module 007: competitive pricing of construction · pdf filebuild up analytical unit rates and...

TRANSCRIPT

Module 007: Competitive Pricing

of Construction Works

Module code: NCC/WB/007 Level: A +B CPD Points: 2.4 Guided learning hours: 24 Developed for NCC by:

Ms B. Mwiya Prof. M. Muya Dr L. Matakala Dr. E. Mwanaumo Mr C. Kaliba Mr S. Sanga

Aim and purpose This module will guide and assist participants in developing essential procedures and a systematic approach to quoting and ‘Wining the Work’. It will give learners the opportunity to develop skills needed to calculate unit rates for an element or trade section of a bill of quantities in tender production. Learning outcomes On completion of this module a learner should: 1. Know the basic information needed to produce a tender; 2. Be able to calculate unit rates for an element or trade section of a bill of quantities; and 3. Be able to produce a tender for a specific construction trade or element.

National Council for Construction Training Manual Competitive Pricing of Construction Works

Page | ii

Module Overview These days competition is what it is all about. Wasted time and money on unsuccessful tenders must be reduced. Most builders and contractors believe that their estimating is orderly and accurate, when in fact they could be missing out on substantial work and profit. The estimator produces an estimate of project cost to enable the company to submit a tender after the decision has been made on the amount of profit to add to the project. This decision is based on the company’s required return whilst taking into account their current workload and advance order book, level of risk associated with the project, the current and future market conditions, and the perceived workload or current order book of competitors who may also tender for the project. Learners will become aware of the need to work with great accuracy as any errors could lead to financial losses or an unsuccessful tender. After completing this module learners will be able to build up analytical unit rates and apply them to tender documentation in order to produce a tender for construction work, taking into account the commercial decisions to be made in arriving at a tender sum. Designed for: Owner/Managers, Administrators, Sole Trader, Partnerships, Small Company Structures

National Council for Construction Competitive Pricing of Construction Works Training Manual

Page | 3

COMPETITIVE PRICING OF CONSTRUCTION WORKS

CourseContents1 ESTIMATING .................................................................................................................... 4

1.1 Definition: ................................................................................................................... 4

1.2 Types of Estimating .................................................................................................... 4

1.2.1 Approximate Estimate ......................................................................................... 4

1.2.2 Superficial or Floor Area Method ........................................................................ 5

1.2.3 Approximate Quantities ....................................................................................... 5

2 Introduction to Unit Rate .................................................................................................... 6

2.1 Bid Based Estimate (Historical) .................................................................................. 6

2.1.1 Bid Price Adjustments ......................................................................................... 7

2.1.2 Summary .............................................................................................................. 7

2.2 Cost Based Estimate (First Principles) ........................................................................ 8

2.2.1 Cost of Labour ..................................................................................................... 8

2.2.2 Cost of Materials ................................................................................................ 10

2.2.3 Cost of Plant & Equipment ................................................................................ 11

2.2.4 Preliminary and General Items .......................................................................... 12

2.2.5 Estimating Lump Sum Items ............................................................................. 13

2.2.6 Subcontractors .................................................................................................... 13

2.2.7 Provisional and Prime Cost (PC) Sums ............................................................. 14

2.2.8 Escalation ........................................................................................................... 14

2.2.9 Overheads .......................................................................................................... 15

2.2.10 Profit .................................................................................................................. 15

2.3 Cost implications in Variations and Extension of Time ........................................... 16

2.3.1 Variations ........................................................................................................... 16

2.3.2 Extension of time ............................................................................................... 17

3 Appendices ....................................................................................................................... 19

3.1 All - in construction worker rates .............................................................................. 19

3.2 All in Plant & Equipment Rate ................................................................................. 22

3.3 Build up rates from first principles ........................................................................... 23

3.4 Variation submission ................................................................................................. 24

3.5 Extension of time application .................................................................................... 25

National Council for Construction Training Manual Competitive Pricing of Construction Works

Page | 4

1 ESTIMATING

1.1 DEFINITION: Estimating is defined as the technical process of predicting cost of construction. It involves both calculation and assessment of technical data and human judgment of circumstances and probabilities which must be brought together in its production.

1.2 TYPES OF ESTIMATING

1.2.1 Approximate Estimate a) Unit Method

This method produces total single price for the project and is based on cost per unit or person to be accommodated. This technique is between the cost of the construction and the number of functional unit it accommodates. Examples are:

schools cost/ student place;

hospital accommodation cost/bed space;

hostel cost/bed space;

cinema cost/sit;

hotel cost/room;

stadium cost/sit;

church cost/space; Total estimate cost is equal to no of functional unit multiply by unit rate. A lot of skill is required in selecting an appropriate rate. Rates can be obtained by careful analysis of the number of recently completed projects of similar types, size and constructional method. However, adjustment would need to be made to account for:

varying site condition;

specification changes; and

market condition. Advantage

It is simple and quick to use Disadvantage

Lack of precision

It is advisable to express cost within a range of prices

b) Cube Method This method was used extensively between the World War I and World War II. But it is not in common used anymore. Rules of must as defined by Royal Institute of British Architect (RIBA) are external plan area of a building is multiply by a height to get the volume of the building. The height is measured from the top of concrete foundation to half way of the roof if pitched or to 600mm above the roof if flat. If the roof space is occupied the height is taken up to ¾ (0.75) way up the roof. If the flat roof has a parapet, the height is taken up to the top of the parapet or 600mm whichever is greater. Total estimated cost is equal to cubic content/m3 multiply by cost/m3

All projections such as porches, steps, domes, bays are measures and added to the cubic content of the building. Where parts of the building vary substantially in constructional method or quantity of finish then it is preferable to calculate separate volume and to apply different rate. Advantage

It is useful in estimating the cost of heating and air conditioning

National Council for Construction Competitive Pricing of Construction Works Training Manual

Page | 5

Disadvantages Building cost could relate better in floor area than with volume

It does not give the client an indication of the amount of the usable floor area

It takes no account of number of stories or plan shape which is known to affect cost.

It produces a large cubic quantity that will increase the possibility of further inaccuracy in estimating.

Large amount of variation have been known to occur in case rate of building of the same type

1.2.2 Superficial or Floor Area Method This is probably the most popular method of cost prediction during the early stages of a project once the general outline drawings are been prepared, the method relate a unit cost to floor area and is more readily appreciated. The area of each of the floor is measured and then multiply by cost/m2

by the convention the superficial area is measured between the inside faces of the external wall and no deduction are made for partitions, stairs, lifts etc. It should be borne in mind that if the client expresses his requirement in term of usable space, it is necessary to add to this area, circulation and other non-usable space to make the building function correct. The rate to be used is usually obtained from cost analysis of previously completed building of similar plan shape, storey height level of finish and method of construction, certain rules must be applied.

if the building is made up of parts that varies substantially in terms of quality of finish and construction method, it is preferable to price it independently using rates appropriate for each part. Items of work which cannot be related to the floor area will need to be priced at separate rate or using different methods and added items such as piling, heating and air conditioning, lift installation and external work. Allowances should be made for site condition, construction method, materials, quality of finish and number and quality of fittings. Total estimated cost equal to gross floor area multiply by cost/m2

Advantage Ease of calculation

Cost are expressed in a way which is readily understood by the average building client

Rates are readily available from many sources and also can be very easily calculated from existing project.

Majority of items in the building and the cost impact are related more to floor area than the volume

Disadvantages Does not directly take account in changes in plan shape or total height of the building

which also have a cost impact.

Adjusting from the variables mention is not easy

1.2.3 Approximate Quantities This method is probably the most favoured by quantity surveyor because it used idea which are similar to those used in preparing bill of quantities. It provides a more detailed estimate than the other method described. Quantities are measured from the drawings and similar omnibus description is given to this measurement. The description will include all items which are associated with that drawing. Example a floor slab will include the stripping of vegetable soil, reduced level excavation, hardcore filling under the floor, concrete bed and reinforcement. An upper floor will

National Council for Construction Training Manual Competitive Pricing of Construction Works

Page | 6

include the ceiling finish and painting of the surface of the slab, the floor construction, the floor screed and floor finish. Using approximate quantities: the strip foundation as 1m depth level and compacting, deldrin anti-termite treatment. Back filling, disposal of surplus material from site, concrete (1:3:6) in foundation 200mm thick, 200mm hollow concrete blockwall in cement mortar (1:4) filled solid with weak concrete. The item is then given a composite price to include every unit in this extended description. Special paper is printed for this form of estimating. It has dimension column on the left and the usual billing price column on the right. With a multi rate system, it is essential to allow for preliminary and contingency in addition to the actual cost of work in pricing also care must be taken to include for all the items ion the description and make any necessary allowance for minor work or labour covered by the overall measurement and prices, accuracy of this method is high, changes in design shape and specification can be allow for both the preparation and calculation is lengthy and labourous. Advantages

It is reliable and give a more detail estimate than any other method

In practice only major items that are of course important are measured Disadvantages

It required more time and effort than any other method

More detail information is required from the designer and with other method

2 INTRODUCTION TO UNIT RATE To analyse something is to break it down into its constituent parts and study each part in detail. Therefore analytical estimating involves the analysis and costing of construction resources to produce an estimate. The production of an estimate normally involves the calculation of unit rates i.e. the cost of an individual measured item for example a square metre of brickwork, a cubic metre of concrete or a metre of skirting as found in a Bill of Quantities. Analytical estimating is therefore the most accurate form of estimating as each resource and unit rate is analysed and costed individually. This form of estimating is used for pricing contracts with bills of quantities, specifications and drawings or where the contractor has measured and prepared their own quantities of work. Unit rate estimating can employ bid based (historical) or cost based (first principle) estimates

2.1 BID BASED ESTIMATE (HISTORICAL) Creating cost estimates from historic bid prices is a relatively straightforward process. After determining the quantities for different items from project plans, the estimator matches the items to appropriate historical unit bid prices or to average historic unit bid prices. Historical bid-based estimating uses data from recent contracts as the basis for determining estimated unit prices for a future project. Historical bid price data from previously let projects are typically stored in a database for 3 to 5 years. However, for price averaging and use in new estimates, the data retrieval period is often limited to 1 to 2 years, unless there is not sufficient bid data for an item, in which case dated data must be used. In such an instance, the estimator may search the bid database across a longer time period. Historical data can be easily sorted and analyzed in a multitude of ways. The prices for the new estimate should be adjusted for specific project conditions in comparison to the previously bid projects. However, there are many factors that need to be considered to develop an

National Council for Construction Competitive Pricing of Construction Works Training Manual

Page | 7

accurate construction estimate using historical bid prices. These factors can pose a certain level of risk in using this method to develop an estimate. Consequently, the estimator must ensure that the selected historical prices match the conditions of the project being estimated.

2.1.1 Bid Price Adjustments a) Geographic considerations

Geographic considerations can have a profound effect on the selection of unit bid prices. A project’s location, whether in an urban, suburban, or rural setting, and in relation to material supply sources should be considered in establishing prices for an estimate.

b) Quantity Considerations The plan or expected quantity of a given work item affects the unit cost of constructing and/or supplying the item. Generally speaking, the unit price for larger quantities of a given material will be less than smaller quantities. Suppliers offer discounts for larger quantity orders, and mobilization, overhead, and profit are all spread out over a larger quantity, thereby reducing their effect on a per-unit basis. Waste is also spread over a larger quantity, thereby having a smaller impact on unit cost. Larger quantities give rise to efficiency by gaining experience and expertise in completing the work.

c) Item Availability Materials that are readily available or ones that are commonly used are generally less expensive to purchase and install/construct. The contracting community is familiar with these types of items, and this experience reduces costs and risks. Non-standard pay items or materials that are in short supply are usually more expensive, and this should be considered in establishing the unit price.

d) Scheduling/Lead Time When a contractor can plan for and maximize resource utilization, the contractor can be more competitive pricing the work. Lead time needs to be considered in the estimating process by estimating the project based upon when it will be built.

e) Difficult Construction/Site Constraints Difficult construction and site constraints will increase the cost of construction for a contractor. Placing piles under water, working near active railroads or adjacent to historic buildings (possibly fragile), constructing on or near environmentally hazardous sites, and having limited room to construct an item are all examples of constraints that should be considered when deriving an estimated unit price.

f) Risk Analysis and Contingency Adjustment of item bid prices for risks should be clearly documented. The estimator is probably in the best position to assess the uncertainty associated with bid pricing. If quantities are determined by the estimator, this person should also provide input on uncertainty associated with any quantity take-off. The estimator should adjust bid prices to reflect uncertainty associated with the particular item of work being estimated. This uncertainty should be captured in the bid price as an adjustment (i.e., contingency).

2.1.2 Summary Advantages

Straight forward process

Reduced estimate preparation time Disadvantages

Database of bid data must be maintained;

National Council for Construction Training Manual Competitive Pricing of Construction Works

Page | 8

Consistent bid items must be utilized for all contracts, and the work covered by these bid items must be consistent.

Difficult for lump-sum items

During times of rapidly fluctuating prices, it is advisable to limit the period of time from which unit bid data are analysed

Thoroughly understand the project characteristics of the similar project to adjust the project bid prices to reflect the similar project being estimated.

If the item in question is unique in some manner, whether it is innovative, new, or experimental, or is considered a specialty item, costs may need to be adjusted to account for the contractor’s unfamiliarity with the work and potential increased risk in construction

Historical approach is not ideal for Zambia due to the lack of construction cost indices

2.2 COST BASED ESTIMATE (FIRST PRINCIPLES) Contractors typically use cost-based estimating methods for arriving at a contract bid price. Such estimates reflect the cost to construct the specified work in the most economical manner based on the contractor’s capability and considering the time allowed by the contract. These detailed task-by-task estimates reflect the unique character of a project, geographical influences, market factors, and the volatility of material prices. In addition to the direct costs for performing the tasks, indirect costs of project overhead expense are calculated and a reserve to protect for project risk is determined. Finally, to arrive at a bid number, the contractor adds a desired profit amount to the total estimate of project expenses. Cost-based estimating requires the estimator to carefully review the construction requirements as described in the contract documents, visualize the construction process, and model the costs to complete the work. These estimates are based on many sub-estimates of work crews and equipment completing tasks at assumed rates of productivity. Bid items are broken down into detailed task-by-task work activities. The direct cost for each task is developed with separate costs for the labour, equipment, subcontractor, and material components of the work required to complete a task. Cost-based estimating uses the latest price data for materials, equipment, and labour, so unlike bid-based estimating that used historical data, it provides a much more accurate projection of costs during periods when prices are escalating rapidly. Unit Rates maybe calculated in one of two ways:

Net Rate – (Excludes Overheads and Profit)

Gross Rate – (Includes Overheads and Profit) In our industry, most estimators will calculate costs based on net rates these will then be enhanced later to include overheads and profit. The resources which compromise a unit rate are direct cost namely labour, materials and plant, then add an overhead expense, a risk amount, and a reasonable profit amount.

2.2.1 Cost of Labour Labour may be paid for on an hourly, daily, weekly or piecework basis. Directly employed operatives are usually paid in accordance with a working rule agreement which will specify the rates and allowances to be paid. Cost of labour considers the recognized basic wage rate for both skilled and unskilled operatives, as stipulated by ABCEC including appropriate allowances, employer’s statutory payments and other payments relating to union or trade agreement. The

National Council for Construction Competitive Pricing of Construction Works Training Manual

Page | 9

estimator calculates a labour rate per hour which is realistic and which reflects the actual cost of labour to the contractors. According to ABCEC agreement the following items are included in arriving at the ‘all-in’ labour rate. a) Basic wage rates b) Holiday Pay (annual leave) c) Sick leave d) Occasional leave e) Public holidays f) Inclement weather g) Overtime h) Housing allowance i) Tool allowance j) Service benefits k) NAPSA l) WCF m) Protective clothing n) Funeral benefit o) Maximum advance p) Incentive q) Lunch r) Transport s) Medical / first aid t) Wagetkt u) Incidental costs

National Council for Construction Training Manual Competitive Pricing of Construction Works

Page | 10

However, if the project is of firm contract, additional allowances are added to take care of possible increase in labour rate by recognizing the size and likely duration of the contract. Refer to appendix 1 for calculation of All-in-rate of Labour

2.2.2 Cost of Materials Material in the building industry refers to varying components delivered to site which when articulated or appropriately combined, result to functional element of a building project. Material cost affect the estimate greatly and this depends on the source of supply and the competitiveness of quotation received by the estimating department. Several factors affect the cost contractors pay for materials. In addition to the actual cost of the material the estimator must also consider:

Transportation costs

Unloading and Stacking costs

Materials movement on site

Extra Materials to compensate for: o Wastage o Allowance for materials being measured net in B o Q o Loss in consolidation, shrinkage etc

Note: Where prices of materials are described by suppliers as ‘ex works’ this means the price at the factory and delivery costs will have to be added. The estimating department does send out enquiries to suppliers of materials with a view to obtaining a more realistic and workable information. The CIOB code of estimating practice outlined this information to include:

a) Title and location of the work b) Specification, class and quality of the material c) Quantity of material required d) Likely delivery programme and special delivery requirements e) Access to site and any restrictions f) Date by which the quotation is required g) Period for which the quotation is to remain open h) Whether a fluctuation or firm price required i) Discount required and j) Person in the contractor’s organization to be contacted when queries arise.

The code recommended a further check on the obtained information so as ascertain that the following criteria are satisfied:

i. The material comply with the specification ii. The material will be available in sufficient quantities to meet the requirements of the

construction programme iii. The supplier has imposed no special delivery conditions iv. The method and rate of delivery complies with the contractors requirement(s) v. The condition contained a counter offer, which is at variance with the terms and conditions

of the enquiry. vi. The quotation is valid for the required period

vii. Prices are given for small quantities where applicable

National Council for Construction Competitive Pricing of Construction Works Training Manual

Page | 11

viii. Discount conform to the requirements of the enquiry ix. Requirement concerning fixed or fluctuating prices are satisfied.

The next line of action for estimating department is the calculation of the unit rates for material. Prices should therefore include the basic price, less discounts retained by the contractor, allowance for waste, unloading, stacking, storing, distributing around the site and the return of crates or packings where appropriate.

2.2.3 Cost of Plant & Equipment Plant is employed on a building site in order to save money, labour or time, or a combination of all. For any given project, the estimate department obtains information on plant to be required from the method statement and the programme while the period of requirement is found from the tender programme. Plant may be divided into two main categories, the costs of which can be allocated to contracts in differing ways.

a) Non-Mechanical Plant Basic items of plant including – barrows, hosepipes, spades, trestles, scaffolding, small powered hand tools etc. With the exception of scaffolding and one or two other items it is virtually impossible to allocate the cost of non-mechanical plant items to a contract, let alone to a specific unit rate. Example a wheelbarrow may be used on several contracts in its lifetime. The cost may be included in overhead charges as a percentage, as a lump sum in the preliminaries bill or, more accurately, on longer contracts a list of non-mechanical plant items is prepared, costed and included in the contract sum.

b) Mechanical Plant Mechanical plant such as excavators, lorries, dumpers, mixers etc. require a more complex approach. Mechanical plant can be very expensive. Mechanical plant can further be categorised as Mechanical plant with operator or Mechanical plant without operator A factor which affects the costs of plant is the source of provision. According to the CIOB code of Estimating practice, a contracting firm has three alternatives to make a choice and these are:

Purchase plant for the contract;

Hiring existing company owned plant; and

Hiring plant from external sources The purchase of plant by a contracting firm for any given project is a function of many variables including the nature of the contract, the size of the project, the type of the client, the location and complexity of the project. Often times, contracting firms resort to hiring plant from external sources. This action has relatively proved to be cheaper. However, reasonable carefulness is usually required to ensure that quotations obtained are for plants, which will meet the contractor’s requirements including the job specification(s). Articulating these requirements the code of estimating practice posit that clarification should be that:

i. The plant complies with the specifications ii. It is available to meet the needs of the construction programme

iii. Delivery and collection charges can be identified iv. Where appropriate all operator costs are included and that operators will conform to the

intended working hours of the site; v. Any attendance or supplies to be provided by the contractor are clearly identified

vi. Maintenance responsibilities, charges and liabilities are identified

National Council for Construction Training Manual Competitive Pricing of Construction Works

Page | 12

vii. The quotation conforms to the terms and conditions of the enquiry and does not represent a counter offer; and

viii. Requirements concerning fixed or fluctuating prices are met. If the contracting firm chose hiring existing company owned plant for the proposed project, then action shifts to the calculation of the associated costs. Plant is normally charged to the contract on a rental basis, except in the case of plant specially made or purchased for a specific operation. The later plant is normally charged in full to contracts and allowance made for disposal on completion, often at scrap value. Example of calculation of unit rate for mechanical plant is included in Appendix 2

2.2.4 Preliminary and General Items Mobilization is a contract pay item used to cover a contractor’s preconstruction expenses and the costs of preparatory work and operations. Since there is no clear list defining this work effort, and since contractors have the ability to adjust their bids as needed to cover these expenses, there are no true rules as to what percentage should be used per contract. Therefore, when starting an estimate for a project, enter 10% as a beginning point for mobilization and adjust it up or down as below:

less than US$100,000 Use 8% to 12%

$100,000 - $250,000 Use 6 % to 10 %

$250,000 - $500,000 Use 6 % to 9%

$500,000 - $1,000,000 Use 5 % to 9 %

$1,000,000 - $2,000,000 Use 6 % to 9 %

$2,000,000 - $5,000,000 Use 7 % to 9 %

$5,000,000 - $10,000,000 Use 8 % to 10 %

$10,000,000 - $20,000,000 Use 7 % to 11 %

Over $20,000,000 Use 7 % to 10 %

To more accurately calculate the Mobilization percentage that should be used for each individual project, consideration should also be given to:

The location of the project; The complexity of the project; The need for specialized equipment; The type of work being performed; Rural vs. Urban Projects with multiple work sites; Excessive preparatory removal items; Large quantities of excavation; Spanning of constructions seasons when it would become necessary for the contractor to

shut down and clear the work site between these seasons.

National Council for Construction Competitive Pricing of Construction Works Training Manual

Page | 13

2.2.5 Estimating Lump Sum Items From an estimating standpoint, lump sum bid items are often more difficult to price. Lump sum items can reduce administrative costs in contract administration, as well as allowing a contractor a variety of work means and methods, and thus do make sense in some instances. They also transfer the risk of performance and quantities to the contractor. If the work to be performed can be quantified, then a payment method that includes a quantity should be used. However, lump sum bid items are often used when an item of work can only be defined in general terms, such as when the finished product can be defined but not all the components or details can be easily determined. This can make estimating lump sum items difficult for the estimator. The more information and breakdown of a lump sum item that an estimator has available, the greater the likelihood that an accurate lump sum estimate can be developed. An estimator should define a lump sum item in terms of its simplest, most basic components and should consider other factors that may not be easily estimated. By breaking out a lump sum item into smaller items of work which have historical data, and then applying reasonable estimated prices to those sub units, the estimator can accurately establish a price for the overall lump sum item. Using lump sum items typically transfers risk to a contractor, and the contractor may adjust his price upward to take on this risk. Contractors cannot necessarily rely on overruns to cover work that they did not foresee. Lump sum items are typically bid at higher costs than component costs due to the transfer of risk from the owner to the contractor. Therefore, the use of lump sum items should be used with great care.

In roadworks, as may be the case for a time-based lump sum bid item such as Project Temporary Traffic Control, the lump sum payment may provide the basis as an incentive to perform the work more quickly. In such a situation, hourly pay items offer no incentive, and may even cause the contractor to stay in the work zone as long as possible.

2.2.6 Subcontractors Subcontractors derive their definition from the mode of selection including the type of service they are required to render in a given project. Generally, subcontractors are defined as individuals or firms who enter into a legal contract with the main contractor to complete an agreed part of the contract. Subcontractors can be:

Domestic referring to the main contractor’s own subcontractors

Nominated which arises where the design team/client requires control in the selection of a specialist

In order to arrive at the likely cost of items to be undertaken by the domestic subcontractor, the estimating department abstract from the bills items applicable to each trade including the trade preamble. Thereafter, enquires are sent with a view to obtaining subcontractors’ bills of quantities from selected number of tenderers. The sent out enquiries usually contain conditions of the main contract and the date by which the tenders are to be submitted to enable the main contractor determine the rates to be inserted in the tendering bills. The main contractor adjust rates obtained from the subcontractors by adding to the most competitive subcontractors rates, a percentage to accommodate profit and attendance before inserting in the tendering bills of quantities. Usually nominated subcontractors undertake works included in the bills as provisional or prime cost sums. The main contractor is allowed to add an amount of money or percentage to cover any profits he may require on such work. He is also required to provide general attendance on nominated subcontractors and to allow the use of general facilities such as standing scaffolding, mess-room and sanitary accommodation, welfare facilities, storage for plant and material, provision of water and electricity and clearing away of rubbish. It is usual for such attendance to

National Council for Construction Training Manual Competitive Pricing of Construction Works

Page | 14

be described in the bills and the main contractor is allowed to add an amount of money or percentage to cover the cost involved.

a. Nominated Suppliers Nominated suppliers are involved when goods and materials expected to be used in a given project are covered by the inclusion of a provisional or prime cost sums in the bills. Under the arrangement, the main contractor is allowed to add an amount of money or a percentage to cover any profit he may require on such items. The cost of fixing goods and materials which are obtained from a nominated supplier is measured and the unit items are priced in accordance with the trade involved. The cost of unloading, storing, hoisting the goods/materials and returning packing cases etc, to the nominated supplier, carriage paid and obtaining credits therefore, is included with the item of fixing.

2.2.7 Provisional and Prime Cost (PC) Sums In a typical bill of quantities where the contract is with quantities and specification where contract is without quantities, some parts of the work remain unmeasured and/or specified in details. Lump sums are usually appropriately included to take care of this shortfall. A prime cost sum is a sum provided for work or services to be executed by nominated subcontractor, a statutory authority or a public undertaking or for materials or goods to be obtained from a nominated supplier. A provisional sum is a sum provided for either defined or undertaken work. It is defined when work is not completely designed at the time of tender documents are issued but for which certain specified information can be given. In either case of prime cost and provisional sums, elementary precaution should be taken of, checking to ensure that the sums of money included in the text are extended into the pricing column. Following each prime cost item there will provision for addition of profit and attendance. Profit is normally calculated on a percentage basis while attendance will be assessed on the cost of the services to be provided and entered as a lump sum.

2.2.8 Escalation The future cost of material, labour and plant can be difficult to predict. Prices for these commodities have risen across time, but they have also experienced increases and decreases within the same year. The art of budgeting for a construction program that spans more than 12 months is a challenge because of the price volatility in construction commodities. In addition, a boom in construction followed by a bust can change both contractor and supplier margins as markets move from being very tight to slack. For these reasons, and others not listed here, it is vital to account for inflation when preparing any estimates for any project.

Price volatility among inputs to construction leading to inflation, occur for several reasons and can originate from either consumers or suppliers. One accepted method for tracking cost escalation involves the use of indexes. By tracking all of these goods at once, the supply and demand movements that cause the price of single goods to fluctuate and can be observed. When there is no system to properly account for cost volatility, the possibility that price inflation will be accounted for multiple times, or not at all, in a project’s estimate becomes a significant concern. This is very probable in Zambia as there is a lack of construction specific indices. At the moment contractors rely on expert judgement or experience.

National Council for Construction Competitive Pricing of Construction Works Training Manual

Page | 15

2.2.9 Overheads Overheads may be defined as the cost of maintaining (running) the contractor’s organisation or those costs incurred in the operation of a business which are not directly related to individual items of production. There are two types of overheads:

a) Head Office Annual cost of staff salaries, expenses, rentals and rates, water, electricity, telephones, maintenance and depreciation of office equipment, postage, insurance, advertising, maintenance of buildings and equipment etc. The cost of these items is expressed as a percentage of a company’s turnover and included in the tender.

b) Project or Site Project site costs including non – productive or non-key staff such as site supervisory staff, site office costs, storage facilities temporary roads and services and other preliminary / site organisation costs. Items are priced as individual items and may be fixed or time related costs or a mix of fixed and time related costs. The costs of these items are included in the tender. The techniques and methods applicable in the calculation of overheads revolve on the policy of the contracting firm and the type of overhead involved. Usually with site overheads each contract will have a calculated allowance in the tender, but head office overheads are a percentage of budget turnovers and this is applied to all contracts. Most contractors use systems which record past and present overheads, the projection of overheads for the future, and rate at which overheads are being recovered. An important part of a contractor’s general overheads is the cost of financing construction works in advance of payment, which needs to be calculated and included in the tender. The appropriate addition for head office overheads varies with the extent of centrally provided services and the size of organization, but could be in the range of 4 to 8% of turnover.

2.2.10 Profit Profit is defined as the difference between the contract sum and that required to pay for overheads site costs, labour, plant and materials to complete the contract. The amount of profit that a contractor can make is determined by a number of factors largely outside the remit of an estimator. However, in larger companies the senior or managing estimator may be a member of the management team and in smaller companies / firms the estimator may be a director or the managing director. In both cases they may be party to, or may have to make commercial decisions regarding profit margins. Factors affecting profit levels are:

Market forces of supply and demand

Amount of competition

Who the competitor are

Size / Value of contract

Interest rates.

the size and nature of the contracting firm,

the organization of the contracting firm,

the client and even the disposition of the project consultants.

Risk involved in contract such as: o Contractual risks. These are risks stemming from the contract documents and the

necessary arrangements for work to be done by subcontractors and/or deliveries

National Council for Construction Training Manual Competitive Pricing of Construction Works

Page | 16

from suppliers of materials or components. Also included would be the firm price tender risk.

o Technical risks. These risks revolve around the form of construction (whether traditional or non-traditional) and the ease of otherwise of executing the work, previous experience of erecting buildings of similar construction and the problems of programming and plant utilization.

Basically, the greater the risk involved the higher the profit requirement and vice versa. In practice however, the following allowances provided by most contracting firms to accommodate the much cherished profit.

i. Builders work(10 – 15%) ii. Subcontractors and suppliers (contractor’s own) 5 – 10%

iii. Nominated subcontractors (2 ½ - 7 ½ %) iv. Nominated suppliers (5 – 10%)

2.3 COST IMPLICATIONS IN VARIATIONS AND EXTENSION OF TIME

2.3.1 Variations A variation is an alteration to the scope of works in a construction contract in the form of an addition, substitution or omission from the original scope of works.

Almost all construction projects vary from the original design, scope and definition. Whether small or large, construction projects will have inevitably depart from the original tender design, specifications and drawings prepared by the design team. This can be because of technological advancement, statutory changes or enforcement, change in conditions, geological anomalies, non-availability of specified materials, or simply because of the continued development of the design after the contract has been awarded.

Variations may include:

Alterations to the design. Alterations to quantities. Alterations to quality. Alterations to working conditions. Alterations to the sequence of work.

Variations may not (without the contractors consent):

Change the fundamental nature of the works. Omit work so that it can be carried out by another contractor. Be instructed after practical completion. Require the contractor to carry out work that was the subject of a prime cost sum.

In legal terms, a variation is an agreement supported by consideration to alter some terms of the contract. No power to order variation is implied. Hence there should be express terms in contracts which give the power instruct variations. In the absence of express terms in the contract the contractor may reject instructions for variations without giving rise to any legal consequences.

Standard forms of contract generally make express provisions for variations. Such provisions enable the continued, smooth administration of the works without the need for another contract.

National Council for Construction Competitive Pricing of Construction Works Training Manual

Page | 17

Variation instructions must be clear as to what is and is not included, and may propose the method of valuation.

Valuation of variations

Variations may give rise to additions or deductions from the contract sum. The valuation of variations may include not just the work which the variation instruction describes, but other expenses that may result from the variation, such as the impact on other aspects of the works. Variations may also (but not necessarily) require adjustment of the completion date.

Variations may be valued by:

a) Similar rates

Valuations of variations are often based on the rates and prices provided by the contractor in their tender, provided the work is of a similar nature and carried out in similar conditions. This is true, even if it becomes apparent that the rates provided by the contractor were higher or lower than otherwise available commercial rates. They do not become reasonable or unreasonable by the execution of variations.

b) New rates

If similar types of works to those instructed by a variation cannot be found in the drawings, specification or bills of quantities, then fair valuation of the contractor's direct costs, overheads and profit is necessary. Rates will be built up from first principles.

Limits on variations

Forms of contracts put limitations on variations that can be instructed. If the value of the contract increases or decreases by more than 15% of the net contract sum (excluding provisional sums and day works) then the contract administrator can add or deduct from the contract sum a determined value upon consultation with the contractor, having due regard to their site expenses and other general overheads. Note that this 15% increase or decrease is not for a single item of work, but the total contract sum at completion.

If the rate in the bill multiplied by the final total quantity of work done is more than 1% of the priced total of the bill at the contract date, than it will constitute a variation.

Refer to sample in appendix 3.4

2.3.2 Extension of time Many construction contracts allow the construction period to be extended where there are delays that are not the contractor's fault. This is described as an extension of time (EOT).

When it becomes reasonably apparent that there is a delay, or that there is likely to be a delay that could merit an extension of time, the contractor gives written notice to the client identifying the relevant event that has caused the delay. If the client accepts that the delay was caused by a relevant event, then they may grant an extension of time and the completion date is adjusted.

Relevant events may include:

Variations. Exceptionally adverse weather. Civil commotion or terrorism.

National Council for Construction Training Manual Competitive Pricing of Construction Works

Page | 18

Failure to provide information. Delay on the part of a nominated sub-contractor. Delay in giving the contractor possession of the site. Force majeure (such as an epidemic or an 'act of God'). The supply of materials and goods by the client. Changes in statutory requirements. Delays in receiving permissions that the contractor has taken reasonable steps to avoid.

The contractor is required to prevent or mitigate the delay and any resulting loss, even where the fault is not their own.

Assessing claims for an extension of time can be complicated and controversial. There may be multiple or concurrent delays, some of which are the contractor's fault and some not. There are many occasions where contractors contribute to delay themselves by their performance during design periods, when producing drawings, mock ups and samples or in inter-facing with sub-contractors. Crucial in assessing applications for extension of time is the quality of the information provided and records available.

All claims should be judged against the progress of the works and not the programme and must demonstrate the link between the breach (cause) and the delay. Supplemental and wrap-up agreements previously agreed by both parties can weaken the contractor’s final entitlement.

The client representative may review extensions of time after practical completion and further adjust the completion date.

Mechanisms allowing extensions of time are not simply for the contractor's benefit. If there was no such mechanism and a delay occurred which was not the contractor’s fault, then the contractor would no longer be required to complete the works by the completion date and would only then have to complete the works in a 'reasonable' time. The client would lose any right to liquidated damages.

Claims for EOT can be with or without costs. The EOT application should considers:

The event - the circumstance which has given rise to extension of time request. Liability for the event Contractual entitlement referring to provisions entitling the contractor to a claim Contractual compliance such as notices and detailed particulars the contractor is

obligated to submit. Statement of claim containing a succinct statement of what the contractor is claiming. Substantiation showing documentary evidence in support of the assertions made within

the claim submission. Recommendation as to the way forward

Refer to sample in appendix 3.5

National Council for Construction Competitive Pricing of Construction Works Training Manual

Page | 19

3 APPENDICES

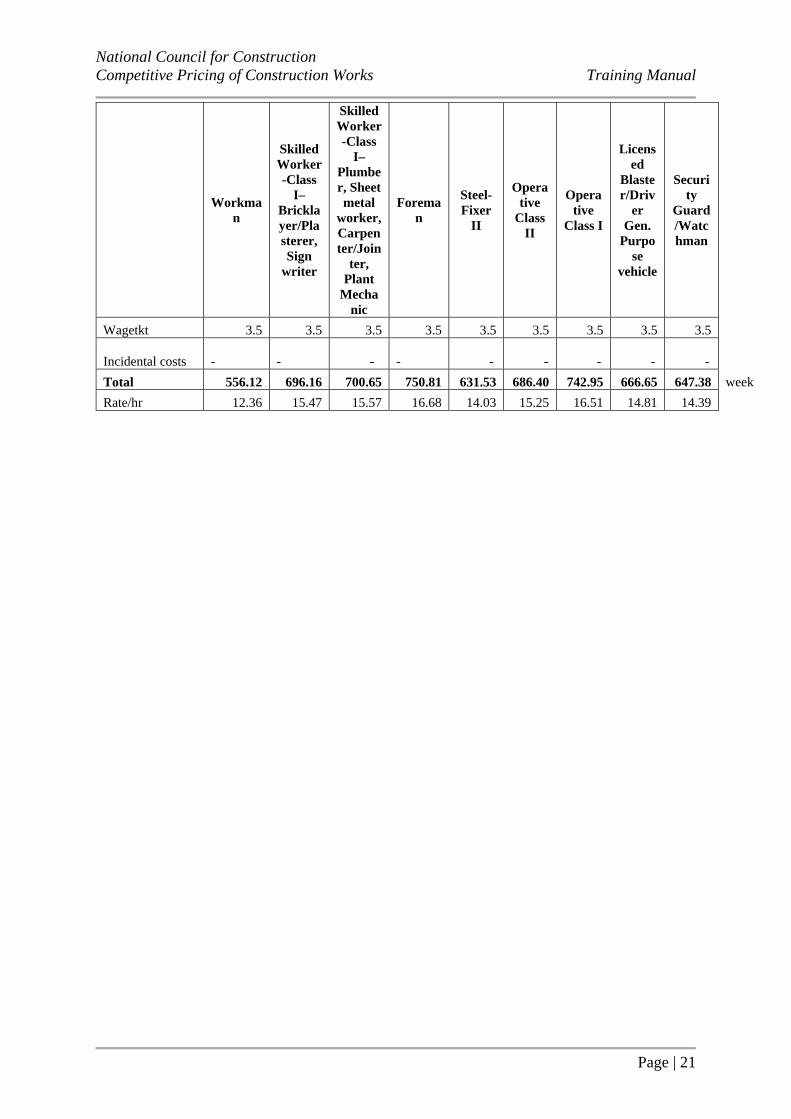

3.1 ALL - IN CONSTRUCTION WORKER RATES

Based upon Association of Building & Civil Engineering contractors (ABCEC) and National Union of Building, Engineering & General Workers (NUBEGW)

Joint Industrial Council Collective Agreement (2014 - 2015)

Description Unit Qty Average working weeks in Zambia

Working hours per day hrs 9 No of weeks in a year 52

Working hours per week hrs 45 less annual leave (includes industry close down) 4.8

Working hours per month hrs 195 less public holidays 2.6

Public holidays per year day 13 44.6 (UK has 46.2 working weeks)

Annual leave day 24

Sick leave day 30 2007 working hours

Inclement weather hrs 40

Service benefit hrs/ mth 30

Napsa

%/(basic hrs + annual leave pay + occasional leave pay) 5

WCF

%/(basic hrs + OT + leave pay + service pay + tool allowance) 1.97

Medical %/medical scheme 50

HIV training/first aid %/probation period 0.5

Work suit (overalls) K/no. 120

Gumboots K/pair 75

Head gear K/no. 35

Raincoat K/no. 120

Uniform K/no. 150

Reflector vest K/no. 35

Safety shoes K/pair 200

Tool allowance (car/pl) %/basic rate 7.5

Housing allowance %/basic rate 30

Funeral Benefit K/event 2050

Max Advance K/event 800

Incentive K/day 0

Overtime rate %/basic rate 1.5

Lunch allowance K/day 11

transport K/day 11

UTH medical scheme k/mth 20

Risk 0

National Council for Construction Training Manual Competitive Pricing of Construction Works

Page | 20

Workman

Skilled Worker-Class

I–Bricklayer/Plasterer, Sign

writer

Skilled Worker-Class

I–Plumber, Sheet metal

worker, Carpenter/Join

ter, Plant

Mechanic

Foreman

Steel-Fixer

II

Operative

Class II

Operative

Class I

Licensed

Blaster/Driv

er Gen.

Purpose

vehicle

Security

Guard/Watchman

Rate 3.97 5.53 5.61 6.10 4.81 5.39 6.02 5.17 55.86

Basic 45 178.65 248.85 252.45 274.50 216.45 242.55 270.9 232.65 223.44 (4 Shifts) Holiday Pay (annual leave) 19.23 26.78 27.17 29.54 23.30 26.10 29.16 25.04 24.05

Sick leave 17.36 24.18 24.53 26.67 21.03 23.57 26.32 22.60 21.71

Occasional leave 12.82 17.85 18.11 19.70 15.53 17.40 19.44 16.69 16.03

Public holidays 10.41 14.51 14.72 16.00 12.62 14.14 15.79 13.56 13.03 Inclement weather 3.56 4.96 5.03 5.47 4.31 4.83 5.40 4.64 4.45

Overtime -

- -

- - - - - -

Housing allowance 53.60 74.66 75.74 82.35 64.94 72.77 81.27 69.80 67.03

Tool allowance 13.40 18.66 18.93 20.59 16.23 18.19 20.32 17.45 16.76

Service benefits 32.04 44.64 45.28 49.24 38.83 43.51 48.59 41.73 40.08

NAPSA 10.53 14.67 14.89 16.19 12.76 14.30 15.97 13.72 13.18

WCF 4.79 6.68 6.77 7.37 5.81 6.51 7.27 6.24 6.00 Protective clothing

Work suit (overalls) 2.69 2.69 2.69

- 2.69 2.69 2.69 2.69 -

Gumboots 1.68 1.68 1.68

- 1.68 - - - -

Head gear 0.78 0.78 0.78 0.78 0.78 0.78 0.78 0.78 -

Raincoat 2.69 2.69 - 2.69 2.69 2.69 2.69 2.69 2.69

Uniform -

- - 3.36 - - - - 3.36

Reflector vest 0.78 0.78 0.78 0.78 0.78 0.78 0.78 0.78 -

Shoes -

- - 4.48 - 4.48 4.48 4.48 4.48

Funeral benefit 45.96 45.96 45.96 45.96 45.96 45.96 45.96 45.96 45.96 Maximum advance 17.94 17.94 17.94 17.94 17.94 17.94 17.94 17.94 17.94

Incentive - - -

- - - - - -

Lunch 55.00 55.00 55.00 55.00 55.00 55.00 55.00 55.00 55.00

Transport 66.00 66.00 66.00 66.00 66.00 66.00 66.00 66.00 66.00

Medical / first aid 2.69 2.69 2.69 2.69 2.69 2.69 2.69 2.69 2.69

National Council for Construction Competitive Pricing of Construction Works Training Manual

Page | 21

Workman

Skilled Worker-Class

I–Bricklayer/Plasterer, Sign

writer

Skilled Worker-Class

I–Plumber, Sheet metal

worker, Carpenter/Join

ter, Plant

Mechanic

Foreman

Steel-Fixer

II

Operative

Class II

Operative

Class I

Licensed

Blaster/Driv

er Gen.

Purpose

vehicle

Security

Guard/Watchman

Wagetkt 3.5 3.5 3.5 3.5 3.5 3.5 3.5 3.5 3.5

Incidental costs -

- -

- - - - - -

Total 556.12 696.16 700.65 750.81 631.53 686.40 742.95 666.65 647.38 week

Rate/hr 12.36 15.47 15.57 16.68 14.03 15.25 16.51 14.81 14.39

National Council for Construction Training Manual Competitive Pricing of Construction Works

Page | 22

3.2 ALL IN PLANT & EQUIPMENT RATE

Average working weeks in a year 44.6

Average working hours in a year 2007

Finance charges (lending rate + 3%) 23

Insurance rate 7.5

Road tax % 1

Cost of diesel per litre 6.59

Less tire / consummable replacement costs

*Purchase price is price landed in Zambia

Depreciation Interest Insurance

licence tax Sub total

Fuel / oil Litres/hr

Fuel / oil consumption

Maintenance

Sub total

Total Owning & Operating costs / hr

Concrete Mixer (a) 0.4/0.28 m3 85 1,705.95 7 11,941.65 160,000.00 2 3,200.00 156,800.00 13.13 12.08 3.94 0.53 29.67 1.2 7.91 1.88 9.78 39.46Concrete Mixer (b) 1 m3 85 1,705.95 7 11,941.65 180,000.00 2 3,600.00 176,400.00 14.77 13.59 4.43 0.59 33.38 1.2 7.91 2.11 10.02 43.40Dozer D - 80 - A 12 78 1,565.46 10 15,654.60 1,289,484.00 6 77,369.04 1,212,114.96 77.43 97.95 31.94 4.26 211.57 38 250.42 49.42 299.84 511.42Dozer D - 50 - A 15 78 1,565.46 10 15,654.60 1,230,684.00 3 36,920.52 1,193,763.48 76.26 96.46 31.46 4.19 208.37 21 138.39 23.58 161.97 370.35Front End loader 1 m3 bucket capacity 80 1,605.60 9 14,450.40 128,576.00 4 5,143.04 123,432.96 8.54 9.82 3.20 0.43 22.00 18 118.62 3.20 121.82 143.82Generator( b) 33/63 KVA 85 1,705.95 5 8,529.75 103,978.00 3 3,119.34 100,858.66 11.82 8.16 2.66 0.35 23.00 4.9 32.29 1.83 34.12 57.12Hydraulic Excavator of 1 m3 bucket 80 1,605.60 9 14,450.40 403,270.00 4 16,130.80 387,139.20 26.79 30.81 10.05 1.34 68.99 18 118.62 10.05 128.67 197.65Motor Grader complete with scarifier, CAT 14 or equivalent 78 1,565.46 10 15,654.60 862,250.00 5 43,112.50 819,137.50 52.33 66.19 21.58 2.88 142.98 19 125.21 27.54 152.75

295.73

Pneumatic Road Roller 75 1,505.25 6 9,031.50 513,324.00 7.5 38,499.30 474,824.70 52.57 42.32 13.80 1.84 110.54 7.6 50.08 25.58 75.66 186.20Pot Hole Repair Machine 78 1,565.46 7 10,958.22 454,524.00 5 22,726.20 431,797.80 39.40 36.25 11.82 1.58 89.05 5 32.95 14.52 47.47 136.52Road marking machine 85 1,705.95 7 11,941.65 6,958.00 2.8 194.82 6,763.18 0.57 0.52 0.17 0.02 1.28 1.8 11.86 0.11 11.98 13.26Smooth Wheeled Roller 8 tonne 85 1,705.95 6 10,235.70 9,555.00 7.5 716.63 8,838.38 0.86 0.70 0.23 0.03 1.82 17 112.03 0.42 112.45 114.27Tipper - 5 m3 90 1,806.30 6 10,837.80 226,870.00 3 6,806.10 220,063.90 20.31 16.35 5.33 0.71 42.69 17 112.03 3.77 115.80 158.49Tractor 86 1,726.02 7 12,082.14 79,000.00 2 1,580.00 77,420.00 6.41 5.90 1.92 0.26 14.48 9 59.31 0.92 60.23 74.71Water Tanker 75 1,505.25 7 10,536.75 256,270.00 2 5,125.40 251,144.60 23.84 21.93 7.15 0.95 53.87 9 59.31 3.41 62.72 116.58Plate compactor 85 1,705.95 9 15,353.55 9,310.00 3 279.30 9,030.70 0.59 0.68 0.22 0.03 1.51 9 59.31 0.16 59.47 60.99

Less tire / consummable replacement

costs Nett value

Owning Costs 'ZMW/hr Operating costs 'ZMW/hr

Equipment Basic RatesCost of Owning and Operating Construction Equipment: Caterpillar Method

S/No. DescriptionUtilization Factor %

Hours per annum

Plant period (years)

Life (Hours)

*Purchase price 'ZMW

Percent for consummable replacement

costs

EquipBuildUp 1

National Council for Construction Competitive Pricing of Construction Works Training Manual

Page | 23

3.3 BUILD UP RATES FROM FIRST PRINCIPLES

BUILDING RATES FROM FIRST PRINCIPLESK/hr K/hr

General workman 5.16 Tipper 5m3 18.00 Skilled workman 5.75Foreman 6.10Equipment operator 6.00

1 Excavate

Hand dig 2.5 hrs /m3 @ 5.16 12.9OHP 20%

Can dig 2.83m3/day 15.48 /m3

EXCAVATION TRENCHA Machine digging (Excavator)

EX: Barloworld US $30.00 Per HourKwacha Equivalent 195.00 Per HourAdd Operator cost per hour 6.00 per Hour

201.00 per hourOut put 9.00 m3/hourCost Per m3 22.33 per m3

Add handling at 5% 1.12

23.45 /m3B. Labour Based

1 labourer can dig 1m3 of trench in 2.5 hoursAll in-rate per hour for labourer 5.16 Per hourCost per m3 = 12.90 Add handling at 5% 0.65

13.55

Combined rate Excavator 50% 11.73 Man 50% 6.77

18.50

Method: Machine only Man Only Combined23.45 13.55 18.50

Add waste at 5% 1.17 0.68 0.92

24.62 14.22 19.42 Add OH

At 10% 27.08 15.64 21.36 12.5% 27.70 16.00 21.85

15% 28.32 16.36 22.34 17.5% 28.93 16.71 22.82

20% 29.55 17.07 23.31 Say 28 16.00 22

2 Return, Fill & Ram (Backfilling)5m3/day

= 8 x 5.16 8.26 5 20%

9.91 /m3

3 Cart AwayHand load = 1m3/hr = 5.165m3 tipper return trip = 1hr = 18 3.6

5 8.7620%

10.51 /m3

4 Ant repellantcan spray 10m2/hr 0.52 1L (Aldanol 48) with 95L water (1:95) @ 5L/m21L bottle of Aldanol 48 covers 95 = 19m2

51L bottle of Aldanol =K40.80 40.8 2.15

19 2.66 10% waste 0.27

2.93 20%

3.52 /m2

5 Form sinking in laterite bed 400x100mm3 m /hr @ 5.16 1.72

OHP 20%2.06 /m3

6 Concrete

Cement 65 x 20 1,300.00 TTransport 5m3 (7.5T) truck @K18/hr 18x8 19.20

I load / day 7.5 1,319.20 (Offloading??)1.442 tons = m3 = 1,902.29 /m3

River Sand: K 40/m3 delivered to site

Stone 130.00 TCollect 0.35/T/km x 22km 7.70

Transport (rate x Dist x ton) 137.701.5 T/m3

206.55 /m3

1:3:6 1:2:4Cement 1,902.29 /m3 0.16 304.37 0.23 434.81 Sand 40 /m3 0.48 19.20 0.46 18.29 Stone 206.55 /m3 0.96 198.29 0.91 188.85

521.85 641.94 Mix and place1 mix. Ope 6.00 6.001 Dumper 6.00 6.002 skilled 5.75 11.506 labourer 5.16 30.96

54.46 /hr @ 8hrs/day 54.46 54.46Crew can mix & place 8m3 per day 576.31 696.40

Waste @ 10% 57.63 69.64

633.95 766.04 OHP @ 20% 126.79 153.21

760.73 m3 919.25 (100mm slab) x 0.10

91.92 Add 10% labour (curing) 9.19

101.12

National Council for Construction Training Manual Competitive Pricing of Construction Works

Page | 24

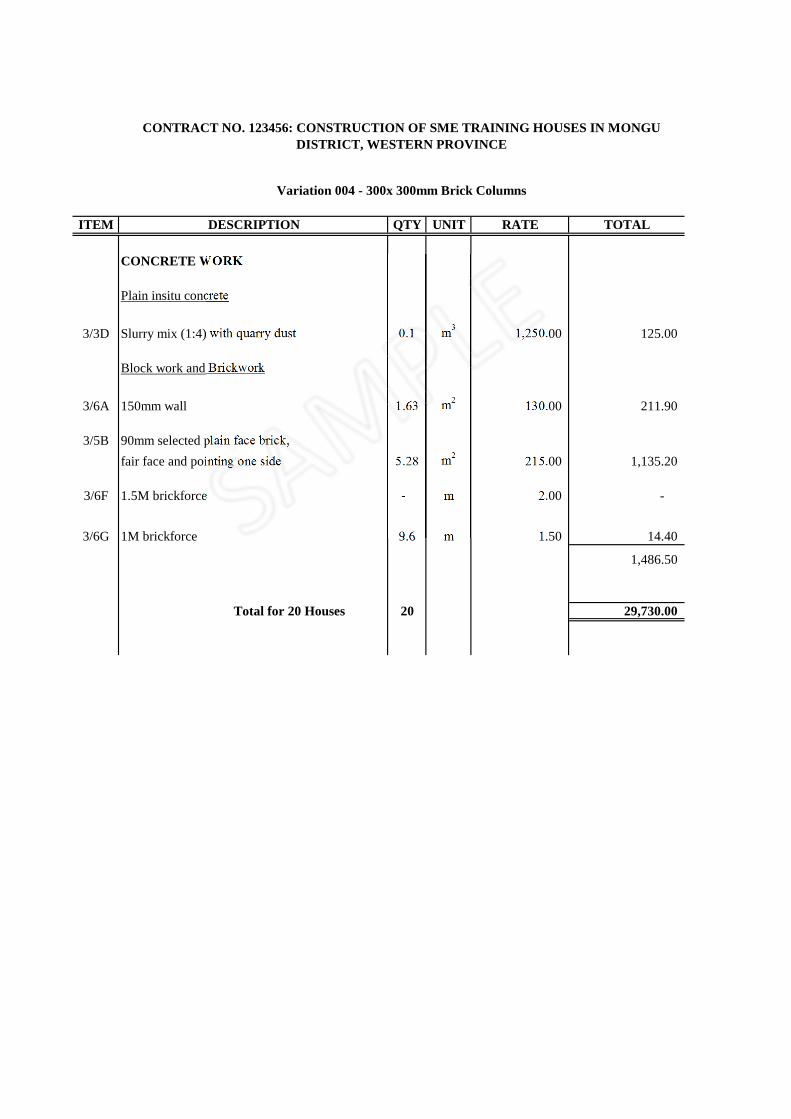

3.4 VARIATION SUBMISSION

25 March 2015 Director of Building Buildings Department Lusaka, Zambia Attention: Director of Buildings

Dear Sir, CONTRACT NO. 123456 CONSTRUCTION OF SME TRAINING HOUSES – Variation No. 004

Please find enclosed Variation no. 4 as per drawing. The drawing indicates two (2) brick columns to the verandah of each house. But there is no description for columns in the Bill of Quantities.

Yours faithfully, Contractor XYZ

VARIATION ORDER NO. 004

CONTRACT No: 123456 CONTRACT NAME: Construction of SME training houses in Mongu District,

Western Province CONTRACTOR: XYZ Contractors P.O. Box 1111111 Lusaka EMPLOYER: Ministry of Transport, Works, Supply and Communication P.O. Box 50800 Lusaka PROJECT MANAGER: Director of Buildings P.O. Box 50800 Lusaka The following Variation Order is instructed in accordance with clause 37 of the Conditions of Contract. Description of Variation Design of 300 x 300mm brick columns to the house as indicated on the drawing. This item is omitted from the Bill of Quantities As per the attached schedule. The estimated cost of this Variation Order is: VARIATION (as per attached summary sheet) ZMK 29,730.00

The recommended extension of time to be granted: 0 WEEKS.

Source of Contingencies Funding from Client BOQ items re- Funding arrangement

X Prepared by: ________________________ Verified by: ___________________________ Date: ________________________ Date: ___________________________ XYZ Contractors Consultant

Accepted by: ________________________ Approved by: ___________________________ Date: ________________________ Date: ___________________________ Director of Buildings Ministry of Transport, Works, Supply and Communication

ITEM DESCRIPTION QTY UNIT RATE TOTAL

CONCRETE WORK

Plain insitu concrete

3/3D Slurry mix (1:4) with quarry dust 0.1 m3 1,250.00 125.00

Block work and Brickwork

3/6A 150mm wall 1.63 m2 130.00 211.90

3/5B 90mm selected plain face brick,

fair face and pointing one side 5.28 m2 215.00 1,135.20

3/6F 1.5M brickforce - m 2.00 -

3/6G 1M brickforce 9.6 m 1.50 14.40

1,486.50

Total for 20 Houses 20 29,730.00

CONTRACT NO. 123456: CONSTRUCTION OF SME TRAINING HOUSES IN MONGU DISTRICT, WESTERN PROVINCE

Variation 004 - 300x 300mm Brick Columns

National Council for Construction Competitive Pricing of Construction Works Training Manual

Page | 25

3.5 EXTENSION OF TIME APPLICATION

CONTRACT NO. 123456: CONSTRUCTION OF SME TRAINING HOUSES IN MONGU DISTRICT, WESTERN PROVINCE EXTENSION OF TIME APPLICATION No. 1

Contract No. 123456: Contract for the Proposed Construction of SME training houses in Mongu district, Western Province

XYZ Contractors Extension of Time Application

ii

TABLE OF CONTENTS List of tables .................................................................................................................................................... ii 1. Introduction ............................................................................................................................................... 1

1.1. Background ....................................................................................................................................... 1 2. The Event .................................................................................................................................................. 2 3. Liability for the event ............................................................................................................................... 2

3.1. Delayed release of the advance payment........................................................................................... 2 3.2. Delays in certificate payments .......................................................................................................... 2

4. Contractual compliance ............................................................................................................................ 2 5. Statement of claim and Substantiation ..................................................................................................... 2

5.1. Delayed Release of the Advance Payment ........................................................................................ 2 5.2. Delays in Certification of Payments .................................................................................................. 3

6. Recommendation ...................................................................................................................................... 3 7. Appendices: .............................................................................................................................................. 3

LIST OF TABLES

Table 1: Contract details .................................................................................................................................. 1 Table 2: Notice of Claim within Reasonable Time .......................................................................................... 2

Contract No. 123456: Contract for the Proposed Construction of SME training houses in Mongu district, Western Province

XYZ Contractors Extension of Time Application

1

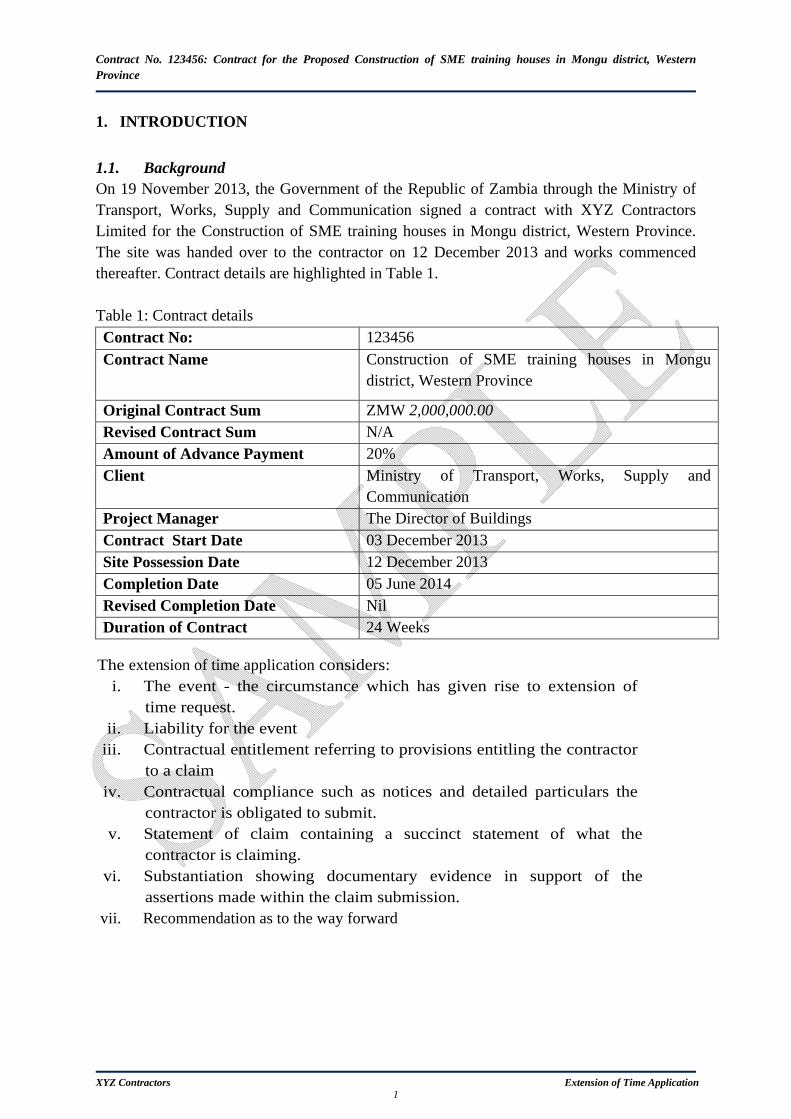

1. INTRODUCTION

1.1. Background On 19 November 2013, the Government of the Republic of Zambia through the Ministry of Transport, Works, Supply and Communication signed a contract with XYZ Contractors Limited for the Construction of SME training houses in Mongu district, Western Province. The site was handed over to the contractor on 12 December 2013 and works commenced thereafter. Contract details are highlighted in Table 1. Table 1: Contract details Contract No: 123456

Contract Name Construction of SME training houses in Mongu district, Western Province

Original Contract Sum ZMW 2,000,000.00 Revised Contract Sum N/A Amount of Advance Payment 20% Client Ministry of Transport, Works, Supply and

Communication Project Manager The Director of Buildings Contract Start Date 03 December 2013 Site Possession Date 12 December 2013 Completion Date 05 June 2014 Revised Completion Date Nil Duration of Contract 24 Weeks

The extension of time application considers: i. The event - the circumstance which has given rise to extension of

time request. ii. Liability for the event

iii. Contractual entitlement referring to provisions entitling the contractor to a claim

iv. Contractual compliance such as notices and detailed particulars the contractor is obligated to submit.

v. Statement of claim containing a succinct statement of what the contractor is claiming.

vi. Substantiation showing documentary evidence in support of the assertions made within the claim submission.

vii. Recommendation as to the way forward

XYZ Contractors Extension of Time Application

2

2. THE EVENT

The contractor is claiming that two major events gave rise to the current circumstances. These are:

delayed release of the advance payment; and

delays in certification of payments.

3. LIABILITY FOR THE EVENT

3.1. Delayed release of the advance payment 20% Advance payment was a condition of the contract. Therefore, delay in the release of advance payment is tantamount to a breach. Consequently, any delay in the payment of advance payment entitles the contractor to a compensation event under clause 41.1(i). 3.2. Delays in certificate payments According to clause 56 of the GCC, delay in certificate payment is a fundamental breach of contract.

4. CONTRACTUAL COMPLIANCE

For a compensation event claim the contractor is obligated to submit notice(s) and detailed particulars within a specified time frame. Clause 30.1 states that the contractor shall warn the project Manager at the earliest opportunity of specific likely future events that may likely increase the contract price, or delay the execution of the Works. From Table 2 all events qualify in contract compliance regarding reasonableness of notice. Table 2: Notice of Claim within Reasonable Time S/No. Event Period Reasonablenessi. Delayed release of the advance payment April 2014 Yes ii. Delays in certificate payments On going Yes

5. STATEMENT OF CLAIM AND SUBSTANTIATION

Documents provided as evidence in support of the assertions made within the claim submission are attached in Appendix 1. 5.1. Delayed Release of the Advance Payment In accordance with Clause 41.1(i) delayed payment of Advance is a compensation event. The Advance payment certificate was submitted on 13 November 2013 and part payment made on 16 July 2014. The balance of the advance amounting to K390,163.01 has not been paid to date. This notwithstanding, plant was delivered to site and the performance guarantee issued. The performance guarantee is necessary for implementation of any contract.

XYZ Contractors Extension of Time Application

3

5.2. Delays in Certification of Payments IPC No. 1 dated 13 April 2014 in the sum of K639,953.03 has not been paid to date. This has adversely affected cash flow forecasts.

6. RECOMMENDATION

Due to the affected cash flow, the contractor has continued to have presence on site though works have been slowed down. The contractor is claiming an extension of time with costs of 52 weeks with the revised completion date as 05 June 2015. OR The Contractor is therefore claiming an extension of time with costs of 20 weeks from date of payment of the full advance claimed. The client is urged to settle the balance advance.

7. APPENDICES:

Contractor’s Letter of early warning