medical supplies and devices

TRANSCRIPT

May 12, 2016

Reason for report:

PROPRIETARY INSIGHTS

Richard Newitter(212) [email protected]

Danielle Antalffy(212) [email protected]

Ravi Misra(212) [email protected]

Puneet Souda(212) [email protected]

MEDICAL SUPPLIES AND DEVICESTakeaways From West Coast MedTech Doc Day

• Bottom Line: Key highlights from our discussions with 11MEDACorp specialists below and additional detail on p3.

• Hospital Admins: Utilization Up Though Likely To Normalize/Bundled Payment Nearer-Term Focus Remains on Post-AcuteCare/Scale Still Viewed as Important. Specialists noted an uptick inadmissions/volumes in 1Q -- consistent with strong utilization trends thathave been broadly reported across MedTech this quarter. While volumesare likely to stabilize, currently this patient inflow is having a negativemargin impact, as incoming newer patients are higher risk. Consistent withrecent checks with other hospital admins (LINK) on bundled payments:1) the biggest priority is migrating care from the inpatient to ambulatory/outpatient settings; 2) bundled payment models will likely expand intoother service lines and institution's will focus on patient selection anddownstream costs before revisiting implant pricing, and 3) device multi-linecontracting is on the rise (scale matters).

• Neuromodulation could be on the cusp of significant growthinflection. Our neuromodulation specialist brought up several tailwindsthat should expand use of SCS devices, with volumes potentiallyincreasing 2-3x in the next few years and beneficial for all playersincluding STJ [OP], NVRO [OP], BSX [OP], and MDT [MP]. NVROhas been gaining share in and growing his practice, with nearly all of hispredominant back pain patients receiving a Senza given the stronglysupportive data as well as a significant increase in trial to permanentimplant rates (now over 80% from ~50% previously).

• “Leave nothing behind” trend bodes well for drug coated balloon(DCB) adoption. DCB adoption has been gaining share in our specialist'spractice and he has a positive view on increasing adoption as indicationsexpand. Regarding new entrants (i.e., SPNC’s [NR] Stellarx), early dataappears encouraging in his view, but his institution would find it difficult tostock all three DCBs if approved. Product breadth is an important factorin this service line that could ultimately limit manufacturers without adiversified portfolio, which we think bodes well for MDT [MP] and BCR’s[MP] and their ability to maintain share within this expanding mktlonger term in our view.

• Spine discussion focuses on better management of surgeries andnew technologies. Patient stratification is becoming more important asinstitutions manage outcomes across the continuum of care. While thereis no bundled payment program in spine tied to outcomes, the specialist/institution’s processes are in sync with outcomes based approachestowards case management. From a product perspective, the specialistprefers SYK’s [OP] expandable interbody over GMED [OP] thoughnoted that GMED’s usage could be higher if the company could supplymore biologics, a position that we view as supportive of GMED’s ongoinginvestments in biologics. He thinks NUVA [OP] is positioned well in his

S&P 500 Health Care Index: 800.22

Companies Highlighted:ABT, BCR, BSX, CNMD, CSII, EW, GMED, HTWR,

ISRG, IVTY, JNJ, MDT, NUVA, NVRO, STJ, SYK

Please refer to Pages 12 - 13 for Analyst Certification and important disclosures. Price charts and disclosures specific tocovered companies and statements of valuation and risk are available athttps://leerink2.bluematrix.com/bluematrix/Disclosure2 or by contacting Leerink Partners Editorial Department, OneFederal Street, 37th Floor, Boston, MA 02110.

MEDICAL SUPPLIES AND DEVICES May 12, 2016

practice and has captured 60-70% of his lateral cases, and thinksEllipse will allow NUVA to gain market share in early onset scoliosis, andopen an opportunity for NUVA [OP] to pull through screws/rods sales overtime.

• Case for robotics is becoming more compelling according togeneral surgeon. The specialist views robotics as a “must have”technology with better outcomes and perhaps even cost equivalence vs.lap in hernia (giving us increased confidence in sustainability of DDprocedure growth for ISRG [OP]). He was positive on CNMD’s [OP]Airseal ("nice to have," used in all robotic cases except inguinal hernia).He was particularly bullish about IVTY's [OP] illumination platformwhich he considers “must-have” and expects will gradually get usedin 100% of his mastectomy cases---he is working to push this through hishospital's value access committee, and thinks approval will come shortly.

• In electrophysiology, ablation volumes growing double-digits whileCRM seeing share shift to MRI compatible devices. The EP specialistbelieves ablation volumes have increased 20%+ in some cases vs.our ~10% AF ablation market estimate. With higher success ratesand shorter procedure times from contact force sensing catheters(JNJ [OP] and STJ), his institution is taking a more aggressive approachto patient treatment and in some cases shifting treatment paradigms;ablation is now preferred as an earlier intervention vs. drug therapy.He also uses MDT’s Arctic Front cryoballoon in most of his paroxysmalpatients and even some persistent patients. Within CRM, he views MRIcompatibility as the most motivating factor in device choice. Because ofthis, he’s moved the majority of his cases towards MDT and Biotronik overthe last few years but does believe he will likely shift share back to STJonce the company launches its own MRI compatible systems.

• Intermediate risk indication set to drive dramatic growth in TAVRadoption, TMVR still early. With an upcoming intermediate risk approval– possible in late 3Q16/early 4Q16 according to EW – the interventionalcardiology specialist believes that TAVR volumes are poised for20%-30% growth overall. And ultimately, he thinks TAVR canpenetrate nearly 100% of the intermediate risk patient population,which we believe represents the size of high risk and inoperablepatients combined. This physician – a key thought leader in mitralsurgery – believes that TMVR is still over a decade away from becominga truly viable and commercializable technology like TAVR though mitralremains a highly underpenetrated and undertreated disease state.

• In Neurovascular, interventional radiologist expects MechanicalTherapy (MT) to increase as a % of a still underpenetrated ischemicstroke intervention mkt oppt'y; though he is cautious about overutilization down the road. The MRCLEAN study has led to an inflectionin the specialist's stroke volumes, and he sees room for higher penetrationin the US where treatment using mechanical retrievers is just <2%penetrated (15K of 800K ischemic strokes/year) but one that could becapped in his view as he believes brain vessel physiology and strokediagnosis limitations (i.e. timing) could lead to diminishing returns beyond~50K treatments/year (~6% penetration), in his view. Overall, theconversation suggests there is a significantly greater role for MT instroke that should continue to provide meaningful DD growth runwayfor the next several years at least within MDT's, SYK's and PEN's[NR] neurovascular franchises.

2

Doc Day: A Deep Dive into Physician Views across Multiple Specialties We hosted a doc day in San Francisco, CA last week with MEDACorp physicians across a

number of key MedTech specialties to assess market growth outlooks and key technologies

driving growth and share shifts within each specialty. Below, we provide highlights from our

discussions with 11 physicians and hospital administrators covering a range of topics

including the outlook on utilization and reimbursement, as well as in-depth discussions on

each specialist’s service lines and views on new technologies.

Hospital Admins: Utilization Up Though Likely To Normalize/Bundled Payment

Commentary Focuses on Downstream Costs/Scale Still Viewed as Important. The

hospital administrators included the interim CEO of the institute, the chairman of the

orthopedic surgery department, and the director of accountable care. On the utilization front,

volumes have been up at their institution, with both hospitals operating at maximum capacity.

The admins attributed the recent uptick in admissions to residual effects of the ACA that is

allowing previously uninsured patients access to care, which could account in part for the

recent Q1 sales and earnings strength across MedTech broadly. While these admins think

volumes are likely to stabilize, currently this patient inflow is having a negative margin impact,

as incoming newer patients are higher risk patients.

On bundled payments, all three echoed commentary that we’ve heard from our recent checks

with other hospital admins (LINK), namely 1) the biggest priority is migrating care from the

inpatient to ambulatory/outpatient settings, 2) bundled payment models will likely expand into

other service lines – the next most logical service line being cardiology/heart failure while

they believed spine was actually still several years off from falling under this payment model

– with institutions continuing to focus on patient selection and downstream costs before

revisiting implant pricing, and 3) device bundling across service lines is likely to increase and

scale is important for both the buyer and the seller of devices.

Nearer term, the admins’ priorities are on care coordination as new Medicare payment

models such as CJR and BPCI become more prominent. With payment now tied to

outcomes/readmissions, the specialists are looking to reduce readmissions which they

believe are related more to post-discharge care than to surgery. Thus not only are admins

looking for better coordination with rehab/nursing facilities, they are also looking for better

ways to screen patients before surgery (something we heard from orthopedic surgeons at

NASS as well) and maintain contact with patients through outreach programs such as

telemedicine and other patient engagement products. One theme that emerged during our

Q&A was that there will likely be a continuing trend of risk stratification among patients, both

in terms of which patients are eligible for surgery, as well as in terms of where higher risk

patients get treated (i.e. shunting complex cases to more specialized or academic centers).

Longer term, these admins plan to turn back towards reducing device costs once they get

through the downstream care coordination process. Still, the focus on post-acute care

3

MEDICAL SUPPLIES AND DEVICES May 12, 2016

remains the “low hanging fruit’ and will take 2-3 years before they can refocus on implant

prices. In orthopedics for example, implant remains the most costly line item in the surgical

stay, and looking forward administrators plan to reduce this expense by:

Dissuading surgeon preference by negotiating one shelf price for all implants.

Currently UCSF orthopedic surgeons pick implants off a color coded chart stratified

by implant price; or

Moving to a bundled purchase option with tiered service plans. The specialists noted

that Cardinal Health (OP) offers trauma implants at a lower cost as they can “make

up the difference” on other service lines in the hospital (a scale strategy which we

think could apply to MDT [MP]/JNJ [OP] as well). Moreover, the ortho specialist noted

that Cardinal is developing tiered service plans depending on levels of rep support.

And while the admins have seen this low cost/reduced service implant model begin

to play out in ortho, they believe it will extend into other service lines, with these

admins calling out cardiology/heart failure as the next most logical target with spine

still several years away. That said, the ortho admin continues to think reps will have

an important role and will never be fully eliminated from the OR, both in the

community setting (to help the surgeons that perform 1-2 cases/year) as well as in

academic centers (having reps in the OR for medium/complex cases is cost effective

because they can help move the case through and save on OR time).

Scale was again reiterated as a key factor for both providers and manufacturers. From the

hospital perspective, the specialists believe there will be additional consolidation and

centralization of volumes at academic/specialized centers. In their view this should benefit

large chains as they will have even greater leverage on device prices. For manufacturers, the

admins noted that multi-service line purchasing does not yet exist at UCSF, but that

expanding bundled payment programs (i.e. cardiac/heart failure is expected by 2018) is likely

to make the institution more amenable to multiline contracting.

Neuromodulation Growth on the Cusp of Major Inflection. Our neuromodulation

MEDACorp specialist believes there are a number of tailwinds that should expand use of

SCS (Spinal Cord Stimulation) devices, ultimately anticipating a 2x-3x increase in volumes

over the next few years. A number of favorable dynamics support his view, including: 1) the

FDA/CDC focus on better pain control as reduction in opioid usage is likely to turn attention to

alternative pain management therapy including SCS; 2) an expanding neuromodulation

device selection that is already broadening treatment – i.e. NVRO’s [OP] Senza in

predominant back pain and STJ’s [OP] DRG in extremities pain – and bound to expand

further into new indications and non-traditional areas including pre-surgical pain

management, chronic angina, peripheral pain and IBD; 3) use of therapy earlier in the

treatment paradigm rather than its traditional position as an end-stage therapy for pain

management before moving onto drug pumps – a shift this physician believes is being driven

by NVRO’s Senza HF10 therapy. With NVRO’s Senza, which this physician now uses in

nearly any and all predominant back pain patients – ~1/3 of total chronic pain patients, based

4

MEDICAL SUPPLIES AND DEVICES May 12, 2016

on our estimates – with Senza pushing trial to implant success rates to 80%+ from ~50%

previously.

Taken together the MEDACorp physician commentary is supportive of all players – MDT,

BSX [OP], STJ, and NVRO – in the broader neuromodulation and specifically within the SCS

market in the near to medium term. Beyond NVRO’s Senza, this physician noted other

interesting technologies and/or important features, including: (1) STJ’s Burst therapy –

expected to launch in the U.S. in 2H16 and Dorsal Root Ganglion stimulation (DRG) currently

launching in U.S.; (2) MDT’s full-body MRI products, which he believes does help MDT

defend against current share shift to an extent but also noted that all devices will eventually

have MRI compatibility; and (3) StimWave, wireless technology that reduces the implant size

by externalizing the battery allowing the therapy to penetrate additional areas and Nalu,

another wireless technology delivering pain relief which is still in early stages of development.

The physician specialist noted that the number of neuromodulation devices have doubled in

the last two years and should double again in two years. And while MRI compatibility is an

important feature that previously restricted his usage primarily to MDT, an expanding number

of indications has helped spur adoption of other devices.

Clinical data is also helping drive utilization according to this physician, and this has been led

almost entirely by NVRO’s Senza RCT – the first randomized controlled trial within SCS that

demonstrated sustained superiority to a conventional device. While the majority of SCS

devices are placed in private practice, and academic centers have historically not had the

leading edge, that is likely to change given the innovation in the space and number of trials

enrolling as a result of these new devices, with more data only raising awareness. This

physician believes that the decision making process has gone from whether to use

neuromodulation to which device offers the best solution for the patient’s therapeutic needs –

definitely representing a sea change from earlier approaches to the treatment paradigm for

chronic pain patients. Ultimately, he believes different devices are better suited to different

patients, and with more device options available, physicians will be able to tailor therapy to

better meet each patients’ needs based on factors like location and intensity of pain, to name

a few.

“Leave nothing behind” trend bodes well for drug coated balloon adoption. The

peripheral vascular specialist performs a broad range of procedures including atherectomy,

stenting, drug coated balloons (DCB), and abdominal aortic aneurysm repair (AAA). DCB is

used in ~20% of his overall practice currently (in his SFA/popliteal cases) and has gained

share at the expense of stent usage. Over time, he continues to see DCB usage increasing,

particularly in combination with atherectomy and as surgeons move towards “leaving nothing

behind” (i.e. no stents left in the vasculature). As well, he sees utility in in-stent restenosis

cases, where DCBs are being currently used off-label as a standalone first line therapy at his

institution and BCR [MP] plans to submit a PMA application to the FDA for this indication by

3Q16. The specialist also has a favorable view on other label expanding indications for DCBs

such as dialysis access, which represents a “dramatically larger market” vs. SFA/pop. As a

5

MEDICAL SUPPLIES AND DEVICES May 12, 2016

reminder, BCR’s AV access trial completed enrollment in 1Q16 and expectations are for a

PMA submission in 1Q17 and US launch by 2H17.

The specialist noted that MDT’s In.pact is the preferred DCB at his institution and used in

60% of procedures (vs. 40% for Lutonix) given the slightly better clinical data. That said, he

thinks that embolization could be more of a risk with MDT’s In.pact (we think potentially tied

to higher paclitaxel level on the balloon vs. Lutonix), but this hasn’t affected his usage and he

believes it’s too early to gauge whether/how much of an issue this may or may not become.

Regarding SPNC’s [Not Rated] Stellarx, the early data appears encouraging in his view, but

his institution would find it difficult to stock all three DCBs if/when Stellarx is approved. In his

view, product breadth is important and a lack thereof for SPNC could limit the willingness to

purchase from a manufacturer that specializes exclusively in this area (e.g. bodes well for

diversified operators like MDT and BCR and their ability to maintain share longer term in our

view).

On the atherectomy front, he noted that it represents 10-20% of his volumes, and he’s using

the devices in combination with DCBs in cases with calcified lesions. The specialist’s primary

device is MDT’s Silverhawk, and while they do use CSII’s (MP) Stealth/Diamondback in the

cath lab, he personally has been satisfied with Silverhawk’s outcomes. The physician was

less enthusiastic about SPNC’s laser atherectomy given the high cost and limited utility,

though he does find it useful in CTO crossing cases.

Spine discussion focused on better management of surgeries and new technologies.

The spine specialist noted that 60% of his institution’s volumes are in revision and, in his

view, the largest opportunity for innovation will be around technologies that can limit

revisions, reoperations, and readmissions. As in the orthopedic surgeon’s practice, this

specialist noted that patient stratification is becoming more important as institutions manage

outcomes across the continuum of care (pre- to post-operative). While there is no bundled

payment program in spine tied to outcomes, the surgeon/institution’s processes are in sync

with outcomes based approaches towards case management. His institution provides fitness

trackers to all patients to assess movement and physiology pre- and post-surgery, with this

specialist not operating on patients with BMI >35 (4x more likely to be readmitted according

to data at his institution) and preferring to send patients home after surgery vs. rehab (fewer

readmissions). He is also trying to form a multidisciplinary panel at the institution that would

review and greenlight complex cases to avoid unnecessary surgery.

The specialist also believes that the number of spine procedures done in outpatient settings

will increase to ~30% over the next few years vs. 15% today. He sees an addressable pool of

~300K surgeries with cervical/lumbar stenosis that could be suited to the outpatient

approach, including discectomies, laminotomies and cervical laminotomies. The advantages

to outpatient in his view include improved surgical efficiency, patient convenience, lower cost,

and more profitable for the surgeons (if they have ownership stakes in the outpatient

facilities). That said, he noted that insurers haven’t been pushing institutions to perform more

6

MEDICAL SUPPLIES AND DEVICES May 12, 2016

surgeries out of the hospital; we think this could be a result of limited comparative outcomes

around readmissions/reoperations in outpatient spine vs. inpatient.

On implant price, the institution allows any vendor to compete as long as they can match the

set formulary pricing. This currently translates to MDT/JNJ splitting the majority of the

institution’s caseloads, followed by NUVA [OP], and then SYK [OP]/GMED [OP] getting the

remaining cases. The specialist primarily uses MDT, followed by SYK, then GMED/NUVA

tied for third, and he uses NUVA in 60%-70% of his direct lateral cases.

Product-wise, the specialist has favorable views on SYK and NUVA. He prefers SYK’s

expandable interbody (Coalign) to GMED and Spinewave, though noted that GMED’s usage

could be higher if the company could supply more biologics, a position that we view as

supportive of a positive ROI from GMED’s ongoing investments in biologics. While this

specialist does not perform many early onset scoliosis cases, he believes that Ellipse will

allow NUVA to gain market share in this segment and that there will be an opportunity for

NUVA to pull through screws/rods sales with Ellipse.

General surgeon believes case for robotics is becoming more compelling. Our general

surgeon performs a mix of open/lap/robotic procedures and his robotic procedures have been

increasing (32 in ’15, 10 ytd) as ISRG’s Xi launch rekindled his interest in the technology,

particularly in ventral hernia. In his view, robotics is a “must have” technology. Currently, his

institution has an Si machine which is primarily used by urologists/ob-gyns and is close to

purchasing an Xi system (with table motion, “a big deal that will facilitate colorectal

resections”) with installation expected by the summer.

The specialist views robotics as a game changer in ventral hernia repair and cited the

advantages of suturing and repairing the primary defect with mesh as more effective and also

less fatiguing than laparoscopy. Currently he performs ~50% of his ventral hernia cases

using the robot and plans to increase that to 70%-80% as table motion and multiquadrant

capabilities make it easier for him to do more cases.

Cost has been a key pushback for robotics usage vs. lap, and this specialist doesn’t see

instrument costs as substantially higher in ventral hernia procedures vs. lap. In his view,

robotics is actually enabling him to do cases even faster. In inguinal hernia, he noted that the

cost factor is also negligibly different, although he sees less utility for robotics and only uses it

in recurring inguinal hernia cases.

We continue to view general surgery as a key growth driver for ISRG [OP], and we believe

the company will be able to deliver double-digit procedure growth for the next 2-3 years on

the back of ongoing dV utilization in hernia and colorectal. The surgeon’s comments that

every fellowship trained colorectal surgeon undergoes robotic training should also act as a

long term tailwind that favors robotics adoption.

The specialist also had positive commentary around CNMD’s [OP] Airseal, which he uses in

all robot cases except inguinal hernia, and sees it as a “nice to have” technology. In breast

surgery, the specialist called IVTY [OP] a “must have” technology that would be used in all of

7

MEDICAL SUPPLIES AND DEVICES May 12, 2016

his ~15 mastectomies/year, and he likes the clinical literature findings around fewer patient

burns and faster OR times. Still, the product is going through value analysis committee and,

while it has been approved, he hasn’t received it yet.

In electrophysiology, ablation volumes growing double-digits while CRM seeing share

shift to MRI compatible devices. The electrophysiology (EP) specialist estimates that his

caseload split is 50/50 between implants and ablation, but he noted that while his implant

volumes have been flat over the last five years, ablation volumes have increased significantly

– 20%+ in some cases vs. our ~10% AF ablation market estimate. New products that can

ablate deeper and sense muscle contact – notably contact force sensing catheters from both

JNJ and STJ – have led to increased success rates (~5% points better) and reduced

procedure time by 20-30 mins. As a result, the institute is taking a more aggressive approach

to patient treatment and in some cases shifting treatment paradigms; ablation is now

preferred as an earlier intervention vs. drug therapy, with this shift likely only accelerating as

awareness within the referral chain continues to grow. He also uses MDT’s Arctic Front

cryoballoon in most of his paroxysmal patients and even some persistent patients given what

he believes are even higher success rates – 10-12 points – and a significant reduction of an

hour or more in OR time. This, in his view, is more than enough to offset the price premium

for the cryoballoon.

Contact force sensing catheters have also prompted more treatment of persistent AF

patients. This physician initially tried to limit his use of contact force sensing catheters given

the price premium. But after gaining some experience with these devices, he’s now shifted

almost 100% of his cases to contact force sensing catheters given the higher success rates

and shorter procedure times. From a product perspective, he believes JNJ’s ThermoCool and

STJ’s TactiCath catheters are similar; however, he personally prefers the visualization

capabilities and open architecture of STJ’s EnSite mapping system vs. JNJ’s Carto. For BSX,

this physician seemed to imply that the company is a bit late to the game within AF ablation

given an already-large installed base for both STJ and JNJ. At his institution, BSX’s Rhythmia

mapping system was considered for the 3rd

mapping system, but they ultimately purchased a

2nd

Carto due to physician preference and experience. In his view, BSX may have trouble

penetrating the AF ablation market given that he believes their mapping system feature set is

not dramatic enough to prompt switches and the company’s MiFi catheter has shown a

limited incremental benefit at a higher cost. He also discussed other technologies, including:

(1) CardioFocus, a balloon catheter that uses laser energy to ablate pulmonary veins, that

requires a separate energy source relative to cryo but might not be as effective in his view,

(2) ABT’s [MP] Topera, of which he was skeptical based on difficulty replicating clinical trial

results in real-world practice; and, (3) STJ’s MediGuide, which reduces fluoro time and which

he deems “interesting, but not necessary”.

Within cardiac rhythm management (CRM), he views MRI compatibility as the most

motivating factor in device choice as most patients will eventually require an MRI. Because of

this, he’s moved the majority of his cases towards MDT and Biotronik over the last few years,

8

MEDICAL SUPPLIES AND DEVICES May 12, 2016

as both have been the only manufacturers with MRI-safe technology on the market. He noted

that while STJ will likely continue to donate share in the near-term, he is likely to shift share

back to STJ once the company launches its own MRI compatible systems with a pacer

expected in 2H16 and high power devices expected in early 2017. He also believes that

STJ’s MPP (MultiPoint Pacing) CRT-P technology is an important innovation that could drive

incremental share shift in favor of STJ, but he believes this is a niche patient population

limited to those patients with ejection fractions of 35%-40%. Still, he plans to double his CRT-

P cases in 2016 vs. 2015 based on the availability of this technology.

Intermediate risk indication set to drive dramatic growth in TAVR adoption, TMVR still

early. The interventional cardiology specialist noted that they do ~50 TAVR (Transcatheter

Aortic Valve Replacement) implants per year at his institution, 80% EW’s [OP] Sapien 3 and

20% MDT’s Evolut R given that he is a proctor for EW. With an upcoming intermediate risk

approval – possible in late 3Q16/early 4Q16 according to EW – he believes that TAVR

volumes are poised for 20%-30% growth overall. And ultimately, he thinks TAVR can

penetrate nearly 100% of the intermediate risk patient population, which we believe

represents the size of high risk and inoperable patients combined. He does believe, however,

that ~10%-20% of TAVR patients today are already intermediate risk. From a product

perspective, he noted his preference for Sapien 3 based on ease of delivery. For BSX’s Lotus

– which could launch in the U.S. in late 2017/early 2018 – this physician does not view

recapturability/repositionability as an important or key differentiating feature and thus does

not see meaningful competition for either EW or MDT in the near-term at his practice.

This physician – a key thought leader in mitral surgery – believes that TMVR (Transcatheter

Mitral Valve Replacement) is still over a decade away from becoming a truly viable and

commercializable technology like TAVR though mitral remains a highly underpenetrated and

undertreated disease state. This is due to difficult and non-homogenous anatomy of the mitral

valve, and difficult delivery of the current devices under development – all of which will drive a

more difficult learning curve vs. TAVR. He did note that MDT’s Twelve looks most appealing

to him from an architecture perspective. Lastly, the cardiac surgeon specialist who was also

present discussed LVADs (Left Ventricular Assist Devices) – relevant to both HTWR [OP]

and STJ – expressing enthusiasm for STJ’s next-gen HeartMate 3 now in clinical trials in the

U.S. based on CE Mark trial data presented to-date. However, he also noted that the first

manufacturer that brings a fully implantable system to market that also delivers on outcomes

will be the winner longer-term.

In Neurovascular, interventional radiologist expects Mechanical Therapy (MT) to

increase as a % of a still underpenetrated ischemic stroke intervention mkt

opportunity; though he is cautious about over utilization down the road. The

neurovascular specialist pointed to an increase in stroke interventions in 2015 following the

publication of the MRCLEAN study which showed that endovascular intervention within six

hours was more effective than using TPA alone and challenged the prevailing mindset

resulting from the IMS3 trial conclusions in 2013. As a result, stroke volumes in his institution

9

MEDICAL SUPPLIES AND DEVICES May 12, 2016

have doubled (50 in 2015, vs. 20-30/year after IMS3 vs. 20-40/year pre-IMS3). In his practice

he uses a combination of stentrievers and aspiration in 40-50% of his cases, with aspiration

in more proximal clot burdens (<25% of cases) and stentrievers alone in distal lesions (the

remaining 25-35%). The specialist noted that cost isn’t a consideration in his device selection

and that he’ll use SYK’s Trevo and MDT’s Solitaire interchangeably, but pricing could

become more of an issue as more competitors eventually enter the space (i.e., PEN and

Phenox). As a reminder, PEN has a stentriever in development (Separator 3D, FDA

submission expected by year end 2016). This device will likely be the only device with an

official on label indication for combined aspiration stentriever therapy – currently the two

devices are used in combination with one another, but off label. Interestingly the specialist

said that he does not expect an on label indication to have an effect on operator willingness

to use the device and does not view it as a competitive advantage. In his practice he thinks

PEN could gain traction with a stentriever and our sense is that it would probably come down

to price.

Looking forward, procedure growth at his institution is likely to be limited but this is due to

localized conditions in the region; there are several neurovascular operators in the SF area,

and the population has a lower stroke risk. However, the specialist sees room for higher

penetration but one that could be capped, given brain vessel physiology, the occult nature of

stroke and the difficulty in diagnosing stroke and current lack of data that demonstrates utility

of MT outside of 6 hours. Still, he thinks MT is clearly the preferred treatment protocol and it

should be the method of treatment when intervention is required and that MT remains

underpenetrated relative to its longer term potential.

He expects utilization both within his practice and within industry at large to increase rapidly

over the next several years. In 2015 we estimate 15K procedures representing 2%

penetration out of ~800K stroke opportunity. And for his part, the specialist thinks that market

could reach 50K interventions going forward.

But, he did caution there might be a point of diminishing returns unless diagnosis of stroke

(i.e. timing/identification of symptoms) can be improved as he thinks intervention may have

limited potential for outcome improvement if too much time has elapsed. He thinks it might

even prove to be outcome negative to intervene in such cases (where it’s “too late”).

Two studies are currently underway to assess how far beyond 6 hours you can go for

successful mechanical intervention. Per clinicaltrials.gov:

DAWN, to evaluate the hypothesis that Trevo thrombectomy plus medical

management leads to superior clinical outcomes at 90 days as compared to medical

management alone in appropriately selected subjects experiencing an acute

ischemic stroke when treatment is initiated within 6-24 hours after last seen well; and

DEFUSE, to evaluate the hypothesis that FDA cleared thrombectomy devices plus

medical management leads to superior clinical outcomes in acute ischemic stroke

patients at 90 days when compared to medical management alone in appropriately

10

MEDICAL SUPPLIES AND DEVICES May 12, 2016

selected subjects with the Target mismatch profile and an MCA (M1 segment) or ICA

occlusion who can be randomized and have endovascular treatment initiated

between 6-16 hours after last seen well.

11

MEDICAL SUPPLIES AND DEVICES May 12, 2016

MEDICAL SUPPLIES AND DEVICES May 12, 2016

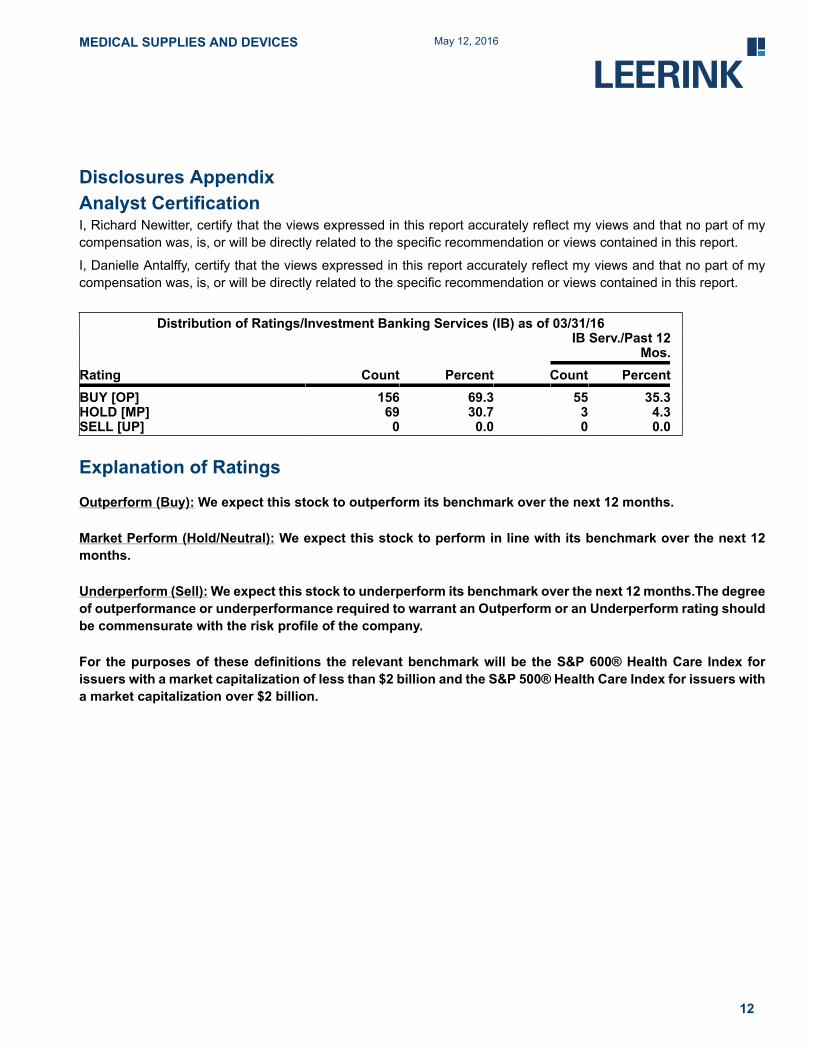

Disclosures AppendixAnalyst CertificationI, Richard Newitter, certify that the views expressed in this report accurately reflect my views and that no part of mycompensation was, is, or will be directly related to the specific recommendation or views contained in this report.

I, Danielle Antalffy, certify that the views expressed in this report accurately reflect my views and that no part of mycompensation was, is, or will be directly related to the specific recommendation or views contained in this report.

Distribution of Ratings/Investment Banking Services (IB) as of 03/31/16IB Serv./Past 12

Mos.Rating Count Percent Count PercentBUY [OP] 156 69.3 55 35.3HOLD [MP] 69 30.7 3 4.3SELL [UP] 0 0.0 0 0.0

Explanation of Ratings

Outperform (Buy): We expect this stock to outperform its benchmark over the next 12 months.

Market Perform (Hold/Neutral): We expect this stock to perform in line with its benchmark over the next 12months.

Underperform (Sell): We expect this stock to underperform its benchmark over the next 12 months.The degreeof outperformance or underperformance required to warrant an Outperform or an Underperform rating shouldbe commensurate with the risk profile of the company.

For the purposes of these definitions the relevant benchmark will be the S&P 600® Health Care Index forissuers with a market capitalization of less than $2 billion and the S&P 500® Health Care Index for issuers witha market capitalization over $2 billion.

12

MEDICAL SUPPLIES AND DEVICES May 12, 2016

Important Disclosures

This information (including, but not limited to, prices, quotes and statistics) has been obtained from sourcesthat we believe reliable, but we do not represent that it is accurate or complete and it should not be reliedupon as such. All information is subject to change without notice. This is provided for information purposesonly and should not be regarded as an offer to sell or as a solicitation of an offer to buy any product to whichthis information relates. The Firm, its officers, directors, employees, proprietary accounts and affiliates mayhave a position, long or short, in the securities referred to in this report, and/or other related securities, andfrom time to time may increase or decrease the position or express a view that is contrary to that containedin this report. The Firm's salespeople, traders and other professionals may provide oral or written marketcommentary or trading strategies that are contrary to opinions expressed in this report. The Firm's proprietaryaccounts may make investment decisions that are inconsistent with the opinions expressed in this report.The past performance of securities does not guarantee or predict future performance. Transaction strategiesdescribed herein may not be suitable for all investors. Additional information is available upon request bycontacting the Editorial Department at One Federal Street, 37th Floor, Boston, MA 02110.

Like all Firm employees, analysts receive compensation that is impacted by, among other factors, overall firmprofitability, which includes revenues from, among other business units, Institutional Equities, and InvestmentBanking. Analysts, however, are not compensated for a specific investment banking services transaction orcontributions to the Firm's investment banking activities.

MEDACorp is a network of healthcare professionals, attorneys, physicians, key opinion leaders and otherspecialists accessed by Leerink and it provides information used by its analysts in preparing research.

For price charts, statements of valuation and risk, as well as the specific disclosures for covered companies,client should refer to https://leerink2.bluematrix.com/bluematrix/Disclosure2 or send a request to LeerinkPartners Editorial Department, One Federal Street, 37th Floor, Boston, MA 02110.

Member FINRA/SIPC. ©2016 Leerink Partners LLC. All rights reserved. This document may not be reproducedor circulated without our written authority.

13

LEERINK PARTNERS LLC EQUITY RESEARCH

Director of Equity Research John L. Sullivan, CFA (617) 918-4875 [email protected]

Associate Director of Research Alice C. Avanian, CFA (617) 918-4544 [email protected]

Associate Director of Research James Kelly (212) 277-6096 [email protected] Director of Therapeutic Research Geoffrey C. Porges, MBBS (212) 277-6092 [email protected] Major Pharmaceuticals Seamus Fernandez (617) 918-4011 [email protected]

Le-Yi Wang, Ph.D. (617) 918-4568 [email protected] Specialty Pharmaceuticals Jason M. Gerberry, JD (617) 918-4549 [email protected]

Derek C. Archila (617) 918-4851 [email protected]

Etzer Darout, Ph.D. (617) 918-4020 [email protected] Large Cap Biotechnology Geoffrey C. Porges, MBBS (212) 277-6092 [email protected]

Mid and Small Cap Biotechnology Joseph P. Schwartz (617) 918-4575 [email protected]

Seamus Fernandez (617) 918-4011 [email protected]

Michael Schmidt, Ph.D. (617) 918-4588 [email protected]

Paul Matteis (617) 918-4585 [email protected]

Jonathan Chang, Ph.D. (617) 918-4015 [email protected]

Richard Goss (617) 918-4059 [email protected]

Dae Gon Ha, Ph.D. (617) 918-4093 [email protected]

Brett Larson (617) 918-4039 [email protected]

Mark Sevecka, Ph.D. (617) 918-4022 [email protected]

Assaf Vestin, Ph.D. (212) 277-6073 [email protected] Life Science Tools & Diagnostics Dan Leonard (212) 277-6116 [email protected]

Kevin C. Chen (212) 277-6045 [email protected]

Michael A. Sarcone, CFA (212) 277-6013 [email protected] Medical Devices, Cardiology Danielle Antalffy (212) 277-6044 [email protected]

Puneet Souda (212) 277-6091 [email protected]

Medical Devices, Orthopedics Richard Newitter (212) 277-6088 [email protected]

Ravi Misra (212) 277-6049 [email protected] Healthcare Services, Managed Ana Gupte, Ph.D. (212) 277-6040 [email protected] Care & Facilities Healthcare Technology David Larsen, CFA (617) 918-4502 [email protected]

& Distribution Christopher Abbott (617) 918-4010 [email protected] Digital Health Steven Wardell (617) 918-4097 [email protected] Matt Dellelo, CFA (617) 918-4812 [email protected]

Sr. Editor/Supervisory Analyst Mary Ellen Eagan, CFA (617) 918-4837 [email protected]

Supervisory Analysts Randy Brougher [email protected]

Robert Egan [email protected]

Amy N. Sonne [email protected]

Boston One Federal St., 37th Fl.

New York299 Park Ave., 21st Fl.

Charlotte227 West Trade St., Ste. 2050

San Francisco255 California St., 12th Fl.

Boston, MA 02110 New York, NY 10171 Charlotte, NC 28202 San Francisco, CA 94111 (800) 808-7525 (800) 778-1653 (704) 969-8944 (415) 905-7200