microinsurance in colombia: lessons and...

TRANSCRIPT

MICROINSURANCE IN COLOMBIA:Lessons and Challenges

FPD WEEK 2010

Washington D.C March 4 - 2010

1/37

1. Low Income Markets Vs. Traditional Insurance Markets

2. Development of Microinsurance Market in Colombia

3. Distribution Channels

4. Microinsurance for Familias en Acción and Red Juntos

Content

2/37

Low Income Markets Vs. Traditional Insurance Markets

Different Client Product and Distribution Characteristics

3/37

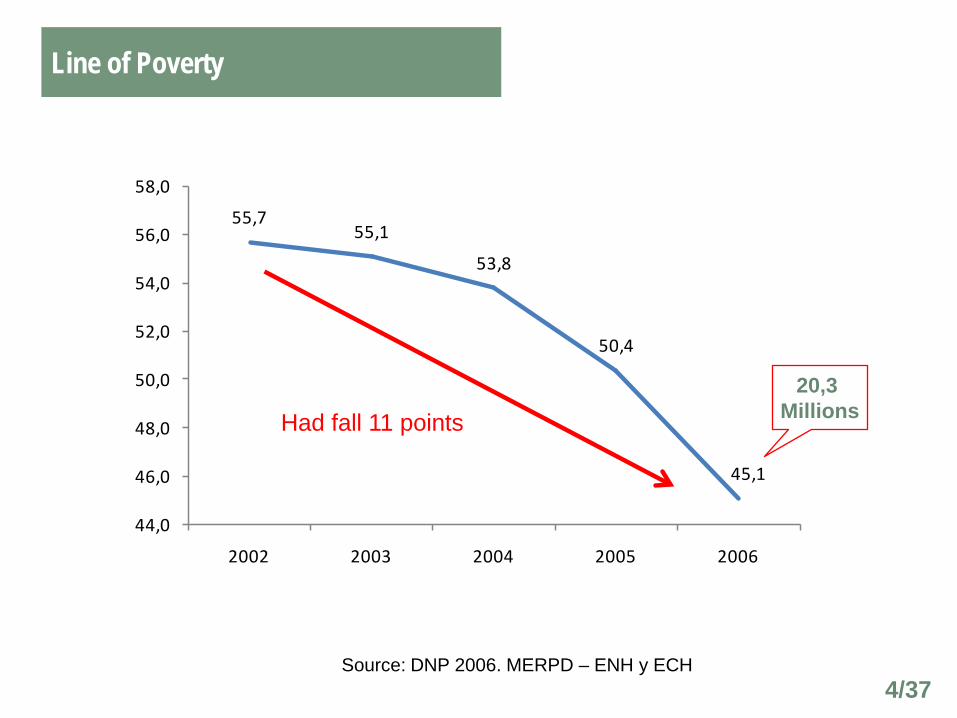

Line of Poverty

Source: DNP 2006. MERPD – ENH y ECH

55,755,1

53,8

50,4

45,1

44,0

46,0

48,0

50,0

52,0

54,0

56,0

58,0

2002 2003 2004 2005 2006

Had fall 11 points20,3

Millions

4/37

21,6

18,8 19,0

15,4

12,012,0

14,0

16,0

18,0

20,0

22,0

24,0

2002 2003 2004 2005 2006

Line of Extreme Poverty

Had fall 10 points5,4

Millions

Source: DNP 2006. MERPD – ENH y ECH5/37

Source: Living Standards Measurement Study Survey, 2003

The Poor Are More Vulnerable to Risks

1 1

1

22

2

3 3

3

44

4

5

5

5

0%

5%

10%

15%

20%

25%

30%

35%

Any serious illness or disease Head of household unemployed

Natural Disasters

1 2 3 4 5Income Quintile

6/37

PERVERSE INFORMAL AND FORMAL

Source: Living Standards Measurement Study Survey, 2003

The Poor Adopt Perverse Strategies to Cover Losses

7/37

11

1

1

1

2 2

2

2

2

33

3

3

3

4 4

4

4

45

5

5

5

5

0%

5%

10%

15%

20%

25%

30%

Food expenses were reduced

Clothing expenses were reduced

Take Their Children Out of the School

Incurred debts Savings were spent

1 2 3 4 5

Household´s Monthly Income per Socioeconomic Level

Source: FASECOLDA - YANHAAS 2009

20,6%

13,7%

11,8%

23,8%

18,3%

8,7%

3,2%

14,6%

6,0%

4,5%

20,2%

26,2%

22,8%

5,7%

12,3%

2,4%

2,8%

10,3%

24,9%

27,7%

19,6%

NS/NR

> $1.001 USD

$701 - 1.000 USD

$501 - $750 USD

$351 - $500 USD

$251 - $350 USD

< $250 USD

SEC 1 SEC 2 SEC 3

8/37

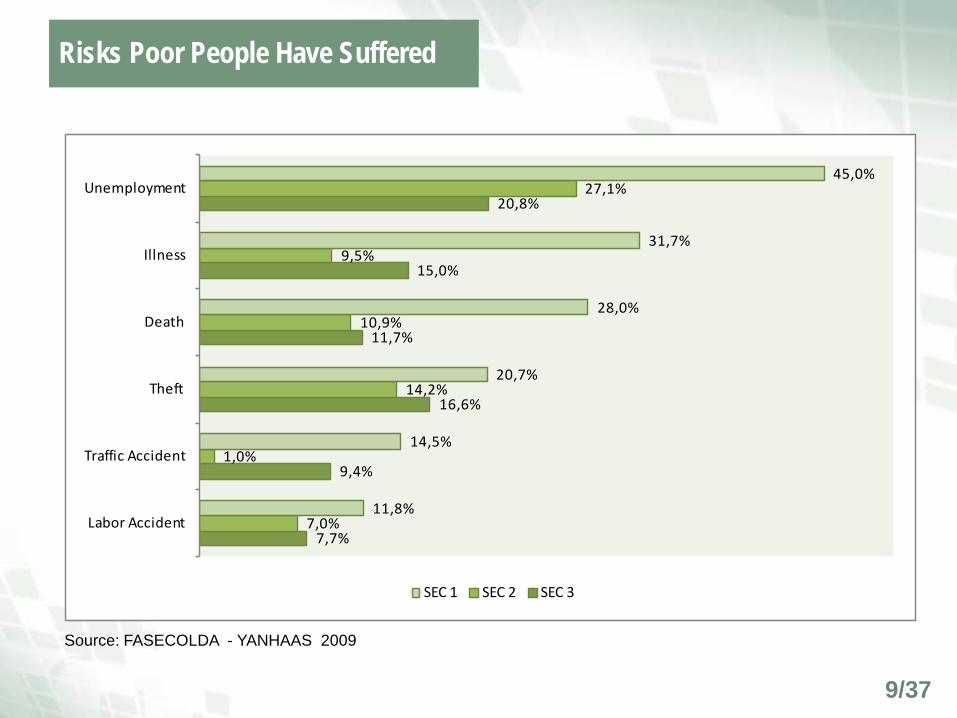

Risks Poor People Have Suffered

7,7%

9,4%

16,6%

11,7%

15,0%

20,8%

7,0%

1,0%

14,2%

10,9%

9,5%

27,1%

11,8%

14,5%

20,7%

28,0%

31,7%

45,0%

Labor Accident

Traffic Accident

Theft

Death

Illness

Unemployment

SEC 1 SEC 2 SEC 3

Source: FASECOLDA - YANHAAS 2009

9/37

How Poor People Covered Their Risks

0,4%

2,9%

3,2%

3,7%

6,5%

8,1%

20,2%

55,2%

Others

Look for another income

Lottery and charity

Insurance

Sell assets

Reduce comsuption

Savings

Loans

Source: FASECOLDA - YANHAAS 2009

10/37

• Products that respond to the protection needs of low income people.

• The costs are high in training agents and in educating the clients. In thatregard, policies should be easy to understand and to explain.

• Periodical payments regarding their cash flow.

• The scale of operation must be very small in terms of premiums but in highvolumes.

• Microinsurance is not an economic version of traditional products.

• Easy to sign: without previous inspections, special conditions to be apolicyholder and moral hazard.

• No exclusions.

Different Product Characteristics

11/37

• Easy to collect the premium thanks to the alliances with utilities services,microfinances institutions and retailers, among others.

• Easy to compensate. Fast payment and without many requirements.

• Claim process could not be the same for an insurance value of 100thousands dollars than for an insurance value of one thousand dollars.

• Payment process with minimal verifications. Evidence could replace somerequirements which are needed in traditional insurance products.

• Products are meant to be used, so the best reward in terms of clientconfidence is to pay with minimal conditions.

Different Product Characteristics

12/37

Development of Microinsurance Market in Colombia

Reasons and Results

13/37

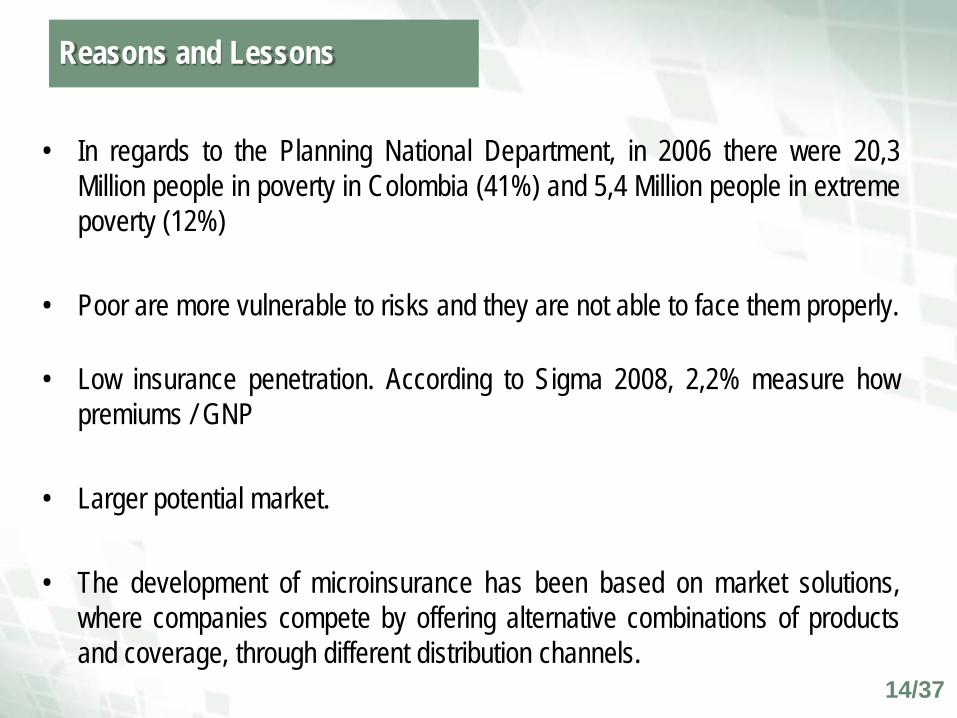

• In regards to the Planning National Department, in 2006 there were 20,3Million people in poverty in Colombia (41%) and 5,4 Million people in extremepoverty (12%)

• Poor are more vulnerable to risks and they are not able to face them properly.

• Low insurance penetration. According to Sigma 2008, 2,2% measure howpremiums / GNP

• Larger potential market.

• The development of microinsurance has been based on market solutions,where companies compete by offering alternative combinations of productsand coverage, through different distribution channels.

Reasons and Lessons

14/37

• Colombia is a country case where microinsurance has been developingrapidly through the private sector initiative, without any special laws, rules orregulations.

• According to the Microinsurance Center and our own statistics there arethree million policiyholders. Microinsurance encompasses more than 1,3% ofall premiums.

Lessons From The Colombian Experience

15/37

• More than 40% of insurance companies in Colombia (national and foreigncapital based, mutual cooperatives and one state-owned) already offer sometype of microinsurance products.

• Cooperative insurance companies have had microinsurance operations formore than 15 years.

• They have had to adjust their internal process to serve low income people.

• Licensed and regulated providers ensures client protection.

• A microinsurance business not as a special line of business or a specialinsurance company, but as a product under the regular lines of business,allows the application of the large numbers law and permits internal crosssubsidies which ensure the viability and sustainability of this new kind ofbusiness.

Microinsurance Providers

16/37

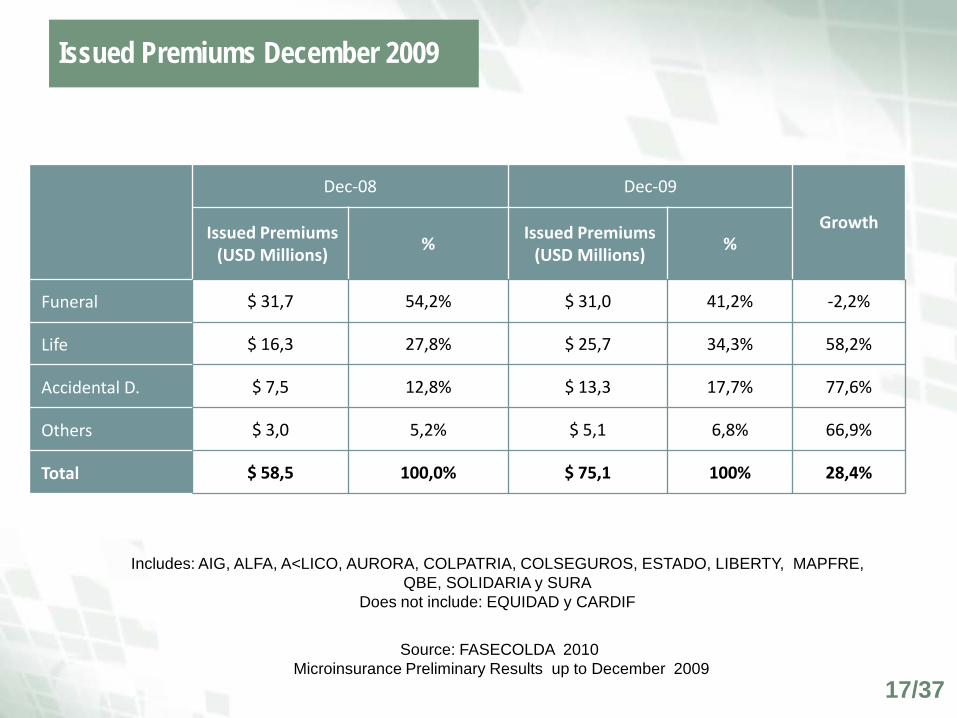

Issued Premiums December 2009

Source: FASECOLDA 2010 Microinsurance Preliminary Results up to December 2009

Includes: AIG, ALFA, A<LICO, AURORA, COLPATRIA, COLSEGUROS, ESTADO, LIBERTY, MAPFRE, QBE, SOLIDARIA y SURA

Does not include: EQUIDAD y CARDIF

Dec-08 Dec-09

GrowthIssued Premiums (USD Millions)

%Issued Premiums

(USD Millions) %

Funeral $ 31,7 54,2% $ 31,0 41,2% -2,2%

Life $ 16,3 27,8% $ 25,7 34,3% 58,2%

Accidental D. $ 7,5 12,8% $ 13,3 17,7% 77,6%

Others $ 3,0 5,2% $ 5,1 6,8% 66,9%

Total $ 58,5 100,0% $ 75,1 100% 28,4%

17/37

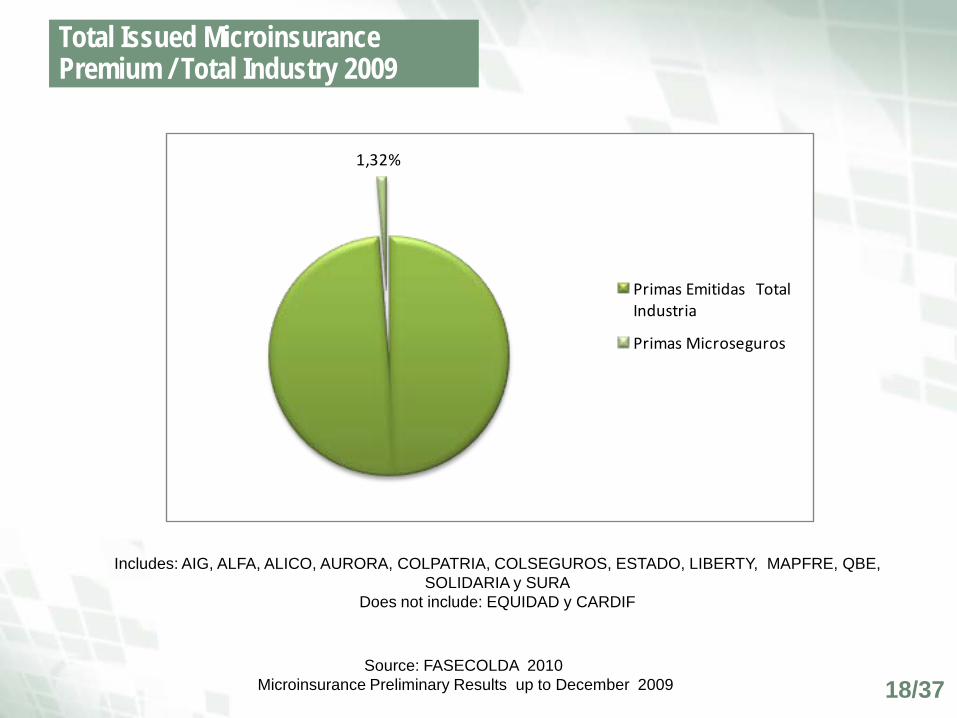

Total Issued Microinsurance Premium / Total Industry 2009

Source: FASECOLDA 2010 Microinsurance Preliminary Results up to December 2009

Includes: AIG, ALFA, ALICO, AURORA, COLPATRIA, COLSEGUROS, ESTADO, LIBERTY, MAPFRE, QBE, SOLIDARIA y SURA

Does not include: EQUIDAD y CARDIF

1,32%

Primas Emitidas Total Industria

Primas Microseguros

18/37

Policyholders December 2009

Dec - 2008 Dec - 2009Growth

Policyholders % Policyholders %

Funeral 780.783 31,7% 722.123 24,6% -7,5%

Life 738.558 30,0% 1.017.273 34,7% 37,7%

Accidental D. 657.757 26,7% 699.275 23,8% 6,3%

Others 288.573 11,7% 496.385 16,9% 72,0%

Total 2.465.671 100,0% 2.935.056 100,0% 19,0%

Source: FASECOLDA 2010 Microinsurance Preliminary Results up to December 2009

Include: AIG, ALFA, ALICO, AURORA, COLPATRIA, COLSEGUROS, ESTADO, LIBERTY, MAPFRE, QBE, SOLIDARIA

Does not include: EQUIDAD, CARDIF y SURA

19/37

Average Monthly Premium

(1) Note: The anual average premium in funeral services corresponds to the whole nuclear family, meaning 4 people in average per house. This means that the anual premium per person in funeral services is in average 11 dollars.

Dec-08 Dec-09

GrowthAverage Anual Premium

Average Monthly Premium

Average Anual Premium

Average Monthly Premium

Funeral $ 40,6 $ 3,4 $ 42,9 $ 3,6 5,7%

Life $ 17,8 $ 1,5 $ 20,5 $ 1,7 14,9%

Accidental D. $ 11,4 $ 0,9 $ 19,0 $ 1,6 67,1%

Others $ 10,6 $ 0,9 $ 10,2 $ 0,9 -3,0%

Total $ 22 $ 1,9 $ 23,9 $ 2,0 6,5%

Source: FASECOLDA 2010 Microinsurance Preliminary Results up to December 2009

Includes: AIG, ALFA, ALICO, AURORA, COLPATRIA, COLSEGUROS, ESTADO, LIBERTY, MAPFRE, QBE, SOLIDARIA

Does not include: EQUIDAD, CARDIF, SURA

20/37

Average Insured Value

Source: FASECOLDA 2010 Microinsurance Preliminary Results up to December 2009

Includes: AIG, ALFA, ALICO, AURORA, COLPATRIA, COLSEGUROS, ESTADO, LIBERTY, MAPFRE, QBE, SOLIDARIA

Does not include: EQUIDAD, CARDIF y SURA

Dec-08 Dec-09

GrowthAverage

Insured ValueAverage

Insured Value

Funeral $ 1.108 $ 1.124 1,4%

Life $ 2.614 $ 4.201 60,7%

Accidental D. $ 9.277 $ 14.651 57,9%

Others $ 9.925 $ 10.043 1,2%

Total $ 4.770 $ 6.922 45,1%

21/37

Paid Claims December 2009

Source: FASECOLDA 2010 Microinsurance Preliminary Results up to December 2009

Includes: AIG, ALFA, ALICO, AURORA, COLPATRIA, COLSEGUROS, ESTADO, LIBERTY, MAPFRE, QBE, SOLIDARIA y SURA

Does not include: EQUIDAD y CARDIF

Dec-08 Dec-09

GrowthPaid Claims(USD Millions)

%Paid Claims

(USD Millions) %

Funeral $ 21,5 78,9% $ 18,9 72,2% -12,5%

Life $ 4,5 16,5% $ 5,6 21,6% 25,2%

Accidental D. $ 0,8 3,1% $ 1,0 3,8% 18,3%

Others $ 0,4 1,4% $ 0,6 2,4% 58,1%

Total $ 27,3 100,0% $ 26,1 100,0% -4,3%

22/37

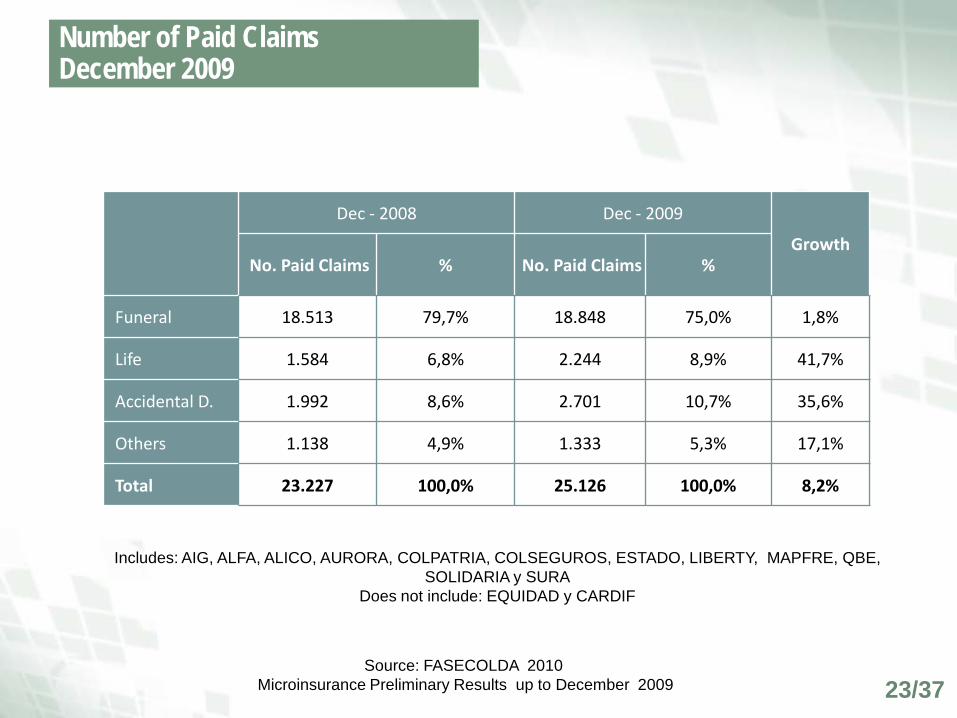

Number of Paid ClaimsDecember 2009

Dec - 2008 Dec - 2009

GrowthNo. Paid Claims % No. Paid Claims %

Funeral 18.513 79,7% 18.848 75,0% 1,8%

Life 1.584 6,8% 2.244 8,9% 41,7%

Accidental D. 1.992 8,6% 2.701 10,7% 35,6%

Others 1.138 4,9% 1.333 5,3% 17,1%

Total 23.227 100,0% 25.126 100,0% 8,2%

Source: FASECOLDA 2010 Microinsurance Preliminary Results up to December 2009

Includes: AIG, ALFA, ALICO, AURORA, COLPATRIA, COLSEGUROS, ESTADO, LIBERTY, MAPFRE, QBE, SOLIDARIA y SURA

Does not include: EQUIDAD y CARDIF

23/37

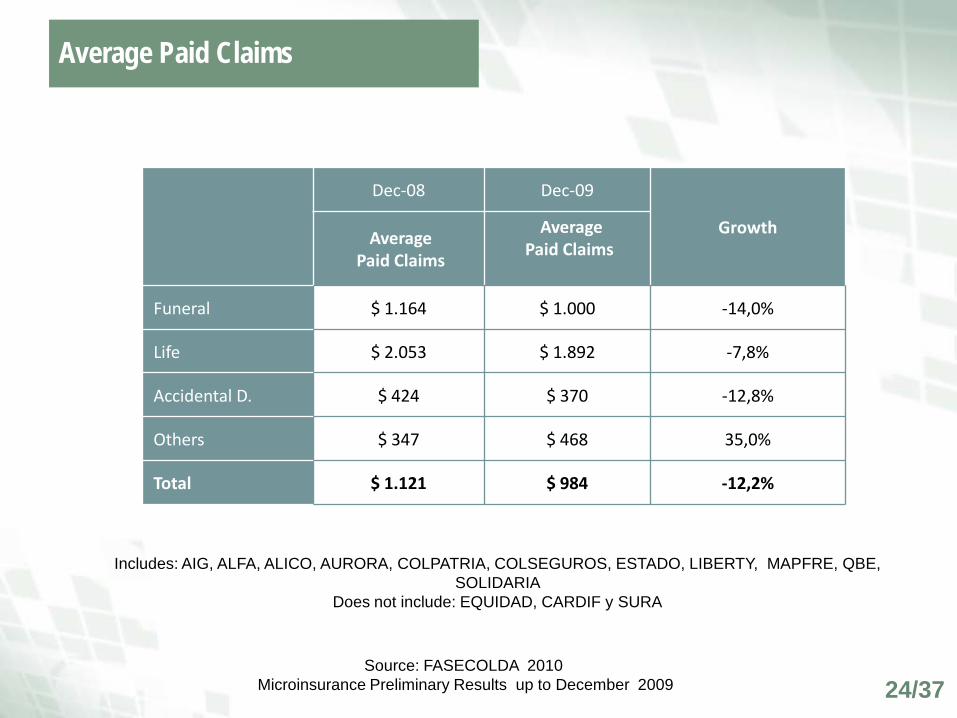

Average Paid Claims

Source: FASECOLDA 2010 Microinsurance Preliminary Results up to December 2009

Includes: AIG, ALFA, ALICO, AURORA, COLPATRIA, COLSEGUROS, ESTADO, LIBERTY, MAPFRE, QBE, SOLIDARIA

Does not include: EQUIDAD, CARDIF y SURA

Dec-08 Dec-09

GrowthAveragePaid Claims

AveragePaid Claims

Funeral $ 1.164 $ 1.000 -14,0%

Life $ 2.053 $ 1.892 -7,8%

Accidental D. $ 424 $ 370 -12,8%

Others $ 347 $ 468 35,0%

Total $ 1.121 $ 984 -12,2%

24/37

Paid Claims Ratio

Source: FASECOLDA 2010 Microinsurance Preliminary Results up to December 2009

Includes: AIG, ALFA, ALICO, AURORA, COLPATRIA, COLSEGUROS, ESTADO, LIBERTY, MAPFRE, QBE, SOLIDARIA

Does not include: EQUIDAD y CARDIF

dec-08 dec-09Growth

Paid Claims Ratio Paid Claims Ratio

Funeral 68,0% 60,9% -10,5%

Life 27,7% 21,9% -20,9%

Accidental D. 11,3% 7,5% -33,4%

Others 13,0% 12,3% -5,3%

Total 46,7% 34,8% -25,5%

25/37

Distribution Channels

Where is the success?

26/37

• Sign alliances with proper distribution channels that know the market andensure easy access to the same.

• The channel should ensure fast and massive sales, and the collection ofpremiums.

• The distribution of microinsurance products is easier when done along withother financial and non financial services.

• Distribution mechanisms ought to be innovative, low cost and massive.

• Most used channels: Utilities Services, MFI, Cooperatives, etc.

Different Distribution Characteristics

27/37

Access to Utilities

Source: DANE ECV - 2008

95,8%

87,3%

72,9%

35,3%

54,7%

17,7%

97,2%

86,7%

73,9%

47,4%44,3%

83,8%

Electricity Aqueduct Sewer system Town gas Phone Mobile phone

2003 2008

28/37

Issued Premiums per ChannelDecember 2009

Source: FASECOLDA 2010 Microinsurance Preliminary Results up to December 2009

Does not include: EQUIDAD y CARDIF

Dec-08 Dec-09

GrowthIssued Premiums(USD Millions)

%Issued Premiums(USD Millions)

%

Banks $ 3,6 6,5% $ 6,7 9,5% 85,1%

Familiar Benefits Unions $ 0,5 0,8% $ 0,8 1,2% 74,7%

Cooperatives $ 24,3 43,9% $ 22,5 32,1% -7,3%

Utilities $ 18,9 34,0% $ 27,4 39,0% 45,1%

MFI $ 5,6 10,2% $ 9,7 13,8% 72,0%

Supermarkets $ 1,1 1,9% $ 1,2 1,7% 12,9%

Others $ 1,5 2,6% $ 1,9 2,7% 31,7%

TOTAL $ 55,4 100,0% $ 70,2 100,0% 26,8%

29/37

Policyholders per Channel December 2009

Source: FASECOLDA 2010 Microinsurance Preliminary Results up to December 2009

Does not include : EQUIDAD ,CARDIF y CARDIF

Dec-08 Dec-09Growth

Policyholders % Policyholders %

Banks 93.599 3,8% 224.445 7,6% 139,8%

Familiar Benefits Unions 5.517 0,2% 8.081 0,3% 46,5%

Cooperatives 612.981 24,9% 508.263 17,3% -17,1%

Utilities 903.572 36,6% 1.290.137 44,0% 42,8%

MFI 476.487 19,3% 726.158 24,7% 52,4%

Supermarkets 309.669 12,6% 66.702 2,3% -78,5%

Others 63.846 2,6% 111.270 3,8% 74,3%

TOTAL 2.465.671 100,0% 2.935.056 100,0% 19,0%

30/37

Microinsurance for Familias en Acción and Red Juntos

The Challenge

31/37

• Familias en Acción is a Cash Conditional Transfer program in which 3 millionfamilies in poverty or extreme poverty with children below 18 years old,receive, per each child, a subsidy to keep children at school and to meetnutrition standards.

• The CCT is $50 dollars, given every month through a saving account (2million families)

• Familias Red Juntos is a program that identifies the extremely poor and picksup a baseline, which is composed of 45 goals in 9 areas (housing, banking,education, health, etc).

• The program encourages 1,5 millions families to meet the goals, otherwisethey will continue in the extreme poverty.

Who are Familias en Acción & Red Juntos

32/37

• Red Juntos does not give subsidies, it just gives an accompaniment to thefamilies through a person who is called the “Cogestor” and whose goal is totake out the family from the poverty.

• The aim of the program is to bring near the families the different public andprivate services supply, which could help them reach the goals and thus,overcome the poverty.

• One of the goals is financial education and access to microinsurance.

• To meet that goal, Acción Social (the policy of the government in charge ofboth programs),the insurance industry, paralife and multilaterals are workingon:

Who are Familias en Acción & Red Juntos

33/37

• Setting up a fund with multilaterals and government resources to insure 1,5millions families, subsidizing 100% of the premium the first year, 70% secondyear and 40% the third year.

• The insured value of the life insurance should be at least $1.000 dollars andthe premium 3 or 3,5 dollars per year.

• No exclusions, no conditions.

• 72 hour for paying claims.

• Government would like that all insurance companies to join to this initiative,and that is the reason why Fasecolda was inviting. Companies interested inparticipating will create a risk pooling.

The Project

34/37

• A portion of the fund´s resources will focus on the financial educationprogram. (Fasecolda has developed for two years a program like that throughworkshops and is going to launch the radio program next May).

• Insurance companies have to commercialize a voluntary product to cover thewife or husband.

• Insurance companies have to develop an innovative idea to collect thepremium since the second year of the project and utilities look like one of thepossible distribution channels.

The Project

35/37

• Colombia is a case where microinsurance has had a fast developmentthrough the private sector´s initiative, without any special laws, rules orregulations.

• The development of micro insurance has been based on market solutions.

• The biggest challenge is selecting the appropriate distribution channel thatensures massive sales and the colletion of the premium.

• Insurance and financial culture must be encouraged.

• The access to insurance from the poorest of the poor could be encouragedthrough public – private initiatives as the one we are working on.

Final Comments

36/37

Thanks !

37/37