module 1: the nature and operations of the iasb

TRANSCRIPT

Module 1:The nature and operations of the IASB

Origins of International Accounting Standard

Boards (IASB)

Structure of IFRS Foundation

International Accounting Standard (IAS

standards) and International Financial

Reporting Standards (IFRS Standards) that are

currently in issue

The purpose of financial statements – The

Conceptual Framework for Financial

Reporting

What you will learn?

Formation of the Board

1973

1997

1 July 2000

1 April 2001

The International Accounting Standards Committee (IASC) was founded

Accounting Standards were set by an IASC Board (13 country members & up to 3 additional organisational members

IASC concluded that there must be a convergence between national accounting standards and practices and global accounting standards

International Accounting Standards Board – a new standards setting body was formed

The Board (IASB) took over from the IASC the responsibility for setting International Accounting Standards

More than 140 accountancies body in IASC membership (1973 – 2001)

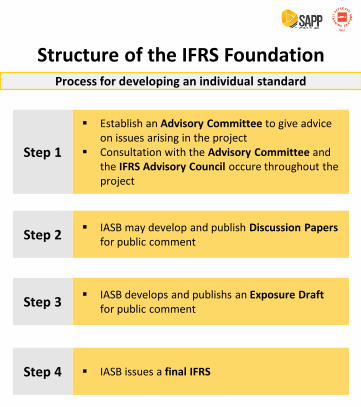

Structure of the IFRS Foundation

The Monitoring Board

IFRS Foundation Trustees

The IFRS Advisory Council

The IASB(the Board)

The IFRS Interpretations

Committee

IFRS Standards

Appoints & advises

Appoints &

oversees

Appoints&

overseesAdvises

Develop & issues Interprets

Appoints&

oversees

Process for developing an individual standard

Structure of the IFRS Foundation

Establish an Advisory Committee to give advice on issues arising in the project

Consultation with the Advisory Committee and the IFRS Advisory Council occure throughout the project

IASB may develop and publish Discussion Papers for public comment

IASB develops and publishs an Exposure Draft for public comment

IASB issues a final IFRS

Step 1

Step 2

Step 3

Step 4

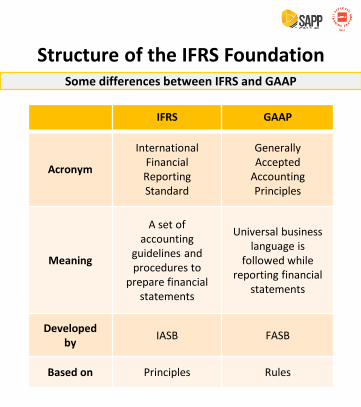

Some differences between IFRS and GAAP

Structure of the IFRS Foundation

IFRS GAAP

Acronym

International Financial Reporting Standard

Generally Accepted

Accounting Principles

Meaning

A set of accounting

guidelines and procedures to

prepare financial statements

Universal business language is

followed while reporting financial

statements

Developed by

IASB FASB

Based on Principles Rules

Advantages of applying IFRS

Structure of the IFRS Foundation

A business can present its FS on the same basis as its

foreign competitors, making FS comparable

Cross-border listing will be facilitated, making it easier

to raise capital abroad

Companies with foreign subsidiaries will have a

common, enabling company-wide accounting language

Foreign companies which are targets for takeovers or

mergers can be more easily appraised

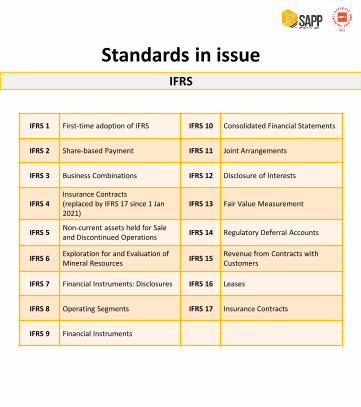

IFRS

Standards in issue

IFRS 1 First-time adoption of IFRS IFRS 10 Consolidated Financial Statements

IFRS 2 Share-based Payment IFRS 11 Joint Arrangements

IFRS 3 Business Combinations IFRS 12 Disclosure of Interests

IFRS 4Insurance Contracts (replaced by IFRS 17 since 1 Jan 2021)

IFRS 13 Fair Value Measurement

IFRS 5 Non-current assets held for Sale and Discontinued Operations

IFRS 14 Regulatory Deferral Accounts

IFRS 6Exploration for and Evaluation of Mineral Resources

IFRS 15Revenue from Contracts with Customers

IFRS 7 Financial Instruments: Disclosures IFRS 16 Leases

IFRS 8 Operating Segments IFRS 17 Insurance Contracts

IFRS 9 Financial Instruments

IAS

Standards in issue

IAS 1Presentation of Financial Statements

IAS 20

Accounting for Government Grants and Discolsure of Governance Assistance

IAS 32Financial Instruments Presentation

IAS 2 Inventories IAS 21The Effects of changrs in foreign exchange rate

IAS 33 Earnings Per Share

IAS 7Statement of Cash Flows

IAS 23 Borrowing costs IAS 34Interim Financial Reporting

IAS 8Accounting policies, changes in accounting estimates & errors

IAS 24Related Party Disclosure

IAS 36Impairment of Assets

IAS 10Events after the Reporting Period

IAS 26

Accounting and Reporting by Retirement Benefit Plans

IAS 37

Provisions, Contingent Liabilities and Contingent Assets

IAS 12 Income Taxes IAS 27Seperate Financial Statement (revised 2011)

IAS 38 Intangible Assets

IAS 16Property, Plant and Equipment

IAS 28

Investments in Associates and Joint Venture (revised 2011)

IAS 40 Investment property

IAS 19 Employee Benefits IAS 29Financial Reporting in Hyperinflationary Economies

IAS 41 Agriculture

Conceptual Framework for Financial Reporting

Qualitative characteristics of financial information

Fundamental characteristics Enhancing characteristics

Relevance

Materality

Faithful representation

Complete

Neutral

Free from bias

Substance over form

Comparability

Verifiability

Timeliness

Understandability

Main purpose of Financial Statements

To give information to users (particularly investors and

creditors) so that they can make financial decisions

Underlying assumption

Going concern

Five main elements of financial statements

Conceptual Framework for Financial Reporting

Assetas a result of past events

has a potential to produce economic benefits

Liabilitya present obligation of the entity

as a result of past events

Equityresidual interest in the assets after

deducting all its liabilities

Incomeincrease in assets or decrease in liabilities

that result in increases in equities

Expensesdecrease in assets or increase in liabilities

that result in decreases in equities

Assets and liabilities

Exercise

Asset Liability Neither

$50,000 spent by a manufacturer on training staff how to operate machinery

$10,000 spent by a business to patent its technology

$30,000 expected expenditure on redecorating business premises in the upcoming year

$15,000 that a retailer expects to have to repay to customers that return purchased items within the 30 day statutory return period

$100,000 losses expected by a car manufacturer in the upcoming financial year as a result of economic recession

$40,000 spent on equity shares in another company