monetary policy challenges under tighter external ... · 2. 11/07/2018 2 current ... reducing the...

TRANSCRIPT

11/07/2018

1

Monetary Policy Challenges under Tighter External Financial Conditions

FLAR‐CAF XIII Annual Conference

Juan José EchavarríaGovernor

1

Policy challenges

• External Risks and Policy Challenges – First line of defense: Exchange rate flexibility but there are preconditions

• Limited currency mismatches

• A credible monetary regime

• Sound and robust financial sector

• Sound fiscal policy

– Second line of defense: External buffers

• Other Policy Challenges– Higher participation of foreign investors in local public debt market poses

other policy challenges.

– Higher debt2

11/07/2018

2

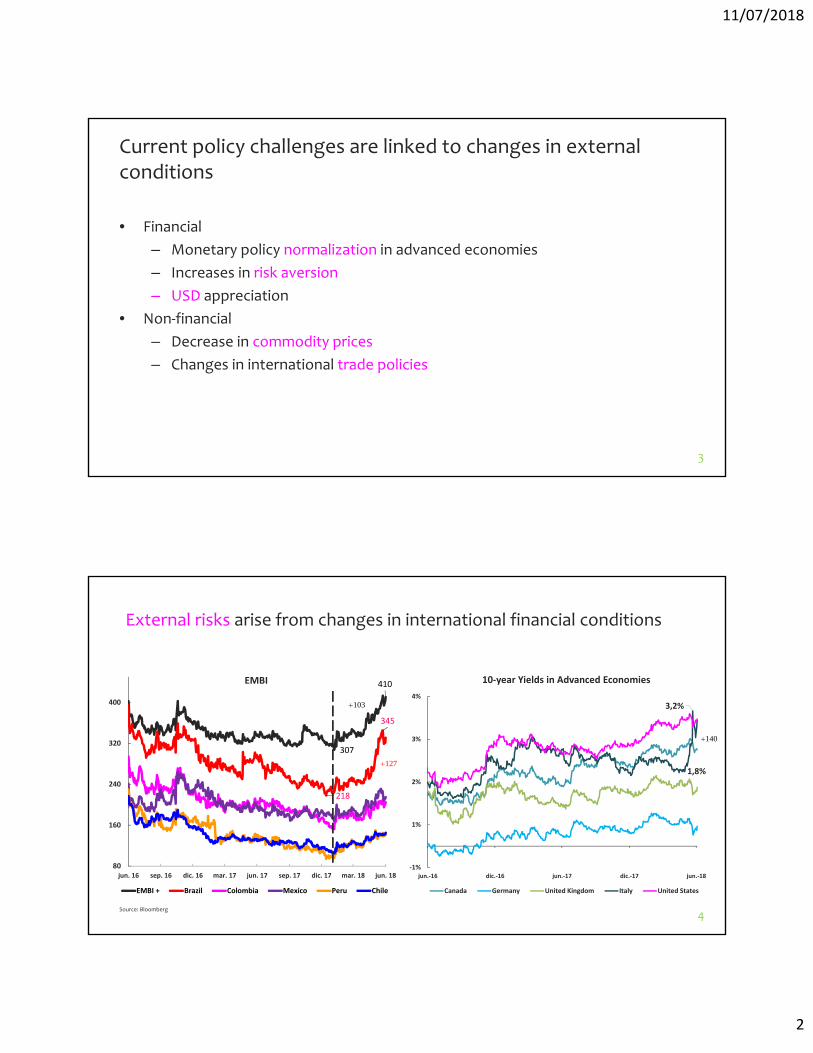

Current policy challenges are linked to changes in external conditions

• Financial

– Monetary policy normalization in advanced economies

– Increases in risk aversion

– USD appreciation

• Non‐financial

– Decrease in commodity prices

– Changes in international trade policies

3

External risks arise from changes in international financial conditions

Source: Bloomberg

4

1,8%

3,2%

‐1%

1%

2%

3%

4%

jun.‐16 dic.‐16 jun.‐17 dic.‐17 jun.‐18

10‐year Yields in Advanced Economies

Canada Germany United Kingdom Italy United States

307

410

218

345

80

160

240

320

400

jun. 16 sep. 16 dic. 16 mar. 17 jun. 17 sep. 17 dic. 17 mar. 18 jun. 18

EMBI + Brazil Colombia Mexico Peru Chile

EMBI

103

127

140

11/07/2018

3

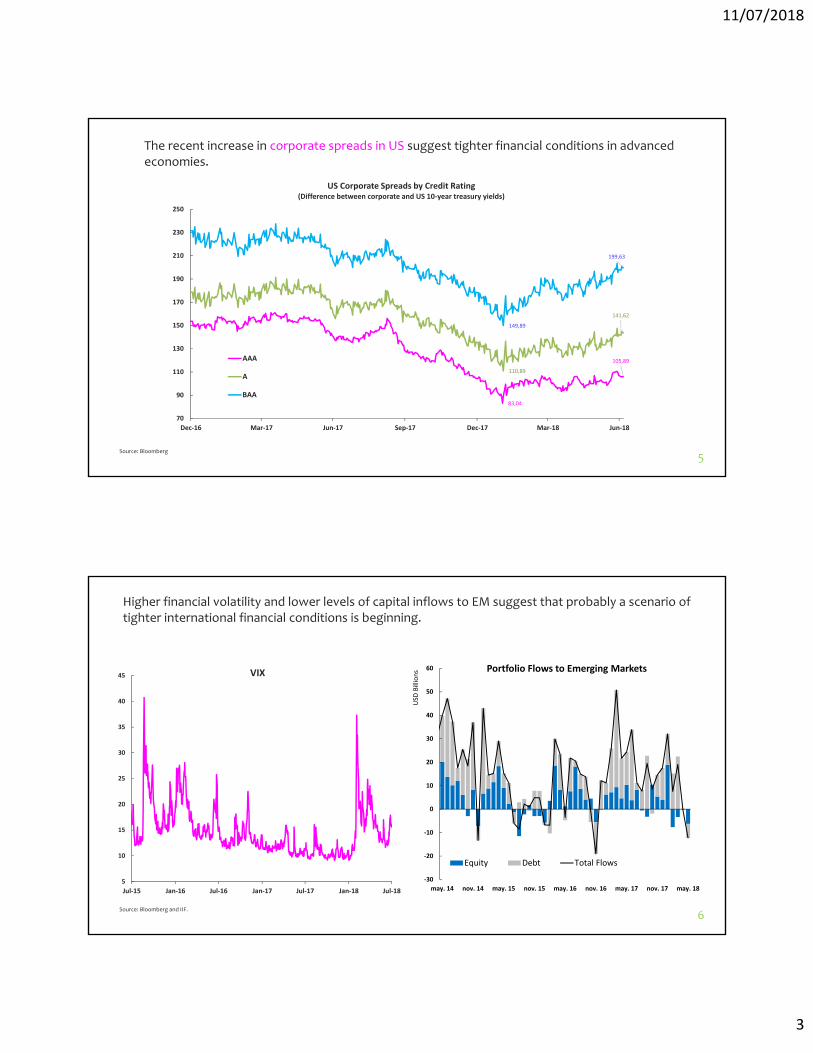

The recent increase in corporate spreads in US suggest tighter financial conditions in advanced economies.

Source: Bloomberg

5

83,04

105,89

110,89

141,62

149,89

199,63

70

90

110

130

150

170

190

210

230

250

Dec‐16 Mar‐17 Jun‐17 Sep‐17 Dec‐17 Mar‐18 Jun‐18

US Corporate Spreads by Credit Rating(Difference between corporate and US 10‐year treasury yields)

AAA

A

BAA

Source: Bloomberg and IIF.

6

5

10

15

20

25

30

35

40

45

Jul‐15 Jan‐16 Jul‐16 Jan‐17 Jul‐17 Jan‐18 Jul‐18

VIX

‐30

‐20

‐10

0

10

20

30

40

50

60

may. 14 nov. 14 may. 15 nov. 15 may. 16 nov. 16 may. 17 nov. 17 may. 18

Portfolio Flows to Emerging Markets

Equity Debt Total Flows

USD

Billions

Higher financial volatility and lower levels of capital inflows to EM suggest that probably a scenario of tighter international financial conditions is beginning.

11/07/2018

4

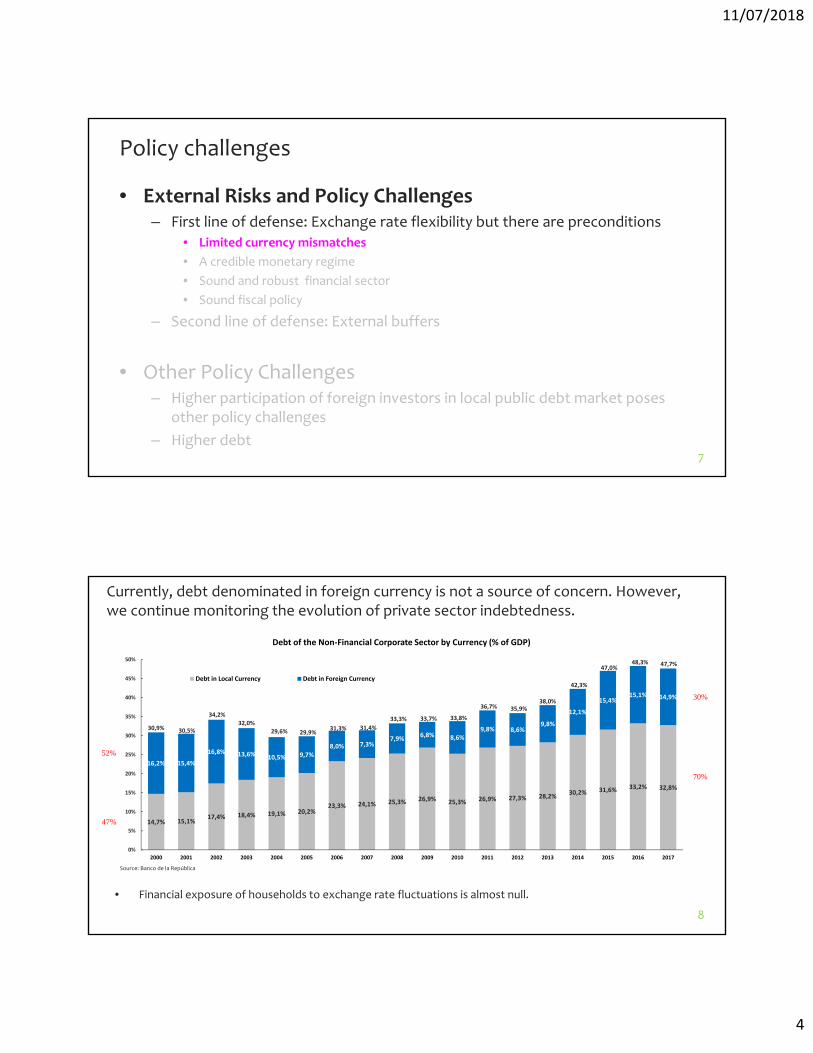

Policy challenges

• External Risks and Policy Challenges – First line of defense: Exchange rate flexibility but there are preconditions

• Limited currency mismatches

• A credible monetary regime

• Sound and robust financial sector

• Sound fiscal policy

– Second line of defense: External buffers

• Other Policy Challenges– Higher participation of foreign investors in local public debt market poses

other policy challenges

– Higher debt7

• Financial exposure of households to exchange rate fluctuations is almost null.

Source: Banco de la República

8

Currently, debt denominated in foreign currency is not a source of concern. However, we continue monitoring the evolution of private sector indebtedness.

14,7% 15,1%17,4% 18,4% 19,1% 20,2%

23,3% 24,1% 25,3% 26,9% 25,3% 26,9% 27,3% 28,2%30,2% 31,6% 33,2% 32,8%

16,2% 15,4%

16,8% 13,6% 10,5% 9,7%8,0% 7,3%

7,9%6,8% 8,6%

9,8% 8,6%9,8%

12,1%

15,4%15,1% 14,9%

30,9% 30,5%

34,2%

32,0%

29,6% 29,9%31,3% 31,4%

33,3% 33,7% 33,8%

36,7% 35,9%38,0%

42,3%

47,0%48,3% 47,7%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Debt of the Non‐Financial Corporate Sector by Currency (% of GDP)

Debt in Local Currency Debt in Foreign Currency

Source: Banco de la República

30%

70%

47%

52%

11/07/2018

5

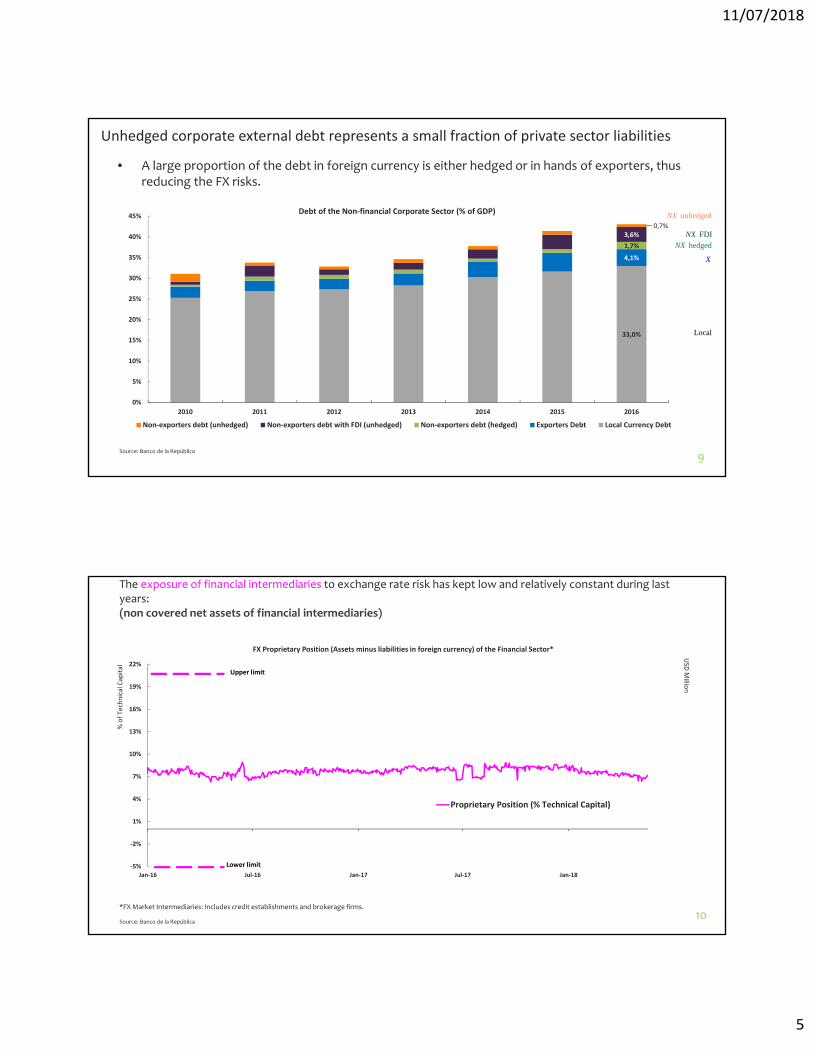

• A large proportion of the debt in foreign currency is either hedged or in hands of exporters, thus reducing the FX risks.

Source: Banco de la República

9

Unhedged corporate external debt represents a small fraction of private sector liabilities

33,0%

4,1%

1,7%

3,6%0,7%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2010 2011 2012 2013 2014 2015 2016

Debt of the Non‐financial Corporate Sector (% of GDP)

Non‐exporters debt (unhedged) Non‐exporters debt with FDI (unhedged) Non‐exporters debt (hedged) Exporters Debt Local Currency Debt

Local

X

hedgedNX FDINX

unhedgedNX

The exposure of financial intermediaries to exchange rate risk has kept low and relatively constant during last years: (non covered net assets of financial intermediaries)

*FX Market Intermediaries: Includes credit establishments and brokerage firms.

10Source: Banco de la República

‐5%

‐2%

1%

4%

7%

10%

13%

16%

19%

22%

Jan‐16 Jul‐16 Jan‐17 Jul‐17 Jan‐18

FX Proprietary Position (Assets minus liabilities in foreign currency) of the Financial Sector*

Proprietary Position (% Technical Capital)

% of Technical Capital

USD

Millio

n

Upper limit

Lower limit

11/07/2018

6

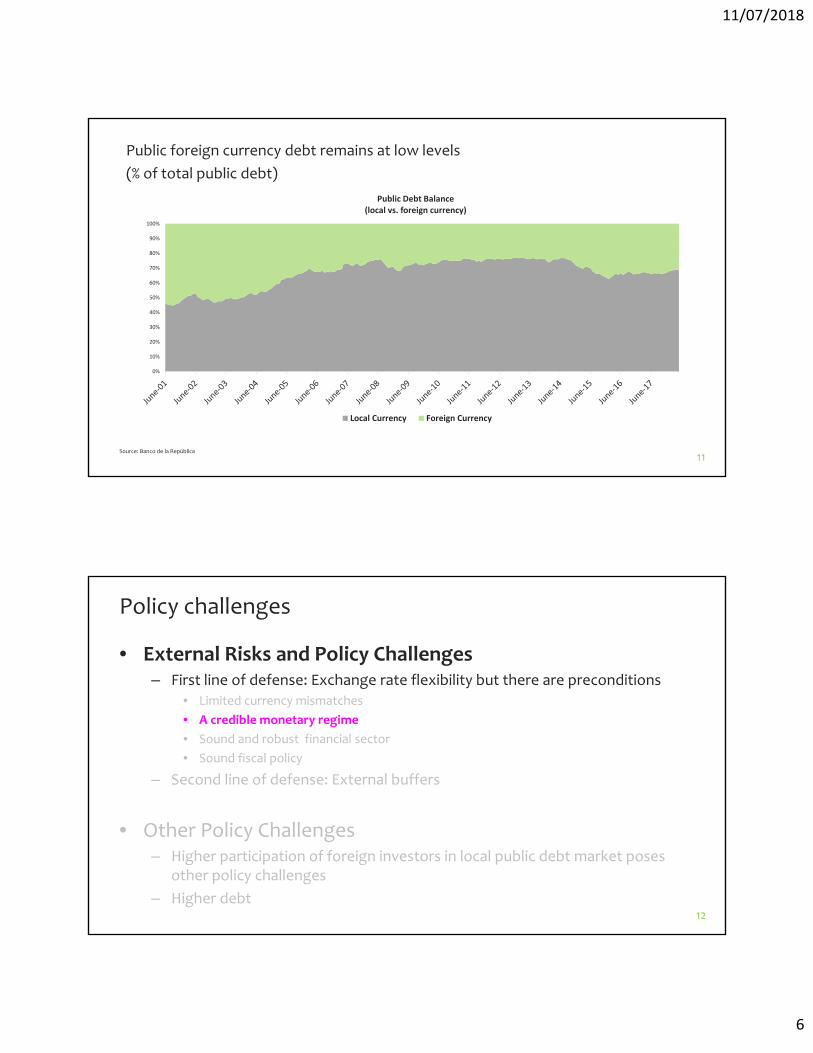

Public foreign currency debt remains at low levels

(% of total public debt)

Source: Banco de la República

11

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Public Debt Balance(local vs. foreign currency)

Local Currency Foreign Currency

Policy challenges

• External Risks and Policy Challenges – First line of defense: Exchange rate flexibility but there are preconditions

• Limited currency mismatches

• A credible monetary regime

• Sound and robust financial sector

• Sound fiscal policy

– Second line of defense: External buffers

• Other Policy Challenges– Higher participation of foreign investors in local public debt market poses

other policy challenges

– Higher debt12

11/07/2018

7

*The maximum value of the index is 15. The index is built using five categories: Political, economical, procedural, policy, operational. Each category has a value between zero and three.

Source : Dincer and Eichengreen (2014).

13

0

2

4

6

8

10

12

14

16

SWE CZE NZL USA GBR JAP AUS CAN NOR POL SWI BRA CHL PER COL MEX SGP ARG SLV GTM

Central Bank Transparency Index*

2014

1998

2008

A credible monetary regime is supported by high levels of transparency and an effective communication.Despite some enhancements, there is still a significant room for improvement.

Source: IMF (2018)

A good comprehension of the Central Bank’ communications by the general public supports a credible monetary regime.

14Source: IMF (2018)

Harry Potter

Readability of Central Bank Press Releases

11/07/2018

8

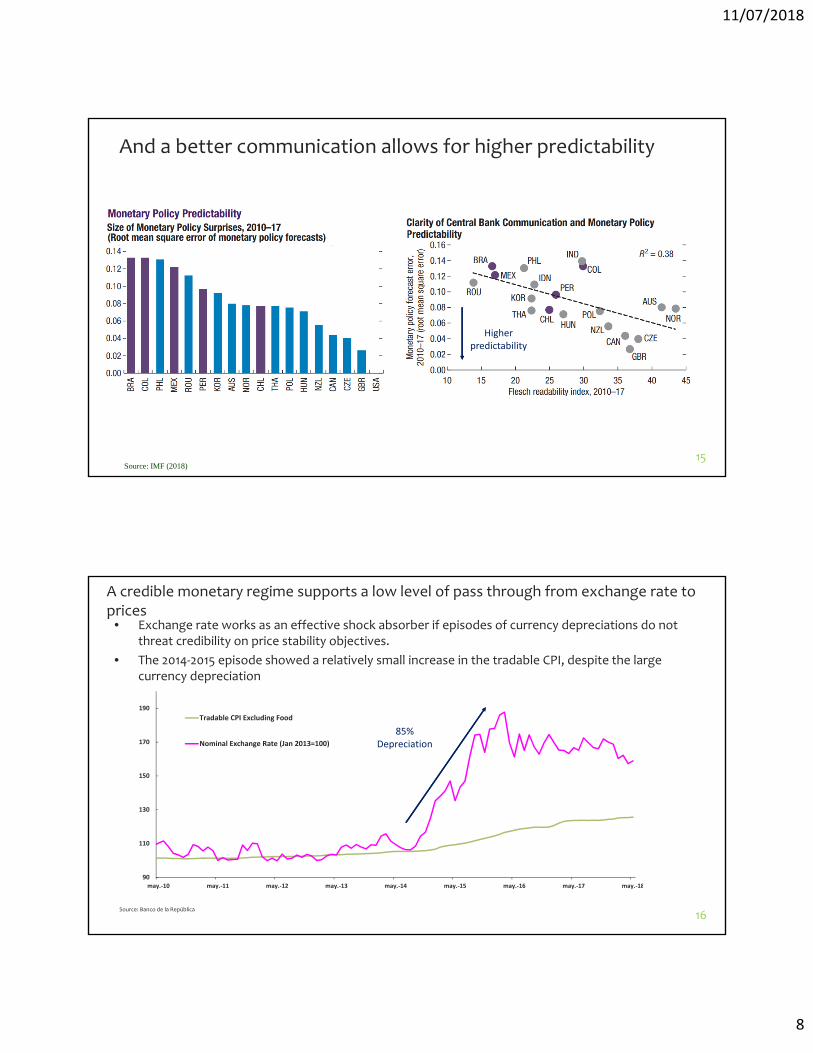

And a better communication allows for higher predictability

15Source: IMF (2018)

Higher predictability

• Exchange rate works as an effective shock absorber if episodes of currency depreciations do not threat credibility on price stability objectives.

• The 2014‐2015 episode showed a relatively small increase in the tradable CPI, despite the large currency depreciation

Source: Banco de la República

16

A credible monetary regime supports a low level of pass through from exchange rate to prices

90

110

130

150

170

190

may.‐10 may.‐11 may.‐12 may.‐13 may.‐14 may.‐15 may.‐16 may.‐17 may.‐18

Tradable CPI Excluding Food

Nominal Exchange Rate (Jan 2013=100)

85%Depreciation

11/07/2018

9

• Exchange rate works as an effective shock absorber if episodes of currency depreciations do not threat credibility on price stability objectives.

• The 2014‐2015 episode showed a relatively small increase in the tradable CPI, despite the large currency depreciation.

Source: Banco de la República

17

A credible monetary regime supports a low level of pass through from exchange rate to prices

7,9%

60,5%

‐15%

‐5%

5%

15%

25%

35%

45%

55%

65%

may.‐12 may.‐13 may.‐14 may.‐15 may.‐16 may.‐17 may.‐18

Tradables CPI Excl. Food (YoY Inflation)

Nominal Exchange Rate (% change YoY)

The low pass through could be partially accredited to the credibility of the inflation targeting regime. Therefore, improving communication and transparency is still one big challenge

Source: Banco de la República – Monthly Survey of Economic Expectations 18

4,50%

3,49%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

May‐10 May‐11 May‐12 May‐13 May‐14 May‐15 May‐16 May‐17 May‐18

Inflation Expectations

Median of 1‐year ahead expectations

Median of 2‐years ahead expectations

Inflation Target

Headline Inflation

2e1

e

11/07/2018

10

Policy challenges

• External Risks and Policy Challenges – First line of defense: Exchange rate flexibility but there are preconditions

• Limited currency mismatches

• A credible monetary regime

• Sound and robust financial sector

• Sound fiscal policy

– Second line of defense: External buffers

• Other Policy Challenges– Higher participation of foreign investors in local public debt market poses

other policy challenges

– Higher debt19

Source: Superintendencia Financiera de Colombia. Calculations by Banco de la República. 20

• Throughout the last few years, the Colombian banking system has kept solid liquidity and solvency indicators.• This has occurred despite the adjustment of the Colombian economy to negative external shocks. At the same

time, domestic regulation has contributed to building buffers for credit risk (e.g. dynamic provisioning) andliquidity risk.

333,65%342,15%

80%

120%

160%

200%

240%

280%

320%

360%

400%

440%

480%

Mar‐13 Sep‐13 Mar‐14 Sep‐14 Mar‐15 Sep‐15 Mar‐16 Sep‐16 Mar‐17 Sep‐17 Mar‐18

30‐Day Liquidity Coverage Ratio (LCR)

Total Depository Institutions

Banks

Minimum Requirement

LCR= Liquid Assets / net cash outflows over the next 30 days

15,79%

16,49%

8%

10%

12%

14%

16%

18%

20%

Mar‐12 Nov‐12 Jul‐13 Mar‐14 Nov‐14 Jul‐15 Mar‐16 Nov‐16 Jul‐17 Mar‐18

Total Solvency Ratio (Tier II)

Banks

Total Depository Institutions

Minimum Requirement

Total Solvency Ratio = Technical capital / weighted assets + (11.11)*Market Risk

Local banks are resilient to tighter external conditions

11/07/2018

11

Local banks are resilient to tighter external conditions II

• The latest stress test exercise simulates the effect of a full exit of foreign investors from domestic public/private debt marketstogether with a significant fall in GDP growth (1.3% for 2018).

• Under this extreme scenario the estimated cumulative losses would generate a reduction in Tier 1 Capital Ratio from 11,6% to 9,8% well above the regulatory minimum: 4,5%.

21

Policy challenges

• External Risks and Policy Challenges – First line of defense: Exchange rate flexibility but there are preconditions

• Limited currency mismatches

• A credible monetary regime

• Sound and robust financial sector

• Sound fiscal policy

– Second line of defense: External buffers

• Other Policy Challenges– Higher participation of foreign investors in local public debt market poses

other policy challenges

– Higher debt22

11/07/2018

12

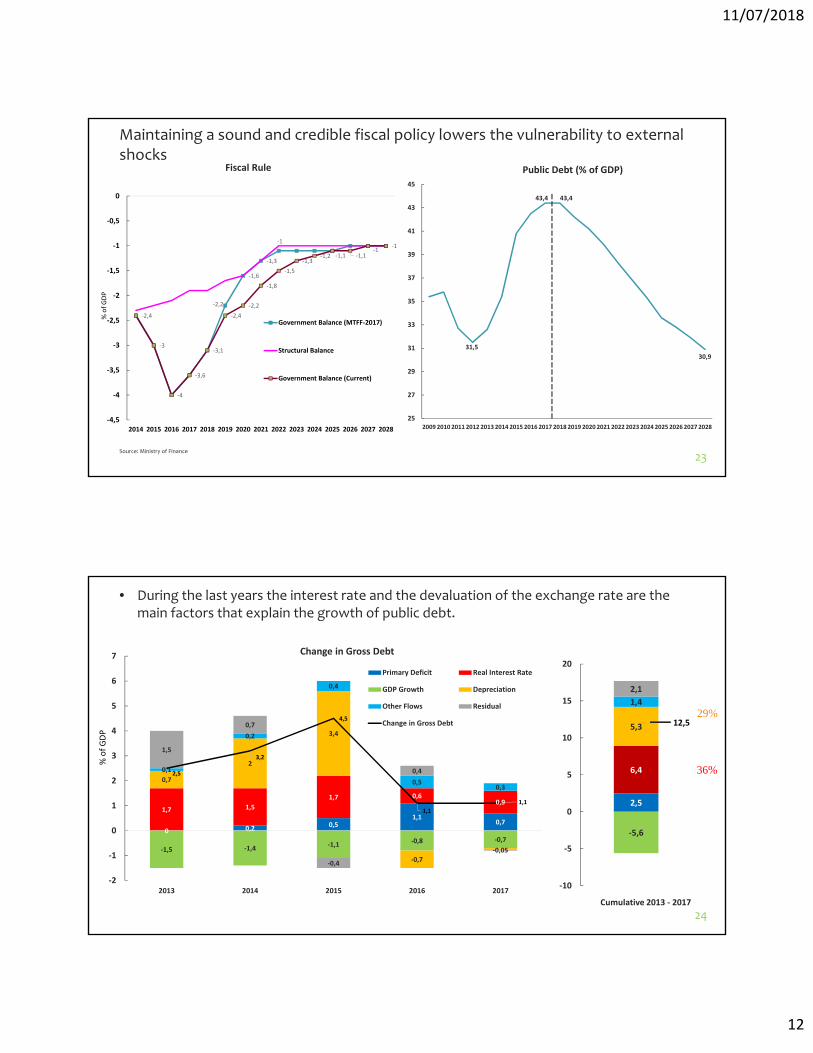

31,5

43,4 43,4

30,9

25

27

29

31

33

35

37

39

41

43

45

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

Public Debt (% of GDP)

Source: Ministry of Finance

‐2,2

‐1,6

‐1,3

‐1

‐2,4

‐3

‐4

‐3,6

‐3,1

‐2,4

‐2,2

‐1,8

‐1,5

‐1,3‐1,2 ‐1,1 ‐1,1

‐1‐1

‐4,5

‐4

‐3,5

‐3

‐2,5

‐2

‐1,5

‐1

‐0,5

0

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

Fiscal Rule

Government Balance (MTFF‐2017)

Structural Balance

Government Balance (Current)

% of GDP

Maintaining a sound and credible fiscal policy lowers the vulnerability to external shocks

23

24

2,5

6,4

‐5,6

5,3

1,4

2,1

‐10

‐5

0

5

10

15

20

Cumulative 2013 ‐ 2017

12,5

0 0,2 0,51,1

0,7

1,7 1,5

1,7 0,60,9

‐1,5 ‐1,4‐1,1 ‐0,8 ‐0,7

0,7

2

3,4

‐0,7

0,1

0,2

0,4

0,50,3

1,5

0,7

‐0,4

0,4

‐0,05

2,5

3,2

4,5

1,1

1,1

‐2

‐1

0

1

2

3

4

5

6

7

2013 2014 2015 2016 2017

Change in Gross Debt

Primary Deficit Real Interest Rate

GDP Growth Depreciation

Other Flows Residual

Change in Gross Debt

% of GDP

• During the last years the interest rate and the devaluation of the exchange rate are the main factors that explain the growth of public debt.

29%

36%

11/07/2018

13

Debt levels have increased but remain below critical levels.

*Annual Moving Average (30% is considered risky and 40% vulneragle)

Source: Banco de la República 25

17,4

14

15

16

17

18

19

20

ene.‐12 ene.‐13 ene.‐14 ene.‐15 ene.‐16 ene.‐17 ene.‐18

(%) Households’ Financial Burden(Interest and Capital payments / Income)*

Total Solvency Ratio = (Interest payments + capital payments) / Monthly Income

Source: Superintendencia Financiera. Calculations by Banco de la República

-5%

0%

5%

10%

15%

20%

25%

30%

0

50

100

150

200

250

ago.-08 feb.-10 ago.-11 feb.-13 ago.-14 feb.-16 ago.-17

Composition and Real Annual Growth Rate of Households' Indebtedness

Consumption Mortgages Indebtedness Real Annual Growth Rate (RHS)

Policy challenges

• External Risks and Policy Challenges – First line of defense: Exchange rate flexibility but there are preconditions

• Limited currency mismatches

• A credible monetary regime

• Sound and robust financial sector

• Sound fiscal policy

– Second line of defense: External buffers

• Other Policy Challenges– Higher participation of foreign investors in local public debt market poses

other policy challenges

– Higher debt26

11/07/2018

14

A sufficient level of external buffers provides another safeguard against external shocks. The Flexible Credit Line (FCL) by the IMF has complemented the accumulation of international reserves.

*A ratio between 1 and 1.5 is considered adequate

Source: IMF. 27

0% 100% 200% 300% 400% 500% 600% 700%

Argentina

Turkey

Malaysia

South Africa

Chile

Poland

Mexico

Colombia (without FCL)

India

Colombia (with FCL)

Indonesia

Brazil

China

Philippines

Peru

Korea

International Reserves to Short‐term Debt and CurrentAccount Balance

0

0,5

1

1,5

2

2,5

3

3,5

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Ratio of Reserves/ARA Metric*

Chile Colombia Mexico Peru

Policy challenges

• External Risks and Policy Challenges – First line of defense: Exchange rate flexibility but there are preconditions

• Limited currency mismatches

• A credible monetary regime

• Sound and robust financial sector

• Sound fiscal policy

– Second line of defense: External buffers

• Other Policy Challenges– Higher participation of foreign investors in local public debt market

poses other policy challenges

– Higher debt28

11/07/2018

15

Source: Banco de la República29

0%

5%

10%

15%

20%

25%

30%

jun.‐13 jun.‐14 jun.‐15 jun.‐16 jun.‐17 jun.‐18

% Offshore investors (TES) / Total outstanding

% Offshore investors (UVR inflation linked bonds) / Total outstanding

The development of the public debt market came hand on hand with an increased participation of foreign investors, particularly in recent years. This increase was mainly driven by the reduction of withholding tax for offshore investors (from 33% to 14% ) and the increase of Colombian debt weight in the JP Morgan’s GBI index since 2014.

The higher presence of offshore investors in Colombia goes in line with the experience of other emerging markets.

Source: IMF WP ‐ Arslanalp and Tsuda (2017)30

28%

43%

0%

10%

20%

30%

40%

50%

60%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Brazil

Colombia

Mexico

Peru

39%

0%

10%

20%

30%

40%

50%

60%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

China

India

Indonesia

Malaysia

Philippines

Thailand

34%

0%

10%

20%

30%

40%

50%

60%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Hungary

Lithuania

Poland

Romania

41%

0%

10%

20%

30%

40%

50%

60%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Russia

South Africa

Turkey

Ukraine

Foreign Holdings of Local‐Currency EM Government Debt Securities (% of total)

11/07/2018

16

• The increase in offshore participation has been positive for diversifying the Government’s financing sources and has helped to finance the current account deficit facilitating the adjustment of the economy to external shocks. In addition, the currency risk is assumed partially by foreign investors.

BUT…

• Foreign investors’ decisions could affect interest rates along the curve offsetting in some cases the transmission of monetary policy to bonds with longer maturities.

• A sudden exit of foreign investors could create pressures on the exchange rate. A big reaction of these agents could amplify the effects of external shocks with possible implications on financial markets and financial stability.

31

A Higher Participation of Non‐Resident Investors in the Local Public Debt Market is Welcomed but Creates Challenges

Policy challenges

• External Risks and Policy Challenges – First line of defense: Exchange rate flexibility but there are preconditions

• Limited currency mismatches

• A credible monetary regime

• Sound and robust financial sector

• Sound fiscal policy

– Second line of defense: External buffers

• Other Policy Challenges– Higher participation of foreign investors in local public debt market poses

other policy challenges

– Higher debt32

11/07/2018

17

Thanks

33

Debt levels in Colombia have increased in last years but the size of the credit expansion is below international averages. Financial depth is still low relative other EME.

Source: Bank for International Settlements 34

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

Apr‐05 Apr‐08 Apr‐11 Apr‐14 Apr‐17

Total Credit to Non‐Financial Private Sector(ratio to GDP)

Emerging markets (aggregate) Advanced economies (aggregate)

Colombia Chile

Mexico Malaysia

Thailand

0%

20%

40%

60%

80%

100%

120%

140%

160%

Mar‐05 Mar‐08 Mar‐11 Mar‐14 Mar‐17

Credit‐to‐GDP gaps(% of GDP)

Colombia Chile Argentina Brazil Mexico Malaysia Thailand

11/07/2018

18

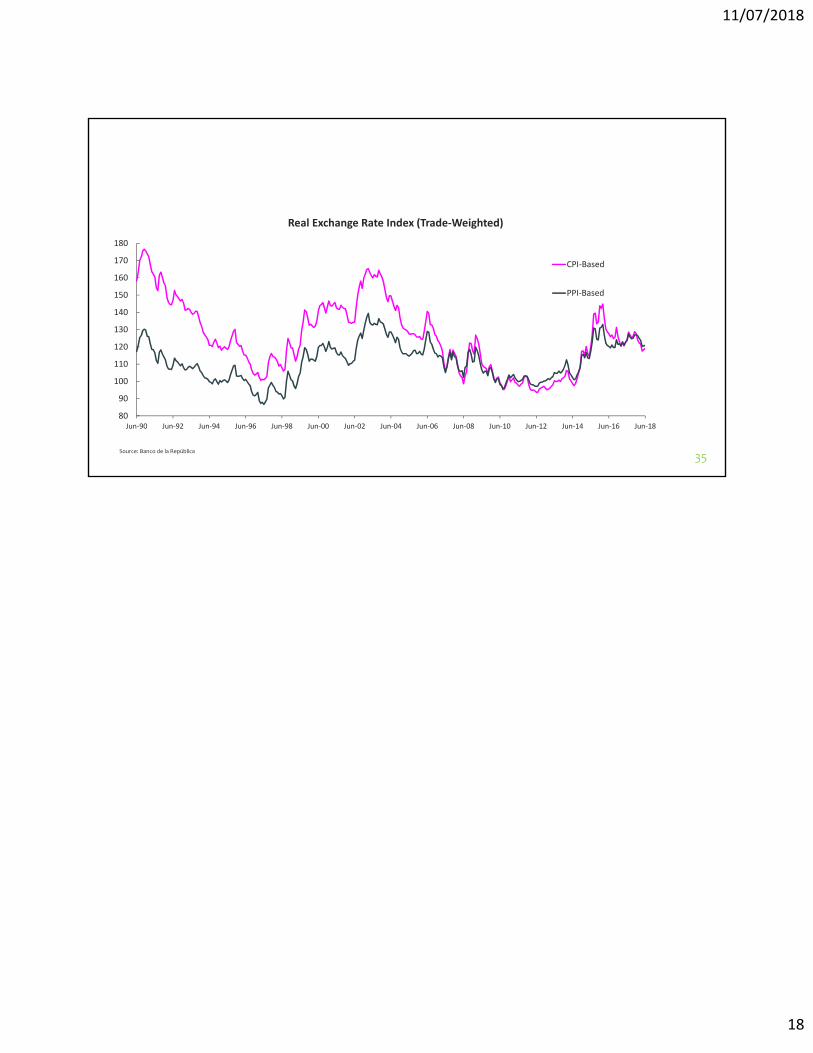

Source: Banco de la República

35

80

90

100

110

120

130

140

150

160

170

180

Jun‐90 Jun‐92 Jun‐94 Jun‐96 Jun‐98 Jun‐00 Jun‐02 Jun‐04 Jun‐06 Jun‐08 Jun‐10 Jun‐12 Jun‐14 Jun‐16 Jun‐18

Real Exchange Rate Index (Trade‐Weighted)

CPI‐Based

PPI‐Based