monetary policy framework in nigeria: formulation and ... policy... · credit ceiling, sectoral...

TRANSCRIPT

Monetary Policy Framework in Nigeria: Formulation and Implementation Challenges*

By

Central Bank of NigeriaCentral Bank of NigeriaCentral Bank of NigeriaCentral Bank of Nigeria

Ezema, Charles Chibundu, PhD

Monetary Policy Department,

Central Bank of Nigeria

African Institute of Applied Economics (AIAE): Monthly Seminar, August 2009

*The views expressed in this paper are entirely that of the author and do not in any way reflect the official position of the

Central Bank of Nigeria

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aOutline

� Introduction

� Monetary Policy Instruments

� Monetary Policy Framework

Monetary Policy Formulation

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

� Monetary Policy Formulation

� Implementation Challenges

� Concluding Remarks

2

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aIntroduction

� Monetary Policy is the deliberate use of monetary instruments

(direct and indirect) at the disposal of monetary authorities such as

central bank in order to achieve macroeconomic stability

� Macroeconomic stability refers to achievement of internal and

external Balance

� Internal Balance here refers to:

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

� price stability (Low inflation)

� Low unemployment

� High and stable Economic growth

� External balance

� Balance of payment equilibrium

� Exchange rate stability

3

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aIntroduction…cont.

� For most central banks, the objective of price stability is given priority

over others in the conduct of monetary policy

� In some instances, however, the laws establishing the central bank

impose dual mandate of low inflation and high growth…necessitating

the formulation of monetary policy that attempt to strike a balance

between the two goals

Mandates of CBN

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

� Mandates of CBN

� The CBN Act. 2007, assigns the following mandates to CBN

� Ensure monetary and price stability

� Issue legal tender currency in Nigeria

� Maintain external reserves to safeguard the internationalvalue of the legal tender currency

� Promote sound financial system in Nigeria; and

� Act as banker and provide economic and financial advice theFederal Government

4

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aIntroduction…cont.

� The CBN is solely responsible for the conduct of monetary

policy in Nigeria

� The General Objectives of Monetary Policy

� Price stability

� High and sustainable economic growth

� (reducing the gap between actual and potential GDPin the short and medium-term)

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

in the short and medium-term)

� Balance of payment equilibrium

� CBN monetary policy targets two major objectives

� Price stability

� Sustainable economic growth

� Monetary Policy is essentially the tool for executing the

mandate of monetary and price stability

5

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

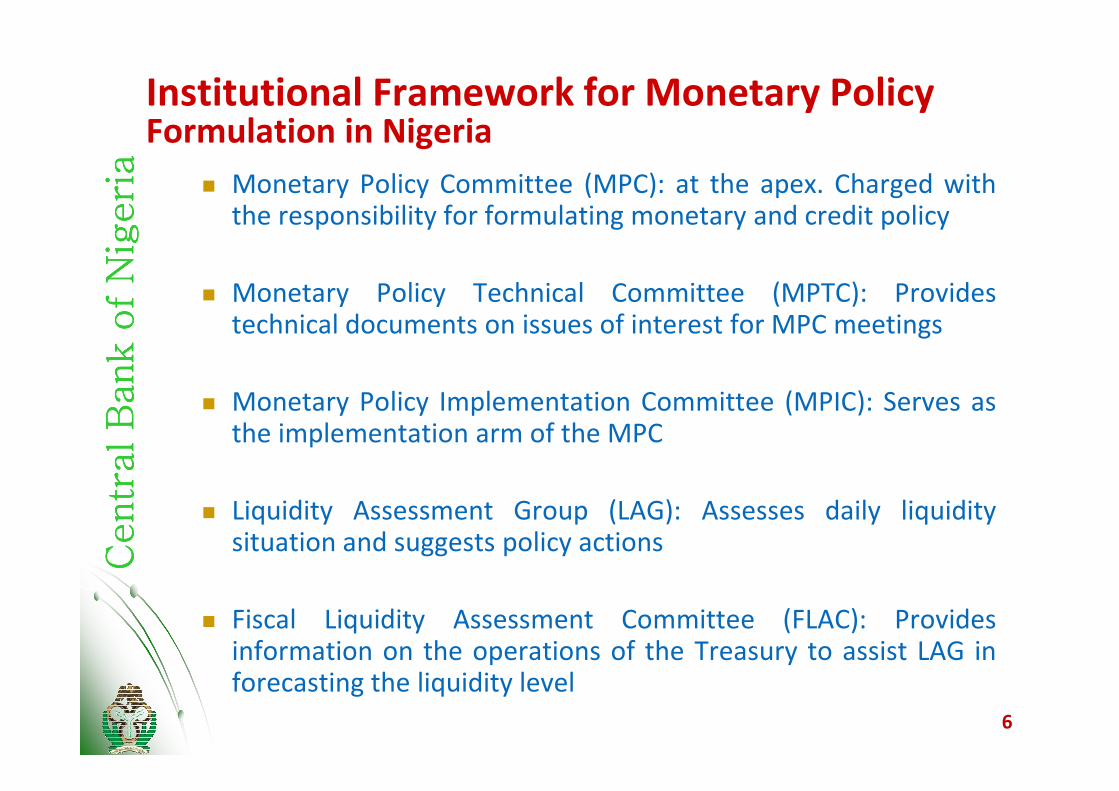

aInstitutional Framework for Monetary Policy Formulation in Nigeria

� Monetary Policy Committee (MPC): at the apex. Charged withthe responsibility for formulating monetary and credit policy

� Monetary Policy Technical Committee (MPTC): Providestechnical documents on issues of interest for MPC meetings

� Monetary Policy Implementation Committee (MPIC): Serves as

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

� Monetary Policy Implementation Committee (MPIC): Serves asthe implementation arm of the MPC

� Liquidity Assessment Group (LAG): Assesses daily liquiditysituation and suggests policy actions

� Fiscal Liquidity Assessment Committee (FLAC): Providesinformation on the operations of the Treasury to assist LAG inforecasting the liquidity level

6

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

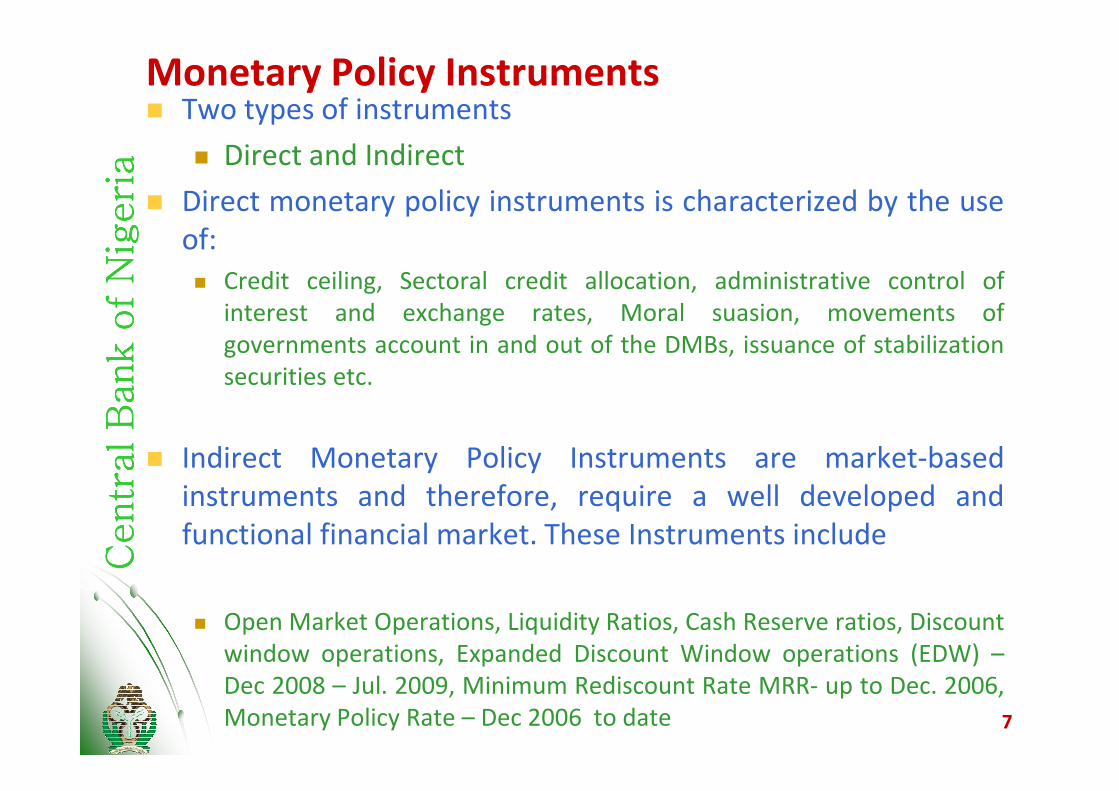

Monetary Policy Instruments� Two types of instruments

� Direct and Indirect

� Direct monetary policy instruments is characterized by the use

of:

� Credit ceiling, Sectoral credit allocation, administrative control of

interest and exchange rates, Moral suasion, movements of

governments account in and out of the DMBs, issuance of stabilization

securities etc.

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

� Indirect Monetary Policy Instruments are market-based

instruments and therefore, require a well developed and

functional financial market. These Instruments include

� Open Market Operations, Liquidity Ratios, Cash Reserve ratios, Discount

window operations, Expanded Discount Window operations (EDW) –

Dec 2008 – Jul. 2009, Minimum Rediscount Rate MRR- up to Dec. 2006,

Monetary Policy Rate – Dec 2006 to date 7

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

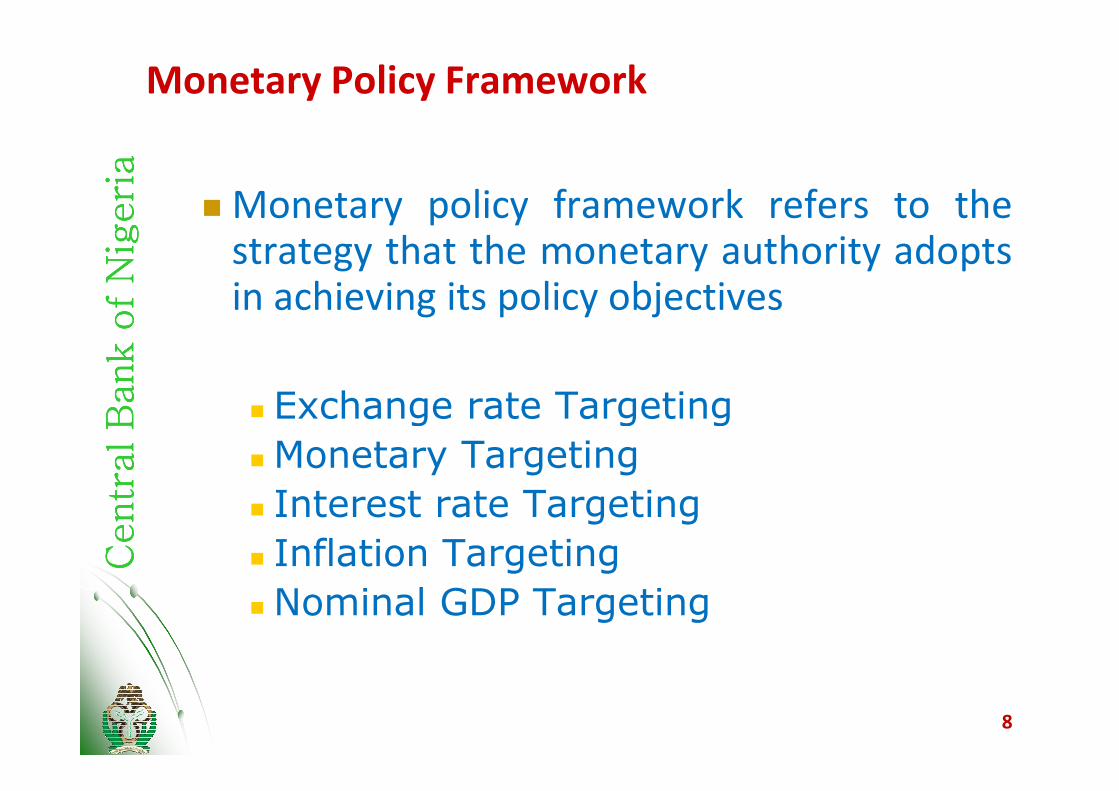

aMonetary Policy Framework

� Monetary policy framework refers to thestrategy that the monetary authority adoptsin achieving its policy objectives

Exchange rate Targeting

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

� Exchange rate Targeting

� Monetary Targeting

� Interest rate Targeting

� Inflation Targeting

� Nominal GDP Targeting

8

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aMonetary Policy Framework…cont.

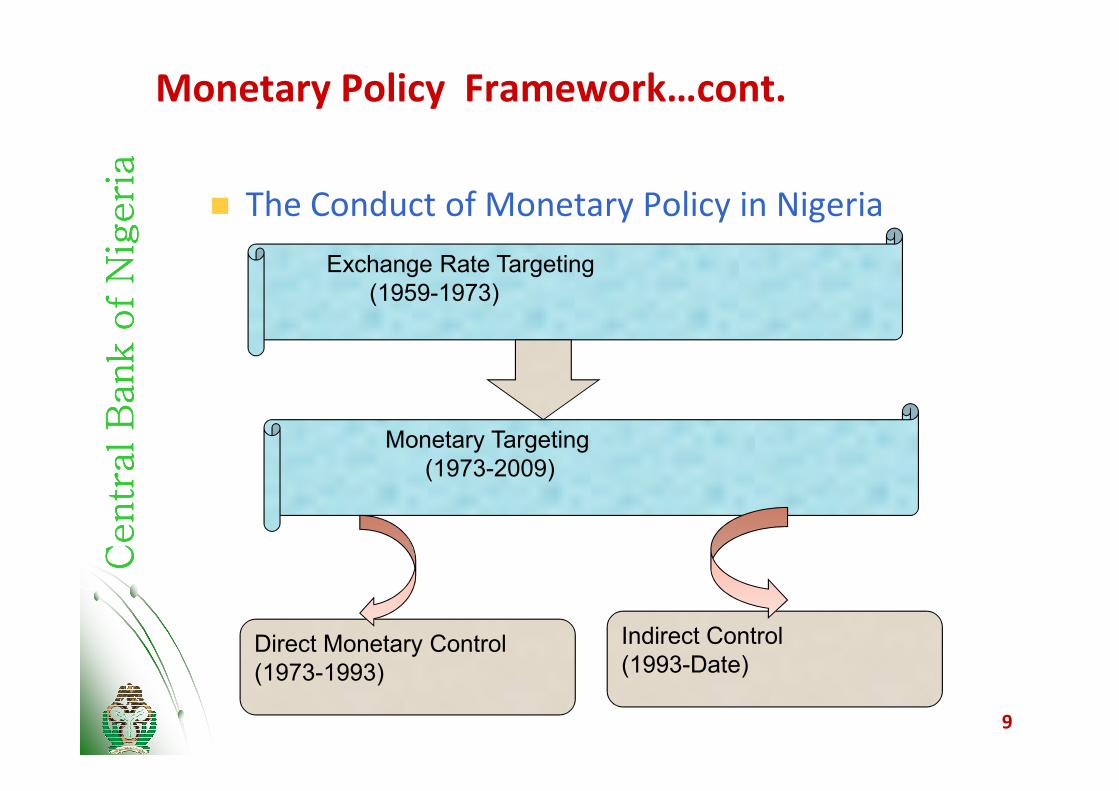

� The Conduct of Monetary Policy in Nigeria

Exchange Rate Targeting

(1959-1973)

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

Monetary Targeting

(1973-2009)

Indirect Control

(1993-Date)Direct Monetary Control

(1973-1993)

9

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aPolicy Framework: Transmission mechanism..cont

� Monetary policy actions affect the real economy through a

process generally referred to as the “transmission mechanism”

� It is complex, time consuming and therefore difficult to

manage (Lags)

� To achieve a goal that can not be directly measured requires

the employment of intermediate targets, or what is generally

referred to as the nominal anchor for monetary policy.

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

referred to as the nominal anchor for monetary policy.

� There are two kinds of nominal anchor:

� Quantity-based nominal anchor

� Price-based nominal anchor

� The quantity-based nominal anchor targets money stock while

the price-based nominal anchor targets exchange rate or

interest rate

� Currently, the CBN uses broad money supply (M2) as the

nominal anchor 10

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aPolicy Framework: Transmission mechanism..cont

� The final targets of monetary policy are macroeconomic

variables, normally, the inflation rate

� These targets are not directly affected by the central bank

policy tools

� The central bank chooses another set of variables called the

operating targets (base money, reserves etc) which are more

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

responsive to its policy tools

� Operating and intermediate targets are used to direct the

monetary policy towards the achievement of its goals

� The criteria for choosing variable/targets include

� Measurability

� Controllability

� Ability to predictably affect goals in desired manner11

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

Monetary Targeting

� The Bank’s current monetary policy framework is monetary

targeting with:

� Base (Reserve) money as operating target

� Broad money supply (M2) as intermediate target

� Inflation as the ultimate or final target

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

� Both the operating target and intermediate target are

employed in determining the optimum level of money

stock/liquidity consistent with the assumed level of expected

output growth and inflation

� This process starts with the design of a short-term monetary

programme approved by MPC using the quantity theory of

money12

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aMonetary Policy Framework…cont.�� TheThe quantityquantity theorytheory ofof moneymoney isis illustratedillustrated inin anan equation,equation, asas::

�� MvMv == PÝPÝ ……………………………………………………………………………………....11WhereWhere MM == moneymoney stockstock // supplysupply

vv == velocityvelocity ofof moneymoney (the(the numbernumber ofof timestimes aa unitunit ofof currencycurrency changeschangeshands)hands)

PP == PricePrice ofof basketbasket ofof goodsgoods transactedtransacted

ÝÝ == thethe sizesize ofof basketbasket ofof goodsgoods transactedtransacted inin aa givengiven periodperiod..

AssumptionsAssumptions::

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

�� AssumptionsAssumptions::�� vv andand YY areare constant,constant, inin thethe shortshort termterm..

�� QuantityQuantity ofof moneymoney determineddetermined byby outsideoutside forcesforces;; isis thethe mainmain influenceinfluence ofof economiceconomicactivityactivity inin aa societysociety..

�� TheThe economyeconomy isis operatingoperating inin fullfull employmentemployment equilibrium,equilibrium, andand ,,

� The optimum liquidity level and aggregate net credit to

the domestic economy are computed using the CBN

balance sheet and solving the following equation:13

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

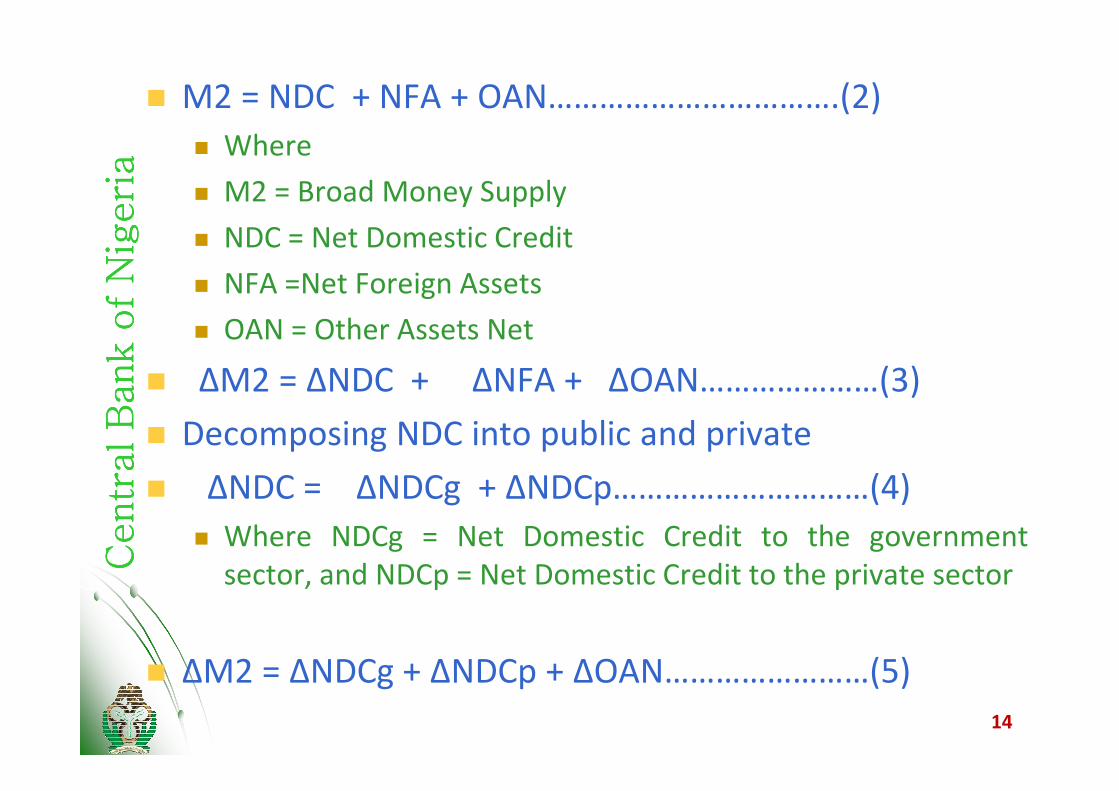

a� M2 = NDC + NFA + OAN…………………………….(2)

� Where

� M2 = Broad Money Supply

� NDC = Net Domestic Credit

� NFA =Net Foreign Assets

� OAN = Other Assets Net

� ∆M2 = ∆NDC + ∆NFA + ∆OAN…………………(3)

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

� ∆M2 = ∆NDC + ∆NFA + ∆OAN…………………(3)

� Decomposing NDC into public and private

� ∆NDC = ∆NDCg + ∆NDCp…………………………(4)

� Where NDCg = Net Domestic Credit to the government

sector, and NDCp = Net Domestic Credit to the private sector

� ∆M2 = ∆NDCg + ∆NDCp + ∆OAN……………………(5)

14

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

Monetary Policy Framework…cont.

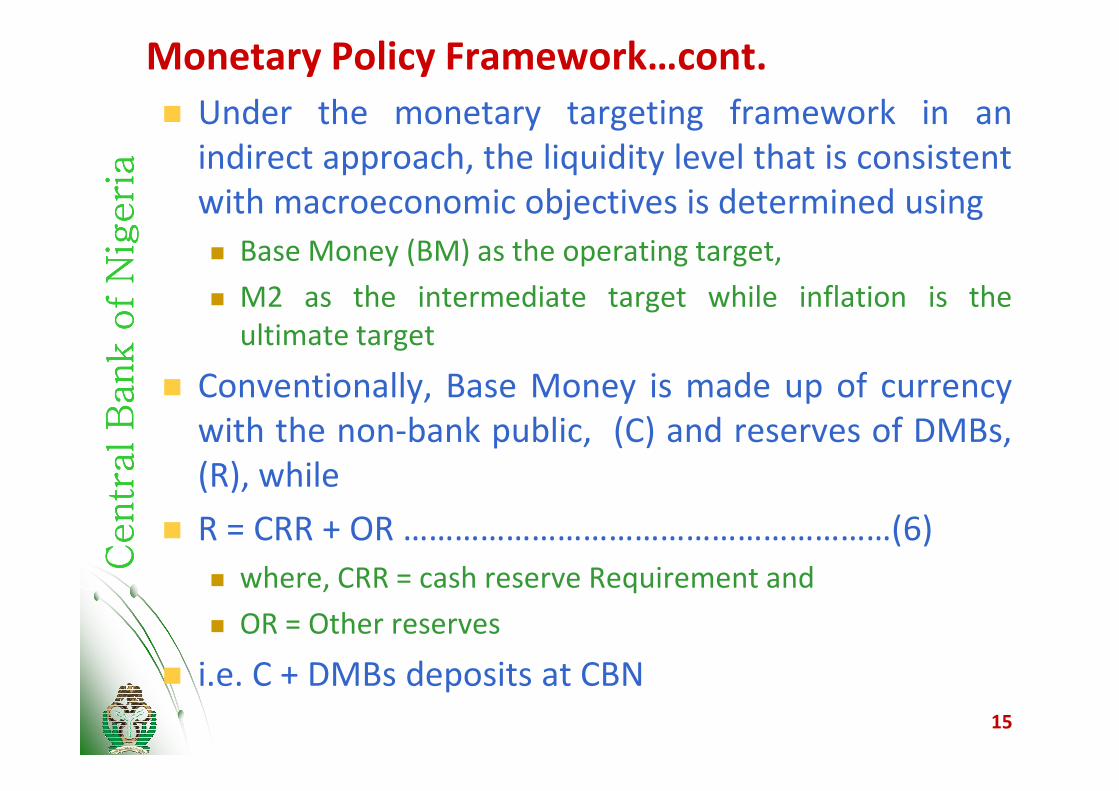

� Under the monetary targeting framework in an

indirect approach, the liquidity level that is consistent

with macroeconomic objectives is determined using

� Base Money (BM) as the operating target,

� M2 as the intermediate target while inflation is the

ultimate target

� Conventionally, Base Money is made up of currency

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

� Conventionally, Base Money is made up of currency

with the non-bank public, (C) and reserves of DMBs,

(R), while

� R = CRR + OR …………………………………………………(6)

� where, CRR = cash reserve Requirement and

� OR = Other reserves

� i.e. C + DMBs deposits at CBN

15

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aMonetary Policy Framework…cont

� The main sources of base money in Nigeria:

� Net Central Bank Claim on Government (NCBCg)

� Net Foreign Assets of the Central Bank (NFACB)

� Other Assets Net of the Central Bank (OACB)

� The balance sheet identity of the Central

Bank can be written as:

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

Bank can be written as:

� NCBCg +NFACB + OACB = C + R = BM………………..(6)

� The process of money creation derives from banks

expanding money supply by a multiple of reserves

� To influence money supply, OMO is applied among

other instruments

16

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aMonetary Policy Framework…cont

� M2 = C + D…………………………………..(7)

� BM = C + R…………………………………..(8)

� M2 = 1 + c……………………………………(9)

� BM = c + r……………………………………(10)

� M2/BM = K = (1+c)/(c+r); 0 < r, c < 1…..(11)

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

� M2 = KBM = [(1+c)/(c+r)BM…………(12)

� Where:

� k = multiplier

� R = DMBs’ Reserve with the Central Bank

� C = Currency outside banks

� c = currency/deposit ratio

� r = reserve/deposit ratio17

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

Monetary Policy Framework…cont

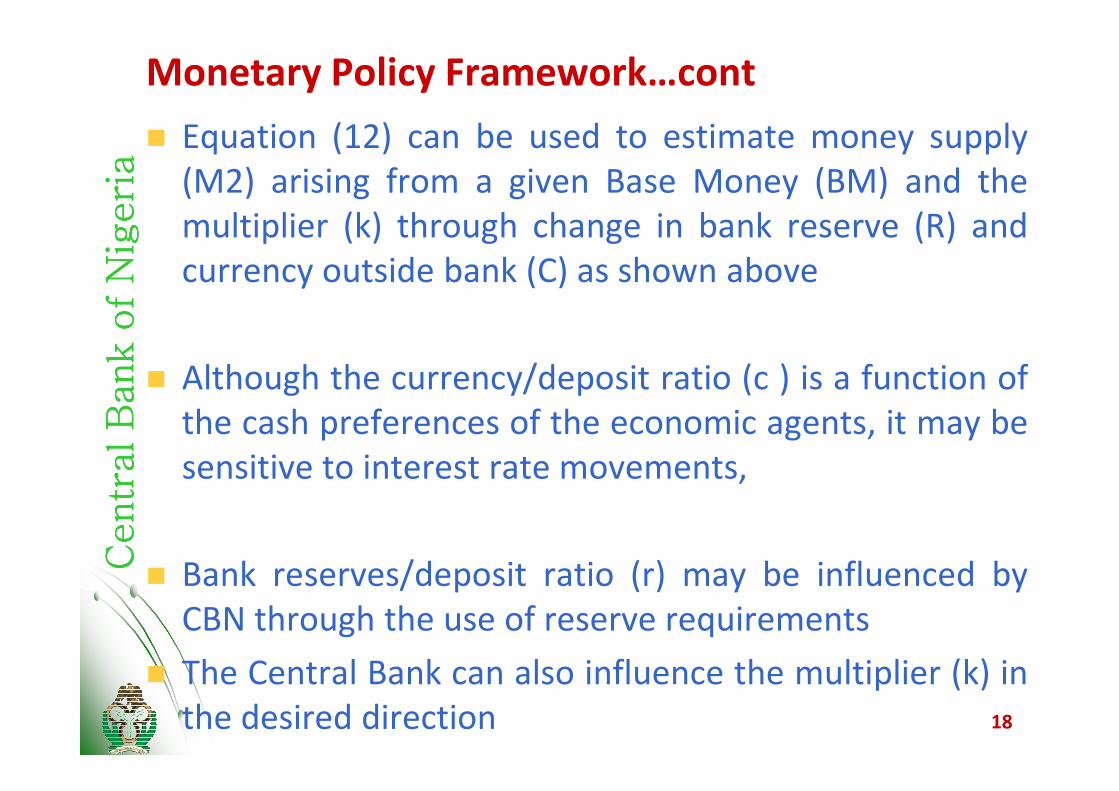

� Equation (12) can be used to estimate money supply

(M2) arising from a given Base Money (BM) and the

multiplier (k) through change in bank reserve (R) and

currency outside bank (C) as shown above

� Although the currency/deposit ratio (c ) is a function of

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

Although the currency/deposit ratio (c ) is a function of

the cash preferences of the economic agents, it may be

sensitive to interest rate movements,

� Bank reserves/deposit ratio (r) may be influenced by

CBN through the use of reserve requirements

� The Central Bank can also influence the multiplier (k) in

the desired direction 18

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aShort-Term Monetary Policy Framework in Nigeria

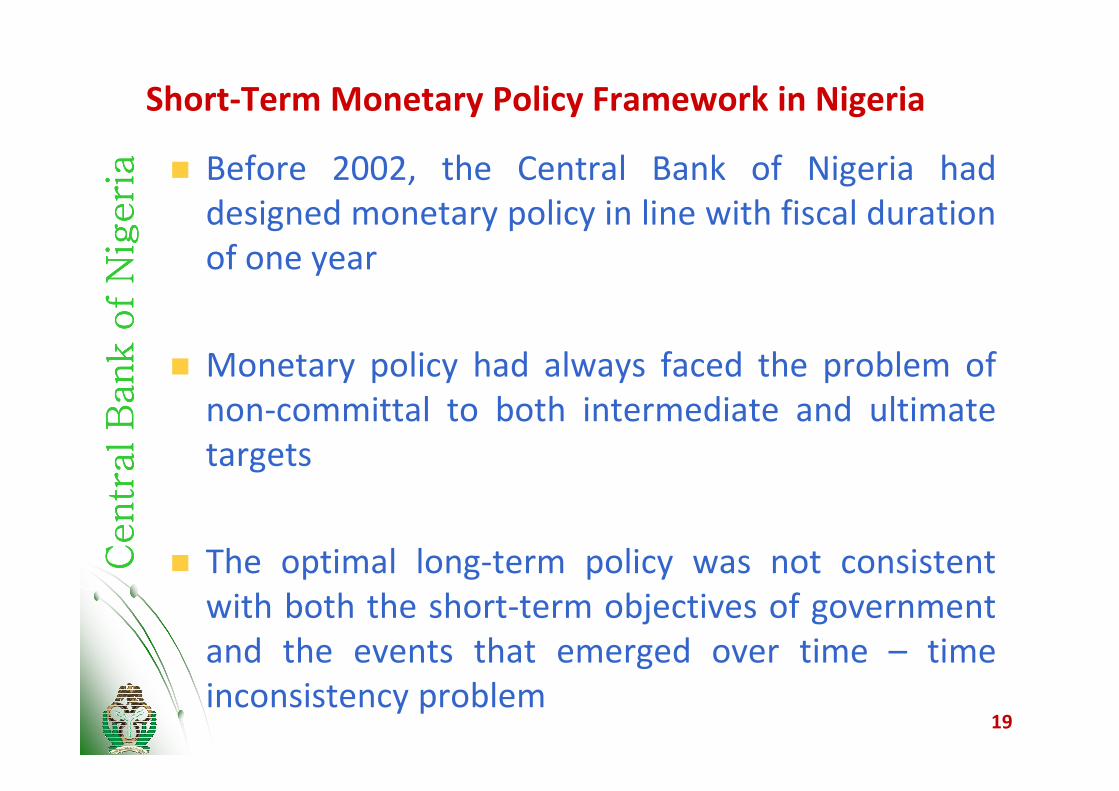

� Before 2002, the Central Bank of Nigeria had

designed monetary policy in line with fiscal duration

of one year

� Monetary policy had always faced the problem of

non-committal to both intermediate and ultimate

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

non-committal to both intermediate and ultimate

targets

� The optimal long-term policy was not consistent

with both the short-term objectives of government

and the events that emerged over time – time

inconsistency problem19

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aKey Policy Targets and Outcomes (%)

Targets Outcomes Targets Outcomes Targets Outcomes

M2 10 31.4 14.6 48.1 12.2 27

M1 4.1 19.9 9.8 62.2 4.3 28.1

Agg.

1999 2000 2001

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

Agg.

Credit to

the

Economy 18.3 35.5 27.8 -23.1 15.8 74.8

Net Credit

to Govt. 10.2 57.1 37.8 -162.3 2.6 -94.6

Net Credit

to Private

Sector 19.9 27.3 21.9 30.9 22.8 43.5

Inflation 9 6.6 9 6.9 7 16.5

Real GDP

Growth 3 2.7 3 3.8 5 4.620

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aMedium-Term Monetary Policy Framework

� With effect from January 2002, the CBN adopted the

medium-term perspective in monetary policy

formulation

� The medium-term framework gives the Bank the

opportunity to set targets on a two yearly basis

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

opportunity to set targets on a two yearly basis

rather than on annual basis

� However, in the course of the implementation,

reviews could be made to reflect current economic

developments

21

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aMedium-Term Monetary Policy Framework

� Rationale:

� This shift was necessitated by the fact that

monetary policy actions affects the ultimate

target with substantial lags

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

� The shift freed monetary policy implementation

from the problem of time inconsistency and

minimized overreaction to some temporary

shocks

22

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

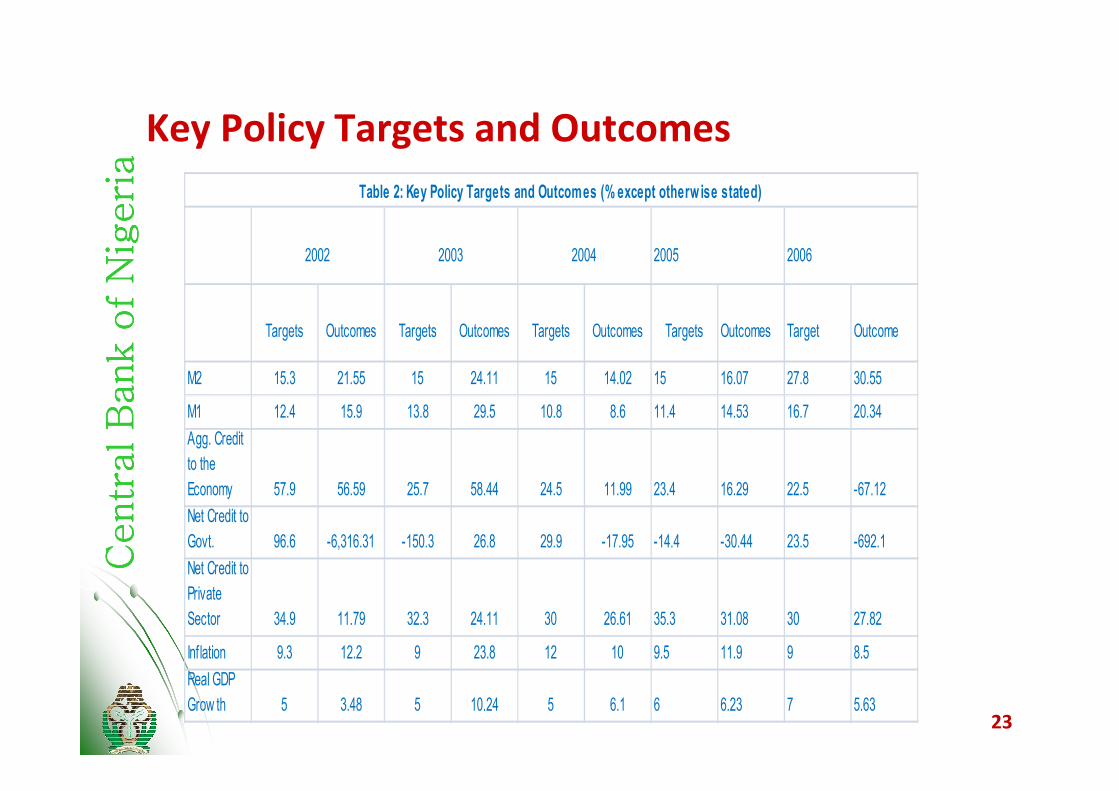

aKey Policy Targets and Outcomes

Targets Outcomes Targets Outcomes Targets Outcomes Targets Outcomes Target Outcome

M2 15.3 21.55 15 24.11 15 14.02 15 16.07 27.8 30.55

2002 2003 2004 2005 2006

Table 2: Key Policy Targets and Outcomes (% except otherw ise stated)

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

M1 12.4 15.9 13.8 29.5 10.8 8.6 11.4 14.53 16.7 20.34

Agg. Credit

to the

Economy 57.9 56.59 25.7 58.44 24.5 11.99 23.4 16.29 22.5 -67.12

Net Credit to

Govt. 96.6 -6,316.31 -150.3 26.8 29.9 -17.95 -14.4 -30.44 23.5 -692.1

Net Credit to

Private

Sector 34.9 11.79 32.3 24.11 30 26.61 35.3 31.08 30 27.82

Inflation 9.3 12.2 9 23.8 12 10 9.5 11.9 9 8.5

Real GDP

Grow th 5 3.48 5 10.24 5 6.1 6 6.23 7 5.6323

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aNew Monetary Policy Implementation Framework

� With effect from December 2006, the Bank

introduced a new monetary policy implementation

framework with the aim of:

� Reducing interest rate volatility to ensure that money

market rates especially the overnight interbank rates are

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

market rates especially the overnight interbank rates are

more responsive to policy rates

� Preparatory steps towards transiting to full fledged

inflation targeting

24

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aNew Monetary Policy Implementation Framework

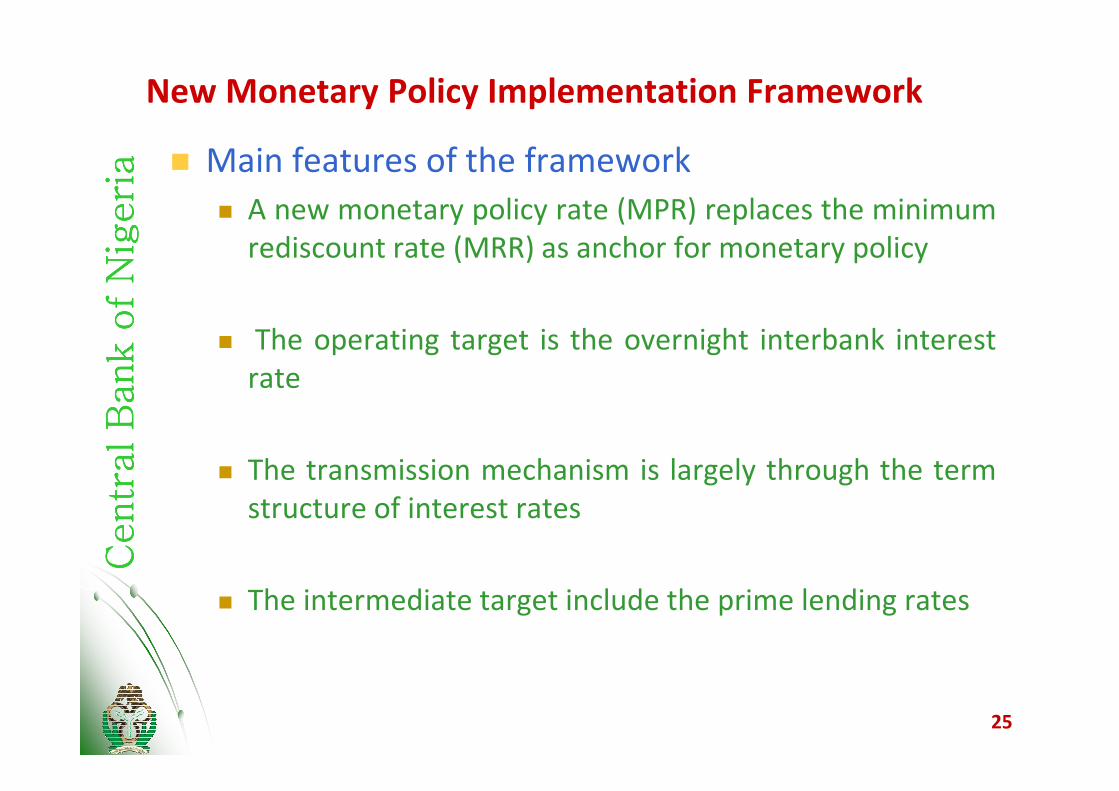

� Main features of the framework

� A new monetary policy rate (MPR) replaces the minimum

rediscount rate (MRR) as anchor for monetary policy

� The operating target is the overnight interbank interest

rate

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

� The transmission mechanism is largely through the term

structure of interest rates

� The intermediate target include the prime lending rates

25

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aNew Monetary Policy Implementation Framework

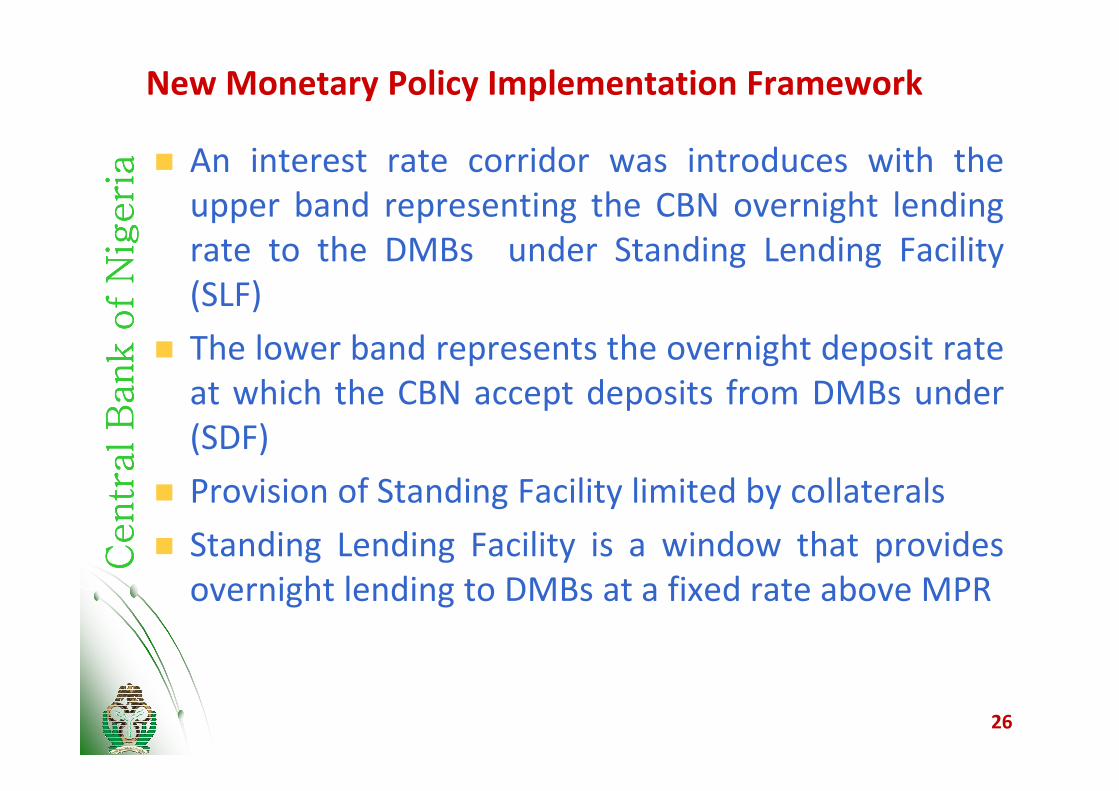

� An interest rate corridor was introduces with the

upper band representing the CBN overnight lending

rate to the DMBs under Standing Lending Facility

(SLF)

� The lower band represents the overnight deposit rate

at which the CBN accept deposits from DMBs under

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

at which the CBN accept deposits from DMBs under

(SDF)

� Provision of Standing Facility limited by collaterals

� Standing Lending Facility is a window that provides

overnight lending to DMBs at a fixed rate above MPR

26

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

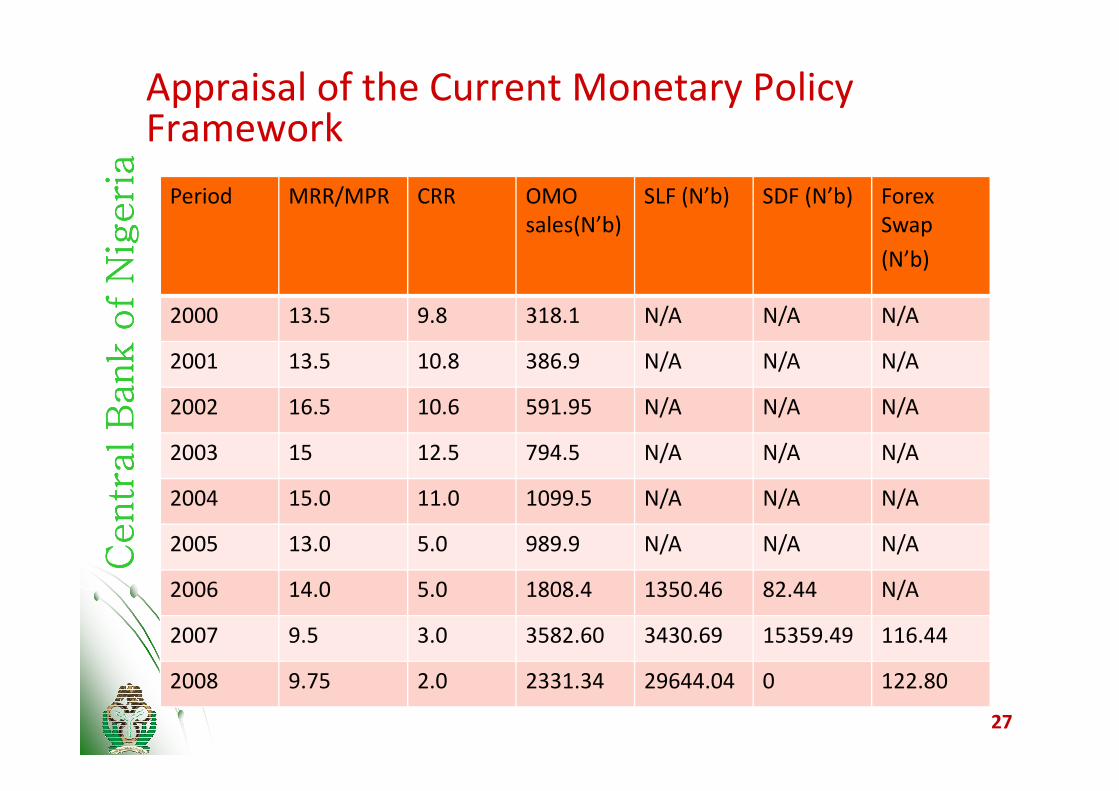

aAppraisal of the Current Monetary Policy Framework

Period MRR/MPR CRR OMO

sales(N’b)

SLF (N’b) SDF (N’b) Forex

Swap

(N’b)

2000 13.5 9.8 318.1 N/A N/A N/A

2001 13.5 10.8 386.9 N/A N/A N/A

2002 16.5 10.6 591.95 N/A N/A N/A

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

2002 16.5 10.6 591.95 N/A N/A N/A

2003 15 12.5 794.5 N/A N/A N/A

2004 15.0 11.0 1099.5 N/A N/A N/A

2005 13.0 5.0 989.9 N/A N/A N/A

2006 14.0 5.0 1808.4 1350.46 82.44 N/A

2007 9.5 3.0 3582.60 3430.69 15359.49 116.44

2008 9.75 2.0 2331.34 29644.04 0 122.80

27

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

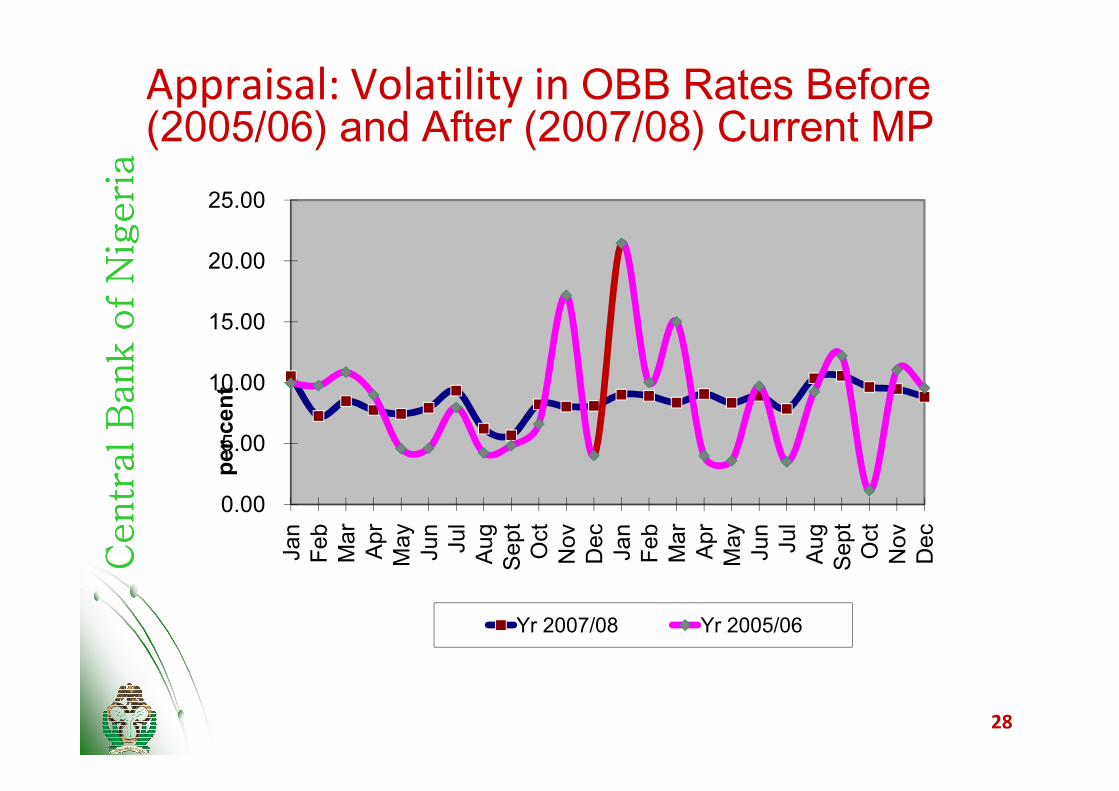

aAppraisal: Volatility in OBB Rates Before (2005/06) and After (2007/08) Current MP

10.00

15.00

20.00

25.00 per cent

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

0.00

5.00

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sept

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sept

Oct

Nov

Dec

per cent

Yr 2007/08 Yr 2005/06

28

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

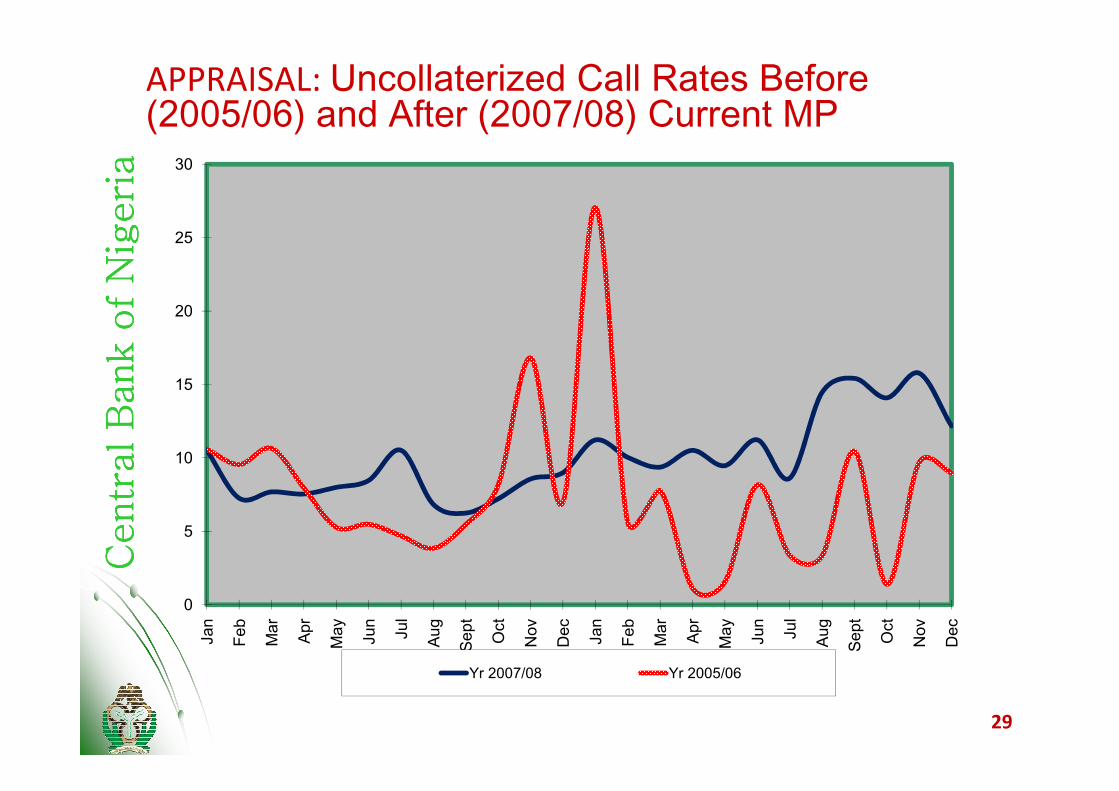

aAPPRAISAL: Uncollaterized Call Rates Before (2005/06) and After (2007/08) Current MP

15

20

25

30

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

0

5

10

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sept

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sept

Oct

Nov

Dec

Yr 2007/08 Yr 2005/06

29

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

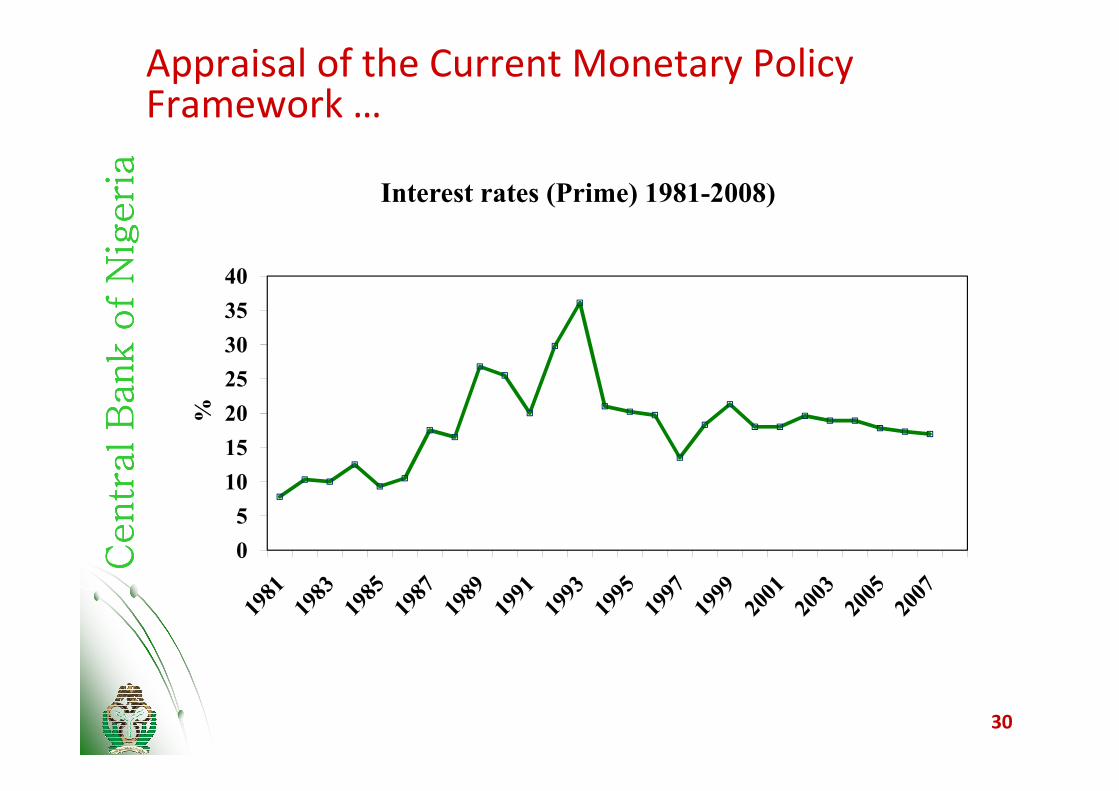

Appraisal of the Current Monetary Policy Framework …

25

30

35

40

Interest rates (Prime) 1981-2008)

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

0

5

10

15

20%

30

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

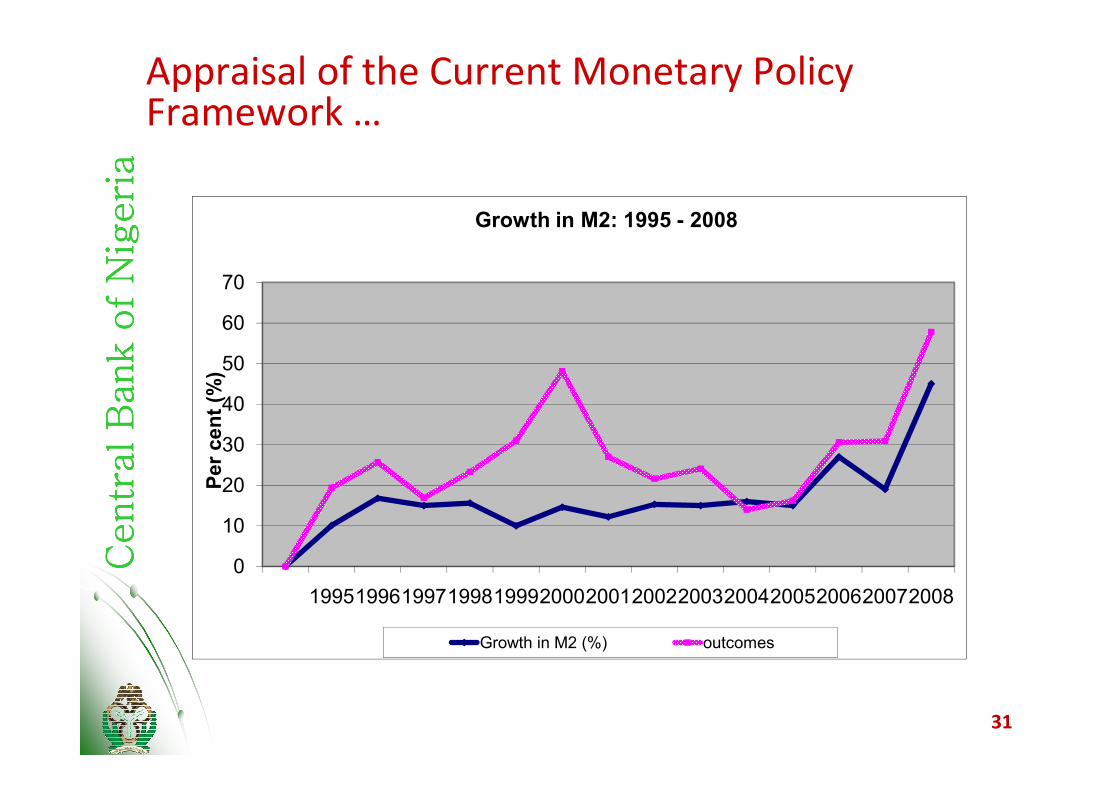

Appraisal of the Current Monetary Policy Framework …

40

50

60

70

Per cent (%)

Growth in M2: 1995 - 2008

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

0

10

20

30

40

19951996199719981999200020012002200320042005200620072008

Per cent (%)

Growth in M2 (%) outcomes

31

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

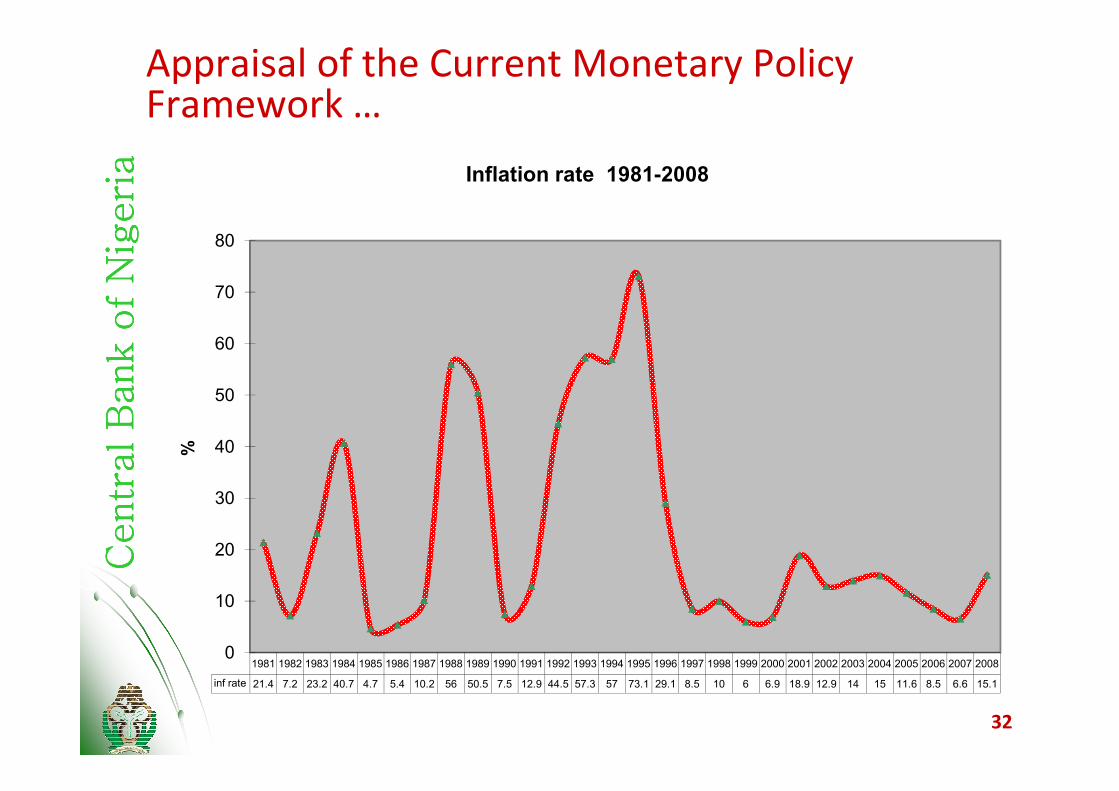

Appraisal of the Current Monetary Policy Framework …

50

60

70

80

Inflation rate 1981-2008

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

inf rate 21.4 7.2 23.2 40.7 4.7 5.4 10.2 56 50.5 7.5 12.9 44.5 57.3 57 73.1 29.1 8.5 10 6 6.9 18.9 12.9 14 15 11.6 8.5 6.6 15.1

0

10

20

30

40

50

%

32

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aAppraisal of the Current Monetary Policy Framework …

�� TheThe useuse ofof MPRMPR providesprovides betterbetter signalsignal ofof

monetarymonetary policypolicy stancestance thanthan whenwhen thethe MRRMRR waswas

usedused..

�� InterInter--bankbank ratesrates areare stabilizingstabilizing

�� DeviationDeviation fromfrom MM22 targettarget inin thethe lastlast fivefive yearsyears

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

�� DeviationDeviation fromfrom MM22 targettarget inin thethe lastlast fivefive yearsyears

havehave moderatedmoderated..

�� InflationInflation ratesrates havehave moderatedmoderated significantlysignificantly inin

relativerelative termsterms

33

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aKey Challenges of Monetary Policy in Nigeria

� Fiscal Dominance

� Relative volatility of the inter-bank rates

� Low Level of Inter-bank Trading and

� Inadequate Infrastructure

Banking Habit is low

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

� Banking Habit is low

� Cost of Liquidity Management

34

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

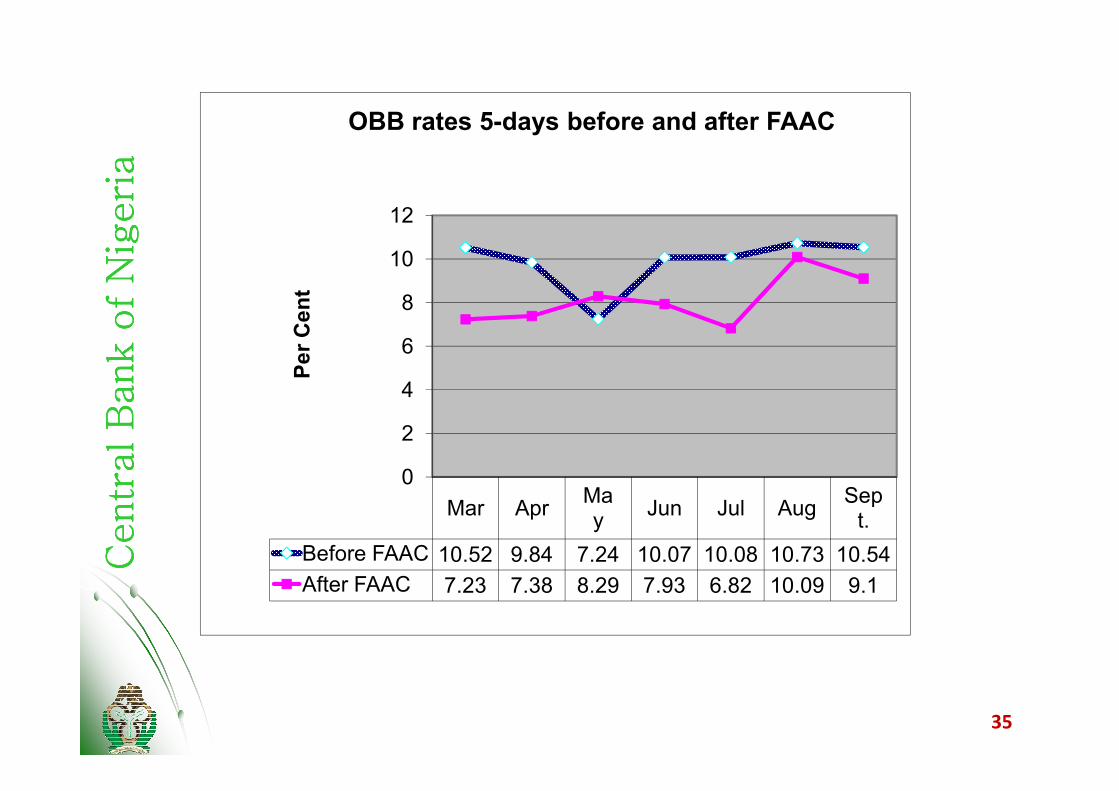

4

6

8

10

12

Per Cent

OBB rates 5-days before and after FAACC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

Mar AprMay

Jun Jul AugSept.

Before FAAC 10.52 9.84 7.24 10.07 10.08 10.73 10.54

After FAAC 7.23 7.38 8.29 7.93 6.82 10.09 9.1

0

2

4

35

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

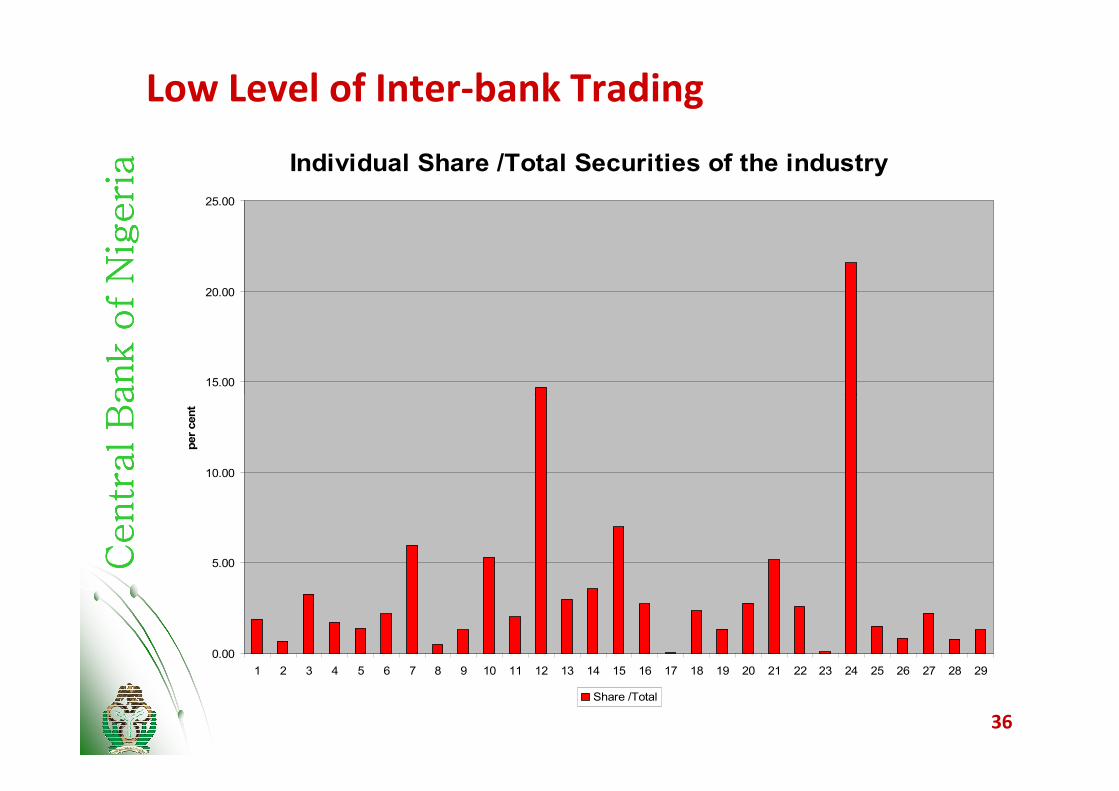

aLow Level of Inter-bank Trading

Individual Share /Total Securities of the industry

15.00

20.00

25.00

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

0.00

5.00

10.00

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29

per cent

Share /Total

36

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aGoing Forward….

� Need for policy harmonization between

monetary and fiscal authorities

� Development of the Financial Infrastructure is

fundamental to efficient and effective monetary

policy

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

policy

� Strengthening of the legal framework

� Enhance Central Bank Independence

� Need to broaden and strengthen regulation and

supervision

37

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aGoing Forward…

� Inflation Targeting……?

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

38

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

Concluding Remarks� This paper presents an overview of monetary policy

framework in Nigeria

� The challenge of monetary policy management rest wholly

on monetary authorities which has over the years been

committed to its effective control

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

� The performance of monetary policy has improved greatly in

recent times- inflation has remained at moderate levels

accompanied by high growth of domestic output

� To sustain the efforts, there is need for appropriate

collaboration with the fiscal authorities as well as the

development of confidence in inter-bank market and the

necessary financial market infrastructure is still relevant 39

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aThanks for Listening

Centr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

aC

entr

al B

ank o

f N

igeri

a

40