metropolitan housing outlook: in-depth housing analysis ... · spring 2013 metropolitan housing...

TRANSCRIPT

metropolitan housing outlook Autumn 2013

in-Depth housing analysis for Canada, the provinces, and nine metropolitan areas.

About The Conference Board of CanadaWe are:

� The foremost independent, not-for-profit, applied

research organization in Canada.

� Objective and non-partisan. We do not lobby

for specific interests.

� Funded exclusively through the fees we charge

for services to the private and public sectors.

� Experts in running conferences but also at con-

ducting, publishing, and disseminating research;

helping people network; developing individual

leadership skills; and building organizational

capacity.

� Specialists in economic trends, as well

as organizational performance and public

policy issues.

� Not a government department or agency,

although we are often hired to provide

services for all levels of government.

� Independent from, but affiliated with, The

Conference Board, Inc. of New York, which

serves nearly 2,000 companies in 60 nations

and has offices in Brussels and Hong Kong.

Publication 14-190©2013 The Conference Board of Canada*Published in Canada • All rights reservedAgreement No. 40063028*Incorporated as AERIC Inc.

®The Conference Board of Canada and the torch logo are registered trademarks of The Conference Board, Inc.

Forecasts and research often involve numerous assumptions and data sources, and are subject to inherent risks and uncertainties. This information is not intended as specific investment, accounting, legal, or tax advice.

Genworth MI Canada Inc.Genworth MI Canada Inc., through its subsidiary, Genworth Financial Mortgage Insurance Company Canada, has been the leading Canadian private residen-tial mortgage insurer since 1995. Known as Genworth Canada, “The Homeownership Company,” it provides default mortgage insurance to Canadian residential mort-gage lenders that enables low-down-payment borrowers to own a home more affordably and stay in their homes during difficult financial times. Genworth Canada com-bines technological and service excellence with risk man-agement expertise to deliver innovation to the mortgage marketplace. As at September 30, 2013, Genworth Canada, had $5.6 billion in total assets and $3.0 billion in shareholders’ equity. Based in Oakville, Ontario, Genworth Canada employs approximately 260 people across Canada. Find out more at www.genworth.ca.

PrefaceThis report provides an in-depth analysis of the housing market at the national, provincial, and metropolitan lev-els. Covering a wide range of housing market statistics, such as interest rates, housing starts, mortgage approvals, and home prices, this report connects the economy with housing market activity. It also provides insights into the financial situation of consumers.

Nine census metropolitan areas are covered: Québec City, Montréal, Toronto, Ottawa–Gatineau, Winnipeg, Calgary, Edmonton, Vancouver, and Victoria.

Provincial coverage includes the Atlantic provinces, Quebec, Ontario, the Prairies, Alberta, and British Columbia.

This report is completed twice a year.

Metropolitan Housing Outlook: In-Depth Housing Analysis for Canada, the Provinces, and Nine Metropolitan Areasby Alan Arcand, Mario Lefebvre, Jane McIntyre, Greg Sutherland, and Robin Wiebe

Contents

What has Changed? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

executive summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

national overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

provincial overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Atlantic Canada . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Quebec . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Ontario . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Prairies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Alberta . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

British Columbia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

metropolitan overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30Québec City . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Montréal. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Toronto . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Ottawa–Gatineau . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

Winnipeg . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

Calgary. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Edmonton. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

Vancouver . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

Victoria. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

Definition and Concepts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

The Conference Board of Canada

The forecast for Canada’s real gross domes-

tic product is relatively unchanged from our

spring 2013 Metropolitan Housing Outlook,

as the main assumptions supporting the outlook seem

to be holding up. Growth in Canada’s real GDP is

expected to be 1.8 per cent in 2013—a second consecu-

tive year of tepid growth. However, housing markets

have strengthened in some regions over the past couple

of months, and consumer and business confidence

has picked up. As a result, the Canadian economy

is expected to perform better in 2014, expanding by

2.4 per cent. This is still a 0.1 percentage point down-

ward revision from six months ago when we completed

the previous housing outlook publication.

The Canadian dollar lost ground this past summer,

pulled down, in part, by weaker commodity prices,

including heavily discounted crude oil. The loonie is

expected to average US$0.97 this year, much lower

than the US$1.02 forecast in the previous housing out-

look. Despite some pickup in the economy in the com-

ing months, the Canadian dollar is expected to slip to

US$0.96 for 2014, a 7-cent drop from the last housing

outlook publication.

Modest economic growth and tighter mortgage rules

lowered demand in Canada’s new housing market in the

first half of this year. Accordingly, builders are expected

to reduce housing starts by 15.5 per cent in total for

2013, down to 181,400 units. This is an 800-unit

reduction from the previous Metropolitan Housing

Outlook. However, demand has already improved in

some markets, and so modest growth of 1.9 per cent is

anticipated for housing starts next year. In level terms,

housing starts are expected to be 184,900 units in 2014,

up from 184,500 units in the last publication.

Weaker demand in the Canadian housing market in

the past few months has also slowed price growth in

the new home market. The current outlook forecasts

new home prices will rise by 1.8 per cent this year

and 2 per cent in 2014. This is down from the 2.1 per

cent and 2.5 per cent increases anticipated six months

ago. Meanwhile, resale prices have been stronger so

far in 2013. Existing home prices are now expected

to increase 3.1 per cent this year, up from the 0.9 per

cent increase expected in the previous outlook. Resale

price growth will be more moderate next year, how-

ever, at 1.7 per cent, down from the 3.3 per cent

forecast previously.

The number of mortgage approvals is also expected

to be lower in 2013, slipping 2.3 per cent, the second

annual decline in a row. This is a more pronounced

drop than the 1.1 per cent decline expected six months

ago. Next year, with housing markets improving, total

mortgage approvals are anticipated to grow by 2.9 per

cent, an upward revision from the 1.7 per cent expected

in the previous forecast.

What has Changed?

The Conference Board of Canada

NaTIONal OVerVIeW

Canada’s economic prospects seem to be bright-

ening: housing markets remain decent, con-

sumer and business confidence has picked up,

and the U.S. economy is improving. Accordingly,

Canada’s real GDP is forecast to advance by 2.4 per

cent in 2014, following 1.8 per cent growth this year.

Employment growth is also forecast to pick up from

1.3 per cent this year to 1.4 per cent in 2014, cutting the

unemployment rate from 7.2 per cent to 7 per cent.

Financial markets have calmed recently. While the

European sovereign debt crisis still lurks, the eurozone

has emerged from crisis mode. The U.S. Federal Reserve

continues its policy of quantitative easing, and the Bank

of Canada has said interest rates will stay low as long as

Canada’s economy remains weak and inflation is dormant.

On the currency front, the Canadian dollar is still below

par with its U.S. counterpart, largely a result of the global

flight to the “safe haven” of the U.S. dollar. Meanwhile,

mortgage interest rates are on the rise as yields on

bonds, from which mortgages are funded, increase.

Accordingly, we expect the posted three-year conven-

tional mortgage rate to increase gradually from 3.8 per

cent in 2013 to 4.4 per cent in 2014 and 5.1 per cent in

2015. This, along with ongoing employment gains,

should allow indebted households to adapt gradually to

the resulting higher mortgage payments. There is little

sign of current mortgage stress; default rates are low.

Canadian housing markets remain generally solid, despite

repeated attempts to cool them by tightening mortgage

insurance rules. Housing starts dipped to 175,500 units

at an annual rate during the first quarter of 2013, but

quickly rebounded to 185,500 units in the second quar-

ter. We expect starts to end the year at 181,400 units.

For next year, we expect nearly 185,000 starts. New

home price growth will remain subdued at 1.8 per cent

this year and 2 per cent in 2014, down from gains of

2.2–2.4 per cent between 2010 and 2012. The national

housing market does not seem out of balance with

demographic requirements. Canada’s ratio of housing

starts to absolute population changes has averaged

0.54 over the past 25 years and has been near that each

of the past three years. Meanwhile, the national average

existing home price, which increased by a marginal

0.2 per cent in 2012, is forecast to rise 3.1 per cent to

$372,770 this year and 1.7 per cent in 2014.

In short, Canadian housing markets should land softly.

The economy continues to advance modestly. Interest

rates, although rising, remain low. Recent homebuyers

have locked in low mortgage rates and will have paid

off a relatively large share of their debt when they have

to renegotiate. New construction does not appear out of

line with demographic requirements, even in Toronto,

where concern over inflated condominium supplies

abounds. A crash would require a significant negative

surprise like an interest rate spike or employment col-

lapse. Since none of this is in the cards, a housing crash

like the one in the U.S. is nowhere near a possibility.

PrOVINCIal OVerVIeW

Stronger performance by British Columbia’s goods-pro-

ducing industries will lift GDP expansion to 3 per cent

in 2014, following a disappointing 1.5 per cent in 2013.

This will produce only 0.3 per cent job growth in 2013

but a stronger 1.7 per cent in 2014. Housing markets

are improving in Vancouver and Victoria, although a

subdued Chinese economy could cool offshore demand

for provincial real estate. Housing starts are nonetheless

forecast to decline 8 per cent in 2013, and then jump

over 10 per cent in 2014. Little change is expected in

prices for both new and existing homes in 2013 and

2014, after both dropped in 2012.

Alberta has largely shrugged off the effect of the June

floods, thanks to decent energy sector activity. Provincial

GDP is forecast to rise 3.2 per cent in 2013 and 3 per cent

in 2014. This will lift employment 2.2 per cent in 2013

and 2 per cent in 2014. Housing starts are predicted to

rise 4.3 per cent in 2013, building on a 30 per cent jump

in 2012. They should essentially stabilize in 2014. We

executive summary

Autumn 2013—metropolitan Housing Outlook | 3

The Conference Board of Canada

expect the average sale price of an existing home to rise

4.5 per cent in both 2013 and 2014; new home price

growth should be closer to 3 per cent in both years.

Healthy GDP growth of 2.5 per cent is forecast in 2013

for Manitoba and Saskatchewan combined and then

2.3 per cent in 2014. This will foster job growth of

2.2 per cent in 2013 and 1.6 per cent in 2014. Economic

momentum will largely come from Saskatchewan’s

goods-producing sector, since Manitoba’s metal mining

and services sectors are expected to be weak. Housing

starts soared 31 per cent in the two provinces combined

in 2012, but should drop 19 per cent in 2013 this year.

But construction volumes will remain very strong, in

line with continued sound population growth, and a

small 4.4 per cent rebound is expected for 2014. The

average resale home price will increase 5.3 per cent in

2013 and 4.7 per cent in 2014, while new home prices

will rise 3.3 per cent and 3.2 per cent.

Continued manufacturing struggles in 2013 will limit

Ontario’s GDP growth to 1.2 per cent, but next year

will see manufacturing improve and GDP advance

2.2 per cent. Employment is forecast to rise 1.3 per cent

in 2013 and 1.6 per cent in 2014. Housing starts are on

track to fall 21 per cent this year, led by a big drop in

multi-family starts. For 2014, we see both single and

multiple construction stabilizing, with total starts rising

by 2.5 per cent. Average existing home price growth is

forecast to slow to 2.8 per cent in 2013 and 1.6 per cent

in 2014. Moderate new home price advances are fore-

cast: 3 per cent this year and 1.8 per cent in 2014.

Quebec’s GDP is forecast to rise only 1.4 per cent this

year but a stronger 2.2 per cent in 2014. Still, employ-

ment will grow 1.4 per cent this year and 1.1 per cent

next. Significant declines in both single-detached and

multi-family construction are forecast to cut total hous-

ing starts by 24 per cent in 2013, the third consecutive

annual decline. Next year is forecast to see both single

and multiple starts stabilize. House price growth will be

modest: 1 per cent this year and 2.7 per cent in 2014 for

existing homes and advances of 1.4 per cent and 1.9 per

cent for new units.

Canada’s four Atlantic provinces will see their com-

bined GDP grow 2.3 per cent in 2013, following a 1.5

per cent contraction in 2012. A 1.9 per cent expansion

is on tap for 2014. Employment advances will remain

sluggish at 0.5 per cent in 2013 and 0.6 per cent in

2014. Housing markets are similarly weak. This year,

we expect double-digit percentage drops in both single-

detached and multi-family construction to cut total

starts by 13.4 per cent. Another 11 per cent drop is on

tap for 2014, as multiples retrench further. The average

existing home price is forecast to dip 1.5 per cent this

year, but rise 2.9 per cent in 2014. The average new

home price is forecast to rise 3.6 per cent this year and

1.7 per cent in 2014.

MuNICIPal OVerVIeW

Most cities are forecast to see somewhat slower GDP

growth in 2013 than in 2012. Victoria’s 0.1 per cent

GDP expansion (down from an already-low 0.3 per cent

in 2012) is predicted to be the slowest among our cities.

Edmonton is forecast to be this year’s leader, although

its GDP growth of 4.2 per cent will be a cooling from

hikes near or above 6 per cent in the previous three

years. For 2014, we expect growth will accelerate in all

cities except Edmonton, where it will slow to a still-

strong 3.2 per cent. Calgary’s 3.4 per cent will be next

year’s fastest advance, while Ottawa’s 1.6 per cent will

be the slowest, as the city grapples with ongoing federal

restraint. Unsurprisingly, the Alberta cities are the only

two cities where GDP growth is expected to average at

least 3 per cent per year between 2015 and 2017. By

contrast, we think Québec City’s GDP expansion will

average only 2 per cent.

For the second consecutive year, sales of existing homes

are forecast to drop everywhere except the Alberta cites in

2013. In the case of Calgary and Edmonton, sales growth,

while positive this year, will slow from the previous

year’s pace. The most notable news elsewhere is the

apparent end of Vancouver’s market correction. Sales

rose briskly during the second quarter of 2013 and

exceeded their year-earlier volume for the first time

since the third quarter of 2011. Nonetheless, sales will

still end 2013 down 2.3 per cent. Sales in Toronto are

also expected to post their second straight annual dip.

This year’s largest forecast drops are in the province of

Quebec—10 per cent in Québec City and 8 per cent in

Montréal. For 2014, we think sales will rise everywhere

except Ottawa, which will suffer a fifth straight annual

4 | metropolitan Housing Outlook—Autumn 2013

The Conference Board of Canada

sale decline. Increases will be modest elsewhere, with a

3 per cent gain in Winnipeg leading the pack. Between

2015 and 2017, sales will rise at an annual average rate

of roughly 2 to 3 per cent in most places except

Toronto, where growth will be slightly faster.

Quarterly sales-to-new-listings ratio data indicate bal-

anced markets in most cities, although the more volatile

monthly data show Calgary has edged into a sellers’ pos-

ition and Québec City has dipped into buyers’ territory.

Measured by annual data, though, we expect balanced

markets everywhere in 2013. Still, the sales-to-new-

listings ratio will fall in our five easternmost cities, led

by a 7 percentage point drop in Québec City. Vancouver

and Victoria will see 6 and 7 percentage point increases

respectively. For 2014, we expect the ratio to advance

in five cities, the largest gain being another 6 percent-

age point rise in Vancouver. Little movement in most

cities’ sales-to-new-listings ratio is expected between

2015 and 2017. A 2 percentage point increase in

Montréal and a similar decline in Winnipeg are the

only two changes greater than 1 per cent.

The average resale price is poised to rise in all cities in

2013 for the first time since 2010. Last year, the average

resale price fell in Vancouver and Victoria. This year,

prices are forecast to inch higher in both these cities,

but still at the slowest pace among our nine areas.

Unsurprisingly, we expect Calgary will enjoy the fastest

price growth in 2013, at 4.7 per cent. For 2014, we

think price growth will remain the strongest in Alberta,

with prices forecast to rise 4.6 per cent in both Calgary

and Edmonton. But price advances will remain below

2 per cent in both B.C. cities, which are again forecast to

have our nine cities’ slowest price growth. Between 2015

and 2017, price gains will be the strongest in Calgary,

Edmonton, and Winnipeg, which are all forecast to see

advances average at least 4 per cent annually.

Widespread pullbacks in housing starts are expected in

2013. Especially large drops are forecast for our eastern

cities; Montréal, Toronto, and Québec City are all

expected to see starts decline near 30 per cent, while

starts are forecast to fall 21 per cent in Ottawa. Only

Edmonton and Winnipeg are forecast to see increases,

and these will both be less than 10 per cent. Another

uneven year is expected in 2014, with starts forecast to

drop in five cities, led by a 16 per cent decline in

Edmonton. Between 2015 and 2017, we see the fastest

starts growth in Toronto and Winnipeg. During the past

five years, more multi-family units than single-detached

homes were built in six of our nine cities; multiples’

share was over 70 per cent in Québec City, Montréal,

Toronto, and Vancouver. This proliferation of multi-

family units is expected to increase, particularly in for-

mer single-family bastions like Calgary, Edmonton, and

Winnipeg. Vancouver will continue to see the lowest

share of single-detached units; these are forecast to make

up only 20 per cent of starts between 2013 and 2017.

Low and easing interest rates following the 2009 reces-

sion have contained increases in average principle and

interest payments in most cities, despite rising house

prices. Indeed, these payments were lower in 2013 than

in 2008 in Calgary, Edmonton, and Victoria and rose

only 5 to 6 per cent in Montréal, Ottawa, and Vancouver.

But carrying costs did rise in double-digit terms in

Toronto, Québec City, and Winnipeg. Rising mortgage

interest rates in 2014 are predicted to lift average monthly

mortgage payments moderately in all cities; the largest

jump will be 4.8 per cent in Calgary and Edmonton.

Vancouver remains our least affordable city, both abso-

lutely and measured against local incomes. Monthly

principle and interest payments in Vancouver are pro-

jected to average $4,030 in 2014 and consume 41 per

cent of average household income. No other city

approaches these levels.

Financial Indicators (Canada)

2012 2013f 2014f

Exchange rate (U.S./Can.) 1.00 0.97 0.96

Inflation rate 1.5 1.1 1.9

Bank rate 1.3 1.2 1.5

One-year mortgage rate 3.2 3.1 3.7

Three-year mortgage rate 3.9 3.8 4.4

Five-year mortgage rate 5.3 5.2 5.3

Federal bonds: 1–3 years 1.1 1.2 1.5

Federal bonds: 7 years 1.5 2.0 2.3

Federal bonds: long term 2.4 2.9 3.0

f = forecastSources: Bank of Canada; Canada Mortgage and Housing Corporation; Canadian Real Estate Association; Statistics Canada; The Conference Board of Canada.

Autumn 2013—metropolitan Housing Outlook | 5Ec

onom

ic In

dica

tors

GDP

(200

2 $

mill

ions

)em

ploy

men

t (00

0s)

unem

ploy

men

t rat

ePe

rson

al In

com

e pe

r Cap

itare

tail

Sale

s ($

mill

ions

)

2012

2013

f20

14f

2012

2013

f20

14f

2012

2013

f20

14f

2012

2013

f20

14f

2012

2013

f20

14f

Cana

da1,

661,

559

1,69

0,67

11,

730,

882

17,5

1017

,736

17,9

867.

37.

27.

034

,136

35,0

2836

,018

468,

252

483,

438

501,

819

1.7

1.8

2.4

1.2

1.3

1.4

3.4

2.6

2.8

2.6

3.2

3.8

atla

ntic

pro

vinc

es89

,660

91,7

0693

,415

1,11

01,

115

1,12

210

.310

.39.

835

,323

36,3

1637

,290

34,4

4935

,119

36,1

74–1.5

2.3

1.9

0.7

0.5

0.6

3.2

2.8

2.7

1.4

1.9

3.0

Queb

ec30

3,32

230

7,65

631

4,38

93,

985

4,04

24,

085

7.8

7.7

7.6

35,9

2136

,486

37,4

4910

3,64

810

5,55

110

9,22

21.0

1.4

2.2

0.8

1.4

1.1

3.1

1.6

2.6

1.1

1.8

3.5

Québ

ec C

ity32

,661

33,0

8533

,811

421

424

433

5.1

4.6

4.6

39,2

2340

,216

41,3

4712

,413

12,6

8513

,064

1.2

1.3

2.2

0.5

0.8

2.0

3.9

2.5

2.8

2.1

2.2

3.0

Mon

tréal

158,

778

160,

851

164,

287

1,97

92,

018

2,03

18.

58.

07.

936

,250

37,3

2038

,118

45,9

9348

,466

50,1

261.1

1.3

2.1

1.4

2.0

0.6

3.6

3.0

2.1

1.7

5.4

3.4

Onta

rio57

4,46

958

1,25

259

4,14

46,

786

6,87

46,

982

7.9

7.7

7.6

38,8

1039

,681

40,8

8716

5,17

716

6,62

417

3,39

11.4

1.2

2.2

0.8

1.3

1.6

2.3

2.2

3.0

1.6

0.9

4.1

Otta

wa

62,5

3263

,015

64,0

2571

269

971

06.

36.

46.

145

,137

44,8

1646

,226

17,3

7917

,470

18,0

720.8

0.8

1.6

2.5

–1.8

1.6

3.1

–0.7

3.1

2.8

0.5

3.4

Toro

nto

284,

318

288,

915

296,

856

3,00

73,

084

3,13

48.

58.

28.

040

,055

41,2

5242

,274

67,6

6968

,348

70,7

941.9

1.6

2.7

1.6

2.5

1.6

3.4

3.0

2.5

1.0

1.0

3.6

Prai

ries

106,

366

109,

063

111,

582

1,16

71,

192

1,21

25.

14.

74.

638

,399

39,5

7140

,617

34,7

6635

,404

36,9

012.4

2.5

2.3

1.5

2.2

1.6

3.7

3.1

2.6

4.6

1.8

4.2

Win

nipe

g33

,144

33,6

0434

,310

417

420

426

5.6

5.9

5.5

37,2

3138

,004

39,0

7810

,360

10,6

6911

,157

1.5

1.4

2.1

2.1

0.7

1.5

3.2

2.1

2.8

1.8

3.0

4.6

albe

rta27

6,90

828

5,64

429

4,22

62,

149

2,19

62,

240

4.6

4.7

4.7

51,7

6853

,516

54,8

5268

,452

73,0

5776

,462

3.9

3.2

3.0

2.6

2.2

2.0

5.6

3.4

2.5

6.9

6.7

4.7

Calg

ary

105,

987

109,

485

113,

164

752

770

792

4.8

4.9

4.6

55,5

2456

,602

58,1

7624

,164

25,2

2426

,531

4.3

3.3

3.4

3.7

2.4

2.8

1.5

1.9

2.8

3.6

4.4

5.2

edm

onto

n78

,082

81,3

8483

,989

693

710

722

4.7

4.5

4.6

49,1

1050

,187

51,2

2522

,467

23,6

5924

,841

5.9

4.2

3.2

3.3

2.5

1.6

2.8

2.2

2.1

4.5

5.3

5.0

Briti

sh C

olum

bia

191,

749

194,

568

200,

473

2,31

32,

320

2,36

06.

86.

56.

237

,742

38,7

0439

,810

61,5

6562

,170

64,4

771.7

1.5

3.0

1.6

0.3

1.7

3.2

2.5

2.9

1.9

1.0

3.7

Vanc

ouve

r10

8,03

811

0,42

811

3,87

21,

275

1,28

11,

313

6.7

6.5

6.2

38,7

1139

,207

40,4

9428

,628

28,9

6330

,074

2.6

2.2

3.1

1.9

0.5

2.5

3.5

1.3

3.3

3.4

1.2

3.8

Vict

oria

14,9

7614

,995

15,3

1818

618

418

55.

55.

65.

240

,656

41,1

6742

,169

4,18

34,

159

4,28

00.3

0.1

2.2

2.2

–1.2

0.7

3.1

1.3

2.4

1.2

–0.6

2.9

f = fo

reca

stIta

lics

indi

cate

per

cent

age

chan

ge.

Sour

ces:

Ban

k of

Can

ada;

Can

adia

n Re

al E

stat

e As

soci

atio

n; S

tatis

tics

Cana

da; T

he C

onfe

renc

e Bo

ard

of C

anad

a.

6 | metropolitan Housing Outlook—Autumn 2013

Dem

ogra

phic

and

Hou

sing

Indi

cato

rs

Popu

latio

n (0

00s)

Hous

ing

Star

tsHo

usin

g Co

mpl

etio

nsex

istin

g Ho

me

Pric

esNe

w H

ome

Pric

es

2012

2013

f20

14f

2012

2013

f20

14f

2012

2013

f20

14f

2012

2013

f20

14f

2012

2013

f20

14f

Cana

da34

,827

35,1

9335

,586

214,

827

181,

446

184,

927

180,

646

188,

966

177,

776

361,

494

372,

769

379,

236

413,

730

421,

284

429,

782

1.1

1.1

1.1

10.8

–15.5

1.9

3.0

4.6

–5.9

0.2

3.1

1.7

2.3

1.8

2.0

atla

ntic

pro

vinc

es2,

363

2,36

12,

366

12,6

4710

,950

9,73

411

,699

11,3

5210

,109

142,

756

140,

607

144,

668

339,

660

351,

763

357,

729

0.1

–0.1

0.2

1.0

–13.4

–11.1

2.8

–3.0

–11.0

1.0

–1.5

2.9

2.3

3.6

1.7

Queb

ec8,

043

8,10

98,

173

47,3

6736

,220

36,3

9544

,564

42,7

5837

,309

272,

014

274,

868

282,

264

304,

180

308,

506

314,

380

0.9

0.8

0.8

–2.1

–23.5

0.5

0.1

–4.1

–12.7

4.1

1.0

2.7

1.5

1.4

1.9

Québ

ec C

ity77

077

778

46,

262

4,38

64,

134

5,51

84,

881

4,00

725

6,19

626

7,82

127

4,74

323

2,17

623

5,38

723

9,89

81.1

1.0

0.9

12.6

–30.0

–5.8

–2.6

–11.5

–17.9

5.0

4.5

2.6

2.9

1.4

1.9

Mon

tréal

3,95

83,

996

4,03

720

,420

14,3

7615

,392

19,0

9217

,110

14,8

8331

8,24

432

3,25

333

1,30

332

5,45

933

0,35

033

6,94

91.0

1.0

1.0

–9.9

–29.6

7.1

–3.9

–10.4

–13.0

3.5

1.6

2.5

1.4

1.5

2.0

Onta

rio13

,489

13,6

0613

,755

76,7

4260

,326

61,8

0558

,613

63,8

8660

,512

381,

328

392,

017

398,

171

517,

813

533,

304

542,

869

1.0

0.9

1.1

13.2

–21.4

2.5

–3.3

9.0

–5.3

5.0

2.8

1.6

4.7

3.0

1.8

Otta

wa

1,27

31,

286

1,29

48,

873

7,03

46,

225

8,12

26,

838

6,63

132

9,15

033

3,74

633

9,77

140

4,02

740

8,56

441

6,64

41.4

1.0

0.7

6.3

–20.7

–11.5

–2.8

–15.8

–3.0

2.5

1.4

1.8

2.6

1.1

2.0

Toro

nto

5,94

16,

042

6,14

748

,368

34,1

3338

,717

31,9

0736

,403

38,7

4852

0,66

353

3,03

554

3,45

660

5,47

362

0,13

763

1,16

91.7

1.7

1.7

21.7

–29.4

13.4

–5.7

14.1

6.4

7.5

2.4

2.0

5.1

2.4

1.8

Prai

ries

2,34

22,

378

2,41

717

,210

13,8

7014

,477

12,8

6914

,715

13,5

1326

0,30

827

4,07

028

6,99

039

7,47

041

0,65

942

3,78

01.6

1.5

1.7

31.2

–19.4

4.4

6.6

14.3

–8.2

5.5

5.3

4.7

3.2

3.3

3.2

Win

nipe

g77

878

979

84,

025

4,30

43,

953

3,25

83,

891

3,93

325

5,08

026

3,52

927

3,44

643

2,93

044

9,45

845

8,24

91.6

1.3

1.2

20.5

6.9

–8.2

2.5

19.4

1.1

5.7

3.3

3.8

4.2

3.8

2.0

albe

rta3,

860

3,97

34,

051

33,3

9634

,823

34,6

9826

,446

31,8

1131

,701

361,

969

378,

376

395,

376

435,

951

447,

813

462,

468

2.4

2.9

2.0

29.9

4.3

–0.4

8.9

20.3

–0.3

2.6

4.5

4.5

1.1

2.7

3.3

Calg

ary

1,30

91,

350

1,37

813

,186

12,8

3413

,444

9,59

312

,129

12,9

1241

2,31

543

1,76

045

1,79

849

0,12

850

9,41

552

6,00

23.2

3.1

2.1

43.5

–2.7

4.8

24.8

26.4

6.5

2.3

4.7

4.6

1.7

3.9

3.3

edm

onto

n1,

230

1,26

41,

289

12,7

5814

,006

11,7

3410

,166

13,1

1412

,442

334,

300

346,

581

362,

609

382,

809

387,

803

399,

334

2.8

2.8

1.9

38.3

9.8

–16.2

13.7

29.0

–5.1

2.7

3.7

4.6

0.9

1.3

3.0

Briti

sh C

olum

bia

4,61

84,

657

4,71

227

,465

25,2

5727

,819

26,3

8025

,564

25,4

2551

2,97

451

6,75

352

9,04

663

4,71

563

4,71

464

4,99

01.0

0.9

1.2

4.0

–8.0

10.1

17.0

–3.1

–0.5

–7.9

0.7

2.4

–0.4

0.0

1.6

Vanc

ouve

r2,

464

2,50

12,

541

19,0

7117

,357

16,5

3616

,958

18,0

7317

,339

730,

063

737,

162

750,

861

662,

097

662,

452

674,

797

1.5

1.5

1.6

6.7

–9.0

–4.7

31.3

6.6

–4.1

–6.4

1.0

1.9

–0.5

0.1

1.9

Vict

oria

363

365

367

1,66

31,

347

1,46

51,

591

1,61

01,

434

484,

164

486,

225

492,

802

400,

585

397,

915

403,

822

0.4

0.4

0.6

1.9

–19.0

8.7

–3.1

1.2

–10.9

–2.8

0.4

1.4

–2.8

–0.7

1.5

f = fo

reca

stIta

lics

indi

cate

per

cent

age

chan

ge.

Sour

ces:

CM

HC H

ousi

ng T

ime

Serie

s Da

taba

se; C

anad

ian

Real

Est

ate

Asso

ciat

ion;

Que

bec

Fede

ratio

n of

Rea

l Est

ate

Boar

ds; S

tatis

tics

Cana

da; T

he C

onfe

renc

e Bo

ard

of C

anad

a.

Autumn 2013—metropolitan Housing Outlook | 7

The Conference Board of Canada

national overview

Canada’s economy is again expected to grow by a modest 1.8 per cent this year, but increase to 2.4 per cent growth in 2014 thanks to the improv-

ing U.S. economy next year. A slower resale housing market and tighter mortgage rules discouraged builders in the new home market through the last half of 2012 and into the first quarter of 2013. Although starts have picked up again in recent months, the outlook calls for total housing starts to decline 15.5 per cent this year and grow by just 1.9 per cent next year.

eCONOMIC OuTlOOk

Canada’s real gross domestic product is set to grow by

1.8 per cent in 2013. For much of the first half of 2013,

economic indicators provided few encouraging signs.

But through the summer, consumer and business con-

fidence picked up and the U.S. economy gained some

speed. Indeed, stronger business investment is expected

to help Canada’s economic growth advance at a reason-

able pace (above 2 per cent) through the second half

of this year, leading to a 2.4 per cent forecast increase

in real GDP for 2014. However, hiring will remain

muted. And, while tight labour markets (especially in

Saskatchewan and Alberta) and subdued inflation will

help lift households’ purchasing power, real consumer

spending will not outpace income as households try to

reduce their debt burdens and increase savings. Public

sector spending will also remain muted this year and

next. Provincial and federal governments are both

targeting balanced budgets, some sooner than others,

resulting in very little contribution to economic growth.

Still, some provinces have avoided cutting back on

much-needed infrastructure, and most provinces are

accommodating modest budgetary increases to health

care spending. Thus, the brunt of the public sector cuts

in 2013–14 will be felt in public administration, educa-

tion, and social programs.

Canada

Housing Starts(000s)

f = forecastSources: The Conference Board of Canada; CMHC Housing TimeSeries Database.

House Price Growth(percentage chage)

f = forecastSources: The Conference Board of Canada; CMHC Housing TimeSeries Database; Canadian Real Estate Association; Quebec Federation of Real Estate Boards.

2010 11 12 13f 14f 15f 16f 17f0

50100150200250

Singles Multiples 20-year average

2010 11 12 13f 14f 15f 16f 17f0

2

4

6

8New Resale

8 | metropolitan Housing Outlook—Autumn 2013

The Conference Board of Canada

FINaNCIal MarkeTS OuTlOOk

The U.S. Federal Reserve has reiterated that the cur-

rent pace of quantitative easing through major bond

purchases will continue until the unemployment rate

falls below 7 per cent, and that interest rates will remain

essentially at zero until even later, when the unemploy-

ment rate falls to below 6.5 per cent. Equity markets

have been appeased, recovering from an early summer

dive and stabilizing. At the same time, given that the

Canadian economy is not yet at full capacity and that

near-term growth may be choppy, the Bank of Canada

has indicated that monetary conditions will remain

loose until economic growth strengthens or inflation

starts to accelerate. We expect the Bank of Canada will

likely start raising rates gradually by mid-2014, well

ahead of the U.S., largely because the gap between the

economic potential and the current output level is sig-

nificantly smaller in Canada than in the United States.

Therefore, as economic conditions improve south of

the border, excess capacity in Canada will be eaten up

more quickly.

Over the past few months, the loonie has lost ground

vis-à-vis the greenback. In part, the swoon in the

Canadian dollar—from above parity in February to

below US$0.95 in July—was the result of softer com-

modity prices, especially heavily discounted Western

Canadian Select crude oil. But it was also about the

strength in the U.S. dollar, as Canada’s currency

remained steady in comparison with many other curren-

cies. Federal Reserve statements about possibly easing

the pace of bond purchases in its quantitative easing

program made global financial and equity markets nerv-

ous and pushed up the value of the U.S. dollar. Overall,

the Canadian dollar is expected to average US$0.97 this

year and US$0.96 in 2014.

HOuSING OuTlOOk

Canada’s new home market capped an impressive

three-year run of growth last year. From 2010 to

2012, a recovering economy and low interest rates

drove demand for new homes, as builders increased

starts by an average of 13.4 per cent per year, up to

214,800 units in 2012—back above 200,000 units for

the first time since 2008. Growth in multiple-unit starts

was particularly strong over the past two years, thanks

to a wave of condominium development across the

country. But new home price growth remained modest,

at an annual average of 2.3 per cent. Average annual

growth in existing home prices was a much stronger

6.7 per cent in 2010 and 2011, but fell to just 0.2 per

cent last year, signalling a slower resale market. While

housing starts rose nearly 11 per cent in total last year,

developers began to curtail new home construction in

the second half of the year. The new home market was

feeling the effects of the federal government’s decision

to limit rising household debt by steadily lowering the

qualifying period for insured mortgages from 40 years

in 2008 to just 25 years by mid-2012, making it diffi-

cult for some first-time homebuyers to enter the market.

With economic growth tepid, builders continued to

reduce housing starts through the first quarter of 2013.

Starts then increased once again in the second quarter

Mortgage Approval Growth(dollar volume percentage change)

f = forecastSources: The Conference Board of Canada; Genworth MI Canada; CMHC Housing Time Series Database.

Household Net Worth(as a per cent of disposable income)

Sources: The Conference Board of Canada; Statistics Canada.

2010 11 12 13f 14f 15f 16f 17f−15−10

−505

1015

Conventional High-ratio

1998 00 02 04 06 08 10 12500

550

600

650

700

Autumn 2013—metropolitan Housing Outlook | 9

The Conference Board of Canada

of this year. In part, builders were lured back to the

market by rising sales of existing homes and prices

in the first months of 2013. Still, the Canadian hous-

ing market is expected to stay cool this year and next.

Following the recent run-up in multiple starts in a

number of urban centres, a significant number of new

units will become available over coming months, help-

ing to keep some builders at bay. Overall, housing

starts are forecast to fall by 15.5 per cent to 181,400

units in 2013 and increase by a modest 1.9 per cent

to 184,900 units in 2014. New home price growth is

expected to remain around 2 per cent this year and next.

Meanwhile, resale home prices are set to rise 3.1 per

cent in 2013, because of stronger gains at the beginning

of this year, and a much more moderate 1.7 per cent

next year.

Looking ahead, there is room for more growth in the

new home market. In general, even with the significant

growth in housing starts since 2010, they are still in line

with demographic requirements. Over the past 20 years

on average, 0.47 homes have been started per additional

person in Canada’s population. During the past three

years, this ratio has been 0.46—well within historical

norms. By 2015, better employment gains will also

reignite demand despite the gradual rise in interest

Consumer Finances(left, per cent; right, per 1 million people)

1998 00 02 04 06 08 10 120.10.20.30.40.50.60.7

100125150175200225250

Mortgages in arrears Bankruptcies

1998 00 02 04 06 08 10 120.3

0.4

0.5

0.6

0.7

50

100

150

200

250Mortgages in arrears Bankruptcies

1998 00 02 04 06 08 10 120.1

0.3

0.5

0.7

0.9

200

250

300

350

400Mortgages in arrears Bankruptcies

1998 00 02 04 06 08 10 120.20.30.40.50.60.7

100150200250300350

Mortgages in arrears Bankruptcies

1998 00 02 04 06 08 10 120

0.2

0.4

0.6

0.8

60

100

140

180

220Mortgages in arrears Bankruptcies

1998 00 02 04 06 08 10 120.1

0.3

0.5

0.7

0.9

100

150

200

250

300Mortgages in arrears Bankruptcies

Atlantic Provinces Quebec

Ontario Prairie Provinces

Alberta British Columbia

Sources: The Conference Board of Canada; Canadian Bankers Association; Superintendent of Bankruptcy Canada.

10 | metropolitan Housing Outlook—Autumn 2013

The Conference Board of Canada

rates. As economic growth accelerates, therefore,

developers will be encouraged to boost housing starts to

about 197,100 units in 2015 and above 210,000 units by

2017. Growth in new home prices is forecast to remain

at 2 per cent on an average annual basis from 2015 to

2017, while resale price growth will be slightly higher,

at 2.5 per cent per year on average.

MOrTGaGe OuTlOOk

Mortgage interest rates are widely expected to increase

in the next year, pushing up carrying costs. Yields on

bonds, from which banks finance mortgages, have already

moved higher. Still, the Bank of Canada is not expected

to start raising its overnight rate before mid-2014, and

even then, the Bank will raise rates only gradually, giv-

ing households time to adapt. Furthermore, employment

and income growth will help to further alleviate some of

the pressure of rising interest rates on households. In fact,

rising mortgage rates could even provide a short-term

boost to the market, as house-hunters with mortgages

pre-approved at low interest rates rush to buy homes

before these contracted rates expire. The current out-

look calls for the three-year conventional mortgage rate

to rise from a record-low 3.8 per cent this year to 4.4

per cent in 2014 and 5.1 per cent in 2015.

The total number of mortgage approvals fell by 0.3 per

cent 2012, as the resale housing market slowed in the

second half of last year. Approvals in the new home

market continued to climb however, rising 2.2 per

cent. Both markets are forecast to see lower levels of

mortgage approvals in 2013, reducing total approvals

by 2.3 per cent. With growth in the new home market

expected to be modest in 2014, the number of new

mortgage approvals will decline once again. However,

thanks to the existing home market, total mortgage

approvals are anticipated to rise in 2014, up by 2.9 per

cent. The dollar volume of mortgage approvals rose

0.7 per cent last year, thanks to price growth in the

new and resale markets. A similar increase is expected

for 2013, with growth in dollar volumes improving to

4.5 per cent next year. Not surprising, tighter mortgage

rules are having a bigger impact on the number of

high-ratio mortgage approvals (set to fall 3.1 per cent

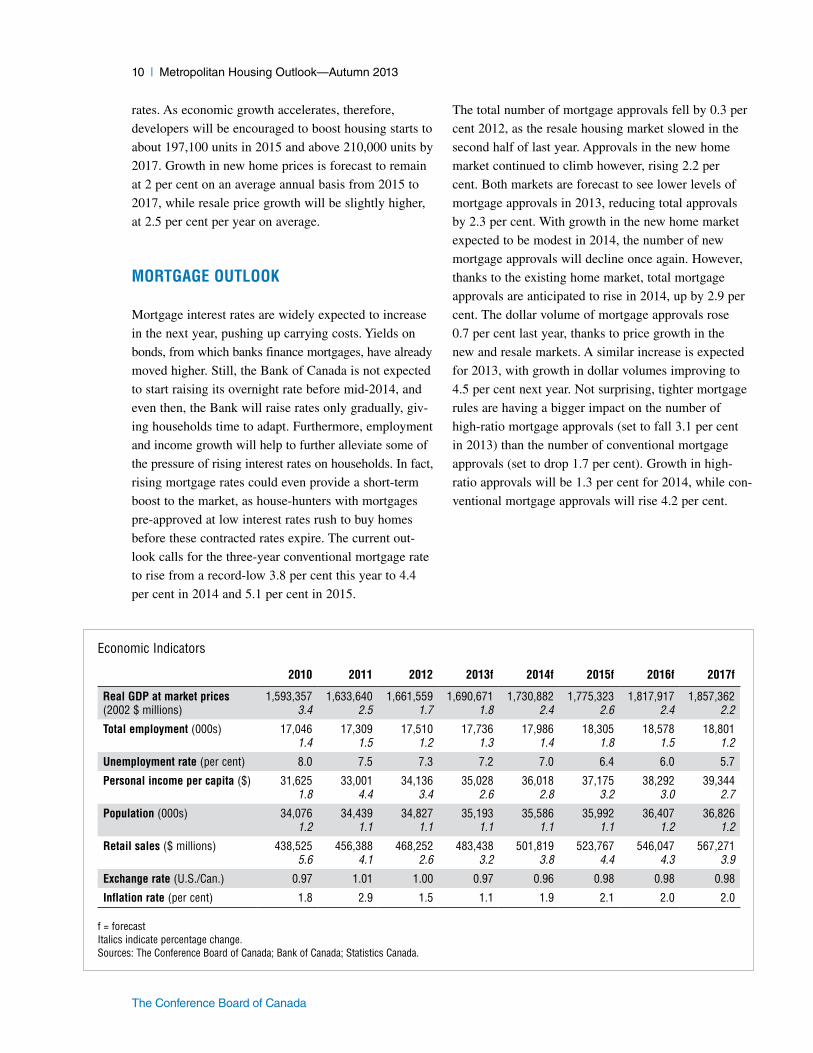

in 2013) than the number of conventional mortgage

approvals (set to drop 1.7 per cent). Growth in high-

ratio approvals will be 1.3 per cent for 2014, while con-

ventional mortgage approvals will rise 4.2 per cent.

Economic Indicators

2010 2011 2012 2013f 2014f 2015f 2016f 2017f

real GDP at market prices 1,593,357 1,633,640 1,661,559 1,690,671 1,730,882 1,775,323 1,817,917 1,857,362(2002 $ millions) 3.4 2.5 1.7 1.8 2.4 2.6 2.4 2.2

Total employment (000s) 17,046 17,309 17,510 17,736 17,986 18,305 18,578 18,8011.4 1.5 1.2 1.3 1.4 1.8 1.5 1.2

unemployment rate (per cent) 8.0 7.5 7.3 7.2 7.0 6.4 6.0 5.7

Personal income per capita ($) 31,625 33,001 34,136 35,028 36,018 37,175 38,292 39,3441.8 4.4 3.4 2.6 2.8 3.2 3.0 2.7

Population (000s) 34,076 34,439 34,827 35,193 35,586 35,992 36,407 36,8261.2 1.1 1.1 1.1 1.1 1.1 1.2 1.2

retail sales ($ millions) 438,525 456,388 468,252 483,438 501,819 523,767 546,047 567,2715.6 4.1 2.6 3.2 3.8 4.4 4.3 3.9

exchange rate (U.S./Can.) 0.97 1.01 1.00 0.97 0.96 0.98 0.98 0.98

Inflation rate (per cent) 1.8 2.9 1.5 1.1 1.9 2.1 2.0 2.0

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Bank of Canada; Statistics Canada.

Autumn 2013—metropolitan Housing Outlook | 11

The Conference Board of Canada

Financial Indicators(per cent)

2010 2011 2012 2013f 2014f 2015f 2016f 2017f

Bank rate 0.9 1.3 1.3 1.2 1.5 2.3 3.2 3.9

Prime lending rate 2.6 3.0 3.0 3.0 3.3 4.1 5.0 5.7

Three-month Treasury bill 0.6 0.9 1.0 1.0 1.2 2.0 2.9 3.5

One-year conventional mortgage rate 3.5 3.5 3.2 3.1 3.7 4.5 5.4 6.0

Three-year conventional mortgage rate 4.3 4.3 3.9 3.8 4.4 5.1 5.9 6.6

Five-year conventional mortgage rate 5.6 5.4 5.3 5.2 5.3 5.6 6.3 6.9

Federal bonds: 1 year 1.5 1.4 1.1 1.2 1.5 2.1 2.9 3.6

Federal bonds: 5 years 2.4 2.1 1.4 1.7 2.0 2.4 3.0 3.6

Federal bonds: 7 years 2.7 2.3 1.5 2.0 2.3 2.5 3.1 3.7

Federal bonds: 10 years 3.2 2.8 1.9 2.3 2.5 2.7 3.2 3.8

Federal bonds: long term 3.7 3.3 2.4 2.9 3.0 3.0 3.4 3.9

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; Bank of Canada; Statistics Canada.

Housing Indicators

2010 2011 2012 2013f 2014f 2015f 2016f 2017f

Housing starts 189,930 193,950 214,827 181,446 184,927 197,088 207,126 210,21227.4 2.1 10.8 –15.5 1.9 6.6 5.1 1.5

Singles 92,554 82,392 83,657 76,797 77,530 81,028 84,391 82,60922.3 –11.0 1.5 –8.2 1.0 4.5 4.1 –2.1

Multiples 97,376 111,558 131,170 104,650 107,397 116,060 122,735 127,60332.6 14.6 17.6 –20.2 2.6 8.1 5.8 4.0

Housing completions 186,212 175,431 180,646 188,966 177,776 183,522 195,782 201,2935.3 –5.8 3.0 4.6 –5.9 3.2 6.7 2.8

Singles 90,578 79,976 80,630 79,303 76,330 78,099 82,314 82,29315.7 –11.7 0.8 –1.6 –3.7 2.3 5.4 0.0

Multiples 95,635 95,455 100,015 109,663 101,446 105,423 113,468 119,000–3.0 –0.2 4.8 9.6 –7.5 3.9 7.6 4.9

average price of a new home ($) 395,561 404,247 413,730 421,284 429,782 439,275 447,938 456,4882.2 2.2 2.3 1.8 2.0 2.2 2.0 1.9

average price of a resale home ($) 338,199 360,648 361,494 372,769 379,236 389,163 399,110 408,6576.8 6.6 0.2 3.1 1.7 2.6 2.6 2.4

f = forecastItalics indicate percentage change.Sources: The Conference Board of Canada; CMHC Housing Time Series Database; Canadian Real Estate Association; Quebec Federation of Real Estate Boards; Statistics Canada.

12 | metropolitan Housing Outlook—Autumn 2013

The Conference Board of Canada

G rowth in the Atlantic Canadian economy is expected to be 2.3 per cent this year and 1.9 per cent in 2014. Rising oil production both in

Newfoundland and Labrador and in Nova Scotia is contrib-uting to these increases. However, housing starts in all four provinces are forecast to decline in 2013 and 2014, having topped 10,000 units for the past 12 years now. Starts will continue to fall in the medium term as well, bringing them back in line with demographic needs.

eCONOMIC OuTlOOk

Atlantic Canada’s real gross domestic product is

expected to grow by 2.3 per cent in 2013, following a

1.5 per cent contraction in 2012. The region’s economy

is then forecast to post a more modest increase in 2014,

rising 1.9 per cent. Much of the decrease in real GDP

last year, and the strength this year, has been driven by

change in the Newfoundland and Labrador economy.

The province’s economy contracted by 4.8 per cent

in 2012, largely because of a 20 per cent drop in oil

production. This year, renewed growth in the oil sec-

tor, along with a booming construction industry, will

allow Newfoundland and Labrador’s economy to grow

by a forecast 5.4 per cent. Meanwhile, after strug-

gling for the past two years, Nova Scotia’s economy

look brighter in the short term as well, thanks to Deep

Panuke’s newly completed offshore natural gas field.

Production at the field is forecast to help lift real GDP

growth from 1.1 per cent 2013 to 2.9 per cent next

year. However, the economy of Prince Edward Island

continues to face a less-than-stellar outlook. Efforts by

the provincial and federal governments to balance their

budgets will continue to weigh on the economy, holding

growth in real GDP to a forecast 1.3 per cent this year

and just 1 per cent in 2014. In New Brunswick, eco-

nomic growth is forecast to accelerate from 0.8 per cent

in 2013 to 1.9 per cent next year, as weakness in the

construction and food processing sectors offsets gains

in the resources and manufacturing sectors.

provincial overview

atlantic Canada

Housing Starts(000s)

f = forecastSources: The Conference Board of Canada; CMHC Housing TimeSeries Database.

2010 11 12 13f 14f 15f 16f 17f0

5

10

15

Singles Multiples 20-year average

House Price Growth(percentage chage)

f = forecastSources: The Conference Board of Canada; CMHC Housing TimeSeries Database; Canadian Real Estate Association.

2010 11 12 13f 14f 15f 16f 17f−2

0

2

4

6

New Resale

Autumn 2013—metropolitan Housing Outlook | 13

The Conference Board of Canada

HOuSING OuTlOOk

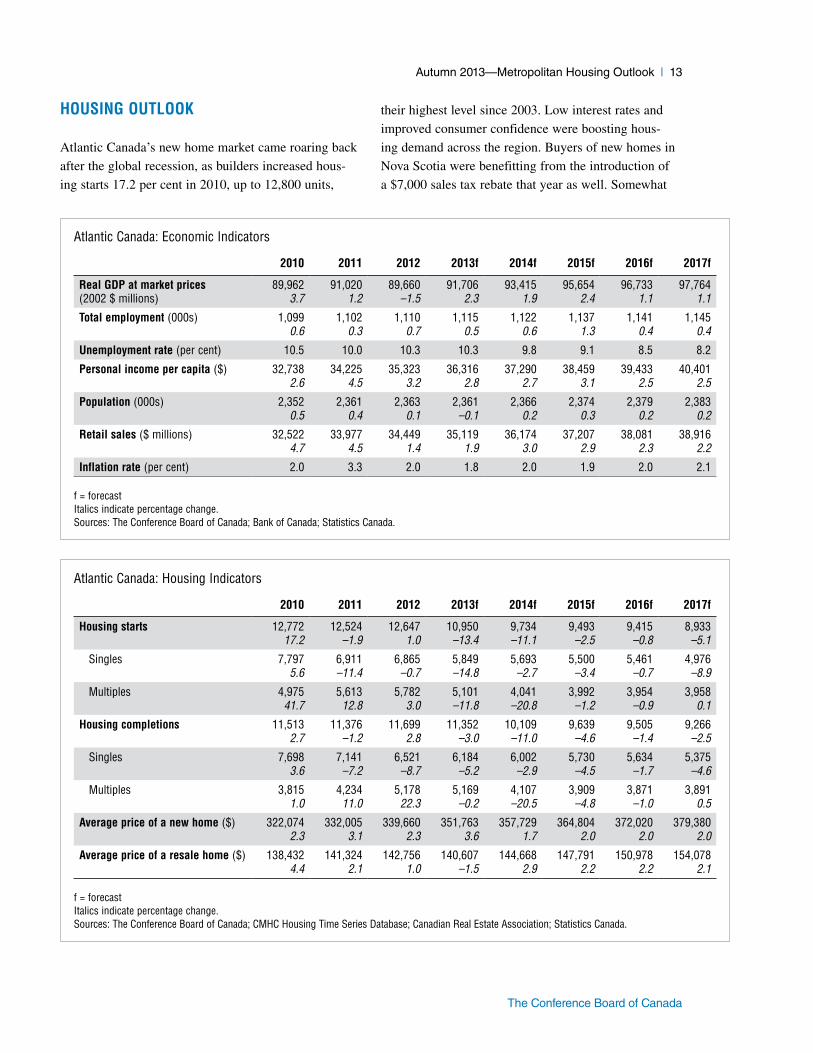

Atlantic Canada’s new home market came roaring back

after the global recession, as builders increased hous-

ing starts 17.2 per cent in 2010, up to 12,800 units,

their highest level since 2003. Low interest rates and

improved consumer confidence were boosting hous-

ing demand across the region. Buyers of new homes in

Nova Scotia were benefitting from the introduction of

a $7,000 sales tax rebate that year as well. Somewhat

Atlantic Canada: Economic Indicators

2010 2011 2012 2013f 2014f 2015f 2016f 2017f

real GDP at market prices 89,962 91,020 89,660 91,706 93,415 95,654 96,733 97,764(2002 $ millions) 3.7 1.2 –1.5 2.3 1.9 2.4 1.1 1.1

Total employment (000s) 1,099 1,102 1,110 1,115 1,122 1,137 1,141 1,1450.6 0.3 0.7 0.5 0.6 1.3 0.4 0.4

unemployment rate (per cent) 10.5 10.0 10.3 10.3 9.8 9.1 8.5 8.2

Personal income per capita ($) 32,738 34,225 35,323 36,316 37,290 38,459 39,433 40,4012.6 4.5 3.2 2.8 2.7 3.1 2.5 2.5

Population (000s) 2,352 2,361 2,363 2,361 2,366 2,374 2,379 2,3830.5 0.4 0.1 –0.1 0.2 0.3 0.2 0.2

retail sales ($ millions) 32,522 33,977 34,449 35,119 36,174 37,207 38,081 38,9164.7 4.5 1.4 1.9 3.0 2.9 2.3 2.2

Inflation rate (per cent) 2.0 3.3 2.0 1.8 2.0 1.9 2.0 2.1

f = forecast Italics indicate percentage change.Sources: The Conference Board of Canada; Bank of Canada; Statistics Canada.

Atlantic Canada: Housing Indicators

2010 2011 2012 2013f 2014f 2015f 2016f 2017f

Housing starts 12,772 12,524 12,647 10,950 9,734 9,493 9,415 8,93317.2 –1.9 1.0 –13.4 –11.1 –2.5 –0.8 –5.1

Singles 7,797 6,911 6,865 5,849 5,693 5,500 5,461 4,9765.6 –11.4 –0.7 –14.8 –2.7 –3.4 –0.7 –8.9

Multiples 4,975 5,613 5,782 5,101 4,041 3,992 3,954 3,95841.7 12.8 3.0 –11.8 –20.8 –1.2 –0.9 0.1

Housing completions 11,513 11,376 11,699 11,352 10,109 9,639 9,505 9,2662.7 –1.2 2.8 –3.0 –11.0 –4.6 –1.4 –2.5

Singles 7,698 7,141 6,521 6,184 6,002 5,730 5,634 5,3753.6 –7.2 –8.7 –5.2 –2.9 –4.5 –1.7 –4.6

Multiples 3,815 4,234 5,178 5,169 4,107 3,909 3,871 3,8911.0 11.0 22.3 –0.2 –20.5 –4.8 –1.0 0.5

average price of a new home ($) 322,074 332,005 339,660 351,763 357,729 364,804 372,020 379,3802.3 3.1 2.3 3.6 1.7 2.0 2.0 2.0

average price of a resale home ($) 138,432 141,324 142,756 140,607 144,668 147,791 150,978 154,0784.4 2.1 1.0 –1.5 2.9 2.2 2.2 2.1

f = forecast Italics indicate percentage change.Sources: The Conference Board of Canada; CMHC Housing Time Series Database; Canadian Real Estate Association; Statistics Canada.

14 | metropolitan Housing Outlook—Autumn 2013

The Conference Board of Canada

surprisingly, even though demand was accelerating,

growth in new home prices was slowing, slipping to a

modest 2.3 per cent in 2010, down from 3.1 per cent the

previous year and 10.9 per cent in 2008. In the resale

market, existing home prices did strengthen a little in

2010, rising from 3.7 per cent in 2009 to 4.4 per cent.

Weaker economies hampered demand in the hous-

ing markets in Newfoundland and Labrador and in

New Brunswick in 2011. In turn, builders in those

two provinces reduced housing starts, lowering them

1.9 per cent for the Atlantic region as a whole—even

though starts in Nova Scotia and Prince Edward Island

continued to increase. Indeed, Prince Edward Island’s

new home market was particularly busy in 2011, with

builders raising starts by nearly 25 per cent in response

to stronger international migration numbers as a result

of the province’s nominee program. Builders in Prince

Edward Island held housing starts steady last year as

well. A number of new condominium developments

also increased starts in Newfoundland and Labrador’s

new home market in 2012. But, with real GDP growth

still muted, starts fell in each of Nova Scotia and

New Brunswick, holding the increase in total starts

for Atlantic Canada to just 1 per cent last year. Home

prices in the new and resale markets continued to be

modest over the past two years, increasing 2.7 per cent

on an average annual basis in the new market and an

average of 1.6 per cent in the resale market.

In spite of stronger economic growth overall for

Atlantic Canada in 2013, tighter mortgage rules, the

completion of some condominium projects, and a return

to more modest population growth in Prince Edward

Island have all been lowering demand in the region’s

new home market. In addition, in level terms, housing

starts in Atlantic Canada have been well above demo-

graphic requirements for a number of years now, having

topped 10,000 units annually for more than a decade.

Moreover, with interest rates eventually rising, builders

are expected to lower Atlantic Canada’s housing starts

both this year and through the medium term. Starts are

forecast to fall 13.4 per cent in 2013, 11.1 per cent in

2014, and by an average of 2.8 per cent per year from

2015 to 2017.

Growth in new home prices is expected to rise slightly

in 2013, up to 3.6 per cent, while resale prices are fore-

cast to fall 1.5 per cent, the first annual price decline in

13 years. Over the rest of the forecast, 2014 to 2017,

price growth in the new market is anticipated to aver-

age 1.9 per cent annually, while it is forecast to average

2.3 per cent per year in the resale market.

Autumn 2013—metropolitan Housing Outlook | 15

The Conference Board of Canada

A soft investment outlook, along with weak external demand, has led to anemic employment growth and unsteady household confidence in Quebec

this year, holding real GDP growth to 1.4 per cent. Quebec’s new home market will also remain weak in 2013, with total starts falling 23.5 per cent. A balanced market and better economic growth in 2014 will encourage builders to raise starts an average of 2.4 per cent annually through 2014 and 2015.

eCONOMIC OuTlOOk

Growth in Quebec’s real gross domestic product is

forecast to accelerate to a still modest 1.4 per cent this

year, following an increase of only 1 per cent in 2012.

A weak investment outlook for both the residential

and non-residential construction sectors, coupled with

weak demand for exports, underpins this year’s soft

prognosis. But the much anticipated recovery in the

U.S. economy and its housing market should improve

export growth and the manufacturing outlook in 2014.

Full production of Bombardier’s CSeries aircraft, to be

assembled near Montréal, will provide an additional

economic boost. Meanwhile, consumer spending is

only slowly improving. Employment is forecast to gain

1.4 per cent in 2013 and 1.1 per cent in 2014, bringing

the unemployment rate down only slightly to 7.6 per

cent next year. Consumers will remain understandably

wary. In all, the provincial economy is forecast to grow

by 2.2 per cent in 2014. The medium term looks decent,

with GDP predicted to rise 2.5 per cent in 2015 and

2 per cent in 2016.

HOuSING OuTlOOk

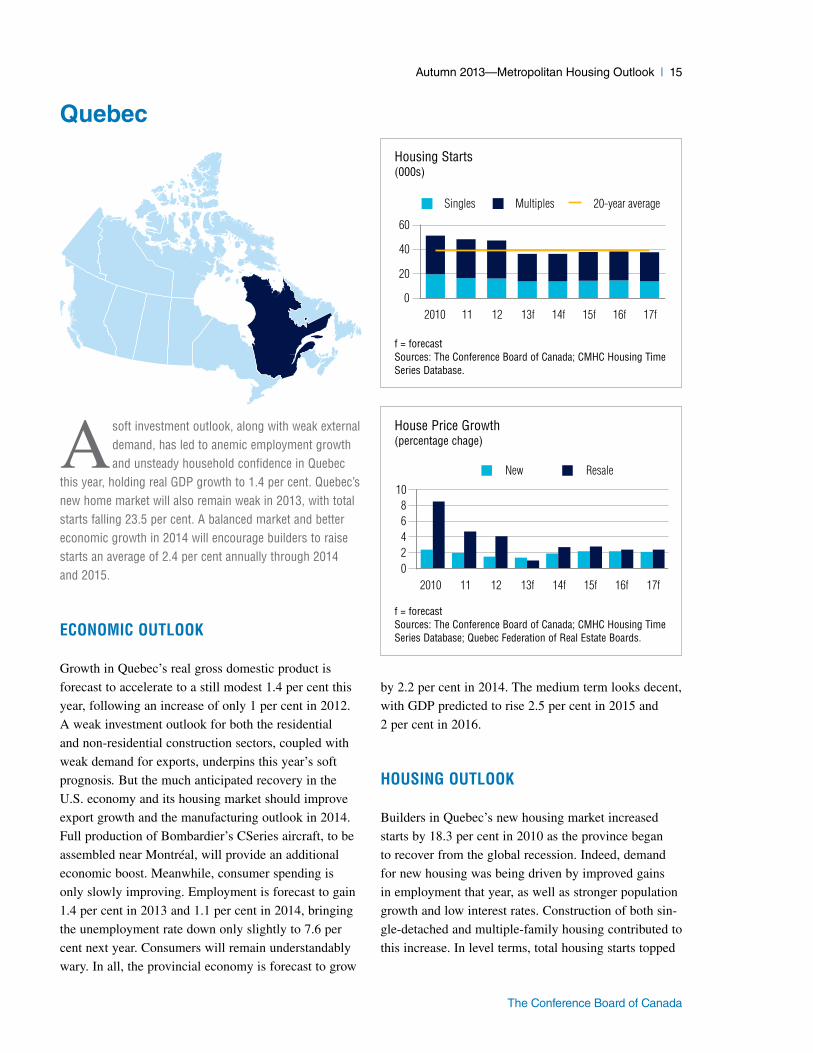

Builders in Quebec’s new housing market increased

starts by 18.3 per cent in 2010 as the province began

to recover from the global recession. Indeed, demand

for new housing was being driven by improved gains

in employment that year, as well as stronger population

growth and low interest rates. Construction of both sin-

gle-detached and multiple-family housing contributed to

this increase. In level terms, total housing starts topped

Quebec

Housing Starts(000s)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database.

2010 11 12 13f 14f 15f 16f 17f0

20

40

60

Singles Multiples 20-year average

House Price Growth(percentage chage)

f = forecastSources: The Conference Board of Canada; CMHC Housing Time Series Database; Quebec Federation of Real Estate Boards.

2010 11 12 13f 14f 15f 16f 17f02468

10

New Resale

16 | metropolitan Housing Outlook—Autumn 2013

The Conference Board of Canada

51,000 units in 2010, their highest level since 2004.

However, in spite of the higher population growth,

at their 2010 level, starts were above demographic

requirements. As a result, inventories rose, and growth

in new home prices slowed, dropping to 2.4 per cent,

down from 2.9 per cent the previous year and an aver-

age of 5 per cent annually in the five years before that.

Quebec: Economic Indicators

2010 2011 2012 2013f 2014f 2015f 2016f 2017f

real GDP at market prices 295,398 300,275 303,322 307,656 314,389 322,277 328,842 334,565(2002 $ millions) 2.5 1.7 1.0 1.4 2.2 2.5 2.0 1.7

Total employment (000s) 3,918 3,955 3,985 4,042 4,085 4,144 4,191 4,2201.8 1.0 0.8 1.4 1.1 1.5 1.1 0.7

unemployment rate (per cent) 7.9 7.7 7.8 7.7 7.6 7.2 6.9 6.8

Personal income per capita ($) 33,518 34,828 35,921 36,486 37,449 38,548 39,591 40,5331.8 3.9 3.1 1.6 2.6 2.9 2.7 2.4

Population (000s) 7,895 7,968 8,043 8,109 8,173 8,236 8,299 8,3621.0 0.9 0.9 0.8 0.8 0.8 0.8 0.8

retail sales ($ millions) 99,551 102,505 103,648 105,551 109,222 113,052 116,600 119,8876.2 3.0 1.1 1.8 3.5 3.5 3.1 2.8

Inflation rate (per cent) 1.3 3.0 2.1 1.2 2.0 2.2 2.0 1.9

f = forecast Italics indicate percentage change.Sources: The Conference Board of Canada; Bank of Canada; Statistics Canada.

Quebec: Housing Indicators

2010 2011 2012 2013f 2014f 2015f 2016f 2017f

Housing starts 51,363 48,387 47,367 36,220 36,395 37,907 38,539 37,64518.3 –5.8 –2.1 –23.5 0.5 4.2 1.7 –2.3

Singles 19,549 16,554 16,059 13,796 13,940 14,355 14,568 13,71311.5 –15.3 –3.0 –14.1 1.0 3.0 1.5 –5.9

Multiples 31,814 31,833 31,308 22,424 22,456 23,552 23,971 23,93223.0 0.1 –1.6 –28.4 0.1 4.9 1.8 –0.2

Housing completions 45,798 44,526 44,564 42,758 37,309 36,899 38,291 38,1175.8 –2.8 0.1 –4.1 –12.7 –1.1 3.8 –0.5

Singles 18,738 15,779 15,847 14,228 13,639 13,548 13,962 13,52511.7 –15.8 0.4 –10.2 –4.1 –0.7 3.1 –3.1

Multiples 27,060 28,747 28,716 28,529 23,670 23,351 24,330 24,5922.1 6.2 –0.1 –0.7 –17.0 –1.3 4.2 1.1

average price of a new home ($) 293,728 299,580 304,180 308,506 314,380 321,452 328,636 335,6442.4 2.0 1.5 1.4 1.9 2.2 2.2 2.1

average price of a resale home ($) 249,591 261,411 272,014 274,868 282,264 290,069 297,039 304,1798.5 4.7 4.1 1.0 2.7 2.8 2.4 2.4

f = forecast Italics indicate percentage change.Sources: The Conference Board of Canada; CMHC Housing Time Series Database; Quebec Federation of Real Estate Boards; Statistics Canada.

Autumn 2013—metropolitan Housing Outlook | 17

The Conference Board of Canada

Higher inventories, a more modest economy, and

increased taxes all led builders to reduce housing starts

through 2011 and 2012. Starts fell 5.8 per cent in

2011 and another 2.1 per cent last year. Much of this

decrease was in the singles market, as multiple starts

were essentially flat in 2011 and declined just 1.6 per

cent in 2012. The multiples market was being boosted

by a number of condominium developments, especially

in Montréal and Québec City. Even with the lower

starts over the past two years, new home price growth

continued to decelerate, slipping to 1.5 per cent for

2012. Growth in resale prices was also slowing during

this time—falling from 8.5 per cent in 2010 to 4.1 per

cent last year—suggesting a weaker resale market

as well.

Builders reduced both single and multiple starts signifi-

cantly in the first quarter of 2013, as economic growth

remained modest and some condominium projects

wound down. The market was also being hampered by

tighter mortgage rules that were introduced last year.

Single starts slowed again in the second quarter of this

year, while multiples recorded a small increase. In all,

total housing starts are expected to decline 23.5 per cent

for 2013, down to 36,200 units, their lowest level since

2001. Price growth, in both the new and resale markets,

is forecast to remain modest in 2013, at 1.4 per cent and

1 per cent, respectively.

With housing starts now closer to demographic require-

ments, an improved economy and steady population

growth should bring builders back to the new home

market starting in 2014. Starts are expected to increase

0.5 per cent next year and 4.2 per cent in 2015. Price

growth is also anticipated to accelerate, albeit slowly,

in the coming years. New home prices are forecast to

grow by 1.9 per cent in 2014 and 2.2 per cent in 2015.

Resale price growth is expected to be just slightly

higher, at 2.7 per cent per year over the same two years.

18 | metropolitan Housing Outlook—Autumn 2013

The Conference Board of Canada

Ontario’s real gross domestic product will grow just 1.2 per cent in 2013, held back by weakness in both the public and private sectors. However,

growth in the economy is then expected to improve to 2.2 per cent next year. The province’s new home market is expected to see housing starts fall for the first time in four years this year as both single and multiple starts decline. With an improved economy next year, builders will slowly return to the new home market, increasing starts a modest 2.5 per cent for 2014.

eCONOMIC OuTlOOk

Broad-based weakness in demand from households,

government, and businesses (especially during late 2012

and early 2013) will result in real GDP growth of just

1.2 per cent for Ontario this year—the slowest pace

since the recession. This lacklustre pace of economic

growth, along with resulting slow employment growth,

is weighing on consumer spending, which is anticipated

to grow just 1.4 per cent for 2013. However, household

confidence (as measured by The Conference Board of

Canada’s Index of Consumer Confidence) has been

increasing recently, and this will translate into higher

spending on goods and services, especially durable

goods. As a result, real consumer spending is expected

to advance 2.7 per cent next year. Improving business

confidence and demand for exports should also help

overall economic growth pick up steam later this year

and into 2014. Accordingly, real GDP will expand

2.2 per cent next year.

HOuSING OuTlOOk

Ontario’s new home market has been robust for the

past three years. Indeed, stronger demand following the

2009 recession enticed builders to increase total hous-

ing starts an average of 15.1 per cent per year from

2010 to 2012. Demand was being boosted not only by

an improved economy but also by healthy population

gains and lower interest rates. In level terms, Ontario’s

housing starts reached 76,700 units in 2012, their

highest level since 2005. With stronger demand came

ontario

Housing Starts(000s)

f = forecastSources: The Conference Board of Canada; CMHC Housing TimeSeries Database.

2010 11 12 13f 14f 15f 16f 17f0

20406080

100

Singles Multiples 20-year average

House Price Growth(percentage chage)

f = forecastSources: The Conference Board of Canada; CMHC Housing TimeSeries Database; Canadian Real Estate Association.

2010 11 12 13f 14f 15f 16f 17f02468

10New Resale

Autumn 2013—metropolitan Housing Outlook | 19

The Conference Board of Canada

increased price growth as well—new home prices rose

an average of 3.8 per cent from 2010 to 2012, after

holding flat in 2009. Growth in resale home prices was

even larger during this time, at 6.7 per cent on an aver-

age annual basis.

The growth in housing starts in 2010 was split between

the singles and multiples markets. However, over

2011–12, all of the increase in starts was due to more

multiple-unit construction, as single-detached starts

declined each year. One of the biggest factors driving

Ontario: Economic Indicators

2010 2011 2012 2013f 2014f 2015f 2016f 2017f

real GDP at market prices 556,863 566,741 574,469 581,252 594,144 610,994 627,020 640,899(2002 $ millions) 3.5 1.8 1.4 1.2 2.2 2.8 2.6 2.2

Total employment (000s) 6,611 6,732 6,786 6,874 6,982 7,114 7,238 7,3301.6 1.8 0.8 1.3 1.6 1.9 1.7 1.3

unemployment rate (per cent) 8.6 7.8 7.9 7.7 7.6 6.6 6.1 5.9

Personal income per capita ($) 37,004 37,942 38,810 39,681 40,887 42,131 43,396 44,5652.7 2.5 2.3 2.2 3.0 3.0 3.0 2.7

Population (000s) 13,203 13,350 13,489 13,606 13,755 13,917 14,091 14,2701.2 1.1 1.0 0.9 1.1 1.2 1.2 1.3

retail sales ($ millions) 156,904 162,528 165,177 166,624 173,391 180,135 186,970 193,1915.4 3.6 1.6 0.9 4.1 3.9 3.8 3.3

Inflation rate (per cent) 2.4 3.1 1.4 1.3 2.0 2.1 2.0 2.0

f = forecast Italics indicate percentage change.Sources: The Conference Board of Canada; Bank of Canada; Statistics Canada.

Ontario: Housing Indicators

2010 2011 2012 2013f 2014f 2015f 2016f 2017f

Housing starts 60,433 67,821 76,742 60,326 61,805 70,458 81,339 86,98520.0 12.2 13.2 –21.4 2.5 14.0 15.4 6.9

Singles 28,089 26,884 25,567 23,282 23,630 26,691 30,789 32,07124.1 –4.3 –4.9 –8.9 1.5 13.0 15.4 4.2

Multiples 32,344 40,937 51,175 37,044 38,175 43,767 50,551 54,91316.6 26.6 25.0 –27.6 3.1 14.6 15.5 8.6

Housing completions 61,419 60,642 58,613 63,886 60,512 62,653 71,303 78,34011.2 –1.3 –3.3 9.0 –5.3 3.5 13.8 9.9

Singles 27,497 24,798 26,351 24,197 23,999 24,852 28,501 30,67011.0 –9.8 6.3 –8.2 –0.8 3.6 14.7 7.6

Multiples 33,922 35,844 32,261 39,688 36,513 37,801 42,802 47,67111.3 5.7 –10.0 23.0 –8.0 3.5 13.2 11.4

average price of a new home ($) 474,960 494,665 517,813 533,304 542,869 554,947 566,368 577,8432.5 4.1 4.7 3.0 1.8 2.2 2.1 2.0

average price of a resale home ($) 340,225 363,073 381,328 392,017 398,171 406,163 414,709 423,1688.3 6.7 5.0 2.8 1.6 2.0 2.1 2.0

f = forecast Italics indicate percentage change.Sources: The Conference Board of Canada; CMHC Housing Time Series Database; Canadian Real Estate Association; Statistics Canada.

20 | metropolitan Housing Outlook—Autumn 2013

The Conference Board of Canada

multiples construction in recent years has been the

influx of big high-rise condominiums, especially in

Toronto. Apartment condominium starts in Toronto

alone grew more than 70 per cent during 2010 and

2011, and by a further 42.8 per cent last year, to reach

a record 27,400 units in 2012. Province-wide, mul-

tiple starts were 67 per cent of the total starts built

last year, up from a share of 39 per cent just 10 years

ago. Apartment condominiums have become a more

attractive purchase for homeowners for several reasons,

not the least of which is their relative affordability

compared with single-detached homes. In addition,