moberg pharma abd1q0gh225dp9f5.cloudfront.net/sites/default/files/moberg...moberg pharma ab...

TRANSCRIPT

0

Corporate presentation Redeye Life Science Day, 8 December 2015 Peter Wolpert, CEO & Founder

Moberg Pharma AB PROVIDING UNIQUE PRODUCTS IN UNDERSERVED NICHES

1

Disclaimer

1

Statements included herein that are not historical facts are forward-looking statements. Such forward-looking statements involve a number of risks and uncertainties and are subject to change at any time. In the event such risks or uncertainties materialize, Moberg Pharma’s results could be materially affected. The risks and uncertainties include, but are not limited to, risks associated with the inherent uncertainty of pharmaceutical research and product development, manufacturing and commercialization, the impact of competitive products, patents, legal challenges, government regulation and approval, Moberg Pharma’s ability to secure new products for commercialization and/or development and other risks and uncertainties detailed from time to time in Moberg Pharma’s interim or annual reports, prospectuses or press releases.

2

2

Net Sales grew to 276 MSEK (TTM, Q315) - U.S. OTC Sales operations - Products sold in 40+ countries - 35 employees in Sthlm and NJ

Focus in OTC/Dermatology/Topicals - Leading OTC SKU in Nail Fungus in North America and other markets - Preparing Ph III for MOB015, based on superior Ph II data

Market Cap ca 900 MSEK (OMX:MOB)

M&A strategy – 4 acquisitions in last 3 years

Moberg Pharma PROVIDING UNIQUE PRODUCTS IN UNDERSERVED NICHES

Q3 2015 – Rapid growth and doubled profit

4

4

Net sales grew by 32% to MSEK 67 (8% at fixed exchange rates)

Doubled profit and strong cash flow Cash position: 43 MSEK, Sep 30, 2015

Asian launch driving growth in distributor sales - Launched in 5 markets, including China - Preparing launches in several additional

Emtrix® rights in six EU markets taken back - Evaluating direct sales in UK and/or Poland

Progressing our Innovation engine - MOB-015 – Preparing Phase III - BUPI – Will soon get Phase II data - Continued focus on M&A

2015 Q3 Highlights

5

Net Sales, MSEK

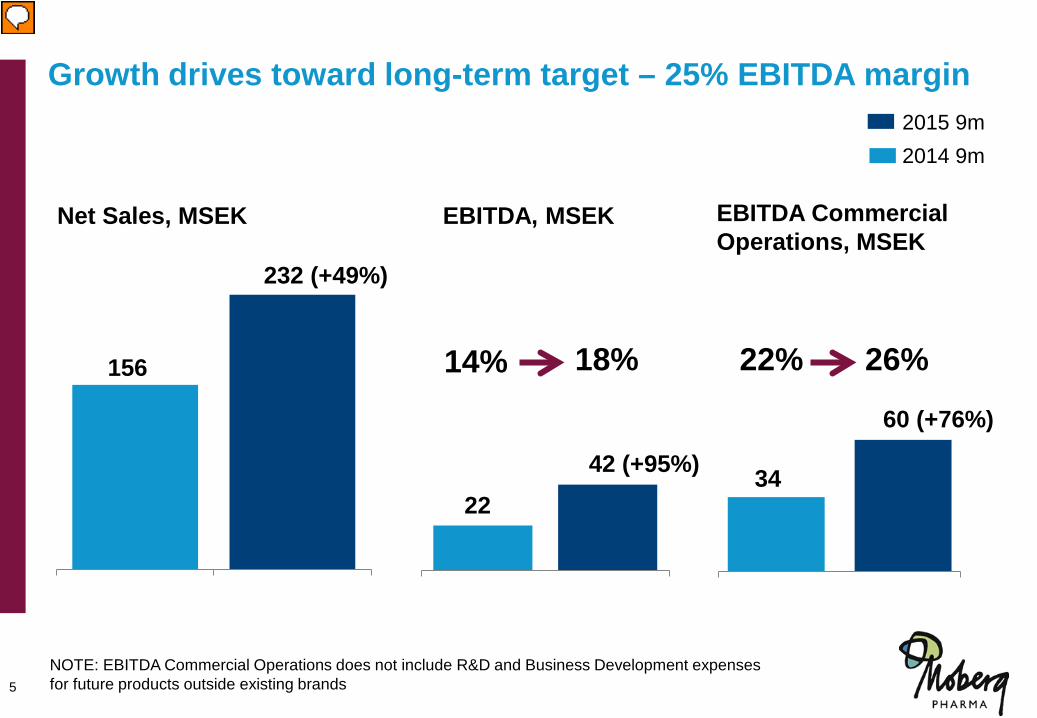

Growth drives toward long-term target – 25% EBITDA margin

5

232 (+49%)

156

EBITDA, MSEK

EBITDA Commercial Operations, MSEK

2015 9m 2014 9m

NOTE: EBITDA Commercial Operations does not include R&D and Business Development expenses for future products outside existing brands

22 42 (+95%)

14%

18%

22%

26%

60 (+76%)

34

6

22 consecutive quarters of Sales growth Product Sales, TTM, MSEK

6

0

50

100

150

200

250

300

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

7

P&L - Sales growth and doubling of profit

7

1) Research and development expenses – existing product portfolio includes R&D expenses for new product variants under existing brands, regulatory work and quality. 2) Research and development expenses - future products includes R&D expenses for new product candidates, for example MOB-015.

Due to the rounding component, totals may not tally.

P&L Summary Jul-Sep Jul-Sep Jan-Sep Jan-Sep Full-year

(MSEK) 2015 2014 2015 2014 2014 Revenue 67 50 232 156 200 Gross profit 49 36 177 119 151 % 73% 72% 76% 76% 75%

SG & A -31 -24 -116 -81 -106 R&D - existing product portfolio1) -1 -2 -5 -6 -7 Other operating income/operating expenses 1 2 4 2 6 EBITDA Commercial Operations 18 12 60 34 43 % 27% 23% 26% 22% 22%

R&D & BD - future products2) -4 -4 -18 -13 -18 EBITDA 14 7 42 22 25 % 21% 14% 18% 14% 13%

Depreciation/amortization -3 -2 -8 -6 -8 Operating profit (EBIT) 11 5 34 16 17

Progress in Commercial Operations

9

9

Strategic brands

Kerasal® - Foot care Emtrix®

Balmex ® - Diaper rash

Domeboro® - Derma/Skin irritation

Mature brands

Jointflex® - External analgesic

Vanquish® - Internal analgesic

Fergon® - Iron supplement

Focus on strategic brands

10

Kerasal Nail - the OTC market leader in the U.S.

10

No 1 with 24% market share in Q3 20151)

Key claim “visible difference in 2 weeks”. Product supported by 4 clinical studies

Available at >30 000 points of sale at all major U.S retailers

1)Retail sales of nail fungus products excluding private label in Multioutlet Stores over the last 52 weeks ending September 30, 2015 as reported by SymphonyIRI

11

TV commercial in Malaysia – aired from Q4 2014

11

12

Launches in Asia a key growth driver

12

Malaysia Launch Q4 2014, market leader

Hong Kong Excellent start of sales and reorders

Singapore Launch started, and ramped up

China Regional launch started in May

Indonesia Launch and TV started Aug 17

Other markets Launch preparations ongoing

Innovation Engine

14

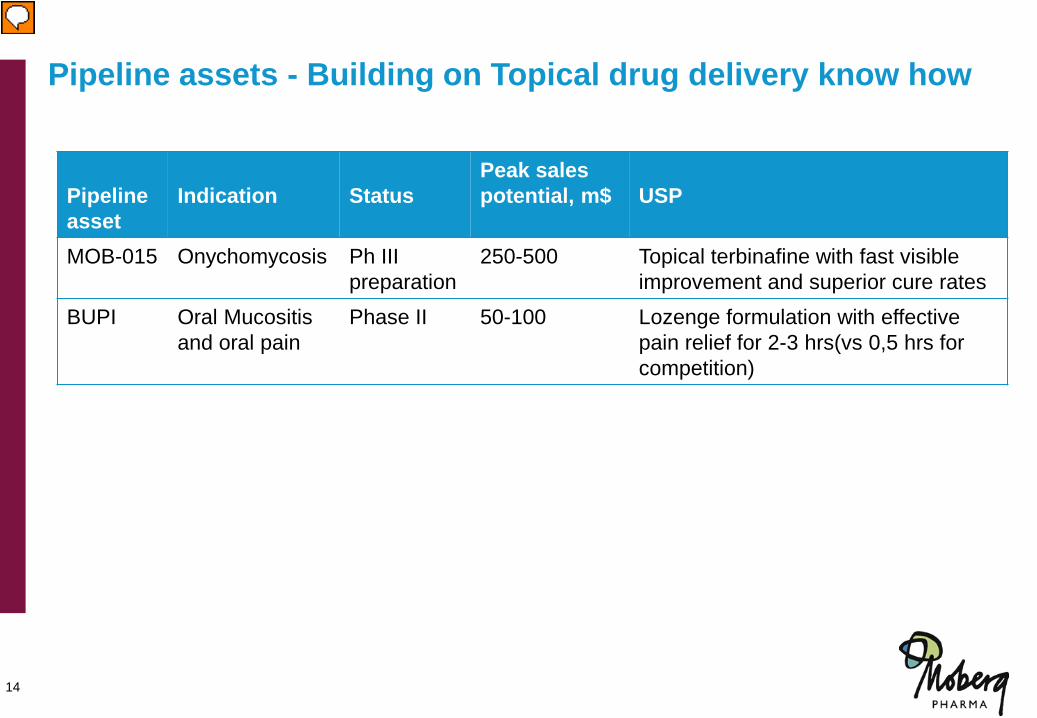

Pipeline assets - Building on Topical drug delivery know how

Pipeline asset

Indication

Status

Peak sales potential, m$

USP

MOB-015 Onychomycosis Ph III preparation

250-500 Topical terbinafine with fast visible improvement and superior cure rates

BUPI Oral Mucositis and oral pain

Phase II 50-100 Lozenge formulation with effective pain relief for 2-3 hrs(vs 0,5 hrs for competition)

14

15

MOB-015 – Business Case

15

Peak Sales $250 – 500 million (Total market > $3 billion) Ph III costs $10 – 15 million ROI case IRR > 100% rNPV > $100 – 200 million (risk-adjusted 50-100%) Conservative assumptions on Market share, upfronts, milestones, royalties & WACC

Source: Moberg Pharma analysis, Wolters Kluvers, IMS

16

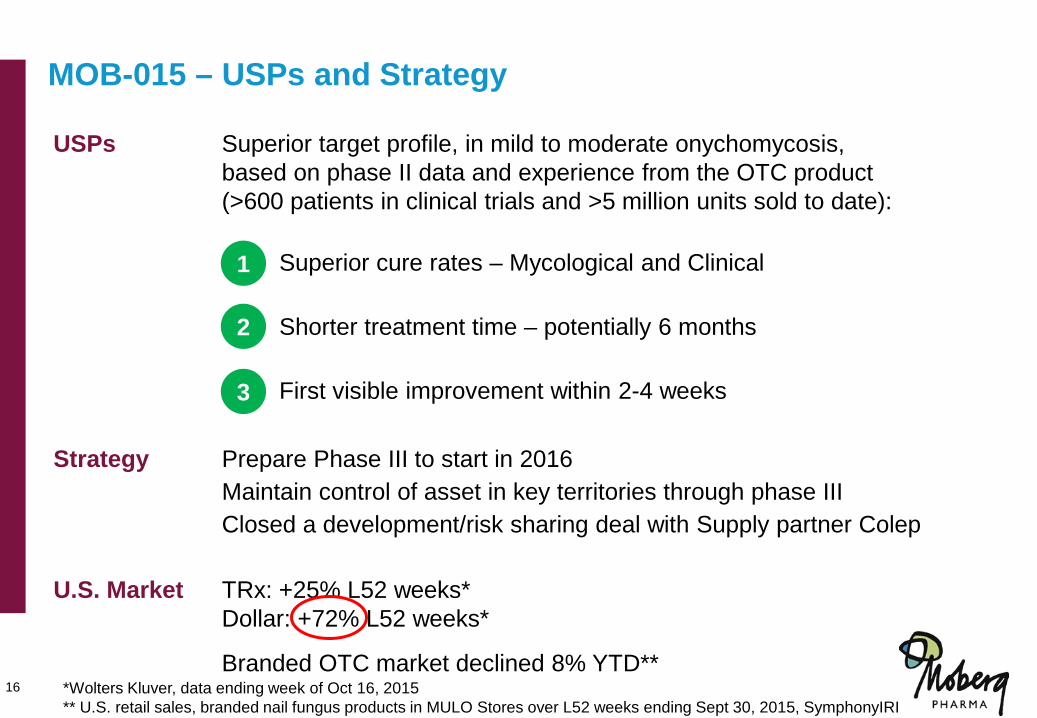

MOB-015 – USPs and Strategy

16

USPs Superior target profile, in mild to moderate onychomycosis, based on phase II data and experience from the OTC product (>600 patients in clinical trials and >5 million units sold to date): Superior cure rates – Mycological and Clinical Shorter treatment time – potentially 6 months First visible improvement within 2-4 weeks Strategy Prepare Phase III to start in 2016 Maintain control of asset in key territories through phase III Closed a development/risk sharing deal with Supply partner Colep U.S. Market TRx: +25% L52 weeks* Dollar: +72% L52 weeks*

Branded OTC market declined 8% YTD**

1

2

3

*Wolters Kluver, data ending week of Oct 16, 2015 ** U.S. retail sales, branded nail fungus products in MULO Stores over L52 weeks ending Sept 30, 2015, SymphonyIRI

17

Jublia U.S. launch confirms the potential for new topicals

17 Source: Valeant Investor Presentation AGM, May 2015, 3Q Earnings Deck, Oct 2015

3Q 2015 Sales = $106 million

18

18

54% 40% 100% 29% >4.5 mm jkjkj

45 µg/g 1610 µg/g

Source: Moberg Pharma data on file, MOB-015 phase II study

MYCOLOGICAL CURE AT 60 WEEKS* MYC CURE AT 24 WEEKS NEGATIVE CULTURE AT 60 WEEKS MYC CURE AND ALMOST CURED OR CURED** CLEAR NAIL GROWTH*** TBF IN NAIL BED (MEDIAN) TBF IN NAIL (MEDIAN)

* 54% of patients completing the treatment (13 of 25), 52% of FAS (13 of 24) and 60% of PPAS ** Means 10% or less clinical involvement *** Post-hoc analysis

MOB-015 Excellent results in Phase 2 demonstrated efficacy and safety

19

Example of successful treatment with MOB-015

Before After

19

20

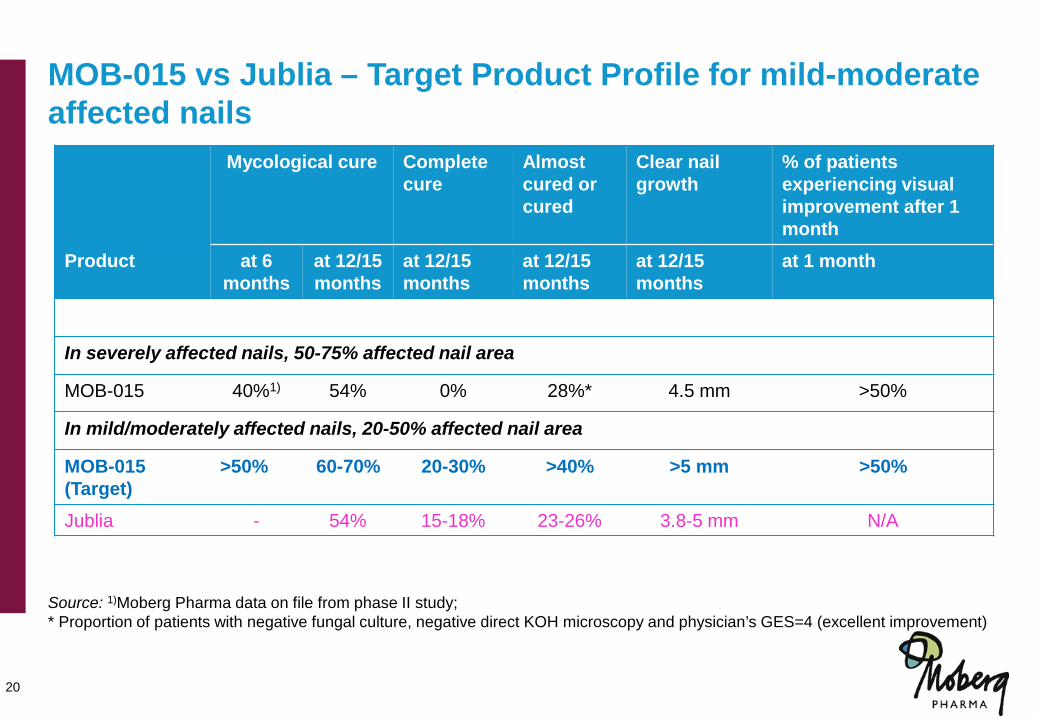

MOB-015 vs Jublia – Target Product Profile for mild-moderate affected nails

20

Mycological cure Complete cure

Almost cured or cured

Clear nail growth

% of patients experiencing visual improvement after 1 month

Product at 6 months

at 12/15 months

at 12/15 months

at 12/15 months

at 12/15 months

at 1 month

In severely affected nails, 50-75% affected nail area

MOB-015 40%1) 54% 0% 28%* 4.5 mm >50%

In mild/moderately affected nails, 20-50% affected nail area

MOB-015 (Target)

>50% 60-70% 20-30% >40% >5 mm >50%

Jublia - 54% 15-18% 23-26% 3.8-5 mm N/A

Source: 1)Moberg Pharma data on file from phase II study; * Proportion of patients with negative fungal culture, negative direct KOH microscopy and physician’s GES=4 (excellent improvement)

21

21

Commercial niche strategy enables a growing and profitable base business

Pipeline with large potential and at reasonable risk - Proven molecules limit development risk, cost and TTM

Acquisition strategy with substantial value potential - 4 acquisitions in 36 months - Team, Systems and infrastructure in place to enable scale-up

Strong Team with track record

Why invest in Moberg Pharma