miller motor co. inventory sampling problem.cmiller/446_01/projects... · the purpose of this...

TRANSCRIPT

1

Miller Motor Co. inventory sampling problem. The following formula will calculate the required sample size. You can memorize this

the night before the test. (𝒁𝜷+𝒁𝜶

𝟐⁄ )𝒔𝒙

𝑻𝑴̅̅ ̅̅ ̅= √𝒏 𝒁𝜷 => 𝜷 𝑟𝑖𝑠𝑘, Risk of Incorrect Acceptance

𝒁𝜶/𝟐 => 𝜶 𝑟𝑖𝑠𝑘, Risk of Incorrect Rejection

Now, let’s try to learn something about sampling.

The purpose of this assignment is to demonstrate how statistical theory helps auditors manage detection risk. This exercise uses mean-per-unit (MPU) sampling because MPU was covered in your statistics class. MPU sampling also clearly illustrates the relationship between sample size and risk. All accounting firms use software incorporating sophisticated sampling techniques such as: probability proportionate to size, dollar-unit sampling and stratified sampling. These methods reduce audit cost because they typically require smaller sample sizes than MPU sampling. However, the underlying theory is more complicated. This assignment utilizes basic confidence intervals and hypothesis tests covered in introductory statistics classes.

A secondary objective is to familiarize you with “audit documentation” or “work papers.”

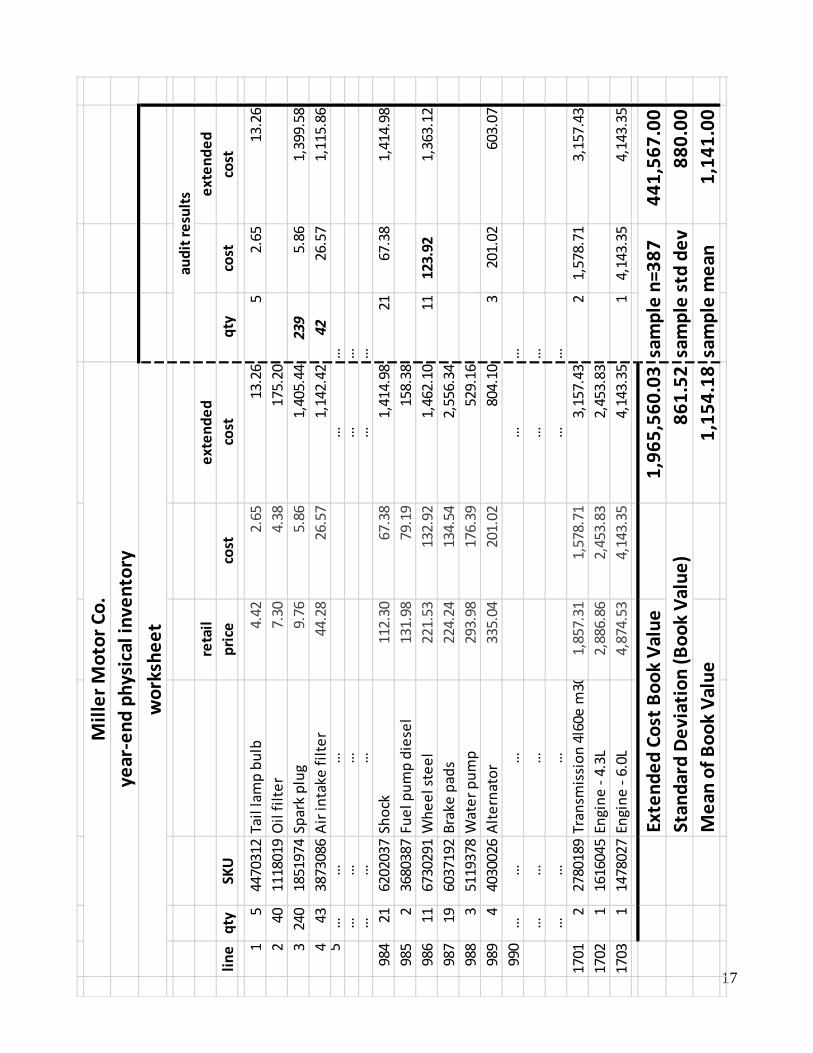

Miller Motor Co.’s “year-end physical inventory worksheet” has two sections. The top section includes 1,703 different parts or SKU (stock keeping unit) numbers. The second section includes the 4 different models of new vehicles in their inventory. The auditors are auditing the parts inventory separately from the vehicle inventory. Auditing the two inventories separately is a simple form of stratification. Including tail lamp bulbs that cost $13.26 in the same pool as Impalas LTZs that cost $86,199.00 would result in a very large standard deviation (and variance). The formula at the top of the page demonstrates that for any level of risk the required sample size increases as the standard deviation (variance) increases.

Although this exercise does not involve any further stratification, notice that the parts prices vary a great deal. Auditors might be able to reduce the required sample size by separating parts that cost more than $1,000 from parts costing less than $1,000. Accounting firms have software to determine the optimal strata to minimize the required sample size for inventory observations.

Designing a sampling plan requires careful consideration. Review the two examples for new vehicles on the back of the “year-end physical inventory worksheet.” We shouldn’t assume that grouping items always reduces the standard deviation. In the case of the new vehicles, the standard deviation is higher when the cars are grouped by model than when each vehicle is counted as an individual item. Auditing requires judgment.

Review the “year-end physical inventory worksheet” for the parts inventory

The attached work sheet shows the results for our sample of parts inventory. From the population of 1,703 SKU lines, we randomly selected 387 SKU lines for which we tested both the quantity and cost. We tested the quantity by counting the number of items on actually hand and comparing this with the quantity in the accounting records. We tested the cost by comparing the cost of the items on purchase invoices with the cost in the accounting records.

2

We detected two types of errors in our sample. There were instances where the quantity on hand differed from the quantity in the client’s accounting records. For instance, on line 3 the auditor counted 239 units of SKU 1851974 during their year-end physical inventory observation even though the client reports having 240 units. We also detected an instance where the cost on the purchase invoice differed from the cost included in the inventory balance. On line 986 the client’s accounting records indicate SKU 6730291 cost $132.92 per unit but the purchase invoice showed these items actually cost $123.92.

We audited the quantity and cost for the 387 items in our sample. We calculated the extended cost for each SKU item by multiplying the quantity times the cost. For example the extended cost for line 1, SKU 4470312 would be 5 x $2.65 = $13.26. The sum of the extended balances for the 387 part lines in our sample was $441,567.00.

Auditing standards require us compare our projected sample results to the population. First, we project our sample results to the population to calculate our best estimate of the balance. Then we compare our best estimate of the balance with the reported balance to determine the projected overstatement error. A balance is overstated when the reported book value exceeds our estimate of the balance. Remember that auditing standards do not require balances to be exact. Auditing standards require auditors to “obtain reasonable assurance about whether the financial statements are FREE OF MATERIAL MISSTATEMENT.” Auditing standards require auditors obtain “sufficient, appropriate evidence” the financial statements “PRESENT FAIRLY, IN ALL MATERIAL RESPECTS.”

𝑝𝑟𝑜𝑗𝑒𝑐𝑡𝑒𝑑 𝑏𝑎𝑙𝑎𝑛𝑐𝑒 = 𝑁 × (𝑎𝑢𝑑𝑖𝑡𝑒𝑑 𝑏𝑎𝑙𝑎𝑛𝑐𝑒

𝑛) 1,703 × (

$441,567

387) = $1,943,123

𝑝𝑟𝑜𝑗𝑒𝑐𝑡𝑒𝑑 𝑒𝑟𝑟𝑜𝑟 = 𝑏𝑜𝑜𝑘 𝑏𝑎𝑙𝑎𝑛𝑐𝑒 − 𝑝𝑟𝑜𝑗𝑒𝑐𝑡𝑒𝑑 𝑎𝑢𝑑𝑖𝑡 𝑏𝑎𝑙𝑎𝑛𝑐𝑒

𝑝𝑟𝑜𝑗𝑒𝑐𝑡𝑒𝑑 𝑜𝑣𝑒𝑟𝑠𝑡𝑎𝑡𝑒𝑚𝑒𝑛𝑡 𝑒𝑟𝑟𝑜𝑟 𝑜𝑓 $22,437.03 = $1,965,560.03, −$1,943,123.00 The work papers state that tolerable misstatement (TM) for the parts inventory is $200,000. Calculating that the projected error that is less than tolerable misstatement does not mean that detection risk is an acceptably low. Auditing standards caution that “AS THE

PROJECTED MISSTATEMENT APPROACHES OR EXCEEDS TOLERABLE MISSTATEMENT, THE MORE

LIKELY THAT ACTUAL MISSTATEMENT IN THE POPULATION EXCEEDS TOLERABLE MISSTATEMENT” (AU 530.27).

Auditing standards do not require the use of statistical sampling. We might compare our $22,437 projected misstatement to the $200,000 tolerable misstatement and conclude that there is an acceptably low risk that an overstatement would exceed $200,000 because the projected error is quite a bit smaller than the tolerable misstatement. Or we might use methods learned in statistics classes to quantify the risk.

“AS THE PROJECTED MISSTATEME NT APPROACHES OR EXCEEDS TOLERABLE MISSTATEMENT, THE

MORE LIKELY THAT ACTUAL MISSTATEMENT IN THE POPULATION EXCEEDS TOLERABLE

MISSTATEMENT” (AU 530.27). How do we determine when the projected error is too close to tolerable misstatement? Statistics provides tools to estimate the probability that the actual misstatement might exceed tolerable misstatement.

3

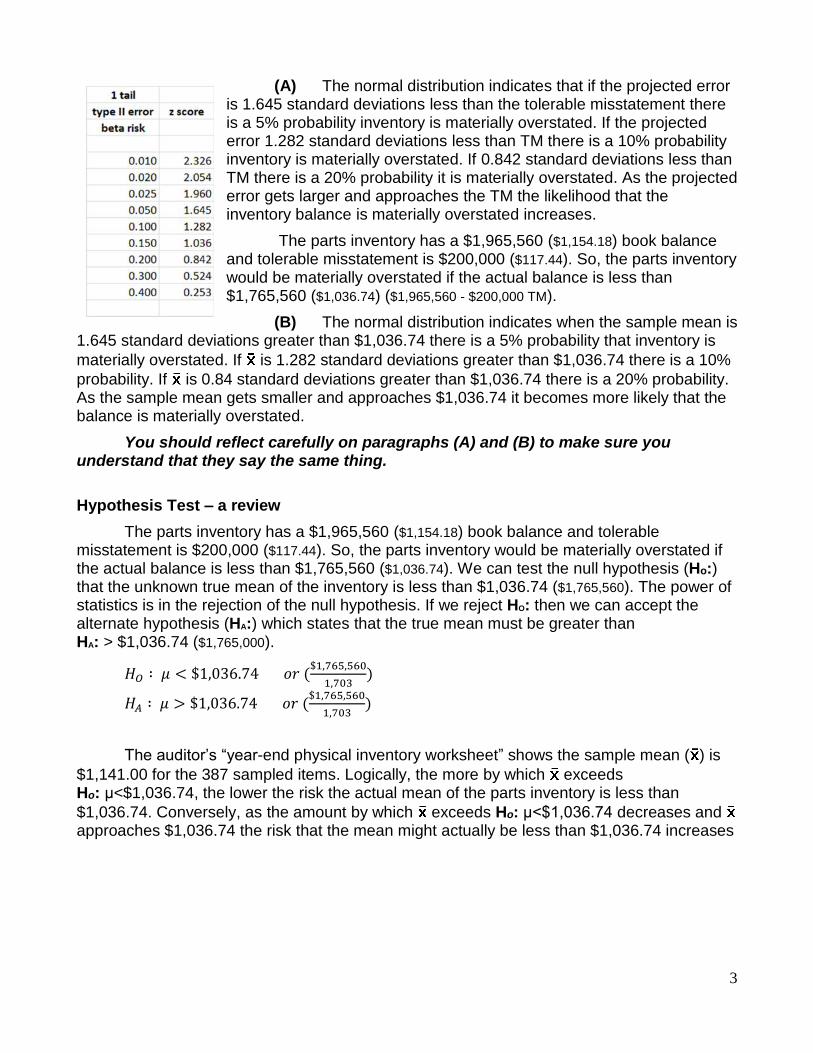

(A) The normal distribution indicates that if the projected error is 1.645 standard deviations less than the tolerable misstatement there is a 5% probability inventory is materially overstated. If the projected error 1.282 standard deviations less than TM there is a 10% probability inventory is materially overstated. If 0.842 standard deviations less than TM there is a 20% probability it is materially overstated. As the projected error gets larger and approaches the TM the likelihood that the inventory balance is materially overstated increases.

The parts inventory has a $1,965,560 ($1,154.18) book balance and tolerable misstatement is $200,000 ($117.44). So, the parts inventory would be materially overstated if the actual balance is less than $1,765,560 ($1,036.74) ($1,965,560 - $200,000 TM).

(B) The normal distribution indicates when the sample mean is 1.645 standard deviations greater than $1,036.74 there is a 5% probability that inventory is

materially overstated. If is 1.282 standard deviations greater than $1,036.74 there is a 10%

probability. If is 0.84 standard deviations greater than $1,036.74 there is a 20% probability. As the sample mean gets smaller and approaches $1,036.74 it becomes more likely that the balance is materially overstated.

You should reflect carefully on paragraphs (A) and (B) to make sure you understand that they say the same thing.

Hypothesis Test – a review

The parts inventory has a $1,965,560 ($1,154.18) book balance and tolerable misstatement is $200,000 ($117.44). So, the parts inventory would be materially overstated if the actual balance is less than $1,765,560 ($1,036.74). We can test the null hypothesis (Ho:) that the unknown true mean of the inventory is less than $1,036.74 ($1,765,560). The power of statistics is in the rejection of the null hypothesis. If we reject HO: then we can accept the alternate hypothesis (HA:) which states that the true mean must be greater than HA: > $1,036.74 ($1,765,000).

𝐻𝑂 ∶ 𝜇 < $1,036.74 𝑜𝑟 ($1,765,560

1,703)

𝐻𝐴 ∶ 𝜇 > $1,036.74 𝑜𝑟 ($1,765,560

1,703)

The auditor’s “year-end physical inventory worksheet” shows the sample mean ( ) is

$1,141.00 for the 387 sampled items. Logically, the more by which exceeds Ho: μ<$1,036.74, the lower the risk the actual mean of the parts inventory is less than

$1,036.74. Conversely, as the amount by which exceeds Ho: μ<$1,036.74 decreases and approaches $1,036.74 the risk that the mean might actually be less than $1,036.74 increases

4

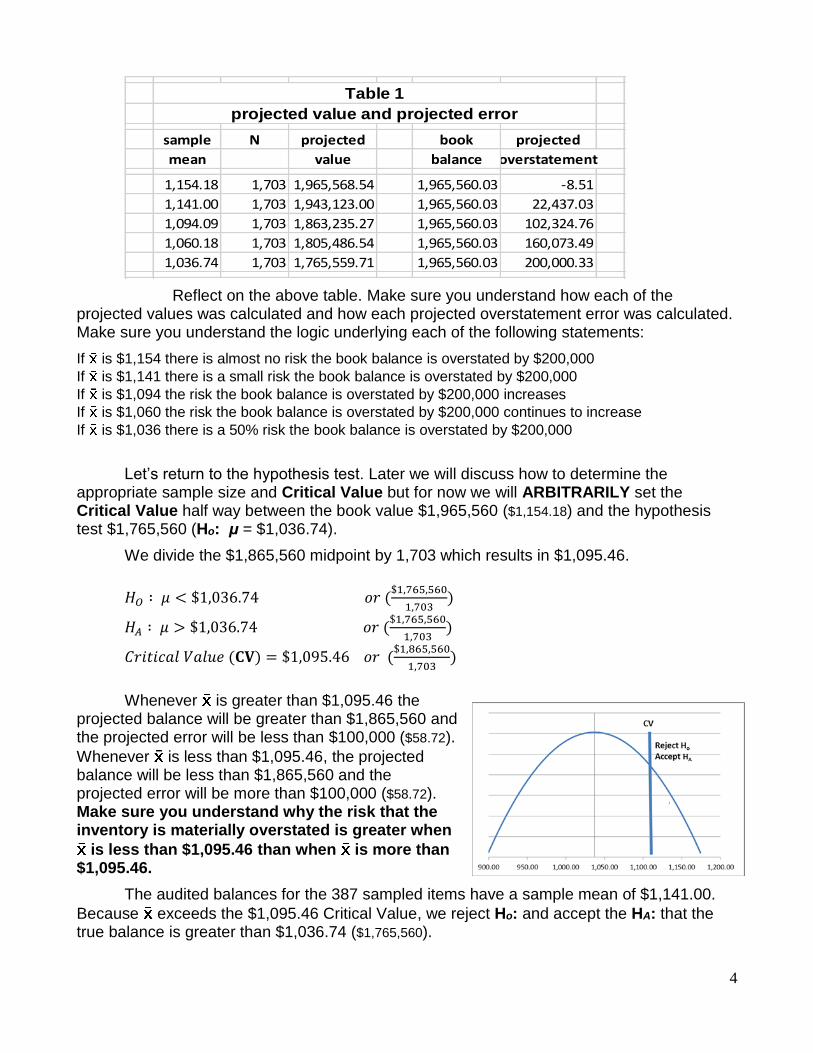

Table 1

projected value and projected error

sample N projected book projected

mean value balance overstatement

1,154.18 1,703 1,965,568.54 1,965,560.03 -8.51

1,141.00 1,703 1,943,123.00 1,965,560.03 22,437.03

1,094.09 1,703 1,863,235.27 1,965,560.03 102,324.76

1,060.18 1,703 1,805,486.54 1,965,560.03 160,073.49

1,036.74 1,703 1,765,559.71 1,965,560.03 200,000.33

Reflect on the above table. Make sure you understand how each of the projected values was calculated and how each projected overstatement error was calculated. Make sure you understand the logic underlying each of the following statements:

If is $1,154 there is almost no risk the book balance is overstated by $200,000

If is $1,141 there is a small risk the book balance is overstated by $200,000

If is $1,094 the risk the book balance is overstated by $200,000 increases

If is $1,060 the risk the book balance is overstated by $200,000 continues to increase

If is $1,036 there is a 50% risk the book balance is overstated by $200,000

Let’s return to the hypothesis test. Later we will discuss how to determine the appropriate sample size and Critical Value but for now we will ARBITRARILY set the Critical Value half way between the book value $1,965,560 ($1,154.18) and the hypothesis test $1,765,560 (Ho: μ = $1,036.74).

We divide the $1,865,560 midpoint by 1,703 which results in $1,095.46.

𝐻𝑂 ∶ 𝜇 < $1,036.74 𝑜𝑟 ($1,765,560

1,703)

𝐻𝐴 ∶ 𝜇 > $1,036.74 𝑜𝑟 ($1,765,560

1,703)

𝐶𝑟𝑖𝑡𝑖𝑐𝑎𝑙 𝑉𝑎𝑙𝑢𝑒 (𝐂𝐕) = $1,095.46 𝑜𝑟 ($1,865,560

1,703)

Whenever is greater than $1,095.46 the projected balance will be greater than $1,865,560 and the projected error will be less than $100,000 ($58.72).

Whenever is less than $1,095.46, the projected balance will be less than $1,865,560 and the projected error will be more than $100,000 ($58.72). Make sure you understand why the risk that the inventory is materially overstated is greater when

is less than $1,095.46 than when is more than $1,095.46.

The audited balances for the 387 sampled items have a sample mean of $1,141.00.

Because exceeds the $1,095.46 Critical Value, we reject Ho: and accept the HA: that the true balance is greater than $1,036.74 ($1,765,560).

5

We conclude that the true mean is greater than $1,036.74 ($1,765,560). Because the sample mean is so much greater than the 𝑯𝑶 ∶ 𝝁 < $𝟏, 𝟎𝟑𝟔. 𝟕𝟒 it is unlikely the sample came from a population with a mean less than $1,036.74 ($1,765,560).

Just for Fun

From your statistics class, you might remember that we use the standard error of the means to evaluate sample results. The standard error the means is the standard deviation for the distribution of sample means and is calculated by dividing the standard deviation for the

population by the square root of the sample size, 𝑠𝑒 =𝑠𝑥

√𝑛.

If = $1,154 there is less than a 0.01% risk the book balance is overstated by $117.44 ($200,000/1,703)

If = $1,141 there is a 0.01% risk the book balance is overstated by $200,000

If = $1,094 there is a 0.10% risk the book balance is overstated by $200,000

If = $1,060 there is a 30% risk the book balance is overstated by $200,000

If = $1,036 there is a 50% risk the book balance is overstated by $200,000

Calculating the Critical Value

The normal distribution allows us to quantify the risk of reaching an incorrect conclusion. If inventory is materially overstated, the risk of concluding inventory is not materially overstated can be limited to 10% by setting the Critical Value 1.282 standard deviations to the right of the hypothetical mean.

The “year-end physical inventory worksheet” indicates the best estimate of the standard deviation is $880.00. In order to limit the risk of incorrectly concluding the inventory balance is not materially overstated when the true mean is less than $1,036.74 ($1,765,560) the Critical Value in the example is $1,094.09. We calculated the Critical Value by adding 1.282 standard deviations to our hypothetical mean.

𝐶𝑟𝑖𝑡𝑖𝑐𝑎𝑙 𝑉𝑎𝑙𝑢𝑒 = 𝜇𝑜 + 𝑍𝛽𝑠𝑥

√𝑛 𝐶𝑉 = $1,036.74 + 1.282

$880.00

√387 = $1,094.09

Continuing with the example, the of $1,141 exceeds the $1,094.09 CV. So, we can reject Ho: with a 10% level of β risk, accept the HA: that the actual mean is greater than

Table 2

difference in std errors converted to probabilities

sample BV - TM sample std differ in

mean hypoth mean difference n std dev error std errors probability

(table 1) Ho: µ "z"

1,154.18 1,036.74 117.44 387 880.00 44.73 2.63 0.004

1,141.00 1,036.74 104.26 387 880.00 44.73 2.33 0.010

1,094.09 1,036.74 57.35 387 880.00 44.73 1.28 0.100

1,060.18 1,036.74 23.44 387 880.00 44.73 0.52 0.300

1,036.74 1,036.74 -0.01 387 880.00 44.73 0.00 0.500

6

$1,036.74 ($1,765,560). There is less than a 10% probability we would obtain greater than $1,094.09 if the mean of the population was $1,036.74. This assumes a sample size of 387 and a standard deviation of $880.00.

If we wanted to limit the risk of concluding inventory is not materially overstated to 5% we would set the Critical Value 1.645 standard deviations to the right of the hypothetical mean and the Critical Value would be $1,110.33.

𝐶𝑟𝑖𝑡𝑖𝑐𝑎𝑙 𝑉𝑎𝑙𝑢𝑒 = 𝜇𝑜 + 𝑍𝛽𝑠𝑥

√𝑛 𝐶𝑉 = $1,036.74 + 1.645

$880.00

√387 = $1,110.33

The of $1,141 in our example exceeds the $1,110.33 Critical Value. So, we reject Ho: with 5% β risk, accept the HA: that the actual mean is greater than $1,036.74 ($1.750.560).

There is less than a 5% probability we would obtain greater than $1,110.33 if the mean of the population was $1,036.74 (again assuming n = 387 and std. dev. = $880.00).

How did we determine the sample size of n =387?

We have only discussed the risk of incorrectly concluding that inventory is fairly presented when it is materially overstated. In your statistics class, this was the risk of incorrect acceptance: Type II error or β risk. You also discussed the risk of concluding inventory is overstated when it is actually correct which is the risk of incorrect rejection: Type I error or α risk.

Typically, hypothesis tests are associated with Type II (β) risk and confidence intervals with Type I (α) risk.

Remember that confidence and risk are complements; they add up to one. If we are 70% confident then there is 30% risk of error.

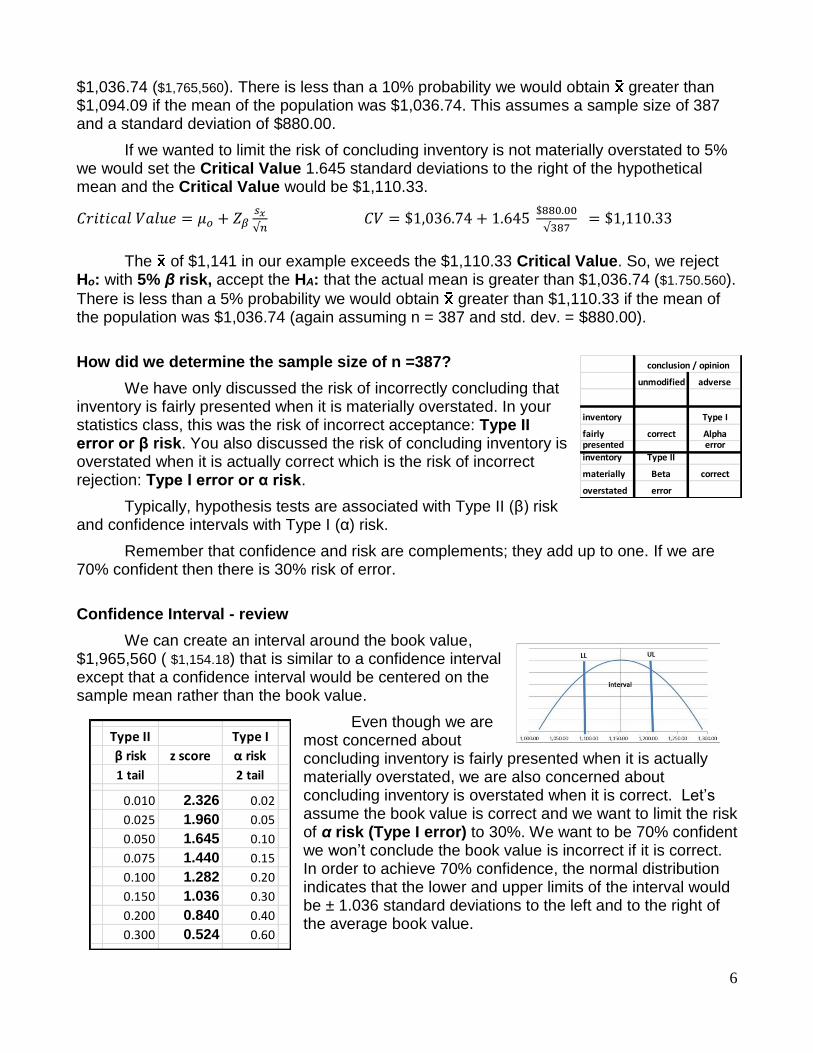

Confidence Interval - review

We can create an interval around the book value, $1,965,560 ( $1,154.18) that is similar to a confidence interval except that a confidence interval would be centered on the sample mean rather than the book value.

Even though we are most concerned about concluding inventory is fairly presented when it is actually materially overstated, we are also concerned about concluding inventory is overstated when it is correct. Let’s assume the book value is correct and we want to limit the risk of α risk (Type I error) to 30%. We want to be 70% confident we won’t conclude the book value is incorrect if it is correct. In order to achieve 70% confidence, the normal distribution indicates that the lower and upper limits of the interval would be ± 1.036 standard deviations to the left and to the right of the average book value.

conclusion / opinion

unmodified adverse

inventory Type I

fairly correct Alphapresented error

inventory Type II

materially Beta correct

overstated error

Type II Type I

β risk z score α risk

1 tail 2 tail

0.010 2.326 0.02

0.025 1.960 0.05

0.050 1.645 0.10

0.075 1.440 0.15

0.100 1.282 0.20

0.150 1.036 0.30

0.200 0.840 0.40

0.300 0.524 0.60

7

Again, the standard error of the means equals 𝑠𝑒 =𝑠𝑥

√𝑛. The 𝑖𝑛𝑡𝑒𝑟𝑣𝑎𝑙 = 𝑎𝑣𝑒 𝐵𝑉 ∓ 𝑍

𝑠𝑥

√𝑛.

The best estimate of the standard deviation of the population is $880.00 and our sample size is n = 387. In this case, the interval turns out to be ± $46.36.

The interval in this example would be

𝑖𝑛𝑡𝑒𝑟𝑣𝑎𝑙 = 𝐵𝑉̅̅ ̅̅ ± 𝑍𝛼/2𝑠𝑥

√𝑛

𝐋𝐨𝐰𝐞𝐫 𝐋𝐢𝐦𝐢𝐭 = 𝐵𝑉̅̅ ̅̅ − 𝑍𝛼

2

𝑠𝑥

√𝑛 𝑼𝒑𝒑𝒆𝒓 𝑳𝒊𝒎𝒊𝒕 = 𝐵𝑉̅̅ ̅̅ + 𝑍𝛼/2

𝑠𝑥

√𝑛

𝐿𝐿 = $1,154.18 − 1.036 880

√387= $1,107.84 𝑈𝐿 = $1,154.18 + 1.036

880

√387= $1,200.52

Planning the Inventory Audit and Determining the Sample Size

The sample size must be determined during the planning stage of the audit prior to the Jan. 1st physical inventory observation. The work papers indicate tolerable misstatement for the parts inventory has been set as $200,000, which is approximately 10% of the $1,965,560 balance. Auditing standards require auditors to “obtain reasonable assurance about whether the financial statements are FREE OF MATERIAL MISSTATEMENT” and obtain “sufficient, appropriate evidence” the financial statements “PRESENT FAIRLY, IN ALL MATERIAL RESPECTS.”

Auditors are typically concerned that asset accounts are overstated. If tolerable misstatement is $200,000, we need evidence that the actual balance of the parts inventory is greater than $1,765,560.

The interval between the hypothetical mean Ho: μ >$1,036.74 ($1,765,560) and the average book value $1,154.17 ($1,965,560) is $117.44 ($200,000). This will remain the same regardless of how we allocate Alpha Risk and Beta Risk. The interval is comprised of two elements: the upper portion of the hypothesis test and the lower tail of the confidence interval. Together these two intervals comprise the tolerable misstatement and are captured by 𝑍𝛼/2 𝑎𝑛𝑑 𝑍𝛽 in the sample size formula.

𝐶𝑟𝑖𝑡𝑖𝑐𝑎𝑙 𝑉𝑎𝑙𝑢𝑒 = 𝜇𝑜 + 𝑍𝛽𝑠𝑥

√𝑛 𝐿𝑜𝑤𝑒𝑟 𝐿𝑖𝑚𝑖𝑡 = 𝐵𝑉̅̅ ̅̅ − 𝑍𝛼/2

𝑠𝑥

√𝑛

The formula to calculate the minimum sample size shown at the very beginning to this paper was determined by setting the Critical Value equal to the Lower Limit. Because we are working with averages, Tolerable Misstatement must be divided by the 1,703 lines in

the parts inventory, 𝑇𝑀̅̅̅̅̅.

𝐶𝑉 = 𝐿𝐿 OR 𝜇𝑜 + 𝑍𝛽𝑠𝑥

√𝑛 = 𝐵𝑉̅̅ ̅̅ − 𝑍𝛼/2

𝑠𝑥

√𝑛

(𝑍𝛼/2 + 𝑍𝛽 )𝑠𝑥

√𝑛= 𝐵𝑉̅̅ ̅̅ − 𝜇𝑜 𝐵𝑉̅̅ ̅̅ − 𝜇𝑜 = 𝑇𝑀̅̅̅̅̅ SO (𝑍𝛼/2 + 𝑍𝛽 )

𝑠𝑥

√𝑛= 𝑇𝑀̅̅̅̅̅

(𝑍𝛼/2+𝑍𝛽 )𝑠𝑥

𝑇𝑀̅̅ ̅̅̅= √𝑛

8

Beta Risk and Alpha Risk can be controlled with the number of standard deviations (𝑍𝛼/2 + 𝑍𝛽) in the formula. In order to limit Beta Risk to 10% and Alpha Risk to 15%,

𝑍𝛼/2 𝑎𝑛𝑑 𝑍𝛽 would be 1.282 and 1.440 respectively. The minimum sample size would be 399.

𝛽 = .10 => 𝑍𝛽 = 1.282 𝛼 = .15 => 𝑍𝛼/2 = 1.440

(𝑍𝛼/2+𝑍𝛽 )𝑠𝑥

𝑇𝑀̅̅ ̅̅̅= √𝑛 √𝑛 = (1.282 + 1.440)

$861.52

$117.44 √n = 19.968

n = 398.7 we must always round up i.e. n = 399

In the work papers for our example, Beta Risk and Alpha Risk were set at .05% and 30%. The interval between the hypothetical mean and the average book value is $117.44, the required sample size will change as Alpha Risk and Beta Risk change. In the case, the sample size is 387 which has been used throughout the paper.

√𝑛 = (𝑍𝛼/2+𝑍𝛽 )𝑠𝑥

𝑇𝑀̅̅ ̅̅̅ √𝑛 = (1.645 + 1.036)

$861.52

$117.44 √n = 19.667

n = 386.8 we must always round up i.e. n = 387 Take a moment to notice that the Critical Value will be different when Beta Risk is 10% than when it is 5%. That is because the number of standard deviations assigned to 𝑍𝛽 will change. In order to

reduce Beta Risk more standard deviations will be included in the portion of the distribution to the left of the Critical Value.

Also, notice that we used the standard deviation from our sample results to calculate the Critical Value in our hypothesis test. We did not know the standard deviation of the sample when we calculated the required sample size. We used the standard deviation of the recorded values to calculate the required sample size because that was the best estimate available at the time we were planning the audit.

𝐶𝑟𝑖𝑡𝑖𝑐𝑎𝑙 𝑉𝑎𝑙𝑢𝑒 = 𝜇𝑜 + 𝑍𝛽𝑠𝑥

√𝑛

CV = $1,036.74 + 1.645$861.52

√387 = $1,108.78 Beta Risk = 5% with $861.52 std dev

CV = $1,036.74 + 1.645$880.00

√387 = $1,110.33 Beta Risk = 5% with $880.00 std dev

Think!

If you want to be conservative when you determine the Critical Value for your hypothesis test would you use:

The standard deviation of the values recorded in the book balance, The standard deviation of the items in the sample, The smaller of the std. dev. of the recorded values or the sample, or The larger of the std. dev. of the recorded values of the sample?

9

What if the Sample Mean is less than the Critical Value?

Assume the sum of the 387 lines that were audited came to $410,289.70; the standard deviation of the sample was $880.00 and the sample mean was $1,060.18. The sample mean would lie in the region where we are unable to reject Ho. However, the sample mean is still larger than the hypothetical mean of $1,036.74. The projected balance would be $1,805,486.54. The projected error is $160,073.49, which is less than tolerable misstatement.

In this case, our sample would not provide sufficient evidence to conclude with 95% confidence that the parts inventory is not materially overstated. However, the sample also does not provide evidence that the parts inventory is materially overstated. We can modify the equation we used to calculate the Critical Value and determine the level of confidence the sample results do provide.

𝐶𝑟𝑖𝑡𝑖𝑐𝑎𝑙 𝑉𝑎𝑙𝑢𝑒 = 𝜇𝑜 + 𝑍𝛽𝑠𝑥

√𝑛 �̅� = 𝜇𝑜 + 𝑍𝛽

𝑠𝑥

√𝑛

(�̅�−𝜇𝑜)√𝑛

𝑠𝑥 = 𝑍𝛽

($1,060.18−$1,036.74)√387

880= 𝑍𝛽 = 0.524 𝑠𝑡𝑎𝑛𝑑𝑎𝑟𝑑 𝑑𝑒𝑣𝑖𝑎𝑡𝑖𝑜𝑛𝑠

A sample mean of $1,060.18 is 0.524 standard deviations to the right of $1,036.74.

The table for one-tail tests indicates there is a 30% probability of a obtaining a sample mean 0.524 standard deviations to the right of the actual mean. There is a 30% probability of a obtaining a sample mean equal to $1,060.18 from a population with a mean of $1,036.74. We would be 70% confident that the parts inventory is not materially overstated. In this situation, the partner may want you to audit additional lines of inventory to increase the confidence level. In other situations, the partner might be satisfied with the sample results because of the results of other audit tests.

10

11

Work Paper Lead Sheet

Miller Motor Co performed by: Tad Inventory Lead Sheet date: 1/01/19

balance balance

per per

G.L. audit

15101 parts 1,965,560.03

15201 new cars 231,824.00

15301 new trucks 866,948.12

15401 used cars 185,558.53

15501 used trucks 479,862.11

Total Inventory 3,729,752.79

12

Work Paper 1 Miller Motor Co. performed by: Tad Inventory date: 1/01/19 Parts inventory Nature of test: Substantive Test of Details of Account Balances

Objective: The objective of this procedure is to determine if the parts inventory account is materially overstated.

Assertion(s): Existence, Accuracy, valuation and allocation

Tolerable Misstatement: For parts inventory, tolerable misstatement has been set at $200,000

Procedure: DC & H, LLP selected a random sample of 387 entries from MMC’s inventory worksheet. On Jan. 1, 2018, we observed MMC’s physical inventory observation.

For each SKU item selected in our sample, we counted the number of items in MMC’s parts warehouse and compared our count with the quantity on MMC’s parts department physical inventory worksheet. For those items where there was a discrepancy between our count and the quantity reported by MMC, we re-counted those items accompanied by MMC’s parts inventory supervisory. For each SKU item selected in our sample, we obtained the most recent invoice to determine the appropriate cost (MMC uses FIFO). In some cases the quantity on hand for an SKU number exceeded the quantity purchased on the most recent invoice. In those cases we obtained sufficient previous invoices to account for the quantity on hand. We compared our cost with the cost on MMC’s parts department physical inventory worksheet. We reviewed all SKU numbers for which we found a discrepancy between the cost on the most recent invoice and the cost reported on MMC’s inventory work sheet with the parts inventory supervisory.

Work Paper 2 shows the sample size calculation and the evaluation of the

sample results. Workpaper 3 shows the sample results. Conclusion: Based on the sample results we conclude that parts inventory is not

materially overstated.

13

Work Paper 2 Miller Motor Co. performed by: Tad Inventory date: 1/01/19 Parts inventory Nature of test: Substantive Test of Details of Account Balances

Objective: The objective of this procedure is to determine if the parts inventory account is materially overstated.

Assertion(s): Existence, Accuracy, valuation and allocation

Tolerable Misstatement: For parts inventory, tolerable misstatement has been set at $200,000

Procedure: Sample size calculation

Book = $1,965,560.03 𝐵𝑉̅̅ ̅̅ = $1,154.18

Tol Mis = $ 200,000. 𝑇𝑀̅̅̅̅̅ = $ 117.44 μo < 1,965,560.03 – 200,000.00 Ho: μo < 1,154.175 – 117.44 std dev = 861.52 Ho: μo < 1,036.74 risk of incorrect rejection α = 0.30 Zα/2 = 1.036 risk of incorrect acceptance β = 0.05 Zβ = 1.645

(𝒁𝜷+𝒁𝜶

𝟐⁄ )𝒔𝒙

𝑻𝑴̅̅ ̅̅ ̅= √𝒏

𝟏.𝟔𝟒𝟓+𝟏.𝟎𝟑𝟔 )𝟖𝟔𝟏.𝟓𝟐

𝟏𝟏𝟕.𝟒𝟒= √𝒏

19.667 = √n 386.8 = n => n = 387 (we always round up) Hypothesis test using sample results to calculate Critical Value using sample results �̅� = $1,141.00 CV = μ + Zβ * Sx/√n 𝑠 = 880.00 = 1,036.74 + 1.645* 880.00 / √387 = 1,036.74 + 73.586

= 1,110.33 Evaluation of Sample Results Sample Mean $1,141.00 is greater than CV of $1,110.33

Since the sample mean of $1,141.00 is greater than the Critical Value of $1,110.33 we can conclude that the mean of the population from which the sample was selected is greater than $1,110.33 with less than 5% risk of incorrect acceptance.

14

15

16

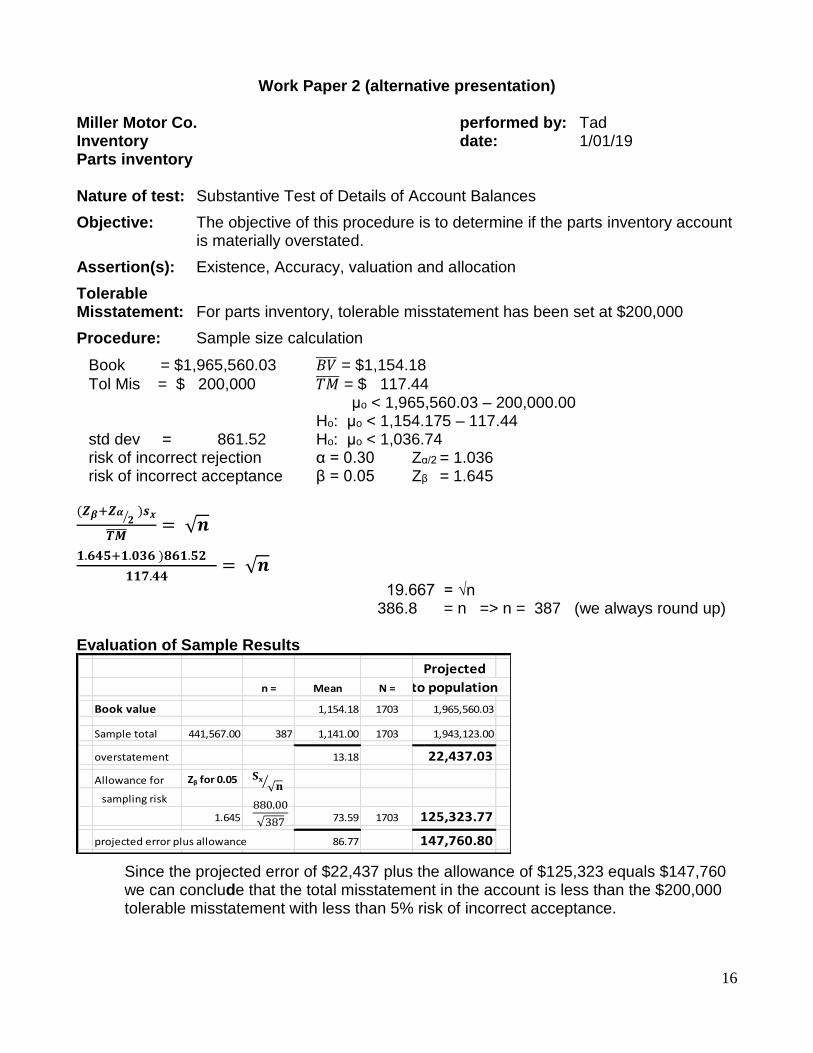

Work Paper 2 (alternative presentation) Miller Motor Co. performed by: Tad Inventory date: 1/01/19 Parts inventory Nature of test: Substantive Test of Details of Account Balances

Objective: The objective of this procedure is to determine if the parts inventory account is materially overstated.

Assertion(s): Existence, Accuracy, valuation and allocation

Tolerable Misstatement: For parts inventory, tolerable misstatement has been set at $200,000

Procedure: Sample size calculation

Book = $1,965,560.03 𝐵𝑉̅̅ ̅̅ = $1,154.18

Tol Mis = $ 200,000 𝑇𝑀̅̅̅̅̅ = $ 117.44 μo < 1,965,560.03 – 200,000.00 Ho: μo < 1,154.175 – 117.44 std dev = 861.52 Ho: μo < 1,036.74 risk of incorrect rejection α = 0.30 Zα/2 = 1.036 risk of incorrect acceptance β = 0.05 Zβ = 1.645 (𝒁𝜷+𝒁𝜶

𝟐⁄ )𝒔𝒙

𝑻𝑴̅̅ ̅̅ ̅= √𝒏

𝟏.𝟔𝟒𝟓+𝟏.𝟎𝟑𝟔 )𝟖𝟔𝟏.𝟓𝟐

𝟏𝟏𝟕.𝟒𝟒= √𝒏

19.667 = √n 386.8 = n => n = 387 (we always round up) Evaluation of Sample Results

Projected

n = Mean N = to population

Book value 1,154.18 1703 1,965,560.03

Sample total 441,567.00 387 1,141.00 1703 1,943,123.00

overstatement 13.18 22,437.03

Allowance for Zβ for 0.05

sampling risk

1.645 73.59 1703 125,323.77

projected error plus allowance 86.77 147,760.80

⁄

880.00

387

Since the projected error of $22,437 plus the allowance of $125,323 equals $147,760 we can conclude that the total misstatement in the account is less than the $200,000 tolerable misstatement with less than 5% risk of incorrect acceptance.

17

Mil

ler

Mo

tor

Co

.

year

-en

d p

hys

ical

inve

nto

ry

wo

rksh

ee

t

aud

it r

esu

lts

reta

ile

xte

nd

ed

ext

en

de

d

lin

eq

tySK

Up

rice

cost

cost

qty

cost

cost

15

4470

312

Tail

lam

p b

ulb

4.42

2.65

13.2

65

2.65

13.2

6

240

1118

019

Oil

fil

ter

7.30

4.38

175.

20

324

018

5197

4Sp

ark

plu

g9.

765.

861,

405.

4423

95.

861,

399.

58

443

3873

086

Air

inta

ke f

ilte

r44

.28

26.5

71,

142.

4242

26.5

71,

115.

865

……

……

……

……

……

……

……

…

984

2162

0203

7Sh

ock

112.

3067

.38

1,41

4.98

2167

.38

1,41

4.98

985

236

8038

7Fu

el p

um

p d

iese

l13

1.98

79.1

915

8.38

986

1167

3029

1W

he

el s

tee

l22

1.53

132.

921,

462.

1011

123.

921,

363.

12

987

1960

3719

2B

rake

pad

s22

4.24

134.

542,

556.

34

988

351

1937

8W

ate

r p

um

p29

3.98

176.

3952

9.16

989

440

3002

6A

lte

rnat

or

335.

0420

1.02

804.

103

201.

0260

3.07

990

……

……

…

……

……

…

……

……

…

1701

227

8018

9Tr

ansm

issi

on

4l6

0e m

301,

857.

311,

578.

713,

157.

432

1,57

8.71

3,15

7.43

1702

116

1604

5En

gin

e -

4.3

L2,

886.

862,

453.

832,

453.

83

1703

114

7802

7En

gin

e -

6.0

L4,

874.

534,

143.

354,

143.

351

4,14

3.35

4,14

3.35

Exte

nd

ed

Co

st B

oo

k V

alu

e1

,96

5,5

60

.03

sam

ple

n=3

87

44

1,5

67

.00

Stan

dar

d D

evi

atio

n (

Bo

ok

Val

ue

)8

61

.52

sam

ple

std

de

v8

80

.00

Me

an o

f B

oo

k V

alu

e1

,15

4.1

8sa

mp

le m

ean

1,1

41

.00

18

retail extended

line qty SKU price cost cost

1 2 S9856 Silverado LT 78.7 26,810.00 24,933.00 49,866.00

2 2 M3780 Malibu LTZ 26,955.00 25,607.00 51,214.00

3 3 I3772 Impala LTZ 29,930.00 28,733.00 86,199.00

4 1 C1851 Corvette Base 48,950.00 44,545.00 44,545.00

Extended Cost 231,824.00

Standard Deviation of Sampling Lines 19,047.53

1 1 S9856 Silverado LT 78.7 26,810.00 24,933.00

2 1 S9856 Silverado LT 78.8 26,810.00 24,933.00

3 1 M3780 Malibu LTZ 26,955.00 25,607.00

4 1 M3780 Malibu LTZ 26,955.00 25,607.00

5 1 I3770 Impala LTZ 29,930.00 28,733.00

6 1 I3770 Impala LTZ 29,930.00 28,733.00

7 1 I3770 Impala LTZ 29,930.00 28,733.00

8 1 C1851 Corvette Base 48,950.00 44,545.00

Extended Cost 231,824.00

Standard Deviation of Sampling Lines6,524.27

19