mifid ii academy: suitability and other non-complex financial instruments mifid ii academy -...

TRANSCRIPT

MiFID II Academy:

Suitability and appropriateness

Floortje Nagelkerke

9 February 2016

2017 2016 2015 2014

2 July

MiFID II and MiFIR

entered into force

1 August

Level 2 Consultation on

advice on delegated acts

and Discussion Paper on

technical standards

closed

19 December

Level 2 Consultation on

technical standards

commenced. ESMA

provided final report on

technical advice to the

Commission on delegated

acts

2 March

Level 2 Consultation

on technical

standards closed

28 September

Level 2 regulatory

technical standards

submitted to

Commission (delayed

from 3 July)

3 January

Level 2

implementing

technical standards

to be submitted to

Commission

3 July

Member States to

adopt and publish

measures transposing

MiFID II into national

law

3 January

MiFID II and MiFIR

Level 1 and Level 2

implementation date

Will likely be postponed

till at least January

2018

Consultation

period

Consultation

period

June

Ministry of Finance to

publish final rules

MiFID II / MiFIR Level 2 Timeline

6 June

Consultation

implementation AFS

MiFID II Academy - Suitability and appropriateness - 9 February 2016 2

Dutch transposition

MiFID II Academy - Suitability and appropriateness - 9 February 2016

MiFID II implementation

• Article 93 MiFID II: Member States shall adopt and publish, by 3 July 2016, the laws, regulations and administrative provisions necessary to implement this Directive

• Consultation Ministry of Finance July 2015

– closed on 6 July 2015

– Lot of the detail will be implemented into the Besluit Gedragstoezicht financiele ondernemingen Wft

– All RTS/ITS will be regulations which will have direct effect into Dutch law

• How to keep informed:

– AFM MiFID review page - https://www.afm.nl/nl-nl/professionals/onderwerpen/mifid-ll

– http://www.regulationtomorrow.com/the-netherlands/

– http://www.nortonrosefulbright.com/knowledge/technical-resources/pegasus/norton-rose-fulbright-briefings-slides-and-webex-recordings/

– http://ec.europa.eu/finance/securities/isd/mifid2/index_en.htm

– http://www.esma.europa.eu/page/Markets-Financial-Instruments-Directive-MiFID-II

3

Suitability

Suitability under MiFID II

• EU sources

• Article 25 (2) of MiFID II

• Final report ESMA 19 December 2014 in combination with articles 35 and 37 of the MiFID Implementing Directive

• Dutch sources

• Article 4:23 Act on the Financial Supervision

• Article 80a and 80c Decree Supervision on Conduct of business

5 MiFID II Academy - Suitability and appropriateness - 9 February 2016

When needs a suitability test be done?

• The rules apply to firms that provide:

• investment advice (whether independent or not) to clients; or

• portfolio management to behalf of clients

• Firms must obtain the following information from a client or a potential client before providing the above services:

– its knowledge and experience of the investment field in which the investment advice or portfolio management is to be offered;

– its financial situation including his ability to bear losses; and

– its investment objectives including the risk tolerance.

• Obligation to take reasonable steps to ensure that investment advice and decisions to trade (incl. to buy or to hold) are suitable

• If limited range of instruments/investment choices and these are not suitable: no recommendation

• Obligation also applicable to a package of services or bundled products and structured deposits

6 MiFID II Academy - Suitability and appropriateness - 9 February 2016

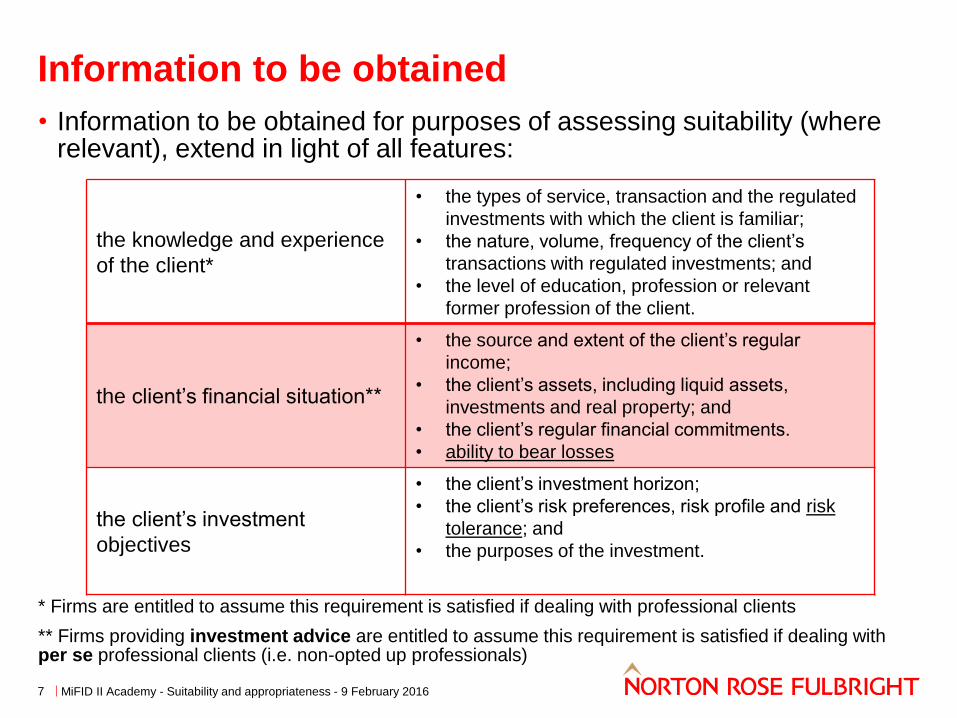

Information to be obtained

7

• Information to be obtained for purposes of assessing suitability (where relevant), extend in light of all features:

* Firms are entitled to assume this requirement is satisfied if dealing with professional clients

** Firms providing investment advice are entitled to assume this requirement is satisfied if dealing with per se professional clients (i.e. non-opted up professionals)

the knowledge and experience

of the client*

• the types of service, transaction and the regulated

investments with which the client is familiar;

• the nature, volume, frequency of the client’s

transactions with regulated investments; and

• the level of education, profession or relevant

former profession of the client.

the client’s financial situation**

• the source and extent of the client’s regular

income;

• the client’s assets, including liquid assets,

investments and real property; and

• the client’s regular financial commitments.

• ability to bear losses

the client’s investment

objectives

• the client’s investment horizon;

• the client’s risk preferences, risk profile and risk

tolerance; and

• the purposes of the investment.

MiFID II Academy - Suitability and appropriateness - 9 February 2016

Requirements suitability assessment (1)

8

• responsibility for carrying out assessment lies with firms

– inform clients clearly and simply reason for assessment is to enable it to act in the client’s best interest

– apply to simplified advice models e.g. through automated or semi-automated systems

• applies to all recommendations

– including when advising to sell, buy or hold instruments

• policies and procedures needed so firms understand the nature, features of instruments , incl. costs and risks, and to assess, while taking into account costs and complexity, whether equivalent financial instruments could meet client’s profile.

– no need to explicitly consider if lower cost or less complex products more suitable, “just” whether alternative financial instrument more suitable

– no detailed consideration individual instruments from across all types or classes; compare individual instruments from within firm’s range that are broadly equivalent (e.g. two or more UCITS investing in same sector)

• if switching (buy/sell/exercise right): benefits must outweigh costs

MiFID II Academy - Suitability and appropriateness - 9 February 2016

Requirements suitability assessment (2)

9

• maintain adequate and up-to-date information in an on-going relationship

• ensure information is reliable

– Ensure clients awareness of importance accurate and up-to-date information

– Undertaking valid and reliable assessments client’s knowledge, experience and risk tolerance

– Tools are appropriately designed for use and fit-for-purpose

– Questions should be understandable, capture accurate reflection of client’s views and needs and information is necessary

– Ensure consistency of information

• Firms can rely on information provided by its clients unless they are aware that it is manifestly out of date, inaccurate or incomplete.

• If a firm does not obtain the necessary information to assess suitability, it must not make a personal recommendation or take a decision to trade

MiFID II Academy - Suitability and appropriateness - 9 February 2016

Suitability report

10

• Firms must provide retail advisory clients with a suitability report

• with outline of the advice given

• specifying how the advice is suitable, including how it meets

• client’s objectives and personal circumstances with reference to investment term required

• client’s knowledge and experience

• Client’s attitude to risk and capacity for loss

• based on the recommended instruments identify if periodic review needed

• if periodic suitability assessments and reports are provided:

• subsequent reports after the initial service would only need to cover any changes in the instrument(s) and/or the circumstances of the client.

• no repetition of all detail of the first report.

• simply refer back the original report to a varying degree depending on any changes

• could be shorter in cases where the on-going assessment affirms the continued suitability of a previous recommendation or portfolio.

MiFID II Academy - Suitability and appropriateness - 9 February 2016

Appropriateness

Appropriateness under MiFID II

• EU sources

• Article 25 (3) and (4) of MiFID II

• Final report ESMA 19 December 2014 in combination with articles 36, 37 and 38 of the MiFID Implementing Directive

• Final Report 26 November 2015 Guidelines on complex debt instruments and structured deposits

• Dutch sources

• Article 4:24 Act on the Financial Supervision

• Article 80b, 80c and 80d Decree Supervision on Conduct of business

12 MiFID II Academy - Suitability and appropriateness - 9 February 2016

When needs an appropriateness test be done?

13

• The rules apply to firms that:

• Receive and transmit orders

• Execute orders

• Deal on own account

• Underwrite and place financial instruments

• Firms must obtain information regarding their clients’ experience and knowledge in order to enable the firm to determine if the products and services envisaged are appropriate

– the types of financial service, transaction and regulated financial instruments the client is familiar with;

– the nature, volume and frequency of the client’s transactions in regulated financial instruments; and

– the level of education, profession or former profession of the client.

• Obligation also applicable to a package of services or bundled products and structured deposits

• Firms may assume that the appropriateness test is satisfied if dealing with professional clients, and not applicable to ECPs

MiFID II Academy - Suitability and appropriateness - 9 February 2016

No test for appropriateness necessary

14

• when providing the service: RTO or execution of orders; and

• no credits/loans/overdrafts are involved; and

• (Potential) clients’ initiative; and

• client must have been clearly informed (may be given in a standardised format) that, in the provision of the service:

• the firm is not required to assess the suitability of the instrument or service provided or offered; and

• therefore, the client does not benefit from the protection of the rules on assessing suitability

and

• the firm must comply with its obligations in relation to conflicts of interest; and

• the financial instruments are non-complex.

MiFID II Academy - Suitability and appropriateness - 9 February 2016

Non-complex product

15

• shares admitted to trading on a regulated market or on an equivalent third-country market or on a MTF, where those are shares in companies, and excluding shares in non-UCITS collective investment undertakings and shares that embed a derivative;

• bonds or other forms of securitised debt admitted to trading on a regulated market or on an equivalent third country market or on a MTF, excluding those that embed a derivative or incorporate a structure which makes it difficult for the client to understand the risk involved;

• money-market instruments, excluding those that embed a derivative or incorporate a structure which makes it difficult for the client to understand the risk involved;

• shares or units in UCITS, excluding structured UCITS as referred to in the second subparagraph of Article 36(1) of Regulation (EU) No 583/2010;

• structured deposits, excluding those that incorporate a structure which makes it difficult for the client to understand the risk of return or the cost of exiting the product before term;

(Please note ESMA’s comment: The above products are complex and not able to be assessed by the additional test for non-complex products)

• other non-complex financial instruments

MiFID II Academy - Suitability and appropriateness - 9 February 2016

Test for other non-complex products

16

• The instrument is not a derivative

• Frequent opportunities to dispose of, redeem, or otherwise realise the instrument at prices that are publicly available to market participants and that are either market prices or prices made available, or validated, by valuation systems independent of the issuer

• It does not involve any actual or potential liability for the client that exceeds the cost of acquiring the instrument

• Adequately comprehensive information on its characteristics is publicly available and is likely to be readily understood by the average retail client

• Additional test for non-complex products:

(1) does not include clause / condition / trigger that fundamentally alters the nature or risk of the investment or pay out profile

(2) does not include explicit or implicit exit charges with the effect of making the investment illiquid

MiFID II Academy - Suitability and appropriateness - 9 February 2016

Recordkeeping assessments

17

Firms shall maintain records of the appropriateness assessments

These records should include:

• the result of the appropriateness assessment;

• any warning given to the client where the investment service or product purchase was assessed as potentially inappropriate for the client, whether the client asked to proceed with purchase despite the warning and, if applicable, whether the firm accepted the client’s request to proceed with the purchase; and

• any warning given to the client where the client did not provide sufficient information to enable the firm to undertake an appropriateness assessment, whether the client asked to proceed with purchase despite this warning and, if applicable, whether the firm accepted the client’s request to proceed with the purchase.

MiFID II Academy - Suitability and appropriateness - 9 February 2016

Disclaimer Norton Rose Fulbright LLP, Norton Rose Fulbright Australia, Norton Rose Fulbright Canada LLP, Norton Rose Fulbright South Africa (incorporated as Deneys Reitz Inc) and Fulbright & Jaworski LLP, each of which is a separate legal entity, are members (‘the Norton Rose Fulbright members’) of Norton Rose Fulbright Verein, a Swiss Verein. Norton Rose Fulbright Verein helps coordinate the activities of the Norton Rose Fulbright members but does not itself provide legal services to clients.

References to ‘Norton Rose Fulbright’, ‘the law firm’, and ‘legal practice’ are to one or more of the Norton Rose Fulbright members or to one of their respective affiliates (together ‘Norton Rose Fulbright entity/entities’). No individual who is a member, partner, shareholder, director, employee or consultant of, in or to any Norton Rose Fulbright entity (whether or not such individual is described as a ‘partner’) accepts or assumes responsibility, or has any liability, to any person in respect of this communication. Any reference to a partner or director is to a member, employee or consultant with equivalent standing and qualifications of the relevant Norton Rose Fulbright entity.

The purpose of this communication is to provide information as to developments in the law. It does not contain a full analysis of the law nor does it constitute an opinion of any Norton Rose Fulbright entity on the points of law discussed. You must take specific legal advice on any particular matter which concerns you. If you require any advice or further information, please speak to your usual contact at Norton Rose Fulbright.

MiFID II Academy - Suitability and appropriateness - 9 February 2016 19