m&g spin free guides to investing

TRANSCRIPT

££ £?? ? Depending on the level of risk you’re willing to take, equities could be right for you. This guide should help you think about how to invest and potentially grow your money.

What is an equity fund?Invest through a managed fund

and you won’t invest alone –

you’ll pool your money with other

investors to buy equities.

An experienced fund manager invests and manages on your behalf. An active manager aims to beat the returns from the stock market.

We are unable to give financial advice. If you are unsure about the suitability of your investment, speak to your financial adviser.

Issued by M&G Securities Limited which is authorised and regulated by the Financial Conduct Authority in the UK and provides investment products. The registered office is Laurence Pountney Hill, London EC4R 0HH. Registered in England No. 90776

FUND

A case for equities LOW HIGH

RISK

LOWHIGH

RETU RN

LOW HIGH

RISK

LOWHIGH

RETU RN

£ LOW HIGH

RISK

LOWHIGH

RETU RN

LOW HIGH

RISK

LOWHIGH

RETU RN

Will I receive an income?

Is my initial investment secure?

Will my investment grow?

Low, in line with interest rates.

Generally higher, stable income. Usually fixed.

Not guaranteed, dependent on the dividend and will

fluctuate.

Generally higher, can fluctuate but

should remain stable.

Up to £85,000 protected in

a bank or building society.

Not secure but generally safer than equities.

Not secure and may fluctuate sharply.

Not secure but generally safer than equities.

Low growth. You could lose money if the interest rate is less than inflation.

Some growth potential.

High growth potential.

Some growth potential.

Cash savings Bonds Equities Property

How do you make money from equities?

The value of stock market investments will fluctuate, which will cause share prices to fall as well as rise and you may not get back the original amount you invested. The level of any income earned will fluctuate.

What drives their value up or down?

More investors want to buy but fewer shareholders want to sell

VALUE INCREASES

More shareholders want to sell but fewer investors want to buy

VALUE DECREASES

Company factors

like business performance and industry

news

SHORT TERM LONG TERM

Profitabilityof the business, both

past and future forecasts

Economic factors

like exchange rates, interest

rates and inflation

External eventssuch as

terrorism, wars, political events,

natural disasters

What are

equities?What are

equities?

The investors become shareholders, partial owners of the company. They could receive a percentage share in its profits and may have the right to vote on how the company is run.

A company can raise money to invest or expand by splitting its ownership into shares (also known as equities) and selling them to investors.

Capital growthYou’ll make money if you sell your shares at a higher price than you bought them.

Income: receive dividendsThe company decides how much profit to pay

in dividends and how much to reinvest.

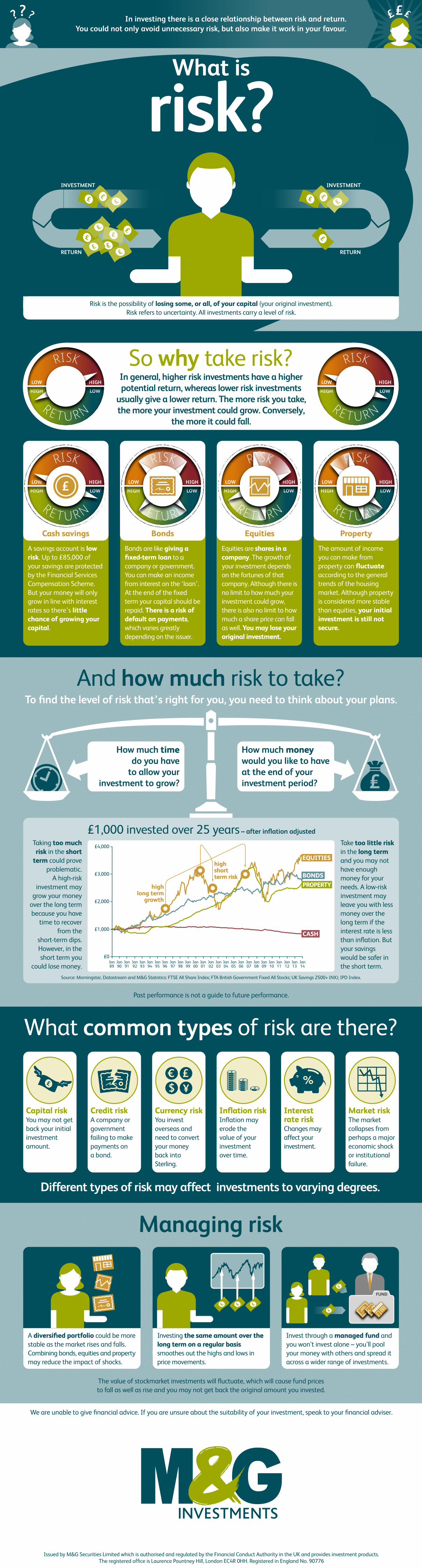

££ £?? ? In investing there is a close relationship between risk and return. You could not only avoid unnecessary risk, but also make it work in your favour.

Managing risk

A diversified portfolio could be more stable as the market rises and falls. Combining bonds, equities and property may reduce the impact of shocks.

Investing the same amount over the long term on a regular basis smoothes out the highs and lows in price movements.

Invest through a managed fund and you won’t invest alone – you’ll pool your money with others and spread it across a wider range of investments.

FUND

We are unable to give financial advice. If you are unsure about the suitability of your investment, speak to your financial adviser.

Issued by M&G Securities Limited which is authorised and regulated by the Financial Conduct Authority in the UK and provides investment products. The registered office is Laurence Pountney Hill, London EC4R 0HH. Registered in England No. 90776

What common types of risk are there?

Capital riskYou may not get back your initial investment amount.

Credit riskA company or government failing to make payments on a bond.

Currency riskYou invest overseas and need to convert your money back into Sterling.

Inflation riskInflation may erode the value of your investment over time.

Interest rate riskChanges may affect your investment.

Market riskThe market collapses from perhaps a major economic shock or institutional failure.

¥$£€ £

£

£

Different types of risk may affect investments to varying degrees.

£

Past performance is not a guide to future performance.

£4,000

£3,000

£2,000

£1,000

Jan90

Jan91

Jan92

Jan93

Jan89

Jan95

Jan96

Jan97

Jan98

Jan94

Jan00

Jan01

Jan02

Jan03

Jan99

Jan05

Jan06

Jan07

Jan08

Jan04

Jan10

Jan11

Jan12

Jan13

Jan14

Jan09

£0

EQUITIES

BONDS

CASH

PROPERTY

£1,000 invested over 25 years – after inflation adjusted

high long term

growth

high short term risk

Taking too much risk in the short

term could prove problematic.

A high-risk investment may

grow your money over the long term because you have

time to recover from the

short-term dips. However, in the short term you

could lose money.

Take too little risk in the long term and you may not have enough money for your needs. A low-risk investment may leave you with less money over the long term if the interest rate is less than inflation. But your savings would be safer in the short term.

Source: Morningstar, Datastream and M&G Statistics: FTSE All Share Index; FTA British Government Fixed All Stocks; UK Savings 2500+ (NX); IPD Index.

And how much risk to take?To find the level of risk that’s right for you, you need to think about your plans.

How much time do you have

to allow your investment to grow?

How much money would you like to have at the end of your investment period?

LOW HIGH

RISK

LOWHIGH

RETURN

LOW HIGH

RISK

LOWHIGH

RETURN

So why take risk?In general, higher risk investments have a higher potential return, whereas lower risk investments

usually give a lower return. The more risk you take, the more your investment could grow. Conversely,

the more it could fall.

Cash savings

LOW HIGH

RISK

LOWHIGH

RETURN

£

A savings account is low risk. Up to £85,000 of your savings are protected by the Financial Services Compensation Scheme. But your money will only grow in line with interest rates so there’s little chance of growing your capital.

Bonds are like giving a fixed-term loan to a company or government. You can make an income from interest on the ‘loan’. At the end of the fixed term your capital should be repaid. There is a risk of default on payments, which varies greatly depending on the issuer.

Equities are shares in a company. The growth of your investment depends on the fortunes of that company. Although there is no limit to how much your investment could grow, there is also no limit to how much a share price can fall as well. You may lose your original investment.

The amount of income you can make from property can fluctuate according to the general trends of the housing market. Although property is considered more stable than equities, your initial investment is still not secure.

LOW HIGH

RISK

LOWHIGH

RETURN

LOW HIGH

RISK

LOWHIGH

RETURN

LOW HIGH

RISK

LOWHIGH

RETURN

Bonds Equities Property

What is

risk?What is

risk?

Risk is the possibility of losing some, or all, of your capital (your original investment). Risk refers to uncertainty. All investments carry a level of risk.

INVESTMENT

RETURN

INVESTMENT

RETURN

The value of stockmarket investments will fluctuate, which will cause fund pricesto fall as well as rise and you may not get back the original amount you invested.

££ £?? ? Bonds can seem complicated but they might suit if you need a regular income. If you don’t know your coupon from your credit, this guide is designed for you.

We are unable to give financial advice. If you are unsure about the suitability of your investment, speak to your financial adviser.

Issued by M&G Securities Limited which is authorised and regulated by the Financial Conduct Authority in the UK and provides investment products. The registered office is Laurence Pountney Hill, London EC4R 0HH. Registered in England No. 90776

What are

bonds?What are

bonds?A bond is basically a loan. When you buy a bond, you lend money to the government or company that issued it.

You then typically receive regular interest payments (coupons). This is normally a fixed amount that is set when the bond is issued.

At the time when the loan is scheduled to end (the maturity), the amount you originally lent is paid back to you.

What is a bond fund?You can pool your

money with other investors to buy a

range of bonds, diversifying to

reduce exposure to any one

government or company.

An experienced fund manager invests and manages on your behalf. An active manager aims to outperform other similar bond funds.

FUND

The value of stockmarket investments will fluctuate, which will cause fund pricesto fall as well as rise and you may not get back the original amount you invested.

How do you make money from bonds?Capital return

If you buy a bond from anotherinvestor for less than its original cost...

...you could make a profit byholding it to maturity.

Income: couponsYou know exactly how much you’ll

receive and when, assuming the issuer doesn’t miss payments.

What drives their value up or down?

More investors want to buy but fewer bondholders want to sell

VALUE INCREASES

More bondholders want to sell but fewer investors want to buy

VALUE DECREASES

Interest ratesA rise in rates causes a fall in bond

prices, and vice versa. The interest on a bond is fixed at the start, so the bond doesn’t benefit from rising

rates, like savings do. The longer the maturity, the greater the impact.

Issuer outlookIf a bond issuer’s finances get worse, its credit rating – the measure of its ability to repay debt – may be downgraded. Its price may fall as investors decide that the interest doesn’t make up for

the increased risk of a missed payment.

InflationThings tend to get more expensive over the years. Because the interest

paid on a bond is fixed, the real value of that payment could be worth less

over time.

£

£

£

What are the different types of bonds?

Index-linkedThe value of payments is adjusted in line with inflation. This means

you will probably get more if inflation rises.

Investment gradeYou’re less likely to lose money on

these bonds, but you’ll probably get less interest as well.

Government bondsIssued by countries, normally to raise money for public spending. Different countries have different levels of risk.

Corporate bondsIssued by companies. They can offer higher interest payments as they are often seen as riskier than government bonds.

A case for bonds LOW HIGH

RISK

LOWHIGH

RETU RN

LOW HIGH

RISK

LOWHIGH

RETU RN

£ LOW HIGH

RISK

LOWHIGH

RETU RN

LOW HIGH

RISK

LOWHIGH

RETU RN

Will I receive an income?

Is my initial investment secure?

Will my investment grow?

Low, in line with interest rates.

Generally higher, stable income. Usually fixed.

Not guaranteed, dependent on the dividend and will

fluctuate.

Generally higher, can fluctuate but

should remain stable.

Up to £85,000 protected in

a bank or building society.

Not secure but generally safer than equities.

Not secure and may fluctuate sharply.

Not secure but generally safer than equities.

Low growth. You could lose money if the interest rate is less than inflation.

Some growth potential.

High growth potential.

Some growth potential.

Cash savings Bonds Equities Property

High yieldLower credit rating than

investment-grade.

££ £?? ? Commercial property investing has underlying bricks-and-mortar assets. These are buildings used by businesses such as offices, shopping centres and factories.

What is a property fund?An experienced fund manager

invests and manages your

money on your behalf, pooling it

with other investors.

Property funds buy buildings and manage them. This allows individuals to invest without the high costs of buying properties directly.FUND

We are unable to give financial advice. If you are unsure about the suitability of your investment, speak to your financial adviser.

Issued by M&G Securities Limited which is authorised and regulated by the Financial Conduct Authority in the UK and provides investment products. The registered office is Laurence Pountney Hill, London EC4R 0HH. Registered in England No. 90776

A case for property LOW HIGH

RISK

LOWHIGH

RETU RN

LOW HIGH

RISK

LOWHIGH

RETU RN

£ LOW HIGH

RISK

LOWHIGH

RETU RN

LOW HIGH

RISK

LOWHIGH

RETU RN

Will I receive an income?

Is my initial investment secure?

Will my investment grow?

Low, in line with interest rates.

Generally higher, stable income. Usually fixed.

Not guaranteed, dependent on the dividend and will

fluctuate.

Generally higher, can fluctuate but

should remain stable.

Up to £85,000 protected in

a bank or building society.

Not secure but generally safer than equities.

Not secure and may fluctuate sharply.

Not secure but generally safer than equities.

Low growth. You could lose money if the interest rate is less than inflation.

Some growth potential.

High growth potential.

Some growth potential.

Cash savings Bonds Equities Property

What drives its value up or down?

Supply and demand

The economy drives demand for space and this influences

rental rates.

Location and quality

Prime property attracts the highest

rents, but a building's status

can change.

TenantsIf a tenant can’t pay the rent, the

owner’s costs rise.

Vacancy rateThe percentage of units that are unoccupied and

therefore not making money.

LiquidityProperty can be

difficult to sell and its price may be

affected if it needs to be sold

quickly.

What is

commercialproperty?

What is

commercialproperty?

Shops, shopping centres and retail parks.

Office buildings as well as business parks.

Factories, distribution warehouses and industrial estates.

Retail property Office property Industrial property

There are three main types of commercial property – retail, office and industrial – plus a range of other buildings that fall outside these categories.

££

£

How do you make money from commercial property?

Income: rentCommercial property has the potential for capital growth, though this can only be achieved if the property is sold

and this may not happen very often.

Usually commercial leases last longer than residential ones, and commercial tenants are generally more reliable.

There is still a risk they won't pay.

Capital growth

The value of stockmarket investments will fluctuate, which will cause fund pricesto fall as well as rise and you may not get back the original amount you invested.

££ £?? ? When it comes to choosing where to invest, the option you go for is likely to depend on how you feel about risk and what you need from your investment.

A diversified portfolio could be more stable as the market rises and falls. Combining bonds, equities and property may reduce the impact of shocks.

Investing the same amount over the long term on a regular basis often smoothes out the highs and lows in price movements.

Invest through a managed fund and you’ll pool your money with others and spread it across a wider range of investments.

FUND

We are unable to give financial advice. If you are unsure about the suitability of your investment, speak to your financial adviser.

Issued by M&G Securities Limited which is authorised and regulated by the Financial Conduct Authority in the UK and provides investment products. The registered office is Laurence Pountney Hill, London EC4R 0HH. Registered in England No. 90776

Managing riskINVESTMENT

RETURN

INVESTMENT

RETURN

LOW HIGH

RISK

LOWHIGH

RETURN

LOW HIGH

RISK

LOWHIGH

RETURN

Risk is the possibility of losing some, or all, of your investment. Risk refers to uncertainty.

All investments carry a level of risk. In general, higher risk investments have a higher

potential return, whereas lower risk investments usually give a lower return. The more risk you take, the more

your investment could grow. Conversely, the more it could fall.

How commercial property works

Commercial property is investing in buildings used by businesses, such as offices, shopping centres and factories.

When you buy a property, your income is in the form of regular rent. Commercial leases tend to last a long time and commercial tenants are usually more reliable.

There is also the potential for capital growth when you eventually sell your property.

The investors become shareholders, partial owners of the company. They could receive a percentage share in its profits and may get to vote on how the company is run.

A company can raise money to invest or expand by splitting its ownership into shares (also known as equities) and selling them to investors.

How equities work

Capital growthYou’ll make money if you sell your shares

at a higher price than you bought them.

Income: receive dividendsThe company decides how much profit to pay

in dividends and how much to reinvest.

After buying a bond, you don’t have to hold onto it until the end date. Just as shares can be bought and sold on the stock market, so can bonds.

How bonds work

A bond is basically a loan. When you buy a bond, you lend money to the government or company that issued it and they pay you interest.

At the time when the loan is scheduled to end (the maturity), the amount you originally lent is paid back to you.

Where can you

invest?Where can you

invest?Cash

offers very little potential for growth or income.

However, it can be the most secure place for your money

as the Financial Services Compensation Scheme will pay compensation up to £85000 if your

bank or building society becomes insolvent.

Bonds may be appealing if you need a regular income or

are just looking for a lower-risk place to store

your savings that still has more growth potential

than cash.

Equities can be right for you if you are comfortable with the

idea that the potential for strong growth also comes

with the possibility for greater losses.

Property offers an attractive

combination of a regular income and some

potential for capital growth, particularly if you invest in a fund that buys

property directly.

£

The value of investments will fluctuate, which will cause prices to fall aswell as rise and you may not get back the original amount you invested.