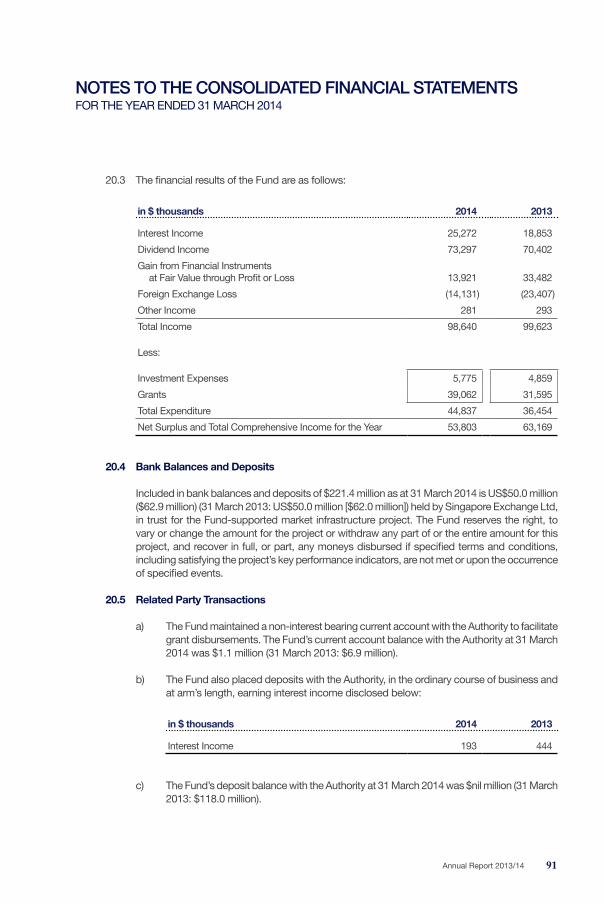

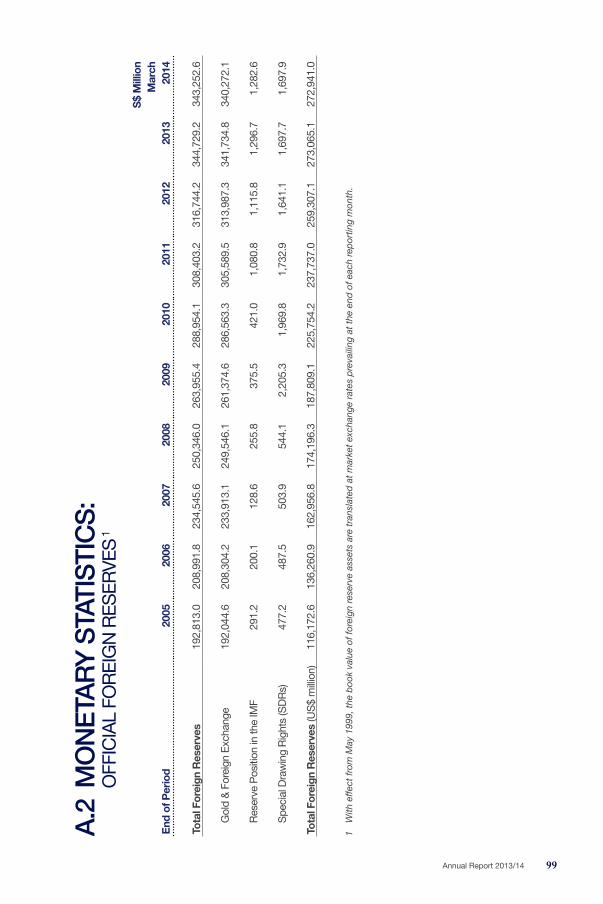

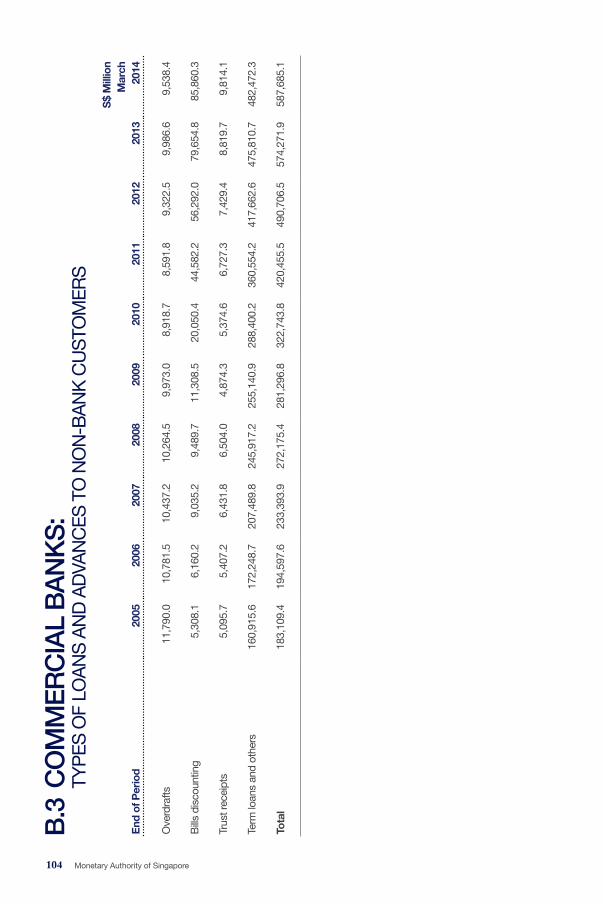

monetary authority of singapore report.pdf · bank of china-mas bilateral currency swap arrangement...

TRANSCRIPT

Monetary Authority of SingaporeAnnuAl RepoRt 2013/14

Monetary Authority of SingaporeAnnuAl RepoRt 2013/14

Contents05 Chairman’s Message

08 Board of Directors

10 Management Team

11 Governance Structure

12 Board Committees

13 Organisational Structure

14 Key Economic and Financial Statistics

16 Financial Structure: Number of Financial Institutions in Singapore

ANChOr OF ECONOMIC AND FINANCIAl STABIlITy

20 the eConomy

20 the Global Recovery picked up pace

20 private Demand Supported Growth in the G3

21 external Demand Driving Growth in Asia ex-Japan

21 Financial Vulnerabilities and Risks

21 Headline Inflation Declined in the G3

22 Singapore Recorded Faster Growth

23 Core Inflation Rose in H2 2013

24 monetary PoliCy

24 manaGement oF liQuiDity

24 enhancing Singapore Dollar liquidity Management Framework

24 enhancing MAS Renminbi Facility

26 manaGement oF oFFiCial ForeiGn reserves

rOBuST, TruSTED, AND PurPOSEFulFINANCIAl CENTrE

30 a robust FinanCial Centre

30 overall

30 Banking

31 Securities

33 Insurance

34 International Supervisory Cooperation

34 Box 1: International Monetary Fund’s Financial Sector Assessment programme

35 a trusteD FinanCial Centre

35 Financial Benchmarks

35 preventing Money laundering and terrorism Financing

36 enhancing exchange of Information on tax

37 a DynamiC anD PurPoseFul FinanCial Centre

37 Growing our Core Industry pillars

38 Box 2: Singapore as a Global Insurance Marketplace

39 new Growth Areas

39 enhancing Workforce Competencies

40 Box 3: Milestones in Developing the RMB Market in Singapore

SErvING ThE PuBlIC, ENGAGING STAKEhOlDErS

44 enGaGinG the PubliC

44 Managing Dollars and Cents

45 MoneySenSe

46 Box 4: MoneySenSe 10th Anniversary

47 ProteCtinG Consumers

47 Financial Advisory Industry Review

47 enhancing prospectus Disclosure Rules for offers of Securities

47 WorKinG With inDustry

47 Industry Initiative on Contract Certainty

48 MASnet-Access

48 partnership with Academia

vAluED PArTNEr ON ThEINTErNATIONAl FrONT

52 international Forums

52 promoting Global Growth and Stability

52 International Financial Regulatory Reforms

53 reGional Forums

53 Asia Region Funds passport

53 ASeAn Cooperation

54 ASeAn+3

54 Box 5: opening of a Representative office in Beijing

55 executive Meeting of east Asia-pacific Central Banks

55 bilateral CooPeration

55 training and technical Assistance

56 Box 6: MAS’ technical Assistance programmes

ONE MAS: INTEGrATED ANDCOhESIvE

60 risK manaGement anD business Continuity

60 Controls anD oPerations

60 Audit Assurance

60 procurement Management

60 Building Services and Safety

60 enhancing Mobility and productivity

61 builDinG a stronG mas Family

61 leadership Development

61 Functional and General training

61 Attachments and Secondments

62 organisational Review exercise

62 Recognition of Staff

62 Fostering esprit De Corps

64 Box 7: Community outreach

67 FinanCial statements

97 statistiCal annex

115 Glossary

our mission is to promote sustained non-inflationary economic growth, and a sound and progressive financial centre

MAS’ FuNCTIONS• to act as the central bank of Singapore,

including the conduct of monetary policy, the issuance of currency, the oversight of payment systems and serving as banker to and financial agent of the Government

• to conduct integrated supervision of financial services and financial stability surveillance

• to manage the official foreign reserves of Singapore

• to develop Singapore as an international financial centre

WhATWe DO

Chairman’s MeSSAGe

the recovery in the global economy has entered a new phase. the advanced economies, which have experienced a slow and protracted recovery from the global financial crisis, are expected to provide much of the impetus for growth in the coming year. the united States is seeing continued labour market strengthening and resilience in private consumption, enabling it to begin a gradual process of normalising monetary policy. In the euro zone, financial stresses are receding, supporting a modest recovery from recession. Japan has experienced a spurt in growth, aided by unprecedented monetary easing. Asia could benefit from a slight uplift in exports this year, although tighter financial conditions and pockets of political uncertainty are weighing down on domestic demand. Growth in China, still a major engine of the world economy, is expected to moderate as it seeks to rein in the shadow banking sector and restructure its economy.

Global financial resilience has also improved. Bank balance sheets have seen further repair in the advanced economies. Asian banks could face some headwinds from slower economic growth, normalisation of global monetary conditions, and moderation in asset prices. But they remain anchored by healthy capital buffers and sound funding profiles.

the Singapore economy has shifted to a path of lower growth, constrained by slower labour force growth. In this context, the economy grew by a relatively strong 3.9%, compared with 2.5% in 2012. CpI-All Items inflation eased to 2.4% in 2013 from 4.6% in 2012, with the sustained appreciation of the Singapore Dollar dampening imported inflation and policy measures to contain Certificate of entitlement price increases and property market rentals bearing fruit.

With the gradual improvement in the global economic environment, our economy should see growth of 2–4% this year. CpI-All Items inflation is projected to average 1.5–2.0% in 2014. However, MAS Core Inflation which excludes the cost of accommodation and private road transport is expected to remain firm at 2–3% during this period of economic restructuring. this is higher than the historical norm, and is underpinned by the persistence of a tight labour market while improvements in productivity growth take time.

MAS will remain vigilant in ensuring that cost pressures are contained over the medium term, and inflation expectations are well-anchored. our monetary policy stance has been consistent with that aim. the slope of the S$ nominal effective exchange rate policy band was kept on a modest and gradual appreciation path in April and october 2013, and in April 2014.

the International Monetary Fund conducted a rigorous assessment of Singapore’s financial system in 2013 under its Financial Sector Assessment programme. the assessment affirmed Singapore’s standing as a sound and stable financial centre. It found Singapore’s regulatory and supervisory frameworks and practices to be among the best globally. the financial system was also assessed to be resilient against robust stress test scenarios.

“the International Monetary Fund conducted a rigorous assessment of Singapore’s financial system in 2013... (and) found Singapore’s regulatory and supervisory frameworks and practices to be among the best globally.”

5Annual Report 2013/14

MAS introduced further measures in 2013 to sustain financial stability and foster prudence among financial institutions and borrowers. We introduced a total Debt Servicing Ratio (tDSR) framework in June 2013 to govern property loans granted by financial institutions. the tDSR will help strengthen FIs’ credit underwriting practices over the long term and encourage financial prudence among borrowers. More immediately, it has had a salutary effect in cooling the property market.

together with the Singapore exchange (SGX), MAS launched a public consultation on measures to strengthen the securities market. MAS and SGX had, following a review of the securities market structure and practices, developed proposals to promote orderly trading and responsible investing, enhance the transparency of market intervention measures, and strengthen the process for admitting new listings and enforcement against listing rule breaches.

MAS has been working closely with the industry in implementing the recommendations of the Financial Advisory Industry Review (FAIR). these include a direct channel for consumers to buy life insurance products without having to pay commissions, a web aggregator for consumers to compare life insurance products, and a balanced scorecard remuneration framework to promote professional and ethical conduct among advisers. the FAIR initiatives will raise the standards and professionalism of the financial advisory industry, and encourage greater efficiency in the distribution of life insurance and investment products in Singapore.

2013 also marked the 10th anniversary of MoneySenSe, the national financial education and literacy programme that MAS has led, alongside various government agencies and financial industry associations. MoneySenSe has reached out to Singaporeans from all walks of life, through a wide range of channels including school programmes, workplace talks, community events,

public seminars, and the mass and social media. In the coming years, we will step up efforts to tailor financial education and outreach to the different segments of the population, such as low-income families and senior citizens as well as couples getting married. We will also equip social workers with basic financial knowledge so that they can better support Singaporeans seeking help.

Singapore continues to actively support global efforts to combat money laundering and the financing of terrorism. together with the Ministry of Home Affairs and the Ministry of Finance, MAS published Singapore’s first national Money laundering and terrorist Financing Risk Assessment (nRA) report in January 2014. Most of the industries covered by the report, including banks and casinos, were found to have robust preventive regimes. MAS is working to further strengthen the frameworks for anti-money laundering and countering the financing of terrorism

“the FAIR initiatives will raise the standards and professionalism of the financial advisory industry, and encourage greater efficiency in the distribution of life insurance and investment products in Singapore. ”

Chairman’s messaGe

in the segments identified for improvement in the report, including remittance agents, money-changers, and internet-based stored value facility holders. We are also introducing new regulations to address risks entailed in virtual currency intermediaries.

the launch of RMB clearing services in Singapore in May 2013 marked a significant milestone. We have taken active steps to support RMB market development, including enhancing the people’s Bank of China-MAS Bilateral Currency Swap Arrangement and the MAS RMB Facility. the introduction of RMB cross-border channels

6 Monetary Authority of Singapore

between Singapore and Suzhou Industrial park and tianjin eco-city, and the RMB Qualified Foreign Institutional Investor programme, should also enable greater RMB flows between China and Singapore. In addition, MAS will be working to foster greater connectivity and cooperation between the key RMB centres globally.

MAS is also working actively to sustain Singapore’s development as a financial centre and provide good career opportunities for Singaporeans in the industry.

We will continue to support the growth of globally competitive teams in Singapore, and work with key financial institutions to develop promising Singaporean talents in the industry. this includes structured programmes to groom Singaporeans for future leadership positions through rotation across various business lines and taking on overseas assignments. A new Asian Financial

“We will continue to support the growth of globally competitive teams in Singapore, and work with key financial institutions to develop promising Singaporean talents in the industry. ”

leaders programme will be launched to equip local practitioners with Asia-relevant leadership capabilities and prepare them for senior regional and global positions.

I would like to thank the financial industry players and our partners who work alongside MAS, and the management and staff of MAS, for their continued commitment to achieving sustainable growth and developing Singapore as a dynamic and well-respected international financial centre.

Tharman ShanmugaratnamChairman

7Annual Report 2013/14

boarD oF DIReCtoRS

Tharman ShanmugaratnamChairmanDeputy prime MinisterMinister for Finance

lim hng KiangDeputy ChairmanMinister for trade & Industry

heng Swee KeatMinister for education

lawrence Wong Shyun TsaiMinister for Culture, Community and Youth, Second Minister for Communications and Information

Quek See TiatChairman of Audit CommitteeChairman, Building and Construction Authority

lim Chee OnnChairman of Risk Committee, Senior International Advisor, Singbridge private ltd

8 Monetary Authority of Singapore

Peter Ong Boon Kweepermanent Secretary,Ministry of Finance

Tan Chorh Chuanpresident,national university of Singapore

ravi MenonManaging Director, MAS

Goh Chok TongSenior Advisor to MASemeritus Senior Minister

9Annual Report 2013/14

manaGement teAM

A. ravi Menon managing Director

B. Ong Chong Tee Deputy managing Director Financial Supervision

C. Jacqueline loh Deputy managing Director Monetary policy & Investment

/ Development & International

D. Andrew Khoo Deputy managing Director Corporate Development

E. Chia Der Jiun assistant managing Director Markets & Investment

F. Chua Kim leng assistant managing Director Banking & Insurance

G. lee Boon Ngiap assistant managing Director Capital Markets

h. leong Sing Chiong assistant managing Director Development & International

I. low Kwok Mun assistant managing Director Finance, Risk and Currency

J. Ng Nam Sin assistant managing Director Corporate, HR & It Services

K. Edward robinson assistant managing Director and Chief economist economic policy

l. Wong Nai Seng assistant managing Director policy, Risk & Surveillance

IK

C

e

ABD

H l JG

F

10 Monetary Authority of Singapore

GovernanCeStRuCtuRe

the Board is responsible for the high-level governance of MAS. the Board Committees exercise broad oversight and approve major changes to policies and strategies relating to the principal functions of MAS. the Managing Director is responsible for the day-to-day operations of MAS and is assisted by various groups and management committees within

MAS Board

Monetary and Investment

policy Meeting

Chairman’s Meeting

Risk Committee

Board StaffCommittee

Audit Committee

executive Committee

Management Committee

Financial Stability

Committee

Financial Supervision Committee

Development and

International Committee

Markets and Investment Committee

payment Systems

Development Steering Group

payments and

Settlement Committee

Civil penalty enforcement Committee

Management Staff

Committee I

Management Staff

Committee II

MAS. the executive Committee is the key decision making body at the management level. Chaired by the Managing Director, it is responsible for ensuring that MAS’ policies and initiatives are aligned with its overall direction and objectives. the executive Committee also oversees matters referred to it by other management decision-making fora.

Board and Board Committees

Management Committees

11Annual Report 2013/14

boarD CoMMItteeS

the MAS Act provides that the Board of Directors shall be responsible for the policy and general administration of the affairs and business of MAS. the Board is assisted by the following committees:

Chairman’s Meeting the Chairman’s Meeting approves major changes to MAS’ supervisory policies and regulatory framework. It also approves major changes to policies and strategies relating to financial centre development and international and regional relations. the Chairman’s Meeting comprises tharman Shanmugaratnam (Chairman), lim Hng Kiang, Heng Swee Keat, lawrence Wong and Ravi Menon.

Monetary and Investment Policy Meeting the Monetary and Investment policy Meeting deliberates and decides on issues relating to the formulation and implementation of monetary policy with the objective of maintaining price stability for sustainable economic growth. the Meeting also oversees the investment of MAS’ reserves. the Monetary and Investment policy Meeting comprises tharman Shanmugaratnam (Chairman), lim Hng Kiang, Heng Swee Keat, lawrence Wong and Ravi Menon.

Audit Committee the Audit Committee provides an independent assessment of MAS’ internal controls and financial reporting process. the Committee also reviews the efforts of MAS’ internal and external auditors. the Audit Committee comprises Quek See tiat (Chairman), peter ong and tan Chorh Chuan.

risk Committee the Risk Committee provides oversight and guidance on the management of risks faced by MAS. the Committee oversees the MAS-wide risk management framework, and reviews MAS’ risk management policies and processes for reporting of risks. the Risk Committee comprises lim Chee onn (Chairman), tan Chorh Chuan and Ravi Menon.

Staff Committeethe Staff Committee approves MAS’ key personnel policies, including overall pay policy. It also approves matters relating to the appointment, promotion and remuneration of senior management staff. the Staff Committee comprises tharman Shanmugaratnam (Chairman), lim Hng Kiang, Heng Swee Keat and Ravi Menon.

As at 1 July 2014

12 Monetary Authority of Singapore

orGanisationalStRuCtuRe

MONETAry POlICy & INvESTMENT / DEvElOPMENT & INTErNATIONAlJacqueline loh Deputy Managing Director

ECONOMIC POlICyedward robinson Assistant Managing Director and Chief economist

Economic Analysisng bok engexecutive Director

Economic Surveillance & ForecastingCeline siaexecutive Director

MArKETS & INvESTMENTChia Der JiunAssistant Managing Director

Monetary & Domestic Markets ManagementChia Der Jiun Assistant Managing Director

reserve Managementyap Chuin houiexecutive Director

DEvElOPMENT & INTErNATIONAlleong sing Chiong Assistant Managing Director

Financial Centre Developmentvalerie tayexecutive Director

Financial Markets Strategybenny Chey Director

Internationalbernard Weeexecutive Director

FINANCIAl SuPErvISIONong Chong teeDeputy Managing Director

BANKING & INSurANCEChua Kim lengAssistant Managing Director

Banking Department IChua Kim leng Assistant Managing Director

Banking Department IIWan aik Chye executive Director

Banking Department IIItai boon leongexecutive Director

Insuranceloo siew yeeexecutive Director

CAPITAl MArKETSlee boon ngiapAssistant Managing Director

Capital Markets Intermediariesmerlyn eeexecutive Director

Investment IntermediariesChristopher tanexecutive Director

Market ConductPaul yuenexecutive Director

Markets Policy & Infrastructureng yao loongexecutive Director

POlICy, rISK & SurvEIllANCEWong nai sengAssistant Managing Director

Prudential Policylim tuang lee executive Director

Specialist riskho hern shinexecutive Director

Macroeconomic Surveillancelam san lingexecutive Director

COrPOrATE DEvElOPMENTandrew KhooDeputy Managing Director

COrPOrATE, hr & IT SErvICESng nam sinAssistant Managing Director

Corporate Servicesbernard yeoexecutive Director

Information Technologylawrence angexecutive Director

human resourceluz Fooexecutive Director

MAS Academyng nam sinAssistant Managing Director

FINANCE, rISK & CurrENCylow Kwok munAssistant Managing Director

Financeteo Kok mingexecutive Director

risk ManagementDaniel Wangexecutive Director

CurrencyChung Wei Kenexecutive Director

As at 1 July 2014

ravi menonManaging Director

MANAGING DIrECTOr’S OFFICE

legalng heng FattGeneral Counsel

Strategic Planning and Communicationsmerlyn eeexecutive Director

Internal Audittimothy ngexecutive Director

teo swee lianSpecial Advisor

13Annual Report 2013/14

Key eConomiCAnD FInAnCIAl StAtIStICS

2009 2010 2011 2012 2013

National Income AggregatesGross Domestic product At Current Market prices (S$m) 279,858.0 322,361.1 344,712.4 358,542.6 372,813.9 Growth Rate (% change) 2.9 15.2 6.9 4.0 4.0 At 2010 Market prices (S$m) 279,729.3 322,361.1 341,886.1 350,446.0 363,941.9 Growth Rate (% change) -0.6 15.2 6.1 2.5 3.9 Gross national Income At Current Market prices (S$m) 266,889.0 320,526.6 339,767.8 350,029.7 363,827.2 Growth Rate (% change) 2.8 20.1 6.0 3.0 3.9

labour Forceunemployment Rate (%) 3.0 2.2 2.0 2.0 1.9 productivity Growth (% change) -3.3 11.6 2.2 -1.4 -0.2 Changes in employment ('000) 37.6 115.9 122.6 129.1 136.2 Average Monthly earnings (% change) -2.6 5.6 6.0 2.3 4.3 unit labour Cost (% change) 0.7 -3.2 1.8 3.9 2.6

Savings and Investment Gross national Savings (S$m) 124,493.0 166,120.1 172,782.5 171,566.5 176,576.1 As % of GnI 46.6 51.8 50.9 49.0 48.5 Gross Domestic Capital Formation (S$m) 77,424.4 89,841.2 94,053.8 108,894.9 108,311.5 As % of GnI 29.0 28.0 27.7 31.1 29.8

Balance of Payments (S$m)Goods Balance 69,205.5 85,682.2 87,472.2 79,249.8 84,827.9 exports of Goods 417,971.9 504,848.8 543,154.4 542,645.1 547,495.9 Growth Rate (% change) -16.3 20.8 7.6 -0.1 0.9 Imports of Goods 348,766.4 419,166.6 455,682.2 463,395.3 462,668.0 Growth Rate (% change) -20.8 20.2 8.7 1.7 -0.2 Services and other Balances -22,136.9 -9,403.3 -8,743.5 -16,578.2 -16,563.3 Current Account Balance 47,068.6 76,278.9 78,728.7 62,671.6 68,264.6 As % of GnI 17.6 23.8 23.2 17.9 18.8 Capital and Financial Account Balance -30,796.5 -24,920.6 -58,122.5 -28,898.2 -46,832.1 Balancing Item 184.1 6,122.2 881.5 -1,167.5 1,298.4 overall Balance 16,456.2 57,480.5 21,487.7 32,605.9 22,730.9 official Foreign Reserves 263,955.4 288,954.1 308,403.2 316,744.2 344,729.2

Inflation (% change)Consumer price Index 0.6 2.8 5.2 4.6 2.4 GDp Deflator 3.5 0.0 0.8 1.5 0.1

Monetary Aggregates (% change)M1 23.5 20.3 16.1 7.7 9.9 M2 11.3 8.6 10.0 7.2 4.3 M3 10.6 8.3 10.1 7.6 4.3

14 Monetary Authority of Singapore

2009 2010 2011 2012 2013

Interest rates (period average, % per annum)prime lending Rate 5.38 5.38 5.38 5.38 5.38Banks' 3-month Fixed Deposit Rate 0.29 0.21 0.17 0.14 0.143-month S$ SIBoR 0.70 0.56 0.41 0.39 0.383-month uS$ lIBoR 0.69 0.34 0.34 0.43 0.27

Exchange rates (period average, S$ per)uS Dollar 1.4545 1.3635 1.2579 1.2497 1.2513 pound Sterling 2.2737 2.1073 2.0161 1.9803 1.9573 euro 2.0242 1.8095 1.7495 1.6071 1.6621 100 Japanese Yen 1.5562 1.5543 1.5780 1.5672 1.2840 Malaysian Ringgit 0.4126 0.4234 0.4111 0.4046 0.3973

Banking and FinanceCommercial Banks' Assets/

liabilities (S$m)706,814.2 781,607.4 855,811.4 911,009.0 973,216.9

Growth Rate (% change) 5.8 10.6 9.5 6.4 6.8

Finance Companies' Assets/ liabilities (S$m)

11,691.9 11,523.6 12,165.3 14,967.5 14,985.7

Growth Rate (% change) -7.1 -1.4 5.6 23.0 0.1

Merchant Banks' Assets/ liabilities (S$m)

76,354.4 89,760.3 87,851.1 92,411.0 84,941.3

Growth Rate (% change) 5.2 17.6 -2.1 5.2 -8.1

Asian Currency units' Assets/ liabilities (uS$m)

869,399.6 971,299.4 1,019,532.9 1,093,264.6 1,180,617.4

Growth Rate (% change) -4.7 11.7 5.0 7.2 8.0

Insurancelife Insurers' Assets/liabilities (S$m) 119,895.5 131,903.7 133,905.4 148,592.5 153,208.7 Growth Rate (% change) 19.9 10.0 1.5 11.0 3.1

General Insurers' Assets/ liabilities (S$m) 15,905.8 17,431.6 27,209.4 26,267.6 26,484.0 Growth Rate (% change) 5.6 9.6 56.1 -3.5 0.8

CPFexcess of Contributions over

Withdrawals (S$m)9,404.4 12,374.2 14,184.8 14,321.6 13,666.8

Domestic Capital Market net Funds Raised in Domestic

Capital Market (S$m)56,566.5 62,296.5 82,763.7 78,664.9 100,252.1

Note: Domestic interbank rates have been discontinued with effect from 1 January 2014 and replaced with S$ SIBOR. US$ SIBOR rates have been also replaced with the US$ LIBOR.

15Annual Report 2013/14

FinanCial struCture:nuMBeR oF FInAnCIAl InStItutIonS In SInGApoRe

31 March 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Banks 111 108 108 113 114 120 120 123 123 124local1 5 5 5 6 6 7 6 6 6 5 Foreign 106 103 103 107 108 113 114 117 117 119 Full banks 24 24 24 24 27 25 26 26 27 28 Wholesale banks2 35 34 36 42 41 46 50 52 53 55 offshore banks 47 45 43 41 40 42 38 39 37 36

(Banking offices including head offices and main offices) (396) (397)

(399) (408) (409) (421) (428) (432) (425) (449)

Asian Currency units 153 151 154 158 161 162 163 165 161 159Banks 106 104 106 111 112 117 117 120 120 121Merchant banks 47 47 48 47 49 45 46 45 41 38

Finance Companies 3 3 3 3 3 3 3 3 3 3(Finance companies' offices including head offices)

(39) (39) (39) (39) (39) (39) (39) (39) (39)

(39)

Merchant Banks 48 48 49 49 50 46 47 46 42 39

Insurance Companies 140 149 153 151 158 158 157 164 168 177Direct insurers 55 56 61 59 62 64 63 70 72 79Reinsurers 28 28 27 25 27 26 28 29 28 31Authorised reinsurers 0 5 5 5 6 6 6 6 6 6Captive insurers 57 60 60 62 63 62 60 59 62 61

Insurance Brokers 61 63 62 65 66 63 64 67 69 71

representative Offices 45 42 43 45 36 32 37 38 40 37Banks 45 42 43 45 36 30 34 36 38 36Merchant banks - - - - - - - - - -Insurance3 - - - - - 2 3 2 2 1

International Money Brokers 10 9 10 10 10 10 10 9 9 9

16 Monetary Authority of Singapore

1 Local banks comprise 5 full banks. 2 Previously known as restricted banks. 3 Data is unavailable for the period between 2004 and 2009. 4 Regulation of real estate investment trust management came into effect on 1 August 2008. 5 Regulation of credit rating services came into effect on 17 January 2012. 6 Regulation of trust companies came under the purview of MAS when the Trust Companies Act came into effect

on 1 February 2006. 7 Registration of fund management companies commenced under an enhanced regulatory regime which came into effect on 7 August 2012.

31 March 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

licensed Financial Advisers 56 61 67 69 73 71 67 67 62 58

Capital Markets Services licensees

168 171 183 215 221 224 251 250 295 443

Dealing in Securities 65 72 77 93 90 99 98 94 106 118trading in Futures Contracts

34 38 40 46 50 48 47 50 52 59

Advising on Corporate Finance

30 33 36 37 37 34 33 34 37 40

Fund Management 91 92 97 110 113 107 118 119 158 289leveraged Foreign exchange trading

11 13 14 18 19 19 19 20 23 24

Securities Financing 15 16 15 16 16 17 18 17 17 17providing Custodial Services for Securities

27 31 34 38 40 39 40 40 38 37

Real estate Investment trust Management4

- - - - 1 7 22 23 26 31

providing Credit Rating Services5

- - - - - - - - 3 3

licensed Trust Companies6 - - 31 35 38 40 48 50 51 52

registered Fund Management Companies7

- - - - - - - - 74 236

17Annual Report 2013/14

ANChOR of

eCONOMIC and FINANCIAL STABILITY

ThE ECONOMy

ThE GlOBAl rECOvEry PICKED uP PACE

the global economy expanded by 3.8% in 2013, similar to the 3.9% growth in 2012. However, the recovery gathered momentum as the year progressed. In the united States (uS), private consumption remained resilient despite a large fiscal contraction that dragged growth down, particularly in the first half of the year. the euro zone emerged from recession in the second quarter of 2013, on the back of strengthening private investment. Japan’s growth was boosted by fiscal and monetary stimuli, although weaker exports dampened momentum in the second half. In Asia ex-Japan, a slowdown in domestic demand was partially offset by a strengthening of external trade in late 2013.

After five years of unconventional monetary policy, the uS Federal Reserve started the process towards policy normalisation last year. In mid-2013, concern over the timing of the Federal Reserve’s withdrawal of quantitative easing (Qe) sparked a market sell-off and an abrupt reversal of capital flows in some emerging economies. Following this bout of financial volatility, several countries in Asia took decisive policy action to halt the build-up of external imbalances and bolster confidence. As a result, market reactions following the start of Qe tapering in December 2013 were generally more subdued.

PrIvATE DEMAND SuPPOrTED GrOWTh IN ThE G3

Growth in the uS economy slowed to 1.9% in 2013, from 2.8% in 2012, as the fiscal drag and heightened uncertainty over future economic policies worsened investor sentiment. In FY2013,

anChor oF eConomiC AnD FInAnCIAl StABIlItY

fiscal tightening amounted to an estimated 2.9% of GDp, mainly due to the budget sequester that came into effect in March 2013. expectations of an early Qe tapering in May 2013 triggered a rise in mortgage rates, dampening the recovery in the housing market, while the partial government shutdown in october 2013 weighed further on business sentiment. nonetheless, household confidence remained resilient and private consumption spending stayed firm throughout the year, on the back of steady employment gains. policy uncertainty was significantly lifted towards the end of the year when the uS Congress agreed on a budget that would keep the federal government funded for the next two fiscal years.In Q1 2014, however, an unusually cold winter led to a contraction in uS GDp, although the economy has since picked up.

economic conditions in the euro zone improved progressively in 2013. the region exited from recession in Q2 and continued to expand at a modest pace in the two subsequent quarters. private investment led the recovery, as borrowing costs fell and corporate profitability improved. the recovery broadened to the periphery in H2 2013, with Spain and Italy returning to positive growth in Q3 and Q4, respectively, after being mired in recession for two years. However, private consumption remained sluggish and government spending in the highly indebted economies was cut back to meet deficit targets. As a result, the pace of recovery was insufficient to prevent an overall contraction in GDp of 0.4% for the whole of 2013, after a 0.6% decline in 2012. nevertheless, the euro zone economy continued to expand in Q1 2014, registering GDp growth of 0.7% on a q-o-q seasonally adjusted annualised rate (SAAR) basis.

Japan’s GDp growth picked up to 1.5%, from 1.4% in the previous year, as large-scale monetary

20 Monetary Authority of Singapore

easing and fiscal expansion were rolled out in the first half of the year. the effects of the stimulus measures waned towards the end of the year and flagging exports weighed on growth. nonetheless, economic activity in Q4 2013 was supported by the frontloading of household expenditure in anticipation of the scheduled rise in the consumption tax from 5% to 8% in April 2014. In the first three months of 2014, GDp growth accelerated to 6.7% q-o-q SAAR, as discretionary spending peaked ahead of the tax hike.

ExTErNAl DEMAND DrIvING GrOWTh IN ASIA Ex-JAPAN

Growth in the Asia ex-Japan economies slowed slightly to 5.1% in 2013 from 5.2% in 2012, as domestic demand weakened due to several headwinds. In China, monetary tightening and curbs on the informal financial sector restrained manufacturing and real estate investment, while an official campaign to rein in lavish government spending curtailed retail sales. nonetheless, China’s economy grew by 7.7% in 2013, unchanged from 2012, as state-financed infrastructure spending helped to shore up investment in the second half of the year.

Growth in the ASeAn-4 economies slowed more rapidly to 5.0% in 2013, from 6.1% in 2012. Credit expansion, which had been constrained by deteriorating external balances and rising household leverage, moderated further amid tighter global liquidity and higher long-term interest rates. economic activity across the region was also dampened by the partial retraction of fiscal spending. nevertheless, an improvement in external demand in the second half of the year helped to cushion the pullback in domestic demand, with net exports contributing positively to growth since Q3 2013, after posing a drag for seven consecutive quarters.

the newly industrialised economies’ (nIes) strong economic fundamentals enabled them to better weather the effects of market volatility arising from Qe tapering. As a result, GDp growth in the nIes as a whole accelerated to 2.7% in 2013, from 1.7% in 2012, as an export-led recovery towards the end of 2013 boosted domestic demand. Despite some slippage in Q1 2014 due to the temporary retraction in uS demand and slower growth in China, Asia ex-

Japan exports and economic activity have picked up again in recent months.

FINANCIAl vulNErABIlITIES AND rISKS

Global financial markets performed strongly in FY2013, underpinned by improved economic prospects in advanced economies and still-accommodative global monetary conditions. From April 2013 to March 2014, the S&p 500 rose by 19.9%, the DJ eurostoxx rose by 21.5%, and the nikkei 225 rose by 22.2%. Meanwhile, the MSCI Asia ex-Japan Index rose by a more moderate 0.6% as emerging markets experienced some market volatility triggered by uncertainty over Qe tapering.

In the advanced economies, financial conditions have improved significantly alongside continued progress in financial system reforms and the repairing of bank balance sheets. In europe, investor confidence was buoyed by the successful bailout exits by a number of crisis-hit euro zone economies. While immediate risks to the euro zone have been contained, structural reforms to ensure fiscal sustainability and the clean-up of bank and corporate balance sheets are needed to avoid further flare-ups.

In China, there are concerns over shadow banking and rising local government debt. policymakers are taking active measures to contain growth in shadow banking and reform China’s banking system.

Despite market volatility in emerging markets, Asian banks have remained resilient, supported by healthy capital buffers and sound funding profiles. looking ahead, Asian banks face headwinds from Qe tapering, slower economic growth and declining asset quality - risks that may be amplified by the continued build-up of leverage in emerging Asia.

hEADlINE INFlATION DEClINED IN ThE G3

Global inflation remained benign in 2013. In the G3, headline inflation fell to 1.3% in 2013 from 1.9% in 2012. the uS and the euro zone faced mild disinflationary pressures stemming from lower energy costs and slack in capacity utilisation. However, Japan saw a significant rise in inflation in H2 2013, as higher prices of imported goods were

21Annual Report 2013/14

passed through to consumer prices. Meanwhile, inflation in Asia ex-Japan was unchanged at 3.9% in 2013. While supply-side constraints in India kept prices elevated and the rationalisation of fuel subsidies in some ASeAn-4 countries put upward pressure on inflation rates in the second half of 2013, these were offset by an easing of price pressures in the nIes due to subdued commodity prices.

In the first three months of 2014, global inflation remained subdued. While headline inflation increased slightly in the uS, a stronger euro held down import costs and contributed to much smaller price increases in the euro zone. price pressures in Asia ex-Japan eased somewhat, on account of lower food prices in India and China.

SINGAPOrE rECOrDED FASTEr GrOWTh

the domestic economy grew by 3.9% in 2013, following a modest outturn of 2.5% in the preceding year. notwithstanding intermittent bouts of volatility, economic activity in Singapore strengthened throughout the course of last year (see Chart 1).

this was largely on account of the pickup in trade-related activities. In particular, Singapore’s electronics production posted its first annual expansion after two consecutive years of contraction, on the back of a turnaround in the

anChor oF eConomiC anD FinanCial stability

global It cycle. Growth in the manufacturing sector, in turn, led to positive spillovers to the supporting wholesale trade, and transport and storage industries. At the same time, financial services staged a strong rebound amid positive investor sentiment and strong credit demand from the trade-related industries. Meanwhile, domestic demand remained resilient. notably, the construction sector recorded robust growth, boosted by a steady roll-out of commercial and residential projects.

nonetheless, growth momentum eased at the start of this year with the Singapore economy recording a sequential expansion of 2.3% q-o-q SAAR in Q1 2014, following a 6.9% increase in the preceding quarter. Despite the stellar outturn in the manufacturing sector, most of the trade-related industries saw some pullback in Q1 2014. In particular, Singapore’s re-exports to the uS and China contracted amid a slowdown in both economies early this year. Meanwhile, the sentiment-sensitive financial services segment experienced some headwinds as global financial markets retracted on a resurgence of jitters over possible risk events, such as a sharper-than-expected slowdown in China, and an escalation of conflict in ukraine. Concurrently, sectors dependent on domestic demand slowed, partly reflecting weaker private sector construction activities and softer demand for real estate business services.

Chart 1. Singapore’s real GDP Growth

YoY

QoQ SAARper

Cen

t

12

8

4

0

-4

2012Q1 Q2 Q3 Q4 Q2 Q3 Q4 2014Q12013Q1

22 Monetary Authority of Singapore

Chart 2. Contribution to CPI-All Items Inflation

For the rest of the year, gradual improvements in the external environment, together with a sustained recovery in the global It industry, should provide some support to Singapore’s external-oriented industries. Meanwhile, the domestic-oriented sectors are expected to remain resilient over the course of the year, buttressed by public infrastructure expansions in the construction, education and healthcare industries. nonetheless, while cyclical factors are broadly supportive of growth this year, the effects of the ongoing restructuring could dampen growth. this is because pressures from resource constraints continue to be binding, given slowing resident labour force growth and foreign worker inflows. Firms could also experience compressed profit margins in this transitional period, even as they undertake the necessary investments in capital, improve work processes and augment the skill sets of workers. on balance, the Singapore economy is projected to expand by 2–4% this year. COrE INFlATION rOSE IN h2 2013

Singapore’s labour market remained tight in 2013, with the overall unemployment rate falling to 1.9%, a 16-year low. this reflected strong labour demand from the domestic-oriented sectors alongside further foreign worker tightening measures. Consequently, resident wage growth rose from 2.3% in 2012 to 4.3% in 2013, which, together

with flat labour productivity, resulted in a build-up in business cost last year.

While the pass-through of domestic cost to consumer prices was muted in H1 2013, it picked up in H2. As a result, MAS Core Inflation, which excludes the cost of accommodation and private road transport, edged up in the latter part of the year. For the whole of 2013, MAS Core Inflation was 1.7% compared to 2.5% in 2012. Meanwhile, CpI-All Items inflation came in at 2.4% in 2013, lower than the 4.6% in the preceding year, due to softer housing rentals and a correction in Certificate of entitlement premiums following the introduction of motor vehicle loan restrictions in February 2013.

As the economy transits towards more sustainable, productivity-driven growth, the labour market will remain tight. Wage pressures will persist and firms are likely to continue passing on higher business cost to consumer prices. In comparison, price pressures from most of Singapore’s key import source countries should remain subdued. the impact from global commodity prices should also be relatively contained, given the supply buffers in most markets. nonetheless, there are risks from higher oil prices if geopolitical tensions in the Middle east escalate significantly. taking these factors into account, MAS Core Inflation is expected to stay elevated at 2–3% in 2014. CpI-All Items inflation would be lower, with modest contributions from

2012Q1 Q2 Q3 Q4 2013Q1 Q2 Q3 Q4 2014Q1-1

0

1

2

3

4

5

6

% P

oint

Con

trib

utio

n

CpI-All Items Inflation Services Food Accommodation others Car prices oil-Related

23Annual Report 2013/14

anChor oF eConomiC anD FinanCial stability

car prices and imputed rentals on owner-occupied accommodation.

MONETAry POlICy

economic activity in Singapore in 2013 saw sustained albeit uneven growth as the year progressed, underpinned by a mild recovery in the G3. the trade-related activities improved, while financial services rebounded on the back of robust lending. Domestic-driven sectors, such as construction and other services, were broadly resilient. overall job creation was strong, while the supply of labour was constrained by tighter foreign worker policies. Accordingly, the economy remained at full employment and wage pressures picked up.

Against this backdrop, MAS kept the slope of the S$ nominal effective exchange rate (S$neeR) policy band on a modest and gradual appreciation path in April and october 2013. Despite near-term uncertainties in the emerging economies, the Singapore economy is projected to grow at a moderate pace in 2014. the labour market will likely remain tight and MAS Core Inflation should stay elevated as firms pass on accumulated costs to consumer prices. MAS therefore maintained the policy stance in April 2014 to keep inflationary pressures contained.

Monetary policy in Singapore is formulated with the objective of promoting price stability over the medium term as the basis for sustainable economic growth. Chart 3 traces the evolution of monetary policy against the backdrop of changes in key macroeconomic variables. MAS has maintained a modest and gradual appreciation path for the S$neeR policy band since April 2010, which has restrained but not fully offset temporary inflationary pressures from economic restructuring.

MANAGEMENT OF lIQuIDITy

ENhANCING SINGAPOrE DOllAr lIQuIDITy MANAGEMENT FrAMEWOrK

In 2013, MAS continued to enhance our liquidity management framework, to improve our ability

to provide Singapore dollar (SGD) liquidity and to meet the demand for high quality liquid assets by banks operating in Singapore.

BOJ Cross-border Collateral ArrangementMAS has been entering into cross-border collateral arrangements (CBCAs) with foreign central banks since 2009 to strengthen our ability to provide banks in Singapore with SGD liquidity against safe and liquid foreign currency and foreign currency-denominated collateral. In July 2013, MAS added the Bank of Japan (BoJ) to the list of CBCAs established with foreign central banks. the arrangement with BoJ allows banks in Singapore to pledge Japanese government securities at the Standing Facility to obtain SGD liquidity. this collaboration reinforces the commitment of BoJ and MAS to support the long-standing economic and financial relationship between Japan and Singapore, and brings the total number of CBCAs established by MAS to eight.

Introduction of 24-week MAS Billsto continue to meet the banking system’s demand for high quality liquid assets and further deepen domestic money markets, MAS has stepped up the issuance of MAS Bills, which have replaced 3- and 6-month t-Bills. to further develop the capacity of the MAS Bill market, MAS also extended the maturity of MAS Bills to include the 24-week tenor in January 2014. At the end of FY2013, about S$74.4 billion in outstanding MAS Bills was available to financial institutions, including S$12.8 billion of 24-week MAS Bills.

ENhANCING MAS rENMINBI FACIlITy

In March 2013, MAS renewed and enhanced the bilateral currency swap arrangement with the people’s Bank of China. under this arrangement, up to RMB 300 billion is available to eligible financial institutions in Singapore for trade and market stability purposes. In July 2013, MAS enhanced the MAS Renminbi (RMB) Facility to provide RMB liquidity in tenors of one week and one month for market stability purposes, in addition to the existing 3-month tenor for trade and direct investment into China. the pool of eligible collateral was also expanded from SGD cash to include Singapore Government Securities (SGS) and MAS Bills.

& Wi

24 Monetary Authority of Singapore

Chart 3. Key Macroeconomic variables and the Monetary Policy Stance

Wide

25Annual Report 2013/14

116

112

108

104

100

96

6

4

2

0

6

5

4

3

2

1

0

20

16

12

8

4

02010 2011 2012 2013 2014Q1

Inde

x (Q

1 20

10=1

00)

% o

f Pot

entia

l GD

P%

yO

y%

yO

y

2014Q1:4.9%

2014Q1:2.0%

1.0%

real GDP Growth

Output Gap

CPI-All Items Inflation

MAS Core Inflation

S$NEEr

neutralpolicy

Re-centre

ReduceSlope

Shift to Modest & Gradual

Appreciation & Re-centre

Increase Slope Slightly & Widen Band

Increase Slope Slightly & Restore narrower

Band

Maintain

Modest & Gradual Appreciation

MANAGEMENT OF OFFICIAl FOrEIGN rESErvES

As at 31 March 2014, MAS held S$343 billion (uS$273 billion) of official foreign reserves (oFR) on its balance sheet. MAS invests the oFR conservatively, ensuring sufficient liquidity to support the conduct of monetary policy while preserving the international purchasing power of the reserves.

Accounting Policy the oFR constitute more than 90% of the assets on MAS’ balance sheet. they are accounted for on a lower of cost and market valuation basis in MAS’ financial statements. the key components of the investment gain from the oFR are interest income from cash and bonds, dividends from equity holdings and realised capital gains/losses arising from sale of the oFR assets. the investment gain also comprises write-back of, or provision for, diminution in the value of the oFR assets. When the market value of oFR assets falls below cost, a provision is made against investment gain. Should the market value subsequently recover, the provision is written back as investment gain, by up to the amount of value recovered.

Asset and Currency Allocation the oFR are invested in a well-diversified portfolio including cash, bonds and equities. Investment-grade bonds comprise the largest allocation in the portfolio. With regard to currency composition, about three-quarters of the oFR are denominated in the major G4 currencies i.e. uS Dollar, euro, British pound and Japanese Yen, with no single currency allocation making up more than one-third of the composition.

risk Management MAS monitors investment risks in the oFR closely. Besides establishing risk controls and limits to manage financial and liquidity risks, MAS conducts regular stress tests to ensure its portfolio can weather the impact of potential tail risk events and would consider appropriate actions to mitigate risk where necessary.

Currency Translation EffectsMAS’ financial results are reported in Singapore Dollars. the reported value of the oFR hence depends on the movements of the Singapore Dollar vis-à-vis the foreign currencies in which the reserves are held. Such currency movements will result in translation effects in MAS’ financial statements.

the translation effects in MAS’ financial statements have no impact on the international purchasing power of the oFR, and hence do not have bearing on MAS’ ability to conduct exchange rate policy and provide a buffer in the event of a sharp deterioration in Singapore’s balance of payments. Accordingly, it would not be meaningful to hedge against the Singapore Dollar to mitigate translation effects.

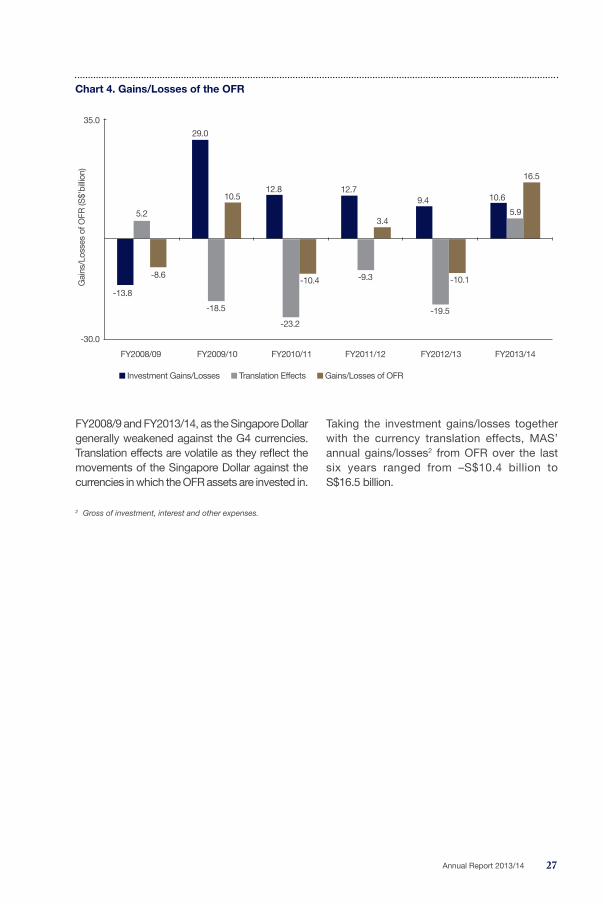

Investment PerformanceChart 4 shows the investment performance of the oFR in MAS’ income statement over the period comprising the global financial crisis and the recovery since the crisis. the gains/losses of oFR, as represented by the dark yellow bars in Chart 4, comprise two separate components – investment gains/losses (blue bars) and currency translation effects (grey bars). Holding the Singapore Dollar exchange rate constant to strip out translation effects, the oFR recorded an investment loss of S$13.8 billion in FY2008/09 as a result of the global financial crisis. As market prices fell across all asset classes, significant valuation provisions were made. In FY2009/10, as markets gradually recovered, the oFR posted an investment gain of S$29.0 billion due primarily to the write-back of valuation provisions. the yearly investment gain from FY2010/11 to FY2013/14 was relatively stable at between S$9.4 billion and S$12.8 billion, mainly from interest income and realised capital gains/losses from sale of oFR assets.

As MAS’ financial results are reported in Singapore Dollars, MAS recorded a negative translation effect as the Singapore Dollar strengthened between 15% and 26% against the G4 currencies from FY2009/10 to FY2012/13. However, there were positive translation effects1 in

anChor oF eConomiC anD FinanCial stability

1 The translation effect in MAS’ financial statements is dependent on the exchange movements of the Singapore Dollar vis-à-vis the

currencies in which the OFR assets are invested in, which are primarily denominated in the G4 currencies. However, MAS’ monetary

policy is centred on the management of the Singapore Dollar against a basket of currencies of our major trading partners.

26 Monetary Authority of Singapore

Chart 4. Gains/losses of the OFr

-30.0

FY2008/09

Investment Gains/losses translation effects Gains/losses of oFR

FY2009/10 FY2010/11 FY2011/12 FY2012/13 FY2013/14

Gai

ns/l

osse

s of

oFR

(S$’

billi

on)

35.0

-13.8

-8.6

29.0

10.512.8 12.7

9.4

-19.5

-10.1

10.6

5.9

16.5

3.4

-9.3

-23.2

-10.4

-18.5

5.2

FY2008/9 and FY2013/14, as the Singapore Dollar generally weakened against the G4 currencies. translation effects are volatile as they reflect the movements of the Singapore Dollar against the currencies in which the oFR assets are invested in.

2 Gross of investment, interest and other expenses.

taking the investment gains/losses together with the currency translation effects, MAS’ annual gains/losses2 from oFR over the last six years ranged from –S$10.4 billion to S$16.5 billion.

27Annual Report 2013/14

ROBUST, TRUSTeD, and PURPOSeFUL FINANCIAL CeNTRe

robust, trusteD, anD puRpoSeFul FInAnCIAl CentRe

A rOBuST FINANCIAl CENTrE

OvErAll

Industry-Wide Stress TestsMAS conducts industry-wide stress tests of financial institutions in Singapore annually. In 2013, financial institutions were stress tested on two adverse scenarios – a V-shaped recession where GDp declines sharply in the first year and recovers thereafter, and a protracted recession where GDp declines over three years. Both scenarios entail large declines in domestic and regional economic activity. the stress tests showed that banks and insurers are resilient to adverse macroeconomic scenarios. the International Monetary Fund’s Financial Sector Assessment programme in 2013 also assessed that Singapore’s financial system is resilient to the domestic and global risks it is exposed to.

Industry-Wide Business Continuity ManagementMAS published an information paper in December 2013, providing a comprehensive overview of the Business Continuity Management landscape in the financial industry. Drawing on the results from an extensive survey of the industry, the information paper shared good practices as well as opportunities for improvement in various areas, such as business resiliency and crisis management.

Financial District Security ProgrammeIn 2013, the Financial District Security programme (FDSp) was restructured to engage and strengthen partnership with the industry on physical security, contingency planning and business continuity management issues. the FDSp now has more

financial institutions represented on its Steering Committee and senior representatives from financial institutions (such as Chief operating officers or equivalent) as Steering Committee members.

Enhancing Technology risk ManagementMAS issued the technology Risk Management Guidelines and notice to financial institutions in June 2013. the Guidelines set out MAS’ minimum expectations of financial institutions’ technology risk governance and security practices to address existing and emerging technology risks within the financial industry.

the notice allows specific penalties to be imposed on financial institutions that fail to maintain a high level of reliability, availability and recoverability of their critical It systems, or do not implement strong It controls to protect customer information from unauthorised access or disclosure.

BANKING

Strengthening resilienceMAS implemented fully the Basel III capital standards for Singapore-incorporated banks with effect from 1 January 2013. MAS requires Singapore-incorporated banks to meet capital adequacy standards that are higher than the Basel capital standards. For Common equity tier 1 capital, Singapore-incorporated banks will be required to maintain a ratio of at least 9% by 1 January 2015 (inclusive of a capital conservation buffer requirement of 2.5%) compared to the Basel III requirement of 7%. MAS also implemented in 2013 the other Basel III capital reforms to improve the quality of capital, enhance risk coverage and begin monitoring the leverage ratio.

30 Monetary Authority of Singapore

effective 1 January 2014, MAS also implemented the disclosure and submission requirements set out in the Basel Committee on Banking Supervision (BCBS)’s framework for assessing global systemically important banks (G-SIBs). this will facilitate assessment of the systemic importance of Singapore-incorporated banks based on the BCBS’ G-SIB assessment methodology.

Mortgage loans underwriting StandardsMAS conducted a thematic inspection of the residential property loans business of major banks in late 2012. the thematic inspection revealed that the banks have put in place adequate policies and procedures to assess the credit worthiness and repayment capability of their borrowers. the inspection also found that the overall non-performing loan ratio across the major banks was low. In addition, the banks have also been subjecting their residential property portfolios to regular monitoring and reviews, as well as stress testing to ensure that any vulnerabilities or deterioration in asset quality is promptly detected and addressed.

nonetheless, there were variations in the methodologies and practices used by banks to compute the debt servicing ratio and determine the loan approval thresholds. to strengthen and standardise credit underwriting practices among banks, MAS issued the notice on Computation of total Debt Servicing Ratio (tDSR) for property loans and refined the existing housing loan rules for banks in June 2013.

Macroprudential PoliciesMAS introduced a tDSR framework in June 2013 to strengthen the credit underwriting practices of financial institutions and encourage financial prudence among borrowers. the tDSR has to be computed for individual borrowers obtaining a property loan from a financial institution and should generally not exceed 60%.

to instil greater financial prudence among borrowers, MAS also lowered the maximum tenure of new loans granted by financial institutions for the purchase of HDB flats from 35 years to 30 years in August 2013. loans with tenures that exceed 25 years or whose loan periods extend beyond the borrower’s age of 65 are subject to tighter loan-to-value limits. In addition, MAS introduced

a mortgage servicing ratio of 30% on loans for the purchase of executive condominium units bought directly from property developers in December 2013.

SECurITIES

review of Market Structure and Practices In February 2014, MAS and Singapore exchange (SGX) published a consultation paper on a review of the securities market structure and practices. the consultation paper follows an extensive review by MAS and SGX, and sets out broad policy proposals that are aimed at strengthening the securities market in Singapore. the review concluded that the securities market remains sound but identified three key areas for possible enhancements:

• promoting orderly trading and responsible investing;

• Improving the transparency of market intervention measures; and

• Strengthening the process for admitting new listings and enforcing against listing rule breaches.

Key proposals in the consultation paper include:

• Introducing a minimum trading price for issuers listed on the SGX Mainboard to address risks of high volatility generally associated with low-priced securities, which in turn make them more susceptible to excessive speculation and potential market manipulation;

• Requiring securities intermediaries to impose minimum collateral for securities trading based on customers’ open positions;

• Introducing short position reporting requirements to enhance transparency;

• Requiring trading restrictions by securities intermediaries to be announced through the SGX website to ensure fair and transparent dissemination of such information; and

• Strengthening SGX’s process for admitting new listings and enforcing against listing rule breaches by setting up an independent listings Advisory Committee, listings Disciplinary Committee and

listings Appeals Committee.

31Annual Report 2013/14

MAS and SGX will consider carefully all feedback received during the 12-week consultation period, and will further engage key stakeholders and the public before we implement any of the proposals.

OTC Derivatives reforms MAS remains fully committed to meeting the G20 objective to strengthen regulation of over-the-counter (otC) derivatives. In line with G20 and Financial Stability Board (FSB) recommendations to strengthen regulation of the global otC derivatives markets, MAS has been implementing reforms in domestic otC derivatives steadily over the past year.

the regulatory regimes for otC derivatives clearing facilities and trade repositories commenced in August 2013. Following the introduction of the regulatory regime for trade repositories, DtCC Data Repository (Singapore) pte ltd (DDRS) set up the first local trade repository and was approved by MAS as a licensed trade repository in Singapore in november 2013. DDRS enables reporting of otC derivative trades and is an important financial market infrastructure in enhancing transparency and regulatory oversight of the otC derivatives market in Singapore.

the Securities and Futures Act (SFA) amendments to allow MAS to mandate central clearing came into effect in november 2012. MAS is currently drafting regulations on mandatory central clearing. In line with the G20’s recommendation of implementing a trading mandate where appropriate, MAS is studying the implications of implementing a trading mandate in Singapore. We participated actively in discussions at various international fora, such as the FSB, the International organisation of Securities Commissions (IoSCo) and the Committee on payment and Settlement Systems (CpSS). MAS also chairs the IoSCo Working Group on Risk Mitigation Standards for non-Centrally Cleared Derivatives, which is developing standards on risk mitigation techniques for uncleared otC derivative transactions.

At the bilateral level, MAS has continued to engage in constructive discussions with foreign regulators, such as the uS Commodity Futures trading Commission (CFtC), the european Commission

(eC) and the european Securities and Markets Authority (eSMA), on substituted compliance or equivalence assessments of our otC derivatives regulatory regime.

Singapore exchange Derivatives Clearing limited (SGX-DC) is the first Asian-based central clearing counterparty (CCp) to be registered by CFtC as a derivatives clearing organisation (DCo). With effect from 31 December 2013, SGX-DC, as a DCo, is able to clear swaps for uS persons. In connection with the DCo registration, MAS signed a supervisory Memorandum of understanding with CFtC in December 2013.

eSMA has also assessed and recommended to the eC that our clearing house and trade repository regulatory regimes are broadly equivalent to the european regime. MAS continues to engage the eC to finalise the outcome of the assessment.

MAS views these assessments as important measures to avoid the application of potentially duplicative or conflicting rules on entities with cross-border operations. Recognition of regulatory frameworks across jurisdictions through substituted compliance or equivalence assessments will enable entities to comply with the set of rules applied by the jurisdictions in which they operate, and avoid market fragmentation.

Electronic lodgement of Prospectuses and OffersMAS has enhanced the offers and prospectuses electronic Repository and Access (opeRA) platform. Since January 2014, lodgements of prospectuses for offers of shares, debentures, and units in business trusts can be made electronically through opeRA. physical attendance at MAS is no longer required. electronic lodgement of applications for the authorisation or recognition of collective investment schemes (CIS) and their offer documents will be made available in the second half of 2014.

Enforcement Actions2013 was an eventful year for MAS’ enforcement efforts. We obtained a default judgment for S$100,000 against an individual for contravening the provision against false trading in part XII of the SFA in october 2013. We also commenced

robust, trusteD, anD PurPoseFul FinanCial Centre

32 Monetary Authority of Singapore

3 With the exception of marine mutual insurers, captives and Lloyds’ insurers.

two further court actions, seeking civil penalties of up to S$150,000 against two individuals for unauthorised trading and about S$2.5 million against another individual for insider trading.

Besides taking court action, MAS entered into settlement agreements with five separate individuals in 2013. these individuals admitted to contravening a range of provisions in part XII of the SFA and paid a civil penalty of S$50,000 to S$150,000 without court action. one of these individuals, a director of a listed company, also undertook not to be a company director for a period of one year.

Separately, in november 2013, MAS successfully obtained an injunction on a bank account belonging to the former Chief executive officer (Ceo) of a listed company in Singapore. the High Court allowed MAS’ application to freeze uS$3.7 million in the bank account, pending the outcome of on-going investigations into possible breaches of the SFA. this is MAS’ first application for a freezing order on a bank account, pursuant to its powers under the SFA.

Between April 2013 and March 2014, MAS also published a total of 43 formal regulatory and enforcement actions against companies and individuals for market conduct breaches. these actions included reprimands, composition fines, civil penalties and prohibition orders. over this period, MAS took other regulatory and administrative actions in another 159 cases.

INSurANCE

Enhanced Macroprudential Framework In 2011, MAS carried out a pilot study based on a group of larger insurers to establish a macroprudential surveillance framework for insurers. Since then, MAS has collected more granular data on all insurers’3 assets and liability exposures on a regular basis through MAS notice 122. this allowed MAS to extend the macroprudential surveillance framework to the entire insurance industry and conduct more comprehensive analysis of the insurance sector’s vulnerabilities, as well as the interconnectedness and linkages with the economy, financial markets and other financial intermediaries.

risk Based Capital FrameworkMAS is reviewing its Risk Based Capital Framework (RBC 2) for insurers to keep pace with evolving market practices and global regulatory developments. the review aims to improve the comprehensiveness of risk coverage and the risk sensitivity of the framework, as well as define more clearly MAS’ supervisory approach with respect to the solvency intervention levels. the review has taken into account the practices of major jurisdictions as well as the risk profile of the Singapore insurance sector.

MAS issued its second consultation paper in March 2014, following the first consultation that set out the broad direction of the RBC 2 review about two years ago. the latest consultation paper revisited several earlier proposals, taking into consideration responses received for the first consultation paper. the consultation paper also contained technical specifications of a first quantitative impact study (QIS 1) to be conducted by the insurers, in order for insurers to understand the full impact of the proposals. the key proposals include:

• Introduction of a matching adjustment to the discount rate for life insurers;

• Recalibration of the risk requirements to a consistent target criterion i.e. Value at Risk (VaR) measure of 99.5% confidence level over a one year period;

• Recognition of diversification benefits between the insurance and asset risk requirements, as well as between some of the underlying risk requirements within these two categories of risk requirements; and

• Alignment of insurers’ available capital components with those in MAS’ capital adequacy framework for banks, wherever appropriate.

MAS expects to finalise the main features of the RBC 2 framework by 2014 and formally implement the RBC 2 requirements from 1 January 2017, subject to further consultation with the industry. MAS will continue to engage the industry closely on the review, especially on the implementation timeline and the transitional provisions.

33Annual Report 2013/14

requirements on Key PersonsMAS amended the Insurance (Actuaries) Regulations (Actuaries Regulations) in April 2013 to expand the responsibilities of actuaries approved by MAS. Specifically, certain existing responsibilities of actuaries of direct life insurers were extended to actuaries of other types of insurers. these include the requirement to assist the insurer on matters such as investment policy and risk management, as well as to report to MAS and notify the insurer’s board of directors if the insurer has failed to take appropriate steps to rectify any matter that has a material adverse effect on the insurer’s financial condition. the amended Actuaries Regulations also provide for the actuaries to have free and unfettered access to the insurer’s board of directors.

At the same time, a new MAS notice 106 on Appointment of Directors, Chairman and Key executive persons was issued. the new notice clarifies that insurers should ensure that approved persons meet the board of directors’ approved fit and proper policy not only at the time of appointment but also on a continuing basis.

robust, trusteD, anD PurPoseFul FinanCial Centre

INTErNATIONAl SuPErvISOry COOPErATION

Promoting Consolidated Supervision and Cooperation with Foreign regulators MAS continues to participate in supervisory college meetings of international and regional banks as host supervisor. this allows MAS to cooperate more closely with the home supervisors of foreign banks and strengthen our understanding of developments in other parts of the group that may have an impact on the Singapore operations. MAS also hosted supervisory college meetings for the three Singapore banking groups, involving supervisors in the region where the banks have sizeable operations. these meetings provided a forum for MAS and host supervisors of these institutions to exchange views and assessments of the institutions’ cross-border activities.

Crisis Management Group Meetings MAS is a member of the Crisis Management Group (CMG) of six of the G-SIBs that have significant operations in Singapore and participates in their

BOx 1: international monetary Fund’s Financial sector assessment Programme

As one of 29 systemically-important financial centres in the world, Singapore underwent the International Monetary Fund’s (IMF) Financial Sector Assessment programme (FSAp) in 2013. the FSAp is an in-depth external assessment of the stability and resilience of a country’s financial sector.

the FSAp findings were published by the IMF in november 2013. they affirmed Singapore’s standing as a sound and stable financial centre. the assessment found that Singapore maintained a very high level of compliance with international standards

for the regulation and supervision of the banking, insurance and securities sectors, and financial market infrastructures. Stress tests conducted as part of the assessment indicated that banks and insurers were resilient to adverse macroeconomic scenarios. Crisis management and resolution arrangements were also generally strong, with the necessary framework in place for crisis information sharing and coordination.

MAS has been reviewing the IMF’s recommendations and will take appropriate measures where needed.

34 Monetary Authority of Singapore

CMG meetings. the meetings facilitate information exchanges between home and host supervisors and the establishment of institution-specific cross-border cooperation agreements to support recovery and resolution planning. this enhances preparedness and cross-border coordination for crisis management, including recovery and resolution planning, for these institutions.

Alternative Investment Fund Managers Directive MAS entered into an Mou with the authorities of 27 european union or european economic Area countries on 22 July 2013. this provides a formal basis for supervisory cooperation between MAS and the european authorities for the regulation and supervision of alternative investment funds (AIFs), managers of AIFs and depositaries of AIFs. the Mou paves the way for enhanced sharing of information and mutual assistance between MAS and the european authorities for more effective supervision of AIFs’ managers that operate on a cross-border basis.

A TruSTED FINANCIAl CENTrE

FINANCIAl BENChMArKS

Following the completion of MAS’ supervisory review in June 2013, the Association of Banks in Singapore and the Singapore Foreign exchange Markets Committee announced new measures to strengthen the governance and design of benchmark rates setting processes for key financial benchmarks in Singapore. Benchmarks which were not widely used were discontinued. SGD SoR and several FX benchmarks were transitioned from a poll-based methodology to a traded methodology that uses price data from actual market transactions, while the governance of SGD SIBoR submission processes was strengthened at each submitter bank and at the administrator in line with a set of industry guidelines on benchmark rate setting. In line with international regulatory developments on financial benchmarks, MAS proposed a new regulatory framework in June 2013 with two key thrusts:

• Introduction of criminal sanctions for the manipulation of any financial benchmarks under the SFA; and

• Regulation of the setting of key financial benchmarks set in Singapore.

MAS has consulted the public on its policy recommendations and plans to table the proposed legislative amendments to the SFA in parliament in the first half of 2015. If passed by parliament, MAS will have powers under the SFA to designate key benchmarks based on considerations such as systemic importance of the benchmark, and an assessment of its susceptibility to manipulation. Administrators and submitters of designated benchmarks will be regulated by MAS. In formulating the regulatory framework, MAS took reference from the work of the IoSCo principles for Financial Benchmarks published in July 2013, which MAS helped to develop. these principles were endorsed by the FSB as the roadmap for benchmarks reform. they seek to enhance the integrity and reliability of benchmarks by providing guidelines to benchmark administrators on areas such as governance, methodology and accountability. MAS also contributed to international reform efforts as a member of the IoSCo Review team that conducted an assessment of the degree of implementation of the IoSCo principles by the administrators of the most widely used global interest rate benchmarks (lIBoR, euRIBoR and tIBoR). In addition, MAS was a member of the FSB official Sector Steering Group (oSSG). Apart from providing oversight of the IoSCo review, the oSSG worked to encourage private sector participants to identify alternative benchmarks.

PrEvENTING MONEy lAuNDErING AND TErrOrISM FINANCING

As an international financial centre and transport hub, Singapore supports global efforts to combat money laundering (Ml), terrorism financing (tF) and proliferation financing. Singapore is a member of the Financial Action task Force (FAtF) and a founding member of the Asia pacific Group on Money laundering, and is committed to implementing a robust regulatory and supervisory regime in line with the revised FAtF Standards and international best practices.

35Annual Report 2013/14

robust, trusteD, anD PurPoseFul FinanCial Centre

on 10 January 2014, Ministry of Home Affairs, Ministry of Finance (MoF) and MAS published Singapore’s first national Risk Assessment (nRA) report on Ml/tF. the nRA report was the culmination of a government-wide exercise that lasted two years and covered 14 financial sub-sectors4 and eight non-financial sectors5 in Singapore. Most of these sectors were found to have a robust regime in place to combat Ml/tF. nonetheless, there are a number of areas where controls need to be strengthened. In the financial sector, MAS is focusing on strengthening the supervisory framework for remittance agents, money-changers and internet-based stored value facility holders. Virtual currencies have also been identified as an emerging risk in the financial sector for further study and, in March 2014, MAS announced that it will be putting in place a new regime to address Ml/tF risks in the area.

Financial institutions operating in Singapore are required to put in place the necessary controls to detect and deter the flow of illicit funds through Singapore’s financial system. Such controls include the need to identify and know their customers (including beneficial owners), to conduct regular account reviews, and to monitor and report any suspicious transactions. Singapore is also committed to implementing the various united nations Security Council Resolutions against countries such as Iran and north Korea. the MAS notices and Guidelines relating to the prevention of Ml/tF will be updated in the second half of 2014 following a consultation with the industry.

In 2013, MAS conducted 83 anti-money laundering and countering the financing of terrorism (AMl/CFt) inspections covering banks, insurance companies, money-changers, remittance agents, capital markets services licensees and licensed trust companies. Arising from the inspections, MAS noted several areas where there was room for improvement. Some institutions needed to put in place more robust AMl/CFt controls for their trade finance and correspondent banking businesses,

while others had to strengthen customer due diligence measures for higher risk clients, clear backlog of suspicious transaction alerts in a more timely manner, as well as enhance transaction monitoring reports in line with changing business and/or customer profiles. MAS had required the affected institutions to promptly address all deficiencies and take steps to strengthen their controls and risk management framework.

MAS continues to take a serious view of breaches of AMl/CFt regulations and failure by FIs to institute a robust AMl/CFt control framework. Sanctions are imposed on institutions for regulatory contraventions and deficiencies in AMl/CFt measures. these include formal warnings, reprimands, restrictions on operations, financial penalties and revocation of licences. In 2013, MAS issued a total of nine warnings and reprimands to financial institutions, restricted the operations of or imposed special conditions on six institutions, and revoked or did not renew the licences of two money-changers/remittance agents. In the past year, MAS has also imposed financial penalties on five institutions, ranging from approximately S$12,000 to S$450,000. ENhANCING ExChANGE OF INFOrMATION ON TAx

Singapore has significantly strengthened its channels for international cooperation to combat cross-border tax fraud and tax evasion. on 14 May 2013, MAS, MoF and Inland Revenue Authority of Singapore announced four measures to further enhance the exchange of Information (eoI) framework:

• extension of eoI assistance on tax in accordance with the international eoI-on-request Standard;

• Signing of the Multilateral Convention on Mutual Administrative Assistance in tax Matters;

• Removal of the court order requirement to obtain bank and trust information; and

4 The 14 financial sub-sectors are: (i) full banks and qualifying full banks, (ii) wholesale banks, offshore banks and merchant banks, (iii)

finance companies, (iv) money-changers, (v) remittance agents, (vi) direct life and composite insurers, (vii) other insurers, (viii) insurance

brokers, (ix) fund management companies (x) trust companies, (xi) broker-dealers, (xii) corporate finance advisory firms, (xiii) financial

advisory firms, and (xiv) stored value facility holders.

5 The eight non-financial sectors covered are: (i) casinos, (ii) pawnbrokers, (iii) moneylenders, (iv) corporate service providers, (v) real estate

sector, (vi) lawyers, (vii) public accountants and other professional accountants, and (viii) non-profit organisations.