micro captives: the insurance company you keepdallasbar.org/sites/default/files/micro-captives - the...

TRANSCRIPT

© 2015 Giordani, Swanger, Ripp & Phillips, LLP. This report has a been prepared for informational purposes only. It does not constitute an offer or solicitation for the purchase or sale by our firm to you or to any other person to acquire a life insurance product. The information contained herein has been obtained from sources believed to be reliable, but our firm cannot guarantee its accuracy or completeness.

1 0 0 C O N G R E S S A V E N U E , S U I T E 1 4 4 0 | A U S T I N , T E X A S 7 8 7 0 1

phone 5 1 2 . 7 6 7 . 7 1 0 0 | fax 5 1 2 . 7 6 7 . 7 1 0 1 | W W W . G S R P . C O M

Micro‐Captives: The Insurance Company You Keep

Dallas Bar Association April 4, 2016

Cindy L. Grossman

2M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

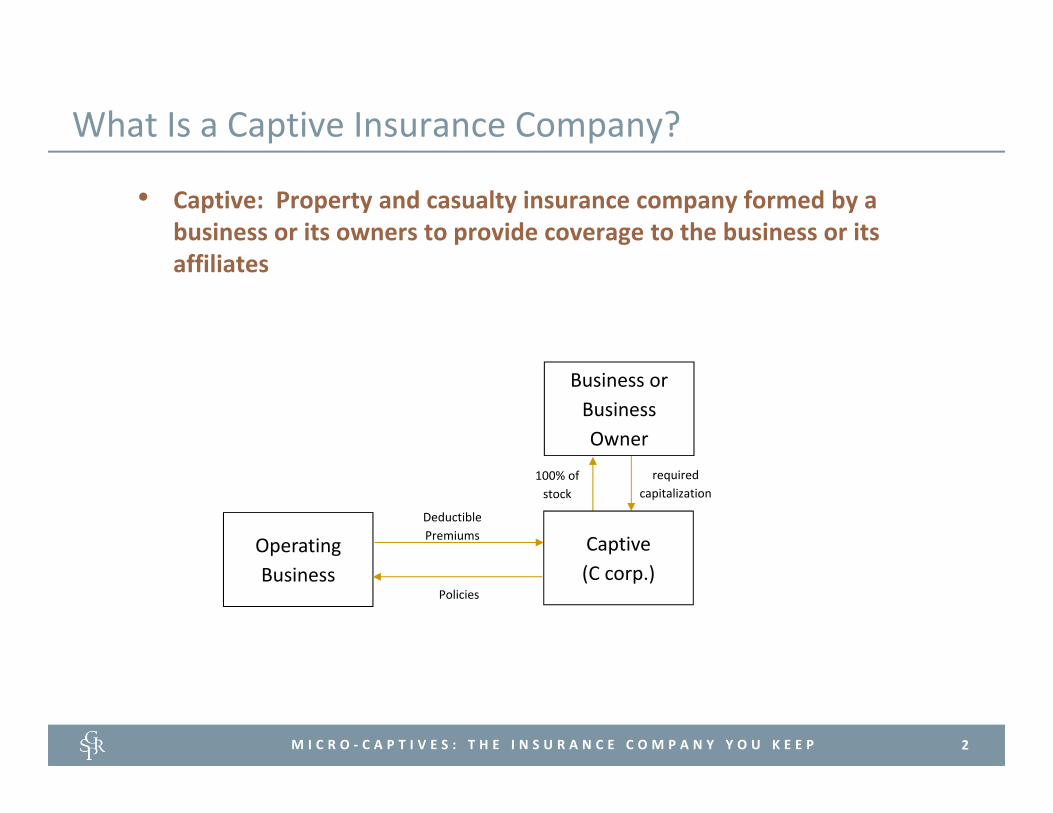

What Is a Captive Insurance Company?

Operating Business

Captive(C corp.)

Deductible Premiums

Policies

100% of stock

Business or Business Owner

requiredcapitalization

• Captive: Property and casualty insurance company formed by a business or its owners to provide coverage to the business or its affiliates

3M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

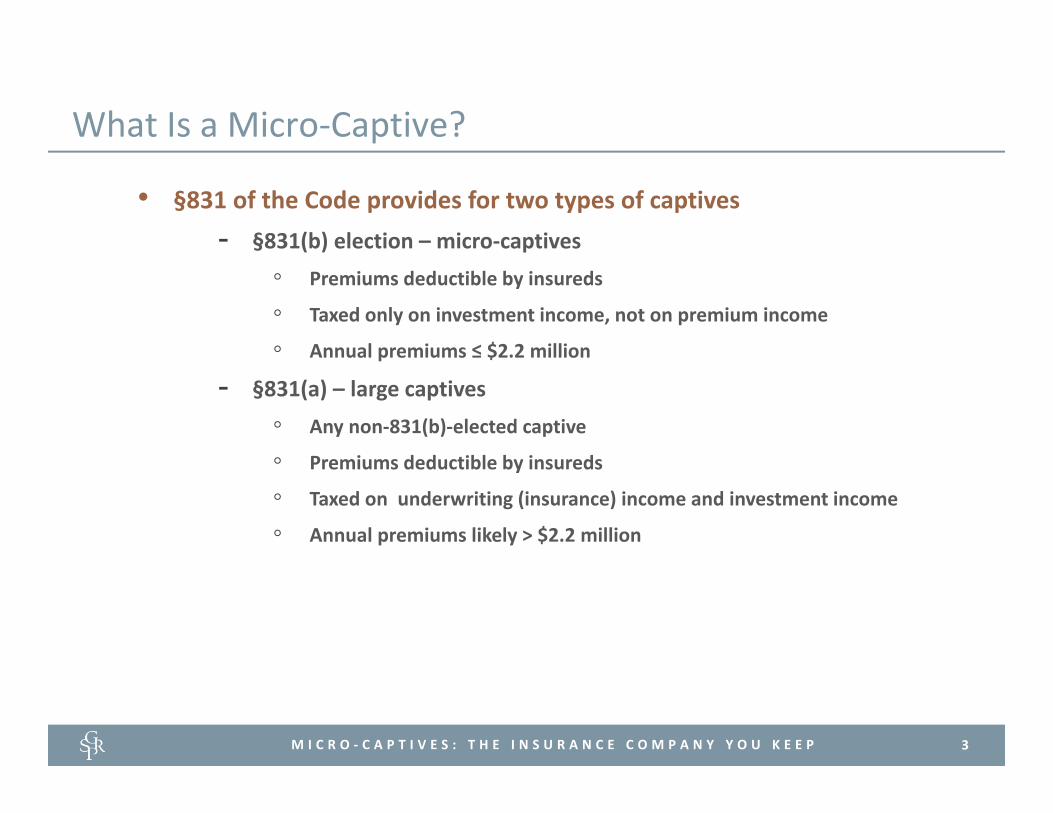

What Is a Micro‐Captive?

• §831 of the Code provides for two types of captives- §831(b) election – micro‐captives

◦ Premiums deductible by insureds

◦ Taxed only on investment income, not on premium income

◦ Annual premiums ≤ $2.2 million

- §831(a) – large captives◦ Any non‐831(b)‐elected captive

◦ Premiums deductible by insureds

◦ Taxed on underwriting (insurance) income and investment income

◦ Annual premiums likely > $2.2 million

4M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Why Should I Care?

• Heavily promoted to small and mid‐size business owners

• Why?

5M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Sample Captive EconomicsIncome Statement

Yr 0 Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 Underwriting revenueWritten Premium 1,000,000 1,000,000 1,000,000 1,000,000 1,000,000

Total Underwriting Revenue 1,000,000 1,000,000 1,000,000 1,000,000 1,000,000

Underwriting ExpenseRisk Pool Losses (15,300) (15,300) (15,300) (15,300) (15,300)Administration Expenses (64,100) (52,300) (52,300) (52,300) (52,300)Total Underwriting Expense (79,400) (67,600) (67,600) (67,600) (67,600)

Net Underwriting Profit 920,600 932,400 932,400 932,400 932,400

Investment Income 53,530 102,735 154,296 208,342 264,807

Federal Corporate Income Tax Estimate * (1,832) (3,917) (5,767) (11,455) (13,273)

Net Income 972,298 1,031,218 1,080,929 1,129,288 1,183,933

Opening Retained Earnings - 972,298 2,003,516 3,084,445 4,213,733 Closing Retained Earnings 972,298 2,003,516 3,084,445 4,213,733 5,397,666

Balance SheetYr 1 Yr 2 Yr 3 Yr 4 Yr 5

AssetsCash & Investments 150,000 1,122,298 2,153,516 3,234,445 4,363,733 5,547,666 Total Assets 150,000 1,122,298 2,153,516 3,234,445 4,363,733 5,547,666

LiabilitiesUnearned Premium - - - - -Total Liabilities - - - - - -

Capital and SurplusCapital Contribution 150,000 150,000 150,000 150,000 150,000 150,000 Retained Earnings - 972,298 2,003,516 3,084,445 4,213,733 5,397,666 Total Capital and Surplus 150,000 1,122,298 2,153,516 3,234,445 4,363,733 5,547,666

Total Liabilities, Capital and Surplus 150,000 1,122,298 2,153,516 3,234,445 4,363,733 5,547,666

* ASSUMES THE INVESTMENT PLAN IS MANAGED FOR C CORPORATION INCOME TAX EFFICIENCY.

6M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

What’s the Fuss About?

• February 2015: IRS “Dirty Dozen” List of Tax Scams- “Another abuse involving a legitimate tax structure…”

- “In the abusive structure, unscrupulous promoters persuade [businesses] to participate in this scheme…”

- Promoters create and sell “…poorly drafted ‘insurance’ binders and policies to cover ordinary business risks or esoteric, implausible risks for exorbitant ‘premiums,’ while maintaining economical commercial coverage…”

- “The promoters manage the entities’ captive insurance companies year after year for hefty fees, assisting taxpayers unsophisticated in insurance to continue the charade.”

7M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

What Are the Benefits?

• Benefits to the Business

• Tax Benefits

• Estate Planning Benefits

8M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Benefits to the Business

• Risk Management- Obtain coverages not commercially available

- Increase coverage amounts

• Cash Flow- Lower cost of coverage difficult to obtain

- Premiums stripped of brokerage, marketing expenses

- Access to less expensive reinsurance market

• Policy Design

• Control over claim processing timing

9M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Tax Benefits (of Micro‐Captive)

• Premiums paid by insured business are tax deductible

• Premiums received by captive are tax free

• Captive taxed (as C corp.) only on investment income

• Dividends paid to captive owner taxed at qualified dividend rates

10M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Estate Planning Benefits – Pre‐PATH Act

• Opportunity shifting

• Low capitalization with quick growth

IF no or low loss experience

• Be judicious with lifetime gift tax exclusion

11M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Estate Planning Benefits – Pre‐PATH Act (cont’d)

Operating Business

CaptivePremiums

Policies

Children’s Trust

100% of stock

Business Owner

$250,000*

$250,000capitalization

* At least required capital of captive

12M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Estate Planning Benefits – Pre‐PATH Act (cont’d)

Operating Business

CaptivePremiums

Policies

LLC

100% of stock

Business Owner

$127,500

$250,000capitalization

Children’s Trust

Business Owner

13M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Captive Insurance Companies Under the PATH Act• The PATH Act added Section 831(b)(2)(B)(ii), which eliminates the estate

planning advantages of captives as of January 1, 2017. Under PATH, a captive can make an 831(b) election only if it annually satisfies one of the following tests:

- Risk Diversification: No more than 20% of the insurer’s written premiums can come from a single policyholder. Related policyholders will be treated as a single policyholder for purposes of this section.

- Ownership Diversification: no spouse or descendant of a business owner, either directly or indirectly (e.g., through a trust or entity), own a percentage interest in the captive that exceeds by more than 2% their ownership interest in the underlying insured business or business assets.

• Consequence of no 831(b) election: premiums are taxable to the captive.

14M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Captive Insurance Companies under the PATH Act

Invalid 831(b) Captive Structure:

15M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

What’s Required to Obtain Tax Benefits?

• Form a corporation / protected cell / series (LLC) that is:- an insurance company

- providing insurance

- §831(b) election

16M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

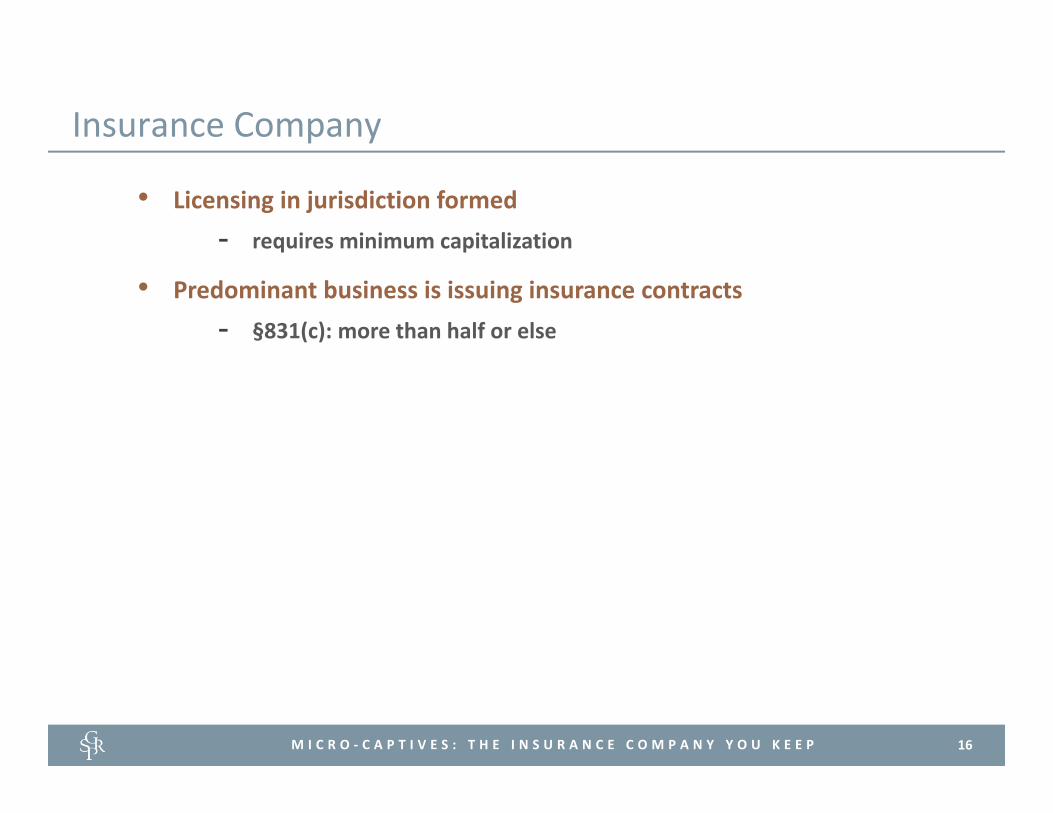

Insurance Company

• Licensing in jurisdiction formed- requires minimum capitalization

• Predominant business is issuing insurance contracts- §831(c): more than half or else

17M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Providing Insurance

• Arrangements must be “insurance” under federal tax law

• Criteria:- Insurance risk

- Insurance in commonly accepted sense

- Risk shifting and risk distribution

18M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Providing Insurance (cont’d)

• Insurance risk- Insured faces loss resulting from hazard and Insurer provides benefit

or performs act when loss materializes

- Not investment risk or business risk

19M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Providing Insurance (cont’d)

• Insurance in commonly accepted sense:- Insurer organized and operated as insurance company

- Company is regulated by jurisdiction’s insurance regulator

- Premiums negotiated at arms‐length

- Arrangement is valid and binding

- Arrangement between insured with insurable interest in insurable hazard or risk and insurer who accepts risk in exchange for premium

20M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Providing Insurance (cont’d)

• Risk Shifting- Risk is transferred from insured to insurer

- Not self‐insurance

• Risk Distribution- Risk is dispersed by insurer among a larger pool of policy holders

- Insurer reduces risk that single claim exceeds total premiums of all

21M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Providing Insurance (cont’d)

• Risk shifting / Risk distribution- Prior to 2001: Economic family doctrine

- Courts eschew economic family for balance sheet test

- Rev. Rul. 2001‐31: IRS withdraws economic family doctrine

- Revenue Rulings in 2002◦ 2002‐89: > 50% of premiums from unrelated policy holders

◦ 2002‐90: ≥ 12 operating entities acquire policies from captive

none < 5%, none > 15% of total risk

◦ 2002‐91: Diverse ownership of captive: none > 15% of ownership,

no owner’s risk > 15% total captive risk

• Avoid interrelated risks

22M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

§831(b) Election

• Annual premiums cannot exceed $2.2 million

• Timely election via statement attached to captive’s income tax return

• Effective until premiums > $2.2 million or revoked with IRS consent

• Premium aggregation for related captives- controlled group rules: > 50% common ownership

◦ parent ‐ subsidiary

◦ brother ‐ sister

◦ combined group

• Watch out for multiple captives

23M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Where Can I Do This?

• Domestic- Vermont is oldest

- Delaware, North Carolina, Utah typically micro‐captives

- Now Texas

• Foreign- Bermuda, Guernsey

- 953(d) election: domestic treatment; avoids excise tax on premiums

- Special Subpart F regime for non‐953(d) captives

• Factors- capitalization

- allowable risks

- operational requirements

- local professionals

- loans permitted?

24M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

How Does It Work?

• Policy Design- Layered Risk:

- First Dollar Quota Share:

- Hybrid:

Policy Limits80% above retained layer borne by pool(% pooled varies)

1st 20% of policy limit retained by captiveDeductible (insured)

Policy Limits49% of first dollar quota share retained by captive(% varies)

51% of first dollar quota share borne by pool(% varies)

Deductible (insured)

Policy Limitstop 20% of policy limit retained by

captive15 % quota

share retained by captive

85% of quota share borne by pool

Deductible (insured)

25M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

How Does It Work? (cont’d)

• Achieving risk shifting / risk distribution through pooling- Example 1: Premium paid directly to captive

Operating Business

Captive

Risk Pool

ReinsuranceAgreement

Premiums

Policies

RetrocessionAgreement

ReinsurancePremiums

RetrocessionPremiums

26M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

How Does It Work? (cont’d)

• Achieving risk shifting / risk distribution through pooling- Example 2: Premium paid directly to risk pool

Operating Business

Risk Pool

Captive

ReinsuranceAgreement

Premiums

Policies

ReinsurancePremiums

27M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

Who’s a Good Candidate?

• Risks that are different or expensive to insure

• At least $300,000 in premiums, in light of expenses:- Startup: $60,000 to $100,000

- Annual: $50,000 to $60,000 – captive management, audit, accounting, legal

• Sufficient cash flows from business operations

28M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

How Do I Stay Out of Hot Water?• Lack of Business Purpose

- Tax motivation, marketing

- Wealth Transfer / Assignment of Income

- Avoid parental indemnification

• Capitalization and Excess Accumulated Earnings- Meet jurisdictional and actuarial requirements

- Avoid loans from captive

• Management and Operational Formalities- Employ a quality captive manager

29M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

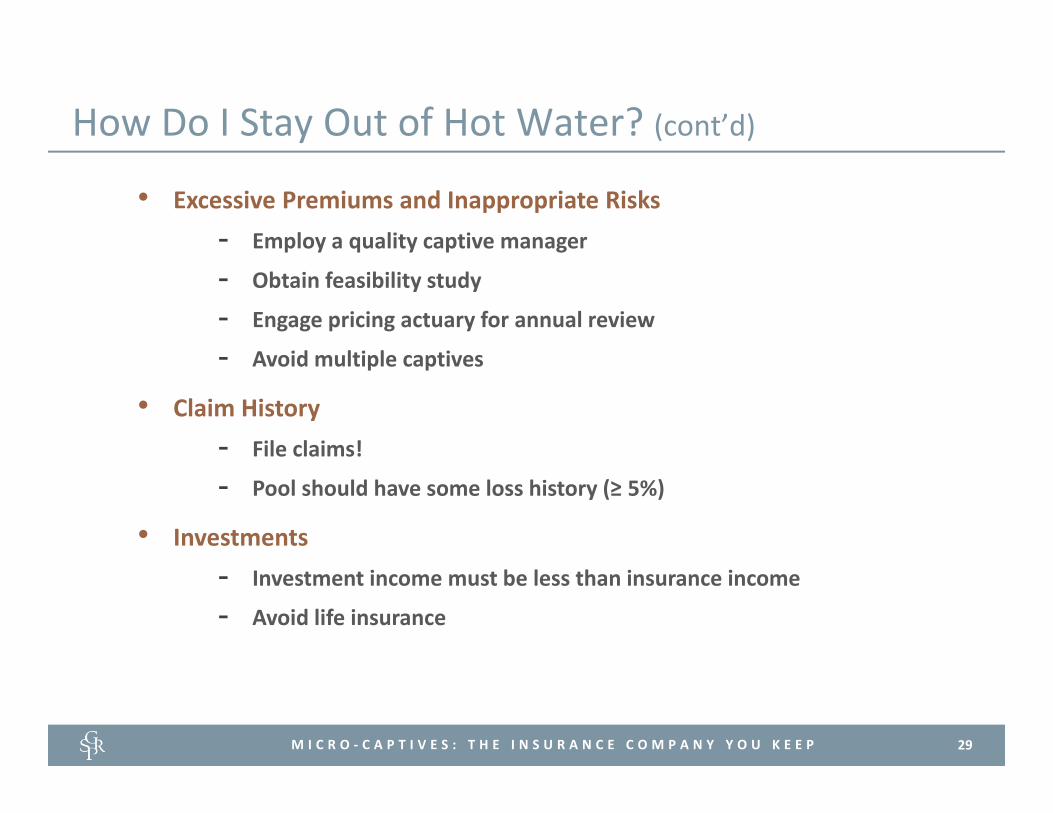

How Do I Stay Out of Hot Water? (cont’d)

• Excessive Premiums and Inappropriate Risks- Employ a quality captive manager

- Obtain feasibility study

- Engage pricing actuary for annual review

- Avoid multiple captives

• Claim History- File claims!

- Pool should have some loss history (≥ 5%)

• Investments- Investment income must be less than insurance income

- Avoid life insurance

30M I C R O ‐ C A P T I V E S : T H E I N S U R A N C E C O M P A N Y Y O U K E E P

And What Happens If It Blows Up?

• Loss of deductions for premiums- Amendment of returns for all entities and their owners

- Increased taxes and interest

- Accuracy‐related (20%) or even nondisclosed noneconomic

substance (40%) penalties

• Pool‐related risks- Loss of participants can eliminate risk distribution

- Pool invalidation effects all

• Possible taxation of “premium” payments

• State taxes and impact on licensing

1 0 0 C O N G R E S S A V E N U E , S U I T E 1 4 4 0 | A U S T I N , T E X A S 7 8 7 0 1

phone 5 1 2 . 7 6 7 . 7 1 0 0 | fax 5 1 2 . 7 6 7 . 7 1 0 1 | W W W . G S R P . C O M

Micro‐Captives: The Insurance Company You Keep