minnesota demographic and economic trends

DESCRIPTION

Minnesota Demographic And Economic Trends. Tom Gillaspy, State Demographer Mn Dept of Administration May 2010. U.S. Employment Not Expected to Return to Pre-Recession High Until Spring 2013. Minnesota Wages and Employment Fell During This Recession. - PowerPoint PPT PresentationTRANSCRIPT

Minnesota Demographic And Economic Trends

Tom Gillaspy, State Demographer

Mn Dept of Administration

May 2010

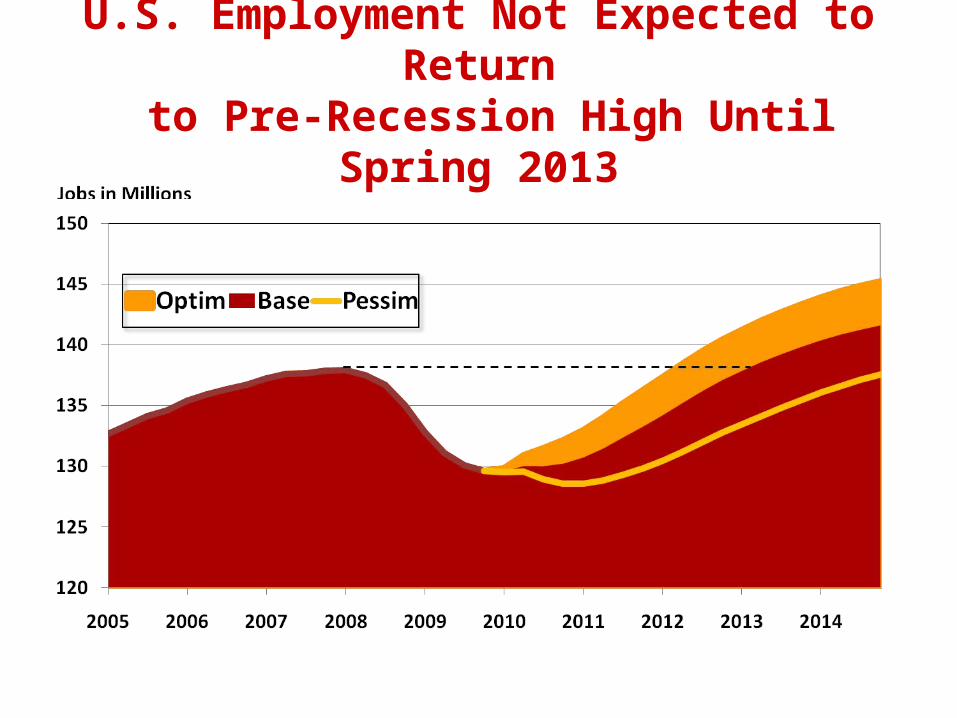

U.S. Employment Not Expected to Return to Pre-Recession High Until Spring 2013

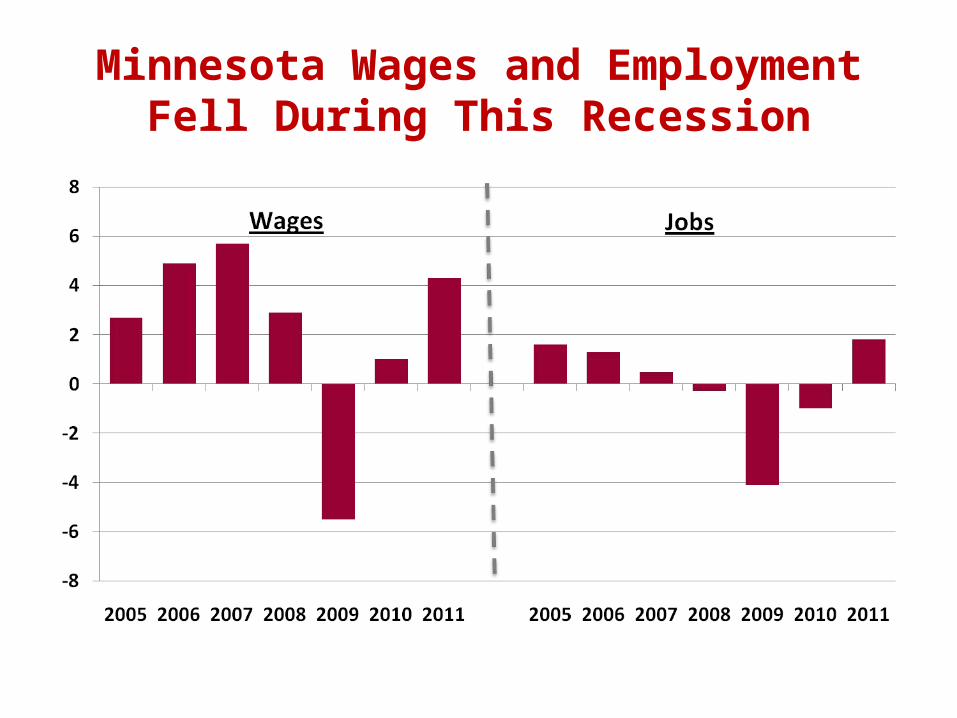

Minnesota Wages and Employment Fell During This Recession

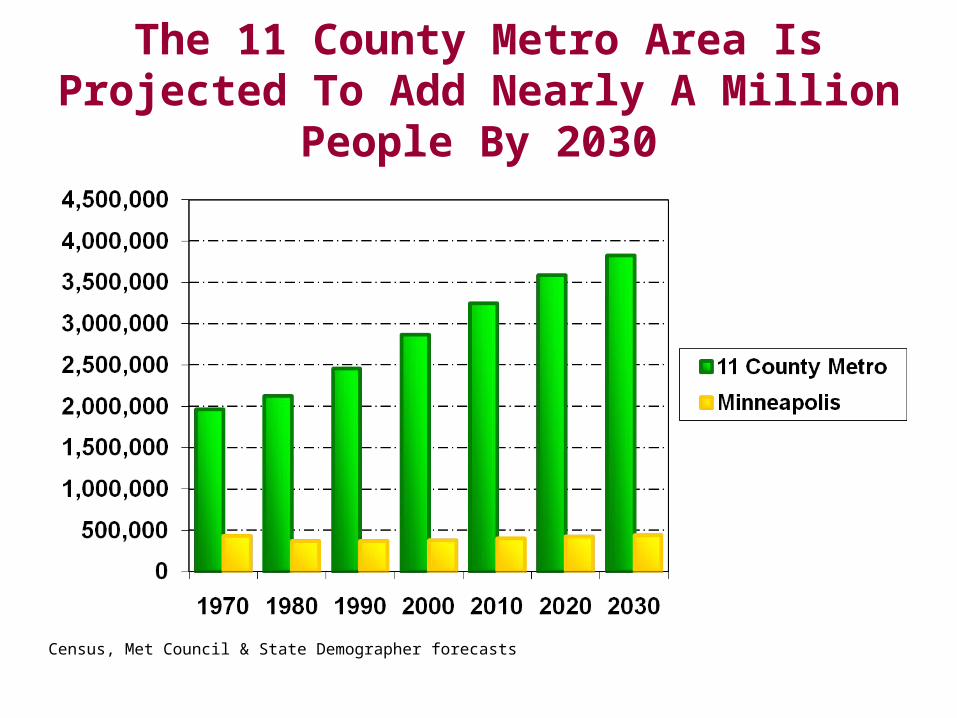

The 11 County Metro Area Is Projected To Add Nearly A Million People By 2030

Census, Met Council & State Demographer forecasts

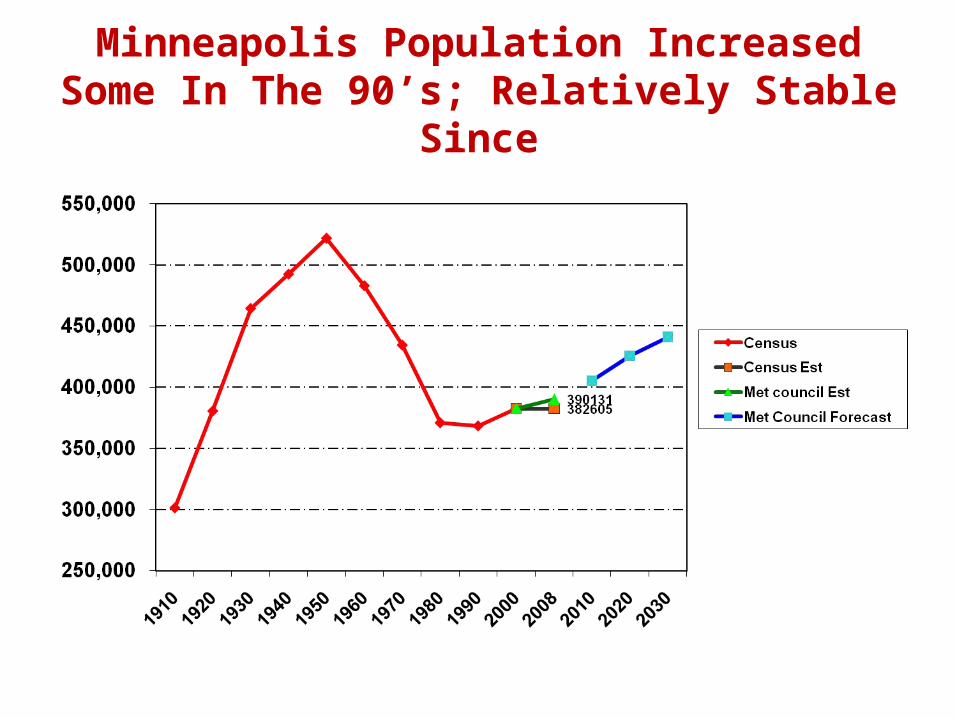

Minneapolis Population Increased Some In The 90’s; Relatively Stable Since

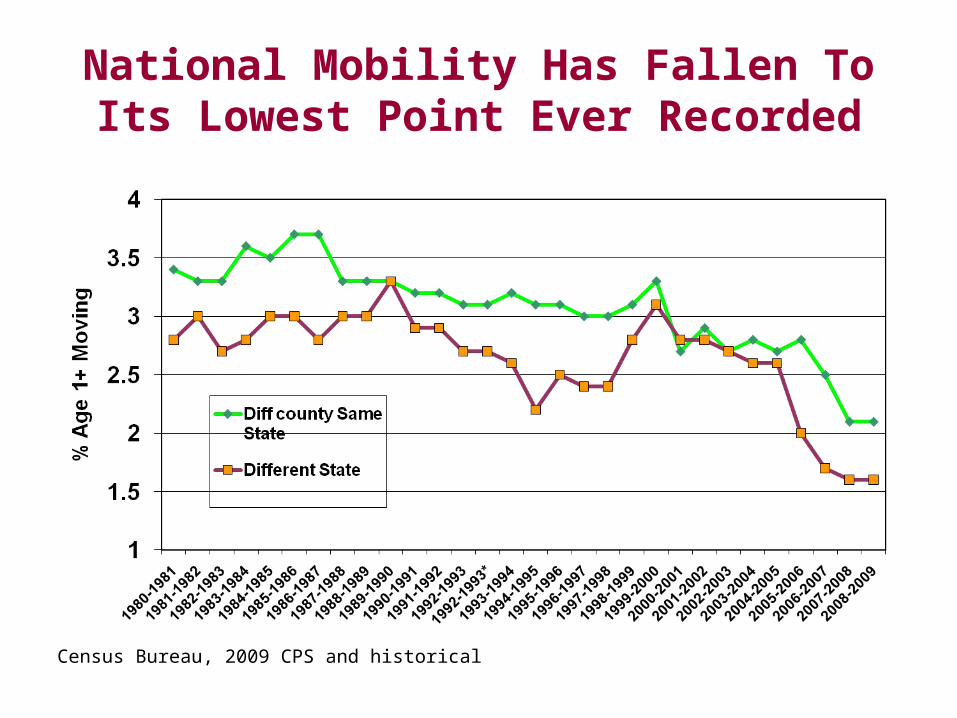

National Mobility Has Fallen To Its Lowest Point Ever Recorded

Census Bureau, 2009 CPS and historical

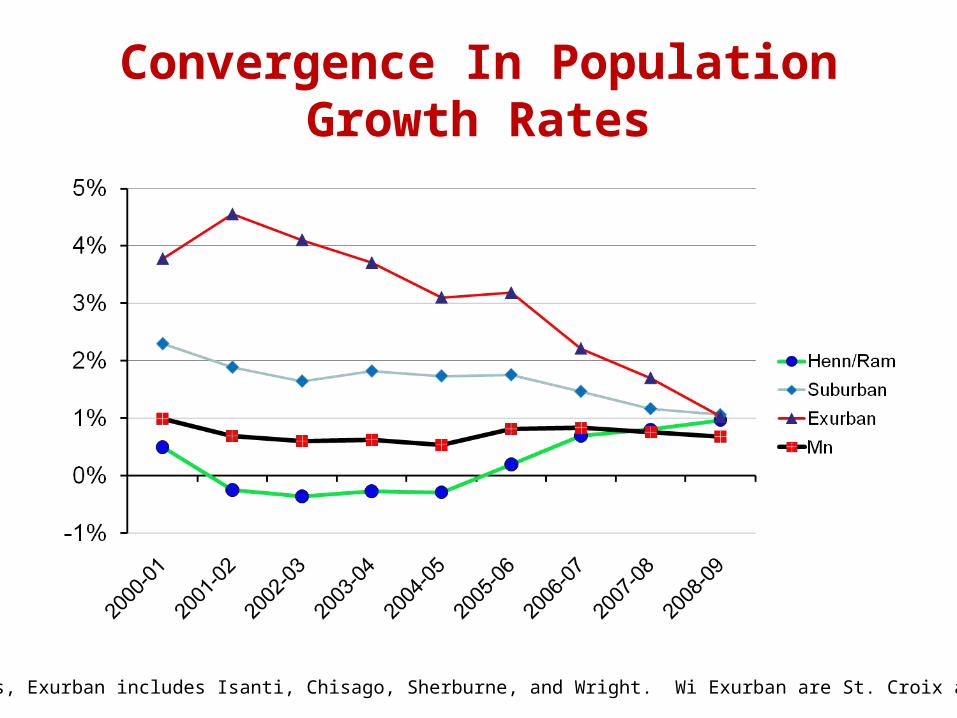

Convergence In Population Growth Rates

Census ests, Exurban includes Isanti, Chisago, Sherburne, and Wright. Wi Exurban are St. Croix and Pierce

The Economic/Demographic Environment Has Changed for as

Far as We Can Forecast

Short run economic cycle has merged with long run demographic cycle

We have entered the Age of Entitlement—economic growth in the next 25 years will be about half what it was in the past 25.

State revenue growth will slow while spending pressures will accelerate

This is a national/global issue

Minnesota Saw a 30 Percent Jump in Workers Turning Age 62 in 2008

0

10,000

20,000

30,000

40,000

50,000

60,000

7/05 to7/06

7/06 to7/07

7/07 to7/08

7/08 to7/09

7/09 to7/10

7/10 to7/11

7/11 to7/12

Year Turning Age 62

Wo

rke

d W

ith

in P

as

t 5

ye

ars

2005 ACS

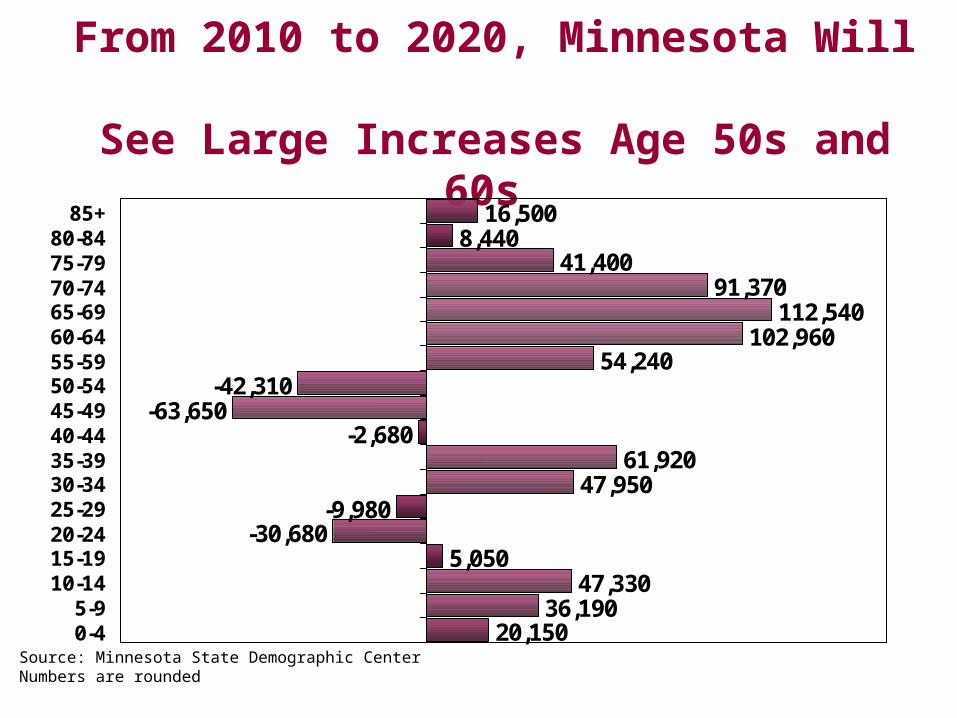

From 2010 to 2020, Minnesota Will See Large Increases Age 50s and 60s

20,15036,190

47,3305,050

-30,680-9,980

47,95061,920

-2,680-63,650

-42,31054,240

102,960112,540

91,37041,400

8,44016,500

0-45-9

10-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-7980-84

85+

Source: Minnesota State Demographic CenterNumbers are rounded

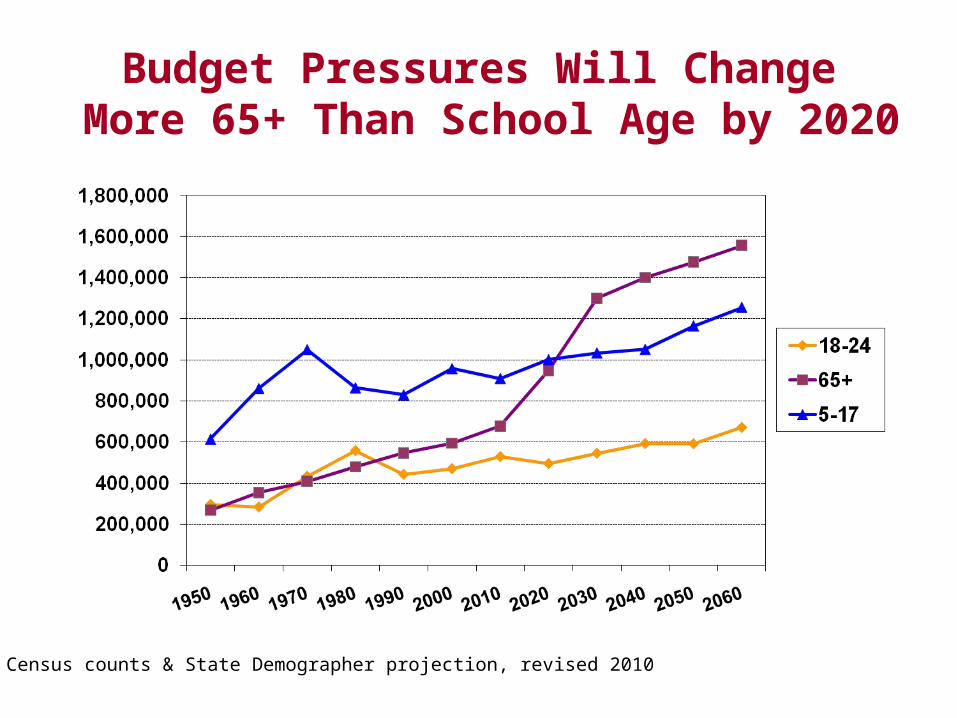

Budget Pressures Will Change More 65+ Than School Age by 2020

Census counts & State Demographer projection, revised 2010

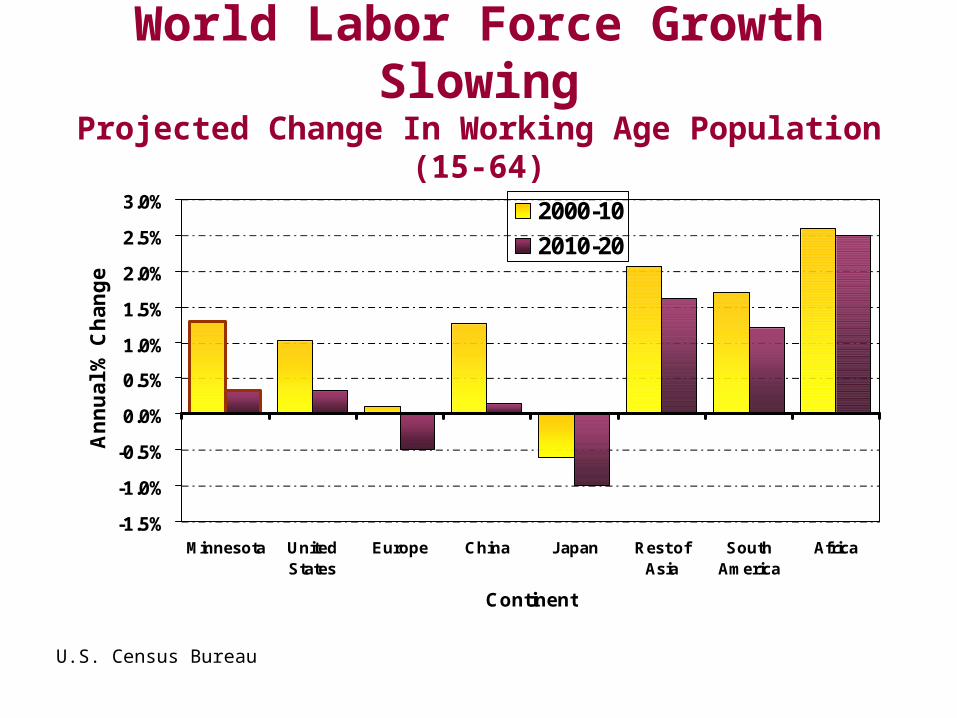

Labor Force Growth Is About To Slow Sharply

1.52%

1.12%

0.75%

0.43%

0.10% 0.13%

0.27%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1990-2000

2005-10 2010-15 2015-20 2020-25 2025-30 2030-35

Ave

An

nu

al C

han

ge

World Labor Force Growth SlowingProjected Change In Working Age Population (15-64)

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Minnesota UnitedStates

Europe China Japan Rest ofAsia

SouthAmerica

Africa

Continent

An

nu

al

% C

ha

ng

e

2000-10

2010-20

U.S. Census Bureau

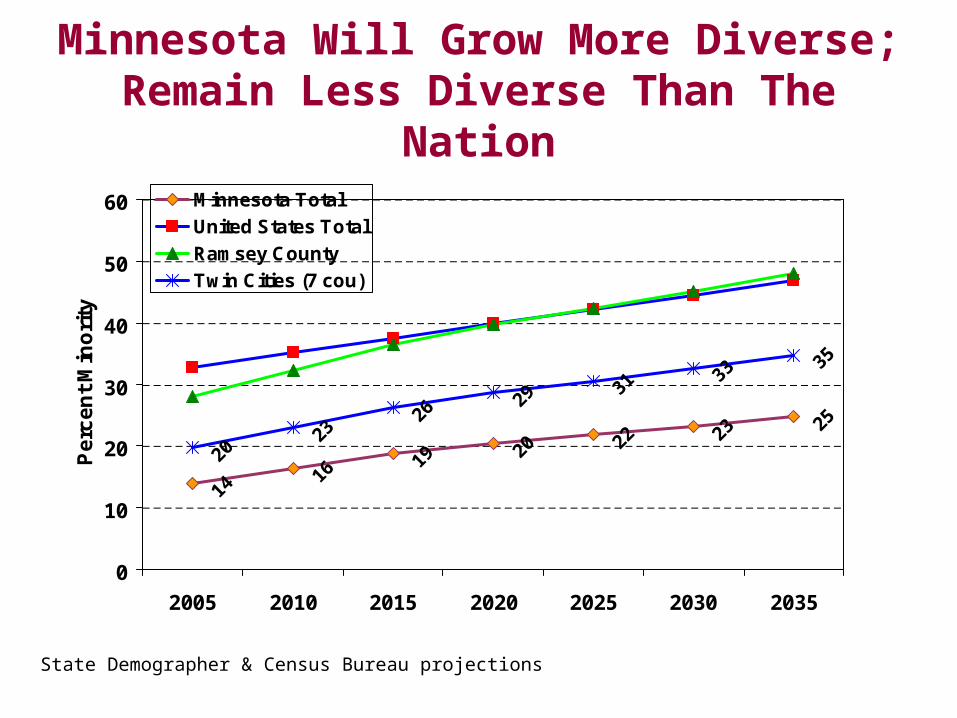

Minnesota Will Grow More Diverse; Remain Less Diverse Than The Nation

1416

19 20 22 23 25

2023

2629

3133

35

0

10

20

30

40

50

60

2005 2010 2015 2020 2025 2030 2035

Pe

rce

nt

Min

ori

ty

Minnesota Total

United States Total

Ramsey County

Twin Cities (7 cou)

State Demographer & Census Bureau projections

The “New Normal” Probably Means

• Slower economic growth—about 85% as fast

• Slower growth of wages, portfolio incomes, & profits

• Less consumption; more saving

• Retirements will create many of the job openings

• Skills mismatch will present a problem in replacing retiring workers

• Creative destruction/disruptive innovation are creating a new set of opportunities

• More uncertainty about the future

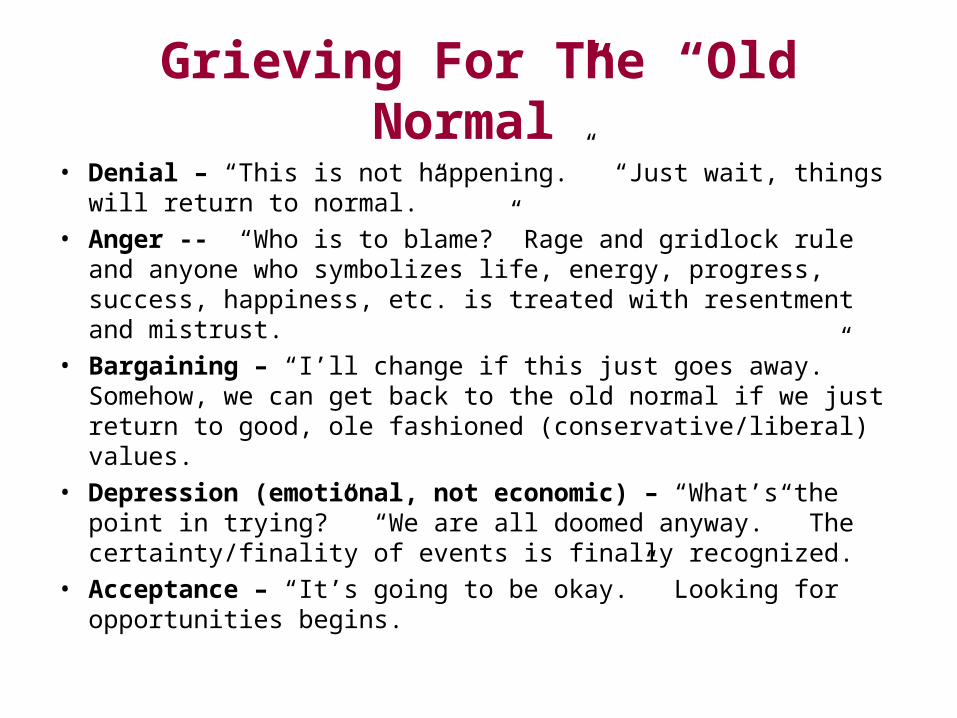

Grieving For The “Old Normal”

• Denial – “This is not happening.” “Just wait, things will return to normal.”

• Anger -- “Who is to blame?” Rage and gridlock rule and anyone who symbolizes life, energy, progress, success, happiness, etc. is treated with resentment and mistrust.

• Bargaining – “I’ll change if this just goes away.” Somehow, we can get back to the old normal if we just return to good, ole fashioned (conservative/liberal) values.

• Depression (emotional, not economic) – “What’s the point in trying?” “We are all doomed anyway.” The certainty/finality of events is finally recognized.

• Acceptance – “It’s going to be okay.” Looking for opportunities begins.

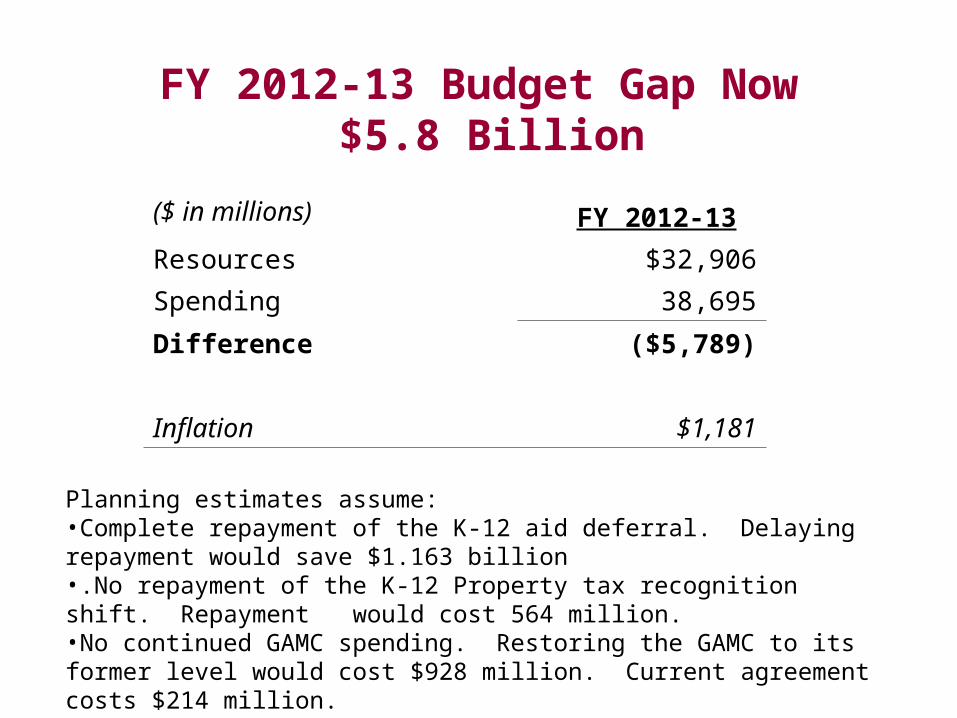

FY 2012-13 Budget Gap Now $5.8 Billion

($ in millions) FY 2012-13

Resources $32,906

Spending 38,695

Difference ($5,789)

Inflation $1,181

Planning estimates assume:•Complete repayment of the K-12 aid deferral. Delaying repayment would save $1.163 billion•.No repayment of the K-12 Property tax recognition shift. Repayment would cost 564 million.•No continued GAMC spending. Restoring the GAMC to its former level would cost $928 million. Current agreement costs $214 million.

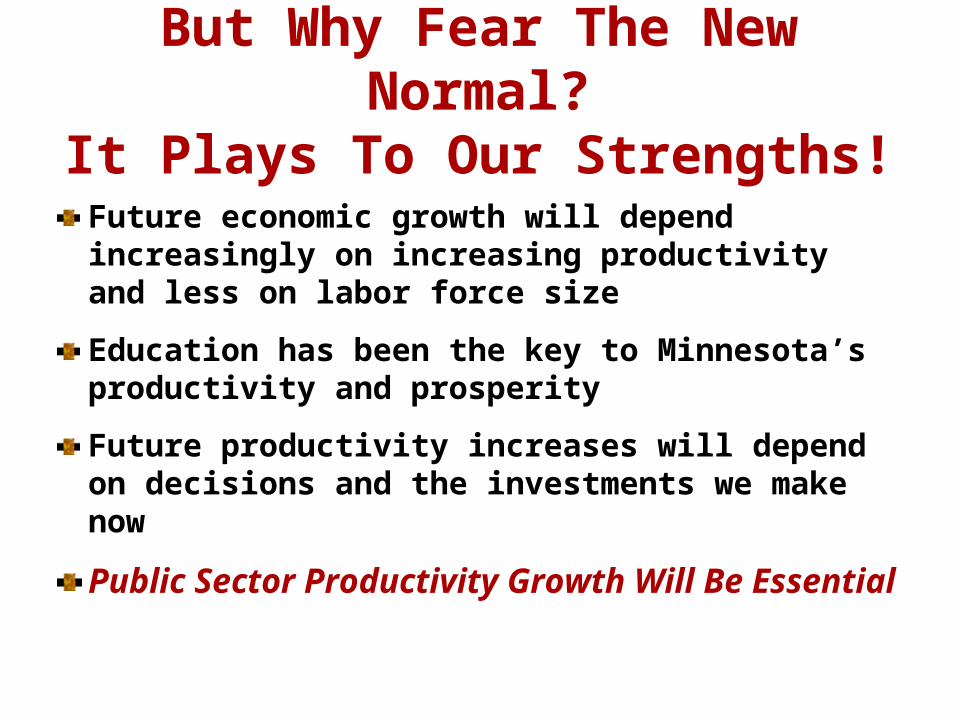

But Why Fear The New Normal?It Plays To Our Strengths!

Future economic growth will depend increasingly on increasing productivity and less on labor force size

Education has been the key to Minnesota’s productivity and prosperity

Future productivity increases will depend on decisions and the investments we make now

Public Sector Productivity Growth Will Be Essential