module 1 cost slides

TRANSCRIPT

8/8/2019 Module 1 Cost Slides

http://slidepdf.com/reader/full/module-1-cost-slides 1/15

1

Module OneBasic Concepts & Terms of Costing

8/8/2019 Module 1 Cost Slides

http://slidepdf.com/reader/full/module-1-cost-slides 2/15

2

(A) Meaning of costing

Collection, analysis, interpretation &

presentation of relevant cost data for

managerial decision making & control

Set of Procedures which translates

raw data into useful information

for managerial decision making &

knowing costs & Profitability of

products/services

8/8/2019 Module 1 Cost Slides

http://slidepdf.com/reader/full/module-1-cost-slides 3/15

3

(B) Significance of costing

Profitability analysis

Analysis of cost behaviour

Actual Vs Expected results

Pricing policies/Pricing Strategies

Effect of in output on profitability

Continue or shut down of activities Actions for optimum use of resources

Management Performance

Effect of Productivity rise, Plant modernization &

new management techniques On Costs & Profits

A.B.C. for unprofitable & non value added activities

Effect of Strategies on cost of products/services

8/8/2019 Module 1 Cost Slides

http://slidepdf.com/reader/full/module-1-cost-slides 4/15

4

(C) Cost Management

Approach of managers for planning & control to

increase value to customer

Broad focused Planning & control of costs linked to profit planning

Integral part of strategic decision making

Features

-Calculate cost of products/services/cost objects

- M.I.S. for planning, control & performance evaluation

- Information analysis for decision making

8/8/2019 Module 1 Cost Slides

http://slidepdf.com/reader/full/module-1-cost-slides 5/15

5

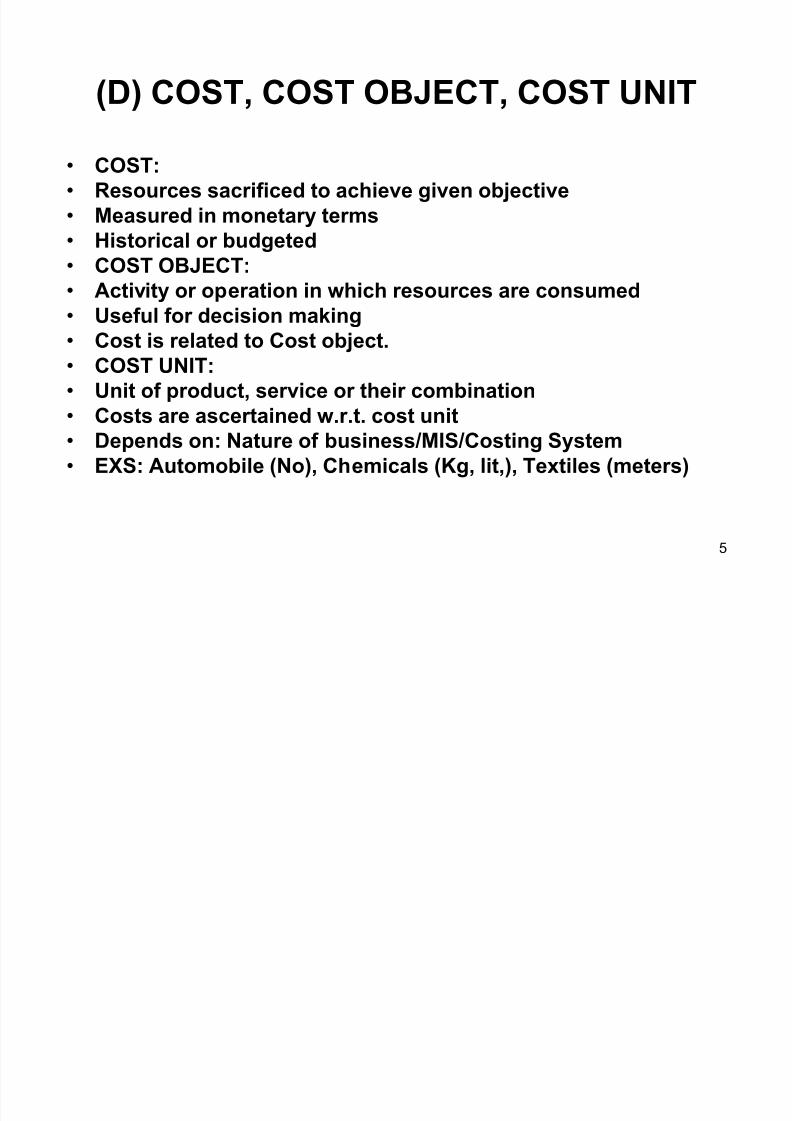

(D) COST, COST OBJECT, COST UNIT

COST:

Resources sacrificed to achieve given objective

Measured in monetary terms

Historical or budgeted

COST OBJECT: Activity or operation in which resources are consumed

Useful for decision making

Cost is related to Cost object.

COST UNIT:

Unit of product, service or their combination

Costs are ascertained w.r.t. cost unit Depends on: Nature of business/MIS/Costing System

EXS: Automobile (No), Chemicals (Kg, lit,), Textiles (meters)

8/8/2019 Module 1 Cost Slides

http://slidepdf.com/reader/full/module-1-cost-slides 6/15

6

(E) DECISION CENTERS

(a) Cost Center

Only cost incurred

Cost collection centre

Departments/Processes/activities/equipments/persons Decisions: Cost- Control / reduction / management

Efficiency of manager by cost saving

Useful for better managerial control

Types:I

mpersonal/P

ersonal/P

roduction/Service Accountability: increase in costs

8/8/2019 Module 1 Cost Slides

http://slidepdf.com/reader/full/module-1-cost-slides 7/15

7

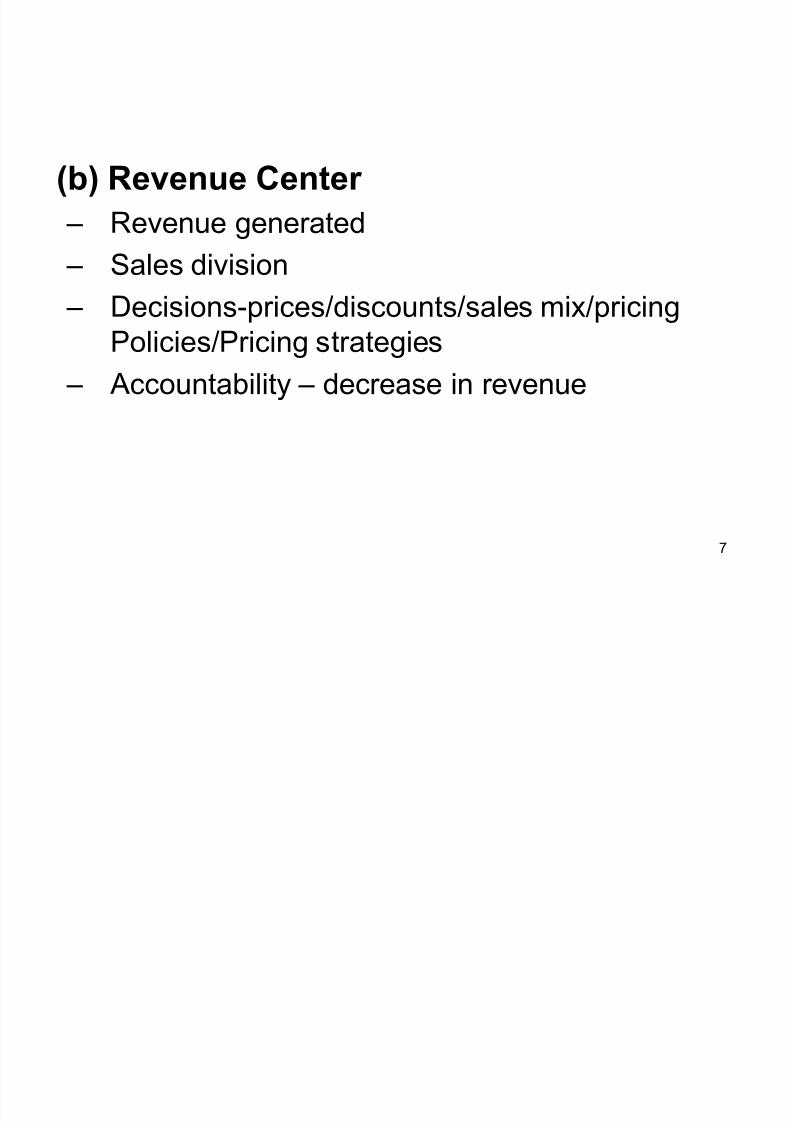

(b) Revenue Center

± Revenue generated

±Sales division

± Decisions-prices/discounts/sales mix/pricing

Policies/Pricing strategies

± Accountability ± decrease in revenue

8/8/2019 Module 1 Cost Slides

http://slidepdf.com/reader/full/module-1-cost-slides 8/15

8

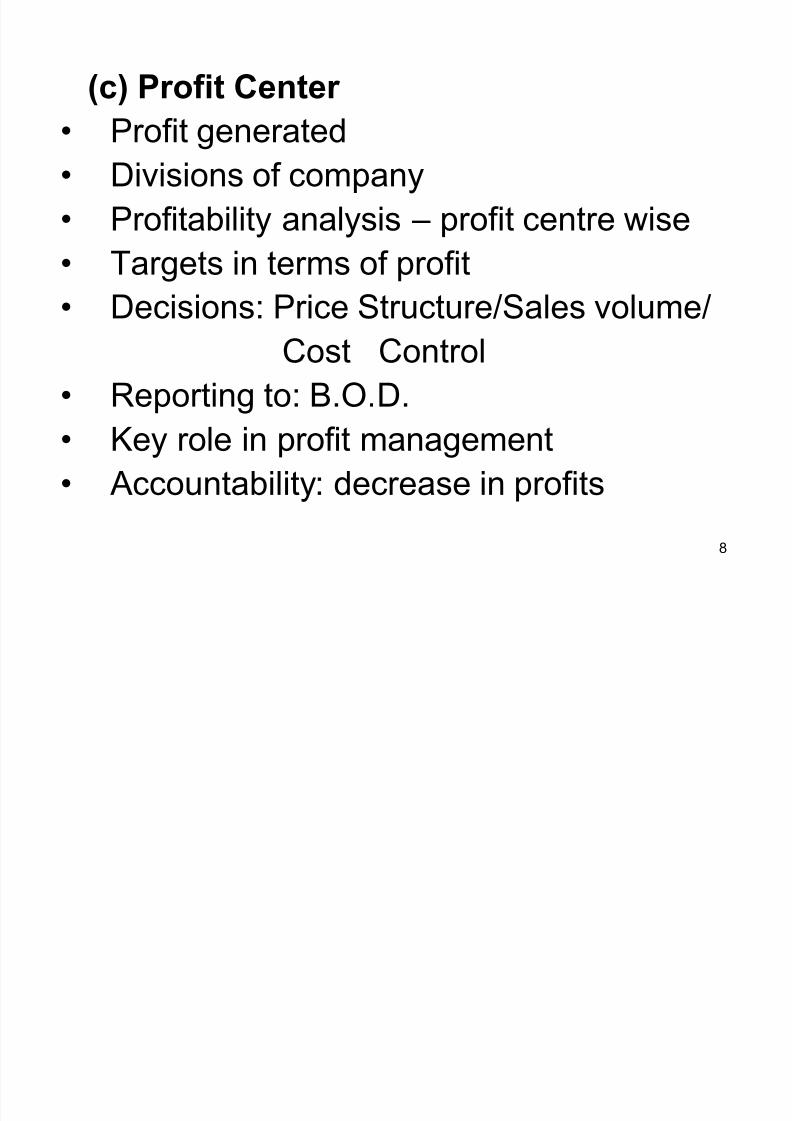

(c) Profit Center

Profit generated Divisions of company

Profitability analysis ± profit centre wise

Targets in terms of profit

Decisions: Price Structure/Sales volume/

Cost Control

Reporting to: B.O.D.

Key role in profit management

Accountability: decrease in profits

8/8/2019 Module 1 Cost Slides

http://slidepdf.com/reader/full/module-1-cost-slides 9/15

9

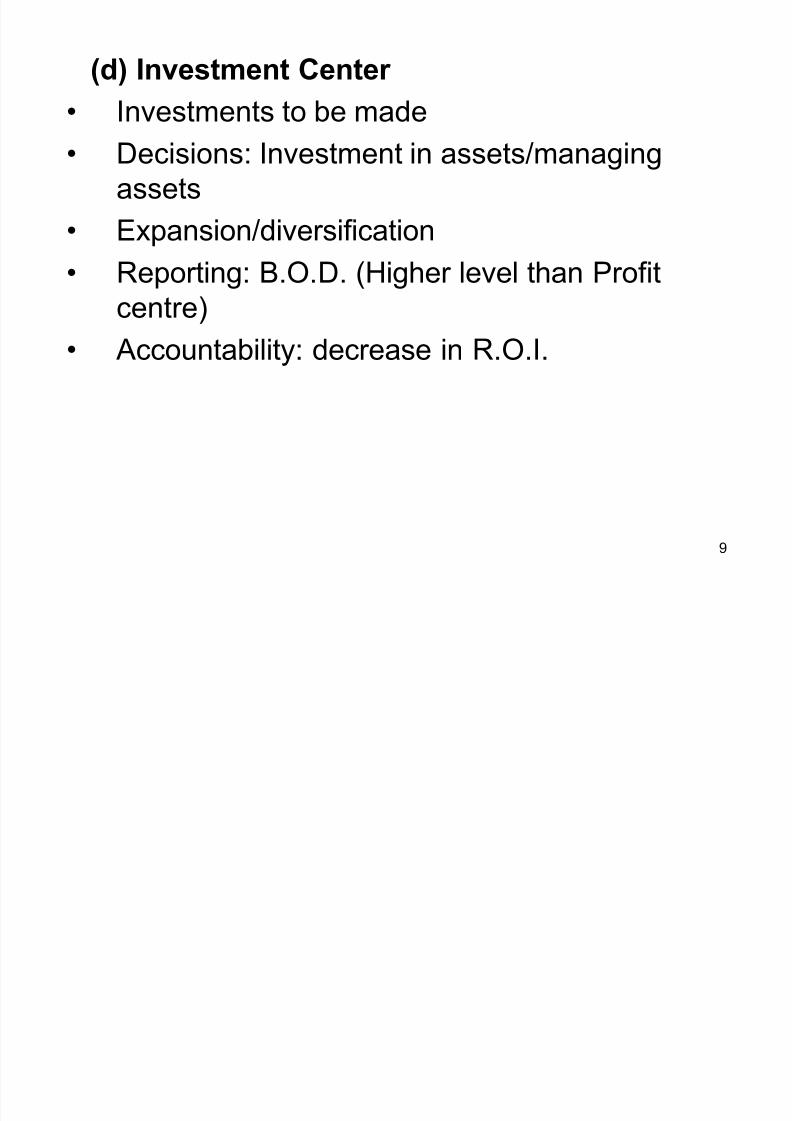

(d) Investment Center

Investments to be made

Decisions: Investment in assets/managing

assets

Expansion/diversification

Reporting: B.O.D. (Higher level than Profitcentre)

Accountability: decrease in R.O.I.

8/8/2019 Module 1 Cost Slides

http://slidepdf.com/reader/full/module-1-cost-slides 10/15

10

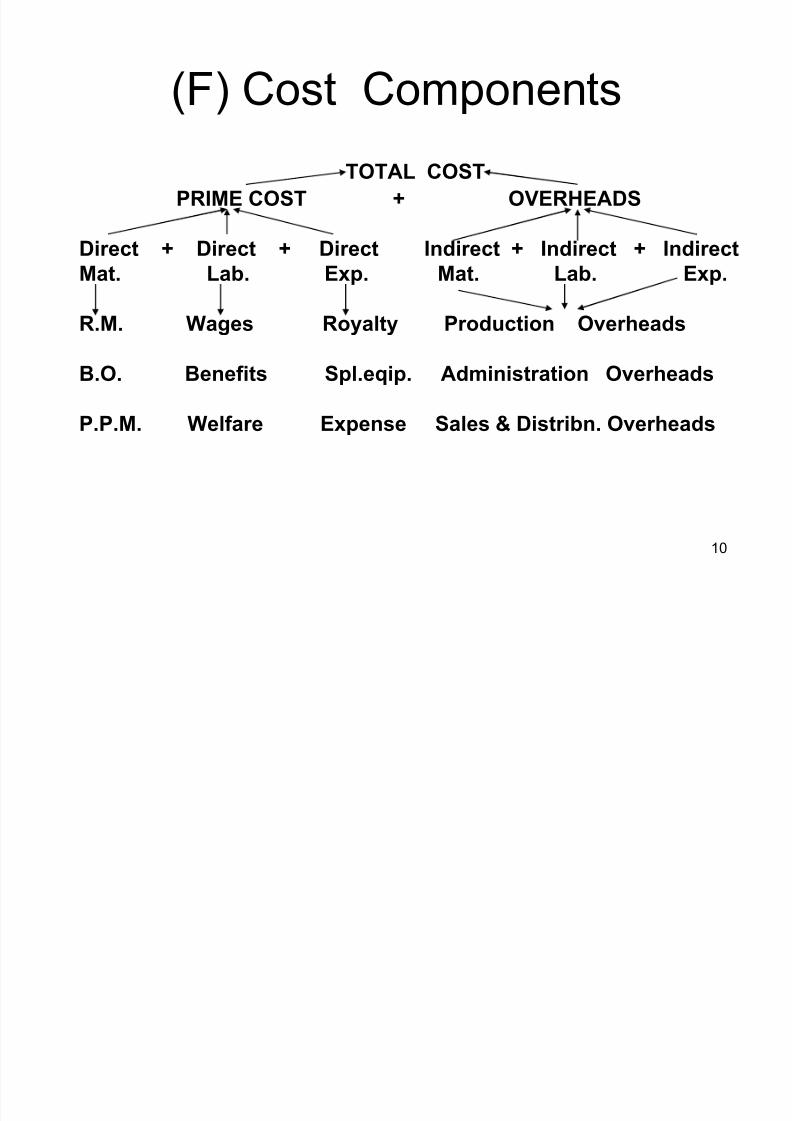

(F) Cost Components

TOTAL COST

PRIME COST + OVERHEADS

Direct + Direct + Direct Indirect + Indirect + Indirect

Mat. Lab. Exp. Mat. Lab. Exp.

R.M. Wages Royalty Production Overheads

B.O. Benefits Spl.eqip. Administration Overheads

P.P.M. Welfare Expense Sales & Distribn. Overheads

8/8/2019 Module 1 Cost Slides

http://slidepdf.com/reader/full/module-1-cost-slides 11/15

11

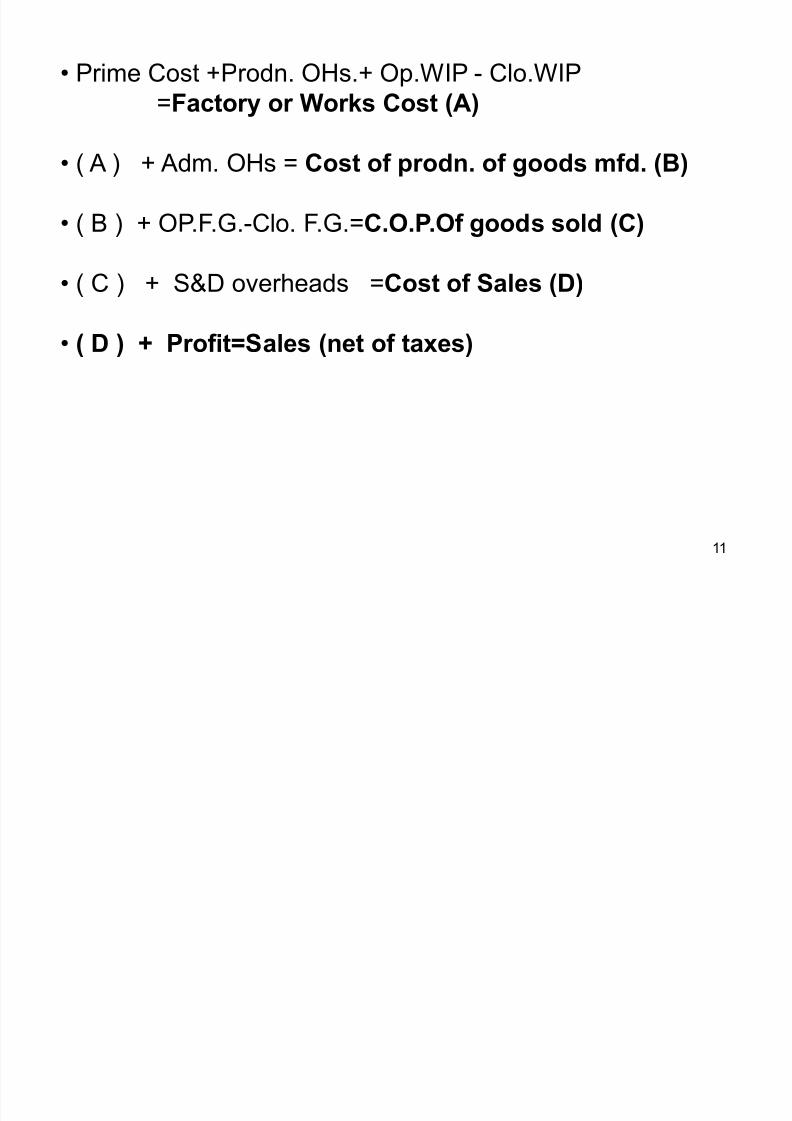

Prime Cost +Prodn. OHs.+ Op.WIP - Clo.WIP

=Factory or Works Cost (A)

( A ) + Adm. OHs = Cost of prodn. of goods mfd. (B)

( B ) + OP.F.G.-Clo. F.G.=C.O.P.Of goods sold (C)

( C ) + S&D overheads =Cost of Sales (D)

( D ) + Profit=Sales (net of taxes)

8/8/2019 Module 1 Cost Slides

http://slidepdf.com/reader/full/module-1-cost-slides 12/15

12

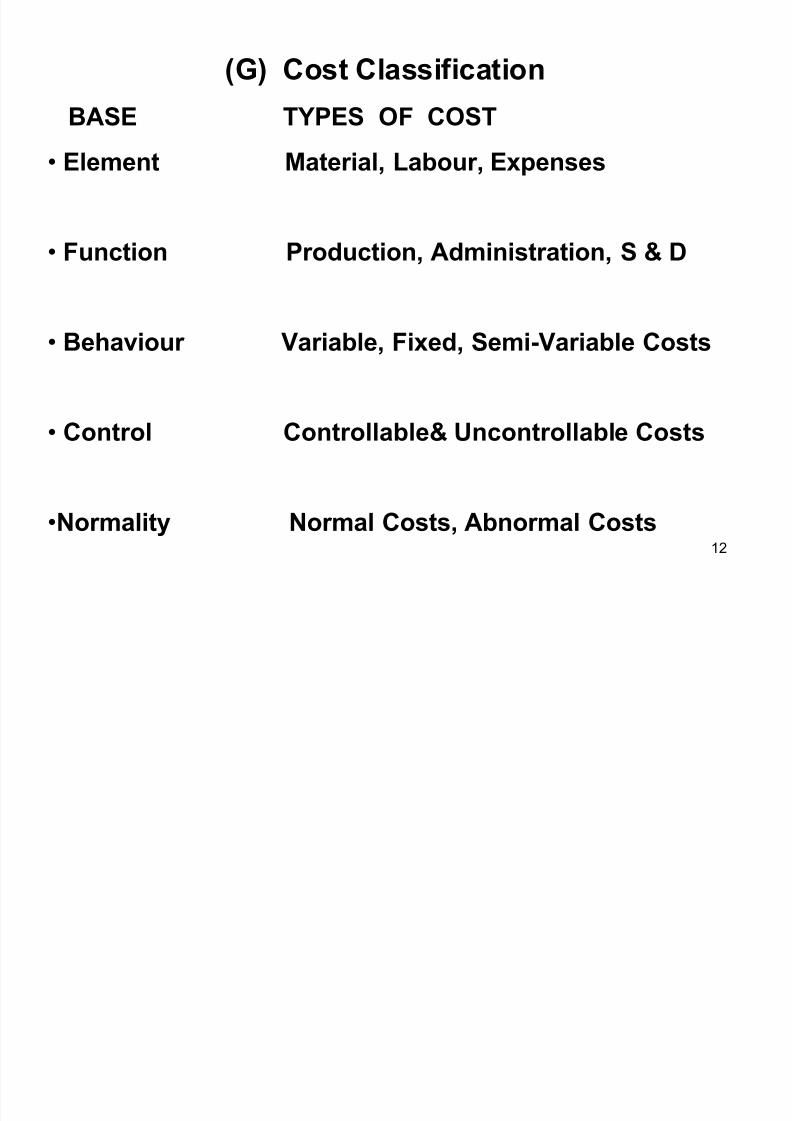

(G) Cost Classification

BASE TYPES OF COST

Element Material, Labour, Expenses

Function Production, Administration, S & D

Behaviour Variable, Fixed, Semi-Variable Costs

Control Controllable& Uncontrollable Costs

Normality Normal Costs, Abnormal Costs

8/8/2019 Module 1 Cost Slides

http://slidepdf.com/reader/full/module-1-cost-slides 13/15

8/8/2019 Module 1 Cost Slides

http://slidepdf.com/reader/full/module-1-cost-slides 14/15

14

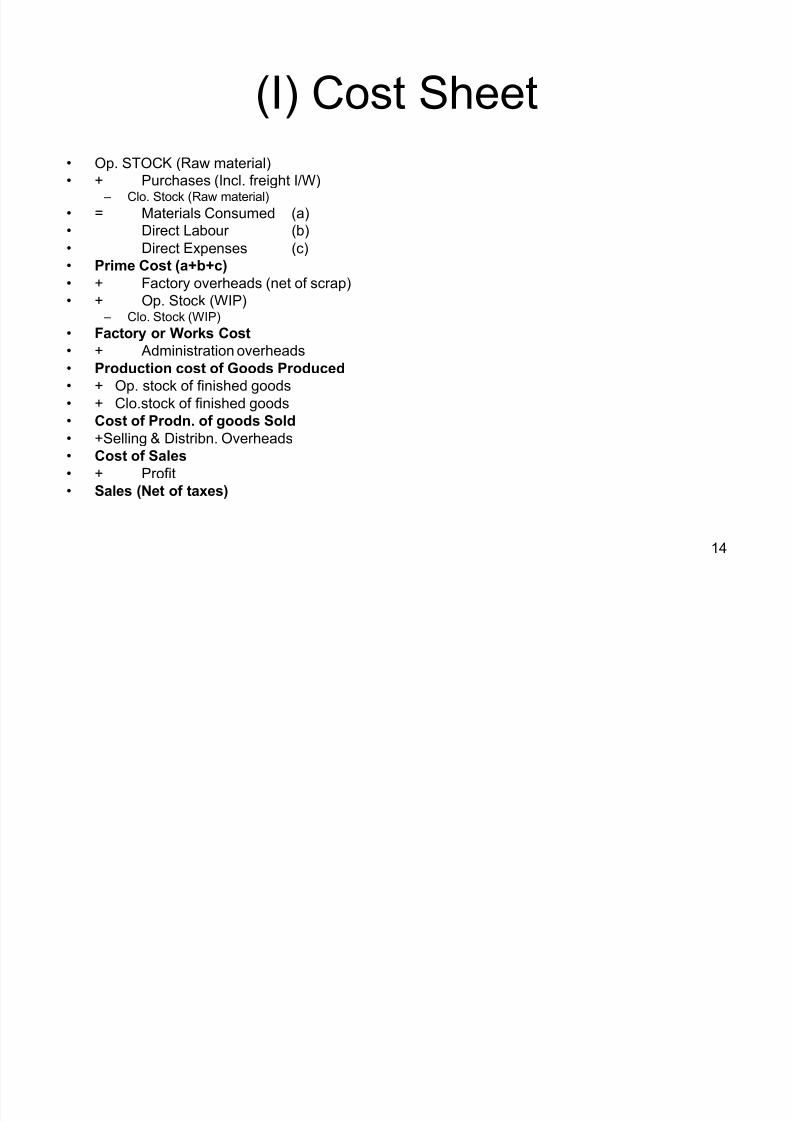

(I) Cost Sheet

Op. STOCK (Raw material)

+ Purchases (Incl. freight I/W) ± Clo. Stock (Raw material)

= Materials Consumed (a)

Direct Labour (b)

Direct Expenses (c)

Prime Cost (a+b+c)

+ Factory overheads (net of scrap) + Op. Stock (WIP)

± Clo. Stock (WIP)

Factory or Works Cost

+ Administration overheads

Production cost of Goods Produced

+ Op. stock of finished goods

+ Clo.stock of finished goods

Cost of Prodn. of goods Sold +Selling & Distribn. Overheads

Cost of Sales

+ Profit

Sales (Net of taxes)

8/8/2019 Module 1 Cost Slides

http://slidepdf.com/reader/full/module-1-cost-slides 15/15

15

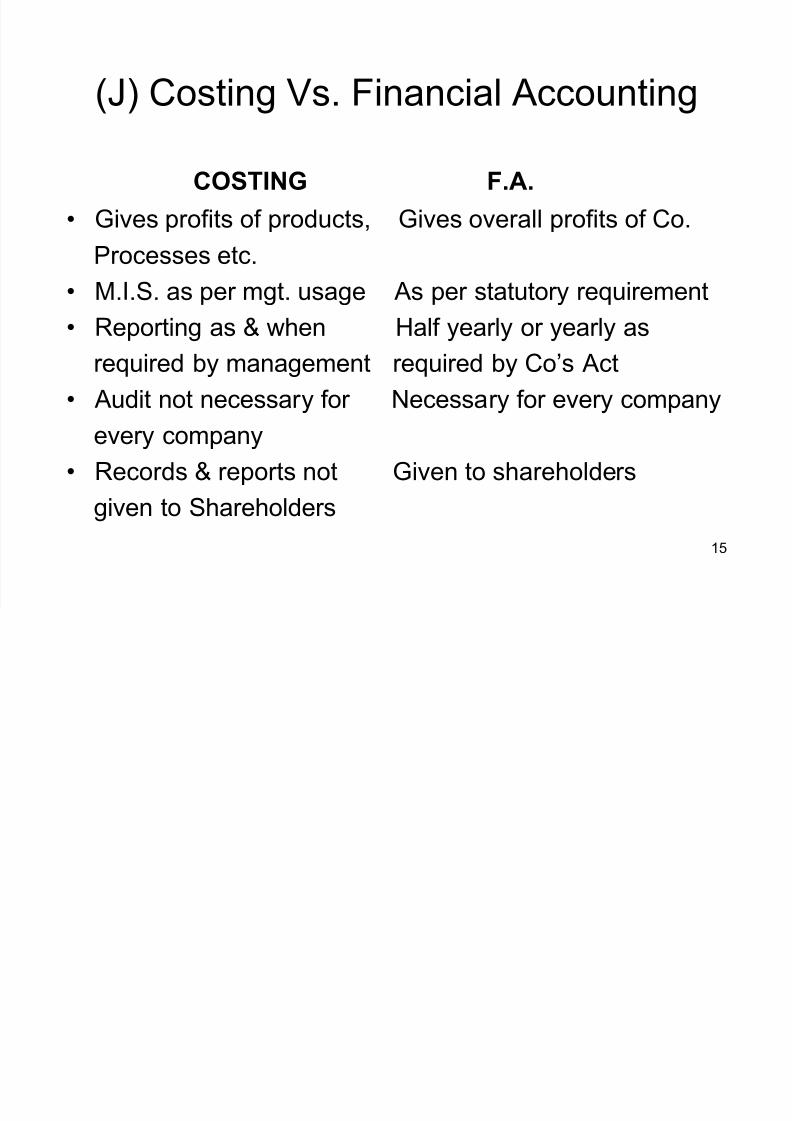

(J) Costing Vs. Financial Accounting

COSTING F.A.

Gives profits of products, Gives overall profits of Co.

Processes etc.

M.I.S. as per mgt. usage As per statutory requirement

Reporting as & when Half yearly or yearly as

required by management required by Co¶s Act

Audit not necessary for Necessary for every company

every company

Records & reports not Given to shareholders

given to Shareholders