metal segment analysis presentation (24 jul 2014)

TRANSCRIPT

METALS SEGMENT[24/7/2014]

© SKF Group 18 April 2023

Objectives of project

1) Provide a top-down macro-economic overview of the performance of the steel industry in each chosen focus market (Japan, India, South Korea, Taiwan, Vietnam)

2) Assess the potential of the industry by predicting future steel production output by

• Identifying significant predictor variables that quantitatively account for steel production output

• Performing multiple regressions with these variables to produce forecasts up to year 2019

Slide 2

© SKF Group 18 April 2023

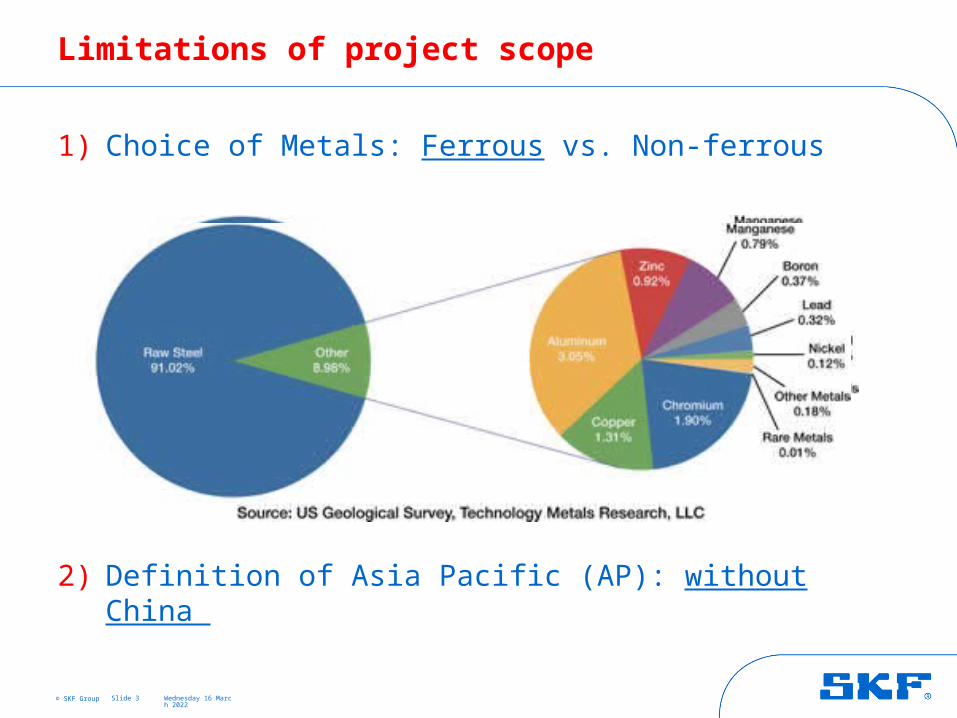

Limitations of project scope

1) Choice of Metals: Ferrous vs. Non-ferrous

2) Definition of Asia Pacific (AP): without China

Slide 3

© SKF Group

Presentation Outline

A. Introduction to the steel industry• Overview of the Global Steel market• Choice of focus markets

B. Analysis of focus markets • Combined overview of focus markets • Data analysis and forecast of steel production output

INTRODUCTION TO THE STEEL INDUSTRY

Part A.

18 April 2023Slide 5

© SKF Group

Global Steel Industry

Over-capacity and decreasing steel prices driven by China 48.5% of world production in 2013, increase from 46.7% in 2012

Continuing robust production Year 2013: 779 mil tonnes vs. Year 2014 (expected): 817 mil tonnes

Jan Feb Mar Apr May56,000

58,000

60,000

62,000

64,000

66,000

68,000

70,000

72,000

Monthly steel production in China (Source: World Steel Organization)

2014

2013

© SKF Group 18 April 2023

Global Steel Industry

Over-capacity and decreasing steel prices driven by China

Low production costs- Heavy subsidization for state-owned steel companies;- Companies’ connection network helps dodge environmental laws

Denting prices around the world - China’s carbon and alloy steel wire rods were sold in the US at “110 percent below fair market value”

Perpetuating supply surplus- High inventories throughout the supply chain - Slow-down of economic growth at sub-7.5 percent

Slide 7

© SKF Group 18 April 2023

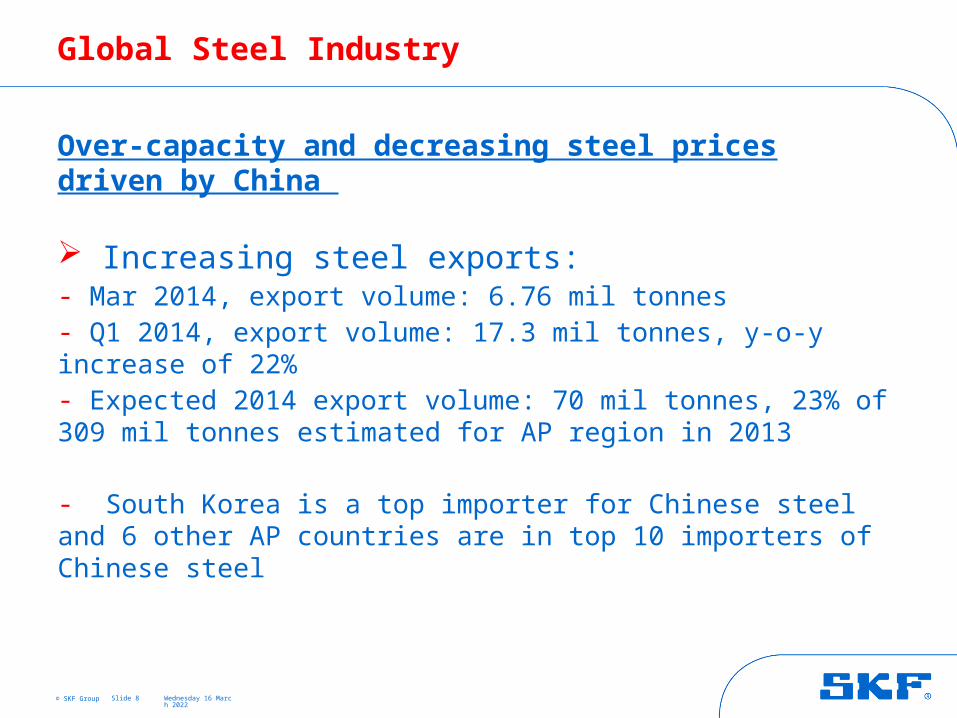

Global Steel Industry

Over-capacity and decreasing steel prices driven by China

Increasing steel exports: - Mar 2014, export volume: 6.76 mil tonnes - Q1 2014, export volume: 17.3 mil tonnes, y-o-y increase of 22%- Expected 2014 export volume: 70 mil tonnes, 23% of 309 mil tonnes estimated for AP region in 2013

- South Korea is a top importer for Chinese steel and 6 other AP countries are in top 10 importers of Chinese steel

Slide 8

© SKF Group 18 April 2023

Global Steel Industry

High bargaining power of suppliers

- Top 3 mining giants: BHP Billiton, Vale and Rio Tinto- Supply two-thirds of processed iron ore

- Increasing price volatility due to recent change from annual pricing to quarterly, index-linked pricing

- Over-supply situation: • Iron ore prices have fallen sharply this year by 31% • Morgan Stanley expects global seaborne iron ore supply to exceed demand

by 79 mil tonnes in 2014

Slide 9

© SKF Group 18 April 2023

Global Steel Industry

Consolidation and divestitures

- Backward integration: Nippon Steel and Sumitomo Metal (2012)- Horizontal integration: ArcelorMittal and ThyssenKrupp Steel (Nov 2013)- Divestitures: ArcelorMittal, world’s largest steelmaker, sold its 15% stake in iron ore mines in Canada for $1.1 billion (2013)

- M&A activity is expected to remain muted in 2014 until steel prices stabilize and there is more balance between supply and demand

Slide 10

© SKF Group 18 April 2023

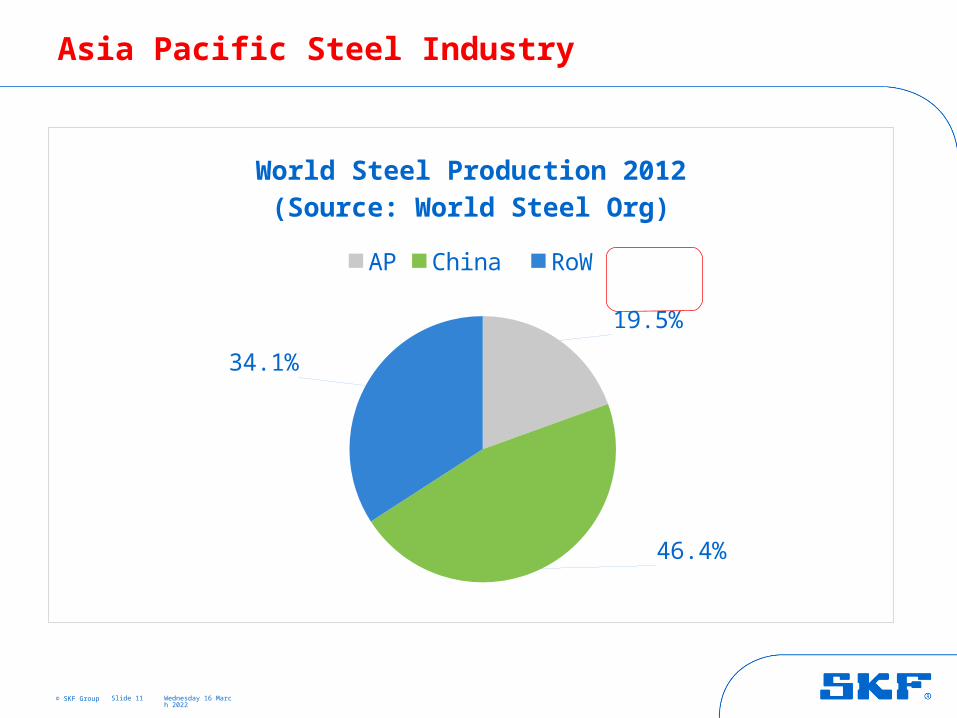

Asia Pacific Steel Industry

Slide 11

19.5%

46.4%

34.1%

World Steel Production 2012(Source: World Steel Org)

AP China RoW

© SKF Group 18 April 2023

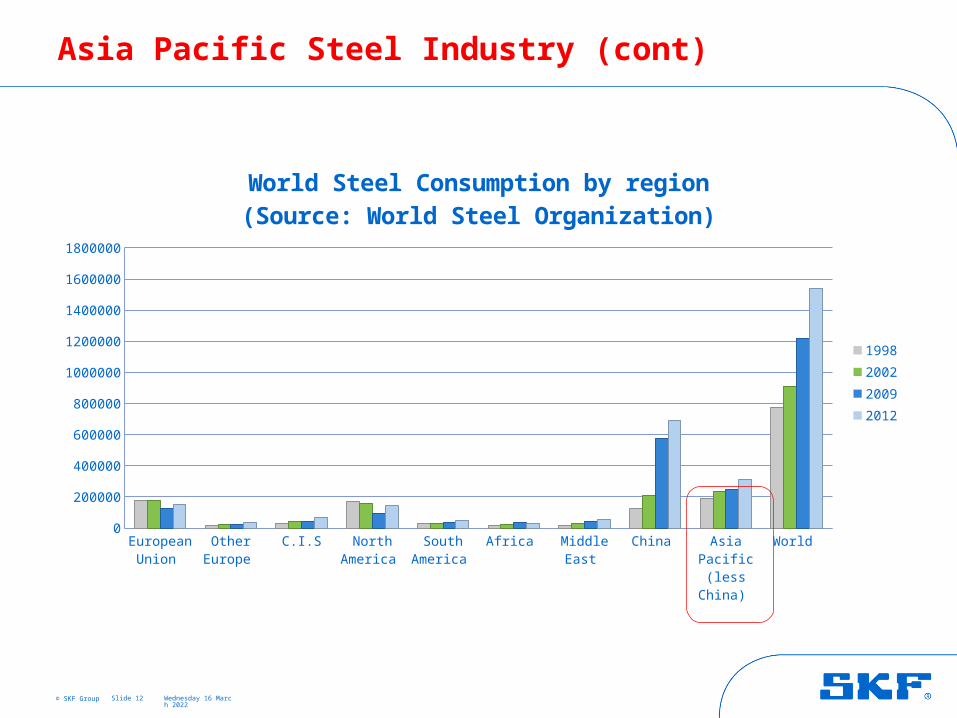

Asia Pacific Steel Industry (cont)

Slide 12

Europ

ean

Union

Other

Eur

ope

C.I.S

North

Am

erica

South

Am

erica

Africa

Midd

le Eas

t

China

Asia P

acific

(les

s Chin

a)

Wor

ld 0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

World Steel Consumption by region(Source: World Steel Organization)

1998

2002

2009

2012

© SKF Group 18 April 2023

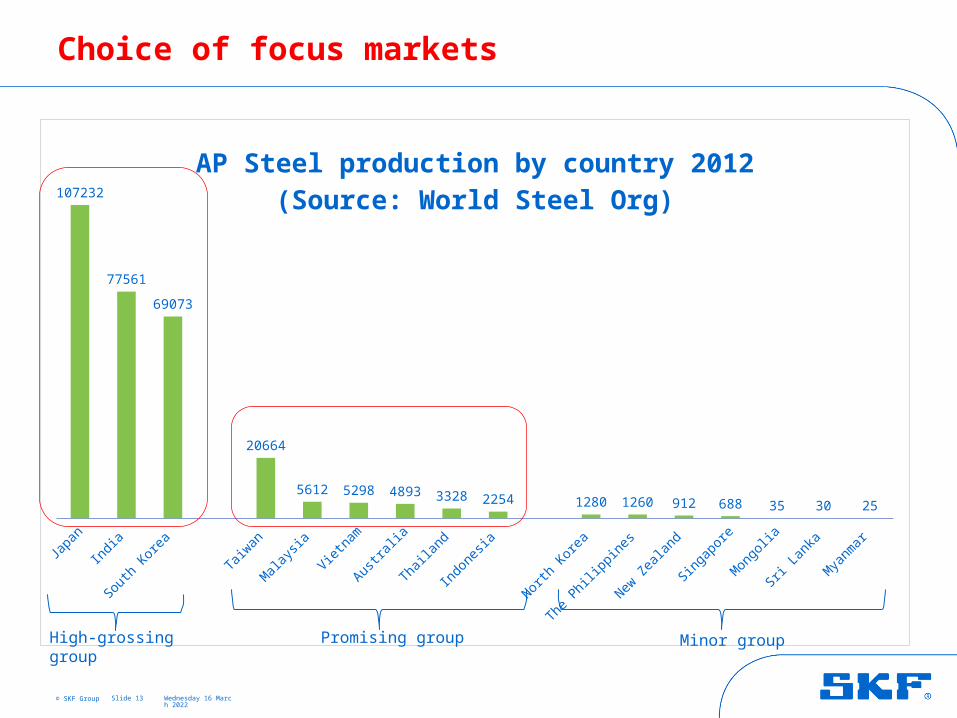

Choice of focus markets

Slide 13

Japa

nIn

dia

South

Kor

ea

Taiwan

Mala

ysia

Vietna

m

Austra

lia

Thaila

nd

Indo

nesia

North

Kor

ea

The P

hilipp

ines

New Z

ealan

d

Singap

ore

Mon

golia

Sri La

nka

Mya

nmar

107232

77561

69073

20664

5612 5298 4893 3328 2254 1280 1260 912 688 35 30 25

AP Steel production by country 2012(Source: World Steel Org)

High-grossing group Promising group Minor group

© SKF Group 18 April 2023

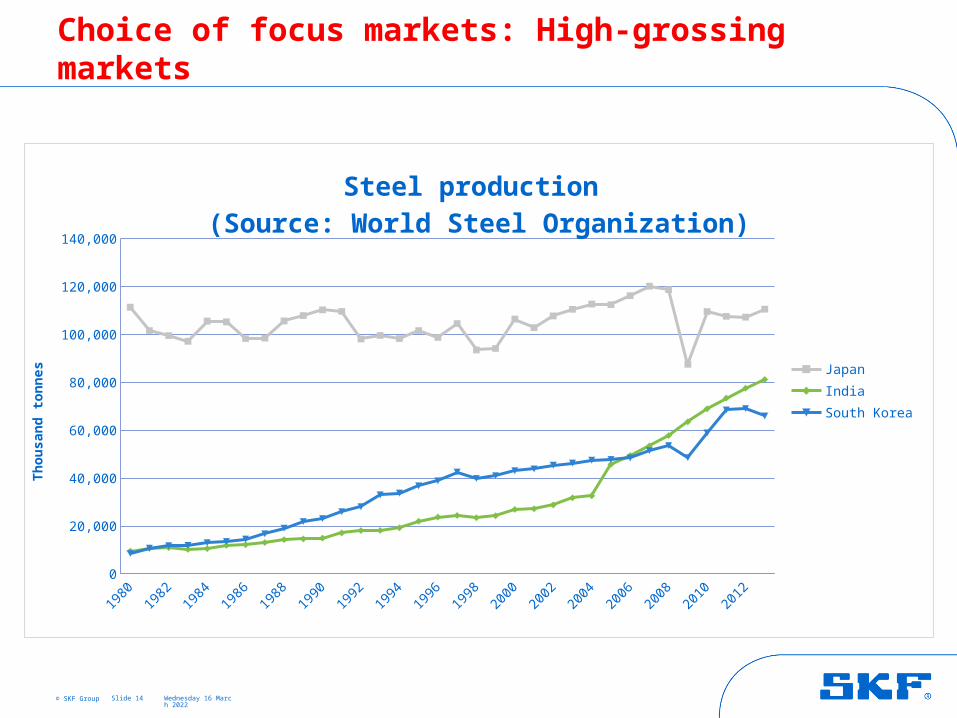

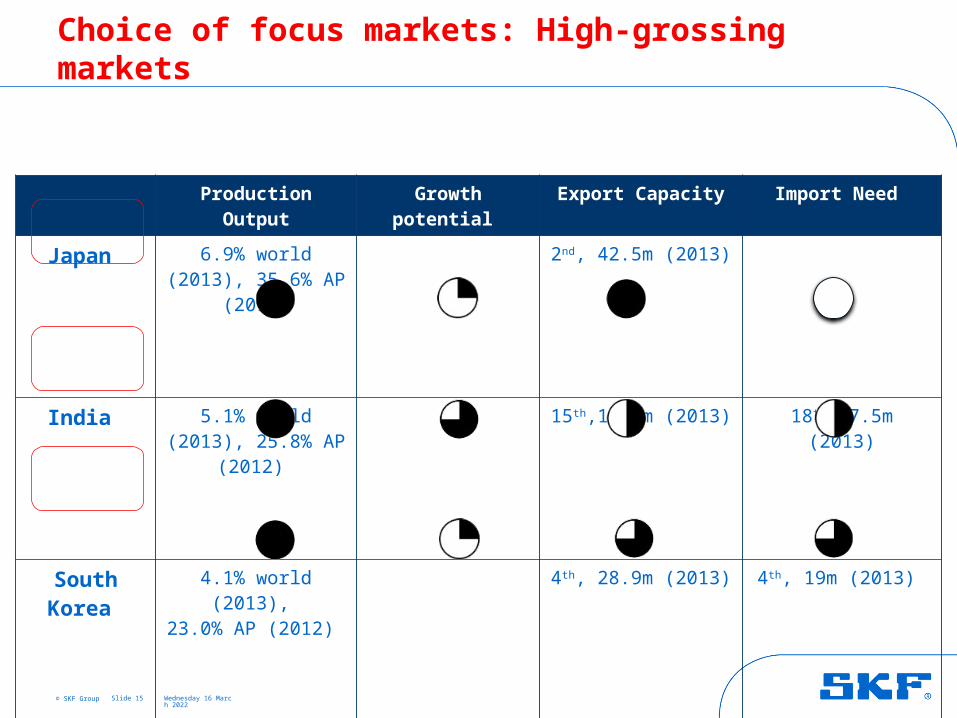

Choice of focus markets: High-grossing markets

Slide 14

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Steel production (Source: World Steel Organization)

Japan

India

South Korea

Th

ou

san

d t

on

nes

© SKF Group 18 April 2023

Choice of focus markets: High-grossing markets

Slide 15

Production Output Growth potential Export Capacity Import Need

Japan 6.9% world (2013), 35.6% AP (2012)

2nd, 42.5m (2013)

India 5.1% world (2013), 25.8% AP (2012)

15th,10.1m (2013) 18th, 7.5m (2013)

South Korea

4.1% world (2013), 23.0% AP (2012)

4th, 28.9m (2013) 4th, 19m (2013)

© SKF Group 18 April 2023

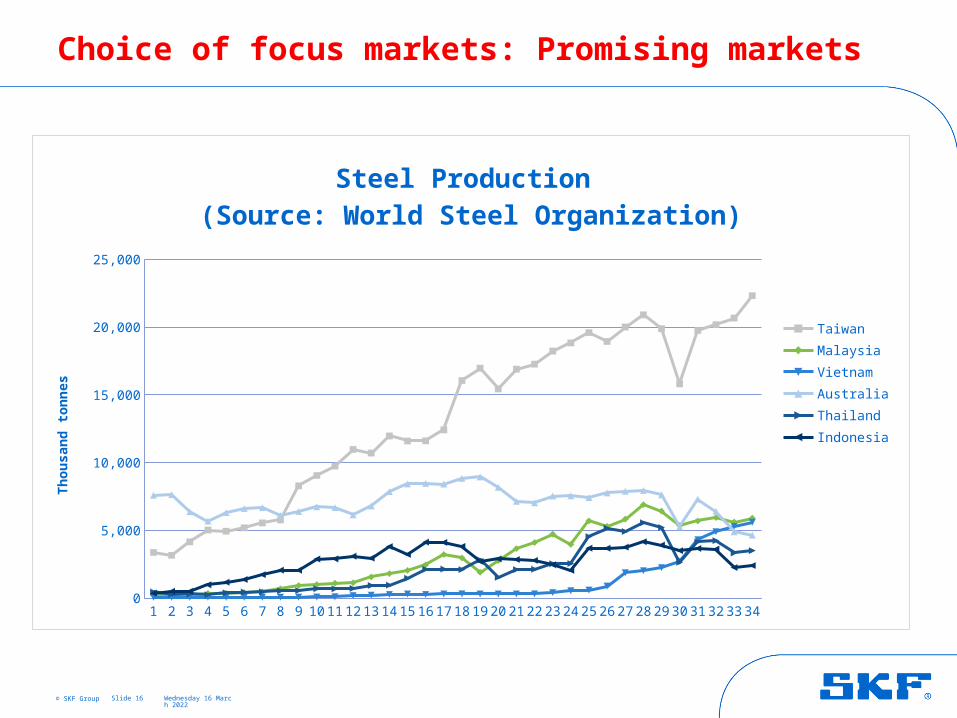

Choice of focus markets: Promising markets

Slide 16

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 340

5,000

10,000

15,000

20,000

25,000

Steel Production (Source: World Steel Organization)

Taiwan

Malaysia

Vietnam

Australia

Thailand

Indonesia

Th

ou

san

d t

on

nes

© SKF Group

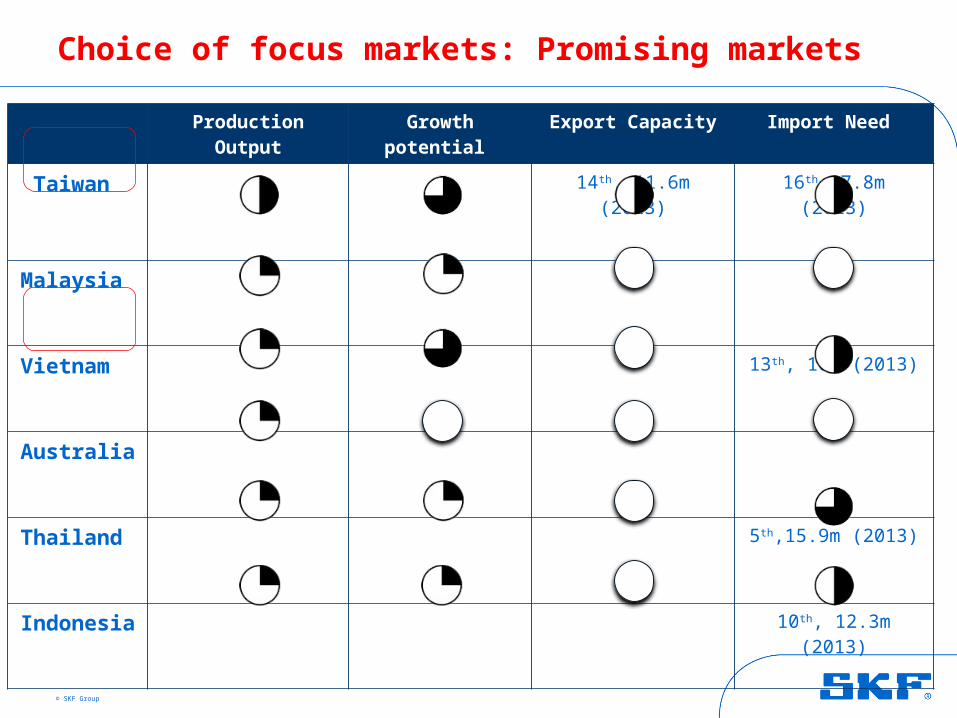

Choice of focus markets: Promising markets

Production Output Growth potential Export Capacity Import Need

Taiwan 14th, 11.6m (2013) 16th, 7.8m (2013)

Malaysia

Vietnam 13th, 10m (2013)

Australia

Thailand 5th,15.9m (2013)

Indonesia 10th, 12.3m (2013)

© SKF Group

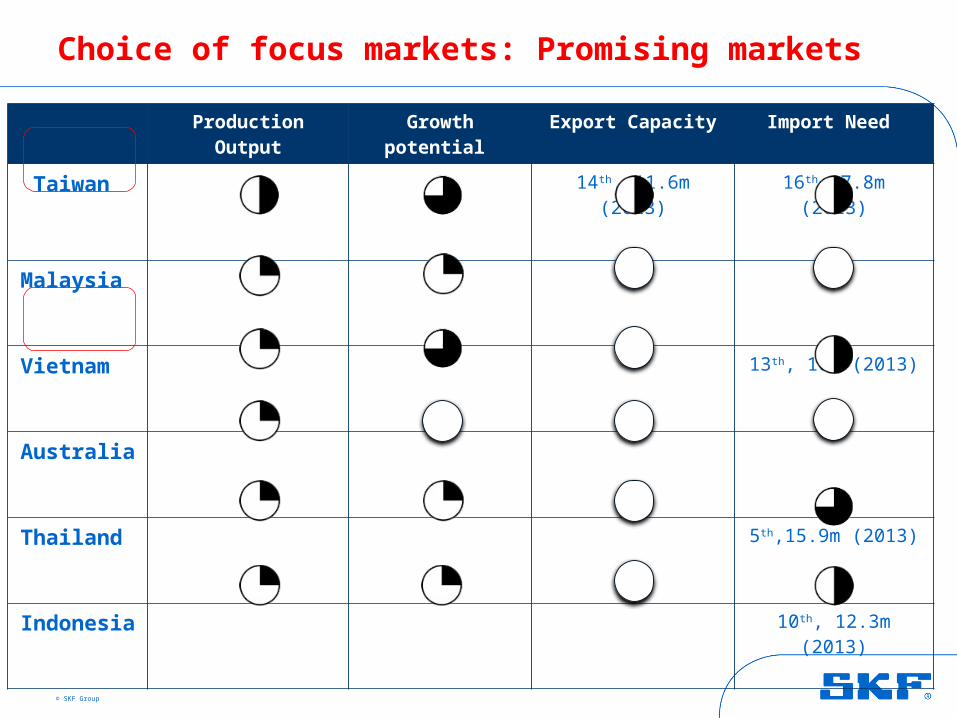

Choice of focus markets: Promising markets

Production Output Growth potential Export Capacity Import Need

Taiwan 14th, 11.6m (2013) 16th, 7.8m (2013)

Malaysia

Vietnam 13th, 10m (2013)

Australia

Thailand 5th,15.9m (2013)

Indonesia 10th, 12.3m (2013)

© SKF Group 18 April 2023

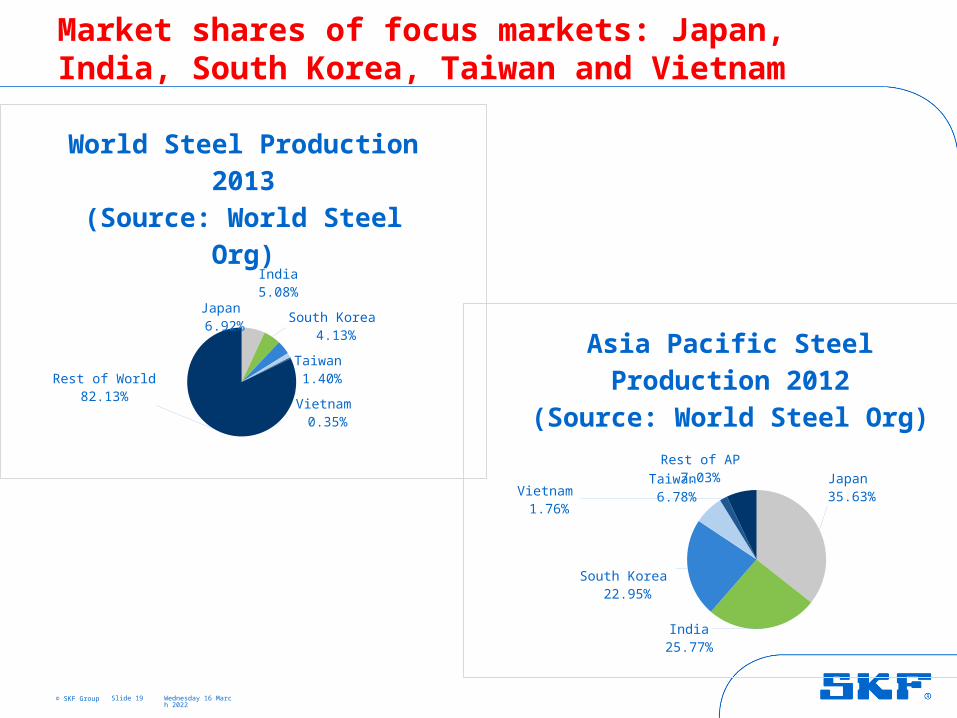

Market shares of focus markets: Japan, India, South Korea, Taiwan and Vietnam

Slide 19

Japan 6.92%

India5.08%

South Korea 4.13%Taiwan 1.40%

Vietnam 0.35%

Rest of World82.13%

World Steel Production 2013(Source: World Steel Org)

Japan 35.63%

India25.77%

South Korea 22.95%

Taiwan 6.78%Vietnam

1.76%

Rest of AP7.03%

Asia Pacific Steel Production 2012

(Source: World Steel Org)

ANALYSIS OF FOCUS MARKETS

Part B.

18 April 2023Slide 20

Overview of focus markets

18 April 2023Slide 21

© SKF Group 18 April 2023

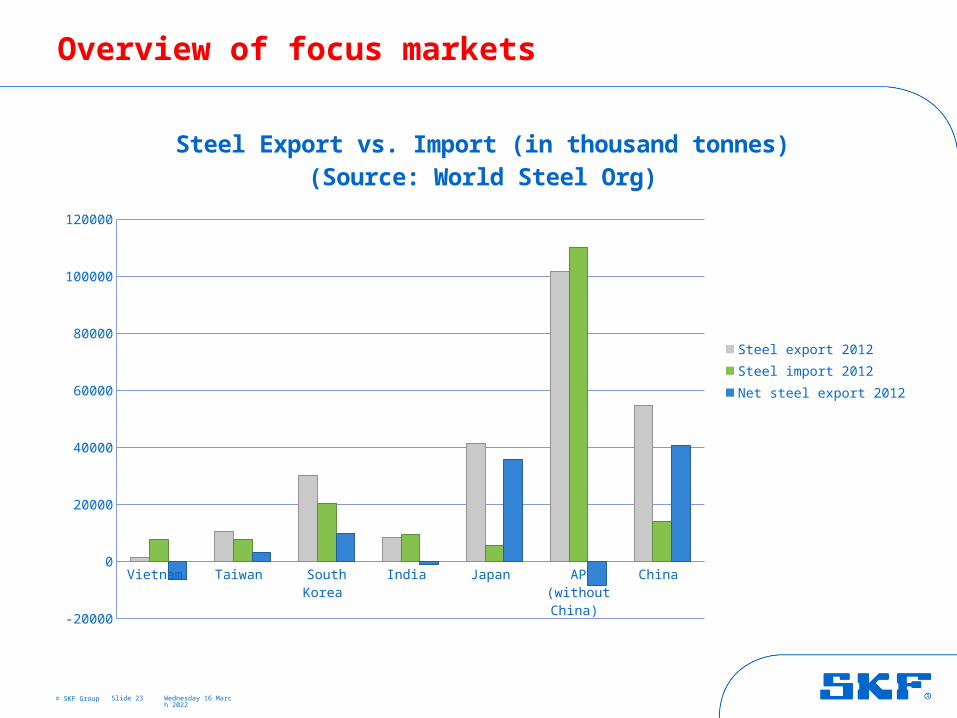

Overview of focus markets

Slide 22

Vietnam

Taiwan

South Korea

India

Japan

AP (without China)

China

World

12,740

21,515

56,322

77,039

68,800

312,611

687,580

1,537,274

5,298

20,664

69,073

77,561

107,232

300,995

716,542

1,545,011

Steel Production vs. Consumption 2012 (in thousand tonnes)(Source: World Steel Org)

Crude Steel Production Crude Steel Consumption

© SKF Group 18 April 2023

Overview of focus markets

Slide 23

Vietnam Taiwan South Korea India Japan AP (without China)

China

-20000

0

20000

40000

60000

80000

100000

120000

Steel Export vs. Import (in thousand tonnes)(Source: World Steel Org)

Steel export 2012

Steel import 2012

Net steel export 2012

Introduction to Multiple Regression Forecasting method

18 April 2023Slide 24

© SKF Group 18 April 2023

Data Analysis – Overview of Regression forecasting method

What is multiple regression?

-Regression or Multiple Regression attempts to express a parameter (dependent variable) in terms of one or more related parameters (predictor variables)

- Regression is performed by hardwired algorithms in Excel

- Predictor variables are macro indicators that have the most significant impact on steel production in each focus market

Slide 25

© SKF Group 18 April 2023

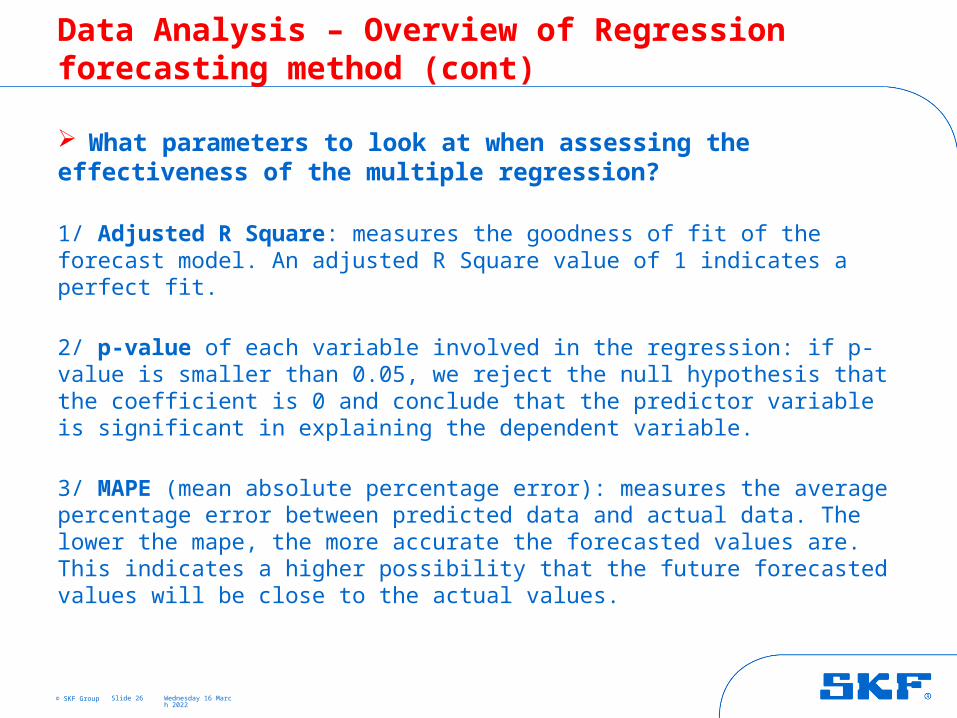

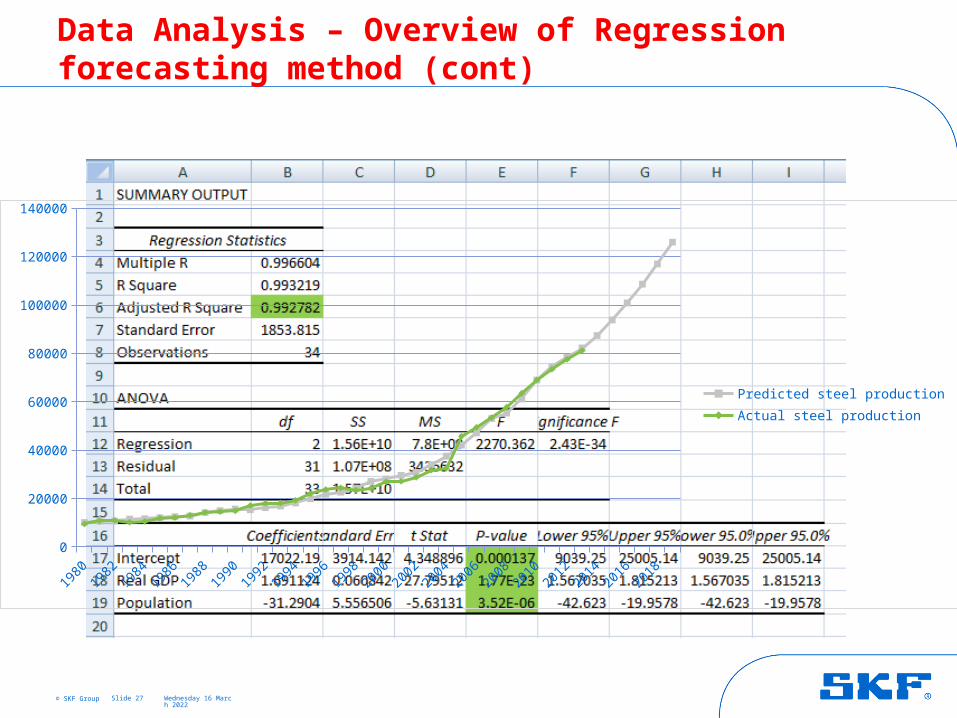

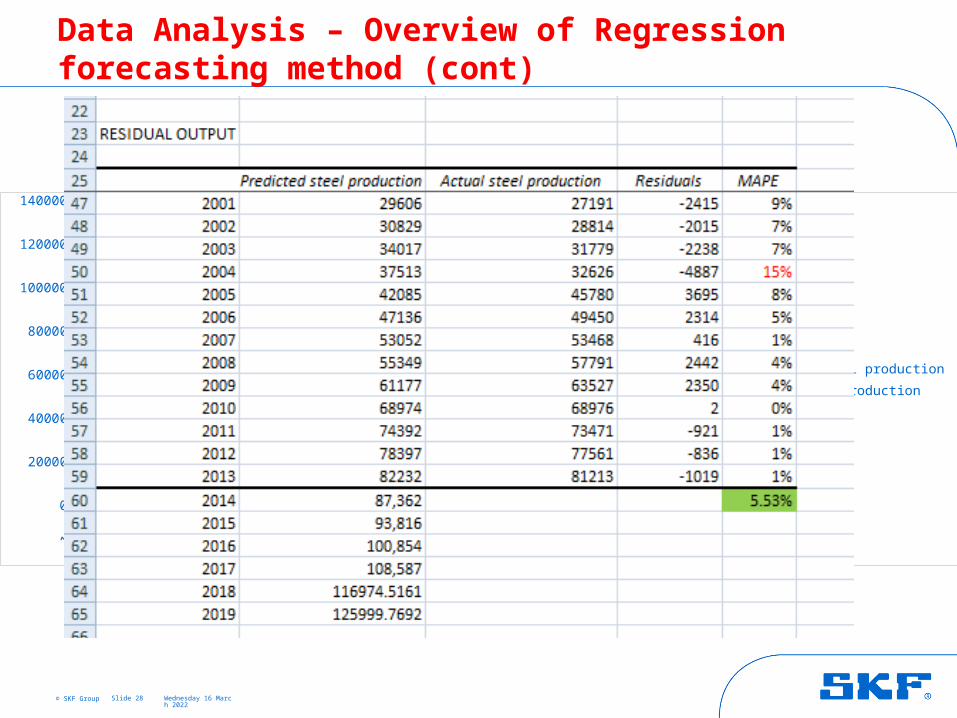

Data Analysis – Overview of Regression forecasting method (cont)

What parameters to look at when assessing the effectiveness of the multiple regression?

1/ Adjusted R Square: measures the goodness of fit of the forecast model. An adjusted R Square value of 1 indicates a perfect fit.

2/ p-value of each variable involved in the regression: if p-value is smaller than 0.05, we reject the null hypothesis that the coefficient is 0 and conclude that the predictor variable is significant in explaining the dependent variable.

3/ MAPE (mean absolute percentage error): measures the average percentage error between predicted data and actual data. The lower the mape, the more accurate the forecasted values are. This indicates a higher possibility that the future forecasted values will be close to the actual values.

Slide 26

© SKF Group 18 April 2023

Data Analysis – Overview of Regression forecasting method (cont)

Slide 27

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

0

20000

40000

60000

80000

100000

120000

140000

Predicted steel production

Actual steel production

© SKF Group 18 April 2023

Data Analysis – Overview of Regression forecasting method (cont)

Slide 28

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

0

20000

40000

60000

80000

100000

120000

140000

Predicted steel production

Actual steel production

© SKF Group 18 April 2023

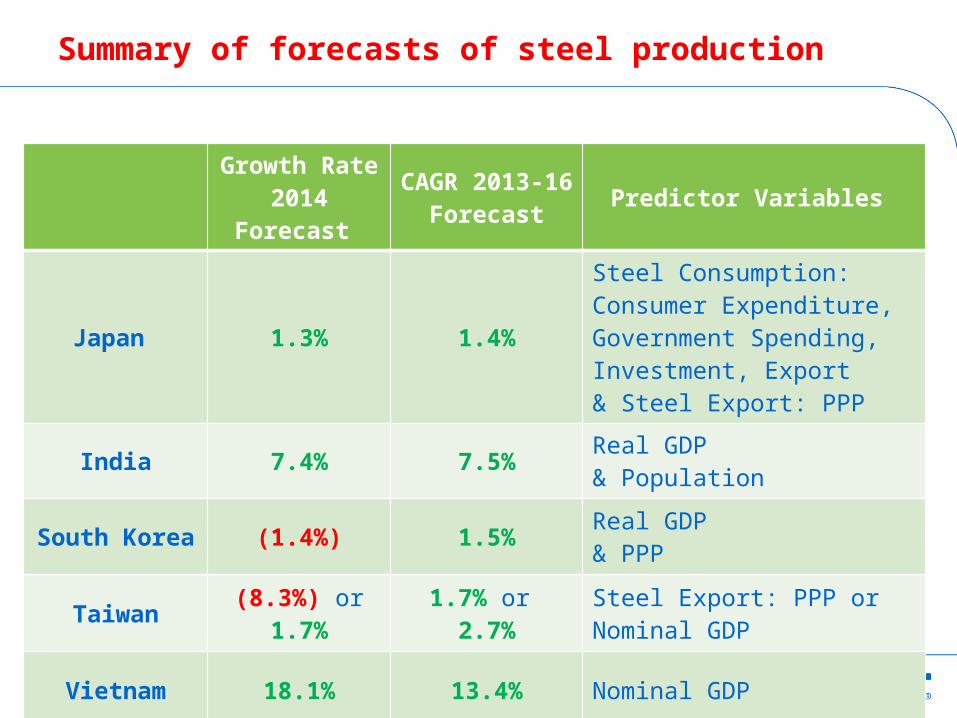

Summary of forecasts of steel production

Slide 29

Growth Rate 2014 Forecast

CAGR 2013-16 Forecast

Predictor Variables

Japan 1.3% 1.4%

Steel Consumption: Consumer Expenditure, Government Spending, Investment, Export& Steel Export: PPP

India 7.4% 7.5%Real GDP & Population

South Korea (1.4%) 1.5%Real GDP & PPP

Taiwan(8.3%) or

1.7%1.7% or

2.7%Steel Export: PPP or Nominal GDP

Vietnam 18.1% 13.4% Nominal GDP

Analysis of Japan

18 April 2023Slide 30

© SKF Group 18 April 2023

Data Analysis – Predictor Variables

Slide 31

Steel Production

Steel ExportSteel

Consumption

1/ Export (bil current USD)2/ Household Consumption (bil current LCU) 3/ Government Expenditure (bil current LCU)4/ Investment (bil current LCU)

1/ Purchasing Power Parity (LCU per international $)

Steel Import

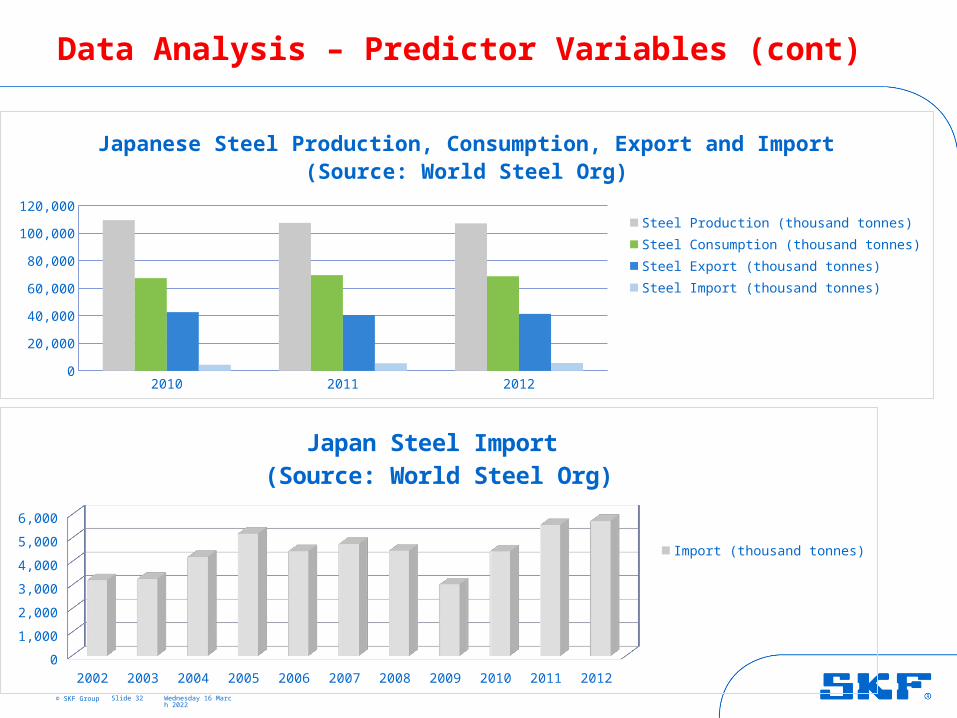

. Import volume is equal to only 5.3% of production in 2012. Import remains relatively stable throughout the years

© SKF Group 18 April 2023

Data Analysis – Predictor Variables (cont)

Slide 32

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 20120

1,000

2,000

3,000

4,000

5,000

6,000

Japan Steel Import (Source: World Steel Org)

Import (thousand tonnes)

2010 2011 20120

20,000

40,000

60,000

80,000

100,000

120,000

Japanese Steel Production, Consumption, Export and Import(Source: World Steel Org)

Steel Production (thousand tonnes)

Steel Consumption (thousand tonnes)

Steel Export (thousand tonnes)

Steel Import (thousand tonnes)

© SKF Group 18 April 2023

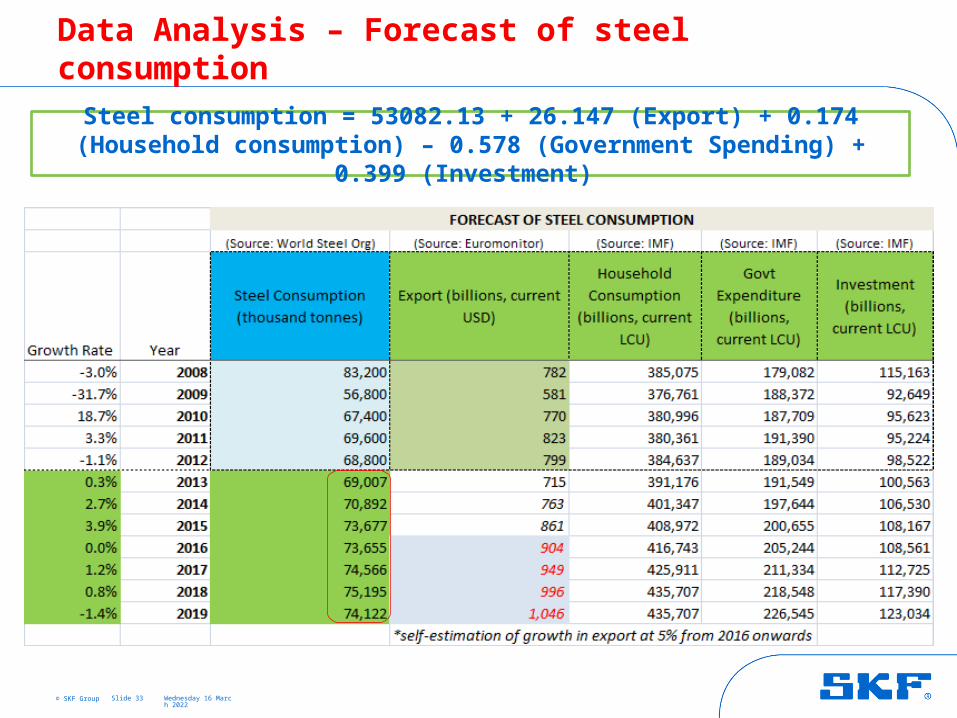

Data Analysis – Forecast of steel consumption

Slide 33

Steel consumption = 53082.13 + 26.147 (Export) + 0.174 (Household consumption) – 0.578 (Government Spending) + 0.399 (Investment)

© SKF Group 18 April 2023

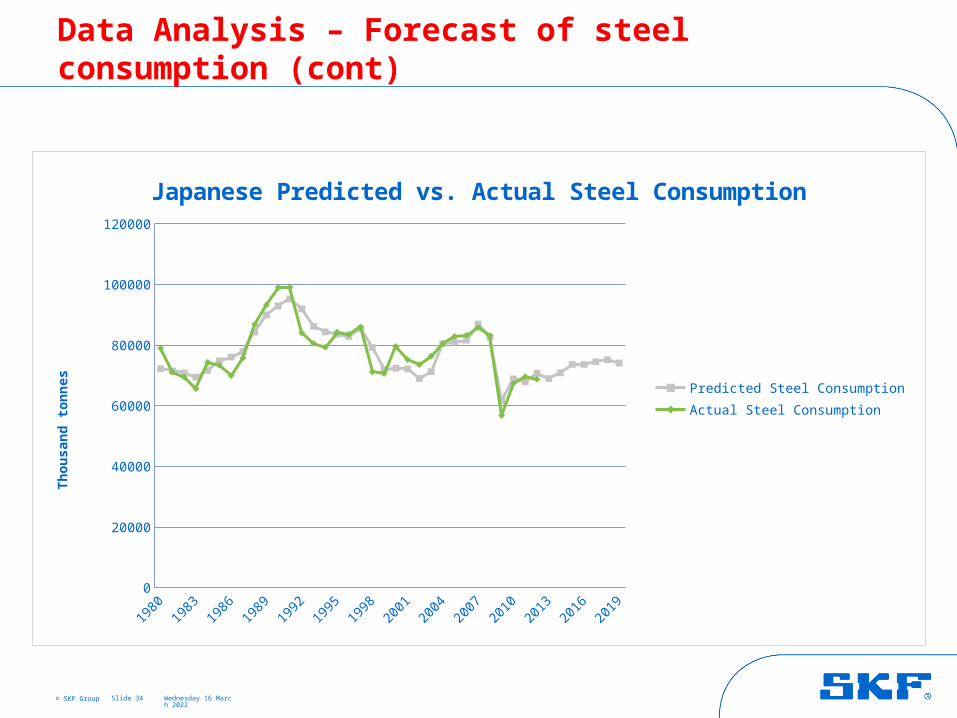

Data Analysis – Forecast of steel consumption (cont)

Slide 34

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

0

20000

40000

60000

80000

100000

120000

Japanese Predicted vs. Actual Steel Consumption

Predicted Steel Consumption

Actual Steel Consumption

Th

ou

san

d t

on

nes

© SKF Group 18 April 2023

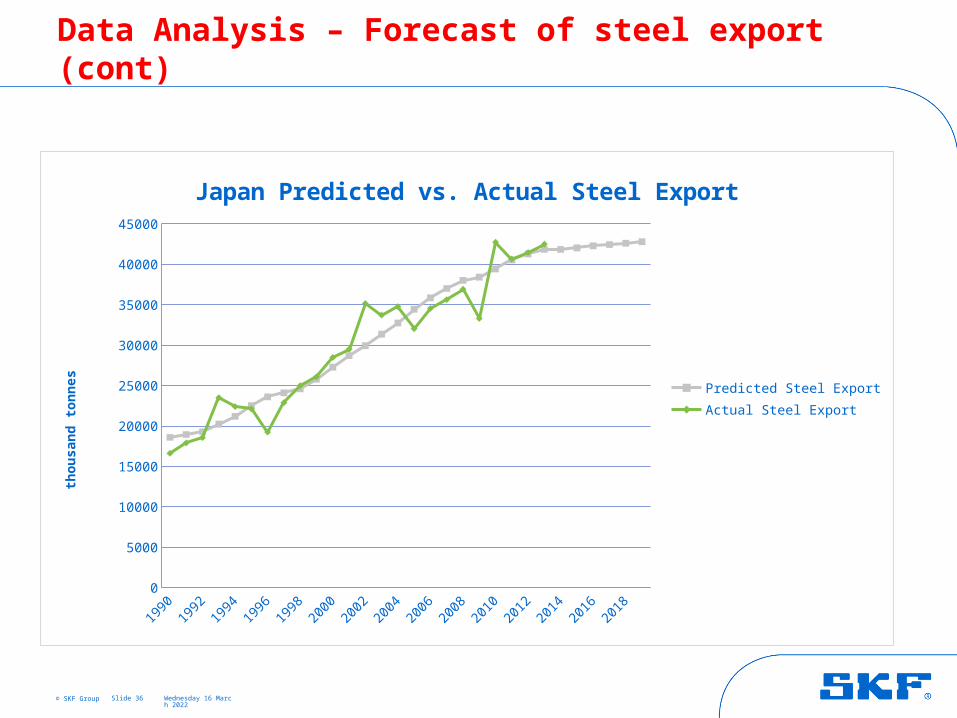

Data Analysis – Forecast of steel export

Slide 35

Steel export = 69042 – 267 (PPP)

© SKF Group 18 April 2023

Data Analysis – Forecast of steel export (cont)

Slide 36

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

Japan Predicted vs. Actual Steel Export

Predicted Steel Export

Actual Steel Export

tho

usa

nd

to

nn

es

© SKF Group 18 April 2023

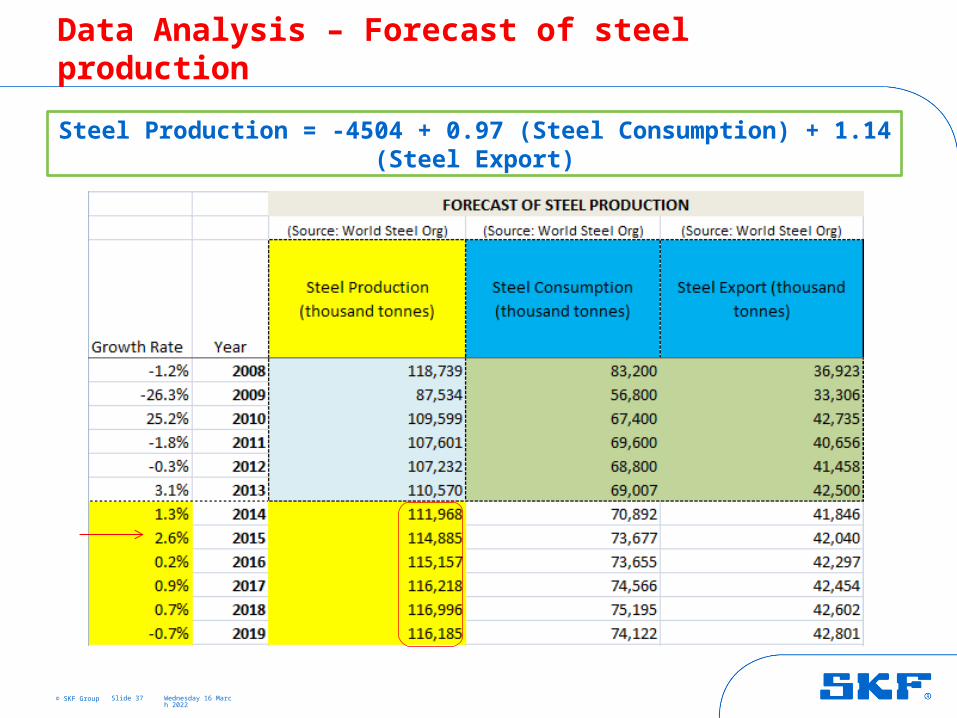

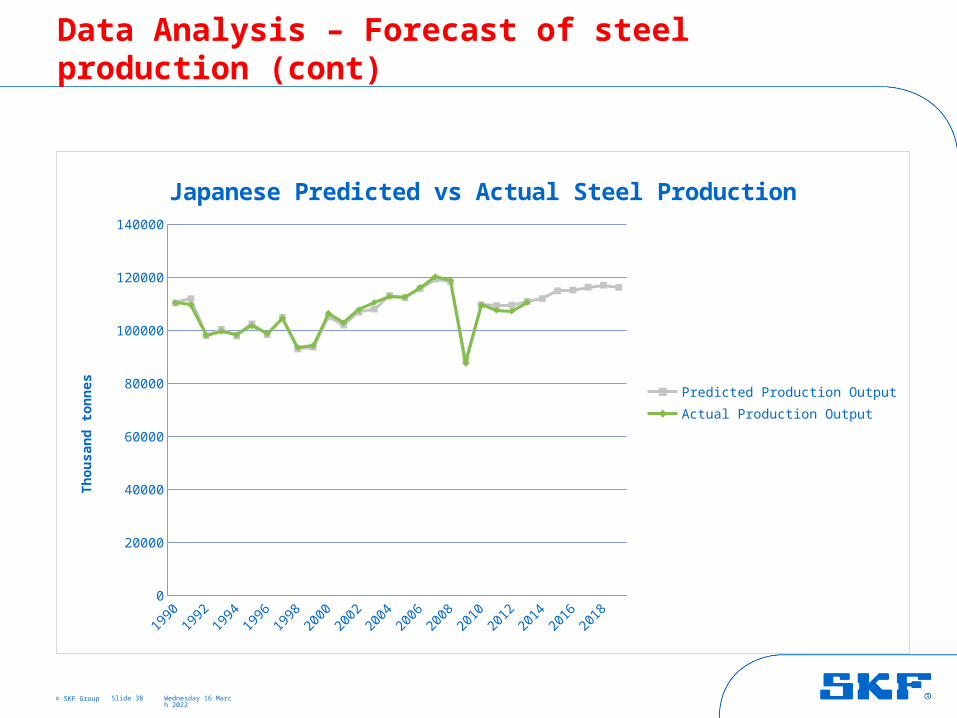

Data Analysis – Forecast of steel production

Slide 37

Steel Production = -4504 + 0.97 (Steel Consumption) + 1.14 (Steel Export)

© SKF Group 18 April 2023

Data Analysis – Forecast of steel production (cont)

Slide 38

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

0

20000

40000

60000

80000

100000

120000

140000

Japanese Predicted vs Actual Steel Production

Predicted Production Output

Actual Production Output

Th

ou

san

d t

on

nes

© SKF Group 18 April 2023

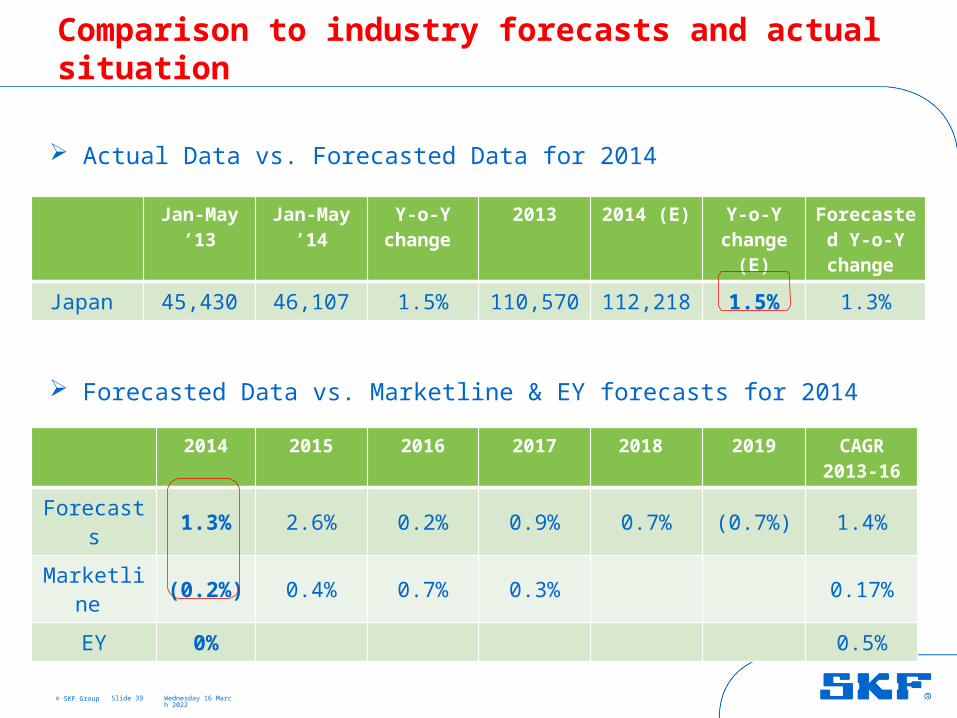

Comparison to industry forecasts and actual situation

Slide 39

Jan-May ‘13

Jan-May ’14

Y-o-Y change

2013 2014 (E) Y-o-Y change

(E)

Forecasted Y-o-Y

change

Japan 45,430 46,107 1.5% 110,570 112,218 1.5% 1.3%

2014 2015 2016 2017 2018 2019 CAGR2013-16

Forecasts 1.3% 2.6% 0.2% 0.9% 0.7% (0.7%) 1.4%

Marketline (0.2%) 0.4% 0.7% 0.3% 0.17%

EY 0% 0.5%

Actual Data vs. Forecasted Data for 2014

Forecasted Data vs. Marketline & EY forecasts for 2014

Analysis of India

18 April 2023Slide 40

© SKF Group 18 April 2023

Data Analysis – Predictor Variables

Slide 41

Steel Production 1/ Real GDP (bil constant LCU)2/ Population (mil)

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Indian Steel Production vs. Steel Export (in thousand tonnes)(Source: World Steel Org)

Steel Production

Steel Export

© SKF Group 18 April 2023

Data Analysis – Forecast of steel production

Slide 42

Steel production = 17022 + 1.7 (Real GDP) - 31.3 (Population)

GDP growth rate

10.3%

6.6%

4.7%

4.4%

5.4%

6.4%

6.5%

6.6%

6.7%

6.8%

© SKF Group 18 April 2023

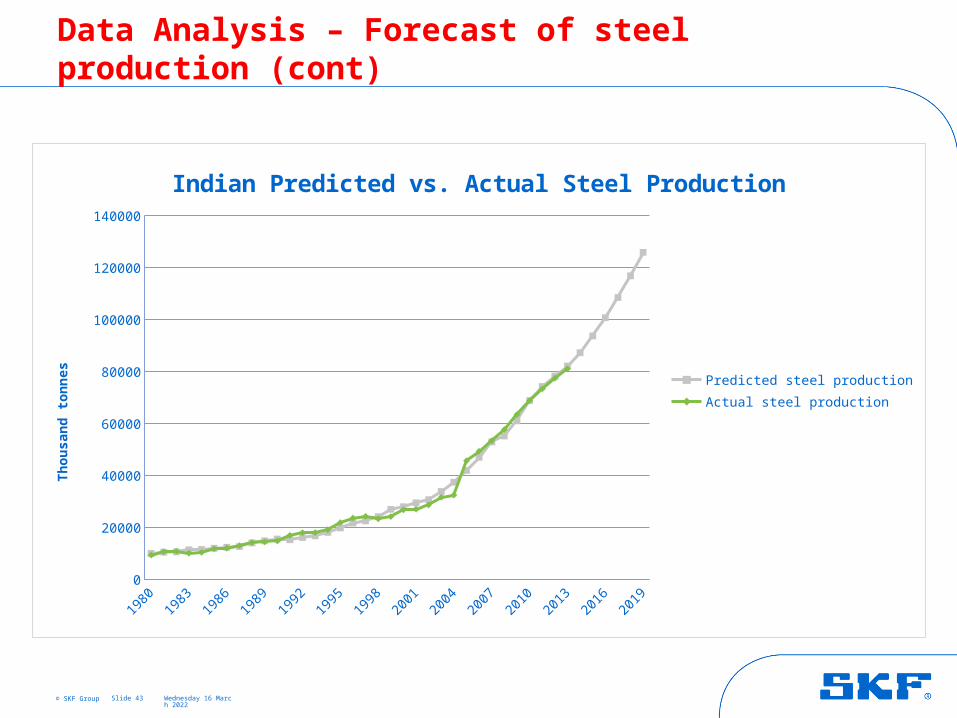

Data Analysis – Forecast of steel production (cont)

Slide 43

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

0

20000

40000

60000

80000

100000

120000

140000

Indian Predicted vs. Actual Steel Production

Predicted steel production

Actual steel production

Th

ou

san

d t

on

nes

© SKF Group 18 April 2023

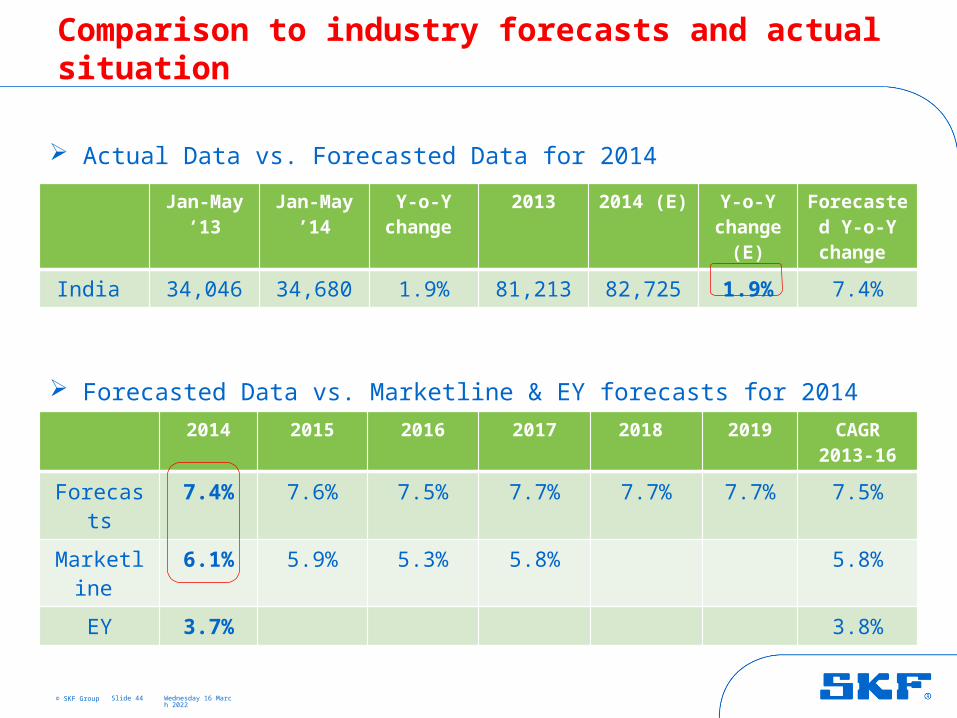

Comparison to industry forecasts and actual situation

Slide 44

Jan-May ‘13

Jan-May ’14

Y-o-Y change

2013 2014 (E) Y-o-Y change

(E)

Forecasted Y-o-Y

change

India 34,046 34,680 1.9% 81,213 82,725 1.9% 7.4%

2014 2015 2016 2017 2018 2019 CAGR2013-16

Forecasts 7.4% 7.6% 7.5% 7.7% 7.7% 7.7% 7.5%

Marketline 6.1% 5.9% 5.3% 5.8% 5.8%

EY 3.7% 3.8%

Actual Data vs. Forecasted Data for 2014

Forecasted Data vs. Marketline & EY forecasts for 2014

Analysis of South Korea

18 April 2023Slide 45

© SKF Group 18 April 2023

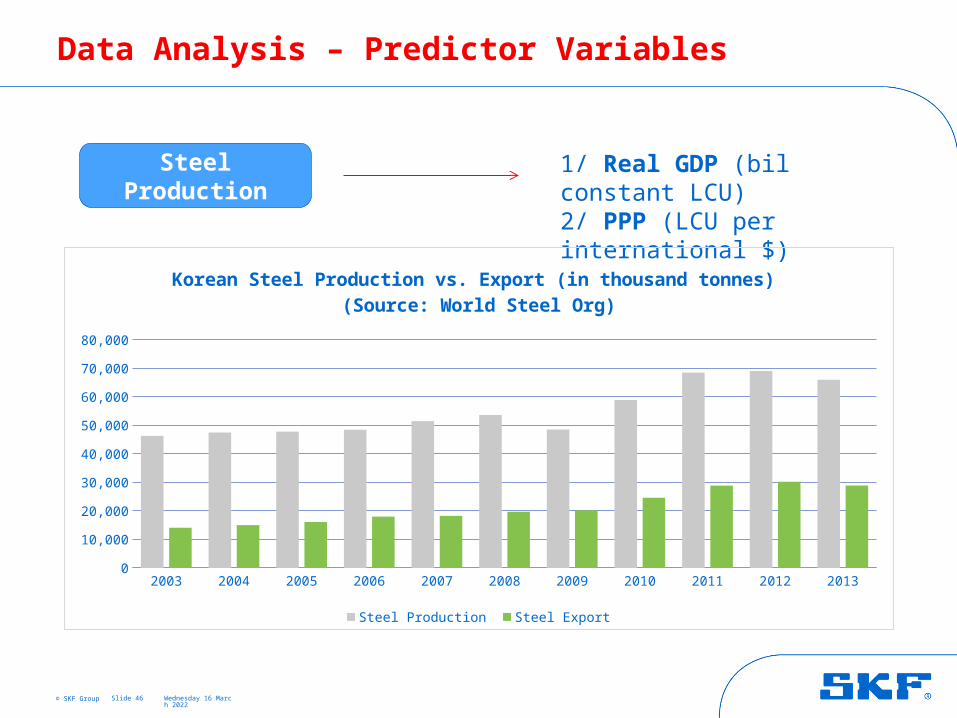

Data Analysis – Predictor Variables

Slide 46

Steel Production 1/ Real GDP (bil constant LCU)2/ PPP (LCU per international $)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Korean Steel Production vs. Export (in thousand tonnes) (Source: World Steel Org)

Steel Production Steel Export

© SKF Group 18 April 2023

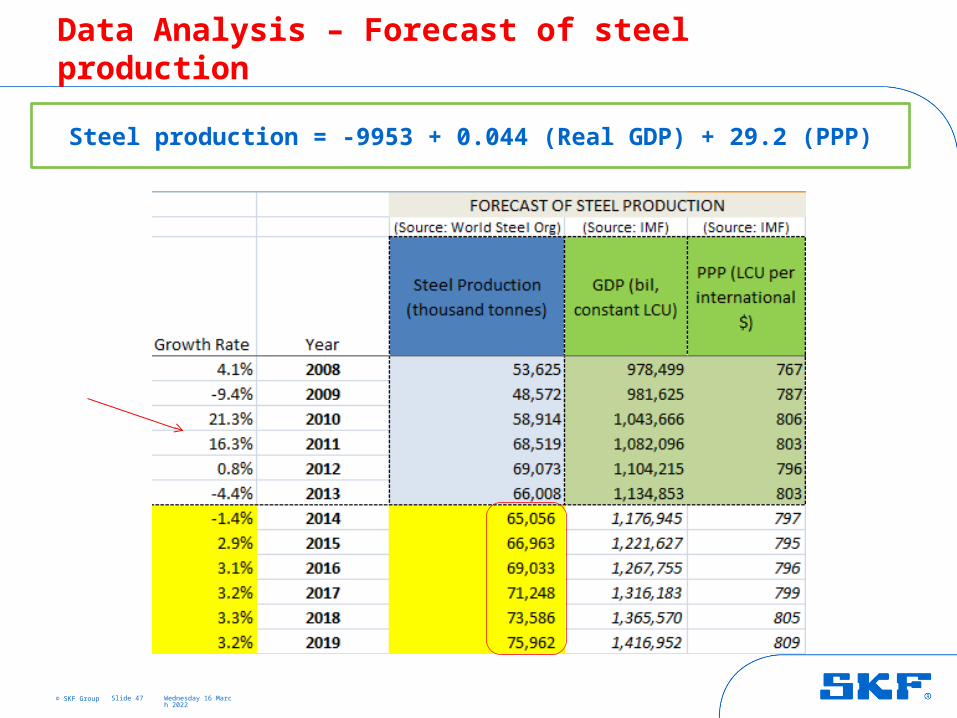

Data Analysis – Forecast of steel production

Slide 47

Steel production = -9953 + 0.044 (Real GDP) + 29.2 (PPP)

© SKF Group 18 April 2023

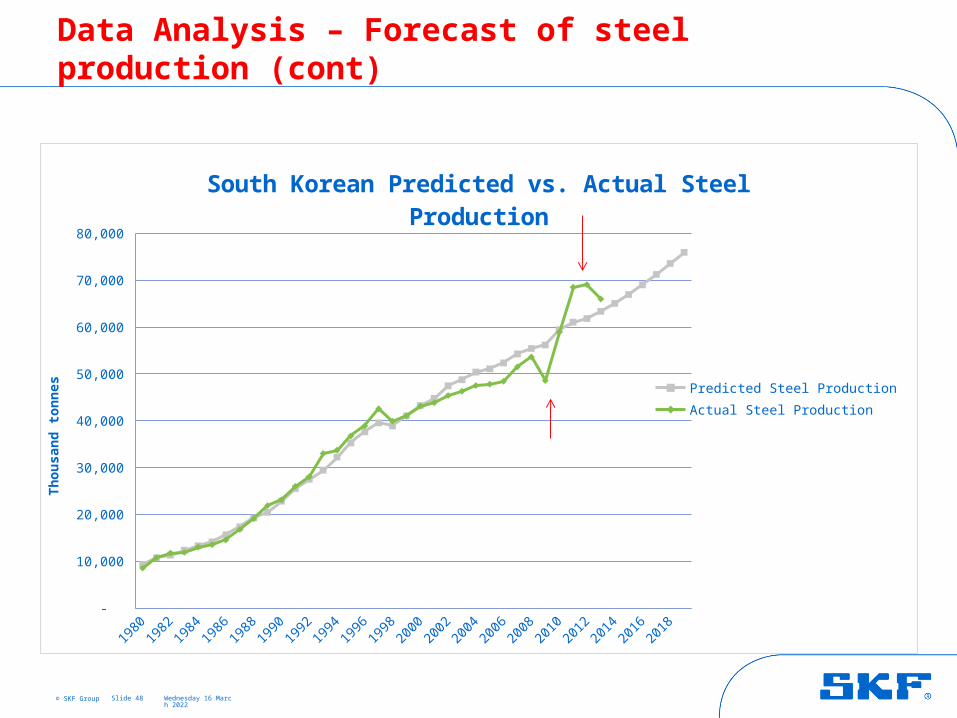

Data Analysis – Forecast of steel production (cont)

Slide 48

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

South Korean Predicted vs. Actual Steel Production

Predicted Steel Production

Actual Steel Production

Th

ou

san

d t

on

nes

© SKF Group

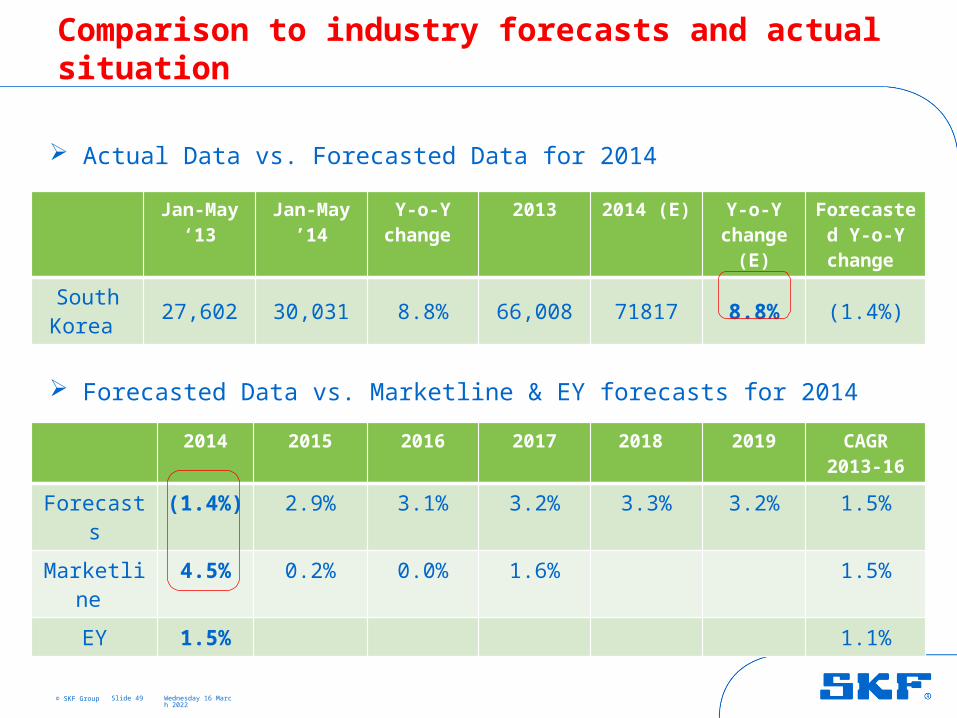

Comparison to industry forecasts and actual situation

18 April 2023Slide 49

Jan-May ‘13

Jan-May ’14

Y-o-Y change

2013 2014 (E) Y-o-Y change

(E)

Forecasted Y-o-Y

change

South Korea 27,602 30,031 8.8% 66,008 71817 8.8% (1.4%)

2014 2015 2016 2017 2018 2019 CAGR2013-16

Forecasts (1.4%) 2.9% 3.1% 3.2% 3.3% 3.2% 1.5%

Marketline 4.5% 0.2% 0.0% 1.6% 1.5%

EY 1.5% 1.1%

Actual Data vs. Forecasted Data for 2014

Forecasted Data vs. Marketline & EY forecasts for 2014

Analysis of Taiwan

18 April 2023Slide 50

© SKF Group 18 April 2023

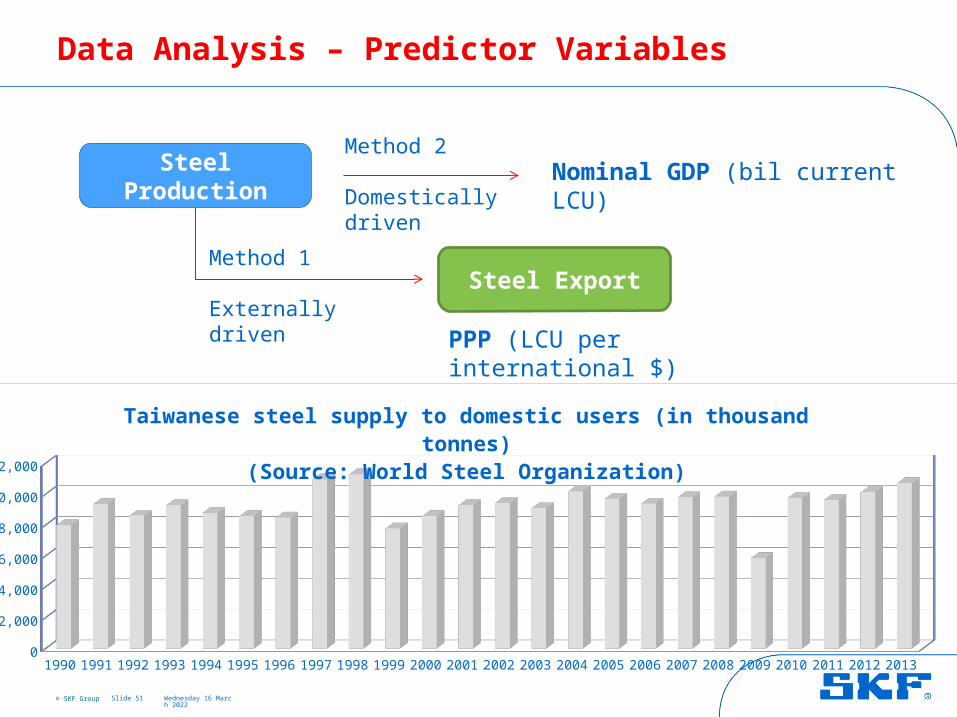

Data Analysis – Predictor Variables

Slide 51

Steel Production Nominal GDP (bil current LCU)

Steel Export

PPP (LCU per international $)

Method 2

Domestically driven

Method 1

Externally driven

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

2,000

4,000

6,000

8,000

10,000

12,000

Taiwanese steel supply to domestic users (in thousand tonnes)(Source: World Steel Organization)

© SKF Group 18 April 2023

Data Analysis – Predictor Variables (cont)

Slide 52

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

0

5,000

10,000

15,000

20,000

25,000

30,000

Taiwanese Steel Production, Export, Consumption and Import(Source: World Steel Org)

Steel Production (thousand tonnes)

Steel Export (thousand tonnes)

Steel Consumption (thousand tonnes)

Steel Import (thousand tonnes)

Th

ou

san

d t

on

nes

© SKF Group 18 April 2023

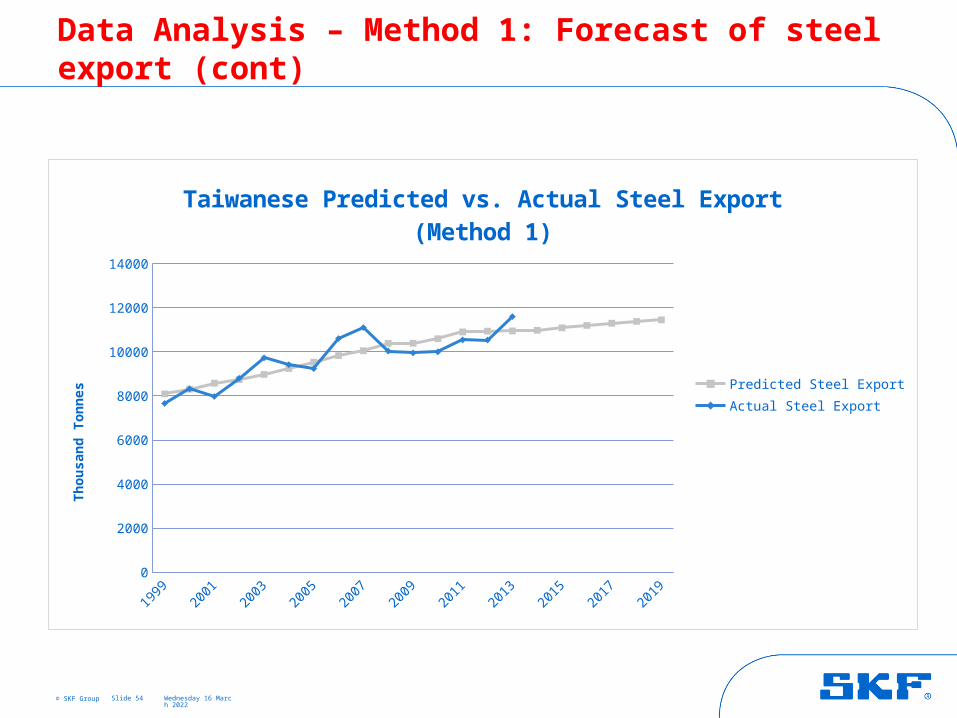

Data Analysis – Method 1: Forecast of steel export

Slide 53

Steel export = 16997 – 386 (PPP)

© SKF Group 18 April 2023

Data Analysis – Method 1: Forecast of steel export (cont)

Slide 54

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

0

2000

4000

6000

8000

10000

12000

14000

Taiwanese Predicted vs. Actual Steel Export (Method 1)

Predicted Steel Export

Actual Steel Export

Th

ou

san

d T

on

nes

© SKF Group 18 April 2023

Data Analysis – Method 1: Forecast of steel production

Slide 55

Steel production = 8983 + 1.0 (Steel Export)

© SKF Group 18 April 2023

Data Analysis – Method 1: Forecast of steel production (cont)

Slide 56

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

0

5000

10000

15000

20000

25000

Taiwanese Predicted vs. Actual Steel Production (Method 1)

Predicted steel production

Actual Steel Production

Th

ou

san

d t

on

nes

© SKF Group 18 April 2023

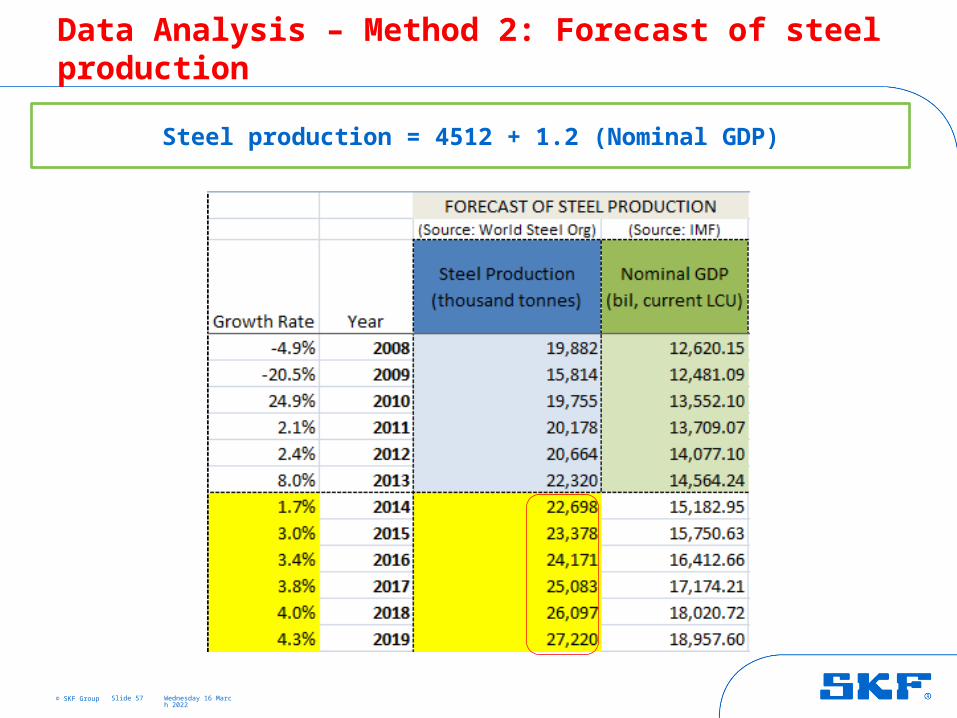

Data Analysis – Method 2: Forecast of steel production

Slide 57

Steel production = 4512 + 1.2 (Nominal GDP)

© SKF Group 18 April 2023

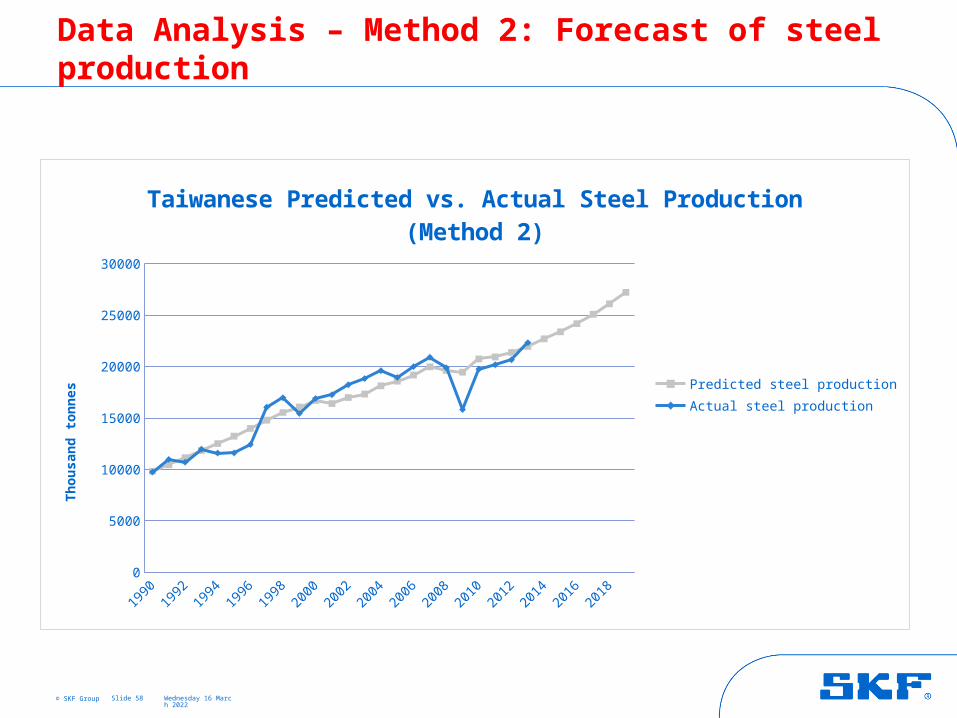

Data Analysis – Method 2: Forecast of steel production

Slide 58

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

0

5000

10000

15000

20000

25000

30000

Taiwanese Predicted vs. Actual Steel Production (Method 2)

Predicted steel production

Actual steel production

Th

ou

san

d t

on

nes

© SKF Group

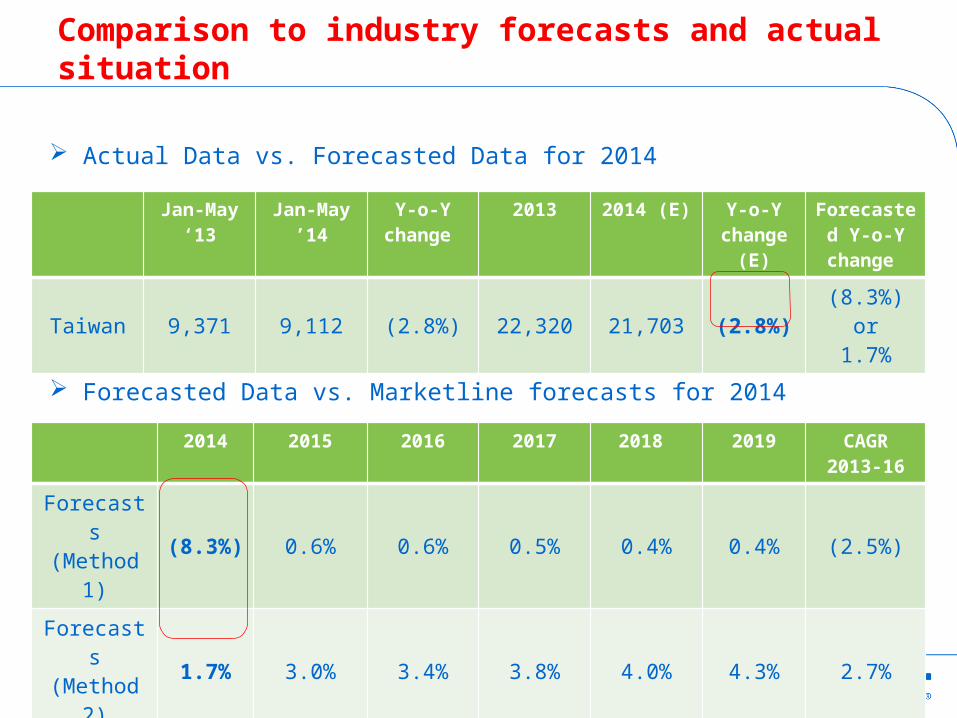

Comparison to industry forecasts and actual situation

18 April 2023Slide 59

Jan-May ‘13

Jan-May ’14

Y-o-Y change

2013 2014 (E) Y-o-Y change

(E)

Forecasted Y-o-Y

change

Taiwan 9,371 9,112 (2.8%) 22,320 21,703 (2.8%) (8.3%) or1.7%

2014 2015 2016 2017 2018 2019 CAGR2013-16

Forecasts (Method 1) (8.3%) 0.6% 0.6% 0.5% 0.4% 0.4% (2.5%)

Forecasts (Method 2) 1.7% 3.0% 3.4% 3.8% 4.0% 4.3% 2.7%

Marketline 6.1% 2.7% 6.5% 5.1% 5.1%

Actual Data vs. Forecasted Data for 2014

Forecasted Data vs. Marketline forecasts for 2014

Analysis of Vietnam

18 April 2023Slide 60

© SKF Group 18 April 2023

Data Analysis – Predictor Variables

Slide 61

Steel Production Nominal GDP (bil current LCU)

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Vietnamese Steel Production, Consumption, Export & Import(Source: World Steel Org)

Steel production (thousand tonnes)

Steel Consumption (thousand tonnes)

Steel Import (thousand tonnes)

Steel Export (thousand tonnes)

tho

usa

nd

to

nn

es

© SKF Group 18 April 2023

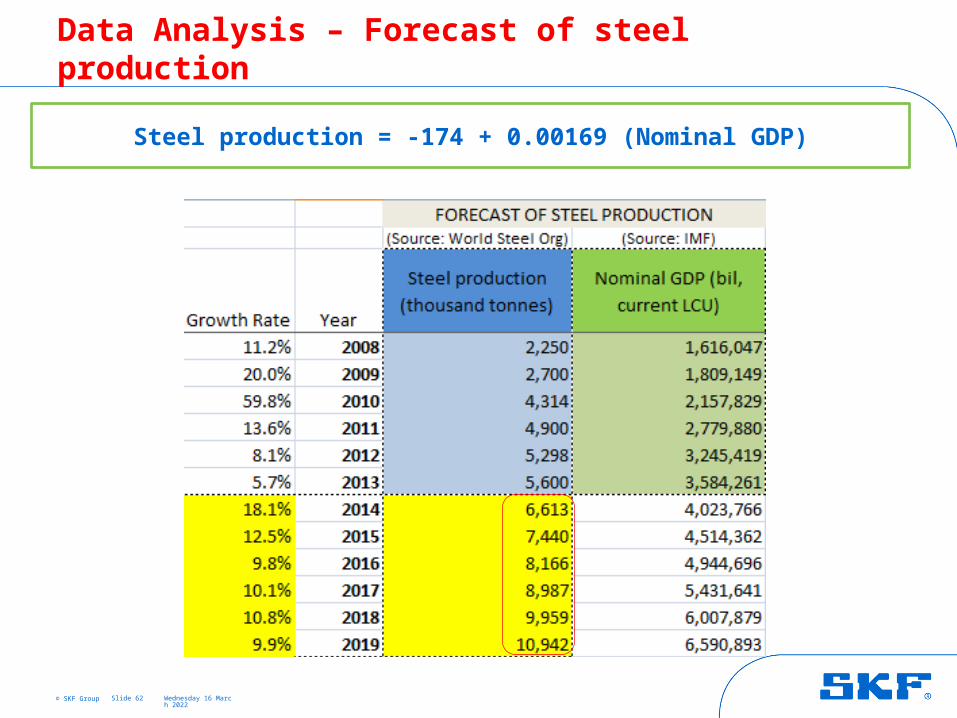

Data Analysis – Forecast of steel production

Slide 62

Steel production = -174 + 0.00169 (Nominal GDP)

© SKF Group 18 April 2023

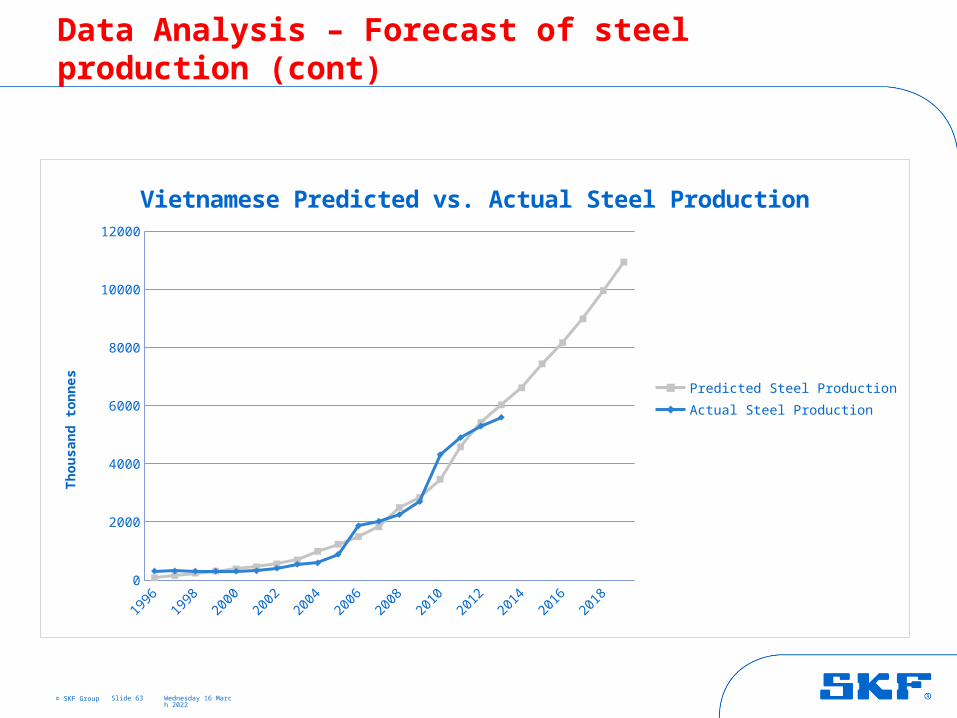

Data Analysis – Forecast of steel production (cont)

Slide 63

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

0

2000

4000

6000

8000

10000

12000

Vietnamese Predicted vs. Actual Steel Production

Predicted Steel Production

Actual Steel Production

Th

ou

san

d t

on

nes