measuring treasury from head to toe

TRANSCRIPT

16 I AFP Exchange September 2016

GLOBAL TREASURER

SpotlightUnder the

Measuring treasury performance from head to toe

NUNO FERREIRA

In the years since the financial crisis, treasury has been under the spotlight. And being under the spotlight means presenting not only quick and accurate information to the board, but also managing typical treasury tasks in a leaner and more efficient and accurate way.Treasury should not only be measured by looking at P&L statements or balance sheet figures. The

best way to measure treasury’s day-to-day activities is by using key performance indicators (KPIs). KPIs provide other departments and the board with a clear view into how treasury is performing.

Establishing KPIsTo set up treasury KPIs, it’s important to consider two key variables: the concerns of the CFO and

board members and how treasury’s role is increasingly expanding. CFOs’ main concerns in recent years still are:• Cash and liquidity: Easy access to a company’s liquidity continues to be very important.• Funding: Treasury needs to settle and optimize arrangements. • Risk management: Hedging risks due to more volatile markets remains essential.• Centralization: CFOs want a better overall picture while reducing costs and gaining efficiency.

KEY TAKEAWAYS:• The only way to measure

treasury’s day-to-day activities is by using KPIs.

• To set up treasury KPIs it is important to consider the concerns of the CFO and board members, and how treasury’s role is increasingly expanding.

• One way to not only improve treasury operations but finance as a whole is to have a set of transversal KPIs.

www.AFPonline.org AFP Exchange I 17

As for treasury itself, the department is increasingly taking on new roles. In addition to the transactional part of their job, treasury professionals are also becoming more strategic.

So, with this in mind, how can we set up treasury KPIs?KPI´s are indicators used to track performance. Do not define a huge set of

KPIs that ultimately take a lot of time to produce and jeopardize what you want to measure—the performance.

When defining KPIs, see what systems you need to produce them. If you find that it requires a lot of manual input, systems that you don´t have access to or data that is not directly delivered by your team, don´t use them.

Look at your team and review the most time consuming, costly, financially important and transversal tasks. These should be the activities to focus on when determining KPIs.

Set a matrix of activities versus a treasury category or segment. For example: FX hedging - > risk management. With these segments, you can more clearly check the importance of each task in a category and define in each segment a specific set of KPIs.

Also, bear in mind who will be reviewing the KPIs and for what they will be used. The set can be selected differently depending on the audience and objective:

• Will these KPIs be presented monthly to the CFO or the board?• Are these KPIs treasury tools to measure performance and evaluate resources?• Will these KPIs be present among other finance department KPIs?

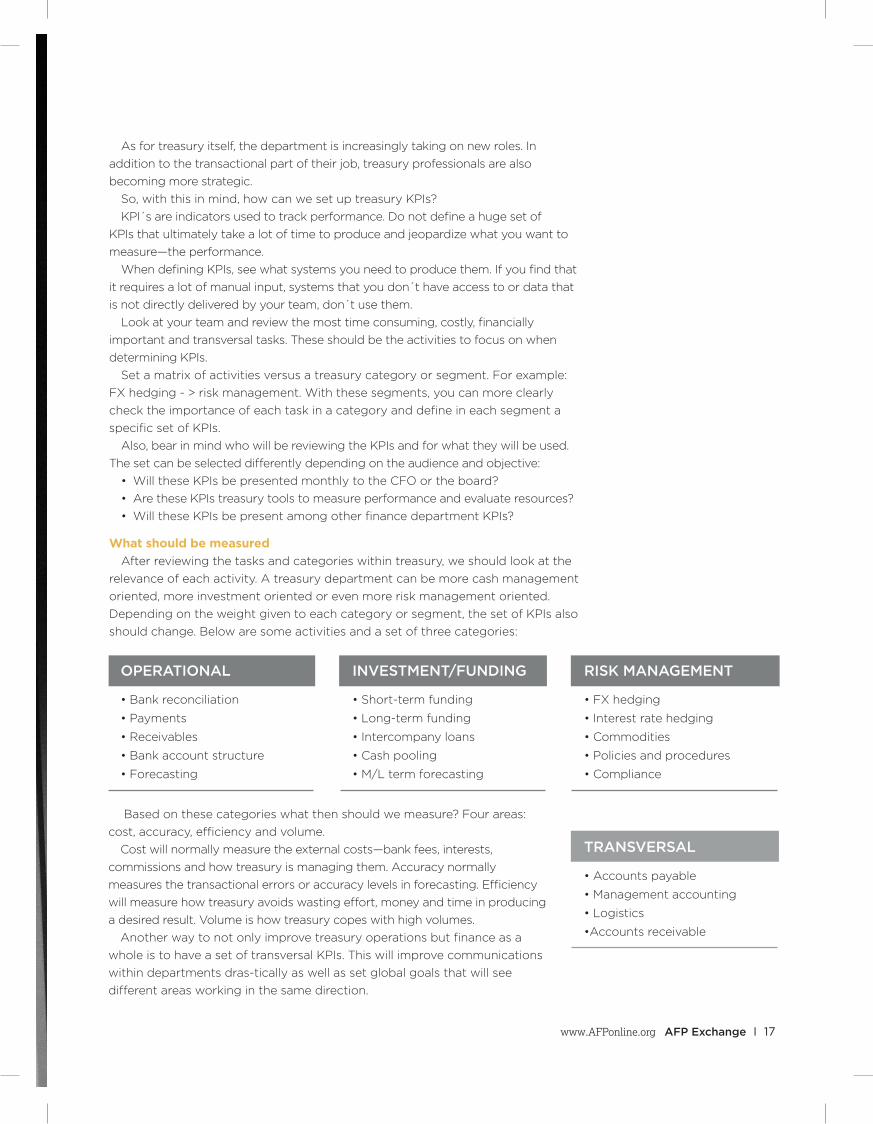

What should be measuredAfter reviewing the tasks and categories within treasury, we should look at the

relevance of each activity. A treasury department can be more cash management oriented, more investment oriented or even more risk management oriented. Depending on the weight given to each category or segment, the set of KPIs also should change. Below are some activities and a set of three categories:

Based on these categories what then should we measure? Four areas: cost, accuracy, efficiency and volume.

Cost will normally measure the external costs—bank fees, interests, commissions and how treasury is managing them. Accuracy normally measures the transactional errors or accuracy levels in forecasting. Efficiency will measure how treasury avoids wasting effort, money and time in producing a desired result. Volume is how treasury copes with high volumes.

Another way to not only improve treasury operations but finance as a whole is to have a set of transversal KPIs. This will improve communications within departments dras-tically as well as set global goals that will see different areas working in the same direction.

OPERATIONAL

• Bank reconciliation

• Payments

• Receivables

• Bank account structure

• Forecasting

TRANSVERSAL

• Accounts payable

• Management accounting

• Logistics

•Accounts receivable

INVESTMENT/FUNDING

• Short-term funding

• Long-term funding

• Intercompany loans

• Cash pooling

• M/L term forecasting

RISK MANAGEMENT

• FX hedging

• Interest rate hedging

• Commodities

• Policies and procedures

• Compliance

18 I AFP Exchange September 2016

GLOBAL TREASURER continued

Let´s now focus on each KPI area.Risk management KPIs

This KPI involves, normally there is an issue of different systems needing to produce information to provide the KPI measurement. There are three ways of dealing with it:

1. Having a front office system to interface all-important information to the back-office system—and then reporting is provided only by one system.

2. Having reporting tools that extract info from both systems, which can be helpful not only to report KPIs but to validate consistency of information between

two systems.3. Do it manually, extracting to Excel from

both system. Of course, this is not the recommended way as it will take time, increase reporting errors and require people to validate data.

Investment and funding KPIsFor investment and funding, we should

focus on monthly/quarterly reporting and not yearly reporting. We should measure not only how cash is used but also the cost of it and how accurate and efficient our teams are at handling the cash.

We can set KPIs to check compliance with the policies—like liquidity buffers—that translate the cash (or credit lines) available for future use. We should also have KPIs to check idle cash balances and inefficiencies in cash usage (as cost). And we can have KPIs to measure the back office and front-office efficiency and accuracy (FTE per number of products).

All will give management and also the board an overview of how cash is being used. This set is normally the most relevant for the board, so in this case they have to be very aligned with board strategy. Giving an example, if there is an investment to be made, the liquidity buffer needs to be readjusted and a different measure needs to be applied.

Operational KPIs These KPIs are normally used for a more

cash management-oriented treasury. They are great for evaluation purposes and to check that the department is up and running. They give transparency into the way evaluation is done within your department, and they can normally be benchmarked with cash-management functions at other companies.

These KPIs also allow us to measure individual staff members, or the department itself. And in this transactional level we should measure:

• How things are done, automatic versus manually (e.g., bank

reconciliation items). This will push the team to constantly optimize systems and processes.• The cost per transaction (cost per

payment, per rejected item, number of rejected items). This again will push the team to reduce costs and manual errors.

6Six Keys to Establishing Good KPIs

Give bonuses to staff members who achieve KPIs. After testing your KPIs and defining them, they should be linked to remuneration packages and evaluations—but only after implementation and some months of monitoring.

Do not define too many KPIs. KPIs are used to monitor efficiency, not to create more administrative tasks and burden everyone.

When defining KPIs, choose a three-layer set: board, management and operational. This will help the definition of the set.

Look carefully at the main task, the percentage of effort and the cost in each function activity. KPIs should focus on each of these.

Strategically choose the weight of each KPI.This should be based on where you want the team and the department to go.

Look carefully at where the information to report each KPI lives. The reporting of KPIs should be made easy, and interfaces or reporting tools may need to be created or amended.

www.AFPonline.org AFP Exchange I 19

• Bank account structure and FTE versus bank accounts. This will help reduce accounts, costs and give a good number of when you need to increase or decrease the number of FTEs.

• Measure transactions settled per FTE. This gives a value of efficiency and internal cost per transaction, a measure for evaluating each team member, and also a number to take into account when deciding about adding new members to the team or not.

• Idle balances measure. This is a great way to get the team working with an objective of streamlining bank structure, optimizing cash pooling structures and being more careful with these inefficiencies.

These KPIs are very important for management to have a clear idea how day-to-day business is being handled by the cash-management team. It’s also very important that KPIs take into account when treasury functions are centralized, to show to the board or management the benefits and costs of

Accounts Payable/Treasury

Accounts Payable/Treasury

Accounts Receivable/Treasury

Accounts Receivable/Treasury

Finance Department/Board

Finance Department? Board

Finance Department

Accounts payable/ Treasury/ Accounts Receivable/

Logistics and Supply Chain

Finance Department

Manual Generated Payment vs. All Payments

Percentage of failed payments due to incorrect data

Manual Generated Payment vs. All Payments

Accounts receivable divided by sales per day

Days to deposit cash/checks

Current Assets / Short + long term debt

Assets/Liabilities

Time required to complete monthly financial close activities vs. Benchmark

CCC = DIO + DSO - DPO

Number of FTE per Revenue

centralization and why that function will stay locally or central.

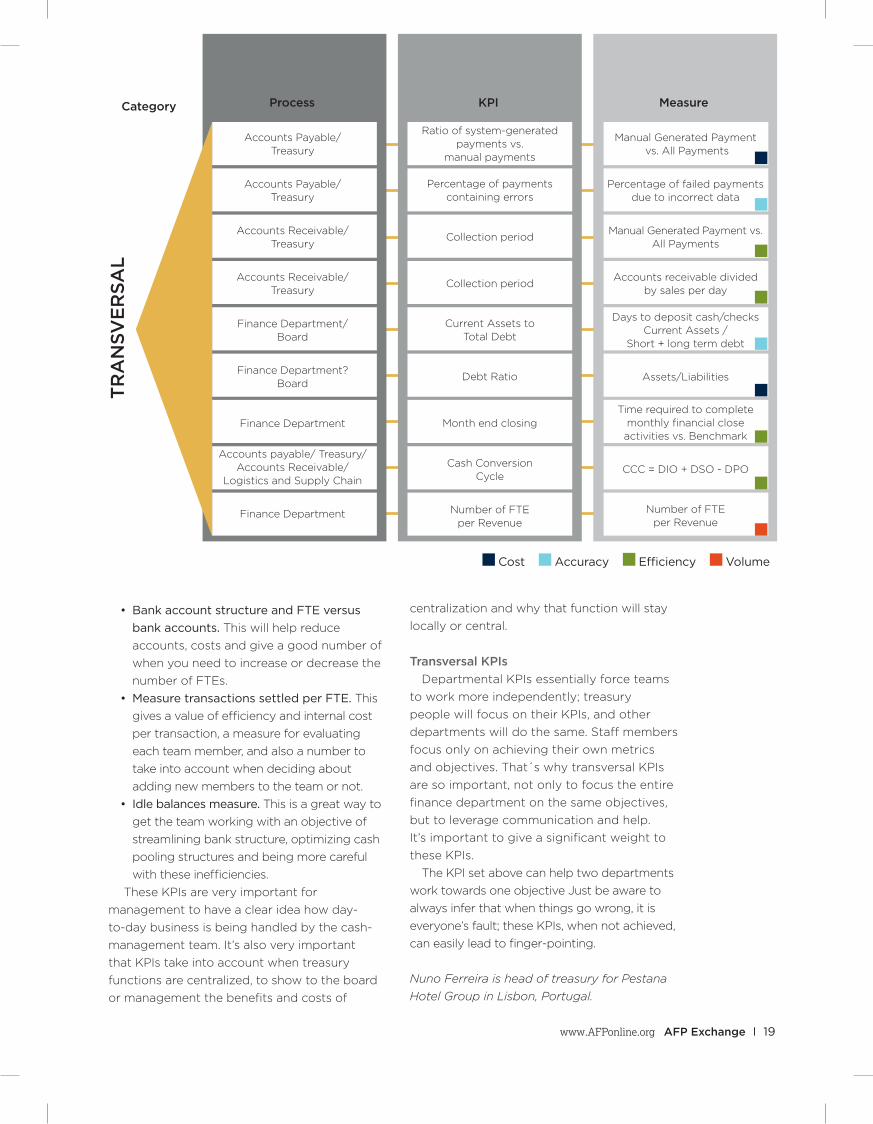

Transversal KPIs Departmental KPIs essentially force teams

to work more independently; treasury people will focus on their KPIs, and other departments will do the same. Staff members focus only on achieving their own metrics and objectives. That´s why transversal KPIs are so important, not only to focus the entire finance department on the same objectives, but to leverage communication and help. It’s important to give a significant weight to these KPIs.

The KPI set above can help two departments work towards one objective Just be aware to always infer that when things go wrong, it is everyone’s fault; these KPIs, when not achieved, can easily lead to finger-pointing.

Nuno Ferreira is head of treasury for Pestana Hotel Group in Lisbon, Portugal.

Category Process MeasureKPI

Ratio of system-generated payments vs.

manual payments

Percentage of payments containing errors

Collection period

Collection period

Current Assets to Total Debt

Debt Ratio

Month end closing

Cash ConversionCycle

Number of FTE per Revenue

TRA

NSV

ER

SAL

Cost Accuracy Efficiency Volume