micro insurance in malawi supply side - inclusive business …€¦ · background •rate of...

TRANSCRIPT

Micro Insurance in Malawi Supply Side

1

Background

• Population of Malawi – 16 million (July 2012 est.)

• Levels of Employment – 97% of the population (This figure includes those involved in

subsistence farming)

3

Background

• Rate of Urbanisation – urban population: 20% of total population (2010)

• Lives Covered Under Health Insurance – Less than 500,000 lives (Data includes figures from both

open and closed schemes)

4

Background

• Out of Pocket Medical Expenditure – Private sector health care financing accounts for 27 percent

of the total health expenditure

– Out of Pocket expenditure averages 34% of the private health expenditure (or 12% of total health expenditure).

– At what price will Malawian households be willing to convert their out-of-pocket health expenditures into pre-paid health expenditure?

– Considering that 97% were willing to pay for health insurance. (Winford Masanjala & Innocent Phiri)

5

What is MASM’s Thinking Towards The Selling of

Insurance To The Informal Economy?

• MASM’S position toward the informal economy -

• The Informal Economic sector poses great potential for growth.

• MASM is greatly interested in tapping into this potential, hence the development of Mlimi Umoyo products.

6

Challenges Faced

• Lack of healthcare facilities in rural areas (distribution channels).

• Challenges in accessing payment channels.

• Lack of appreciation for health insurance.

• The handout syndrome.

• Lack of civic education on insurance products.

• Product development (pricing).

7

Attempts to Collaborate With Other

Players

• Worked with AHL to introduce Mlimi Umoyo.

• Unsuccessfully tried to introduce a product with OIBM.

• Are currently in talks with TNM.

8

Possible Partnerships

• Micro finance institutions – marketing & payment solutions.

• The government – infrastructure development i.e. roads, electricity, water, Civic education.

• The Private sector - infrastructure development i.e. private clinics in rural areas, Civic education.

• Telecommunications & Banking industry – payment solutions.

9

Thank you!

10

Index Based Weather Index

Insurance in Malawi

Supply Side Issues

11

Daise Kachingwe,

Presentation Outline

1. Objective of presentation

2. Background

3. Policy framework

4. Programme implementation

5. Lessons

6. Conclusion

12

Objective of presentation

To share supply side experiences in

implementing index based weather insurance.

13

STATISTICS on selected Socio-Economic indicators

• Agriculture contributes 37.8 % to GDP

• Forex - (90%)

• 85% of the population live in rural and agriculture is their main livelihood

• Access to credit < 5%

• 19% of the population is Banked (FINSCOPE 2008)

• About 3% of the population is insured.

14

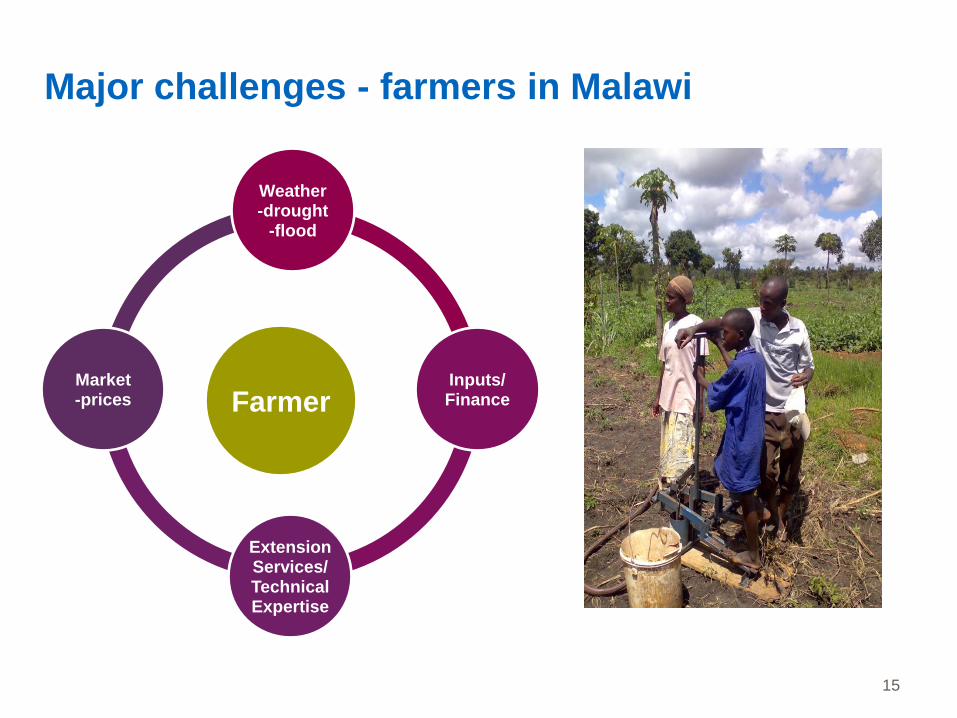

Major challenges - farmers in Malawi

Farmer

Weather -drought

-flood

Inputs/ Finance

Extension Services/ Technical Expertise

Market -prices

15

Weather Related Risks

• Weather is one of the biggest peril

• Weather risk has the most significant impact on the incomes of agricultural producers

• Weather related risks negatively impact individual house holds and local economy

16

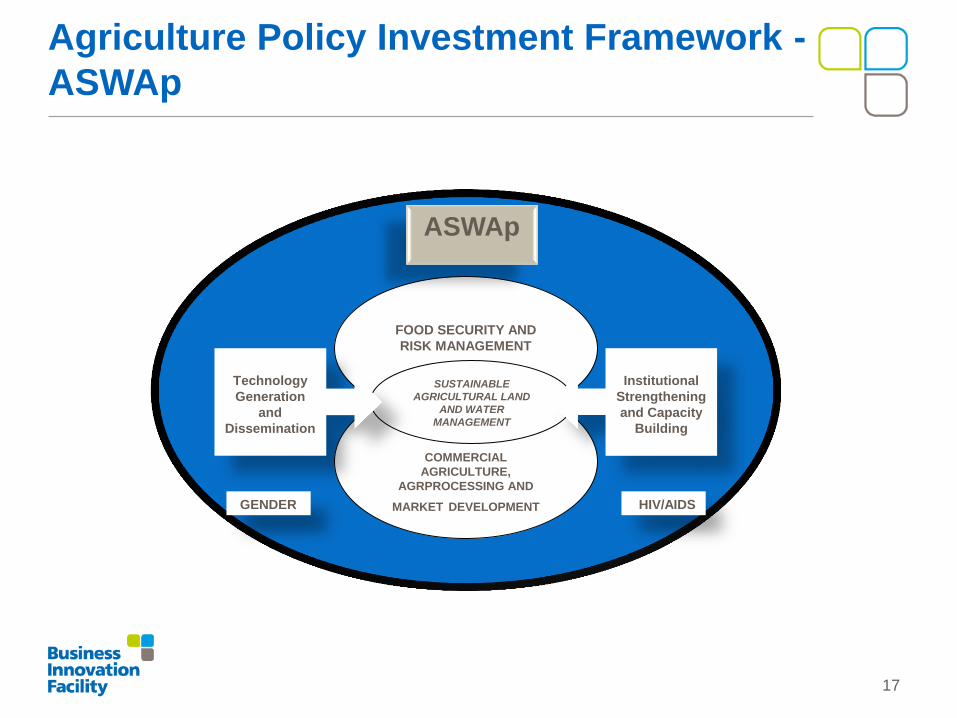

Agriculture Policy Investment Framework -

ASWAp

FOOD SECURITY AND

RISK MANAGEMENT

COMMERCIAL

AGRICULTURE,

AGRPROCESSING AND

MARKET DEVELOPMENT

SUSTAINABLE

AGRICULTURAL LAND

AND WATER

MANAGEMENT

Institutional

Strengthening

and Capacity

Building

Technology

Generation

and

Dissemination

ASWAp

HIV/AIDS GENDER

17

Weather index Insurance: Pilot Program

• Started in 2005 with World Bank support.

• Participating institutions were NASFAM, MRFC, Insurance Association of Malawi.

• Started with groundnuts later included tobacco.

• Insurance sold as a package with a loan.

• Up to 4,500 farmers have benefited from the program.

• OIBM and MRFC provided loans to farmers for purchase of higher-yielding seed if the farmers bought weather insurance as part of the loan package.

• Farmers were compelled to form farmer clubs and the loans were given to the clubs.

• These loans stipulated that the bank will be the first beneficiary if there is a payout from the insurance.

18

Weather Index Insurance: Pilot Program

• If there was a payout from the insurance company in the event of a drought, this would go directly to the bank (OIBM, MRFC) to pay down the farmers’ loan liability.

• Conversely, if there was no drought, farmers would pay the loan in full to the bank.

19

Supply Side Actors

• Government

– Central Bank

– Justice

– Meteorology Dept etc

• Financial Institutions

– Insurance Companies

– Banks

• Development Partners

20

Supply Side Issues

Infrastructure Issue

• The distribution of the weather stations is not strategic to credit demand

• Limited number of automated weather stations limiting the amount of loans available for farmers

21

Supply Side Issues

Capacity Issue

Lack of local expertise to design and price the contracts

Statistics

Lack of complete historical weather data limiting the expansion of the program

Institutional Issues

Regulatory Issues

22

Lessons

• The country has the required institutions to run a weather risk insurance program. However the roles and functions of each of player in such a program must be clearly spelt out and followed.

• Farmers that participated liked the scheme,. The main attraction to the program was that it facilitated the access to farm inputs loans.

• More capacity building for both farmers and field staff engaged in implementation of such a project is required, that way they can understand the objectives and general management of the program.

• The program has worked well with organized marketing system i.e. Groundnuts; NASFAM, Tobacco ; Auction Market. The output market should be clearly identified before the start of the program

23

Challenges

• Disparate rainfall patterns (differences in micro climatic conditions)

• No proper demarcation for the insurance program areas included (working on estimated radius of weather station)

• High premiums

24

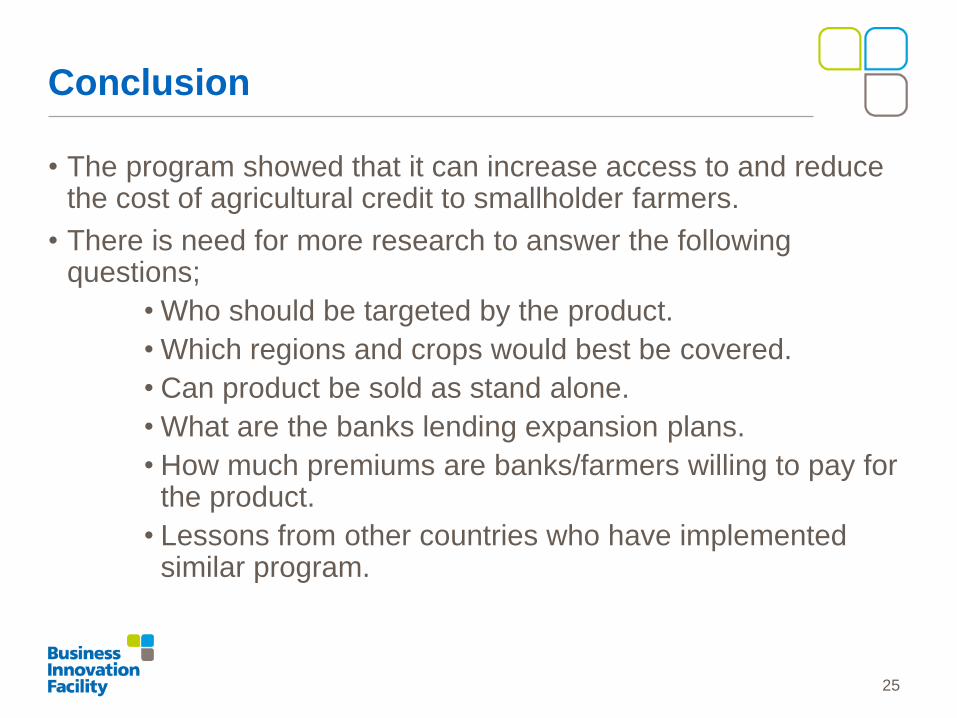

Conclusion

• The program showed that it can increase access to and reduce the cost of agricultural credit to smallholder farmers.

• There is need for more research to answer the following questions;

• Who should be targeted by the product.

• Which regions and crops would best be covered.

• Can product be sold as stand alone.

• What are the banks lending expansion plans.

• How much premiums are banks/farmers willing to pay for the product.

• Lessons from other countries who have implemented similar program.

25

Thank you!

26