microeconomics 3070 prof. barham lecture 1: introduction

TRANSCRIPT

Microeconomics 3070 Prof. Barham

Lecture 1: Introduction

Syllabus and Website

Website: http://www.colorado.edu/ibs/hb/barham/courses/econ3070/

All assignments and solution keys will be posted on the web site.

I will send you a notice when they are posted. Syllabus

Outline

Cover chapter 1 What is microeconomics

Economic models Tools for microeconomics

Constrained optimization Marginal analysis Equilibrium analysis Comparative statics

Next class are going over calculus, may start Chapter 2

What is mircoeconomics

Can you buy all the clothing, vacations, sport equipment, health care, food, beauty products, yoga classes, seasons tickets to sport event, donations to charity you want?

No

Mircoeconomics models our decision making process on how much you decide to spent on what.

What is mircoeconomics

Official Definitions: Microeconomics is the study of how individuals and

firms make themselves as well off as possible in a world of scarcity and the consequences of those individual decisions on the markets and the entire economy.

Microeconomics is the study of the allocation of scarce resources.

Mircoeconomics is also often called price theory. This is to emphasize the important role that price plays. Price not only thing studied – think of health care market

What is mircoeconomics

Because we can’t have everything, we need to make trade-offs and microeconomics helps us make those tradeoffs.

A society faces 3 key tradeoffs:1. Which goods and services to produce2. How to produce them

• How much labor and inputs should a firm use to produce a car

3. Who gets the good and services (allocation)

What is microeconomics

Workers need to choose how to allocate their time between labor and leisure.

Firms need to choose how to allocate their investment between human capital and machines.

Households need to choose how to allocate their incomes between savings and expenditure.

Micro versus MacroeconomicsWhat is the difference between micro and macro

economics?

Microeconomics: behavior of individual economic units like consumers, producers, landowners, families, etc. How and why do they make the decisions they make?

Macroeconomics: analyzes how the entire national economy performs. It analyzes unemployment, inflation, price levels, interest rates (many things we take as given in microeconomics).

Economic Models

How do economists allocate resources?

They develop theoretical model.

“Everything should be made a simple as possible but not simpler” Albert Einstein

Economic Models

The models are abstractions of the real world Too complicated to take into consideration all factors Without simplifications we would not be able to make

predictions. Like a roadmap, does not give each house, but the bare

essentials i.e. major streets, highways and sometime main attractions.

It may appear that the model makes heroic abstractions (assumptions) from the complexities of the real world.

Economic Models Example

Determinants of Poster Demand on CampusYou are advertising a big event for the freshman class how

many posters will you need? Factors in your model:

Price to make poster, size of freshman class Factors not in your model:

Content of poster, placement of poster, relative size of poster Are there any constraints to this model?

the amount of budget you have to spend on poster advertising.

Types of Variables in a Model

Exogenous Variable: one whose value is taken as given in a model.

Endogenous Variable: one whose value is determined within the model being studied

Which factor(s) would have you taken as given in the poster example? Price, size of freshman class (exogenous)

Which factor(s) are determined by your model? The quantity of posters needed (or demanded)

Tools of Microeconomic Analysis

1. Constrained Maximization

2. Equilibrium Analysis

3. Comparative Statics

Constrained Optimization

Constrained optimization: an analytical tool used when a decision maker seeks to make the best (optimal) choice, taking into consideration possible restrictions on the choice.

Constrained Optimization

This tool has two parts:

1. Objective function: is the relationship the decision maker seeks to optimize (maximize or minimize).

2. Constraint: limits or restrictions that are imposed on the decision maker

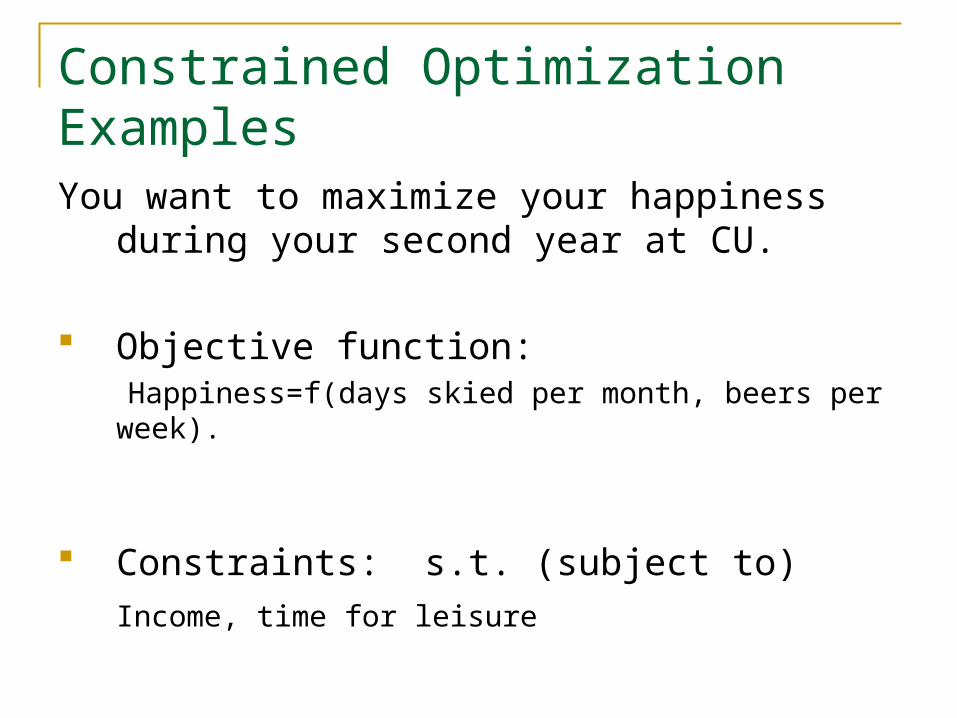

Constrained OptimizationExamplesYou want to maximize your happiness during

your second year at CU.

Objective function: Happiness=f(days skied per month, beers per week).

Constraints: s.t. (subject to)

Income, time for leisure

Marginal Analysis

Solution to a constrained optimization problem depends on the marginal impact of the decision variables on the value of the objective function.

But what is marginal?

The term marginal tells us how the value of the objective function changes as a result of adding one unit of a decision variable.

Marginal Analysis

Happiness

$ spent

From beer

From skiing

0 0 0

25 80 4

50 90 10

75 92 15

100 94 20

Marginal Happiness

From beer

From skiing

80 4

10 6

2 5

2 5

How much do you spend on beer and skiing to Maximize your happiness if you have 100 budget?

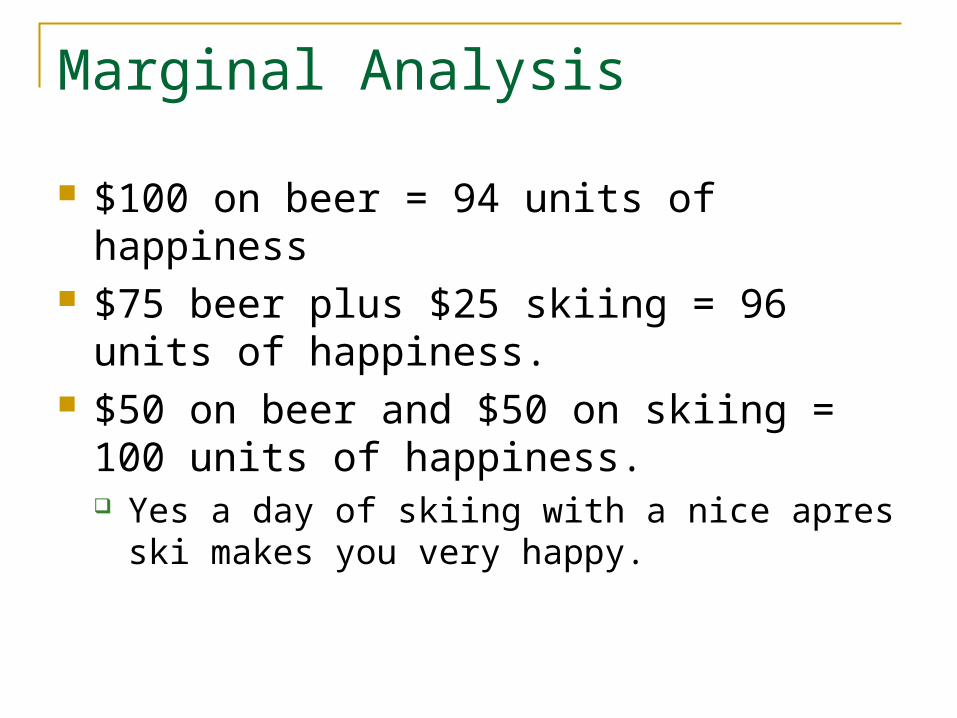

Marginal Analysis

$100 on beer = 94 units of happiness $75 beer plus $25 skiing = 96 units of

happiness. $50 on beer and $50 on skiing = 100 units of

happiness. Yes a day of skiing with a nice apres ski makes

you very happy.

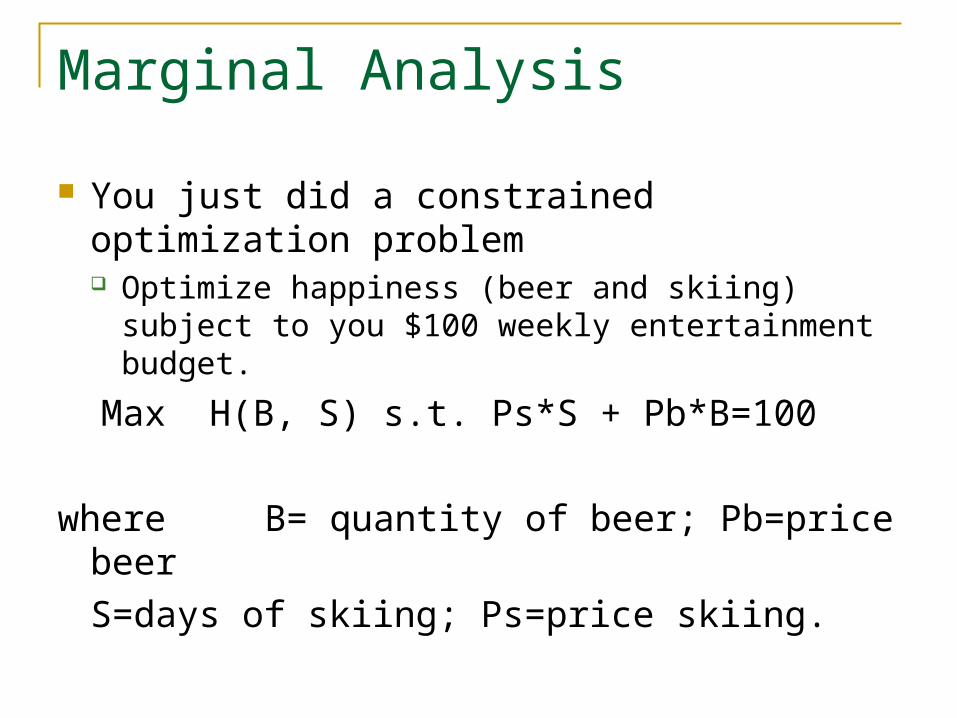

Marginal Analysis

You just did a constrained optimization problem Optimize happiness (beer and skiing) subject to

you $100 weekly entertainment budget.

Max H(B, S) s.t. Ps*S + Pb*B=100

where B= quantity of beer; Pb=price beer

S=days of skiing; Ps=price skiing.

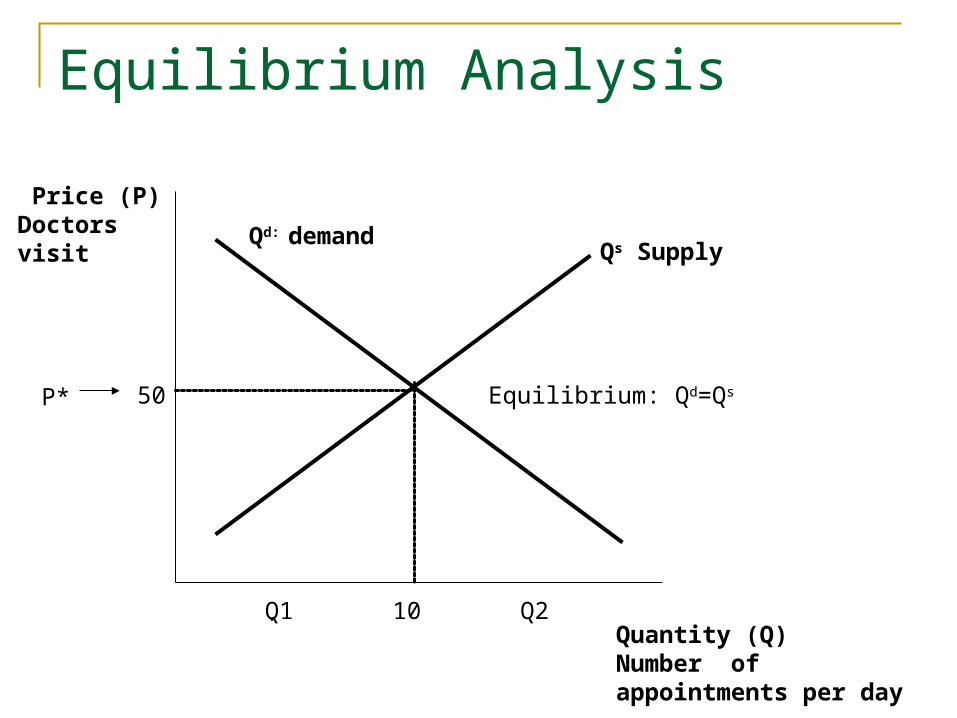

Equilibrium Analysis

Price (P) Doctors visit

Quantity (Q)Number of appointments per day

. 10

P*

Qd: demandQs Supply

Equilibrium: Qd=Qs50

Q1 Q2

Equilibrium Analysis

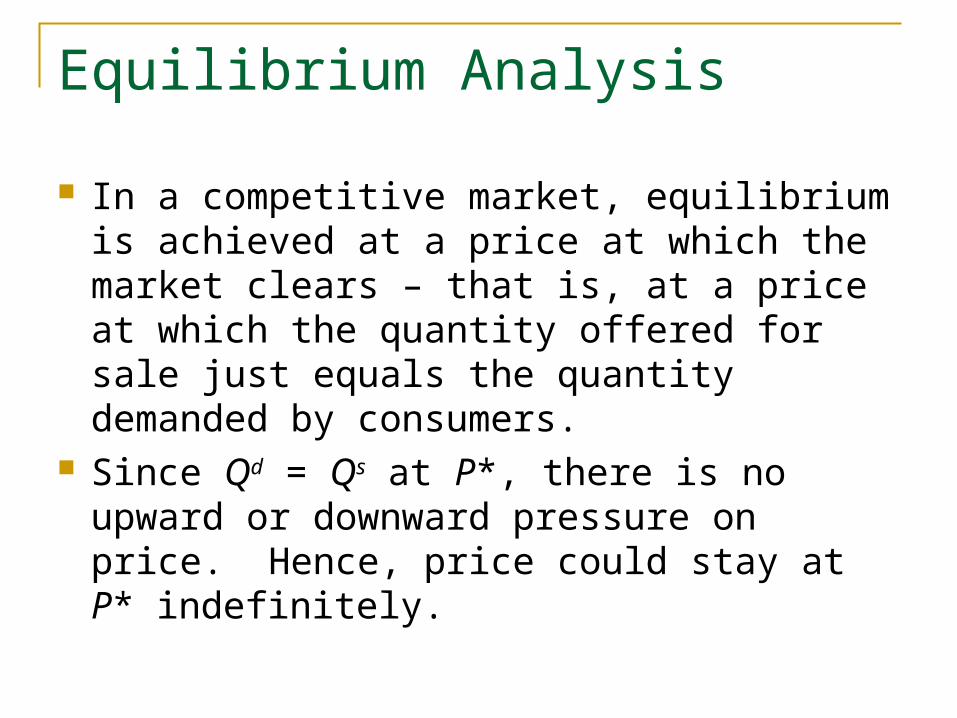

In a competitive market, equilibrium is achieved at a price at which the market clears – that is, at a price at which the quantity offered for sale just equals the quantity demanded by consumers.

Since Qd = Qs at P*, there is no upward or downward pressure on price. Hence, price could stay at P* indefinitely.

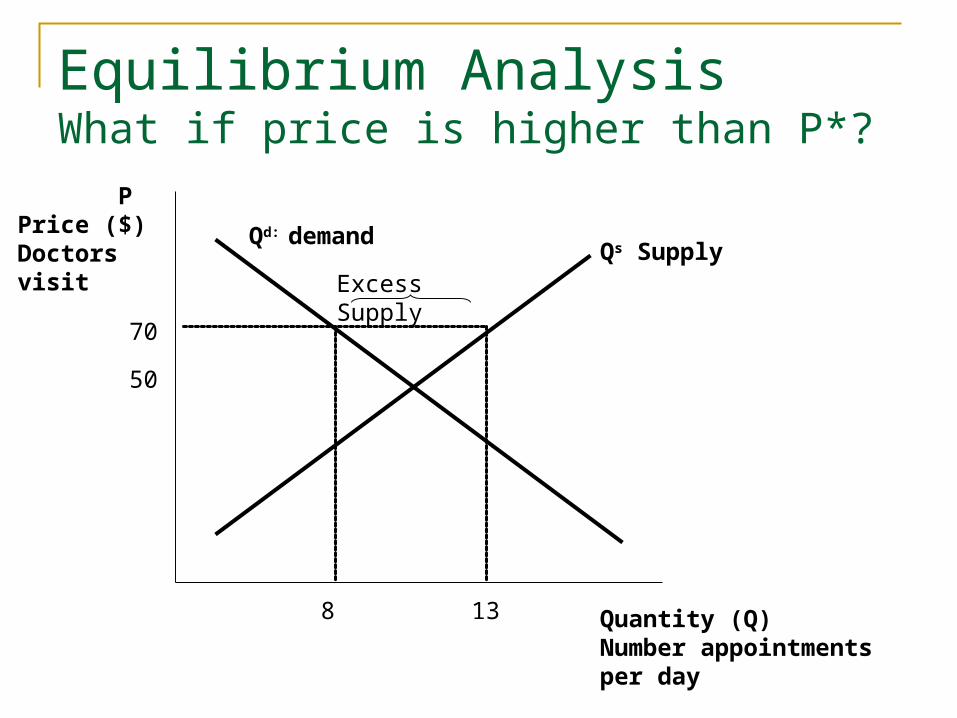

Equilibrium AnalysisWhat if price is higher than P*?

50

8

Qd: demandQs Supply

13

70

Excess Supply

Quantity (Q)Number appointments per day

PPrice ($) Doctors visit

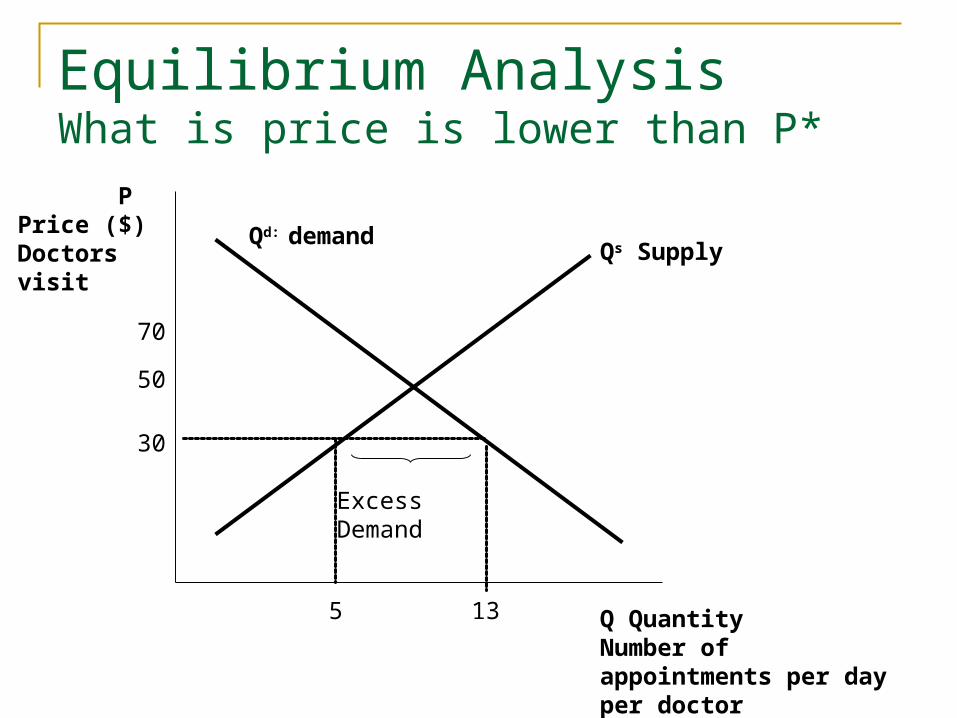

Equilibrium AnalysisWhat is price is lower than P*

50

5

Qd: demandQs Supply

13

70

Excess Demand

30

PPrice ($) Doctors visit

Q Quantity Number of appointments per day per doctor

Comparative Statics

Examine how a change in an exogenous variable will affect the level of an endogenous variable.

First, look at the value of the endogenous variable at the initial level of the exogenous variable

Second, look at the value of the endogenous variable at the new level of the exogenous variable.

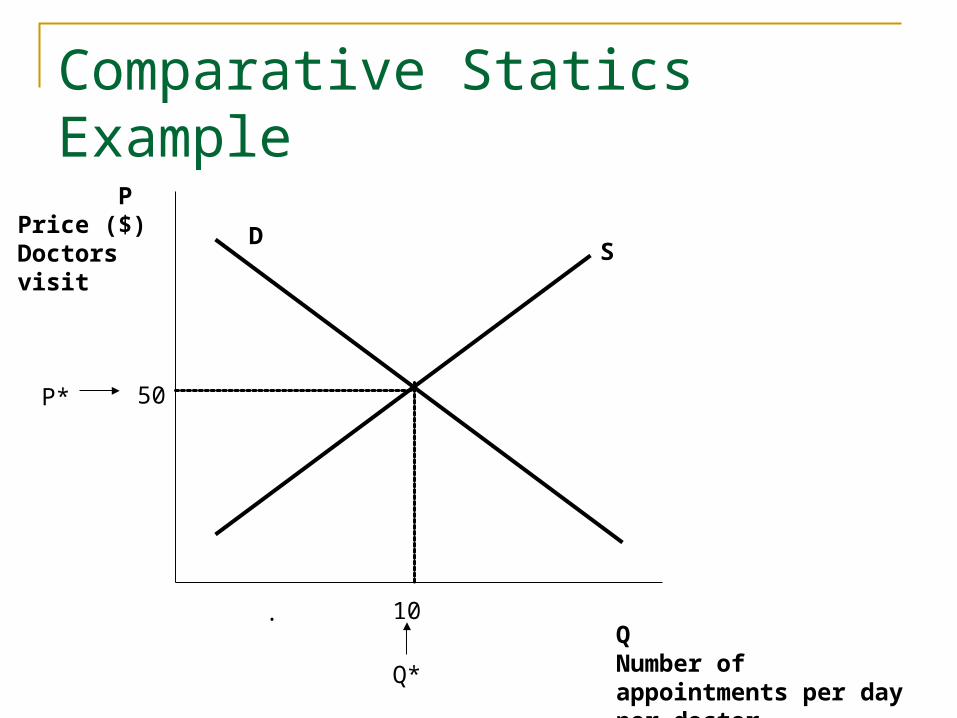

Comparative Statics Example

PPrice ($) Doctors visit

QNumber of appointments per day per doctor

. 10

P*

DS

50

Q*

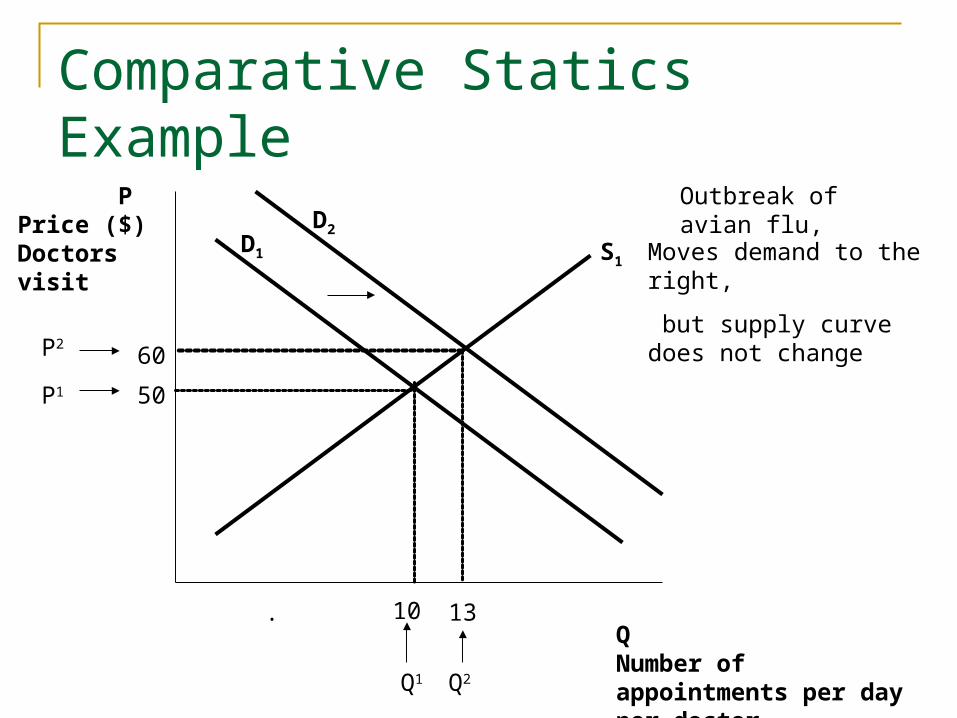

Comparative Statics Example

Suppose we are in China and there is an outburst of the Avian Flu. A few weeks later there are some new regulations put on doctors and they are unhappy about it. So they do a rotating strike.

How will these factors affect our Supply and Demand curve and the price?

Comparative Statics Example

PPrice ($) Doctors visit

QNumber of appointments per day per doctor

. 10

P1

D1 S1

50

D2

Outbreak of avian flu,

P260

13

Q1 Q2

Moves demand to the right,

but supply curve does not change

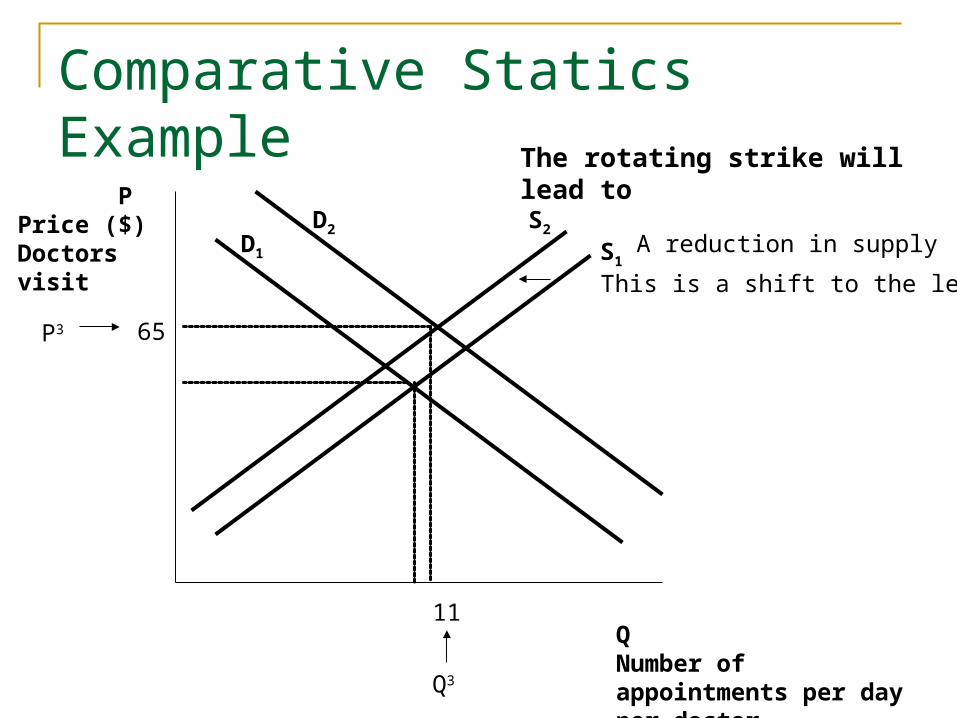

Comparative Statics Example

PPrice ($) Doctors visit

QNumber of appointments per day per doctor

D1 S1

D2

The rotating strike will lead to

P3 65

11

S2A reduction in supply

This is a shift to the left

Q3