moneysmart rookie · web viewthis community educator guide is available under the creative commons...

TRANSCRIPT

MoneySmart RookieCommunity educator guideTopic 2: Credit and debtFinancial literacy for young people

www.teaching.moneysmart.gov.au

Copyright

Copyright information

Website: www.teaching.moneysmart.gov.au

ISBN: 978 0 9805533 9 0.

Creative Commons

This Community educator guide is available under the Creative Commons license (BY - NC - SA). Under this license, the material is available for free use and adaption so that educators can use, adapt and re-publish material from the resource without seeking the permission of ASIC.

Copyright notice

This work is based on materials that constitute copyright of the Australian Securities and Investments Commission and is licensed under a Creative Commons Attribution Non-Commercial Share Alike 2.5 Australia Licence. For an explanation of what this licence allows you to do please refer to the Creative Commons website at http://creativecommons.org.au.

You must include this statement on any adaption of the Community educator guide:

This work is licensed under a Creative Commons Attribution Non-Commercial Share Alike 2.5 Australia Licence (see: http://creativecommons.org/licenses/by-nc-sa/2.5/au/legalcode). A Legal Notice applies to the use of these materials, see: Legal Notice: http://teaching.moneysmart.gov.au/copyright

The material in this Community educator guide is made available for the purpose of providing access to general information about consumer and financial literacy education and is not professional advice. If you intend to rely on the material, you should obtain advice relevant to your particular circumstances to evaluate its accuracy, currency and completeness.

Some material may include or summarise views, standards or recommendations of third parties. ASIC does not endorse such material and its inclusion does not indicate that ASIC recommends any course of action.

ASIC requests that if you re-publish this work that you notify ASIC by email [email protected]. We are interested in hearing how people are using and adapting the materials.

CAL exemption

This Community educator guide is exempt from collection by copyright agencies and is a free resource for educational institutions.

www.teaching.moneysmart.gov.au

1www.teaching.moneysmart.gov.au

Introduction

Introduction

ASIC’s role in financial literacyFinancial literacy is about understanding money and finances and being able to apply that knowledge to make effective decisions.

The Australian Securities and Investments Commission is the Australian Government agency responsible for financial literacy. One of ASIC’s key aims is to have confident and informed consumers and investors.

ASIC’s MoneySmart Rookie education initiativeASIC’s MoneySmart Rookie education initiative helps 16 to 25 year olds avoid expensive mistakes or “rookie errors” when they make their first financial decisions. We want young people transitioning into adulthood to have the motivation and tools to manage their money with confidence.

This education initiative was developed through extensive research and consultation with youth organisations and young people themselves.

TopicsThe MoneySmart Rookie education initiative covers six topics:

Car ownership

Credit and debt

Mobile phone ownership

Moving out of home

Online financial transactions

First job

Who is the Community educator guide for? This Community educator guide is designed for use by youth and community workers, student advisers, mentors and others who assist young people to become aware of their financial decisions and the impact these decisions may have on their lives.

The target audience for activities in this guide is people aged 16 to 25 years of age. Different activities are designed to suit the various levels of knowledge and understanding of participants.

The guide is a flexible learning tool so you can use the parts that are relevant to your participants. There is a logical flow of activities through a topic, but you can use them in any order.

Timing might be affected by:

the needs of the learners

www.teaching.moneysmart.gov.au

Introduction

the setting and context for learning

the time available

The activities and discussions offer young people the opportunity to learn consumer and financial literacy skills using ‘real life’ situations, such as buying a mobile phone, getting a first car and moving out of home.

How to access the MoneySmart Rookie resourcesThe content is structured to suit both young people and educators:

Young people can go directly to the Under 25s section of www.moneysmart.gov.au to see engaging articles, case studies and videos.

For community educators and teachers who are working with young people, additional material is on ASIC’s MoneySmart Teaching website (www.teaching.moneysmart.gov.au):

Teacher lesson plans – assist Year 9 and 10 secondary school teachers to utilise the resources in classroom teaching, and deliver the Australian Curriculum.

Convos – are self-paced online learning activities allowing young people to practice tricky conversations.

Community educator guide [this guide] – has been created to help youth and community workers, student advisers, mentors and others who assist young people to become aware of their financial decisions.

Facilitation optionsThe activities have been designed so that they can be used formally or informally in the following ways:

One-on-one

Participants in pairs

Small groups

Large groups

The facilitator can adapt activities and discussions to suit their learners and context.

www.teaching.moneysmart.gov.au

Introduction

Some general suggestions are provided in the table below:

Participants Activity options

One-on-one Photocopy activity worksheets, individual reflection and discussion with facilitator, sharing individual experiences, insights and challenges with facilitator. If reading skills are required, either the participant or facilitator could read text aloud or review quietly if preferred.

Pairs ‘Buddy’ activity work with photocopied activity worksheets, individual reflection and sharing with each other, sharing individual experiences, insights and challenges with facilitator. If reading skills are required, either the participants or facilitator could read text aloud or review quietly if preferred.

Groups Photocopy activity worksheets, facilitator/participants use whiteboard/butcher’s paper to record activity questions and responses, individual reflection and discussion within small and large groups, sharing individual experiences, insights and challenges with small and large groups. If reading skills are required, one participant per group or the facilitator could read text aloud and individuals could raise hands or point to indicate choices/responses. If writing skills are required, one participant in a group could write down everybody’s ideas.

Complementary resourcesThe activities may be undertaken using this guide and video/s where relevant.

References for further or related MoneySmart Rookie information are included in this guide.

If young people want to explore any of the topics on their own, they can go to the MoneySmart website (www.moneysmart.gov.au) and search for Under 25s.

www.teaching.moneysmart.gov.au

Introduction

Knowledge levelsWhat content will suit your participants? The level of information you use will depend on how much understanding your participants have of a topic. The following describes the content that best suits different levels of understanding (1, 2, and 3):

Your audience has this level of knowledge Description

Level 1: No or a limited understanding

If your participants cannot answer any of your questions or can only answer them a bit, they have no or a limited understanding.

You can help them to understand more by showing the MoneySmart Rookie video for the topic. You can also go through the Level 1 activities in the guide.

After watching the video, see if your participants have developed some understanding of the topic by asking them to answer the questions again.

Level 2: Some level of understanding

If your participants answer one or more of your questions, they have some level of understanding.

You can show them the MoneySmart Rookie video to review the topic.

You may wish to pause the video in sections and discuss key issues shown.

You can also go through the Level 2 activities and stories in the guide, as these are for participants with some level of understanding.

Level 3: Good level of understanding

If your participants are able to answer all of your questions, they have a good level of understanding.

You can show them the MoneySmart Rookie video to review the topic.

You can also go through the Level 2 and 3 activities in the guide, as these are for participants with a good level of understanding.

www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

TOPIC 2:Credit and debt

Activities are arranged so there is a logical flow through the topic, but you can use them in any order you wish.

Activities and resources Level Key messages Pg

A: Understanding credit 4

2.1: Paying for your holiday – is credit the best option?

Level 1 Credit is borrowed money that you have to pay back.

Credit has costs. You pay interest, fees and charges to use credit. Too much credit can cause money problems.

2.2: Chloe’s trick to control her impulse

Level 1

2.3: Amy and Maria make different decisions

Level 2

B: Different types of credit 9

2.4: Tom uses different types of credit

Level 1 There are many different types of credit. Different types of credit are used for different

purposes. Some credit costs more than others. Look for credit that is best for you.

2.5: Tom ends up with repayment problems

Level 2

2.6: Look for credit that is best for you

Level 2

2.7: Different types of credit for different purposes

Level 2

C: Credit contracts 16

2.8: Red-flagging cost items in a credit card offer

Level 2 A contract is a legal agreement. Do not sign anything you do not understand. You may not be able to cancel a contract just

because you change your mind. Get help to understand the contract.

2.9: Asking questions about the red flags

Level 3

2.10: Understanding a contract Level 3

D: Problems with credit 21

1www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

2.11: Chloe makes a rookie error and gets help

Level 2 Get help if you are experiencing financial difficulties.

You may have legal problems by not paying what you owe.

There may be long term effects if you do not pay what you owe.

You may affect your credit rating if you do not meet your financial obligations.

2.12: How Chloe could have ended up with legal problems

Level 2

OverviewThe topic is about how a person can control their use of credit and manage their debt.

It will help young people:

Understand the different types of credit available and the costs involved Understand what their credit rating is Understand how to manage their repayment of debt Know where to go to get help if there is a problem

Reflection questionsAt the end of each session, educators can use the following questions to reflect on the effectiveness of the session:

What worked well? What did not work well? Did the participants understand the key messages? Did the activity engage the participants? How could the activity have been more effective? What questions unexpectedly emerged and how did you handle them? What might you do differently next time?

More information for your participantsFor more information or to search for words you don’t understand, go to the MoneySmart website (www.moneysmart.gov.au) and search for Under 25s.

Knowledge levels Ask these types of questions to check the participants’ existing level of knowledge about credit. Ask the participants to explain the following:

2www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

What types of credit are available to people? What kinds of costs do you have to pay when you get credit? What is meant by a person’s “credit rating”?

Decide what information they need based on their level of knowledge. Use the table below to help you.

Your participants has this level of knowledge Description and suitable activities

Level 1:No or a limited understanding

If your participants cannot answer any of your questions or can only answer them a bit, they have no or a limited understanding.

You can help them to understand more by showing the MoneySmart Rookie: Credit hangover video. You can also go through the Level 1 activities in the guide.

After watching the video, see if your participants have developed some understanding of the topic by asking them to answer the questions again.

Level 2:Some level of understanding

If your participants answer one or more of your questions, they have some level of understanding.

You can show them the MoneySmart Rookie: Credit hangover video to review the topic.

You may wish to pause the video in sections and discuss key issues shown.

You can also go through the Level 2 activities and stories in the guide, as these are for participants with some level of understanding.

Level 3:Good level of understanding

If your participants are able to answer all of your questions, they have a good level of understanding.

You can show them the MoneySmart Rookie: Credit hangover video to review the topic.

You can also go through the Level 2 and 3 activities in the guide, as these are for participants with a good level of understanding.

3www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

A: Understanding credit

Key messages: Credit is borrowed money that you have to pay back Credit has costs You pay interest, fees and charges to use credit Too much credit can cause money problems

Content for the educatorCredit is money you borrow from a financial institution like a bank, credit union or building society.

Credit has a cost; it isn’t your personal money tree growing in the backyard. Any credit you use becomes a debt that must be repaid to the credit provider – usually with interest included.

Interest is an extra amount you have to pay as a cost for borrowing the credit provider’s money. This cost is added to the original amount of money you borrowed.

Many retailers offer interest-free deals but the purchase is only interest-free for a certain period of time which is often 12 to 24 months. If the purchase balance is not paid in full within the interest-free period, interest will be charged on the outstanding amount at a high interest rate.

Before you start looking for credit, do a budget – and make sure you only borrow what you can afford to pay back so you don’t end up with money problems.

The amount you can afford to borrow will depend on a number of factors such as:

Your income Your expenses Estimated repayments

You’ll see the expression ‘fees and charges’ used a lot. They’re really the same thing – amounts of money you’ve got to pay in addition to interest (e.g. an amount you pay each year just to have your credit card, whether you use it or not).

Activities and stories2.1 Level 1: Paying for your holiday – is credit the best option?

2.2 Level 1: Chloe’s trick to control her impulse

2.3 Level 2: Amy and Maria make different decisions

4www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

Activity 2.1Paying for your holiday – is credit the best option? (Level 1)

This activity is only available online: http://www.teaching.moneysmart.gov.au/resource-centre/moneysmart-rookie

The participants interact with their friend in a text and audio simulated conversation. The participants receive feedback on their choices, such as the questions they choose to ask. The participants can go back to change their actions.

The conversational tool supports the participants to develop confidence when deciding if credit is the best option for them. It also highlights what to do if the young person is experiencing financial difficulty.

This activity is aimed at Level 1, but can be undertaken by all levels and should take approximately 10 to 20 minutes.

Activity 2.2Chloe’s trick to control her impulse (Level 1)This activity is based on the MoneySmart Rookie: Credit hangover video. It will help to motivate the participants to consider how attitudes and behaviour affect a person’s use of credit.

Step one

Cue the MoneySmart Rookie: Credit hangover video for the participants to watch.

Ask the participants to watch the video from start to finish and look out for any tips on controlling spending habits.

Step two

Ask the participants the following question:

1 What tip did future Chloe give to her present self to try and get her spending habits under control?

Suggested answer

2 Future Chloe suggests that, for every $100 Chloe wants to spend, she should wait a day before she goes ahead and buys something.

Step three

Ask the participants the following question:

3 Can you think of any other tricks or methods people could try in order to keep a check on their spending?

Educator note: This requires more analytical thought by the participants. Some participants may come up with ideas of their own. Other participants may be able to remember tricks or methods used by family or friends.

5www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

Suggested answer

4 There could be many different ways but if the participants cannot think of any, prompt them by suggesting:

going to another shop to compare prices before you buy setting a budget for non-essential items setting aside money they can spend on certain items and not spending more than that

amount.

Activity 2.3Amy and Maria make different decisions (Level 2) This activity builds on Activity 2.2.

Pre-task preparation

Photocopy the stories of two people from page 31.

Step one

Introduce the two people to the participants by reading out or showing them copies of their self-introductions below.

Amy Maria

Hi, I’m Amy. I hate waiting for things so when I decide on something I want, I want it now! Like this laptop I bought last week for $599. I can use a computer at the library but it’s so much more convenient having your own laptop. I signed up for an interest free deal at the store and there’s 0% interest for 12 months. I probably won’t be able to pay it off within 12 months, but I’ll just worry about the high interest rates later, when the 12 months is up.

Hi, I’m Maria. People tell me I take ages to do things but it’s because I like to really think before I act when it comes to big decisions. Take this laptop I bought last week for $599. I figured out how much I needed to save to buy the model I wanted about a year ago and I put away a bit of money each week until I could afford to buy it. The laptop I wanted wasn’t on the market anymore but I ended up getting a newer model for the same price. It was a hassle not having my own laptop for so long but it was worth the wait.

Ask the participants the following questions:

5 How would you describe Amy’s personality?6 How would you describe Maria’s personality?7 What are the pros and cons of Amy’s situation?8 What are the pros and cons of Maria’s situation?9 Who do you think is making the better financial decision? Why?

Suggested answers

10 Impatient, hasty, a bit reckless.

6www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

11 Slow, thoughtful, careful, cautious, pretty sensible.12 Pros:

Amy gets her laptop sooner.Amy doesn’t have to pay interest for 12 months.

Cons:Amy can’t afford to pay off the laptop within 12 months.Amy has to pay high interest rates if she does not pay off the laptop in 12 months.Amy might have to pay a lot more for the laptop than if she bought it outright.

13 Pros:Maria does not have to pay high interest rates for her laptop.Maria got a better and newer model laptop than she originally planned.

Cons:Maria didn’t save up enough money in time for the model she wanted.Maria had to wait 12 months before she could get the laptop.

14 Maria is making the better financial decision, because she does not have to pay more than $599 for the laptop.

Check for understanding After completing the activities, you can check the participants’ level of understanding and knowledge by asking questions such as:

What is credit?A: Credit is money you borrow from a financial institution like a bank, credit union or building society.

When you get something on credit, what extra money do you have to pay on top of paying back the amount you borrowed?A: Interest is an extra amount you have to pay as a cost for borrowing the credit provider’s money. This cost is added to the original amount of money you borrowed.

Do the participants understand the key points?

If they do not, you can go through the information again at another time. If they do, they have met the learning objectives.

Do the participants have a better understanding?

Result Next steps

Your participants have a higher level of understanding – they comprehensively understand credit.

Good work! Next time you meet you can do the next topic.

Your participants have some level of understanding of credit.

You can work through the activities again with your participants.

Your participants have no or limited understanding of credit.

Watch the MoneySmart Rookie: Credit hangover video and go through the

7www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

Level 1 activities again.

Reflection questionsReflect on the effectiveness of this session by considering the questions included at the start of this topic.

For more information or to search for words you don’t understand, go to the MoneySmart website (www.moneysmart.gov.au) and search for Under 25s.

8www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

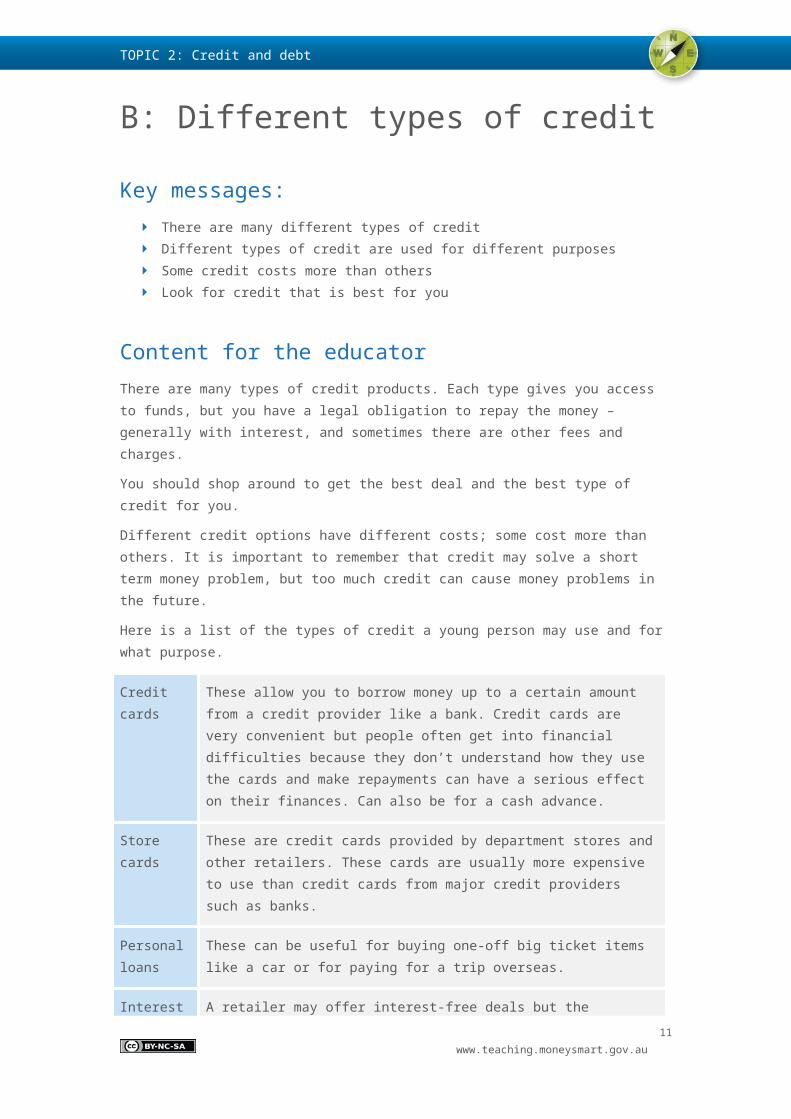

B: Different types of credit

Key messages: There are many different types of credit Different types of credit are used for different purposes Some credit costs more than others Look for credit that is best for you

Content for the educatorThere are many types of credit products. Each type gives you access to funds, but you have a legal obligation to repay the money – generally with interest, and sometimes there are other fees and charges.

You should shop around to get the best deal and the best type of credit for you.

Different credit options have different costs; some cost more than others. It is important to remember that credit may solve a short term money problem, but too much credit can cause money problems in the future.

Here is a list of the types of credit a young person may use and for what purpose.

Credit cards These allow you to borrow money up to a certain amount from a credit provider like a bank. Credit cards are very convenient but people often get into financial difficulties because they don’t understand how they use the cards and make repayments can have a serious effect on their finances. Can also be for a cash advance.

Store cards These are credit cards provided by department stores and other retailers. These cards are usually more expensive to use than credit cards from major credit providers such as banks.

Personal loans

These can be useful for buying one-off big ticket items like a car or for paying for a trip overseas.

Interest-free deals

A retailer may offer interest-free deals but the purchase is interest-free only for a certain period of time.

Home loans These are generally used to buy a house or block of land.

Small amount loans

A small amount loan may be used to meet expenses until your next pay. Loans are for a small amount (less than $2,000) and must be repaid on a set date. This is usually in less than a year.

Consumer lease

This is an arrangement where you rent an item (e.g. a home computer or television) over a period of time. You don’t have the right or option to purchase the item. The

9www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

total amount you pay will be more than if you paid for the item with cash. You may also have to pay fees and charges.

Rent to buy This is an arrangement where you can choose to purchase the item after renting it for a certain period of time or you could continue to rent it.

There are two different types of loans – secured loans and unsecured loans. The difference depends on how much risk there is that the borrower might not pay the loan back to the lender.

With a secured loan the credit provider holds security over one or more of your assets to make sure they get their money back. It protects the lender from losing their money.

With an unsecured loan the credit provider may decide that there is not a lot of risk and so they do not need to hold an item as security. The interest rate for unsecured loans is usually higher than for a secured loan.

Activities and stories2.4 Level 1: Tom uses different types of credit

2.5 Level 2: Tom ends up with repayment problems

2.6 Level 2: Look for credit that is best for you

2.7 Level 2: Different types of credit for different purposes

Activity 2.4Tom uses different types of credit (Level 1)This activity uses Tom’s story as an example for the participants to think about the different kinds of credit.

Pre-task preparation

Photocopy story from page 32.

Step one

Read out the following story.

Tom’s story:

Tom got into the course of his dreams but he needed to buy a computer and arrange internet access to be able to do the course. Also, he had to travel a long way to classes and there was no public transport there from his house. So, he applied for a personal loan to buy a second-hand car.

He got a credit card to pay for the computer and he signed up for a 24 month internet contract. Now he’s six months into his course and he has financial troubles. He is managing to keep up with his personal loan repayments but he doesn’t have much money left over for the credit card repayments and the internet bills, which are both now three months overdue.

10www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

Step two

Ask the participants the following question:

15 What are the different types of credit or service plans Tom got to help him study?

Suggested answers

16 Credit cardPersonal loanInternet contract

Activity 2.5Tom ends up with repayment problems (Level 2) This activity builds on Activity 2.4.

It uses Tom’s story as an example for the participants to think about the importance of a person’s credit rating.

Pre-task preparation

Photocopy story from page 33.

Step one

Read out the following information that is on the same sheet as Tom’s story.

Credit rating:

A credit reporting agency will have a credit report on you if you have:

Applied for a personal loan or credit card in the past 5 years Signed a mobile phone contract Paid a bill of as little as $100, at least 60 days late

Credit providers use credit reports to help them decide whether to provide a person with credit. If the credit report reveals a poor history of repayment, they’ll consider you a higher credit risk. The credit provider may not lend you any money if you are considered too high a credit risk.

Ask the participants the following questions:

17 What would help Tom receive a good credit rating in this situation?18 What are the benefits for Tom in the future by getting a good credit rating?19 What would cause Tom to get a bad credit rating in this situation?20 What kinds of problems will a bad credit rating cause Tom in the future?

Suggested answers

21 By paying his personal loan repayments on time22 It shows future credit providers that he can be financially responsible, so it makes it easier for

him to get a loan or get a mortgage to buy a house in the future.23 Not paying his credit card repayments and internet bills on time.

11www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

24 He may not be able to get a loan or a mortgage for a house in the future, because he may get a record of not keeping up with loan repayments and being financially responsible.

Activity 2.6Look for credit that is best for you (Level 2) This activity builds on Activity 2.5.

It asks the participants to think about what they’ve learned in this session and to apply it with what they already know. By focussing on avoiding repayment problems, the participants will be helped to realise that it’s important to “Look for credit that is best for you”.

Ask the participants the following question:

25 How can people avoid getting into repayment problems?

Suggested answers

26 By not allowing their debt to get too big.By allowing for unexpected events (e.g. a drop in income, sudden health expenses).By allowing for an unexpected increase in expenses.By choosing credit that is best for you in your situation.

Round off the activity by pointing out that “Looking for credit that is best for you” is really important, because different types of credit suit people in different situations. Sometimes no credit at all is the best option.

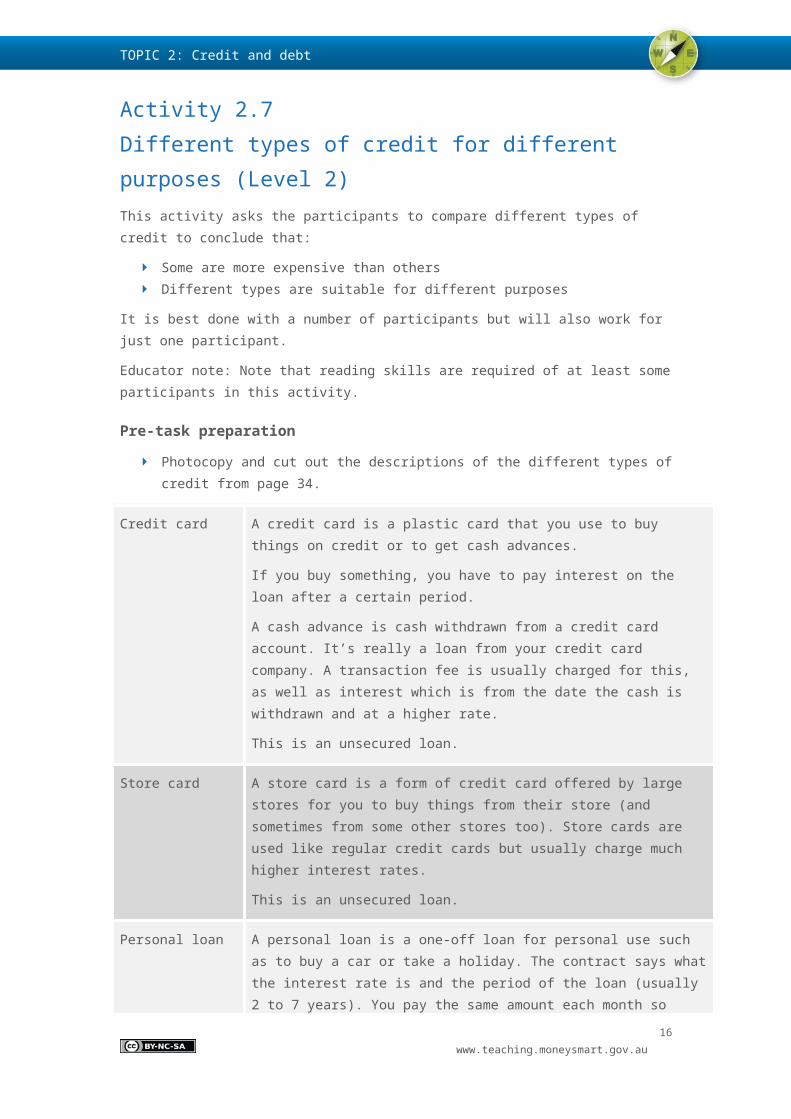

Activity 2.7Different types of credit for different purposes (Level 2) This activity asks the participants to compare different types of credit to conclude that:

Some are more expensive than others Different types are suitable for different purposes

It is best done with a number of participants but will also work for just one participant.

Educator note: Note that reading skills are required of at least some participants in this activity.

Pre-task preparation

Photocopy and cut out the descriptions of the different types of credit from page 34.

Credit card A credit card is a plastic card that you use to buy things on credit or to get cash advances.

If you buy something, you have to pay interest on the loan after a certain period.

A cash advance is cash withdrawn from a credit card account. It’s really a loan from your credit card company. A transaction fee is usually charged for this, as well as

12www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

interest which is from the date the cash is withdrawn and at a higher rate.

This is an unsecured loan.

Store card A store card is a form of credit card offered by large stores for you to buy things from their store (and sometimes from some other stores too). Store cards are used like regular credit cards but usually charge much higher interest rates.

This is an unsecured loan.

Personal loan A personal loan is a one-off loan for personal use such as to buy a car or take a holiday. The contract says what the interest rate is and the period of the loan (usually 2 to 7 years). You pay the same amount each month so that, by the end of the loan period, the total amount has been paid back (including interest).

A personal loan can be secured or unsecured.

Secured loan A loan for which an asset of yours has been used as security. An ‘asset’ is something you already own – such as your car or your home. The credit provider may sell the secured asset to get its money back if you can’t repay the loan.

Unsecured loan A loan for which no asset has been used as security. An ‘asset’ is something you already own – such as your car or your home. The interest rate is usually higher than for a secured loan as there is a higher risk to the credit provider of not getting their money back.

Step one

Divide participants into five groups. Give each group a description of one type of credit to review. Ask which group has ‘Secured loan’ and ask for one person in that group to explain the type of credit in their own words. They may need help with this and you may need to make sure the people listening understand what they hear.

Step two

Ask which group has ‘Unsecured loan’ and ask for one person in that group to explain the type of credit in their own words. They may need help with this and you may need to make sure the people listening understand what they hear.

Step three

Ask the participants the following question:

27 What’s the difference between a ‘secured loan’ and an ‘unsecured loan’?

Suggested answers

28 A ‘secured loan’ is a loan for which an asset of yours has been used as security. An ‘asset’ is something you already own – such as your car or your home. The credit provider may sell the secured asset to get its money back if you can’t repay the loan.

13www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

An ‘unsecured loan’ is a loan for which no asset has been used as security. An ‘asset’ is something you already own – such as your car or your home. The interest rate is usually higher than for a secured loan as there is a higher risk to the credit provider of not getting their money back.

Step four

Ask one person in each of the remaining groups to explain the type of credit in their own words. They may need help with this and you may need to make sure the people listening understand what they hear.

Step five

Ask the participants the following question:

29 What’s one difference between a credit card and a store card?

Suggested answers

30 A store card can often only be used to buy things in the store you got the card from, and sometimes other stores. The interest rate is usually higher. This means it’s more expensive.

Step six

Ask the participants the following question:

31 Which type of credit would be best for each of the following?a Buying a pair of shoesb Buying a car

Suggested answers

32 a Credit card or store cardb Personal loan

Educator note: If store card is suggested, point out that the interest rate will probably be higher and that it would be a good idea to check the fees and charges and compare them with credit cards.

Check for understanding After completing the activities, you can check the participants’ level of understanding and knowledge by asking questions such as:

What are some of the different types of credit?A: Credit cards, store cards, personal loan, home loans, small amount loans.

How are different types of credit used?A: Different types of credit can be used for homes, cars or other purchases.

How can having credit cause you financial problems?A: Too much credit can cause financial problems if you can’t pay back your debts.

Do the participants understand the key points?

If they do not, you can go through the information again at another time. If they do, they have met the learning objectives.

14www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

Do the participants have a better understanding?

Result Next steps

Your participants have a higher level of understanding – they comprehensively understand different types of credit.

Good work! Next time you meet you can do the next topic.

Your participants have some level of understanding of different types of credit.

You can work through the activities again with your participants.

Your participants have no or a limited understanding of different types of credit.

Watch the MoneySmart Rookie: Credit hangover video and go through the Level 1 activities again.

Reflection questionsReflect on the effectiveness of this session by considering the questions included at the start of this topic.

For more information or to search for words you don’t understand, go to the MoneySmart website (www.moneysmart.gov.au) and search for Under 25s.

15www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

C: Credit contracts

Key messages: A contract is a legal agreement Do not sign anything you do not understand You may not be able to cancel a contract just because you change your mind Get help to understand the contract

Content for the educatorWhen you get credit, you will need to sign a credit contract. A contract is a legal agreement of what it says. Before you sign up for credit you should read the contract and make sure you can afford the repayments. It’s essential to know what you’re signing up for, whom you’re getting the credit from, and how they are charging you. You do not want to end up with a poor credit rating.

When you sign up for credit, you are committing to a contract between you and the credit provider. A contract is a legal agreement and you have to take it seriously. You may not be able to cancel it – it depends on the detail of the contract and the circumstances.

If you don’t understand everything in a contract, or you’re not sure about how a contract suits your situation, get advice from someone who can help.

Activities and stories2.8 Level 2: Red-flagging cost items in a credit card offer

2.9 Level 3: Asking questions about the red flags

2.10 Level 3: Understanding a contract

Activity 2.8Red-flagging cost items in a credit card offer (Level 2)This activity is based on the video MoneySmart Rookie: Credit hangover. It will help the participants avoid rookie errors when considering the use of credit.

It will also help people think through whether they should accept a particular credit option.

Pre-task preparation

Photocopy and cut out (one copy per participant) the Credit card special offer advertisement from page 35.

Step one

Cue the MoneySmart Rookie: Credit hangover video for the participants to watch.

16www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

Step two

Before the participants watches the video, ask the participants the following question:

33 Suppose you buy something on credit for $2,000 and the interest rate is 18.5%, and you pay back $50 each month. Guess the total amount of interest you will pay while you’re paying back that $2,000?

Educator note: If the participants needs some guidance, you could give them the following amounts to choose from:

a $300b $600c $900d $1,200

Encourage the participants to suggest an amount but don’t give them the correct answer – let them discover it for themselves by watching the video.

Step three

After watching the video, ask the participants the following question:

34 What is the amount of interest you would pay back?

Answer

35 Approximately $1,200

Step four

Hand out the copies of the Credit card special offer advertisement.

Ask the participants the following questions:

36 What parts or words in the contract should Chloe have asked questions about before signing up for the credit card?

37 Draw a red flag over words that you need to be careful of or do not understand (or call out if there should be a red flag as you read out the content of the advertisement).

Suggested answers

38 Need to add the words in once we get the activity sheet39 The following should be flagged:

0% interest on all purchases for the first 6 months* Low interest for purchases No annual fee for first year Reward points *Does not apply to cash advances

17www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

Activity 2.9Asking questions about the red flags (Level 3)This activity builds on Activity 2.8.

Step one

Ask the participants the following question:

Once the ‘red flags’ for Chloe have been identified:

40 For each ‘red flag’, what question do you think Chloe should have asked the credit provider or done further research on before signing up for the credit card?

Suggested answers

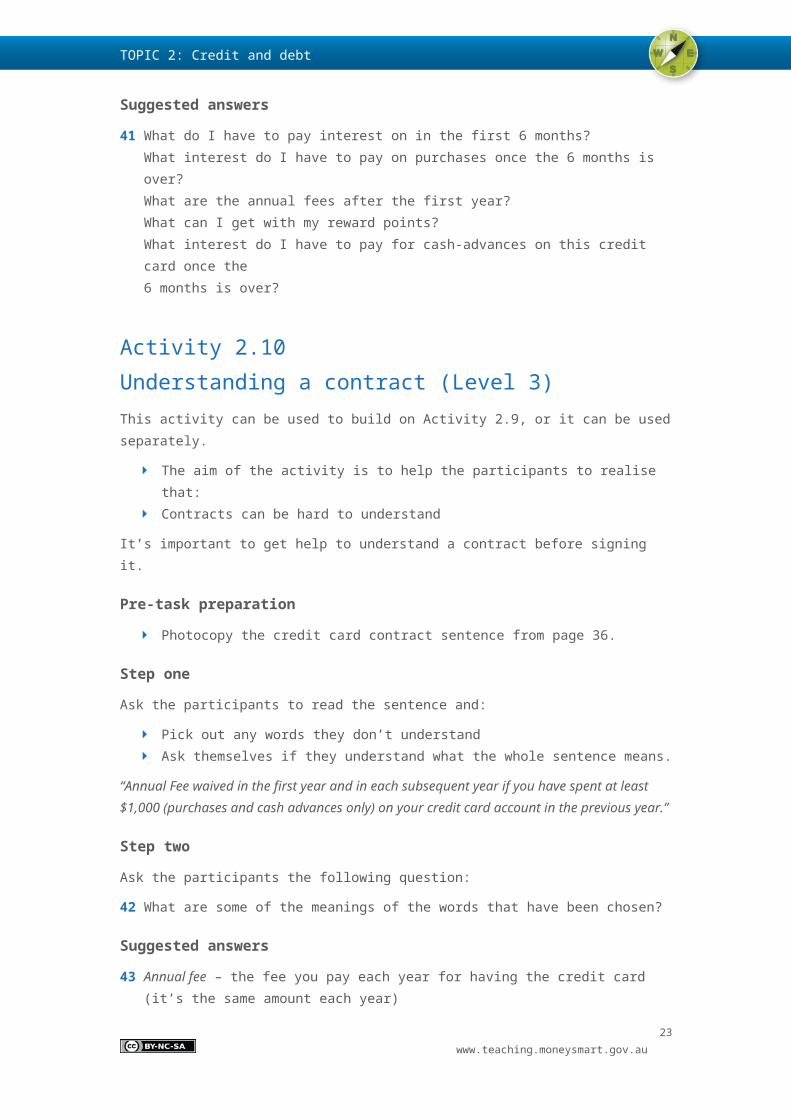

41 What do I have to pay interest on in the first 6 months?What interest do I have to pay on purchases once the 6 months is over?What are the annual fees after the first year?What can I get with my reward points?What interest do I have to pay for cash-advances on this credit card once the 6 months is over?

Activity 2.10Understanding a contract (Level 3)This activity can be used to build on Activity 2.9, or it can be used separately.

The aim of the activity is to help the participants to realise that: Contracts can be hard to understand

It’s important to get help to understand a contract before signing it.

Pre-task preparation

Photocopy the credit card contract sentence from page 36.

Step one

Ask the participants to read the sentence and:

Pick out any words they don’t understand Ask themselves if they understand what the whole sentence means.

“Annual Fee waived in the first year and in each subsequent year if you have spent at least $1,000 (purchases and cash advances only) on your credit card account in the previous year.”

Step two

Ask the participants the following question:

42 What are some of the meanings of the words that have been chosen?

18www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

Suggested answers

43 Annual fee – the fee you pay each year for having the credit card (it’s the same amount each year)

Waive – to put something aside (in this case, it means the annual fee won’t be charged)

Subsequent – the one that comes next

Purchases – things you pay for using your card

Cash advances – cash that you get using your credit card (e.g. from an ATM)

Previous – the one that came before

The whole sentence – In the first year you have the credit card, you won’t have to pay the annual fee. If you spend at least $1,000 in the first year using your credit card, you won’t have to pay the annual fee in the second year. And so on. You can spend $1,000 by paying for things with your card or using your card to get a cash advance.

Step three

Point out that each contract has a lot of sentences, which means that a contract can be difficult to understand.

Point out that a contract is a legal agreement – which means you have legal obligations if you sign one. An example of a legal obligation is meeting your repayments on time. Not meeting legal obligations can create legal problems for you.

Ask the participants the following question:

44 What would you do if you didn’t understand a contract?

Suggested answers

45 Never sign a contract if you don’t understand it.Always ask questions if you’re not sure about something. Don’t rely on the credit provider to explain it.

Step four

Ask the participants the following question:

46 Who could you ask to help explain the contract to you?

Suggested answers

47 ParentOther relativeA free financial counsellor Teacher or youth group person (or similar)Friend

Emphasise the importance of asking more than one person if necessary until you understand.

19www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

Check for understandingAfter completing the activities, you can check the participants’ level of understanding and knowledge by asking questions such as:

What are some of the things to check or ask about in an advertisement? A: Interest rate for purchasesInterest rate for cash advancesFeesAny periods that are ‘free’ of interest or fees

What does an asterisk (*) mean in an advertisement? A: It means there is more information about that point somewhere in the advertisement (usually at the bottom).

Do the participants understand the key points?

If they do not, you can go through the information again at another time. If they do, they have met the learning objectives.

Do the participants have a better understanding?

Result Next steps

Your participants have a higher level of understanding – they completely understand credit contracts.

Good work! Next time you meet you can do the next topic.

Your participants have some level of understanding of credit contracts.

You can work through the activities again with your participants.

Your participants have no or limited understanding of credit contracts.

Watch the MoneySmart Rookie: Credit hangover video and go through the Level 1 activities again.

Reflection questionsReflect on the effectiveness of this session by considering the questions included at the start of this topic.

For more information or to search for words you don’t understand, go to the MoneySmart website (www.moneysmart.gov.au) and search for Under 25s.

20www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

D: Problems with credit

Key messages: Get help if you are experiencing financial difficulties You may have legal problems by not paying what you owe There may be long term effects if you do not pay what you owe You may affect your credit rating if you do not meet your financial obligations

Content for the educatorIt’s important to get help if you are experiencing financial difficulties.

If you fail to repay your loans or credit card debts, your credit rating may be affected which may make it difficult to borrow money in the future.

A credit reporting agency will have a credit report on a person if the person has:

Applied for credit in the past 5 years Paid a bill (for utilities, a mobile phone or the internet) or made a repayment on credit at least

60 days late (that debt can be as little as $100)

Credit providers use credit reports to help them decide whether to provide a person with credit. If the credit report reveals a poor history of repayment, they’ll consider you a credit risk and may not lend you the money.

Failing to repay debts can have long term effects. A poor credit rating can take some time to fix. You may also have legal problems by not repaying what you owe.

You have options available if you are having difficulty making repayments. Contact your credit provider without delay to see how they can help you. For example, you could negotiate an agreed repayment plan until your debt is paid off. A free financial counsellor can help you with this negotiation.

If your circumstances change, you may be able to ask your credit provider for a ‘hardship variation’. For example, you may not be able to make your repayments due to temporary illness or unemployment. A hardship variation means the credit provider can agree to change the way you make repayments to make them more affordable for your situation.

You do not have to go it alone; there are free financial counselling and legal services available to help.

Activities and stories2.11 Level 2: Chloe makes a rookie error and gets help

2.12 Level 2: How Chloe could have ended up having legal problems

21www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

Activity 2.11Chloe makes a rookie error and gets help (Level 2)This activity is based on the MoneySmart Rookie: Credit hangover video. It will help the participants think about ways credit can cause problems, and how they can get help.

Step one

Cue the MoneySmart Rookie: Credit hangover video for the participants to watch.

Ask the participants to watch the video from start to finish and look out for Chloe’s rookie error.

Step two

Ask the participants the following questions:

48 What rookie error did Chloe make?49 What problems did that rookie error cause future Chloe?50 Who did Chloe end up going to for help and how did they help her?

Suggested answers

51 Chloe signed up for a car loan and lots of different credit cards and spent too much money on them. She ended up $20,000 in debt.

52 Chloe had trouble paying off all her credit cards and ended up with a bad credit rating, so it made it hard for her to get a home loan in future. She is still paying off her credit cards so she has less money to live on than before.

53 She went to a financial counsellor who helped her set up a budget and a repayment plan so she can pay off her debts bit by bit.

Educator note: Most young people won’t know what a ‘financial counsellor’ is. It is suggested that you use the following information to explain.

A financial counsellor is a person who “gives free, confidential and independent assistance to people with financial problems. Financial counselling services are usually provided by community or welfare organisations”.

The local council where a person lives may be able to suggest a local organisation that provides financial counselling services. If the young person is confident enough, they can call the Financial Counselling hotline on 1800 007 007 to speak to a financial counselling service in their area.

A financial counsellor can help a person make a budget or help them negotiate with a financial institution, company or a debt collector for more time to pay or a repayment plan that the young person can afford. Financial counsellors are free and young people can find their local service at www.moneysmart.gov.au.

If a company takes a young person to court for a debt, the young person should contact a lawyer from a local community legal centre for free legal advice. To find their local community legal centre, young people can contact the National Association of Community Legal Centres at www.naclc.org.au

22www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

Activity 2.12How Chloe could have ended up with legal problems (Level 2)This activity builds on Activity 2.11.

It is based on the MoneySmart Rookie: Credit hangover video. It will help the participants understand that there can be legal consequences if they do not pay what they owe.

Educator note: If time has passed since the participants did Activity 2.11, you will need to remind them of the story in the video or watch it again.

Step one

Cue the MoneySmart Rookie: Credit hangover video for the participant to watch.

Ask the participants the following question:

54 What could have happened to Chloe if she had not contacted a financial counsellor to arrange a repayment plan with the credit provider?

Suggested answer

55 If Chloe fell further and further behind with her repayments and she didn’t contact the credit provider about it, the credit provider may organise a debt collector to contact Chloe about repaying the debt. She would probably end up with a bad credit rating and the default on her loan would most likely be listed in her credit report.

Step two

Ask the participants the following question:

56 What legal problems could Chloe then end up with?

Suggested answer

57 The credit provider could take legal action to try to get the money from Chloe and/or take back what she had bought. Chloe’s bad credit rating could cause other credit providers to refuse her credit in future.

Check for understandingAfter completing the activities, you can check the participants’ level of understanding and knowledge by asking questions such as:

What sort of situation can lead to problems paying back credit?A: Too much creditA decrease in income Unexpected expenses

Where can you go for help?A: Financial counsellor

23www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt

Do the participants understand the key points?

If they do not, you can go through the information again at another time. If they do, they have met the learning objectives.

Do the participants have a better understanding?

Result Next steps

Your participants have a high level of understanding – they comprehensively understand where to get help if they are having financial difficulties.

Good work! Next time you meet you can do the next topic.

Your participants have some level of understanding of where to get help if they are having financial difficulties.

You can work through the activities again with your participants.

Your participants have no or limited understanding of where to get help if they are having financial difficulties.

Watch the MoneySmart Rookie: Credit hangover video and go through the Level 1 activities again.

Reflection questionsReflect on the effectiveness of this session by considering the questions included at the start of this topic.

For more information or to search for words you don’t understand, go to the MoneySmart website (www.moneysmart.gov.au) and search for Under 25s.

24www.teaching.moneysmart.gov.au

TOPIC 2:Credit and debt activity worksheets

TOPIC 2: Credit and debt activity worksheets

A: Understanding credit

Activity 2.3 Amy and Maria make different decisions (Level 2)

Amy Maria

Hi, I’m Amy. I hate waiting for things so when I decide on something I want, I want it now! Like this laptop I bought last week for $599. I can use a computer at the library but it’s so much more convenient having your own laptop. I signed up for an interest free deal at the store and there’s 0% interest for 12 months. I probably won’t be able to pay it off within 12 months, but I’ll just worry about the high interest rates later, when the 12 months is up.

Hi, I’m Maria. People tell me I take ages to do things but it’s because I like to really think before I act when it comes to big decisions. Take this laptop I bought last week for $599. I figured out how much I needed to save to buy the model I wanted about a year ago and I put away a bit of money each week until I could afford to buy it. The laptop I wanted wasn’t on the market anymore but I ended up getting a newer model for the same price. It was a hassle not having my own laptop for so long but it was worth the wait.

Questions

58 How would you describe Amy’s personality?

59 How would you describe Maria’s personality?

60 What are the pros and cons of Amy’s situation?

61 What are the pros and cons of Maria’s situation?

62 Who do you think is making the better financial decision? Why?

26www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt activity worksheets

B: Different types of credit

Activity 2.4 Tom uses different types of credit (Level 1)Tom got into the course of his dreams but he needed to buy a computer and arrange internet access to be able to do the course. Also, he had to travel a long way to classes and there was no public transport there from his house. So, he applied for a personal loan to buy a second-hand car.

He got a credit card to pay for the computer and he signed up for a 24 month internet contract. Now he’s six months into his course and he has financial troubles. He is managing to keep up with his personal loan repayments but he doesn’t have much money left over for the credit card repayments and the internet bills, which are both now three months overdue.

Questions

63 What are the different types of credit or service plans Tom got to help him study?

27www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt activity worksheets

B: Different types of credit

Activity 2.5 Tom ends up with repayment problems (Level 2)A credit reporting agency will have a credit report on you if you have:

Applied for a personal loan or credit card in the past 5 years Signed a mobile phone contract Paid a bill of as little as $100, at least 60 days late

Credit providers use credit reports to help them decide whether to provide a person with credit. If the credit report reveals a poor history of repayment, they’ll consider you a higher credit risk. The credit provider may not lend you any money if you are considered too high a credit risk.

Questions

64 What would help Tom receive a good credit rating in this situation?

65 What are the benefits for Tom in the future by getting a good credit rating?

66 What would cause Tom to get a bad credit rating in this situation?

67 What kinds of problems will a bad credit rating cause Tom in the future?

28www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt activity worksheets

B: Different types of credit

Activity 2.7 Different types of credit for different purposes (Level 2)

Credit card A credit card is a plastic card that you use to buy things on credit or to get cash advances.

If you buy something, you have to pay interest on the loan after a certain period.

A cash advance is cash withdrawn from a credit card account. It’s really a loan from your credit card company. A transaction fee is usually charged for this, as well as interest which is from the date the cash is withdrawn and at a higher rate.

This is an unsecured loan.

Store card A store card is a form of credit card offered by large stores for you to buy things from their store (and sometimes from some other stores too). Store cards are used like regular credit cards but usually charge much higher interest rates.

This is an unsecured loan.

Personal loan A personal loan is a one-off loan for personal use such as to buy a car or take a holiday. The contract says what the interest rate is and the period of the loan (usually 2 to 7 years). You pay the same amount each month so that, by the end of the loan period, the total amount has been paid back (including interest).

A personal loan can be secured or unsecured.

Secured loan A loan for which an asset of yours has been used as security. An ‘asset’ is something you already own – such as your car or your home. The credit provider may sell the secured asset to get its money back if you can’t repay the loan.

Unsecured loan A loan for which no asset has been used as security. An ‘asset’ is something you already own – such as your car or your home. The interest rate is usually higher than for a secured loan as there is a higher risk to the credit provider of not getting their money back.

29www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt activity worksheets

C: Credit contracts

Activity 2.8 Red-flagging cost items in a credit card offer (Level 2)

30www.teaching.moneysmart.gov.au

TOPIC 2: Credit and debt activity worksheets

C: Credit contracts

Activity 2.10 Understanding a contract (Level 3)This is a sentence taken from a real credit card contract.

“Annual Fee waived in the first year and in each subsequent year if you have spent at least $1,000 (purchases and cash advances only) on your credit card account in the previous year.”

31www.teaching.moneysmart.gov.au