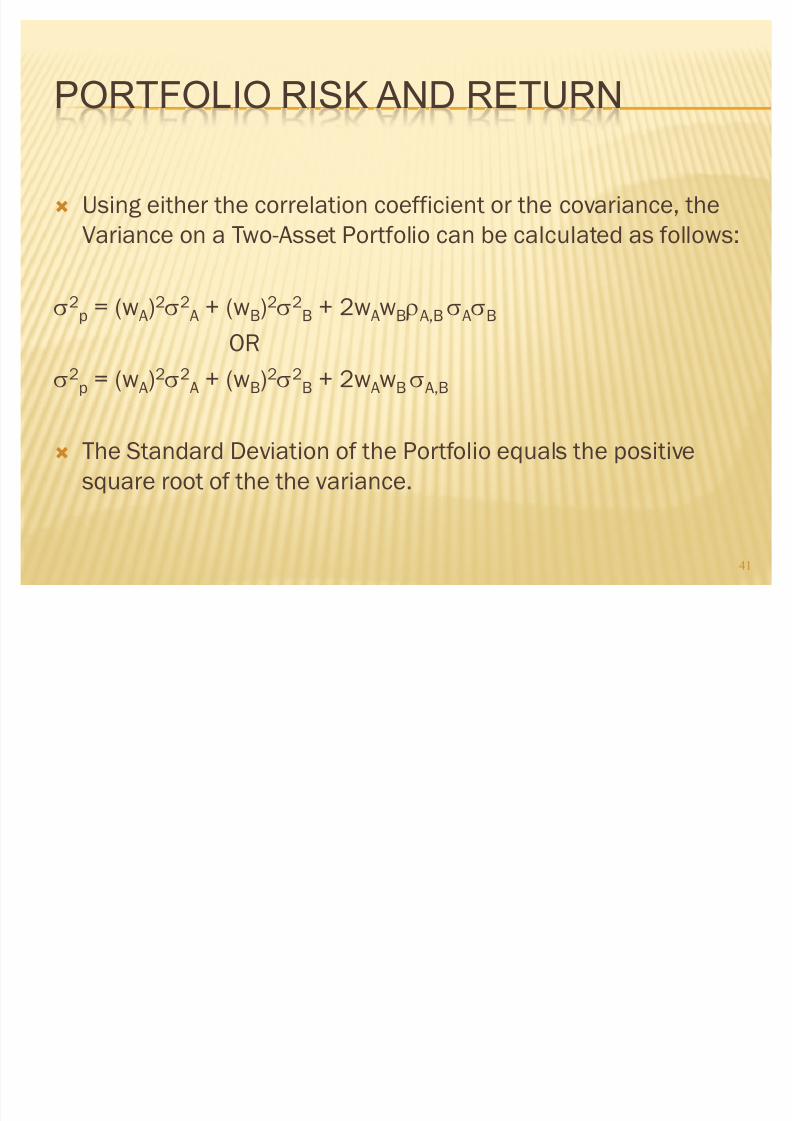

PORTFOLIO RISK AND RETURN

´ Using either the correlation coefficient or the covariance, the

Variance on a Two-Asset Portfolio can be calculated as follows:

W2p = (wA)2W2

A + (wB)2W2B + 2wAwB VA,BWAWB

OR

W2p = (wA)2W2

A + (wB)2W2B + 2wAwBWA,B

´ The Standard Deviation of the Portfolio equals the positive

square root of the the variance.

41

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 42/45

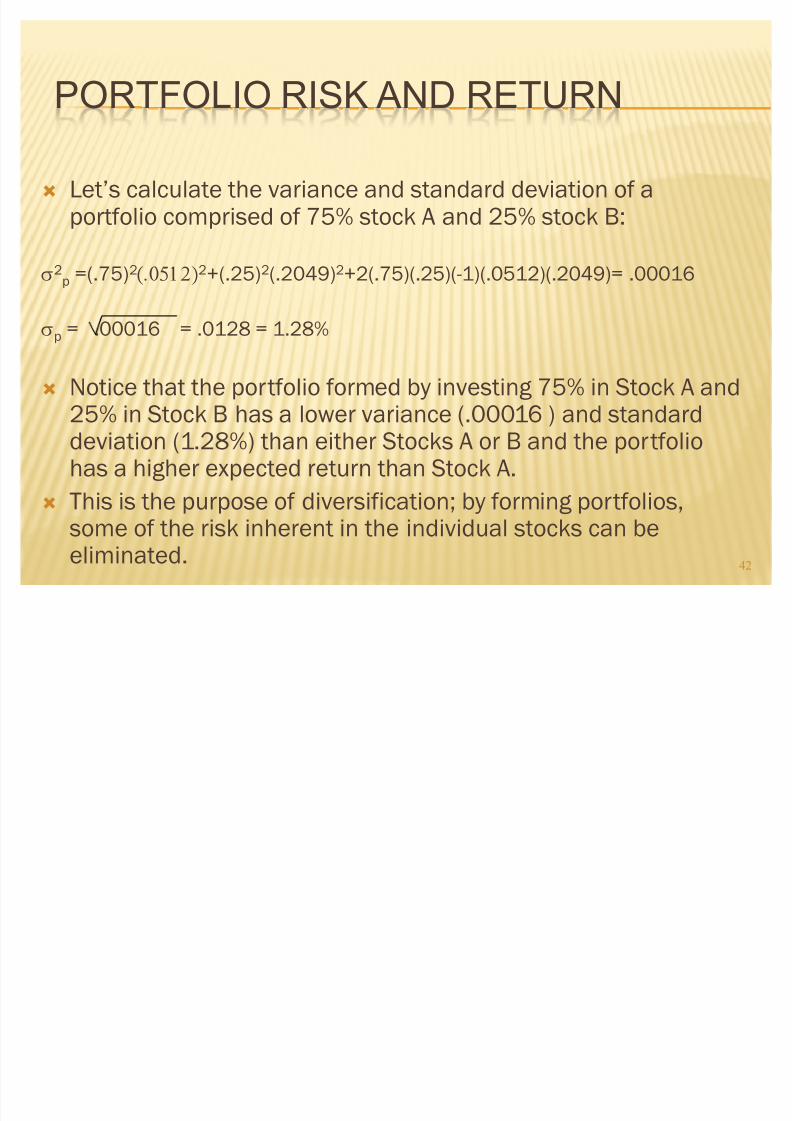

PORTFOLIO RISK AND RETURN

´ Let·s calculate the variance and standard deviation of aportfolio comprised of 75% stock A and 25% stock B:

W2

p =(.75)2

2

+(.25)2

(.2049)2

+2(.75)(.25)(-1)(.0512)(.2049)= .00016

Wp = .00016 = .0128 = 1.28%

´ Notice that the portfolio formed by investing 75% in Stock A and

25% in Stock B has a lower variance (.00016 ) and standarddeviation (1.28%) than either Stocks A or B and the portfoliohas a higher expected return than Stock A.

´ This is the purpose of diversification; by forming portfolios,some of the risk inherent in the individual stocks can be

eliminated. 42

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 43/45

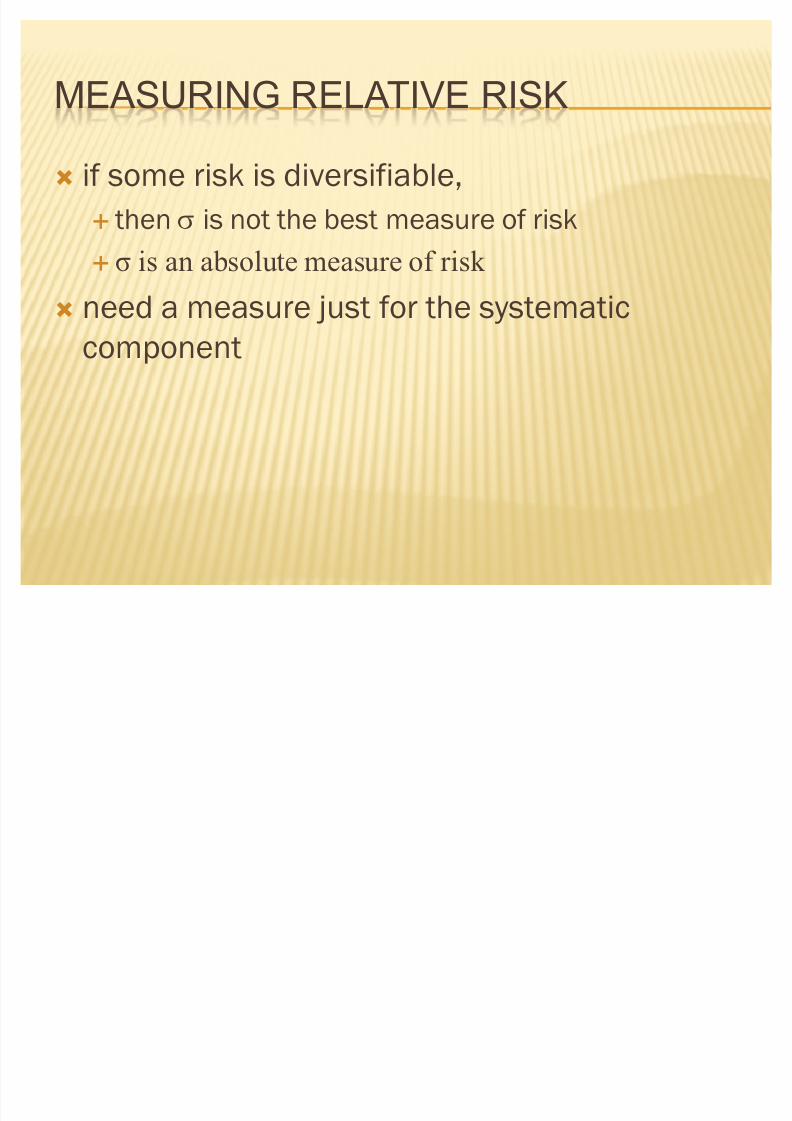

MEASURING RELATIVE RISK

´ if some risk is diversifiable,

« then W is not the best measure of risk

« is an absolute measure of risk

´ need a measure just for the systematic

component

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 44/45

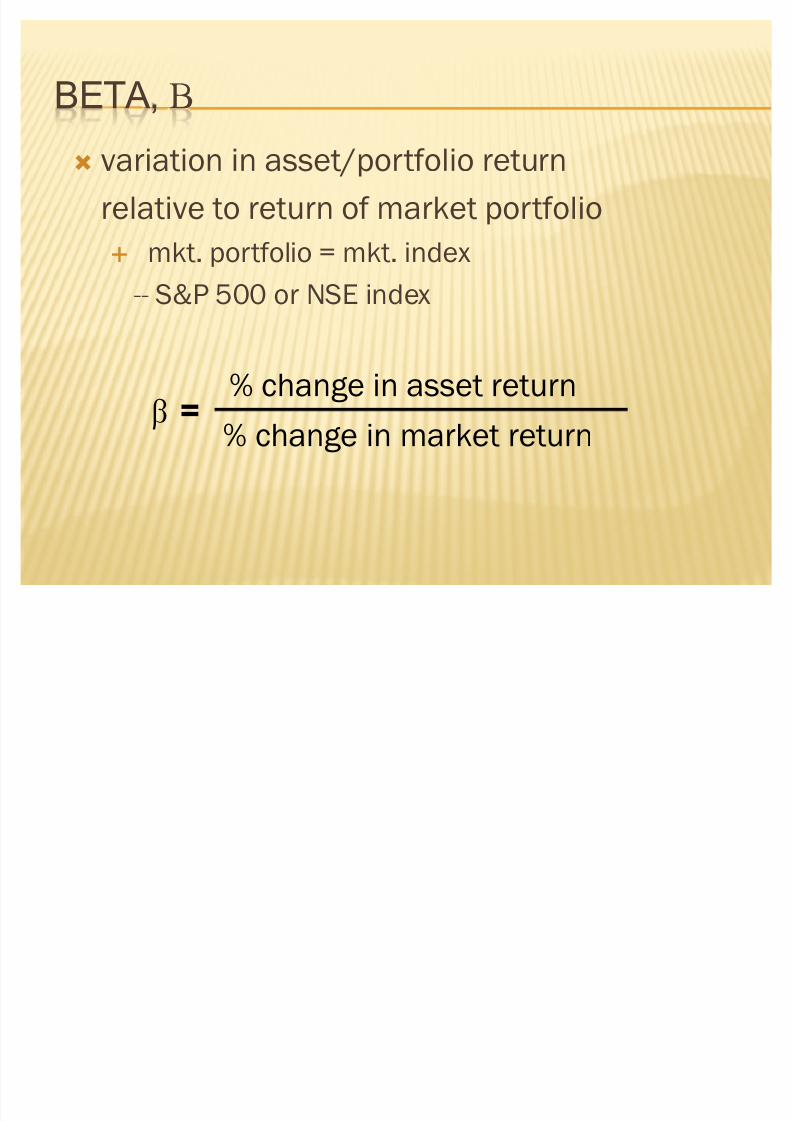

BETA, &

´ variation in asset/portfolio return

relative to return of market portfolio

« mkt. portfolio = mkt. index

-- S&P 500 or NSE index

F=

% change in asset return

% change in market return

8/8/2019 Measuring Rate and Return

http://slidepdf.com/reader/full/measuring-rate-and-return 45/45

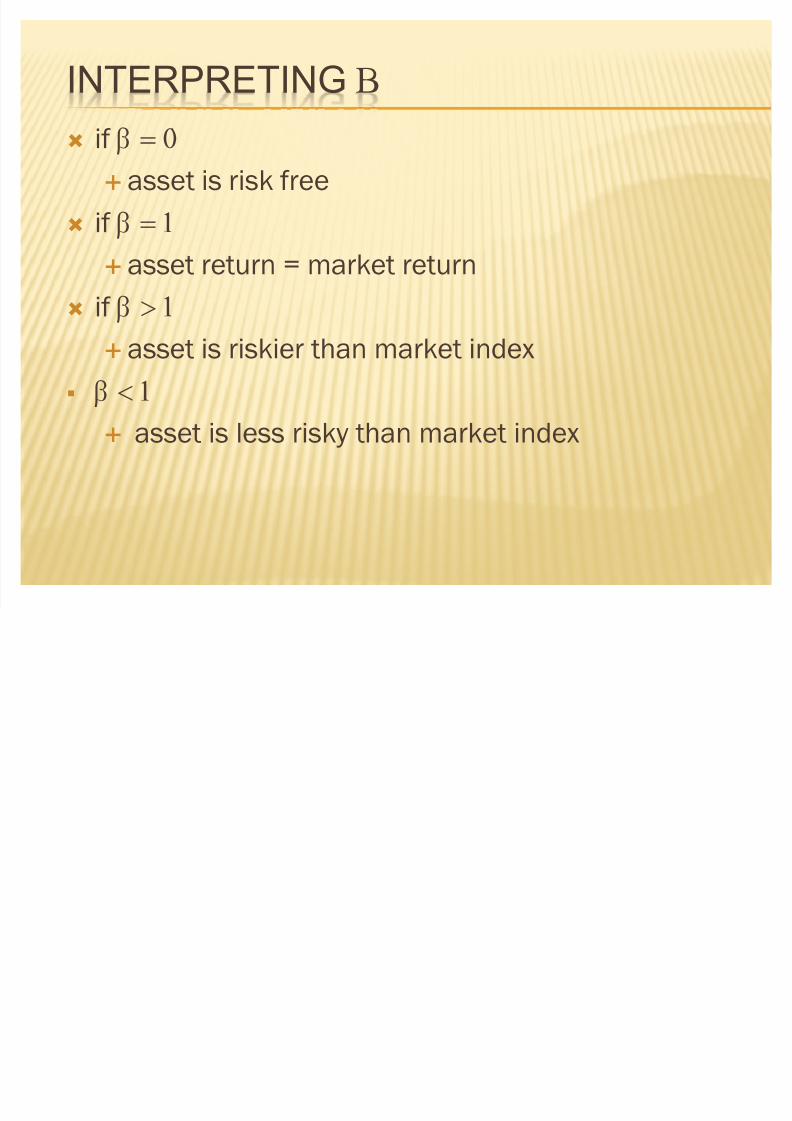

INTERPRETING &

´ if F!« asset is risk free

´ if F!

« asset return = market return

´ if F"

« asset is riskier than market index

F

« asset is less risky than market index