mobile telecoms tech & market disruptions - april 2015 version

TRANSCRIPT

Mobile Telecoms Disruptions 2015-2020

Dean Bubley, Disruptive Analysis

April 2015

[email protected] @disruptivedean

About Disruptive Analysis

Tech/telecom analyst house & strategic consulting firm

Cross-silo, contrarian, independent

Forecasting & anti-forecasting

Consultant & advisor to telcos, vendors, regulators & investors

Speaker at 30+ events per year in Europe, US & Asia

Reports on Mobile Broadband, WebRTC etc

Twitter @disruptivedean Blog: disruptivewireless.blogspot.com

Copyright Disruptive Analysis Ltd 2015 April 2015

Many of the topics covered in this report tie into more detailed comment

pieces on the Disruptive Wireless blog

Coverage of this document

Introduction – overarching trends & challenges in telecoms

Reshaping the comms, telco service & Internet landscape Future of Voice (& video, messaging, WebRTC, context etc)

Service innovation / service curation for telcos

New roles & value chain (Apple SIM, Google MVNO etc)

The market, technical & regular battles for the mobile data 4G, WiFi, 5G networks

Spectrum considerations

Net Neutrality, zero-rating & sponsored data

Dangers of “creeping cellular-isation”

Copyright Disruptive Analysis Ltd 2015 April 2015

This document does not give all the answers or cover all strategic

areas. Contact [email protected] for a custom

private workshop or advisory engagement

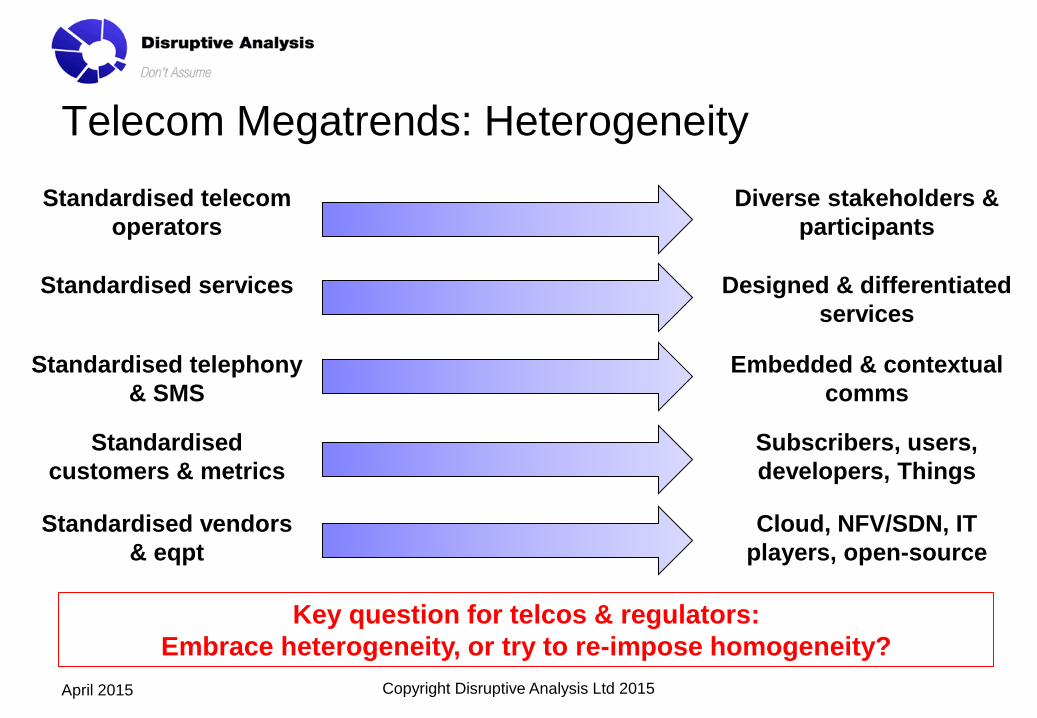

Telecom Megatrends: Heterogeneity

Copyright Disruptive Analysis Ltd 2015 April 2015

Standardised services Designed & differentiated

services

Standardised telecom

operators

Diverse stakeholders &

participants

Standardised

customers & metrics

Subscribers, users,

developers, Things

Standardised vendors

& eqpt

Cloud, NFV/SDN, IT

players, open-source

Standardised telephony

& SMS

Embedded & contextual

comms

Key question for telcos & regulators:

Embrace heterogeneity, or try to re-impose homogeneity?

The big problem

Copyright Disruptive Analysis Ltd 2015 April 2015

Beyond Peak Telephony

Top-level strategic options & threats for telcos

Copyright Disruptive Analysis Ltd 2015 April 2015

Mainstream Evolution

Digital Innovator

Vertical Specialist

Diversified Portfolio

Business Services & Wholesale

Focus

Evolved messaging

voice / video

Fragmentation & “OTTs”: The best tool for the job

Copyright Disruptive Analysis Ltd 2015 April 2015

Telcos vs. “OTT” is a logical fallacy (false dichotomy)

Telecom industry thinks of “voice” & “messaging” as services

In fact, they are capabilities for a given use / purpose

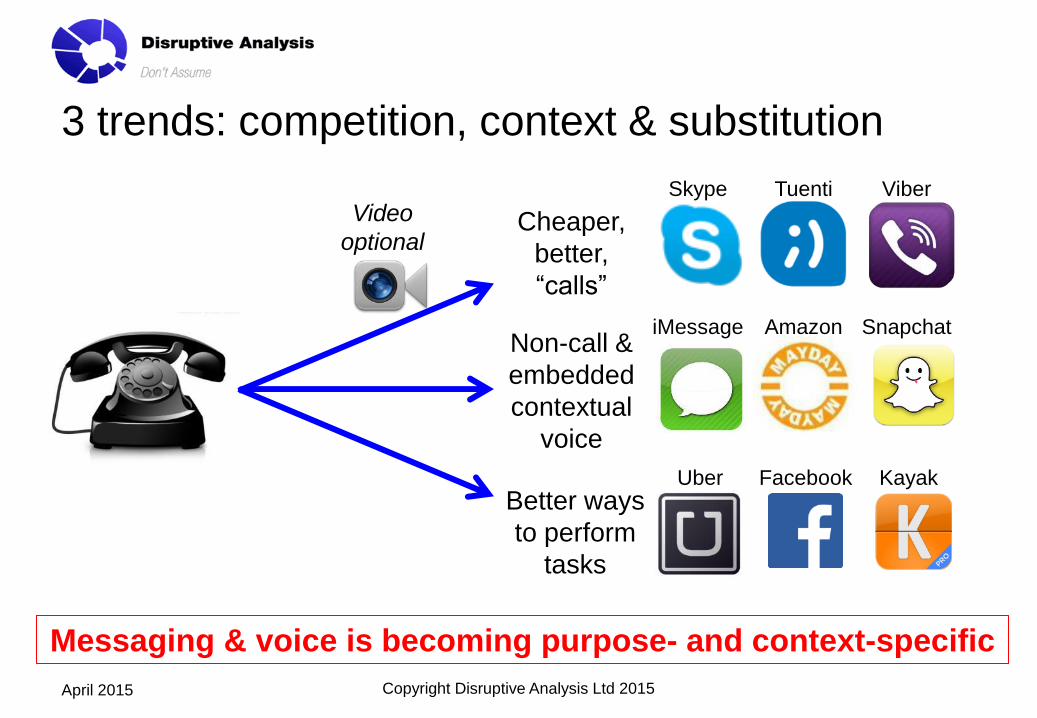

3 trends: competition, context & substitution

Copyright Disruptive Analysis Ltd 2015 April 2015

Cheaper,

better,

“calls”

Better ways

to perform

tasks

Non-call &

embedded

contextual

voice

Skype Tuenti Viber

iMessage Amazon Snapchat

Uber Facebook Kayak

Messaging & voice is becoming purpose- and context-specific

Video

optional

Communications in Context

Copyright Disruptive Analysis Ltd 2015 April 2015

In-app In-Browser In-Thing

VoLTE: Slow growth vs. contextual headwinds

Core business of telephony under threat

Competition from direct & indirect substitutes

“Official” new standard of VoLTE is too little, too late

Bundling & data-led prices just delay the inevitable

Copyright Disruptive Analysis Ltd 2015 April 2015

Source: Disruptive Analysis

LTE uptake not mirrored by VoLTE use “Phone calls” slowly becoming obsolete

Peak telephony a reality in developed markets

Copyright Disruptive Analysis Ltd 2015 April 2015

136%

74%

63%

40% 38%

15% 15%

5% 5% 1% 0%

0% - 7% - 7%

- 12% - 14% - 14% -20%

0%

20%

40%

60%

80%

100%

120%

140%

160%

IND CHN BRA RUS POL SGP FRA AUS JPN ITA KOR

GER NED USA ESP SWE UK

Source: Ofcom, IHS, Disruptive Analysis

Aggregate Fixed+Mobile Outgoing Voice Telephony

Volumes, Minutes, 2013 vs. 2008

VoLTE Status (GSA, Jan’15)

Copyright Disruptive Analysis Ltd 2015 April 2015

• 50-100 VoLTE

networks expected live

by end-2015

• ViLTE video irrelevant

• RCS useless & unused

• Most will not reach all

areas / subs / phones /

usage

• Complex & costly

• Needs IMS, upgrade to

core network etc

• Telephony v1.1 not a

ground-up rethink of

voice

WebRTC: #1 catalyst for voice / video evolution

Puts voice/video into

browsers & mobile apps

Enables thousands more

developers to do comms

Can be used to extend telco

voice/VoLTE too

Oppo’s for telcos in PaaS,

enterprise comms, UC/DUC

But will be very fast-moving &

very crowded

Players include Google,

Ericsson, Cisco, Avaya etc

Leading telcos: Telefonica,

NTT, Telenor, AT&T, Tata

Copyright Disruptive Analysis Ltd 2015 April 2015

0

1000

2000

3000

4000

5000

6000

7000

2011 2012 2013 2014 2015 2016 2017 2018 2019

Other (TV+M2M/IoT)

Smartphones

Tablets

PCs

WebRTC-enabled

devices, m installed

base, year-end

Source: Disruptive Analysis Q1 2015 WebRTC update

Next phase of voice/video innovation starting now

Two equal domains for telco service innovation

Copyright Disruptive Analysis Ltd 2015 April 2015

Network-based

services

(IMS, SS7, IPTV etc)

Non-network based

services (Telco-OTT, partners etc)

Internal telco APIs, NFV resources,

bundling, OTT extensions etc

Policy & innovation…… …..vs. politics

Copyright Disruptive Analysis Ltd 2015 April 2015

Strategy

Telco execs & central

labs

In-house apps & content

Marketing / Product

IT Core network

Radio network

Devices

Legal

Tensions

Tensions

Distance

Tensions

New stakeholders in telecom services creation

Copyright Disruptive Analysis Ltd 2015 April 2015

Telco /

MSO

End-user

Vendors &

standards

Services creation

Experiences

consumption

Experiences curator

Experiences designer

Experiences developer

Cloud

API

player IT vendor

Platform creation

Open-

source

In-house

develop-

ment

Element creation

SIM-card evolution: Apple & beyond Trend Likelihood / extent Impact on MNOs

Full Soft-SIM & MVNOs by Apple etc Limited / theory only Major risk but likely far

off / never

eUICC for M2M Already starting Beneficial

Programmable / eUICC for tablets Apple SIM Poss up/downsides,

sentiment hit

Programmable / eUICC for phones Maybe. No signs yet Risky but complex

Multi-IMSI M(V)NOs Existing but niche eg

Truphone, Google Minor impact

Multi-SIM devices Common Easy switching

MNC liberalisation, new MVNO models Slow & patchy

changes Unpredictable

Copyright Disruptive Analysis Ltd 2015 April 2015

Google Fi MVNO

Announced April 2015

Interesting, but only trial stage & some good / some bad aspects

US-based, uses multi-IMSI SIM on T-Mobile US & Sprint

WiFi via a curated network – details of locations/partners unclear

Only available on $650 Nexus 6 device ($27/mo financed)

Not cheap for US domestic use at $20/mo + $10/GB + taxes

Good value for outbound US roamers as $10/GB in 120 countries, 20c/min

Allows multi-device telephony & SMS, but needs Hangouts for this

Unclear data/privacy implications – but auto-VPN use on WiFi is cool

Model is very hard to extend internationally (MVNO regulation & deals,

porting number to Google Voice/Hangouts, data/privacy etc)

Copyright Disruptive Analysis Ltd 2015 April 2015

Overall: worth watching & some nice ideas, but not a big deal for now

Data traffic growth: is there really a “tsunami”? Rapid growth of 4G user-adoption & continued network deployment….

… 500m+ subs, but next billion users will be lower-ARPU / data-users

Many forecasts overlook shift to prepay segment (& use of WiFi)

Mean data-use brought down by late-adopters (falling median)

“Congestion” just a convenient pseudo myth to persuade regulators / ITU?

Copyright Disruptive Analysis Ltd 2015 April 2015

0%

50%

100%

150%

200%

250%

'11 '12 '13 '14 '15 '16 '17 '18 '19 '20

Subscriber numbers

Data per subscriber

Smartphone 3G/4G data traffic growth

Source: Ericsson, Disruptive Analysis

Dominated by

subs growth

Unrealistic view of

usage growth in

prepay-dominated

market?

0

500

1000

1500

2000

2500

3000

3500

4000

4500

'12 '13 '14 '15 '16 '17 '18 '19

Postpaid

Prepaid

Mobile data subs, year-end, m

Source: Disruptive Analysis Mobile Broadband report

Mostly fixed

monthly quotas

Incentivised to

use less data?

Traffic & spectrum forecasts overcooked?

Copyright Disruptive Analysis Ltd 2015 April 2015

585% increase in 4G users

149% increase in 4G usage

Early adopters = heaviest

Late adopters use less

Traffic growth mostly subs #

Incremental use grows slowly

M2M/IoT mostly small

Only c10% cells congested

Source: Vodafone

Application-based mobile data models

Mobile Data models

Neutral open access

User pays for all data

Certain data zero-rated

Certain data sponsored

Partial Internet access

Specific applications

allowed

Specific applications

blocked

Differentiated Internet access

Paid priority “specialised”

services

Differentiated Wholesale /

MVNO

Copyright Disruptive Analysis Ltd 2014 April 2015

Many of today’s mobile broadband plans

“Fully neutral mobile Internet”

Data treated equally, charged

differently: “Grey Area”

Data treated differently by network

“Non-Neutral”

Neutrality, Zero-rating & “Specialised Services” Ongoing debates in US, Europe, elsewhere. Asia more relaxed

No obvious major new workable sources of revenue AT&T Sponsored Data very limited uptake. Bharti Airtel likely to be similar

Threat of future “Internet regulation” (eg TRAI) increases risk / uncertainty Also mostly unworkable (encryption, definitions, mashups, WiFi, speed of change etc)

Prisoners’ dilemmas may drive lose-lose outcomes

Copyright Disruptive Analysis Ltd 2015 April 2015

QoS, Sponsored Data etc have little

impact on potential mobile data revenue

Source: Disruptive Analysis Mobile Broadband report

Net Neutrality does not necessarily

impact investment: eg Netherlands

Sponsored data – attractiveness matrix

Copyright Disruptive Analysis Ltd 2015 April 2015

Ads Web Apps BYOD

Ease of implementation

Ease of selling by telco

Ease of buying by client

Revenue potential

Impact on network

Reputational risk

Market maturity required

Workarounds/"gotchas"

Adjacent revenues/costs

Prevalence 2014

Prevalence 2019

Sponsored data for:

Good

Fair

Poor

Bad

Source: Disruptive Analysis “Non-Neutral Mobile Broadband” report, Dec 2014

Attractiveness for mobile operators vs. key criteria

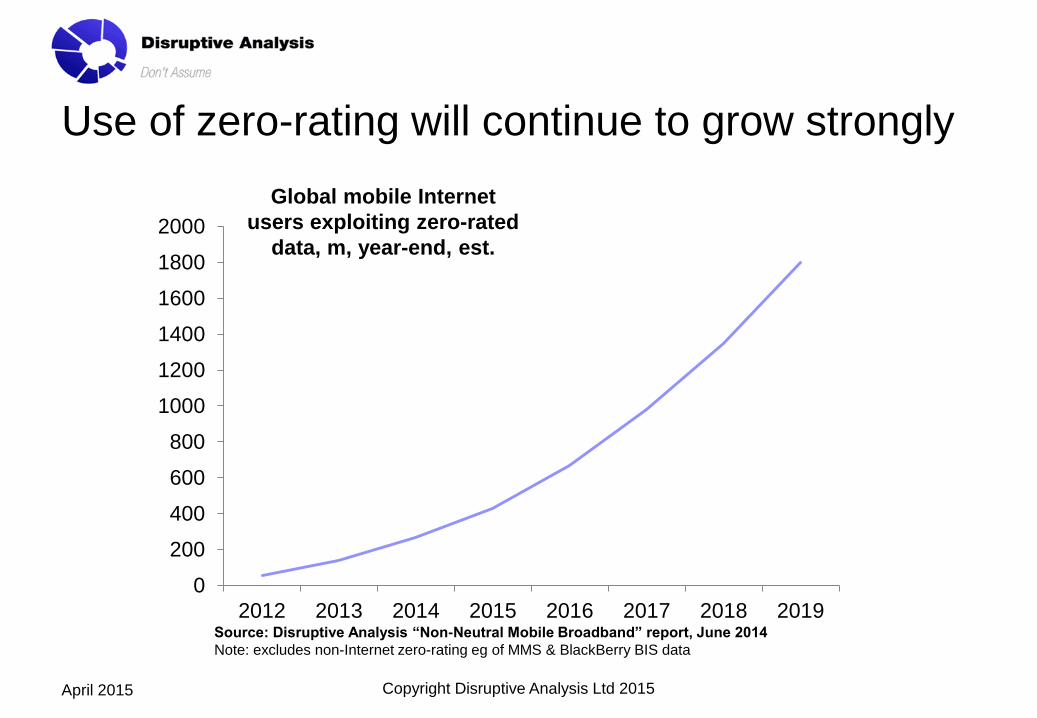

Use of zero-rating will continue to grow strongly

Copyright Disruptive Analysis Ltd 2015 April 2015

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2012 2013 2014 2015 2016 2017 2018 2019

Global mobile Internet

users exploiting zero-rated

data, m, year-end, est.

Source: Disruptive Analysis “Non-Neutral Mobile Broadband” report, June 2014

Note: excludes non-Internet zero-rating eg of MMS & BlackBerry BIS data

Towards 5G - the underlying story…

“We need more spectrum to contain the forecast* growth of current

3G/4G mobile data uses & biz models.

We’re designing 5G to absorb many other uses, as well as

continued forecast* growth of the current ones, so we’ll need much

more spectrum in future too.

We’re not huge fans of WiFi & alternative mobile architectures that

consume spectrum, add competition & arbitrage, unless we can

integrate & control them. Or displace them entirely”

*rather aggressive & questionable forecasts

Copyright Disruptive Analysis Ltd 2015 April 2015

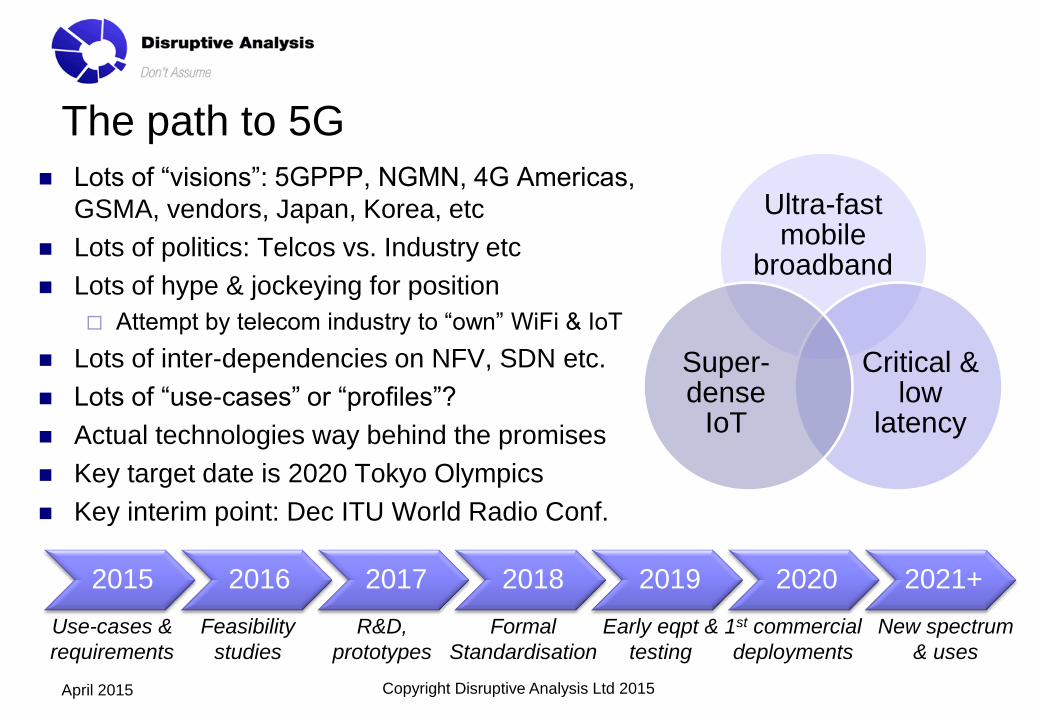

The path to 5G

Lots of “visions”: 5GPPP, NGMN, 4G Americas,

GSMA, vendors, Japan, Korea, etc

Lots of politics: Telcos vs. Industry etc

Lots of hype & jockeying for position

Attempt by telecom industry to “own” WiFi & IoT

Lots of inter-dependencies on NFV, SDN etc.

Lots of “use-cases” or “profiles”?

Actual technologies way behind the promises

Key target date is 2020 Tokyo Olympics

Key interim point: Dec ITU World Radio Conf.

Copyright Disruptive Analysis Ltd 2015 April 2015

Ultra-fast mobile

broadband

Critical & low

latency

Super-dense

IoT

2015 2016 2017 2018 2019 2020 2021+

Use-cases &

requirements

Feasibility

studies

R&D,

prototypes

Formal

Standardisation

Early eqpt &

testing

1st commercial

deployments

New spectrum

& uses

Specifying 5G needs to be multi-stakeholder

Copyright Disruptive Analysis Ltd 2015 April 2015

5G

MNOs

Govt & cities

Large Co’s

App/IT Co’s

Users

Requirements

Telco Vendors

M2M & IoT

Acad- emia

Web Co’s

IT vendors

Innovations

5G must not just be another telco/vendor-defined technology. Other parties –

Cities, App/Internet players, Transport & other players need to be involved

WiFi = multi-stakeholder & complex landscape

Copyright Disruptive Analysis Ltd 2015 April 2015

User Mobile

operator

Venue Fixed/cable

operator

App /

content

OS / OEM

Employer

/ sponsor

Many groups excluded

from standards /

regulatory discussions Advertiser

/ brand

Do we need “WiFi Neutrality” regulations?

“Seamless handover” sounds compelling…

… until one considers that “seams” are decision-points users &

applications, about which network/biz models to use

Some early signs of concern among regulators about telcos dominating /

over-exploiting WiFi spectrum (eg Israel nearly banned WiFi offload)

Many 3GPP & related technologies aimed at integrating WiFi with cellular

(ANDSF, I-WLAN, EAP-SIM, Passpoint, HotSpot 2.0…)

Some add user utility & value, others reduce choice & options, or reduce

WiFi utility for other stakeholder groups

Who has “admin rights” over WiFi selection, on/off, preference lists etc. ?

Some arguments for specific instances (eg disallowing children access to

“fully open” 3rd-party WiFi, or enterprises choosing based on security)

Regulators have not addressed this issue so far. Little analysis of “3rd-

party WiFi as partial access competition to cellular”

Copyright Disruptive Analysis Ltd 2015 April 2015

Other “Disruptive” trends & opinions

Privacy & encryption becoming more important post-Snowden

LTE-U / LAA has a lot of questionmarks, tech & regulatory

Lots going on with enterprise & cloud comms – watch MS

Lync / Skype4B, IM/social-centric & various PaaS

Trend to “disunified” comms out-stripping “unified comms”

Telco developer platforms struggle without “anchor tenants”

Security is a major oppo (& threat) for telecoms operators

SDN & NFV likely game-changers, but patchy & slow

IoT is important but fragmented. Watch low-power networks

Reach & impact of Apple, Facebook, Amazon, Google,

Microsoft cannot be underestimated. Watch capex & R&D

Copyright Disruptive Analysis Ltd 2015 April 2015

Copyright Disruptive Analysis Ltd 2015 April 2015

Want a private “Telecom Disruptions” workshop for your company?

For details email [email protected]

www.disruptive-analysis.com

disruptivewireless.blogspot.com

@disruptivedean

Skype:disruptiveanalysis

Copyright Disruptive Analysis Ltd 2015 April 2015