middle east aviation yearbook

TRANSCRIPT

WORLD AVIATIONYearbook 2013middle east

2 2 aiRliNe leadeR | MAR-APR 2012

PROFILES

middle east tOP 10 aiRliNesSOURCE: CAPA - CENTRE FOR AVIATION AND INNOVATA | WEEk STARTINg 31-MAR-2013

middle east tOP 10 aiRPORtsSOURCE: CAPA - CENTRE FOR AVIATION AND INNOVATA | WEEk STARTINg 31-MAR-2013

Middle EastOutlookEvEn for a rEgion as fast

dEvEloping as thE MiddlE East, few years could match the changes wrought during 2012. The year saw the most influential

carriers in the region engage with the rest of the airline industry in a way that has profound implications for global aviation. 2013 will be the year that this dramatic reshaping begins to make its effects felt on the global competitive landscape ...

middle east caPacity seats PeR weekSOURCE: CAPA - CENTRE FOR AVIATION AND INNOVATA | WEEk STARTINg 31-MAR-2013

Emirates

Saudia

Flydubai

Air Arabia

Qatar Airways

Etihad Airlines

Oman Air

Gulf Air

Others

21.0%

12.2%

9.9%

5.8%3.9%2.9%2.6%

2.5%

39.2%

RaNkiNg caRRieR Name seats

1 emirates 138146

2 saudi arabian airlines 88275

3 Qatar airways 65680

4 etihad airways 38904

5 Flydubai 26073

6 Oman air 18768

7 air arabia 17982

8 gulf air 17136

9 el al israel airlines 16796

10 iran air 14941

RaNkiNg caRRieR Name seats

1 dubai international airport 1,639,176

2 doha international airport 604,630

3 Jeddah king abdulaziz international airport 568,138

4 Riyadh king khaled international airport 466,557

5 abu dhabi international airport 394,258

6 tel aviv-yafo Ben gurion international airport 265,145

7 kuwait international airport 241,591

8 muscat seeb international airport 211,896

9 Bahrain international airport 208,001

10 cairo international airport 176,202

3

middle east FleetSOURCE: CAPA - CENTRE FOR AVIATION | WEEk STARTINg 31-MAR-2013

middle east PROJected deliveRy dates FOR aiRcRaFt ON ORdeRSOURCE: CAPA - CENTRE FOR AVIATION | WEEk STARTINg 31-MAR-2013

middle east Fleet BReakdOwN FOR aiRcRaFt iN seRviceSOURCE: CAPA - CENTRE FOR AVIATION | WEEk STARTINg 31-MAR-2013

middle east mOst POPulaR aiRcRaFt tyPes iN seRviceSOURCE: CAPA - CENTRE FOR AVIATION

middle east caPacity seats shaRe By alliaNceSOURCE: CAPA - CENTRE FOR AVIATION AND INNOVATA | WEEk STARTINg 31-MAR-2013

iata middle east PRemium tRaFFic: 2009-2013SOURCE: CAPA - CENTRE FOR AVIATION AND IATA

Widebody Jet

Narrowbody Jet

Turboprop

Military Transport

Small CommercialTurboprop

Regional Jet

Piston EngineAircraft

47.7%

35.0%

6.5%

5.7%3.5%

1.6%0.1%

A320

777

A300

A330

737

Others

747

A340

21.8%

17.8%

9.3%7.3%

7.3%

4.3%

4.0%

28.1%

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12-20

-10

0

10

20

30

40

Prem

ium

Tra

ffic

Gro

wth

%Unaligned

SkyTeam

oneworld (affiliate)

oneworld

Star

62.6%16.0%

14.2%

7.2%0.0%

1,250

1,000

750

500

250

0

1,1796

45

699

In service In storage On order

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

0

50

100

150

A320 A330 A350 A380 737

787 777 ERJ170 CRJ

4

... Outside of this competitive re-ordering, the region continues to produce outstanding levels of growth. During 2012, Middle Eastern airlines lead growth rates for international passenger and cargo traffic. With the global economy slowly warming up again, particularly in advanced economies, the rest of the world will catch up, although the region is still expected to lead growth in 2013.

the Big three: the super connectors take sides

A generation ago, travellers to Europe swapped aircraft in London, Paris, Frankfurt or Amsterdam. Travellers to Asia connected in Hong Kong, Singapore or Bangkok. They flew typically with Lufthansa, British Airways, Cathay Pacific and Singapore Airlines. Increasingly though, these traditional carriers and their hubs have been superseded by Dubai, Doha and Abu Dhabi and their home carriers: Emirates, Qatar Airways and Etihad Airways.

The rapidity of the shift has been breathtaking. In the past five years, London Heathrow, Paris Charles de Gaulle, Frankfurt and Amsterdam added a total of 11.7 million new passengers between them, growth of just 5%. In Asia-Pacific, Hong Kong, Singapore and Bangkok Suvarnabhumi have added 34.4 million passengers over the same period, an increase of 27%.

In comparison, the three upstart Middle East hubs have added 35 million passengers, an increase of just under 60%. In 2012, the three Middle East hub airports handled 93 million passengers. In 2013, if their traffic projections are correct, the three hubs will handle a combined 110 million.

Dubai, the largest hub in the region and almost wholly dedicated to international traffic, has seen its traffic increase from 34.5 million in 2008 to 57.7 million in 2012. The airport is now the third largest hub in the world by international passengers, and plans to eclipse London Heathrow as the largest international airport within five years.

The transformation is being wrought by three state-owned but commercially focused airlines. Emirates, Qatar Airways and Etihad Airways are not only there to funnel traffic into and

lcc caPacity shaRe (%) OF tOtal seats: 2001-2013SOURCE: CAPA - CENTRE FOR AVIATION WITh DATA PROVIDED by OAg

middle east tRaFFic: 2008-2013SOURCE: CAPA - CENTRE FOR AVIATION AND IATA

Increasingly though, these traditional carriers and their hubs have been superseded by Dubai, Doha and Abu Dhabi and their home carriers: Emirates, Qatar Airways and Etihad Airways.

0.1%0.9%

1.9%

3.5%

5.6%

7.4%8.3%

11.6% 11.3%

13.3%

15.3%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Jan-Mar

2013

0

2

4

6

8

10

12

14

16

18

Jan-09Jul-08Jan-08 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-130

5

10

15

20

25

30

Reve

nue

Pass

enge

r Ki

lom

etre

s %

5

of the Middle Eastern hub carriers. This advantage means that these airlines have been able to tap into the burgeoning global travel growth, capturing an ever-increasing share of international long-haul traffic, particularly the important business and premium market segments.

Like the shifting centre of gravity of global economic power, the balance of global aviation is gradually moving east. For years, the traditional hub carriers, as well as some governments, fought a vocal battle to stem the shift and the threat of the Middle Eastern sixth freedom carriers. However, 2012 saw them move away from antagonism and more towards embracing their opponents.

In doing so, each of the three Middle Eastern carriers picked a different strategy. Emirates chose to enter a partnership with Qantas, in a deal that will see the Australian carrier shift its European transit hub from Singapore to Dubai, ending a 17-year strategic codesharing agreement with British Airways, as well as another codeshare deal with Cathay Pacific. Emirates is also eager to enter a tie-up with American Airlines, although a partnership may depend on the outcome of the carrier’s merger with US Airways.

During 2012, Etihad Airways also entered a major partnership, this time with Air France-KLM. Less than a month after the Emirates-Qantas deal, Etihad Airways and the Franco-Dutch airline group sealed a joint codeshare deal covering destinations in Europe, the Middle East, Asia and Australia. As a part of the deal, Air France also entered a new codeshare agreement with airberlin, Europe’s through their hubs, they are also there to make money. The airlines, and

the forward and far thinking governments behind them, have married geographic advantage, modern and integrated infrastructure and tourism support from their home governments along with ambitious expansion plans.

Around 80% of the world’s population lies within 10 hours flight of Dubai. This puts the fast growing economies of China, Southeast Asia, Africa and India, along with their rapidly expanding and increasingly travel-inclined middle classes, within the extended catchment areas

euROPeaN, asiaN aNd middle east huB aiRPORt tRaFFic: 2008-2012 SOURCE: CAPA – CENTRE FOR AVIATION & AIRPORT REPORTS

middle east glOBal PRemium tRaFFic maRket shaRe: aPR-2008 tO aug-2012 SOURCE: IATA AND CAPA – CENTRE FOR AVIATION

The transformation is being wrought by three state-owned but commercially focused airlines.

2008 2009 2010 2011 20120

50

100

150

200

250

300

Middle East hubs Asia Pacific hubs European hubs

15%

14%

13%

12%

11%

10%

9%

8%

7%

6%

Premium traffic share 12 month moving average

110millio

nprojected passenger through-put for abu dhabi, dubai and doha in 2013

6

sixth largest airline, in which Etihad Airways holds a 29.21% stake.

Since its launch in 2004, Etihad Airways has built an extended network of codeshares, investments and strategic agreements, developing what it terms the world’s first “equity alliance”. Aside from airberlin, it controls shares in Air Seychelles, Virgin Australia and Aer Lingus.

The relationships have allowed Etihad Airways to dramatically expand its global coverage. The airline now boasts a total of 248 codeshare destinations, compared to just 86 destinations it serves with its own metal. The equity alliance looks set to expand in 2013, with Etihad interested in a 24% stake in Jet Airways, an investment estimated at around USD300 million. The carrier could take its shareholding up to 49% – the limit allowed under Indian regulations – at a later date.

Qatar Airways has chosen a third route, announcing that it will join the oneworld alliance in either late 2013 or early 2014. The airline will join Qantas, Cathay Pacific and British Airways in the grouping. After Emirates, Qatar Airways was the second largest full-service airline in the world not involved in one of the three major global airline alliances. The carrier’s move into the alliance will allow oneworld to redirect much of its east-west traffic through Qatar Airways’ Doha hub, providing superior routing alternatives across many hundreds of city pairs.

the Middle East lCCs

2013 will see the 11th year of the low-cost model in the Middle East. In 2012, LCCs in the Middle East reached a milestone 10% of overall regional capacity. Even with the rapid growth the LCC model remains under-developed in the region. In Europe, North America and even in developing areas such as Southeast Asia and India, low-cost carriers

2004 2005 2006 2007 2008 2009 2010 2011 2012

0

2

4

6

8

10

12

14

16million

Intra-Middle East To/from Middle East

middle east lcc caPacity: 2004-2012 SOURCE: CAPA – CENTRE FOR AVIATION & OAg

BOeiNg 737Ng RaNge chaRt SOURCE: bOEINg

account for a far greater proportion of traffic. A number of bankruptcies have seen smaller, privately-owned LCCs

fall by the wayside, with Sama and most recently Bahrain Air declaring bankruptcy. There are only four LCCs left in the Middle East regional market, down from six a few years ago. However, the surviving carriers represent the fastest growing segment in a region characterised by high levels of growth. If anything, the impact that LCCs have in the market belies their status.

Most LCCs in the Middle East deploy the majority of their capacity to destinations within the region. This is perhaps a surprising statistic given the fact that there are two billion people within 4.5 hours flying time of Dubai. However, the region’s fast growing population and developing tourism markets, as well as the number of underdeveloped markets, have ensured the strong growth.

There are only four LCCs left in the Middle East regional market, down from six a few years ago.

7

of SkyTeam during the year. The ascension of these airlines fills a long-standing Middle East black spot in the alliance’s global network coverage. For the airlines, it holds the promise of boosting yields by increasing their attractiveness to foreign travellers and business passengers.

growth is likely to continue unabated

Growth continues in the Middle East at a rate that has confounded the critics of airlines in the region. According to IATA, airlines in the Middle East contributed almost a third of the growth in international passenger travel in 2012. The region also led the world in terms of freight growth, defying the global contraction in cargo traffic.

There are still areas that carriers in the region can improve. Compared to developed markets such as North America and Europe, load factors, particularly on inter-regional flights remain low. Secondary airports, particularly ones favourable to the low-cost carrier models, are a rarity in the region, stifling the potential for growth in some of the larger domestic markets. Government ownership and government protectionism remains high in the Middle East, with state-owned carriers controlling all of the largest markets.

Despite the unparalleled levels of aircraft on order in the region, passenger and freight traffic levels in the Middle East in 2012 grew ahead of capacity. The trend indicates that the upward trajectory of the region is sustainable and part of a re-ordering of the way the world travels.

There are a number of opportunities for further development in 2013. Even with their dwindling numbers, the Middle East LCCs are still entering new markets, taking more aircraft into their fleet and offering their customers an enhanced and increasingly sophisticated array of product and services.

developing markets and ailing airlines, the rest of the Middle East

Outside of the Gulf sixth freedom carriers and the LCCs, airlines in the Middle East suffer a variety of mixed fortunes. The region has few listed airlines, but those that are – such as Royal Jordanian – have generally been profitable. The smaller state-owned carriers have typically struggled with heavy losses, which were only exacerbated due to the disruption of the Arab Spring period. These carriers are typically over staffed, under financed and saddled with ageing fleets and inefficient business structures. The results are losses that would be unsustainable without state support.

However, there is hope yet for the region’s smaller state-owned carriers. Efforts are under way at perennial loss-makers of the region to transform them into commercially viable airlines. For some, such as Kuwait Airways and Saudia, this is taking place via thorough modernisations ahead of planned privatisations, although political pressures have ensured that the process is a drawn-out one. Others, including Gulf Air, Iraqi Airways and Oman Air, are undergoing bottom-up restructurings, often in the face of politically and socially painful choices.

The Middle East became increasingly connected to the alliance network in 2012. Apart from Qatar Airways’ impending membership of oneworld, Saudia and Middle East Airlines both became members

Compared to developed markets such as North America and Europe, load factors, particularly on inter-regional flights remain low.

The trend indicates that the upward trajectory of the region is sustainable and part of a re-ordering of the way the world travels.

shaping an informed discussion through knowledge sharing

At CAPA, we don’t just ‘do’ conferences. We live and breathe the content. It’s our industry, our expertise, our constant focus.

So at CAPA Knowledge Events, you’ll hear from airline CEOs, CFOs and other industry thought leaders. CAPA Knowledge Events offer great

content and networking opportunities with the people that truly shape the direction of our industry.

We shape an informed discussion based on the latest research from our global team.

CAPA’s 2013 knowledge forums include:

Sydney, 7-9 August 2013

3

Dublin, 11-12 April 2013

A CEO Gathering

Seoul, Korea, 4-5 September 2013

Amsterdam, 25/26 November

Our CAPAbilities – helping you keep yourfinger on the pulse of global aviation

Need to know more? Visit our website: www.centreforaviation.com

Insight. Interaction. Information. Follow us @CAPA_Events

9

aiR aRaBia ....................................................................pp.11“air arabia reports another six months of profit and consistent growth”First published on www.centreforaviation on 21st august, 2012

emiRates .......................................................................pp.19“how emirates and friends will soon reshape american aviation”First published on www.centreforaviation on 11th may, 2013

etihad aiRways ............................................................pp.31“etihad jolts the status quo again – Jet airways and (wait for it) air canada are its newest partners”First published on www.centreforaviation on 27th april, 2013

FlyduBai .......................................................................pp.39“flydubai has bright outlook after recording first profit and emerging as close partner to emirates”First published on www.centreforaviation on 19th February, 2013

MIDDLE EAST:Selected airlines

10

gulF aiR ........................................................................pp.51“gulf air turn around plan offers a glimmer of hope for the beleaguered flag carrier”First published on www.centreforaviation on 2nd may, 2013

JaZeeRa aiRways .........................................................pp.60“could Jazeera airways, a small and nimble carrier, come to the rescue of kuwait airways?”First published on www.centreforaviation on 9th may, 2013

Nas aiR ..........................................................................pp.69“nasair plans ambitious expansion in 2013 ahead of further liberalisation in saudi arabian market”First published on www.centreforaviation on 22nd april, 2013

QataR aiRways .............................................................pp.77“Qatar airways set to join oneworld by late 2013”First published on www.centreforaviation on 1st may, 2013

saudia ...........................................................................pp.86“saudia faces new competitive threats in 2013 as saudi arabia loosens the regulatory reins”First published on www.centreforaviation on 6th may, 2013

11

Air Arabia Key Data Fleet and Orders Air Arabia Fleet Summary: as at 9-Apr-2013

Source: CAPA Fleet Database

Air Arabia projected delivery dates for aircraft on order: as at 8-Apr-2013

Source: CAPA Fleet Database

12

Route area pie chart Air Arabia international capacity seats by region: as at 8-Apr-2013

Source: CAPA - Centre for Aviation and Innovata Top routes table Air Arabia top ten international routes by seats: as at 8-Apr-2013

Source: CAPA - Centre for Aviation and Innovata

13

Premium/Economy profile Air Arabia schedule by class of seat - one way weekly departing seats: as at 8-Apr-2013

Source: CAPA - Centre for Aviation and Innovata

Share price 2012/2013

Source: CAPA - Centre for Aviation and Yahoo! Financial

14

Air Arabia reports another six months of profit and consistent growth Air Arabia continues to prove it is one of the Middle East’s most consistently profitable airlines. While other carriers in the region have suffered through the vagaries of the regional economic climate and the various social and political disruptions, the carrier has continued to report solid results, despite the external shocks buffeting it and mounting competition in the market space it pioneered in the Middle East. With its low-cost operation, solidly installed passenger base and nimbleness in exploring new routes and reallocating capacity, the carrier soldiered through the high oil prices and Arab Spring period with comparative impunity. Although the regional political climate is far from settled, economic conditions are improving and the carrier is now looking to capitalise on renewed traffic in the Middle East. 2012: A return to double-digit margins? 2012 is looking likely to be a significant improvement on 2011 in terms of both traffic and the bottom line. Air Arabia’s net profit for 1H2012 was AED115 million (USD31.3 million), an increase of 22% on the previous period in 2011. The net result is the carrier’s best since 1H2009, although the 2011 figures were dragged down slightly by the carrier continually adjusting operations to deal with the unrest in the region. Net margin was 9.6%, up slightly from 1H2011. Air Arabia first half revenue and net profit: 1H2008 to 1H2012

Source: CAPA – Centre for Aviation & Air Arabia Revenue grew 22% in the six-month period, to a record AED1300 million (USD354 million). The airline handled 1.3 million passengers for the half year, at an average load factor of 85%. This is an improvement of 3ppts on the same period in 2011, and a particularly strong result for the first half of the year.

15

Air Arabia quarterly revenue and net profit: 2008 to 2012

Source: CAPA – Centre for Aviation & Air Arabia Second quarter results were notably strong, and indicate positive momentum for the important third quarter. During 2Q2012, Air Arabia reported a net profit of AED66 million (USD18 million), an increase of 31% year-on-year. Turnover for the quarter was AED729 million (USD198.5 million) an increase of 23%. Yield levels were up 11%, with the carrier reporting strong demand despite regional competitors continuing to expand apace. Capitalising on underserved markets Air Arabia chairman Shaikh Abdullah Bin Mohammad Al Thani attributed the recent strong results to the carrier’s ability to identify and capitalise on underserved routes in the Middle East. During the first six months of 2012, the airline added new routes to Taif in Saudi Arabia and Salalah in Oman, both secondary regional destinations that have shown impressive traffic growth. Saudi Arabia in particular has become a core market for Air Arabia: the carrier operates 66 weekly frequencies to seven Saudi Arabian destinations: Madinah, Riyadh, Jeddah, Dammam, Qassim, Taif and Yanbu. During 1H2012 the airline also increased capacity to Dammam, Riyadh and Kuwait, primarily from its Sharjah hub. Also seeing increased capacity was Nagpur.

16

Air Arabia destination map: Aug-2012

Source: Air Arabia There are plenty of markets that Air Arabia has yet to fully develop in the Middle East and further afield. The carrier has only two routes into Iran – Shiraz and Tehran – and the Iranian market remains a major growth opportunity, even with the uncertain political environment. Air Arabia is also yet to add any routes into the fast-growing Iraqi market. Regional low cost rivals such as flydubai and Jazeera Airways are already serving the Iraq market. Outside of the Middle East, South Asia remains Air Arabia’s core market. The airline has an extensive network in India, operating to 11 destinations, but its network into Pakistan is comparatively underserved. Pakistan is an important migrant worker market for GCC countries, but Air Arabia’s operations into the country are limited to Pashawar and Karachi. Pakistan International Airlines already operates to Sharjah from Sialkot and Turbat. Similarly, connections into Northern and Eastern Africa are yet to be properly explored; outside of Morocco and Egypt, the carrier’s only African destinations are Khartoum and Nairobi. Multi hub strategy proving its worth Air Arabia’s multi-hub strategy of using local joint-venture partnerships to operate Air Arabia branded carriers adds another layer to its strategic options. The carrier’s Morocco and Egypt hubs are recovering well after the disruption of 2011. Both have reached cash flow and profitability break-even and are operating in excess of 70% load factors. From hubs in North Africa, the carrier has easy access to Western and Central Europe. Having taken delivery of its fourth A320 in Jun-2012, and launching a new route to Milan, the carrier is also assessing the possibility of adding more European destinations. Air Arabia Egypt launched a successful charter operation between the Red Sea and Europe in 2011, and the carrier sees enormous potential for leisure travel between Egypt and Europe.

17

Thanks to the open skies agreement between the EU and Morocco, Air Arabia Maroc already operates to 18 designations in the EU, 13 of them year-round. The carrier reportedly plans to introduce Nador-Bologne service and is also looking at a London service from Casablanca, although the UK is not a major market for the carrier despite no carrier having a stronghold. Ranking of carriers serving the UK from Morocco (seats per week): 20-Aug-2012 to 26-Aug-2012 Rank Airline Total seats 1 U2 easyJet 1932 2 BA British Airways 1892 3 AT Royal Air Maroc 1398 4 FR Ryanair 1323 Source: CAPA – Centre for Aviation Eastern Europe is also an attractive option for Air Arabia, particularly Russia and the CIS states, which have a combined market of more than 175 million people. Air Arabia already operates to Moscow, Kiev, Donetsk and Almaty from Sharjah, but is looking at additional routes, possibly as seasonal destinations. Both Sharjah and Alexandria are viable options to serve and Egypt is a popular tourist destination for Russian nationals. A major unresolved strategic question for the carrier is its fourth hub in Jordan, which remains on hold for the moment. The launch of the new hub was suspended last year due to the Arab Spring disruption. The present instability related to neighbouring Syria makes it unlikely the carrier will add to its Amman hub until regional stability returns and the global economic climate improves. Solid outlook for 2012 While net margins are down on the 20% plus levels seen in 2008 and 2009, Air Arabia is still consistently profitable and has largely managed to avoid the creep in unit costs that has affected some of its contemporaries. Unit costs were up 10.4% in 2Q2012, behind the increase in unit revenue of 9.9%. However, excluding fuel, Air Arabia managed a 6% reduction in per passenger unit costs. Air Arabia unit revenue and unit costs: 2004 to 2011

Source: CAPA – Centre for Aviation & Air Arabia

18

Fuel costs remain a concern, with overall 1H2012 costs up 15% and fuel costs continuing to challenge regional carriers, according to Air Arabia CEO Adel Ali. Air Arabia has hedged 25% of its expected fuel acquisitions for 2012 at USD90.45 per barrel, and is taking a conservative approach to its fuel strategy. In May-2012, Mr Ali said oil at USD85-95 per barrel would be good for the aviation industry and that “plus or minus USD100 is reasonable for the seller and the buyer”. He does not expect a return to the USD70-80 per barrel oil prices seen earlier this year. Air Arabia fuel hedging strategy: Aug-2012

Source: Air Arabia Air Arabia started 2H2012 with record monthly traffic: Jul-2012 passenger numbers rose almost 10% year-on-year to 477,839. The busy summer holiday travel period is the key to profitability for the airline. Generally, the carrier earns between 35% and 45% of its profits in the quarter. With strong Jul-2012 traffic and solid forward bookings promising record passenger levels in the vital summer travel period, the carrier has a positive outlook for the full year period. According to Mr Ali, the airline is witnessing “significant customer demand” across its network. Air Arabia will target growth into Central Asia, Russia the CIS and Eastern Europe from its Sharjah hub. Egyptian operations will be grown organically, focusing on the Gulf region, Europe and Africa. Moroccan operations will expand into Europe, and the carrier will seek further flying rights to Africa. The low cost market segment is a growing part of the Middle East’s aviation ecosystem and complements the sixth-freedom, and often long-haul focused, behemoths. Air Arabia plans a continuous expansion over the next few years. LCC market penetration in the Middle East is still only 6%, so there is plenty of room for growth and Arab intra-regional traffic shows increasing demand for air travel as local economies develop.

19

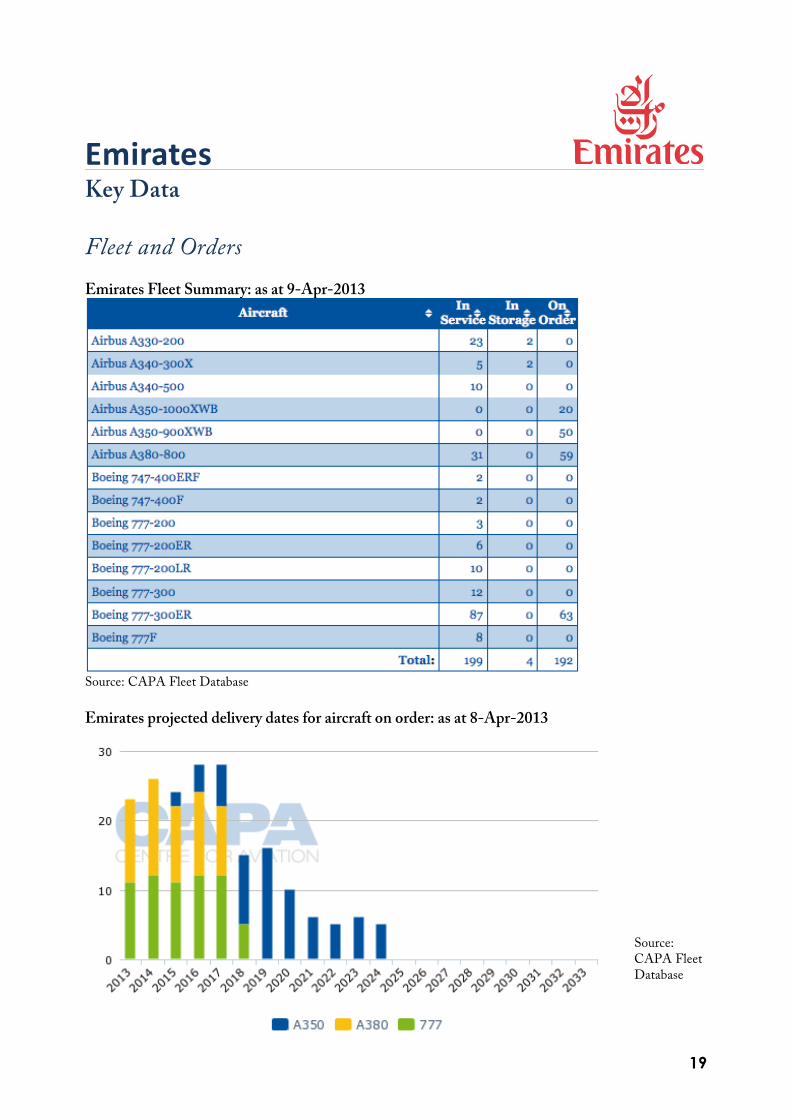

Emirates Key Data Fleet and Orders Emirates Fleet Summary: as at 9-Apr-2013

Source: CAPA Fleet Database

Emirates projected delivery dates for aircraft on order: as at 8-Apr-2013

Source: CAPA Fleet Database

20

Route area pie chart Emirates international capacity seats by region: as at 8-Apr-2013

Source: CAPA - Centre for Aviation and Innovata Top routes table Emirates top ten international routes by seats: as at 8-Apr-2013

Source: CAPA - Centre for Aviation and Innovata

Premium/Economy profile Emirates schedule by class of seat - one way weekly departing seats: as at 8-Apr-2013

Source: CAPA - Centre for Aviation and Innovata

21

How Emirates and friends will soon reshape American aviation

Shortly after Emirates Airline announced its remarkable breakthrough partnership with Qantas in Sep-2012, Emirates CEO Tim Clark said he had also been talking to American Airlines for some time and publicly expressed hopes that the two would also establish a close relationship. This was despite the fact that American already had an extensive codeshare relationship with Etihad; and the third Gulf carrier, Qatar Airways, has since been invited to join the oneworld alliance – which American leads.

The Gulf airlines, and particularly Emirates, have had a devastating impact on European long-haul hub carriers. The impact will be different for US airlines, but despite the different geography, it will be much bigger than most expect. For one thing they will cut across the developed boundaries of the global alliances.

Emirates is the world’s largest international long-haul operator by a wide margin; even on a seat basis, only three European airlines (Ryanair, easyJet and Lufthansa) head it, thanks to their high density short-haul operations. World top 20 international airlines (ASKs)

Source: CAPA – Centre for Aviation, Innovata

22

Emirates’ all-widebody 200-strong fleet already contains, among others, 32 A380s and some 120 Boeing 777s. Moreover, it continues to grow at a remarkable rate.

Another 191 widebody aircraft (currently including 58 A380s, 70 A350s and 63 777s) are on order. The delivery schedule provides for more than two of these aircraft entering service every month for the next five years.

23

Inevitably, with this global coverage, Emirates has numerous airline partnership opportunities, aside from the Qantas joint venture. This is no minor operation either. (Despite Australia’s small population there is a high propensity for international travel and the country’s relatively strong economy means that several sixth freedom airlines each fly around 100 widebody weekly services into Australia; Emirates operates around 11,000 seats daily into that market.)

Necessarily, the bulk of Emirates’ traffic is networked over its Dubai hub (although a growing amount is now end-to-end; Dubai receives more inbound tourists than India). Emirates’ geographic position and increasing ability to disperse over a wide range of global points (currently to 119 cities non-stop) encourages massive flows between the Indian subcontinent (“South Asia”) and Europe, for example. Given the relative geographical differences the dynamics of the US market are different, but they are no less potentially compelling. The US-Emirates proposition differs from the European hub geography As can be seen from the graph above the US is still underdone when it comes to Gulf carrier penetration. This is both because it is early days and because the hub proposition is different for the US. Although Emirates is undoubtedly well placed to service Indian travellers between the US and the sub-continent, the hub value for the US market deteriorates the further east the origin point is. So, few would think of flying between Shanghai and San Francisco via Dubai; but Shanghai-New York over the Gulf becomes potentially competitive, as a search on Expedia will show. And, the further south the East Asian point, the more competitive it becomes – for example, a daily Ho Chi Minh City service by Emirates over the Gulf, one-stop to New York offers a direct

24

challenge to any other product (as a combination of elapsed time, inflight quality, frequency, network coverage, price etc). Then, for Bangkok, where Emirates has a five-times daily operation, or Singapore, with thee daily non-stops from Dubai, connecting with three-times daily New York flights, the “product”, especially for business/premium travellers, emerges as a winner for travellers to the Big Apple. This is one reason the Gulf airlines, with their extremely high quality inflight product, are capturing the lion’s share of global premium traffic, just as many airlines are cutting back on front-end capacity. For the still small, but fast growing and high yielding African market, the Gulf carriers are becoming a more and more attractive proposition from US points. Their extensive networks in the region and their explosive entry into partnerships with many of the key African carriers are positioning the Gulf airlines to compete aggressively with European hubs, where the rare direct services are not available. Yet it takes time to build network strength. For the time being the US (and Canada) does not have adequate capacity, frequency and network to have the pulling power the hub carrier enjoys in Europe. Thus, strategically, Emirates must achieve two goals:

• First, enhance its partnership/reciprocal codeshare linkages. This will allow it to feed its network via third party airlines, both providing Emirates with more traffic and its partner with greater access to a global network; then

• Secondly, having constructed its foundation, expand its own services. As European, Australian and African based airlines have learned, the first part of this equation becomes almost unavoidable, on the basis of “if you can’t beat them join them”. Air France for example had been so sternly opposed to the expansion of the Gulf carriers that, when the carrier last year agreed to codeshare with Etihad, IAG CEO Willie Walsh described the about-face as being the equivalent to Air France “talking to the devil.” Mr Walsh had meanwhile persuaded Qatar Airways to join oneworld and Emirates was dealing with Qantas. Consequently, working with Emirates offers a highly attractive alternative, even though it may appear to limit the longer term options of the foreign airline. And, if it does so limit the airline, well, the reality is that the Gulf carriers have changed the world – there is no looking back. The new partnerships will cut across the previous evolution of the multilateral alliances This development is occurring just as the major airlines (and their host airports) have begun to settle into a regime where there are three global teams, each with their various allegiances and internal connectivity. The upshot will be upheaval for airlines and, in many cases, airports alike. As the post Sep-2012 world unfolds, enormous changes are occurring beneath the surface. Things may look the same, but they are not.

25

For one thing, Emirates had, prior to its Qantas deal, eschewed the concept of partnerships, beyond a number of codeshares and some FFP cooperation. It saw itself as being large enough to achieve its goals without resort to other airlines – and certainly was not going to constrain its freedom of movement by allying with Star, SkyTeam or oneworld. In this respect oneworld co-founder American Airlines is in the tantalising position that it will now become a bellwether of the future pattern for alliances. As American emerges from its relatively brief hibernation in Chapter 11, now under new ownership, it finds itself at the centre of a love triangle in what could be pivotal moves in the worldwide alliance regime. American has an important and extensive codeshare agreement with Etihad; meanwhile its British Airways partnership and oneworld membership point it in the direction of oneworld member-elect Qatar Airways. Yet, as part of Emirates’ new approach to US expansion, Mr Clark, last year publicly expressed hopes that a deep partnership could be established between his airline and American. The intriguing prospect that American/US Airways now faces is the opportunity to partner with all three of the Gulf carriers. In a previous world, this would have been unthinkable, with such a formidable assortment of potential conflicts. Today perhaps the real issue is how to manage those conflicts, not how to avoid them. If conflict management becomes the corporate thinking, there will indeed be a revolution afoot. At that stage others become impelled to respond; as has happened in Europe in 2012, one such move can quickly trigger a chain reaction. The fast spreading role of pragmatic partnerships is changing the world, as Emirates announces a Milan-New York service Yet another dimension was added to Emirates’ operations when on 08-Apr-2013 it announced the launch of the airline’s first trans-Atlantic (Europe-US) operation since it dropped Hamburg-New York in 2008. Emirates from 1-Oct-2013 will operate 777-300ER service between Milan and New York JFK as an extension of one of Emirates’ existing three times daily Dubai to Milan flights, making for a total of three times a day service by Emirates into New York (the other two being non-stop from Dubai). Mr Clark said at the announcement, “Operating a trans-Atlantic route has been on our agenda for some time. Having carefully monitored traffic flows we have identified strong demand for both a direct connection and, importantly, for the Emirates product. The route is currently underserved, particularly with a strong premium product offering this is where we see a clear opening for Emirates. We intend to capitalise on this opportunity, stimulating further demand and encouraging additional traffic flow in both directions.” The partnership dynamics are made even more intriguing as Emirates will also leverage its relationships with JetBlue (also an American partner) in the US and, in Europe, its frequent flyer partnership with easyJet to help feed each end of the operation.

26

The often-restrictive ENAC (Italy’s Civil Aviation Authority) has authorised the Milan-New York operation “on an extra-bilateral basis”. The fifth freedom route approval was somewhat unusual, as the Milan-JFK route is also served on a daily basis by home-grown Alitalia (which is frequently protected by the Italian administration) as well as by Delta, United and American itself. The decision was specifically made on the basis that it would deliver “significant economic benefits for the Italian economy, exporters, tourism and airports”. This is a seemingly obvious driver for governments, but in international aviation it represents an important shift in emphasis away from supporting the national flag carrier, regardless of the negative impact the policy had on other stakeholders. In the present context it is a fundamental change which allows Emirates and the other Gulf carriers to gain the access they need to expand their networks. And it is the other key piece of the jigsaw that opens the door to Emirates and the others negotiating on such powerful terms with the established flag carriers. In the case of the Emirates-Qantas JV (and others like it formed by Etihad) the key to liberal access is utilising so-called third country codeshare rights (where a third country’s airline “metal” is used in exercising bilateral rights between two other countries); the Italian example goes a step further up the liberalisation path, using fifth freedom rights. And, if Italy, not renowned for its liberal approach to air services rights, is prepared to allow third country airlines to support a local economy, how long will it be until other regional communities in European countries argue for similarly enlightened access? Protectionist barriers are eroding quickly, but there are still some holdouts Despite the enormous shifts in global attitudes to market access, there are however still a few major logjams for Emirates’ expansion. Not all countries are so enlightened. These simultaneously present short term barriers to entry, while holding out the promise of mid-term future opportunities as liberalisation inevitably erodes government support for nationalist protectionism. Austria is a case in point, where Lufthansa-owned Austrian Airlines is able to use obscure bilateral wording to prevent either Emirates operating its A380 into Vienna or allowing partner Qantas to offer seats on a third country codeshare basis – despite Australia having bilateral access rights. As noted above, Air France and its government also maintained a typically protectionist / mercantilistic approach against admitting the Gulf carriers. But once Etihad secured a toe in the door with its announcement of a codeshare agreement with Air France, the opening is likely to be followed by fellow SkyTeam member Kenya Airways also joining forces with the Abu Dhabi carrier. This does not directly help Emirates, but it indicates clearly that the last defences are crumbling. In Europe Emirates makes the point forcefully that protecting the relatively lower economic value of the national airline is illogical where Emirates is the largest single buyer of Airbus aircraft and notably of the iconic A380. In Apr-2013, Mr Clark noted that his airline contributes EUR200 million annually into the French economy as a result.

27

Canada too occupies a position at the protectionist end of the spectrum, although, as with Air France, an Apr-2013 announcement that Air Canada signed an MoU with Etihad with a view to future codesharing again accentuates the pressures on national administrations (and the partnership potential for airlines) to open doors to the highly attractive consumer opportunities offered by the Gulf carriers. Lufthansa, although it once came close to breaking ranks and dealing with Etihad, is now instead electing to work with fellow Star member and neo-Gulf carrier, Turkish Airlines, itself embarked on a rapid growth trajectory. Lufthansa and Germany consequently are the standouts in the European market as far as liberalised access is concerned. Even with a supportive government, airport and airways infrastructure is still a problem where airline growth is so rapid But even the Gulf carriers are hostage to infrastructure limits. The rapid growth trajectory of Emirates (and other airlines operating into Dubai airport) has placed enormous strains on Dubai Airport to expand to accommodate future growth while maintaining day-to-day operational integrity. Added to the expansion of Dubai Airport, a second, massive airport, is in construction nearby, but there is more to the challenge than simply laying concrete. Inevitably Emirates’ remarkable expansion has done wonders for the airport’s growth. For the full year to 31-Dec-2012, Dubai handled just under 57.7 million passengers, making it the fourth largest airport by international traffic, after London Heathrow, Paris Charles de Gaulle and Hong Kong. Unlike its main competitors though, Dubai is still experiencing high growth levels. Passenger numbers exceeded five million for the fourth consecutive month in Mar-2013, handling a record 5.8 million passengers in Mar-2013. Passenger traffic grew a phenomenal 20.6% year-on-year, the highest growth since Aug-2012. Cargo volume increased 14.7% to 213,248 tonnes and aircraft movements increased 8.3% to 31,713 (reflecting both higher load factors and larger gauge aircraft when measured against the much bigger increase in passenger numbers). For the first three months of 2013, passenger traffic increased 15.6% to 14.3 million. According to CAPA’s airport rankings, applying weekly seat capacity from Innovata, Dubai Airport’s international seat offering was at the end of Apr-2013 only 20,000 less than London Heathrow, so Dubai is poised to soon become the biggest international airport in the world. Dubai Airport's world ranking based on weekly seats, ASKs and frequencies: as of 6-May-2013

Source: CAPA – Centre for Aviation and Innovata

28

Dubai International Airport annual passenger traffic and growth rates: 1996 to 2012

Source: CAPA – Centre for Aviation and Dubai Airports Traffic has doubled at Dubai in less than seven years while seat capacity has almost tripled since 2004. The airport is projecting traffic of over 65 million passengers for 2013, an addition of nearly eight million passengers over last year. Traffic at the airport has already outstripped the airport’s own 2010 projections and is now close to a year ahead of estimates. Dubai International Airport passenger traffic growth projection

Note: based on Dubai Airports 2010 estimate Source: CAPA – Centre for Aviation and Dubai Airports The UAE’s open skies policy and the simple fact of increased transfer activity has increasingly attracted foreign airlines to serve Dubai, progressively reducing the total market share that Emirates holds. As partnerships and connectivity opportunities expand, so the share will diminish further.

29

Meanwhile, on CAPA’s rankings, Qatar Airways’ base of Doha Airport is 20th largest globally in international seats offered and Etihad’s home airport Abu Dhabi stands at 35th. With each expanding at similar rates, the pressure on the region’s ANS systems is immense. There is no shortage of funding, or of the political will, to expand the respective airports, but it is the air traffic control systems that are proving the real Achilles heel of the system. Here multinational politics, as always, creeps in. The multiplicity of ANS jurisdictions, along with a substantially reduced airspace thanks to military restrictions, is beginning to inhibit growth, causing sometimes substantial delays. For hub operations this can become a very costly impediment, where on-time arrival and departures are not possible. The problems will be solved, but they are proving complex and time consuming. Shifting the global axis, as access is made easier Emirates will overcome these obstacles, seemingly expanding remorselessly. As the partnership changes filter through the US system and Emirates and friends increase their presence, unthinkable things begin to occur on long-haul connectivity. The carrier’s initial A380 “flagship” deployment strategy was based around key destinations such as New York, London and Sydney, which feature exceptional traffic volumes and a high proportion of premium travellers. Key aviation ‘megacities’ – to borrow Airbus’ term for destinations with more than 10,000 long-haul passengers per day – formed the backbone of the carrier’s A380 network. At present there are 39 of these aviation megacities according to Airbus’ estimates. By 2031, Airbus estimates that this number of aviation megacities will increase to 92, and 95% of long-haul traffic will operate on routes to/from or via these destinations.

30

Meanwhile, the carrier’s ubiquitous 777s serve numerous smaller cities. Once the main city gateways are secured and frequency is locked in, supporting the overall network, the second phase of expansion begins. This next stage, as experienced in Europe, can be even more startling. The second phase of Gulf airline expansion targets regional centres At first when Emirates began serving non-capital “regional” cities such as Manchester and Birmingham in the UK, or even Dublin (with its population of just over a million), there were cries of “capacity dumping”. The market response has generally given the lie to that, as new global one-stop travel opportunities opened up.. Today, Greater Manchester, with a population of around 2.5 million, and only 290km (180 miles) from London, is host to seven widebody services each day from the three Gulf carriers: an A380 and two 777s from Emirates; two A330s from Etihad; and two A330s from Qatar Airways – well over 2,000 seats daily. These airlines have the power to transform the landscape, and not just around major hubs. They are accordingly – and Emirates in particular – highly dangerous competitors and, by the same token, increasingly attractive airline partners. Their expanding presence in the world market will continue to be highly disruptive. As a result, this change process will continue not just to redirect passenger flows, but also to transform the fundamental nature of alliances and partnerships. The past year has proven that, for alliances, the unlikely becomes commonplace and the impossible a reality. Who knows, by this time next year, Emirates may well be Lufthansa’s new best friend. And the distinctive tail, in its UAE colours, will be much better known across the North American continent, as well as the EK code on US airlines’ flight information displays. Partnership conflicts will abound, as new equilbria are built – and rebuilt. And soon it will not just be the major gateways that are chasing Emirates tails.

31

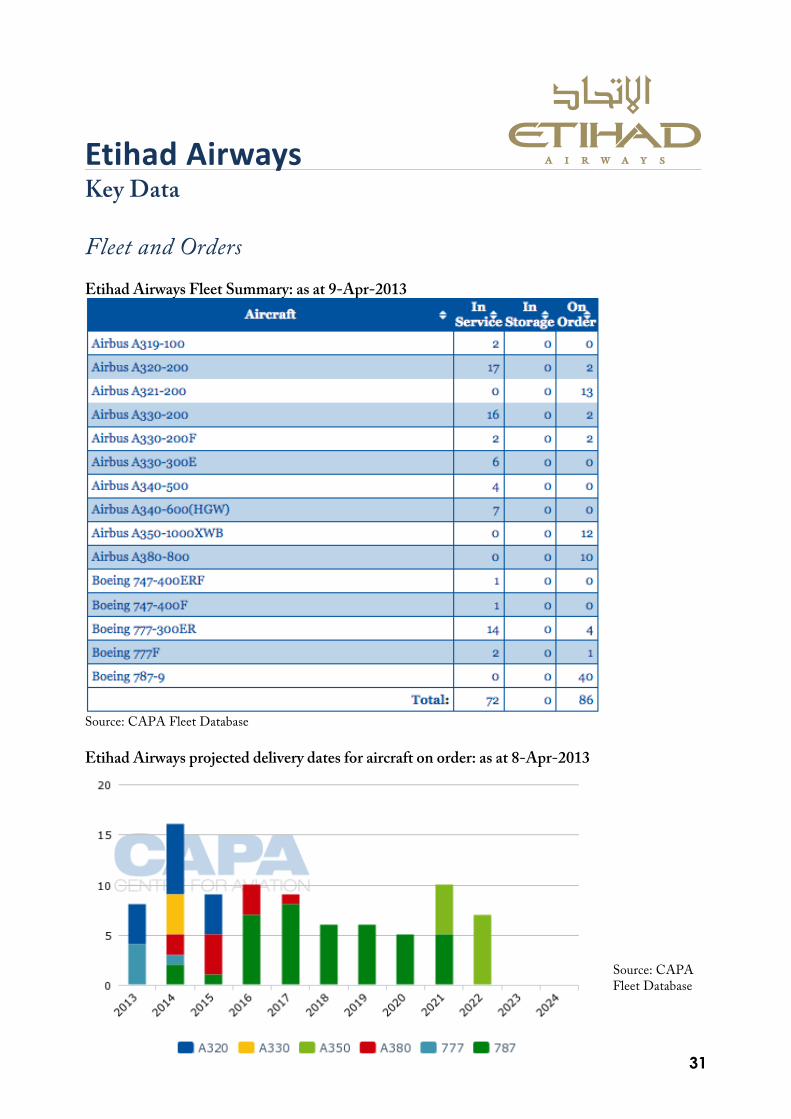

Etihad Airways Key Data Fleet and Orders Etihad Airways Fleet Summary: as at 9-Apr-2013

Source: CAPA Fleet Database

Etihad Airways projected delivery dates for aircraft on order: as at 8-Apr-2013

Source: CAPA Fleet Database

32

Route area pie chart Etihad Airways international capacity seats by region: as at 8-Apr-2013

Source: CAPA - Centre for Aviation and Innovata

Top routes table Etihad Airways top ten international routes by seats: as at 8-Apr-2013

Source: CAPA - Centre for Aviation and Innovata

Premium/Economy profile Etihad Airways schedule by class of seat - one way weekly departing seats: as at 8-Apr-2013 Source: CAPA - Centre for Aviation and Innovata

33

Etihad jolts the status quo again – Jet Airways and (wait for it) Air Canada are its newest partners By purchasing a large minority share in Jet Airways in Apr-2103, Etihad enormously entrenches its long term global position, as it secures intimate access to one of the world’s fastest growing markets. The deal is accompanied by expanded bilateral access and a new US pre-clearance facility at Abu Dhabi Airport. The near-billion dollar deal will not only radically shake up the Indian market – to the substantial disadvantage of now-marooned Air India – but the ramifications will be felt well beyond Indian borders.

And right on the heels of this announcement comes the remarkable news that staunch Gulf airline opponent Air Canada is to codeshare with….Etihad. For now the scope is limited – but it will expand, as Etihad’s virtuous circle spreads.

With the far-reaching purchase of Jet Airways, the UAE is entrenched as India’s main international hub, although as Etihad/Jet expands, Emirates’ powerful position in the Indian market will be eroded.

Other sixth freedom airlines, notably Lufthansa, whose gateway access is limited to a handful of points and is subject to capacity controls, will see their roles significantly diluted.

Etihad's growing virtuous circle develops: a remarkable sequence

Etihad is moving so fast to tie up new arrangements, almost all of which are ground-breaking in their own right, that it becomes increasingly hard to interpret the implications – there are so many new permutations being created with each new move. But, assuming that the array of deals can be effectively managed, the momentum is now such that it is almost creating a virtuous circle.

Each piece that “UAE’s national airline” now adds to its jigsaw of alliance relationships begins to have – usually very positive – knock on impacts for other partnerships.

For example, as CAPA has previously wondered aloud, what happens in the American Airlines “love triangle”? Here American, recently bought by US Airways, is at the apex of all three major Gulf carriers.

Close partner Qantas/oneworld has eloped with Emirates; and equally close British Airways/Iberia have tied up with Qatar Airways. American is at the heart of oneworld’s US market access. Yet Etihad has a vital (for Etihad) and extensive codeshare arrangement with American. Although today’s world is becoming much more complex than a contest between the apparently simple three global alliance teams, it strains credibility that American could have a deep and meaningful relationship with all three, Emirates, Etihad and Qatar. Alliance promiscuity can only go so far before conflict arises; but today's question perhaps becomes more about how to manage that conflict rather than how to avoid it.

Until the Jet Airways purchase – and an extremely important Abu Dhabi US pre-clearance agreement – Etihad looked like an easy call for American to walk away from. Not any more.

34

The combination of easy US passenger access and a much stronger hold on the large and growing Indian market not only makes Etihad much more attractive for American, but also Abu Dhabi soars as a desirable transfer point. In this respect, there are few better holistic examples of airline-airport-government policy working together. European governments take note.

The US-India market is not small, with around a million passengers in each direction and roughly evenly distributed origin and destination; importantly it is growing fast – and US airlines have a relatively small part of the action. Non-stop service is possible, but to establish a combination of frequency and city pair access, intermediate stops outside India will remain an attractive proposition. If pre-clearance is possible too, the attraction of Etihad and Abu Dhabi increases considerably.

India-US in one-way passenger numbers

Source: IATA MarketIS

The Etihad-Jet Airways deal, 24-Apr-2013 in a nutshell:

• Etihad will invest USD600 million in Jet Airways; • This includes an equity investment of USD379 million, giving Etihad Airways 24% of an

enlarged share capital of Jet Airways; • A further USD220 million will be injected “to create and strengthen a wide-ranging

partnership between the two carriers”. As part of this Etihad Airways previously announced it had paid USD70 million to acquire Jet Airways’ three pairs of Heathrow slots through the sale and lease back agreement announced on 27-Feb-2013. Jet Airways continues to operate flights to London utilising these slots;

• Etihad will also invest USD150 million to buy a majority equity share in Jet Airways’ frequent flyer programme "Jet Privilege". Etihad has majority ownership of airberlin’s frequent flyer programme too. And Etihad has leased two A330s from Jet;

35

• Codeshare expansion will significantly extend Etihad’s reach into India’s fast growing 42 million passenger travel market, feeding Etihad’s Middle East, North American and European destinations, and opening up Jet Airways' access from up to 23 Indian cities;

• An expanded India-UAE bilateral access agreement gives Jet the lion's share of almost 40,000 new seats weekly;

• Together the carriers will establish “a Gulf gateway for flights to the US, Europe, Africa and the Middle East”;

• The respective frequent flyer programmes will be "fully integrated", with reciprocal ‘earn-and-burn’

Jet Airways’ future is now assured, if India's politicians deliver

In an overall deal encompassing around a billion dollars, Jet Airways’ previously fragile position is greatly enhanced. The size and scope of the agreement also means that Etihad will seek to ensure that the partnership will work to their mutual benefit.

Accompanying the purchase arrangements, an essential part of the equation was to secure adequate support from the Indian government too.

India has a sad reputation when it comes to practical implementation of foreign investment measures introduced by its relatively forward looking leaders, so Etihad and its government owners were anxious to ensure that this major addition to the airline’s armoury would not be unravelled by the usual prevarication and obstacles. The UAE had previously fallen foul of India’s waywardness (with a negative experience by the UAE telco in India), and so was seeking an Investment Protection Treaty; however because these can take a long time to negotiate it was eventually dropped as a pre-condition, but remains on the agenda.

Expanded UAE-India bilateral access sealed the deal

However bilateral access became a central feature of the deal. If Etihad was to spend several hundred million dollars buying into Jet, it was essential that they be able to leverage market access. India and Abu Dhabi agreed to the revised bilateral agreement shortly before announcement of the purchase, and within 24 hours the Jet-Etihad deal went ahead. The short-notice negotiations displeased some in the Indian industry, but is merely another example of India’s ad-hoc “policy” implementation.

Under the revised terms, each side has been granted an additional 36,670 weekly seats, taking the current 13,330 entitlements to just 50,000. The increased entitlements will be phased in over a period of two years, with 11,000 additional seats effective immediately. There are now 23 designated points of call in India – all of them in principle available for use by the Jet-Etihad partnership.

The bilateral agreement does still have to be approved by Cabinet and, given the likely severe impact on Air India, political opponents will undoubtedly seek to exploit this as a reason for reneging on the deal. Prime Minister Manmohan Singh has however continually stressed the importance to India’s overall interests in abiding by its international commitments, as repeated failure to do so in the past has seriously jeopardised inbound investment.

Also, the other Gulf carriers, along with European carriers, are likely to seek additional concessions, apart from increased seats, as a result; for example, Lufthansa and Emirates are

36

currently not permitted to deploy A380s in the Indian market and will almost certainly now request that access. Meanwhile too, Turkish Airlines is seeking an increase to 56 weekly frequencies (to allow double dailies to each of the six main cities). Previously, Etihad, Emirates, Air Arabia and Qatar Airways had together been seeking approximately 150,000 additional weekly seats in total, so it can be expected that the noise will intensify now.

Agreement on US pre-clearance in the UAE will also be a major asset for Abu Dhabi Airport and for Etihad

The intricate details accompanying this major move by Etihad further enhance the value of the Jet purchase to Etihad and the UAE. Important among these is a US-UAE agreement to establish a US Customs and Border Protection (CBP) pre-clearance facility at Abu Dhabi International Airport. The US is India’s biggest air market by far and Indian (and US) travellers are forced to endure the less than tender mercies of America’s immigration and security authorities. If these processes can be provided in a civilised way by flying through Abu Dhabi, that is an enormous incentive for travellers to use the joint services of Etihad/Jet Airways.

There are currently 15 CBP pre-clearance facilities in Canada, Ireland and the Caribbean and all have been well patronised.

Understandably, this has already invoked the envy – and wrath – of European airlines, whose trade body, the Association of European Airlines (AEA) has argued this will provide a competitive advantage to Etihad Airways and will be "detrimental to a level playing field in the transatlantic aviation market…European airlines are forced to change their flight schedules in order to avoid rush hours at the customs clearance in the USA, putting connectivity, commercial opportunities and passenger convenience at stake. The measure in Abu Dhabi has a distortive effect on the liberalised EU-US transport market, which is the largest in the world with clear benefits to industry, consumers and the economy. AEA calls on constructive discussions between the respective parties in order to deal with this issue and to avoid further conflicts."

While this neglects to point out that the exclusive US-Europe liberalisation had also previously delivered a powerful advantage to European airlines, it also sends a message to European governments to work to support the interests of their national industries – airports and airlines.

Meanwhile, US airline pilots, always fast to jump at any improvement in the system that could possibly affect their well-being, have, through the Air Line Pilots Association (ALPA), actually called on the US government to repeal the agreement. The Association is, somewhat quaintly, concerned that no US airline currently services Abu Dhabi and therefore cannot benefit from it (although US airlines will now certainly see the agreement as an added incentive to operate to the airport). ALPA argued the US government was "putting US airlines and American jobs at great risk" with the agreement and called on Congress to act if the Department of Homeland Security does not rescind the agreement.

The Air Canada codeshare is potentially a major breakthrough for Etihad

Following an acrimonious aviation policy dispute between the governments of Canada and the UAE which resulted in a series of diplomatic spats, peace has now been restored and Air Canada has tentatively embarked on a whole new realpolitik course. A staunch member of the Star Alliance, Air Canada has strictly adhered to the historic application of bilateral air services terms,

37

where capacity is to be allocated reciprocally, based on third and fourth freedom traffic flows (these are the provisions described by a former IATA CEO as “archaic”; most countries now regard consumer interests ahead of flag carrier protection).

The codeshare announced by both airlines on 25-Apr-2013 relates mainly to these end-to-end flows, with long-haul reciprocal codesharing limited to the Toronto-Abu Dhabi sector, both non-stop and via London. Etihad also has codeshares on Air Canada metal over Toronto. One result is apparently to allow Etihad effective daily service to Toronto; its capacity-limited three times weekly non-stop service to Toronto will now be able to be augmented by one-stop codeshare operation on Air Canada over London. If the London routing is to be useful this would however imply that Canada is now prepared to grant Etihad additional one-stop capacity. Technically, the two parties have "signed a Memorandum of Understanding (MoU) for a commercial cooperation agreement", so it is still subject to potentially substantial elaboration.

But – and here again the magic of the virtuous circle may come into play – once Etihad/Jet is able to deliver high levels of traffic from 23 points in India, the proposition for Air Canada to become more intimate with Etihad becomes very powerful. Currently, Air Canada does not serve the large Indian market non-stop, preferring to codeshare on – once again, the virtuous circle – Jet Airways over London. It also connects with Lufthansa over Frankfurt and Swiss over Zurich.

According to the airlines’ media releases, “the two parties have commenced discussions to finalise details with the objective of introducing codeshare services in the third quarter 2013.” It would not be fanciful to think that the passage of another few months will see further evolution of this fast moving alliance scene, as Jet falls increasingly into line with a wider Etihad strategy. There will now be much for Air Canada to gain from a closer relationship with Etihad, in ways that its Star partners may not be able to deliver, both in India and elsewhere.

Domestically, Air India, along with Delhi and Mumbai Airports lose ground – but the wider outcome is generally positive

Etihad’s investment was made possible since India recently, after much delay, moved to allow expanded foreign airline ownership of Indian carriers. Ironically, the long delay in introducing the change was mostly due to Jet Airways’ influential opposition, as it feared that its own position would be eroded if other airlines like Kingfisher were strengthened by receiving foreign airline support.

Now, in the current circumstances, with Kingfisher out of the picture, the impact of the Etihad-Jet combination will be devastating for the country’s largest international carrier, Air India, just as it was starting to show signs of improvement.

The logical response, if it is unable to compete, is to allow Air India to fail – or at least drastically downsize – but logic is rarely the first refuge when national flag carriers are concerned. Nonetheless it will become increasingly difficult to justify injecting a billion dollars a year into an airline that now has a negligible prospect of independent survival, now that Jet has been so substantially empowered. And, so long as the Indian Government's policy incoherence continues, there is little hope for a reversal. This surely must be the last nail in the flag carrier’s coffin.

38

And Etihad continues, criss-crossing the global alliances with its 'new business model'

Although India is the object of this week's developments, the real story here is however Etihad's remarkable expansion path. Aside from the investment in Jet Airways, over the past year Etihad has acquired stakes in airberlin (nearly 30%), Air Seychelles (40%), Virgin Australia (8.56%) and Aer Lingus (nearly 3%), the airline "will continue to explore opportunities where they make financial and strategic sense", according to CEO James Hogan, who believes “the new business model delivers benefits which previously were available only through full mergers or acquisitions”. The high level of involvement in Air Seychelles for example (which announced an important codeshare with South African Airways on 25-Apr-2013) has de facto provided additional market access for Etihad in capacity limited Hong Kong, as well as generally being a highly positive outcome for the Seychelles' previously ailing airline.

Etihad’s equity ownership

Airline Region Shareholding airberlin Europe 30% Aer Lingus Europe 3% Air Seychelles Africa 40% Jet Airways South Asia 24% Virgin Australia South Pacific 8.6% (Note: Etihad has non-equity based codeshares with another 40 airlines)

In addition to these direct equity stakes in its airline partners, Etihad has also been quietly accumulating majority shareholdings in the frequent flyer programmes of some of its acquisitions (although foreign airline ownership is subject to restrictions, no such inhibition exists on FFPs). Etihad's growing network creates synergies that expand the value of the programmes, while at the same time making them available for data mining. As loyalty programmes assume greater intrinsic value, the possibilities in this still relatively young marketplace may be extensive.

The fast pace of Etihad's ascension to a major player and game changer has been accompanied by this suite of equity investments and, while the efficacy of minority shareholding connections remains unproven in the airline industry, it increasingly appears that Etihad's combination is working well for it. Notably, where the airline invested in is in a weaker position, Etihad's ability to deliver it sustainability creates a greater reliance on the UAE flag carrier – and therefore the minority shareholding takes on greater significance, almost in proportion to the weakness of the acquired airline.

In the process of establishing its partnerships, equity or otherwise, Etihad, like its Gulf siblings, has been careless of global alliance affiliations; relations with the leader of SkyTeam, Air France-KLM, go side by side with its extensive codeshares with oneworld's American and its acquisition of oneworld's airberlin; Star Alliance members, led by arch enemy Lufthansa, have been more resistant, but a budding partnership with Air Canada may alter that status, along with its proxy codeshare with SAA through Air Seychelles.

The result, for the global system, is disruption, something the airline industry badly needs if it is to move towards profitability. That path will not be smooth and not all can follow it, but it is surely inevitable sooner or later.

39

flydubai Key Data Fleet and Orders flydubai Fleet Summary: as at 9-Apr-2013

Source: CAPA Fleet Database

flydubai projected delivery dates for aircraft on order: as at 8-Apr-2013

Source: CAPA Fleet Database

Route area pie chart flydubai international capacity seats by region: as at 8-Apr-2013

Source: CAPA - Centre for Aviation and Innovata

40

Top routes table flydubai top ten international routes by seats: as at 8-Apr-2013

Source: CAPA - Centre for Aviation and Innovata

Premium/Economy profile flydubai schedule by class of seat - one way weekly departing seats: as at 8-Apr-2013

Source: CAPA - Centre for Aviation and Innovata

41

flydubai has bright outlook after recording first profit and emerging as close partner to Emirates flydubai has recorded its first annual profit and is preparing more rapid expansion for 2013 and beyond. flydubai, which has already surpassed Sharjah-based Air Arabia as the largest low-cost carrier in the Middle East based on seat capacity, is now looking at placing a new order for 50 narrowbody aircraft. It is already committed to growing its fleet from a current 28 737-800s to at least 50 aircraft by the end of 2015. flydubai has grown rapidly since being launched in 2009 by the Dubai government, which also owns Emirates. Over the years it has adopted a hybrid model which allows it to fill, in some respects, a role as a regional carrier for its bigger full-service sister carrier. The hybrid approach has resulted in rapid and profitable expansion as flydubai has entered short and medium-haul markets that are too small for Emirates’ all-widebody fleet but in many cases have sufficient yields to support a full-service carrier. At the same time flydubai has been able to stimulate demand by offering low fares and is able to successfully operate alongside Emirates on some of the biggest routes within the Middle East. flydubai has been in the black since 2H2011 flydubai reported on 13-Feb-2013 that it turned a net profit of AED152 million (USD41 million) in 2012 on AED2,778 million (USD756 million) in revenues. The carrier says its EBITDAR operating profit margin reached 24% as passenger traffic exceeded five million. flydubai, which did not report figures for 2011, says it has been consistently in the black since 2H2011, or just over two years after its Jun-2009 launch. The carrier has quickly proven the need for a LCC in the fast-growing Dubai market, carrying 10.4 million passengers since its launch. It already links Dubai with 51 destinations, with two more destinations to be added in Mar-2013. More destinations are expected to be added later in 2013 along with capacity expansion to several existing markets as six additional aircraft are added for a total of 34 737-800s. The opportunities for further capacity expansion are tremendous as about half of flydubai’s routes are served with less than daily frequency. The demand will be there to support more frequencies as in many cases these are fast-growing emerging markets that are under-served and would benefit from increased connectivity with Dubai, and therefore the Emirates network. Slightly over half of flydubai’s destinations are not currently served by Emirates. While flydubai now has more destinations outside the Middle East than within the Middle East most of its capacity is still within the Middle East as its routes within the region are served much more frequently. flydubai currently allocates 70% of its seat capacity to its 21 routes within the Middle East, including about 55% within the Gulf Cooperation Council (GCC). The rest of its capacity is mainly allocated to South Asia (nine routes and 13% of seat capacity) and Eastern Europe (14 routes, primarily to Russia and other CIS countries, and 10% of capacity). The remaining

42

capacity is allocated to Africa (five routes and 5% of seat capacity) and Central Asia (two routes and 2% of capacity). flydubai capacity share (% of seats) by region: 18-Feb-2013 to 24-Feb-2013

Source: CAPA – Centre for Aviation & Innovata flydubai stated in its 2012 earnings release that its traffic within the GCC – which includes the UAE, Bahrain, Kuwait, Oman, Qatar and Saudi Arabia – grew by 63% in 2012. According to CAPA and Innovata data, flydubai now has a 26% share of capacity from the UAE to Kuwait, 23% to Qatar, 22% to Saudi Arabia, 19% to Oman and 16% to Bahrain. It is currently the largest low-cost carrier in each of these markets. flydubai stated that the total size of this market grew by 21% in 2013. Most of this growth occurred between the UAE and Saudi Arabia, which is by far the largest country pair within the GCC. According to CAPA and Innovata data, the UAE-Saudi Arabia market has seen a 46% increase in capacity over the last year to over 180,000 weekly return seats. The other UAE-GCC markets have seen modest increases or flat capacity over the last year. flydubai now serves nine destinations in Saudi Arabia In Saudi Arabia, flydubai has been successful at operating alongside Emirates on trunk routes and building up an operation in secondary markets that are not served by Emirates. Riyadh, Jeddah and Dammam are among flydubai’s 10 largest routes and are each served with between three and four daily frequencies. Emirates also serves these three destinations with roughly a similar number of frequencies. flydubai also now serves six secondary destinations in Saudi Arabia following the 13-Feb-2013 launch of service to Ha’il, joining Abha, Qassim, Taif, Tabuk and Yanbu. flydubai is currently the only carrier linking Dubai with any of these destinations in Saudi Arabia. Rival Air Arabia only serves half of these six destinations – Qassim, Taif and Yanbu – from its hub at Sharjah, which is only about 30km from Dubai. flydubai has nearly doubled seat capacity to Saudi Arabia over the last year from about 10,400 weekly one-way seats to just over 20,000 currently, according to CAPA and Innovata data. Its 22% share of the UAE-Saudi Arabia market is second only to Emirates’ 26% capacity share.

43

Saudia is now smaller, with a 20% share, while the two other LCCs in the market, Air Arabia and Saudi Arabia-based NAS Air, only have a 12% and 7% share respectively. Saudi Arabia is the second largest market from the UAE after India. In late 2011, flydubai was only the fifth largest carrier in the UAE-Saudi Arabia market, behind Emirates, Saudia, Etihad and Air Arabia. UAE to Saudi Arabia capacity by carrier (one-way seats per week): 19-Aug-2012 to 11-Sep-2013

Source: CAPA – Centre for Aviation & Innovata flydubai helps Emirates compete against Qatar Airways in key Dubai-Doha market In the other GCC markets flydubai has been used to help its sister carrier compete with other Gulf carriers. As Emirates is the only Gulf carrier that does not have narrowbody aircraft in its fleet, Emirates in some cases is not able to offer the frequencies that competing carriers can offer. Frequencies are key in the intra-GCC market as business passengers make short trips within the region, often just for the day. For example between Dubai and Doha in Qatar, flydubai now operates nine daily frequencies while Emirates operates six. Qatar operates 11 daily frequencies, using a mix of widebody and narrowbody aircraft, giving it a better schedule than rival Emirates but less than Emirates and flydubai combined.

44

Doha is the largest destination from Dubai based on seat capacity with over 37,000 weekly one-way seats. Doha-Dubai is the largest route based on seat capacity for Qatar Airways, the second largest for flydubai after Kuwait and the second largest for Emirates after London Heathrow. The three carriers have almost identical capacity on the route, with Qatar Airways accounting for 33% of capacity, Emirates 32% and flydubai 31% (United Airlines accounts for the remainder). Dubai-Doha is currently the seventh largest international route in the world, according to CAPA and Innovata data. In the broader UAE-Qatar market, Qatar has a leading 37% share of capacity. Emirates has a 24% share and flydubai 23%, giving the duo a strong 47% share. Air Arabia accounts for less than 5% of total capacity between the two countries. UAE to Qatar capacity by carrier (one-way seats per week): 19-Aug-2012 to 11-Sep-2013

Source: CAPA – Centre for Aviation & Innovata flydubai also helps Emirates compete against Oman Air and Gulf Air Between Dubai and Muscat in Oman, flydubai now offers four frequencies on most days compared to only two daily frequencies for Emirates. Combined, flydubai and Emirates are nearly able to match the schedule of Oman Air, which offers seven daily frequencies using a mix of 737s and Embraer E175 regional jets.

45

Oman Air is the largest carrier in the Oman-UAE market with a 28% share, compared to 19% for flydubai and 15% for Emirates. But on just the Dubai-Muscat route, flydubai has a leading 33% share of capacity, while Oman Air has a 32% share and Emirates has a 24% share (with the remaining 11% share held by SWISS). UAE to Oman capacity by carrier (one-way seats per week): 19-Aug-2012 to 11-Sep-2013